SPV Data Room: The Syndicate Lead's Playbook for Co-Investment Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

SPV Data Room: The Syndicate Lead's Playbook for Co-Investment Deals

Last updated: June 2026

Quick answer: An SPV data room is the controlled room a syndicate lead uses to share a single-deal co-investment opportunity with prospective backers — and the reason it's a harder problem than a normal diligence room is what I call the pre-commit window. In an SPV raise you share the most sensitive data (a startup's financials, cap table, and terms) with the least-committed, loosest-known audience (dozens of prospective backers who have signed nothing), on the tightest clock (fill the allocation before the round closes) — and the secrets aren't even yours, they're the founder's. So the room's real job is attribution and control: per-recipient links, dynamic watermarks, instant revoke, and a record of who saw what, before anyone has committed. If you raise on AngelList, Sydecar, or Carta, use their bundled room for the close; a dedicated room like Peony ($30/admin/month Business, $52/admin/month Data Room) earns its place in the pre-commit deal-marketing window and when you raise off-platform.

I'm Sean Yu, co-founder of Peony, a data room company serving 6,800+ customers across M&A, fundraising, and private securities offerings. A meaningful slice of them are syndicate leads and emerging managers running single-deal SPVs — angels and operators who source a deal, get an allocation, and raise it from their network. The mistake I see most often is treating the SPV raise like a founder's fundraise: drop the deck and the company's numbers into a shared Drive folder, send the link to the whole list, and hope. That's a bad fit for the SPV case, because the thing you're sharing isn't yours, and the moment you share it is the leakiest moment in the whole deal.

This guide is the lead-side playbook: why a co-investment raise is structurally harder to share safely than a normal diligence room, what goes in the room stage by stage, the investor-count and Reg D rules that shape it, an honest read on whether you even need a separate room when the platforms bundle one, and how to set it up fast. It sits between two clusters — the founder-side data room for investors and the private placement data room hub — and owns the case neither covers: you, the lead, circulating someone else's company to your own backers.

A scope note before we start: this is the venture minority co-investment SPV — a passive stake alongside a lead investor. If you're an independent sponsor doing a deal-by-deal raise to buy and control an operating company, that's a different animal with its own controls; see the independent sponsor guide. And none of what follows is legal advice — the regulatory points are sourced to primary materials so you can take them to your own counsel.

What is an SPV data room — and why is a co-investment raise a harder sharing problem?

An SPV data room is the secure, permissioned room a syndicate lead uses to share a single-deal co-investment opportunity with prospective backers and to collect what's needed to close them into the vehicle. The "SPV" — special purpose vehicle — is a single-purpose LLC formed to make one investment in one company, so that the LLC, not each individual backer, shows up as a single line on the startup's cap table. The lead pools many small checks into that one entity and invests as a single party.

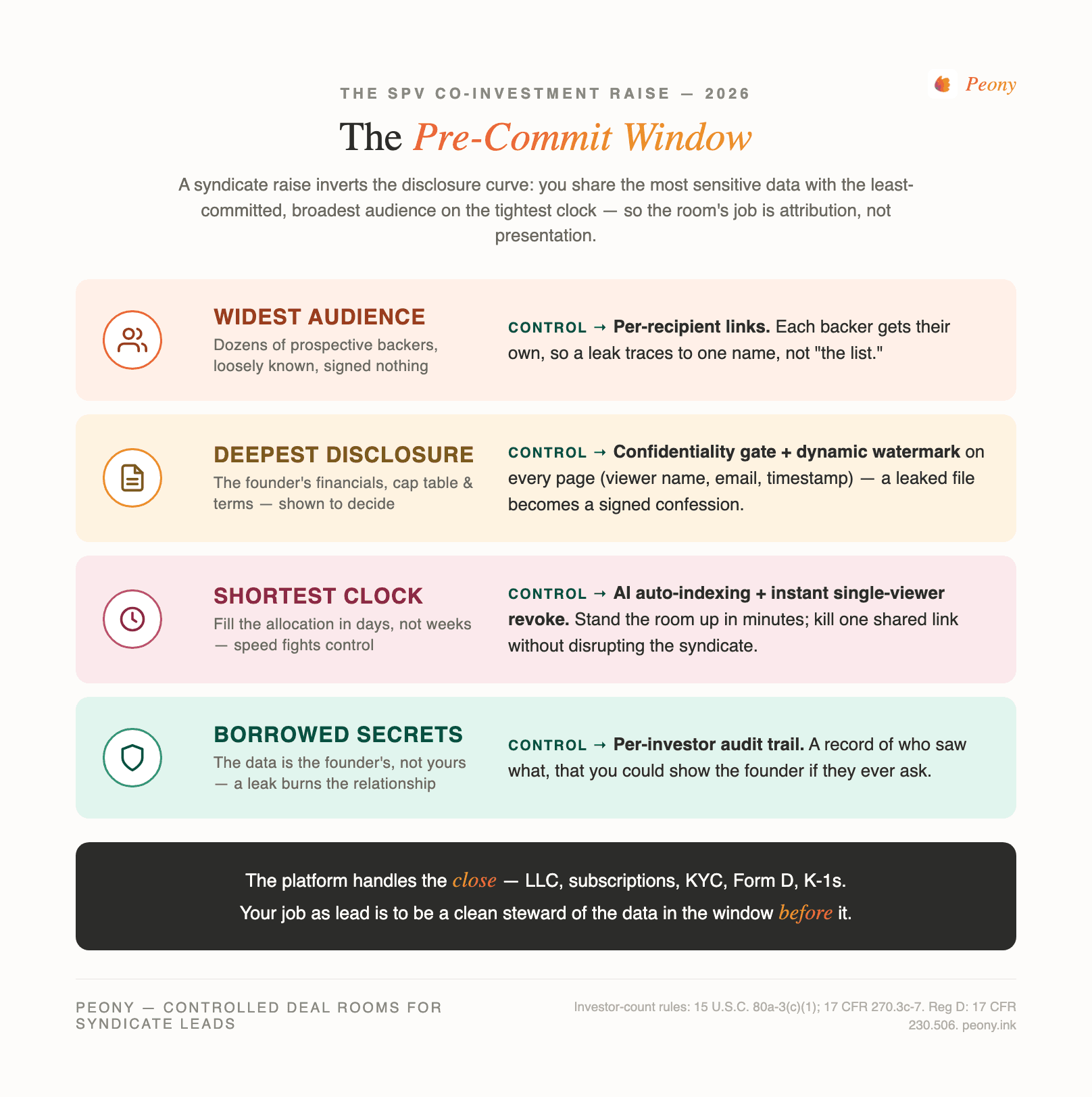

Here's why the sharing problem is harder than a founder's diligence room, and it's the non-commodity point most "best data room" lists miss. A normal diligence room has a rising commitment curve: a VC signs a term sheet, then you open the detailed financials; trust and disclosure climb together. An SPV raise inverts that curve. To get anyone to commit, you have to show the deal first — the thesis, the company's numbers, the terms — to a wide pool of people who have committed nothing and may never invest. The disclosure peaks exactly when the relationship is thinnest. That's the pre-commit window, and it's where SPV deals leak.

Three properties make it acute, and the rest of this guide is organized around managing them:

- The audience is broad and loosely known. A syndicate is a list, not a boardroom. You're sharing with dozens of backers, some of whom you've never met, some of whom are themselves investors who might pass the deal along.

- The clock is short. Allocations close. You often have days, not weeks, to fill the SPV, which pushes leads toward the fastest sharing method (forward the deck to everyone) rather than the safest.

- The secrets aren't yours. You're the steward of the founder's confidential data. Get it wrong and you don't just lose a deal — you lose the relationship with the company and your standing as someone founders trust with an allocation.

Why does the "pre-commit window" make a syndicate deal so easy to leak?

Because the path of least resistance and the path of least risk point in opposite directions, and the clock pushes you toward the wrong one. The fastest way to fill an allocation is to email the deck and memo to the whole list at once. That's also the most leak-prone thing you can do: one PDF, one identical copy in dozens of inboxes, zero attribution. If it shows up on a group chat or in a competitor's hands, you have no idea who forwarded it — and neither does the founder who trusted you with it.

The pre-commit window is leaky for a specific, structural reason: you are sharing before you have any leverage. Nobody has signed an NDA-backed subscription, nobody has wired, nobody has a contractual reason to keep your deal confidential yet. The only thing standing between "shared with my syndicate" and "shared with the world" is the design of how you shared it. A flat file blast has no design. A controlled room does.

The fix isn't to share less — you can't run a syndicate without showing the deal. The fix is to make every copy attributable and every grant revocable, so that the cost of forwarding shifts from "free and invisible" to "my name is on it and the lead can cut me off." We'll get concrete about those controls below, but the mental model is the point: in the pre-commit window, your security is whatever you built into the act of sharing, because you have no other leverage.

Whose secrets are you actually sharing when you run a syndicate?

The founder's — and internalizing that changes how you run the room. When a startup gives you an allocation, they're extending trust: they're letting you circulate their cap table, their metrics, and their round terms to your backers because they want the capital and the validation a good syndicate brings. They are not consenting to having those numbers land in twenty group chats. You are a custodian of someone else's confidential information, and the duty that comes with that is closer to a fiduciary posture than to "it's just a deck."

This is the reputational engine of the whole business. Deal-leaders get allocations because founders and lead VCs trust them to be discreet and professional. One sloppy leak — a financial model that surfaces on a forum, a cap table a competitor screenshots — and that trust is gone, along with your access to future deals. The downside of a leak isn't symmetric with the upside of closing one more backer five minutes faster.

So the practical posture is: share only what the founder has cleared you to share, gate the genuinely sensitive items behind a confidentiality click-through, attribute every view to a named person, and keep a record you could show the founder if they ever ask "who saw our numbers?" A room that can answer that question is doing the steward's job. A Drive folder with link-sharing on cannot.

What goes in an SPV data room, stage by stage?

Organize the room by phase, not by document type, because the SPV raise moves through three distinct moments with different audiences and different risk. Front-loading closing documents into the marketing phase is the most common setup mistake — it clutters the decision and exposes paperwork nobody needs yet.

| Phase | Audience | What's in the room | Sensitivity / control |

|---|---|---|---|

| 1. Pre-commit (deal marketing) | Prospective backers who've signed nothing | Your deal memo (thesis, round, terms, your allocation, carry); the founder-cleared deck and a financial summary; key metrics; round terms (priced/SAFE), lead investor if disclosable; SPV terms (min check, carry, fees, platform, timeline) | Highest exposure, lowest commitment. Per-recipient links, confidentiality gate on sensitive items, watermark every page, analytics on who read it |

| 2. Closing | Backers who've verbally committed | Subscription agreement, SPV operating agreement, investor questionnaire, wiring instructions; KYC/AML intake; 506(c) accreditation-verification evidence | Move committed backers onto your SPV platform (AngelList/Sydecar/Carta) for subs, KYC, and Form D. The room's job here is collecting and logging evidence per investor |

| 3. Post-close (reporting) | Backers who are now in the SPV | Closing confirmation, the executed docs, updated cap table line, then ongoing portfolio updates and K-1 / tax documents | Standing room. Per-investor access, durable audit trail |

The discipline that separates a clean raise from a messy one: in phase 1, the room holds only what a prospective backer needs to decide, and the most sensitive items (full cap table, detailed financials, customer contracts) sit behind a click-through confidentiality agreement so nothing real is visible until the viewer accepts terms. The subscription documents, KYC, and accreditation evidence belong in phase 2 — don't ask people to look at paperwork before they've decided to invest.

One more setup note specific to SPVs: keep the SPV's own documents (your memo, the operating agreement, the sub docs) separate from the company's documents (the founder's deck and numbers). They have different owners and different sensitivity, and conflating them is how a founder's confidential file ends up in a folder you've shared more widely than intended.

How many investors can a venture SPV legally hold?

For most single-deal venture SPVs, the binding ceiling is 100 beneficial owners — and it shapes how you run the raise, because you have to be able to count and document them precisely. An SPV is a pooled vehicle that would be an "investment company" but for an exclusion under the Investment Company Act. The common exclusion, Section 3(c)(1), excludes a vehicle "beneficially owned by not more than one hundred persons" that isn't making a public offering (15 U.S.C. 80a-3(c)(1)).

There's a higher tier. A "qualifying venture capital fund" can hold up to 250 beneficial owners. To qualify, the vehicle must have no more than a capped amount of aggregate capital contributions and uncalled committed capital. The statute set that cap at $10 million; the SEC's inflation-adjusted figure is $12 million as of its August 2024 rulemaking (17 CFR 270.3c-7; SEC press release 2024-102), with the next adjustment due around November 2029. So the rule of thumb: a small SPV (≤$12M) that meets the venture-fund definition can take up to 250 backers; a larger or non-qualifying one is held to 100.

Two practical consequences for the room. First, the count is a hard number you must be able to prove, not estimate — which is one more reason a per-investor record beats a shared folder. Second, the ceiling interacts with your minimum check: a $1M allocation split 100 ways is a $10K minimum, but the same allocation with a $25K minimum needs only 40 backers and stays comfortably under the cap. Structure the minimum so you fill the allocation without crowding the limit. Confirm your specific structure with fund counsel — these are the rules that frame the raise, not legal advice for your deal.

506(b) or 506(c): how does your solicitation path change the room?

It changes who you can talk to and what you must prove — and it's the single most important compliance decision in your raise. Both are safe harbors under Regulation D, but they draw the line at general solicitation: are you advertising the deal publicly, or only sharing it privately with people you already have a relationship with?

| Rule 506(b) | Rule 506(c) | |

|---|---|---|

| General solicitation | Not allowed — no public posts, no advertising the deal | Allowed — you can post the deal publicly |

| Who can invest | Accredited investors, plus up to 35 sophisticated non-accredited | Accredited investors only |

| Accreditation standard | "Reasonable belief" the investor is accredited | Must take "reasonable steps to verify" — self-certification is not enough |

| Room implication | Gate behind a pre-existing-relationship + NDA posture; lighter verification | Add a verification-evidence intake step before access; log it per investor |

Source: 17 CFR 230.506; SEC plain-language on 506(b) and 506(c).

The trap for syndicate leads is that a public deal post is general solicitation, full stop — which pushes you into 506(c) and its affirmative verification duty whether you meant to go there or not. If you tweet "raising an SPV for [hot startup], DM me," you are in 506(c) territory, and a checked "I'm accredited" box does not satisfy the "reasonable steps to verify" standard. The SEC's safe-harbor verification methods include reviewing IRS income forms (W-2, 1099, Schedule K-1, 1040) for the last two years, reviewing net-worth documentation dated within the prior three months plus a credit report, or — most common for syndicates — a written confirmation from a registered broker-dealer, SEC-registered investment adviser, licensed attorney, or CPA (17 CFR 230.506(c)(2)(ii)).

A recent wrinkle worth knowing: on March 12, 2025, the SEC issued a no-action letter to Latham & Watkins — the first interpreting 506(c) since the rule was adopted in 2013 — indicating that a high minimum investment combined with the investor's written representations can constitute reasonable steps in defined circumstances. It's useful, but it carries no legal force and your counsel decides if it fits. Either way, the data room's role is the same: the room does not verify accreditation for you. It gates the deal behind that step and gives you a dated, per-investor place to collect and log the evidence, so your file can show the gate cleared before access. For the full breakdown, see the 506(b) vs 506(c) data room guide.

Do you still need a data room if you raise on AngelList, Sydecar, or Carta?

Honest answer: often you don't — and I'd rather say that than sell you a room you don't need. The major SPV platforms bundle deal-sharing and a data room into the product, and they do the heavy mechanics Peony doesn't touch at all. It's worth being specific about who owns what:

- AngelList forms the LLC, handles subscriptions and KYC, files, and even launched a dedicated "Data Room" product for its fundraising flow. Published pricing: an $8,000 standard SPV setup ($5,000 follow-on), a $2,000 blue-sky pass-through, total fees capped at 10% of the raise.

- Sydecar runs deal-by-deal SPVs with bundled private data rooms, Form D and blue-sky filings, KYC/AML, and K-1s. Published pricing: a one-time 2% of capital ($2,500–$12,500) plus a $2,000 regulatory fee, no carry to Sydecar.

- Carta offers SPVs and fund administration (it acquired the SPV platform Vauban in June 2022); confirm current SPV pricing on Carta's own page.

- Allocations lists a $9,950 one-time standard SPV (plus $1,950/year) and a $19,500 premium tier.

That a platform as deep in the workflow as AngelList built a data room into its SPV product tells you the sharing problem is real. So where does a dedicated room like Peony actually earn its place? Four cases, all in the pre-commit window or outside the platform's lane:

- You raise off-platform or across several platforms and want one consistent, controlled room for the deal memo rather than a different setup each time.

- You want stronger per-viewer attribution than the bundled room — dynamic watermarks with the viewer's name and email on every page, screenshot protection, and single-viewer instant revoke on the memo and deck.

- You want real analytics on who actually opened and read the memo before you spend calls chasing soft commitments.

- The founder wants control — a confidentiality gate and an audit trail over the company data you're circulating on their behalf.

The clean division of labor: use the platform for the close (LLC, subs, KYC, Form D, K-1s — Peony does none of that and won't pretend to), and a controlled room for the sensitive sharing that happens before anyone has signed anything. One more reason leads value a portable, platform-independent room: SPV platforms are businesses too, and when one winds down — as the SPV administrator Assure did in late 2022 — leads scrambled to migrate. A deal-sharing room you own isn't hostage to any one platform's roadmap.

How do you stop a forwarded deal memo from leaking your allocation?

You change the economics of forwarding, because you can't make a file physically un-forwardable and anyone honest will tell you so. Someone can always screenshot the screen or photograph it with a second phone — that's the analog hole, and no data room closes it. What a good room does is shift forwarding from a silent, costless copy to every copy carries the leaker's name, which is what actually deters it inside a tight syndicate where reputation matters.

Three controls do the real work, and they map directly onto the pre-commit window's weaknesses:

- Per-recipient links. Each backer gets their own link, so a leak traces to one person rather than "the list." This alone changes behavior — people forward "the deal" freely but hesitate when the copy is stamped to them.

- Dynamic watermarks. The viewer's name, email, and a timestamp render onto every page of the memo and deck — and onto anything they screenshot. A leaked file becomes a signed confession. (More on how this works in watermarks and screenshot protection.)

- Instant, single-viewer revoke. The moment you learn a link was shared, you kill that one person's access without disrupting the rest of the syndicate.

On Peony, per-recipient links, link expiry, and page-level analytics are on the Business plan ($30/admin/month); dynamic watermarks, screenshot protection, granular per-file permissions, and single-viewer instant revoke are on the Data Room plan ($52/admin/month) — the tier most leads choose, because a watermarked, revocable memo is the entire point of not blasting a PDF. With 6,800+ customers, the pattern we see is consistent: the leads who never have a leak scare aren't the ones who shared less, they're the ones whose every share had a name on it.

How do you set up an SPV data room in under 30 minutes?

Fast, because the allocation clock is real. The setup mirrors the three phases, and you only need phase 1 ready to start sharing:

- Create the room and two top-level sections — "The Deal" (founder-cleared company materials) and "The SPV" (your memo and terms). Keep them separate; they have different owners.

- Upload phase-1 materials only — deal memo, the cleared deck, a financial summary, round terms, your SPV terms. Leave subscription docs and KYC for phase 2.

- Set default permissions to closed, then gate the sensitive items (full financials, cap table) behind a confidentiality click-through. On Peony, AI auto-indexing will classify a bulk upload into a clean structure so you're not dragging files one by one.

- Turn on attribution — per-recipient links, dynamic watermarks, screenshot protection. This is the step that protects the founder's data; don't skip it to save two minutes.

- Generate per-backer links and send, then watch analytics. Follow up with the backers who actually read the memo, not the ones who never opened it.

- When backers commit, move them to your SPV platform for subscriptions, KYC, and Form D — filed on EDGAR within 15 calendar days of your first sale (17 CFR 230.503) — then open a standing phase-3 room for closing confirmations and K-1s.

If you want the generic version of this build (any deal type, the universal workflow), start with how to set up a private placement data room and the private placement memorandum guide; this is the SPV-specific layer on top of it.

The bottom line: the room is the part you actually control

In an SPV raise, almost everything is outside your hands. You don't control the allocation, the founder's willingness to share, whether the round fills, or whether a backer wires on time. The one thing you fully control is how you share the deal in the pre-commit window — and that's exactly the moment that determines whether you protect the founder's trust or burn it. Share with attribution and control, and a leak has a name on it and a kill switch; share with a flat file blast, and you've handed someone else's confidential company to a list with no way to trace or stop a copy.

The platforms will handle your close. Your job as the lead is to be a clean steward of the data in the window before the close — because that's what keeps founders giving you allocations and backers trusting your judgment. Build the room around attribution, gate the sensitive material, keep a record you could show the founder, and you've turned the leakiest moment in the deal into the one you run best.

If you want to see how the controls work, Peony is free to start, and the syndicate workflow above runs on the Business and Data Room plans.

Related resources

- Data Room for Investors — the founder-side mirror of this guide: sharing your own company with VCs.

- Real Estate Syndication Data Room — the real-estate cousin: a single-deal raise for one property instead of a startup.

- Private Placement Data Room — the hub for running any Reg D securities offering as an evidence layer.

- Reg D Data Room: 506(b) vs 506(c) — the solicitation-path decision that governs your accreditation duty.

- How to Set Up a Private Placement Data Room — the generic offering-room build this SPV layer sits on top of.

- Independent Sponsor Guide — the PE control-deal version of deal-by-deal raising.

- Series A Data Room — the founder side of the round your syndicate is co-investing into.

- Dynamic Watermarks and Screenshot Protection — the attribution controls that make a forwarded memo traceable.

- Juniper Square Review (2026) — if you're weighing a full investor platform against the per-deal room model this post runs on.

You might also like

Jun 29, 2026

How to Share an Interactive LP Report With Your Limited Partners (Securely)

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

Real Estate Syndication Data Room: Making the Underwriting Survive the Room (2026)