Real Estate Syndication Data Room: Making the Underwriting Survive the Room (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Real Estate Syndication Data Room: Making the Underwriting Survive the Room

Last updated: July 2026

Quick answer: A real estate syndication data room is the sponsor-side room you use to raise LP equity for one identified property under Regulation D — and its real job is to make your underwriting survive scrutiny. Unlike a blind-pool fund (where LPs bet on your future picks) or a building sale (where a buyer values what exists today), a single-asset syndication asks LPs to bet on your projections for one specific asset. So the room is built around the pro forma and the evidence behind every assumption — exit cap, rent growth, renovation budget, financing — plus the waterfall, the fees, and your track record on this kind of deal. This guide covers what goes in the room, which assumptions LPs scrutinize, how to present the economics, and the 506(b)/506(c) choice. Run it on a flat-rate platform like Peony ($30/admin/month Business, $52/admin/month Data Room).

I'm Sean Yu, co-founder of Peony, a data room company serving 6,800+ customers — among them real estate sponsors raising equity for single-asset deals. The recurring mistake I see is treating the syndication raise like a building sale or a fund pitch: a glossy deck, big projected returns, and a thin room behind it. It doesn't survive a sophisticated LP, because the thing being sold isn't a building or a strategy — it's a set of projections for one property, and projections only hold up if every assumption behind them is on the record. The sponsors who fill their equity fast are the ones whose room makes the pro forma defensible line by line.

This is the sponsor-side playbook for that room: how it differs from a fund room and a sale room, what goes in it before an LP commits, the underwriting assumptions LPs scrutinize hardest in a higher-rate market, how to present the waterfall and fees without losing trust, the 506(b)/506(c) decision, and how to prove your track record. For the Reg D mechanics underneath it, this sits alongside the private placement data room hub.

A fact note: the economic conventions here — preferred return, promote, splits, fees, sponsor co-invest — are market norms, negotiated deal by deal, not regulated figures. I cite them as "commonly" and "typically," and I've flagged the traps (a preferred return is never "guaranteed"). Underwriting ranges are 2026 guidance, not rules.

What is a real estate syndication data room — and how is it different from a fund room or a sale room?

A real estate syndication data room is the secure, permissioned room a sponsor (the general partner) uses to raise equity from accredited limited partners to acquire and operate one specific, already-identified property — typically through an LLC or SPV, under a Regulation D private placement. The distinguishing word is single-asset: you have this building under contract, and you're raising the equity to close it.

That makes it a different document from its two neighbors, and getting the distinction right is what keeps this room from being a worse copy of either:

- Versus a fund room: A blind-pool real estate fund raises committed capital first and deploys it across deals the GP hasn't picked yet, so the fund room sells strategy and track record — the LP is betting on your future judgment. A syndication room sells this deal — the LP is betting on your projections for one asset they can see.

- Versus a sale room: A sell-side real estate data room hands a buyer the asset's diligence so they can value what exists today. A syndication room faces the opposite direction — you're raising equity to buy, and you're asking LPs to fund a future business plan, not price a present asset.

So the center of gravity shifts. In a fund room, the GP's portfolio strategy dominates. In a sale room, the asset's current condition and title dominate. In a syndication room, the underwriting model and the property-specific evidence dominate — because the LP's entire decision is whether your pro forma for this one property is believable. Everything else in the room exists to support that judgment.

Why does a syndication ask LPs to underwrite your projections, not your building?

Because the LP isn't buying the building — they're buying a share of what you project the building will do under your business plan. The current asset is the starting point; the return comes from the gap between today's operations and your stabilized pro forma. That gap is entirely made of assumptions: how much you'll lift rents, what the renovation costs and achieves, how expenses trend, what you refinance or sell into, and at what cap rate. The LP is underwriting that chain of assumptions, with you as the person warranting it.

This is the non-commodity point that most "data room" advice misses for syndications. A sale is a bet on current value — comps and condition settle it. A fund is a bet on future judgment — track record and strategy settle it. A single-asset syndication is a bet on a specific set of projections — and the only thing that settles it is whether each projection is backed by evidence. An 8% projected cash-on-cash is just a number until the room shows the rent roll, the comps, the contractor bids, and the debt term sheet that produce it.

So the room's job is to convert your pro forma from a claim into a defended position. Every assumption that flatters the return is a place a sophisticated LP will push, and the room either has the evidence ready or it doesn't. When it does, diligence builds confidence. When it doesn't, the LP either walks or discounts your projections to their own more conservative numbers — and your deal stops penciling. Make the underwriting survive the room, and the raise takes care of itself.

What goes in the room before an LP commits?

Before commitment, the room holds the offering package and the evidence behind it — not the closing paperwork, which comes later and per-investor. The offering rests on three core documents plus the proof that backs the numbers.

| Layer | Documents | Purpose |

|---|---|---|

| Offering core | Private Placement Memorandum (PPM); LLC operating agreement; subscription agreement + accredited-investor questionnaire | The PPM discloses the deal, terms, fees, waterfall, and risk factors; the operating agreement governs the SPV and distributions; the subscription docs are the LP's binding commitment at close |

| The pitch | Deal deck / offering summary; business plan | The narrative and strategy for this property |

| The proof (what wins the LP) | Underwriting model & pro forma; rent roll; T-12 operating statements; sales & rent comps; renovation scope + contractor budget; purchase agreement; appraisal; debt term sheet | The evidence that makes each pro-forma assumption defensible |

The PPM is the master disclosure document — offering summary, the Reg D legal disclosures and investor qualifications, the property description and business plan, the financial terms (minimum investment, projected returns, preferred return, splits), the fee structure, the distribution waterfall, and the risk factors. The operating agreement governs how the SPV runs and how distributions actually flow. The subscription agreement, paired with the accredited-investor questionnaire, is what the LP signs to commit.

But the framing that matters: the PPM discloses and the closing docs execute — the underwriting model and the property evidence are what actually win the LP. That's where they decide whether your projections are believable, so that's where the room should be strongest. Gate the PPM and detailed financials behind a confidentiality step, keep the property-level proof organized so an LP can tie each assumption to its source, and collect the signed subscription documents in a separate, per-investor closing folder so commitment paperwork never clutters the pitch.

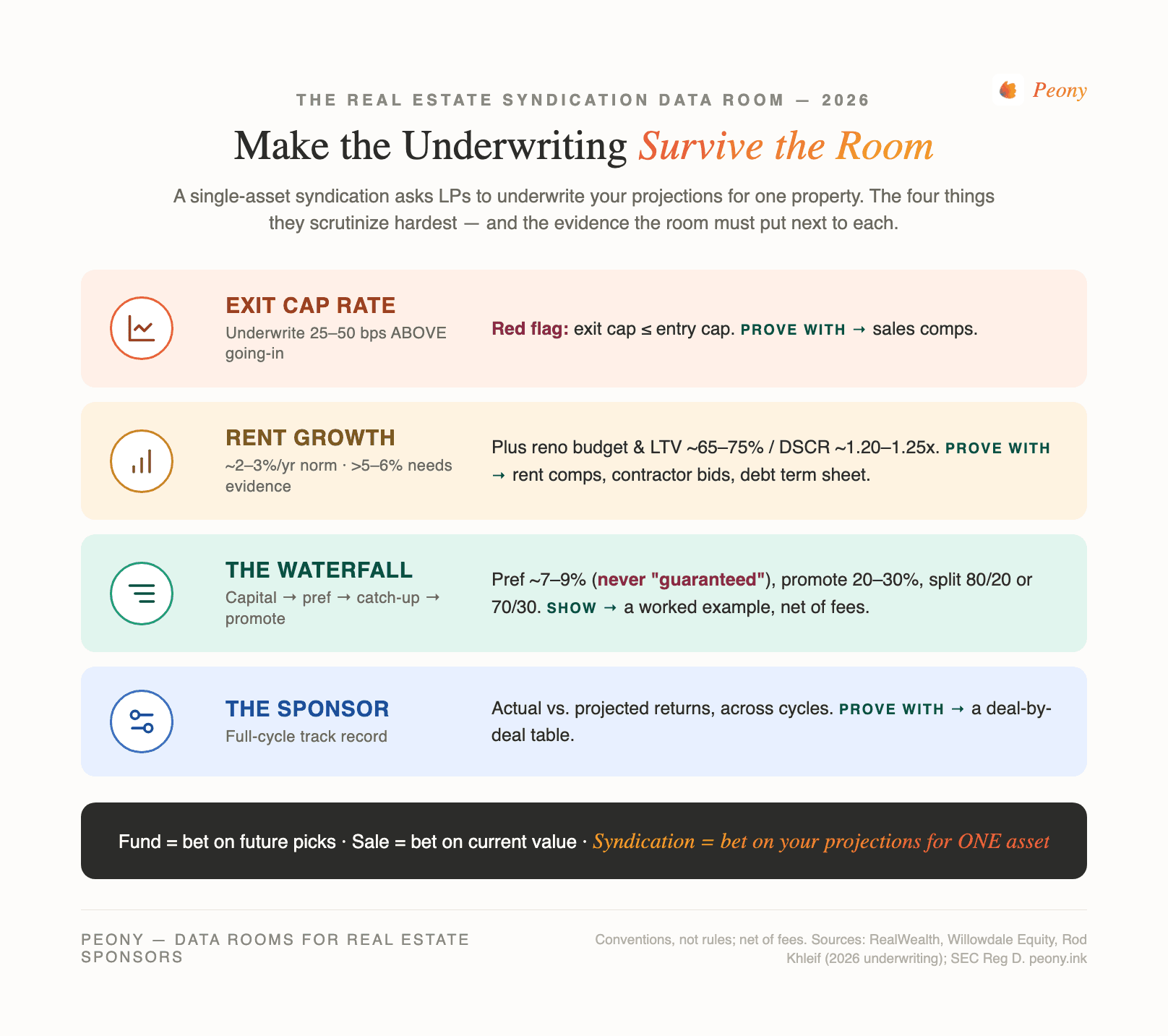

Which underwriting assumptions do LPs actually scrutinize — and what should the room prove?

In a higher-rate 2026 market, LPs scrutinize the assumptions that flatter returns. Pre-empt each one with evidence in the room; here are the ranges they'll measure you against (all guidance, not rules):

- Exit cap rate — the first thing they check. Conservative underwriting sets the exit cap roughly 25–50 bps above the going-in cap (buy at 6.0%, underwrite an exit at 6.5%). An exit cap at or below your entry is the single most common red flag — it assumes you sell into a richer market than you bought into. Prove your cap-rate assumptions with comps.

- Rent growth. ~2–3%/yr is the current norm. Anything above ~5–6% needs hard local evidence (specific comps, a clear value-add thesis) or it reads as a thumb on the scale.

- Renovation / value-add budget. Is the per-unit budget realistic and sourced from contractor bids? An unsupported reno number undermines the whole value-add case.

- Expenses & reserves. Expense growth ~2–3%/yr, with a CapEx reserve commonly ~$200–400/unit/year on stabilized assets.

- Financing. LTV around 65–75%, DSCR at least ~1.20–1.25x to clear agency debt. 2026 agency permanent rates run roughly 5.75–6.5% (Fannie DUS / Freddie Optigo, non-recourse); value-add bridge debt is higher (often ~8.5–13%, interest-only). Back this with the actual debt term sheet, not a placeholder.

- Target returns. Value-add levered IRR commonly ~12–18%, core-plus/stabilized ~8–14%, equity multiples ~1.5–2.5x, cash-on-cash ~6–8% — all quoted net of fees.

The capital stack itself is usually ~65–75% senior debt, ~20–30% LP equity, and ~5% GP equity (your co-invest). The single most useful thing the room can do is put every assumption next to its evidence: comps beside the cap-rate and rent assumptions, contractor bids beside the reno budget, the term sheet beside the financing line. A pro forma whose assumptions are each sourced survives diligence; one built on optimistic round numbers gets re-underwritten by the LP to their own conservative figures — and usually stops penciling.

How do you present the distribution waterfall without burying the LP?

The waterfall is the order in which cash flows to investors, and presenting it clearly is half the battle in earning trust — most LP confusion and back-and-forth comes from a waterfall buried in operating-agreement legalese. The common structure runs in tiers:

- Return of capital — LPs get their invested equity back first.

- Preferred return — LPs receive a priority return before the sponsor shares in profit, commonly cited around 7–9% (8% is the most-quoted figure), often cumulative so it accrues if unpaid in a given year.

- GP catch-up (optional) — a tier that lets the sponsor "catch up" toward its target profit share once LPs have their pref.

- Promote split — remaining profit splits between LPs and sponsor, commonly 80/20 or 70/30 (LP/GP), with LP-friendly deals at 90/10. Tiered waterfalls step the sponsor up (e.g., 80/20 to 70/30) as higher IRR hurdles are hit. The sponsor's share above the pref — the promote or carried interest — is commonly 20–30%.

Two things to get right so you keep LP trust. First, never call the preferred return "guaranteed." It's a priority, typically cumulative, return — not interest, and not assured; if the deal underperforms, the pref may simply accrue unpaid. Calling it guaranteed is both wrong and a credibility-killer with sophisticated LPs. Second, show a worked numerical example at base, upside, and downside exit scenarios, so the LP sees exactly what they receive at each tier rather than parsing legal language. A clear worked example, reconciled to the operating agreement, removes the most common source of LP friction — and signals that you have nothing to obscure.

What fees can a sponsor charge, and how should the room disclose them?

Sponsors commonly charge a few distinct fees, and the room should disclose each plainly — hidden or vaguely-described fees are a fast way to lose a sophisticated LP. The common ones, all market conventions negotiated deal by deal:

- Acquisition fee — commonly ~1–3% of purchase price (large institutional deals cluster near 1–1.5%; smaller or newer-sponsor deals sometimes run higher).

- Asset management fee — commonly ~1–2%/year, charged on gross revenue, equity, or AUM depending on the sponsor.

- Disposition fee — often charged at sale.

Three disclosure rules keep the room clean and trustworthy. Keep the promote and the fees distinct: the promote is performance-based carried interest earned only after the pref, while fees are charged regardless of performance — conflating them reads as either sloppiness or obfuscation. State that returns are net of fees: projected IRR, equity multiple, and cash-on-cash are normally quoted net, so say so explicitly to stop LPs double-counting. And put a single, plain fee table in the PPM and the deck rather than scattering fees across documents. Pair the fee table with your sponsor co-investment — commonly 5–20% of the equity, the "skin in the game" that signals your interests are aligned with the LPs'. Sophisticated investors don't object to fair fees; they object to fees they had to dig for.

506(b) or 506(c): how does your raise method shape the room?

Both are Regulation D private-placement exemptions, and the choice changes how your room gates access. Single-asset syndications almost always raise under one of them.

- Rule 506(b) — the more common choice for syndicators with an established investor network. You cannot generally solicit (no public advertising of the deal), you may accept up to 35 non-accredited but sophisticated investors alongside accredited ones, and accreditation rests on the investor's self-attestation under a "reasonable belief" standard. In the room: gate the PPM behind a confidentiality step and a pre-existing-relationship posture.

- Rule 506(c) — lets you advertise the deal publicly, useful for newer sponsors building a list or marketing digitally, but every investor must be accredited and you must take "reasonable steps to verify" it — a self-certification checkbox is not enough; you collect income or net-worth documentation, or a third-party verification letter from a CPA, attorney, broker-dealer, or registered adviser. In the room: add a verification-evidence intake step where each investor's accreditation proof is collected and logged before they reach the deal.

The room never verifies accreditation for you — it gates the deal behind that step and keeps a per-investor evidence trail that becomes part of your offering file. For the full mechanics of the two exemptions and the verification methods, see the 506(b) vs 506(c) data room guide and the private placement data room hub, and confirm the path with your securities counsel.

Do you need syndication software like Juniper Square or SponsorCloud — or is a data room enough?

It depends which job you're hiring for, because they're different layers — and plenty of sponsors buy the wrong one first. Platforms like Juniper Square, SponsorCloud (formerly SyndicationPro), and InvestNext are investor-management systems: a CRM and fundraising portal on the front end, and investor servicing on the back — distribution processing, K-1 delivery, and investor dashboards across a whole portfolio. They're built for sponsors running several deals and a standing investor base, and they're scoped and priced for that ongoing operation.

The raise itself needs something narrower: deliver the PPM under a confidentiality gate, keep exactly one current version, log per-investor who saw which document and when, and capture the subscription e-signatures. That's the Reg D evidence layer, it's a data-room job, and for a first or single-asset raise it's often all you need — at a flat monthly rate instead of a platform commitment. One of our customers, a 72-year-old owner-broker syndicating his own land-development deal solo, ran exactly this play: PPM and Reg D documents ready, then a self-serve room he set up himself, with email-verified logins giving him the record that each prospect had access to the required disclosures (his story is in the hub).

The honest boundary runs both ways. Peony is not a fund-administration or distribution-processing platform — when you're paying quarterly distributions across dozens of LPs and shipping K-1s every spring, the investor-management platforms are the right tool for that lane. The common-sense sequence for a new sponsor: run the raise's disclosure-and-evidence workflow on a flat-rate data room now, keep the same room as the post-close investor portal for updates and documents, and add an investor-management platform when the portfolio and recurring distributions justify it.

What do LPs diligence about the sponsor's track record?

They diligence whether you've actually done what you're proposing — all the way through. The gold standard is full-cycle deals: properties you acquired, executed the business plan on, and sold or refinanced. "Bought 50 properties" only proves you can buy; closing the loop proves you can execute and exit, which is what the LP's money depends on.

Beyond full-cycle proof, sophisticated LPs look at:

- Actual versus projected returns. A sponsor who projected an 18% IRR and delivered 15% is more credible than one who projected 30% and delivered 20% — consistency signals honest underwriting, not a habit of overpromising.

- A full deal history — acquisitions, dispositions, current portfolio, with outcomes.

- Performance across market cycles — was the return skill, or just a rising market that lifted everyone?

- References from prior LPs.

The room should make this trivial to verify: a sponsor track-record section with a deal-by-deal table showing projected-versus-actual returns, hold periods, and outcomes does more for LP trust than any amount of narrative. If you're a first-time sponsor without a full-cycle record, the honest move is to lead with the team's relevant operating experience and any deals you've done within another sponsor's team — and to underwrite conservatively, because you don't yet have a track record that earns the benefit of the doubt on aggressive projections. Sophisticated LPs reward candor about what you haven't done far more than they punish a short record.

How do you set up and control a syndication room?

Set it up to mirror the raise, and control it to protect the LP relationship and your own credibility:

- Two sections, separated: "The Deal" (offering core + pitch + the property evidence) and "Closing" (per-investor subscription docs, KYC, and any 506(c) verification evidence). Don't let closing paperwork clutter the pitch.

- Gate the PPM and detailed financials behind a confidentiality step, so the sensitive deal terms aren't visible until an investor accepts terms.

- Lead with the evidence: organize the property-level proof so each pro-forma assumption is one click from its source — that's what survives diligence.

- Use per-recipient links and analytics so you follow up with the LPs who actually read the model, and watermark the offering memorandum and financials with each viewer's identity (so a forwarded PPM is traceable). On Peony, per-recipient links and analytics are on the Business plan ($30/admin/month); dynamic watermarks, screenshot protection, granular per-file permissions, and AI auto-indexing are on the Data Room plan ($52/admin/month).

- Keep a standing investor portal after the close for distributions, K-1s, and quarterly updates — the relationship doesn't end at the wire.

The bottom line: make the pro forma defensible, and the raise follows

A single-asset syndication is the one real estate raise where the LP is betting squarely on your projections for one property. Not the building's current value, not your portfolio strategy — your pro forma for this asset. So the room's whole job is to make that pro forma survive scrutiny: every assumption that flatters the return backed by a comp, a bid, or a term sheet; a waterfall shown with worked numbers, not buried in legalese; fees disclosed in one plain table; and a track record that closes the loop on actual-versus-projected returns.

Do that, and diligence becomes confidence-building instead of return-discounting. The sponsors who fill their equity fast aren't the ones with the highest projected IRR on the cover — they're the ones whose room makes a sophisticated LP believe the number. With 6,800+ customers behind this, the pattern is consistent: defensible underwriting raises faster than optimistic underwriting, every time. Peony is free to start, and the syndication workflow above runs on the Business and Data Room plans.

Related resources

- Commercial Property Due Diligence (2026) — how a buyer runs diligence on the property you're syndicating, and what a finding lets them re-trade.

- Real Estate Fund Data Room (The 3-Room Model) — the blind-pool fund version, if you're raising across many future deals.

- Data Room for Real Estate (5 VDR Archetypes) — the sell-side version, if you're selling the asset rather than raising to buy it.

- Multifamily Acquisition Data Room — the buy-side transaction room for the apartment asset you're raising to acquire (reconciling the rent roll to leases without leaking resident PII), distinct from this LP capital raise.

- Real Estate Due Diligence Checklist — the underlying-asset inspection list that feeds your underwriting.

- SPV & Co-Investment Data Room — the venture version: a single-deal SPV into a startup instead of a property.

- Reg D Data Room: 506(b) vs 506(c) and Private Placement Data Room — the securities-law layer under the raise.

- Private Placement Memorandum — what goes in the PPM your room is built around.

- Juniper Square Review (2026) — the platform-vs-data-room decision in full: what Juniper Square includes, costs, and when a flat-rate room covers the raise.