Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling

Last updated: June 2026

Quick answer: A venture debt data room is the lender-facing room a venture-backed company builds to raise debt — and it's a fundamentally different room from your equity raise, because the lender is asking a different question. An equity investor underwrites your ceiling (how big could this get?). A venture lender underwrites your floor (can you service and repay this loan, and what's the backstop if you can't?). That inverts what the room leads with: runway, burn, the durability of your recurring revenue, your covenants, and — above all — the strength and recency of your last equity round, which is the lender's real repayment thesis. This guide covers what lenders diligence, what goes in the room, how the deal is structured (rate, warrants, covenants), the traps, and the post-SVB 2026 landscape. Run it on a flat-rate platform like Peony ($30/admin/month Business, $52/admin/month Data Room).

I'm Sean Yu, co-founder of Peony, a data room company serving 6,800+ customers — many of them venture-backed founders, and a growing number raising venture debt to extend runway between equity rounds. The mistake I see most often is treating the venture debt raise like an equity raise with a different counterparty: founders point the lender at the same growth-story data room they built for VCs, and then wonder why diligence drags and the question list never ends. It drags because the lender is underwriting something that isn't in that room. An equity investor is buying your upside; a lender is protecting against your downside. Build the room for the question actually being asked.

This is the lender-facing playbook: why the burden of proof inverts, what a venture lender diligences that an equity investor weights differently, what goes in the room, how the deal is structured (and the warrant and covenant terms founders underestimate), and how the post-SVB market actually looks in 2026. It sits next to — not on top of — the equity-raise guides like data room for investors and the Series A data room; venture debt is what often comes alongside or after those rounds. And if you built your equity room as a narrative data room — a guided, thesis-first structure — note that lenders are the canonical floor readers: this room serves the checklist, not the story.

One note on the numbers: loan sizes, rates, warrant coverage, and covenants here are market conventions, negotiated deal by deal, not regulated figures. I cite them as "commonly" and "typically," and I've flagged the one piece of terminology — warrant coverage — that trips up the most founders. Always run the actual terms past your own counsel.

What is a venture debt data room — and why is it built for a lender, not an investor?

A venture debt data room is the secure, permissioned room a venture-backed company uses to raise venture debt — a term loan, usually from a specialty lender or bank, typically taken alongside or after an equity round to extend runway, almost always with warrants attached. The room exists to let a lender underwrite the loan, which is a different job from letting an investor underwrite the equity.

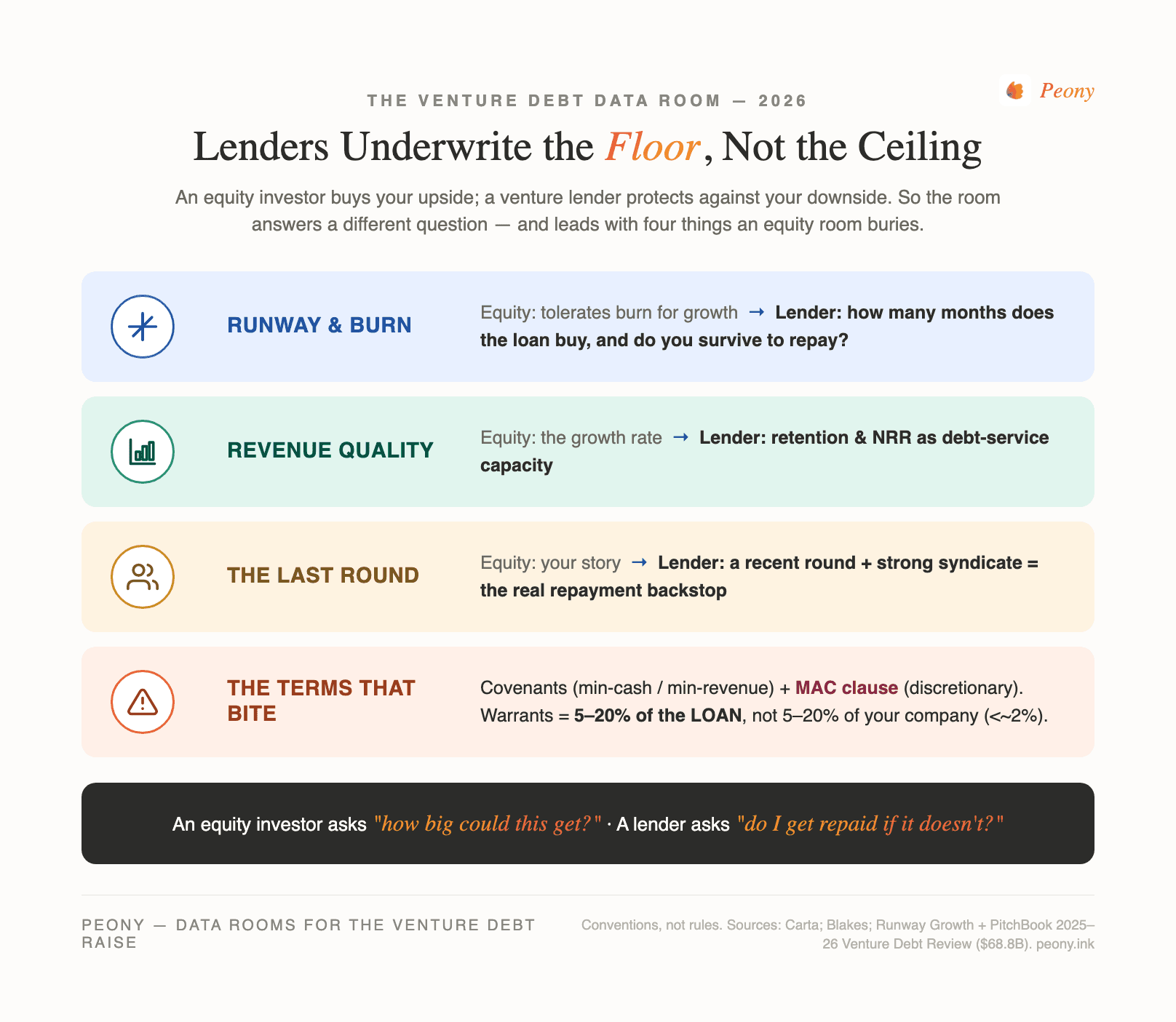

Here's the distinction that defines everything else. When you raise equity, the investor is buying a slice of your upside; their downside is capped at the check, and their return depends on you getting big. When you raise debt, the lender's upside is capped at interest plus a small warrant — they don't get rich if you 10x — so their entire focus is the downside: will they be repaid in full, on schedule, and what protects them if the company stumbles? An equity investor accepts that some bets go to zero. A lender, per the consensus across lenders and advisers, expects to be repaid in full. That single asymmetry reshapes the room.

So a venture debt room is built around debt-service capacity and downside protection, not growth narrative. It leads with the financial model and an explicit runway (how long does the company live, and how much longer does the loan buy?), the burn rate and its trajectory, the quality and retention of recurring revenue (what debt service is sized against), and the existing-lien and last-round picture that frames repayment. The growth story still matters — but as evidence the company will reach its next round, not as the headline. If your venture debt room reads like a pitch deck, it's answering the wrong question.

Why do lenders underwrite the floor while equity investors underwrite the ceiling?

Because their payoffs are shaped completely differently, and the data room should match the payoff. An equity investor's return is unbounded on the upside and zero on the downside, so they rationally underwrite the ceiling — they're hunting for the outcome where you become enormous, and they'll tolerate heavy burn and risk to find it. A venture lender's return is a fixed stream of interest plus a modest warrant, capped no matter how big you get, while their downside is losing principal — so they rationally underwrite the floor: the realistic worst case, and whether they still get paid in it.

This is the non-commodity point most "data room" advice misses for venture debt. The same fact lands in opposite directions depending on which side of the capital stack reads it. A 200%-growth-but-burning-$1M-a-month profile is thrilling to an equity investor and worrying to a lender, who sees a company that needs to raise again soon or run out of cash before the loan is repaid. A modest, capital-efficient, high-retention SaaS business is merely "fine" to a growth investor but attractive to a lender, because it can service debt. When you understand which question is being asked, you stop pitching the ceiling to someone who's underwriting the floor.

Practically, underwriting the floor means the lender weights runway, burn, recurring-revenue durability, and — critically — the assumption that you'll raise another equity round before the debt matures. As Carta puts it, the most recent institutional round is treated as the primary repayment source. So the room's job is to make the floor look solid: enough runway, durable revenue, a credible path, and strong backers who will fund the next round. Sell the floor, and the ceiling takes care of itself.

What does a venture lender diligence that an equity investor weights differently?

A venture lender runs a hybrid of credit and equity analysis, but everything bends toward repayment. The items they weight far more heavily than an equity investor:

- Runway and cash position. The first question is survival: how many months of cash do you have, and how many more does the loan add? Equity investors care about runway too, but for a lender it's the core of the repayment math.

- Burn rate and trajectory. Not just how much you burn, but whether it's trending toward control. High burn that an investor reads as aggression, a lender reads as risk.

- Recurring-revenue quality and retention. ARR/MRR is what debt service is sized against, so cohort retention, net revenue retention, and churn are read as repayment capacity, not just growth signals.

- Gross-margin durability and unit economics. Can the revenue actually fund operations and service the debt as it scales?

- The investor syndicate — strength, reputation, recency. Lenders lean hard on strong institutional backers. Per the law firm Blakes, they evaluate "the historical performance and reputation of the venture capital firm involved." A reputable, deep syndicate that has shown it will support the company is, to a lender, a repayment backstop.

- Existing debt and liens. A prior lender's UCC-1 filing affects the new lender's security position, so the existing-lien schedule matters in a way it never does to an equity investor.

The throughline: an equity investor asks "what could this become?"; a lender asks "what happens if it doesn't — and will the people who already funded you fund you again?" The room has to answer the second question with evidence, not optimism.

What goes in a venture debt data room?

Build it around repayment capacity. The contents overlap a standard startup room, but the emphasis — runway, burn, retention, and liens — is lender-specific.

| Section | Documents | Why the lender wants it |

|---|---|---|

| Financials & runway | Monthly statements + KPIs (24–36 months); financial model with explicit runway and base/downside sensitivities | The core repayment analysis — survival and debt-service capacity |

| Revenue quality | Cohort & retention analysis, NRR/churn, revenue waterfall (billings → GAAP), AR/AP aging, gross/contribution-margin build | ARR/MRR is what debt service is sized against; quality > raw growth |

| The last round | Most recent equity round docs, cap table, board approvals | The primary repayment thesis — recency + syndicate strength |

| Debt & liens | Existing debt, leases, current lien/UCC schedule, any inter-creditor items | The lender's security position relative to prior creditors |

| Corporate & legal | Charter/bylaws, key customer & vendor contracts, IP/filing summaries, insurance, KYC | Standard credit and security diligence |

The two things that distinguish this from an equity room: the runway-to-next-round math (made explicit, with sensitivities), and the existing-lien/UCC picture (which an equity investor barely glances at but a lender underwrites carefully). For the underlying file inventory, build on the startup data room checklist and layer the debt-service and lien sections on top. On Peony, AI auto-indexing will classify a bulk upload into this structure, and granular per-file permissions on the Data Room plan ($52/admin/month) keep the sensitive financials and contracts controlled while you share the runway model with the credit team.

How is a venture debt deal structured — rate, term, warrants, and the fees founders miss?

The headline rate is the part founders focus on and the smallest part of the real cost. Here's the structure, all as market conventions, not fixed rules:

| Term | Common convention (2026) | Watch for |

|---|---|---|

| Loan size | ~20–50% of your last equity round | Higher end needs strong revenue + syndicate |

| Interest rate | Floating — WSJ Prime + a spread (lighter covenants → higher rate) | It's floating, not fixed; model rate moves |

| Term | ~3–5 years | — |

| Interest-only period | ~12–18 months, then P&I amortization | The IO window is much of the runway value |

| End-of-term / final-payment fee | A % of the loan, due at maturity | Often forgotten in the cost math |

| Warrant coverage | ~5–20% of the loan amount | NOT the lender's ownership % (commonly under ~2%) |

The warrant line is where the terminology bites, so be precise: "warrant coverage" is a percentage of the loan amount the lender can use to buy shares — not a percentage of your company. "10% warrant coverage on a $5M loan" means $500K of warrants; the lender's resulting ownership stake is commonly under about 2%. Founders who hear "10–20% coverage" and picture handing over 10–20% of the company are conflating two different numbers — don't.

The real move is to model the all-in cost — interest over the life of the loan, the end-of-term fee, any prepayment penalty, and the warrant dilution — against the dilution you'd take from raising the equivalent in equity. Venture debt usually wins that comparison for a healthy company, but only if you price the whole package, not the rate on the cover.

What covenants will a venture lender ask for — and which ones can bite?

Venture debt generally carries limited financial covenants relative to traditional corporate lending — you typically won't see leverage or EBITDA-coverage tests, because the borrower is often pre-profit. What you'll commonly see is a minimum-liquidity (minimum-cash) covenant and/or a minimum-revenue or revenue-growth covenant, sized to the lender's comfort. Two provisions deserve real attention:

- The acceleration trigger. Tripping a minimum-cash or minimum-revenue covenant can give the lender the right to accelerate — demand repayment — at exactly the moment you can least afford it. The defense is negotiated up front: cure rights and grace periods that give you room to fix a stumble before it becomes a default. Get these into the term sheet; don't discover their absence mid-crisis.

- The MAC clause. The material adverse change clause is the subtle one. Per Blakes, default can be triggered by a "material adverse change to the business or investor support," and the lender has meaningful discretion in deciding whether a breach has occurred. A MAC tied to "investor support" means the lender can act if your backers visibly cool on you — which is precisely when you're most exposed. You can't always negotiate the MAC away, but you can tighten its language, and you can manage it by keeping the lender confident through the room.

That's the quiet role of the data room after the deal closes: ongoing visibility — clean financials, a credible runway, evidence of continued investor support — is what keeps a lender from ever reaching for the acceleration or MAC levers. Have counsel scrutinize every covenant and the MAC definition before you sign; this is the part of the term sheet that determines what happens on a bad day.

Why is your last equity round your real repayment story?

Strip away the collateral language and a venture lender's repayment thesis is simple: strong investors will fund this company again before the debt comes due. The lender takes a blanket lien on IP, receivables, and cash, but everyone involved knows those wouldn't recover much in a fire sale — the genuine backstop is your equity syndicate's willingness and ability to write the next check. That's why your most recent round is the center of gravity in the room.

It does three jobs simultaneously. It sizes the loan (commonly 20–50% of the round). It dates your credibility — lenders generally want to see institutional equity raised within roughly the last 12 months, which is why venture debt is cheapest and most available right after a round, not when you're scraping the bottom of the runway. And it signals your backing — a reputable, deep-pocketed syndicate that has demonstrably supported the company is, to a lender, worth more than a slightly better growth rate from an unknown one.

This also demystifies the MAC clause's focus on "investor support": if your backers cool, the lender's whole repayment thesis weakens, so the protective terms exist for exactly that scenario. The practical implication for the room is to make the repayment story impossible to miss — put the recent round, the cap table, the named institutional backers, the runway, and the durable revenue front and center. You're not selling growth to a lender; you're selling the credibility of your next round.

Is the venture debt market back after SVB — and how should that shape your raise?

It's back and larger, just reshaped. Silicon Valley Bank — long the dominant venture-debt provider — failed in March 2023; First Citizens took its US operations and HSBC took its UK arm, now HSBC Innovation Banking. The void didn't shrink the market; it pulled in specialty business-development companies (Hercules Capital, TriplePoint, Trinity Capital, Horizon, Runway Growth), private-credit funds, other banks, and fintech lenders. Per the Venture Debt Review published by Runway Growth Capital with PitchBook data, US venture debt deal value reached a record of roughly $68.8 billion in 2025, up from about $53.3 billion in 2024.

Three things that should shape how you raise in 2026:

- Shop the structure. There are more lender types than pre-SVB — banks, BDCs, private credit, fintechs — and they price covenants, warrants, and rate differently. Get more than one term sheet.

- The bar for a clean room is higher. Lenders have grown selective (dollars have grown faster than deal counts), so a tight, repayment-focused data room is a real advantage, not a formality.

- Mind the concentration. A large share of recent venture-debt dollars has flowed to AI companies; if you're outside the hottest categories, a well-documented, capital-efficient profile matters more, because you won't get carried by category heat.

The market is open. The founders getting good terms are the ones whose room makes the floor look solid.

The bottom line: sell the floor, not the ceiling

Venture debt is the one raise where your instinct to pitch the upside works against you. The lender isn't buying how big you could get — they're underwriting whether they get repaid if you don't, and leaning on your investors to fund the next round before the loan matures. So the room that wins good terms is the one built around the floor: an explicit runway, controlled burn, durable recurring revenue, a clean lien picture, and a recent, credible equity round with backers who clearly stand behind you.

Build it that way and two things happen. The diligence moves faster, because the lender's questions are already answered. And the relationship stays healthy after close, because the same visibility that earns the loan keeps the lender confident enough never to reach for the acceleration or MAC clauses. With 6,800+ customers behind this, the pattern is consistent — the companies that raise venture debt smoothly aren't the ones with the best growth story, they're the ones whose room makes repayment look obvious. Peony is free to start, and the lender-facing workflow above runs on the Business and Data Room plans.

Related resources

- Data Room for Investors — the equity-side room; venture debt usually comes alongside or after an equity round.

- Series A Data Room: The Step-Change Round — the equity raise whose strength becomes your venture-debt repayment story.

- Startup Data Room Checklist — the underlying document inventory this lender-facing room builds on.

- Startup Fundraising Rounds Guide (Seed to Series C) — where debt fits next to the equity rounds.

- Startup Fundraising Strategy — sequencing debt and equity to minimize dilution.

- Dynamic Watermarks — controlling the financials and contracts you share with a credit team.

You might also like

Jul 7, 2026

Narrative Data Room: What It Is, When It Works, and When It Backfires (2026)

Jun 25, 2026

Series A Data Room: The Step-Change Round Where Your Room Gets Graded (2026)

May 27, 2026

10 Fundraising Data Room Mistakes Sophisticated Bidders See in 2026