Commercial Property Due Diligence: How to Run It Against the Clock (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Commercial Property Due Diligence: How to Run It Against the Clock (2026)

Last updated: June 2026

Quick answer: Commercial property due diligence is the finite, buyer-funded investigation you run after signing a purchase agreement and before the contingency period expires. Unlike a home sale, commercial real estate has no seller's disclosure form — caveat emptor governs and the deal closes "as-is," so the due-diligence period is the only protection a buyer gets. The core is national and standards-driven (a Phase I to ASTM E1527-21, an ALTA/NSPS survey, a Property Condition Assessment to ASTM E2018, estoppels reconciled to the rent roll, a trailing-12, and a zoning check), runs 30–90 days, and costs roughly $12,000–$30,000 in third-party reports. The deal is won or lost on how fast and cleanly that package moves between buyer, seller, and lender — which is why institutional deals run it inside a commercial real estate data room.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't underwrite buildings for a living — but I've watched hundreds of commercial property deals move through data rooms, and the pattern is always the same: the checklist is the easy part. Every law firm and brokerage publishes the same four-pillar list. What actually decides the outcome is how the diligence is run against the clock — the sequence, the contingencies, the re-trade, and how fast the package moves between the parties.

This is the buyer's playbook for that. Where you need the line-by-line document inventory, I'll point you to our real estate due diligence checklist; where you need the seller-side room setup and provider comparison, our data room for real estate guide maps it across five archetypes. This post is the connective tissue: the process.

What is commercial property due diligence — and why is it different from buying a home?

Commercial property due diligence is the buyer's investigation of a commercial asset's legal, physical, financial, environmental, and tenancy condition, run between contract and closing. The reason it is structured the way it is comes down to one doctrine: caveat emptor — let the buyer beware.

In a residential sale, most states require the seller to fill out a disclosure form listing known defects. In commercial real estate, that safety net does not exist. Commercial sellers generally have no affirmative statutory duty to disclose property defects, the deal closes "as-is," and there is little or no post-closing recourse for a problem you could have found yourself. The diligence period is your protection — the one window in which you can still discover something and act on it.

That single fact reshapes everything:

- The investigation is buyer-funded and buyer-driven. You hire and pay for the Phase I, the survey, the engineer, and the appraiser. No one hands you a defect list.

- Value is income, so financial diligence is central. Commercial value is roughly NOI ÷ cap rate. A verified-versus-claimed gap in net operating income doesn't just disappoint — it directly reprices the asset. Residential buyers rarely think this way; commercial buyers think about almost nothing else.

- The windows are longer. A home inspection contingency might be seven to ten days. Commercial diligence commonly runs 30 to 60 days, sometimes 90 or more — because there is far more to verify and no one is verifying it for you.

Get this framing right and the rest of the process follows from it. The checklist isn't a formality you tick on the way to closing; it's the mechanism by which a buyer with no disclosure safety net protects itself before the clock runs out.

What does commercial property due diligence actually check?

Eight workstreams, run in parallel. The trap in most checklists is that they list the documents but not the one thing that goes wrong in each — which is what actually kills or re-trades deals. Here is the buyer's-eye version. For the full document inventory inside each category, pair this with the real estate due diligence checklist.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Title & ALTA survey | Title commitment (Schedule B exceptions), ALTA/NSPS survey, easements, encroachments, access | The survey and the title exceptions are reviewed in isolation, so an encroachment never gets reconciled against the policy — you close with an uninsured gap |

| Environmental (Phase I/II) | Phase I ESA to ASTM E1527-21; Phase II soil/groundwater sampling if a Recognized Environmental Condition appears | Closing on a stale Phase I (it has a 180-day/1-year shelf life) forfeits the CERCLA innocent-landowner defense; treating a controlled REC as if it were closed |

| Zoning & entitlement | Zoning report, permitted use, parking/setback compliance, certificate of occupancy, legal nonconforming status | A parking or setback deficiency makes the building "legal nonconforming" — and it can't be rebuilt as-is after a casualty or re-tenanted to a new use |

| Leases & estoppels | Estoppel certificates and SNDAs reconciled to the rent roll; CAM, options, co-tenancy | Estoppels aren't collected from major tenants in time — and one surfaces an undisclosed free-rent or offset right that changes the underwriting |

| Financial (T-12 & NOI) | Trailing-12 operating statement, expense recoveries, normalized NOI | Underwriting to the seller's pro forma instead of the trailing-12 — and missing the post-sale property-tax reassessment that quietly shrinks NOI |

| Physical (PCA) | Property Condition Assessment to ASTM E2018 — roof, HVAC, structure, remaining useful life | Deferred roof/HVAC capex gets buried in a vague "reserve" instead of priced as immediate cost and negotiated as a credit |

| Insurance & climate | Flood zone, wind/named-storm deductibles, replacement cost, insurability | Underwriting last year's premium instead of next year's — or discovering the asset is barely insurable in a catastrophe zone |

| Tenant credit | Tenant financials, concentration, WALT (weighted average lease term) | Confusing duration with credit — a long lease behind a shaky single tenant is riskier than a short one across a dozen strong ones |

A few of these deserve a closer look because they are where the standards (and the liability) actually live.

Environmental is the one with federal teeth. A Phase I Environmental Site Assessment runs to ASTM E1527-21, which the EPA recognizes as satisfying its All Appropriate Inquiries rule. Since February 13, 2024, only E1527-21 qualifies — the older E1527-13 was retired — and a compliant report is what preserves your CERCLA "innocent landowner" and bona-fide-prospective-purchaser defenses. Miss the standard or close on a stale report and you can inherit strict, joint-and-several liability for contamination you didn't cause. If the Phase I flags a Recognized Environmental Condition, you escalate to a Phase II (ASTM E1903-19) with actual sampling. Our environmental due diligence guide goes deeper on the REC / HREC / CREC distinctions that trip up lay buyers.

Leases are where the income gets verified or evaporates. The rent roll is a claim; the estoppel certificate is the proof. Each tenant signs off on its rent, term, deposit, options, and — critically — whether the landlord owes it anything or is in default. An estoppel that surfaces an unrecorded side letter, a free-rent month, a purchase option, or a co-tenancy trigger can move the price. The SNDA (subordination, non-disturbance, attornment) is its companion: it governs what happens to the lease if the lender forecloses. Get these from the major tenants before your deadline or you're taking the rent roll on faith.

Physical condition is visual, which means it under-scopes. A Property Condition Assessment runs to ASTM E2018 (the current edition is E2018-24, which tightened the definitions and now keys "immediate repair" to imminent life-safety issues). It is non-destructive — a walk-through, not a teardown — so latent roof-membrane, structural, or below-grade problems get under-scoped unless you commission targeted follow-up on flagged items.

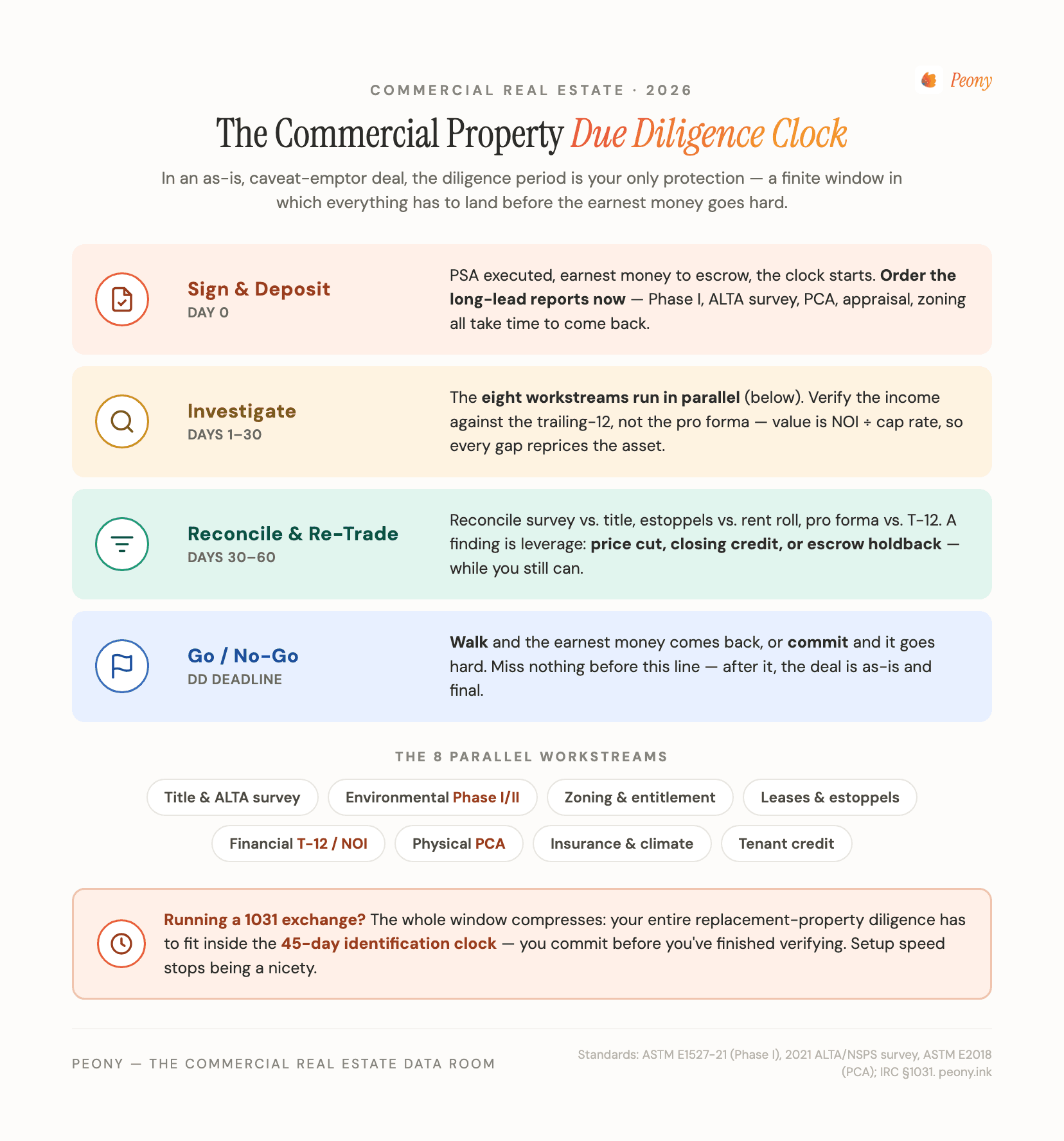

How long does commercial property due diligence take?

Most commercial property due diligence runs 30 to 90 days, with 30 to 60 the common target for a stabilized single asset and 120-plus for anything with entitlements or a Phase II. The number that matters isn't the length, though — it's what's contractually pinned to the end of it.

Three clocks run at once:

- The due-diligence (feasibility/study) period. Inside it, you can typically terminate for any reason and get your earnest money back. When it ends, the money usually goes hard and you're committed. Every report has to be ordered early enough to come back, get reviewed, and become leverage before this date.

- The financing contingency, if you have one — commonly 30 to 60 days, and the lender's own appraisal and survey take 30 to 45 of those, so they have to run inside the window. Worth knowing: financing contingencies are rarer in CRE than buyers assume — they appeared in under 10% of 2025 transactions, because most institutional buyers close on balance-sheet certainty rather than a financing out.

- The 1031 exchange clock, if proceeds are being rolled. This is the brutal one.

A 1031 like-kind exchange imposes two hard, non-extendable deadlines, both starting when your relinquished property closes: 45 days to identify replacement property in writing to your qualified intermediary, and 180 days to close it (or your tax-return due date, whichever is earlier). The identification has to satisfy one of three rules — the 3-property rule, the 200% rule, or the rarely-used 95% rule. The trap: your entire replacement-property diligence has to fit inside that 45-day window, which means committing to a property before you've fully diligenced it. (The One Big Beautiful Bill Act, signed July 4, 2025, left Section 1031 fully intact, so this workflow isn't going anywhere.) Our data room for real estate guide covers how the 45-day clock changes room-setup timing in detail.

The practical takeaway: in commercial diligence, setup speed is a real constraint, not a nicety. A week lost provisioning a data room or hunting for a misfiled rent roll is a week off a finite, often non-extendable clock.

Who pays for due diligence — and what's the difference between the DD fee and earnest money?

The buyer pays for its own investigation. Here's what that actually costs in 2026 — ranges, because every number varies by asset size, age, complexity, and market. Treat them as rules of thumb, not quotes.

| Report | Typical 2026 range |

|---|---|

| Phase I ESA (ASTM E1527-21) | $2,000–$5,000 |

| Phase II ESA (if triggered) | $5,000–$30,000+ |

| ALTA/NSPS survey | $3,000–$8,000 |

| Property Condition Assessment (ASTM E2018) | $1,500–$10,000 |

| MAI appraisal | $4,000–$10,000 |

| Zoning report | a few hundred to a few thousand |

| Legal review | $1,500–$10,000+ |

| All-in (excluding Phase II) | ~$12,000–$30,000 |

Total buyer closing costs — diligence plus financing, title, and recording — usually land around 2% to 5% of purchase price. See our due diligence cost breakdown for how this scales with deal size.

Now the distinction that confuses first-time commercial buyers: the due-diligence fee is not the earnest money.

- Earnest money deposit: held in escrow, normally refundable while you're inside the due-diligence period, and non-refundable once it ends. It's your good-faith stake.

- Due-diligence fee: in some markets — North Carolina is the textbook case — a separate, typically non-refundable payment made directly to the seller to compensate them for taking the property off-market during your study. You usually credit it toward the price at closing, but you forfeit it if you walk.

The single most important thing to do before the clock starts is read the purchase agreement and know which dollars are refundable, and on exactly what date. Everything else in diligence is a race to that date.

What happens when due diligence finds a problem? (The re-trade)

You re-trade, or you walk. The due-diligence period is the one window in which new information still moves the price — which is exactly why experienced buyers treat it as a negotiation, not a formality. "You make your money when you buy it" is a cliché in CRE because it's true: the discount you negotiate off a diligence finding is permanent equity.

When diligence surfaces a problem, you have four moves:

- Price reduction. A deferred-capex finding from the PCA (the roof has three years left, not fifteen) or a normalized-NOI gap (the property taxes reassess on sale and shrink income) is a direct, defensible basis to cut the price.

- Closing credit. Instead of cutting price, the seller credits you cash at closing against a specific, quantified issue — common for capital items.

- Escrow holdback. For an unresolved item — an open permit, an environmental condition mid-remediation, an estoppel still outstanding — money is held back in escrow until it's resolved.

- Walk. If the problem is fatal and you're still inside the window, you terminate and your earnest money comes back. The credible threat to walk is what makes the first three moves work.

The reason disorganized deals re-trade worse isn't that the problems are bigger — it's that they surface late, after the buyer has sunk cost and the seller has lost other bidders. Which brings us to the part nobody writes about.

How does the data room actually run commercial property due diligence?

This is the workstream the four-pillar checklists skip: the diligence has to be executed across buyer, seller, lender, and a stack of third-party consultants — and on an institutional deal that means moving 200-plus documents under access control against the clock. The data room is where that happens. I run Peony, so treat this as informed but interested — and I'll tell you where you don't need it.

Four things separate a deal that closes cleanly from one that re-trades:

1. The document request list flows one way; the package should already be there. Diligence formally kicks off when the buyer's counsel sends a request list. The seller's mistake is treating that list as a to-do — scrambling to find a rent roll, a 2022 CAM reconciliation, a missing estoppel. The seller's winning move is to stage the package before the request lands, mirroring the eight workstreams, so day one of diligence the buyer finds everything indexed and waiting. That single discipline is the most reliable re-trade preventer there is, because problems surface early — while the seller still has leverage and other bidders.

2. Role-based access, one room, no leaks. A commercial deal has parties who should not see the same things. The seller and its broker have full read-write. The buyer and its counsel get read-and-download. The lender is scoped to financial, title, and environmental — not the equity-side returns. Consultants see only their lane: the environmental firm sees the Phase I folder, not the leases. Flat "admin / viewer" file-sharing can't model this without spinning up parallel folders that fragment the audit trail; programmatic permission groups do it in one room.

3. Who-reviewed-what is a deal-velocity signal. When the seller can see that a serious bidder spent forty minutes in the lease folder but never opened the environmental section, that's intelligence — push the Phase I proactively, clear the objection before it becomes a re-trade. Page-level analytics turn the room from a passive file dump into a read on who's real and what they're worried about.

4. The confidential stuff stays traceable. Rent rolls carry tenant PII; offering memoranda get forwarded. Dynamic watermarks stamp every page with the viewer's identity, an NDA gate sits in front of the room, and redaction blacks out tenant names or lease rates for parties who shouldn't see them yet. On a deal where a leaked rent roll can blow up a tenant relationship, traceability changes behavior.

Peony does this at a flat $52/admin/month with AI auto-indexing that sorts a bulk upload into the standard real-estate folder tree in minutes — which is what makes the 45-day-clock math survivable. We serve 5,900+ customers, and our data room for real estate guide maps the setup across CRE single-asset, multifamily portfolio, REIT, distressed, and development archetypes.

Where you don't need any of this: a small, all-cash, single-tenant deal with one attorney can absolutely run on a few emailed PDFs — and for a $1B-plus institutional take-private, the procurement default is still Datasite or Intralinks, whose buyers' counsel often mandates them. The data-room-for-CRE sweet spot is everything in between: a $2M strip center to a mid-market portfolio with a lender, multiple bidders, and a clock.

Does the state actually change commercial property due diligence?

Mostly, no — and this is worth saying plainly, because a wave of "[State] commercial property due diligence checklist" pages can make it look like you have to relearn diligence in all fifty states. You don't.

The spine is national and standards-driven. A Phase I to ASTM E1527-21, an ALTA/NSPS survey to the 2021 standard, a Property Condition Assessment to ASTM E2018, estoppels reconciled to the rent roll, a trailing-12, and a zoning check apply whether the asset sits in Ohio or Oregon. These are uniform national standards, not local conventions. The checklist doesn't change state to state — a short list of line items gets added.

Here are the states that genuinely move the needle, and the specific item that does it:

| State | The genuinely-distinct item | Why it matters |

|---|---|---|

| California | Natural Hazard Disclosure (Alquist-Priolo fault zones), Prop 65, CASp access, local soft-story/non-ductile retrofit ordinances | Seismic-zone constraints, mandatory access disclosures, and hard retrofit deadlines with real capex |

| New York (NYC) | Local Law 97 emissions caps ($268/excess ton), open ECB violations, transfer tax with a controlling-interest rule, sidewalk vault charges | Recurring carbon penalties to underwrite; an ECB judgment blocks clean title; entity deals can still trigger transfer tax |

| Texas | No state transfer tax, no mandatory commercial seller disclosure, severed mineral estates, MUD/PID districts | Pure caveat-emptor on disclosure; a dominant mineral estate can authorize surface drilling; special-district assessments hit underwriting |

| Florida | Wind/named-storm and flood insurability, sinkhole regime, Chapter 558 construction-defect notice, coastal construction line | Insurability now drives deal economics; statutory coverage and notice rules reshape risk and warranty |

| Louisiana | Civil-law system: mineral servitudes, usufruct, notarial acts | Title review and closing mechanics are structurally different from the other 49 states |

| Massachusetts | Chapter 21E strict, joint-and-several environmental liability; municipal betterment liens | You can be strictly liable for pre-existing contamination you didn't cause unless you qualify for a Brownfields exemption |

| Maryland | Ground rent / ground leases; recordation tax on capitalized rent | You may be buying a leasehold subject to redeemable ground rent, taxed on a formula, not just price |

| Illinois (Chicago) | Full Payment Certificate required on every transfer | No water/sewer paid-in-full certificate, no clean recording — a procedural gate national checklists miss |

| New Jersey | ISRA — a transaction-triggered cleanup for industrial sites | The sale itself triggers a mandatory environmental process; non-compliance lets the buyer void the deal |

That's the honest version: learn the national spine cold, then ask a local counsel exactly one question — "what does this state add?" — instead of treating every jurisdiction as a new universe.

Why does commercial property due diligence matter more in 2026?

Because the margin for error has narrowed. Three things changed the backdrop, and each one raises the cost of a missed line item.

Office distress is real and bifurcated. Office values are down roughly 35% from their 2022 peak (Green Street, January 2026), and office CMBS delinquency hit an all-time high of 12.34% in January 2026 before easing slightly in February (Trepp) — above even the financial-crisis peak. But it's split: trophy, well-leased assets are recovering while commodity older office stays impaired. Diligence on tenant credit and WALT is doing more work than it has in a decade.

Insurance is the line item everyone gets wrong — in both directions. The popular narrative ("premiums are exploding") is out of date. The hard market peaked in 2022–2024; in 2025, broad commercial rates actually fell — Marsh's index showed global commercial rates down about 3% and US property down roughly 4%. But the structural climate repricing underneath it persists, concentrated by geography: insured catastrophe losses ran about $108B in 2025, and catastrophe-zone assets face higher deductibles, resiliency requirements, and in places genuine availability problems. The honest 2026 framing: the broad market is softening, but cat-exposed assets are being structurally repriced — so you underwrite next year's actual cost and deductible structure, not last year's premium.

The maturity wall keeps deals — and diligence — coming. Roughly $875B of commercial and multifamily debt matures in 2026 (Mortgage Bankers Association), and cap rates appear to have peaked (CBRE, H2 2025). A lot of that debt resolves through a sale or recapitalization, each of which runs its own diligence. The volume is there; the room for sloppy underwriting is not.

None of this changes the checklist. It changes the stakes of running it well — which loops back to where we started: in a caveat-emptor, as-is market, the diligence period is the only protection you get, and in 2026 you want to use all of it.

The bottom line: due diligence is the only protection you get

Commercial real estate hands the buyer no disclosure form and no post-closing do-over. The due-diligence period is it — a finite, buyer-funded, often non-extendable window to verify the income, the title, the environment, and the bricks before your earnest money goes hard. The checklist is the easy 20%. The hard, deal-deciding 80% is running it against the clock: ordering reports early, collecting estoppels before the deadline, surfacing problems while you still have leverage to re-trade, and moving 200 documents among buyer, seller, and lender without losing a week to disorganization.

- Solo / small all-cash deal: a tight checklist, a good attorney, and a shared folder are plenty. Don't over-tool it.

- Financed single asset or portfolio with multiple bidders: run it in a commercial real estate data room — NDA gate, role-based access, per-viewer watermarks, and who-reviewed-what analytics earn their keep, and a flat-rate room like Peony keeps the cost off the deal.

- $1B-plus institutional: Datasite or Intralinks remain the procurement default; we're honest about that.

If you take one thing from this: read your purchase agreement for which dollars are refundable and on what date, then work backward. Every report, every estoppel, every renegotiation has to land before that line. The buyers who win the re-trade are the ones who saw the problem first — and the room is how you see it first.

For the document inventory, see the real estate due diligence checklist; for seller-side room setup across deal types, the data room for real estate guide; and for the broader process, our M&A due diligence process guide. Peony serves 5,900+ customers — start free or compare Peony for commercial real estate.

Sources

- Environmental standards: ASTM E1527-21 (Phase I ESA) and ASTM E1903-19 (Phase II); US EPA, All Appropriate Inquiries Final Rule (40 CFR Part 312); E1527-21 mandatory for AAI since February 13, 2024.

- Survey & physical standards: 2021 ALTA/NSPS Minimum Standard Detail Requirements (NSPS); ASTM E2018-24 (Property Condition Assessment).

- 1031 exchange: IRC §1031 and Treas. Reg. §1.1031(k)-1 (45-day identification / 180-day exchange; 3-property, 200%, and 95% identification rules); One Big Beautiful Bill Act (July 4, 2025) left Section 1031 intact (IPX1031).

- Market data (2025–2026): Green Street Commercial Property Price Index (office −35% from 2022 peak, Jan 2026); Trepp (office CMBS delinquency record 12.34%, Jan 2026); Marsh Global Insurance Market Index 2025 (commercial rates −3% global, US property −4%); Munich Re (≈$108B insured catastrophe losses, 2025); Mortgage Bankers Association (≈$875B CRE/multifamily debt maturing 2026); CBRE US Cap Rate Survey, H2 2025.

- Process & doctrine: caveat emptor in commercial real estate (various CRE law-firm explainers); estoppel certificates and SNDAs; trailing-12 and NOI normalization; WALT (weighted average lease term).

This guide is general information for commercial real estate buyers and advisors, not legal, tax, environmental, or investment advice. Standards, statutes, and market figures change — verify current editions and consult qualified local counsel, a licensed environmental professional, and your tax advisor before acting. Cost and timeline figures are industry rules of thumb that vary by deal.