Narrative Data Room: What It Is, When It Works, and When It Backfires (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Narrative Data Room: What It Is, When It Works, and When It Backfires

Last updated: July 2026

Quick answer: A narrative data room is a data room organized around the investor's decision journey — the questions a reader must answer to reach conviction, in the order they'll ask them — instead of folder taxonomy. The term is new (a beta-stage vendor, Pageform, built its positioning on it); the practice is older and investor-endorsed. It works when your reader is underwriting your ceiling (equity fundraising) and backfires when they're underwriting your floor (M&A confirmatory diligence, venture debt). The durable architecture is the Two-Layer Room: guided narrative on top, complete neutrally indexed binder underneath, every claim linking down to its evidence.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers, most of them founders and deal teams. One thing running a data room company teaches you — because page-level analytics shows it over and over — is that the room founders think they built and the room investors actually read are two different rooms. Founders design a filing cabinet; investors go looking for an argument. "Narrative data room" is the newest label for closing that gap, and since the term is starting to circulate on founder Twitter and in vendor marketing, it's worth a precise treatment: what it actually means, what the evidence-and-investor consensus supports, where it genuinely helps, and the two situations where it will actively hurt you.

One scope note before we start. This post is about the architecture layer — how a room is organized and read. For what goes into a fundraising room, use the startup data room checklist and data room for investors; for the underlying folder taxonomy, the data room folder structure guide; for the stage-specific bar at Series A, the Series A data room guide. This post is the layer that sits on top of all of that.

What is a narrative data room?

A narrative data room is a data room whose structure follows the reader's decision process instead of a document taxonomy. The top level isn't "01 Corporate, 02 Financials, 03 Legal." It's a sequence: start here → the claim → is it working → does the model hold → why now → who's building it → the full binder. Each section opens with a short written claim and contains the small set of documents that prove it. The room becomes a guided argument with evidence attached, rather than a warehouse with a map. Founders and vendors also call it a "storytelling data room," a "guided data room," or simply "a data room that tells a story" — same idea, same architecture.

The term itself is young. Its most visible champion is Pageform, a currently-in-beta product that positions itself as a "narrative-driven virtual data room for deal teams" — turning fundraising materials into what it calls a guided narrative rather than file storage. Whatever you make of the product category, the positioning names something real that founders have been hearing from investors for years, usually as the vaguer instruction "your data room should tell a story."

The practice is older than the label. Morgan Cheatham — then a vice president at Bessemer Venture Partners, now a partner and head of healthcare and life sciences at Breyer Capital — wrote the canonical investor-side version in his 2022 essay The Anatomy of the Data Room: the best data rooms "make it easy for an investor to write an investment recommendation," and it helps to make your data room "mirror the investment recommendation" itself — while letting "the data tell the story, not the other way around." That last clause is the honest version of the whole concept, and we'll come back to it, because it's also the line between a narrative room and a spin room.

Two disambiguations, because the phrase collides with unrelated jargon. A narrative data room is not a data clean room (privacy-safe data-matching infrastructure from adtech — the company Narrative.io operates in that world, which makes search results for this term genuinely confusing). And it's not data storytelling, the BI discipline of turning dashboards into presentations. A narrative data room is a deal artifact: the same diligence documents you'd share anyway, architected around how a stranger reaches conviction.

How is a narrative data room different from a traditional data room?

The difference is the organizing principle: a traditional room is optimized for verification, a narrative room for comprehension. Both are designs; a folder tree that mirrors a legal checklist is not "no structure," it's structure for a professional reader who arrives with their own list of questions. The narrative room is structure for a reader who arrives with only one question: should I spend more time on this?

| Dimension | Traditional data room | Narrative data room |

|---|---|---|

| Organizing principle | Document taxonomy (corporate, financial, legal, HR) | Reader's decision journey (claim → evidence → conviction) |

| Top-level unit | Folder / category | Question / claim, with proof attached |

| Index looks like | A legal checklist | An investment memo outline |

| First thing read | Whatever sorts first alphabetically | A start-here memo you wrote deliberately |

| Optimized for | Completeness and verification | Time-to-conviction and comprehension |

| Native failure mode | The buried lede — best evidence unread in folder 02 | Perceived spin — story without click-through evidence |

| Best for | Floor readers: counsel, lenders, confirmatory diligence | Ceiling readers: equity investors building conviction |

Notice what the table implies: neither structure is "correct." They serve different readers, and the mistake founders make is picking one when the honest answer — covered below — is layering both.

Why does reading order matter? You're not in the room when it's read

A data room is a pitch that happens in your absence — I think of it as the Unattended Pitch. You present the deck; nobody presents the room. It gets opened at 10pm by an associate assigned to draft the memo, or by a partner your champion forwarded it to, or by someone who was never in any meeting with you. Whatever order they read in is the pitch they receive. In a live meeting you'd never open with your certificate of incorporation — but that is exactly what an alphabetized folder tree does.

Attention makes this worse. DocSend's pitch-deck research has consistently found investors spending only a few minutes on a deck — its original 2015 study measured 3 minutes 44 seconds, and more recent analyses put the figure under three minutes. There is no equivalent published benchmark for time spent in data rooms (be suspicious of anyone who quotes one), but the asymmetry is the point: if a 15-slide deck gets minutes, a 300-file room without a designed path is a bet that a distracted stranger will assemble your argument correctly from folder names. Some will. The ones who don't won't tell you — the room just goes quiet.

The deeper mechanism is what happens after the read. In most firms, your believer has to re-sell you internally: a memo, a partner meeting, a vote. Susan Su, a partner at Toba Capital, frames the well-built room exactly this way — as serving an investor "your complete in-depth narrative on a silver platter, giving them the materials to craft their memo." Cheatham's "mirror the investment recommendation" is the same advice from inside the partnership. The narrative layer isn't decoration; it's you drafting your champion's internal pitch for them, with citations.

One honest observation from our side of the table: when founders compare the reading order they intended against the actual per-page paths in page-level analytics, the two rarely match — readers skip the market section, go straight from the memo to the model, stall on a cohort table. Your intended order is a hypothesis. Treat it like one.

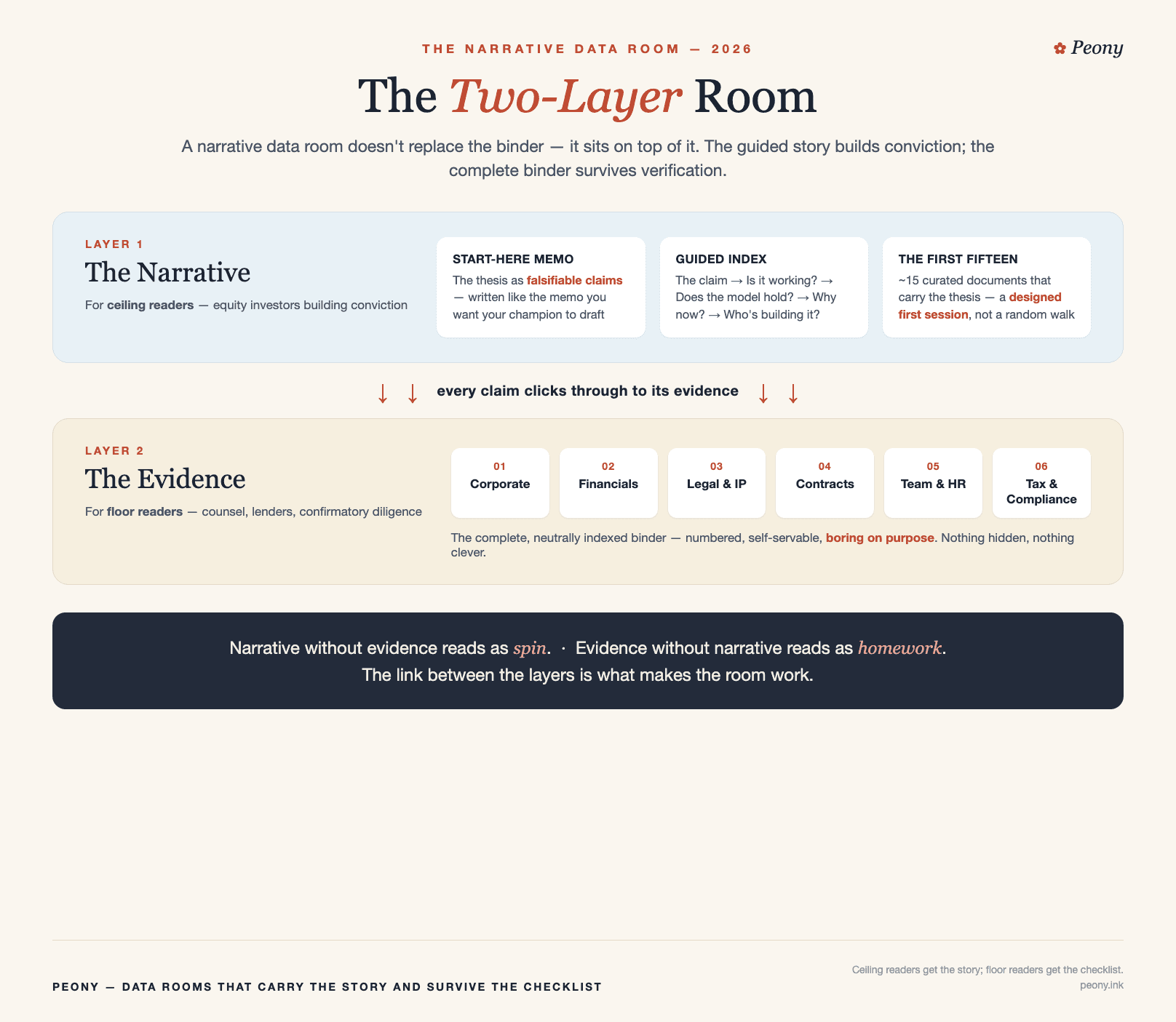

The Two-Layer Room: narrative on top, evidence underneath

The Two-Layer Room is a data room built as two stacked layers — a curated narrative on top, a complete and neutrally indexed binder underneath, with every claim in the top layer clicking through to its proof below. It dissolves the apparent curated-versus-complete dilemma, which is false: you build both, as layers.

Layer 1 — the narrative layer. Three artifacts. First, a start-here memo: one to two pages, written as the investment memo you want your champion to produce — the thesis as three to five falsifiable claims ("NRR is 118% and improving," "we're default-alive on the current plan," "the wedge expands into X"), each claim linking to the documents that prove it. Second, a guided index: five or six sections named as the reader's questions, in the order a skeptical-but-interested reader would ask them, each with a one-paragraph summary and links downward. Third, what I call the First Fifteen: the curated set of roughly fifteen documents that carry the core thesis — the designed first session. (Institutional-fundraising guidance has converged on the same shape; one April 2026 guide for sponsors raising institutional LP capital recommends opening with 15–25 carefully selected documents organized "around the questions an investor will ask, in the sequence they will ask them," rather than releasing hundreds of files on day one.)

Layer 2 — the evidence layer. The complete, neutrally indexed, numbered binder — everything the folder structure guide prescribes, deliberately boring. Corporate, financials, legal, IP, contracts, HR. Nothing hidden, nothing clever.

The rule that makes the architecture work: every claim in Layer 1 clicks through to primary documents in Layer 2. That single rule is the difference between narrative and spin. A narrative layer without click-through evidence is marketing that happens to live in a data room. An evidence layer without a narrative is homework you've assigned to someone deciding whether to fund you. The two failure modes are mirror images, and the link between layers eliminates both.

Why not go narrative-only, as the purest version of the concept tempts you to? Because your hardest readers won't accept it. Counsel and analysts re-sort every room into their own checklist anyway; if the neutral binder doesn't exist, they experience your room as an obstacle between them and the documents. And a room where the raw material can't be self-served reads as control — and control, to a professional skeptic, smells like concealment. The narrative layer is for building conviction; the binder is for the people whose job is to attack it. You need both to close.

What goes in a narrative data room — and in what order?

Sequence the top layer as the questions a skeptical reader asks, in order. For a SaaS Series A, the arc I'd build:

- Start here — the memo above, plus the deck and a 90-second reading guide ("if you only open five things, open these").

- The claim — what has to be true for this to be a fund-returner. One page, no adjectives that don't link to evidence.

- Is it working? — traction and revenue quality: cohort retention, NRR bridge, usage depth, logo concentration. This is where a ceiling reader decides to keep reading, so it comes before anything corporate.

- Does the model hold? — the financial model with explicit assumptions, runway and burn, unit economics, and the sensitivity cases. If your model is strong enough to carry weight, consider sharing it as a live model rather than a dead export so the assumptions are inspectable.

- Why now? — market and timing evidence: the two or three exhibits that make the window credible, not forty analyst PDFs.

- Who's building it? — team, org, key hires, and the cap table (clean, current, with option pool reality visible).

- The binder — Layer 2 in full, per the checklist.

Calibrate depth to stage. At seed, the whole room is often 10–20 documents and the start-here memo does most of the work. At Series A, the room gets graded — diligence formalizes, and every deck claim needs a document behind it (the Series A data room guide covers that bar in detail). By Series B, the evidence layer dominates on volume, but the narrative layer matters more, not less, because the reader is reconciling a bigger story against more data.

The 2026 context sharpens all of this. Per Carta's State of Private Markets: 2025 in Review, 2025 produced the fewest new priced rounds in six years (4,859) even as valuations hit records — the median Series A closed at a $78.7M post-money in Q4 2025, up 37% year over year, and median seed reached $24M. Fewer, bigger, more concentrated checks means each one carries more diligence weight, not less. The room is doing more of the deciding than it did in 2021's spray-and-pray market — which is exactly why its architecture has become worth designing.

Do investors actually care whether your data room tells a story?

They care about what the structure produces, not the philosophy — and it's worth being precise about what it does and doesn't produce, because this is where the concept's marketing outruns its mechanics.

What a narrative structure genuinely buys you: speed to conviction (the thesis is stated, not excavated); fewer redundant Q&A cycles (the answer to "what's your logo churn?" is already sequenced next to the claim it tests); a half-drafted internal memo for your champion; and a legible signal of operator clarity — a founder who knows exactly what has to be true and where the proof lives. In a market where partners see hundreds of rooms, legibility is a real edge.

What it cannot buy you: credibility. Reordering documents does not improve the documents. If retention is weak, a narrative room surfaces that faster — which, honestly, is still in your interest: a fast honest no beats dying in week six of diligence. And the failure mode cuts sharper in reverse: polish wrapped around thin evidence produces doubt, and doubt is the actual deal-killer. A June 2025 fractional-CFO essay on HackerNoon put the principle well: when a data room is sloppy — numbers that don't reconcile, claims that don't trace — it's not the diligence that kills the deal, it's the doubt. An over-produced narrative with an under-produced binder generates exactly the same doubt from the opposite direction.

There's also a stage transition worth respecting: seed rounds are bought substantially on story; by Series A, every claim in the deck is expected to have a document behind it. The narrative room concept works because it respects that transition — it's a story built out of documents, not a story instead of them. Cheatham's clause is the test: let the data tell the story, not the other way around. If you find yourself writing narrative the documents don't support, you've left "narrative data room" and entered fiction.

Verdict, as directly as I can put it: no investor cares that your room is "narrative." Every investor rewards a room that answers their next question before they ask it. Narrative structure is simply the most reliable way to build that room — as long as the evidence layer underneath is complete.

When does a narrative data room backfire? The Ceiling/Floor Test

A narrative data room backfires when your reader is underwriting your floor rather than your ceiling — M&A confirmatory diligence, venture debt, late-stage verification. So before restructuring anything, run one test: is your reader underwriting your ceiling, or your floor?

Ceiling readers are deciding how big this could get. Equity VCs building conviction pre-term-sheet are the canonical case. Their job is to construct the upside argument, and a narrative room does that construction with them. This is where everything above applies.

Floor readers are deciding what happens if it goes wrong — and their process is adversarial by design. Three big cases:

- M&A confirmatory diligence. The buyer's counsel, accountants, and diligence teams arrive with a request list and read against it: unsigned contracts, IP chain-of-title gaps, revenue that doesn't reconcile, change-of-control clauses. A room organized as a persuasion journey is friction at best; at worst it reads as steering, and steering invites deeper digging. In a sale process the narrative has its own dedicated artifacts — the CIM and the management presentation. Put the story there (the CIM guide covers building it thesis-first), and make the room itself reconciliation-grade: indexed to the diligence request list, with every number in the CIM traceable to a source document. The sell-side diligence prep guide walks that 90-day sequence.

- Venture debt and any credit process. Lenders underwrite repayment — the floor, definitionally. They want runway, burn trajectory, revenue durability, existing liens, covenants. Handing a lender a growth-narrative room is the classic mismatch: the thing they're underwriting isn't in it. The venture debt data room guide is the full treatment of that inversion.

- Late-process verification generally — R&W insurers, debt refinancing, serious legal review. Same logic: the reader's checklist beats your arc. Serve the checklist.

The test resolves the "does this work for M&A?" question cleanly: sell-side, narrative belongs in the CIM, proof belongs in the room. The furthest a narrative layer should go for floor readers is a short process and reading guide — orientation, not persuasion. Floor readers don't want to be told a story; they want to confirm the story they were already told, fast.

Staging is not storytelling

Staging is access control; storytelling is comprehension design — different tools. The confusion between them produces most of the "narrative rooms are spin" criticism, so let's kill it explicitly. Staging — teaser-level material pre-NDA, the full room post-NDA, the most sensitive files (customer names, employee comp, source-code escrow) held for confirmatory diligence — is access control, driven by sensitivity and process stage. Narrative is comprehension design within whatever a reader is allowed to see.

Founders get in trouble when they use the second word to do the first job: burying the churn cohort three layers deep and calling it "sequencing." That's concealment with extra steps. Diligence will find it — that's what diligence is — and a discovered burial costs more credibility than the weakness it was hiding, because now the reader wonders what else is staged that way. The clean rule: stage by sensitivity, narrate within each stage, and never let the narrative layer be the reason something is hard to find. If a number is bad, the narrative layer is exactly where you address it head-on, with the mitigation argument attached. Controlling when a reader sees something is legitimate deal hygiene; engineering whether they notice it is not — and the two look identical in a folder tree, which is why your narrative layer must always sit on a complete binder.

How do you build one — in Google Drive, Notion, or a data room platform?

You can build roughly seventy percent of a narrative data room with tools you already have, and at seed that's often the right call.

The DIY version (Drive or Notion). Number the top-level folders in thesis order so the sort order is the reading order: 00 Start Here, 01 The Claim, 02 Traction & Retention, 03 Model & Runway, 04 Market & Timing, 05 Team & Cap Table, 06 Binder. Write the start-here memo as a doc at the top with links to every claimed exhibit. Add a three-line README to each section stating the claim it proves. In Notion, one page becomes the guided index with the binder nested beneath. Total cost: a focused weekend on top of a room you already have — and because nothing moves, nothing breaks mid-raise.

What the DIY version can't do — and when that starts to matter: there's no feedback loop (you can't see who opened what, in what order, or where they stalled — so your narrative stays an untested hypothesis); permissions are coarse (link-level, not per-file per-viewer, so you either overshare or fragment the raise across multiple links); links rot when files move; and there's no watermarking or audit trail when the material gets sensitive. These gaps typically start to bite somewhere around a competitive Series A — more readers, more sensitive exhibits, more need to know which investor went quiet after opening the model.

The platform version. On Peony, the two-layer build maps directly: bulk-upload the binder and AI auto-indexing structures Layer 2 in minutes; the start-here memo can be a live page at the front of the room — including an interactive artifact or live dashboard rather than a static PDF, if your model or metrics deserve a front door that readers can actually drive; page-level analytics (included on every plan, Free upward) closes the loop between intended and actual reading order; and granular per-file permissions plus dynamic watermarks on the Data Room plan ($52/admin/month; Business is $30/admin/month) handle staging without breaking the narrative layer. The feedback loop is the part I'd argue hardest for, whatever tool you use: a narrative room is a hypothesis about how strangers read, and mid-raise you get to test it weekly and reorder accordingly.

Which tools support a narrative data room in 2026?

Four kinds of tools cover the range in 2026 — Pageform (narrative-native, in beta), Peony (the two-layer approach on data room infrastructure), DocSend (deck-first sharing), and classic process VDRs like iDeals and Datasite (binder-first, for floor readers) — and the right one depends on who's reading. The honest segmentation:

- Pageform — the narrative-native bet: an AI-assisted product built specifically around turning materials into a guided deal experience, and the vendor that has done the most to name this category. It's currently in beta with little public operating history, which is the honest trade-off — the purest version of the thesis, on the youngest infrastructure. If you evaluate it, apply this post's test: make sure the guided layer sits on a complete, self-servable binder.

- Peony — the two-layer approach on data room infrastructure: complete permissioned binder underneath, narrative front door on top (live pages and interactive artifacts included), page-level analytics on every plan to test the reading order, from free ($0) up through Data Room at $52/admin/month. Built for the raise-through-diligence lifecycle, which is exactly where the two layers earn their keep. We're the vendor here — weigh accordingly, and check the claims yourself on the free plan.

- DocSend — deck-first sharing with strong per-page analytics and lightweight "spaces." A reasonable narrative front door early in a raise; teams tend to outgrow it as diligence deepens and the binder, permissions, and Q&A load grow.

- Classic process VDRs (iDeals, Datasite and peers) — binder-first infrastructure built for banker-run M&A and floor readers: request-list indexing, granular audit, Q&A workflow at scale. When your reader is confirmatory-diligence counsel, this shape of room — not a narrative one — is the right tool, at a very different price point.

The bottom line

- A narrative data room organizes the room around the reader's decision journey instead of folder taxonomy. New term; old, investor-endorsed practice.

- The room is an Unattended Pitch — reading order is the pitch, and your champion re-sells you with whatever the room hands them. Design the order; then verify it against actual reading behavior, because intended and actual rarely match.

- Build the Two-Layer Room: start-here memo, guided index, and a First Fifteen on top; the complete boring binder underneath; every claim clicking through to evidence. Narrative without evidence is spin; evidence without narrative is homework.

- Run the Ceiling/Floor Test before restructuring anything: narrative for ceiling readers (equity), checklist for floor readers (M&A confirmatory, venture debt). Sell-side, the story goes in the CIM; the room stays reconciliation-grade.

- Staging is not storytelling. Stage by sensitivity, narrate for comprehension, and never let the narrative be the reason something is hard to find.

The instruction "your data room should tell a story" is good advice with a dangerous compression. Uncompressed: state your thesis as falsifiable claims, sequence the evidence in the order a skeptic would test them, and keep the full record one click below. That's a room that raises faster — not because it performs a story, but because it makes the true story easy to verify.

If you want to build the two-layer version, start free on Peony: AI auto-indexing for the binder, a live front door for the memo, and page-level analytics to find out how investors actually read you.

You might also like

Jun 29, 2026

How to Share an Interactive Financial Model With an Investor (Securely)

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

Series A Data Room: The Step-Change Round Where Your Room Gets Graded (2026)