Data Room for Infrastructure Projects: The Project-Finance Raise Room (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Data Room for Infrastructure Projects: The Project-Finance Raise Room (2026)

Last updated: July 2026 · Last verified: July 2026

I'm Sean Yu, co-founder of Peony, a data room company. Most of the rooms I watch move through diligence are about an asset that already exists — a company with revenue, a building with tenants, a portfolio with a rent roll. An infrastructure raise is different in a way that changes everything about how the room has to be built: the asset doesn't exist yet.

An infrastructure raise is diligence on a promise. There is no operating history to interrogate, no in-place cashflow to discount — there is a site, a set of consents in progress, a grid position, a stack of contracts, and a model that says if all of it lands, the thing will be built and it will pay. The data room is where a sponsor proves that promise is bankable — grid, planning, land, contracts, model — before the counterparty's investment committee will spend a pound of internal time. Get the room right and a fund's IC can underwrite the promise. Get it wrong and they never open the model.

This guide is for the person building that room: a capital-markets or finance lead at an infrastructure developer or sponsor, usually a small team, raising JV equity and development debt across the asset classes where this pattern repeats — data centres, renewables, transmission, transport, utilities. The counterparties on the other side of the table are infrastructure funds, private equity, family offices and lenders, and each of them reads the room differently.

Quick answer: An infrastructure project-finance data room is the sell-side room a sponsor builds to prove a not-yet-built asset is bankable to incoming capital. It is organised as a numbered skeleton of roughly ten to twelve folders — 01 Corporate & structure, 02 Land & real estate, 03 Consents & planning, 04 Grid & utilities, 05 Power strategy, 06 Technical, 07 Commercial, 08 Financial model & assumptions, 09 ESG, 10 Insurance, 11 Legal, 12 Q&A — sequenced so the four kill-question documents (grid, planning, land control, model integrity) sit at the top. It serves the sponsor sell-side, and is read by infrastructure funds, PE, family offices and lenders on the buy-side. For sub-£1bn raises, per-admin SaaS pricing has replaced per-page pricing: a room like Peony runs $30-$52 per admin per month with every fund, lender and adviser invited for free — so the bill is bounded by your small team, not by document count or counterparty list.

Where this post sits. This is the horizontal project-finance raise room across asset classes. It is deliberately not the single-asset acquisition guides: if you are buying an operating data centre, read Data Center Data Room (energisation risk on a built asset); for the US solar/wind/BESS project room with its ITC/PTC and interconnection specifics, read Renewable Energy Data Room; for the UK data-centre development diligence detail, see UK Data Centre Due Diligence. For the general property process — caveat emptor, the contingency clock, re-trades — read Commercial Property Due Diligence. This post is the layer above all of them: how you build the raise room itself, whatever the asset class underneath.

Which data room do infrastructure funds expect to see in a raise?

They expect a disciplined room, and they judge it on discipline far more than on the logo. This is the question I get asked most by first-time sponsors, and the honest answer disappoints the people hoping the brand is a shortcut: a fund's investment committee is underwriting your project and your professionalism, not your software vendor.

What they actually read is room discipline, and it has four components:

- Index quality. A clean, numbered top-level folder structure that mirrors the diligence workstreams, so a reviewer lands and immediately knows where the grid offer, the planning pack and the model are.

- Version control. A single current model and a single current contract behind stable links, so nobody is underwriting last month's numbers by accident.

- A real Q&A process. A logged thread where questions, answers and any released documents live together — not a scatter of emails across three inboxes.

- Permission hygiene. Folder-level permissions per counterparty class, so competing funds never see each other and confidential terms never leak sideways.

The VDRs infrastructure funds have seen most are the legacy enterprise platforms — Datasite and Intralinks — because those have dominated large syndicated project finance for years. That is a real fact and worth knowing: on a £1bn+ bank-led deal, the procurement default is one of those, and I won't pretend otherwise. But that is a statement about mega-deals, not about what the room must be. A modern per-admin room is fully accepted when the index is institutional — funds care that the room is well-run, and a well-run per-admin room reads exactly as credibly as a well-run enterprise one.

So what does "institutional-looking" concretely mean, stripped of the marketing? It means: a numbered folder skeleton that follows the workstreams; the single current model behind a stable link so version discipline is visible; watermarked sensitive documents; folder-level permissions per counterparty class; and a logged Q&A thread. A three-person developer that does those five things has a room a fund's IC will take seriously. A fifty-person developer that dumps 800 files into a flat Dropbox folder does not. The discipline is the signal, and it is entirely within your control regardless of budget.

How to structure a data room for an infrastructure project finance raise

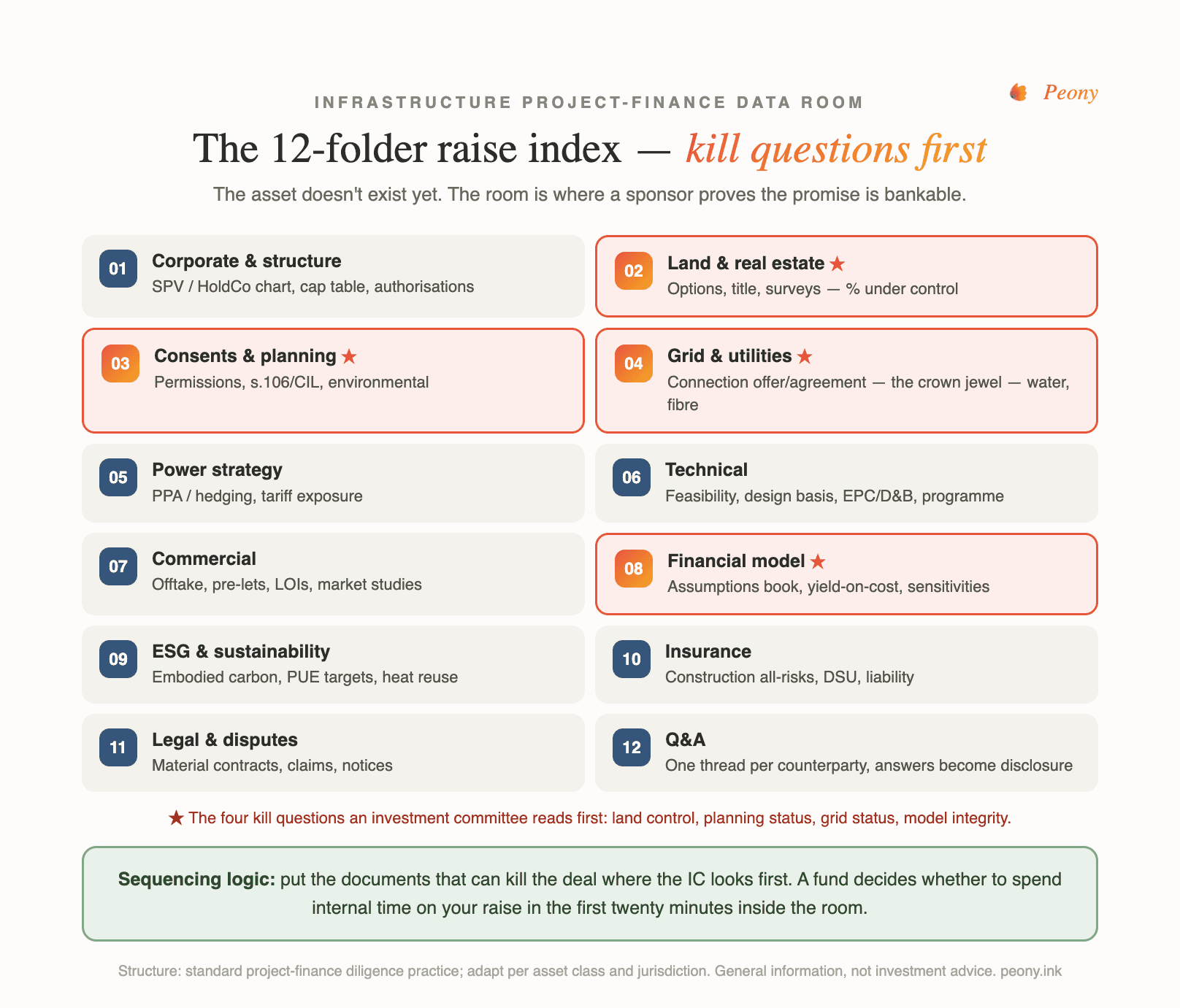

Build a numbered skeleton of roughly ten to twelve top-level folders, sequenced so the kill-question documents come first. The number is less important than the ordering logic, which I'll explain after the skeleton — because an infrastructure fund does not read a room front to back, and the structure has to respect that.

Here is a working top-level structure for an infrastructure project-finance raise:

- 01 Corporate & structure — the SPV/HoldCo chart, incorporation documents, cap table, board consents. The reader's first question is "what am I investing into, legally?"

- 02 Land & real estate — option agreements, title, surveys, access and wayleave rights, the percentage of the site actually under control.

- 03 Consents & planning — planning permissions or their status, s.106/CIL obligations (or the local equivalent in your jurisdiction), the environmental statement and any conditions.

- 04 Grid & utilities — the connection offer or, once accepted, the connection agreement. This is the crown jewel for any energy-adjacent asset — data centres, renewables, anything power-hungry. It also holds water and fibre connectivity where relevant.

- 05 Power strategy — the PPA or offtake for power, hedging arrangements, any behind-the-meter or on-site generation, the energisation programme.

- 06 Technical — feasibility studies, the design basis, the EPC or design-and-build contract, the construction programme, contractor covenant and warranties.

- 07 Commercial — offtake agreements, pre-lets or LOIs, market and demand studies, anchor-counterparty terms.

- 08 Financial model & assumptions — a single current model behind a stable link, with its assumptions book alongside so a reviewer can test it.

- 09 ESG & sustainability — embodied carbon, sustainability targets, community and biodiversity commitments, the ESG narrative institutional capital increasingly requires.

- 10 Insurance — construction and operational insurance, the insurance adviser's report.

- 11 Legal & disputes — material contracts summary, litigation and disputes, permits register.

- 12 Q&A — the logged question-and-answer thread that runs through the whole raise.

The sequencing logic is the point: put the kill-question documents first. An IC does not open folder 01 and read to folder 12 — it goes straight to the four things that can kill the deal and, if any of them fails, stops. Those four are grid, planning, land control and model integrity, so the folders holding them (04, 03, 02 and 08) have to be findable in one click from the front of the room. Everything else — corporate housekeeping, insurance, the disputes register — can sit deeper, because no fund declines a good project over the insurance folder. It declines because the grid connection is indicative not firm, the planning is stuck, the land isn't controlled, or the model doesn't hold. Structure the room so those answers are the first ones a reviewer finds.

What goes in each folder that an infrastructure fund's IC actually reads first?

Four documents, in four folders, answer the four kill questions — and a good IC reader goes to them before anything else. If you understand nothing else about how your room will be read, understand this: the raise lives or dies on these four, and the rest of the room is context.

Grid connection status (folder 04). For any energy-adjacent asset this is the crown jewel, and the reader is looking for one distinction above all: is the connection firm or indicative? A firm, dated connection offer with confirmed capacity is financeable; an indicative or waiting-list position is not, and it materially changes the valuation. The IC reads the offer for capacity (in MW/MVA), connection date, milestones, and any securities or cancellation charges. A conditional grid position is the single most common reason an energy-infrastructure raise stalls, because lenders generally will not fund construction until power is committed. Put the connection document at the top of folder 04 and make its status unambiguous.

Planning status (folder 03). The reader wants to know whether the project can actually be built where it says it will be. Full permission is best; a submitted application with a credible timeline is workable; a pre-application position is early. The IC reads for the route (local planning authority versus a national-significance regime, which differs by jurisdiction), the conditions still to discharge, and any s.106/CIL or local-equivalent obligations that carry cost. Planning risk is binary in a way that scares capital — a refusal can end a project — so evidence of where you are in the process is read early and hard.

Land control percentage (folder 02). A promise you can't build on isn't bankable, so the reader checks how much of the site is genuinely under control — owned, optioned, or under conditional contract — and how secure those rights are. An option with years to run and clean title reads very differently from a handshake and an intention. The number that matters is the percentage of the required site actually controlled, and gaps in it are a kill question because they gate everything downstream.

Model integrity (folder 08). The model is the promise quantified, and the IC reads it for whether it holds together — not just the headline return but whether the assumptions are defensible and internally consistent. Lenders go straight to the cover ratios (debt-service and loan-life coverage); equity goes to the return sensitivities and the downside cases. The fatal error here is a model that has drifted from the documents: a connection date in the model that the grid offer doesn't support, a construction cost that the EPC contract contradicts. The model's assumptions have to be traceable to documents in the room. Keep one current version behind a stable link, with the assumptions book beside it, so a reviewer can test the promise rather than take it on faith.

Get those four folders right and the rest of the room is ordinary diligence. Get any of them wrong and nothing else you've assembled will save the raise.

How is a project-finance room different from an M&A data room?

The defining difference is that the asset doesn't exist yet, and that single fact cascades through the entire room. An M&A room proves what is: audited accounts, existing contracts, an operating history, a rent roll. A project-finance room proves what will be — it is built out of forward-looking documents, and a reviewer is underwriting a promise rather than a track record.

That changes three things concretely:

The documents are forward-looking, not historical. Where an M&A room leads with trailing financials, a project-finance room leads with entitlement, power and contracts — the evidence that the thing can be built and will pay. There are no three years of accounts for an asset that hasn't been constructed; there is a model, a grid offer, a planning consent and an EPC contract, and the diligence is about the credibility of those forward commitments. (For the one case where an "infrastructure" deal is actually an acquisition of a built, operating asset — buying a stabilised data centre with in-place leases — the room reverts closer to M&A shape; that's the subject of the Data Center Data Room guide, which organises around energisation risk on an existing asset.)

The counterparties overlap but read differently. An M&A room has essentially one type of reader — the acquirer and its advisers. A project-finance raise has two, and they underwrite different questions from the same documents. Lenders want the contracts and the cover ratios — the grid agreement, the EPC wrap, the offtake, and the model's debt-service and loan-life coverage — because their return is fixed and their entire focus is downside protection. Equity wants the upside and the control terms — the return sensitivities, the platform and follow-on potential, the shareholders' agreement and governance rights — because their return is the residual. The same model folder serves both, but the lender opens it at the coverage ratios and the equity investor opens it at the IRR. Your permission structure has to serve both sightlines from one room.

The room lives longer. An M&A room is taken down after close. A project-finance room often becomes the construction-phase archive — the same connection agreement, EPC contract and consents pack that funded the raise are the documents the project is administered against through construction and into operation. So the room is not a three-month transaction artefact you delete; it is a longer-lived record, which is another reason a per-admin model that doesn't meter storage or time fits better than a per-project deal room built to close and shut.

For the underlying property-diligence process that sits beneath any real-asset raise — the contingency clock, the caveat-emptor discipline, the re-trade dynamics — the Commercial Property Due Diligence guide covers the mechanics this post assumes.

How do you run phased disclosure without leaking the crown jewels?

You stage disclosure in tiers — teaser, then NDA, then graduated room access — and you use folder-level permissions to make sure the crown-jewel documents only open once a counterparty has earned them. The whole point of phased disclosure is that you are running many funds and lenders through the same room in parallel, and not all of them should see everything on day one.

The standard funnel looks like this:

- Teaser (blind or lightly anonymised). A short overview that lets a fund decide whether to engage, without exposing the site, the pricing, or the confidential contracts. Anyone can see it.

- NDA gate. Access to the room proper is conditional on accepting an NDA — the click-through record that a counterparty agreed before they saw a single confidential document.

- Room tiers. Inside the room, folder-level permissions per counterparty class decide who sees what. An approved fund sees the commercial and model folders; a lender sees the contracts and coverage; neither sees the other's correspondence, and no counterparty sees a competing one. Visitor groups make each class its own isolated view.

Within that structure, the crown jewels get extra protection:

- Watermarks. The full model and the grid documents carry a dynamic watermark with each viewer's identity, so a leaked copy points back to the counterparty it came from — a real deterrent when you are circulating your most sensitive terms.

- Staged unlock. Even inside an approved group, the full financial model and the grid documents can sit behind a later release — the teaser and headline metrics open first, and the model with its assumptions only unlocks once a counterparty is genuinely progressing. You are not obliged to hand your best evidence to a fund that has barely engaged.

- Visitor groups. Each counterparty class is its own group with its own folder map, so managing "who can see the model" is a group setting, not a per-file scramble.

And here is the part sponsors under-use: what page-level analytics tells you during a raise. Because you can see who opened which document and for how long, the room becomes a live read on your process — page-level analytics shows you which fund opened the model and which never got past the teaser. That is not a vanity metric; it is the data to re-forecast your raise from actual engagement. A fund that has spent an hour in the model, the grid offer and the offtake is real and worth chasing for a term sheet; a fund that opened the teaser three weeks ago and never came back is telling you it is cold, whatever it says on a call. Sequence your follow-up, time your term-sheet push, and read your leverage from who is actually in the documents — not from who is politest on the phone. (To be precise about what this is: page-level analytics is view-and-dwell data — who opened what, and for how long — not keystroke capture.)

Best AI-powered VDR platforms for managing complex infrastructure deals

The honest short version: AI in a data room is genuinely useful for Q&A drafting off the room's documents, but you should check two things before you trust it — whether its answers cite the source documents, and whether the model it runs on retains your data. The infrastructure raise is a good use case for AI Q&A precisely because the document set is large and technical, and reviewers ask the same questions in different words.

What AI-powered Q&A actually does well in an infrastructure room: a fund asks "what is the connection capacity and date," and instead of you hand-drafting the answer from folder 04, the AI drafts it from the documents already in the room. On a raise where thirty counterparties ask overlapping questions about the grid offer, the model, and the consents, that is real time saved.

Two things to check before you rely on any of it:

- Citations to source documents. A useful AI Q&A answer points at the document it drew from, so you can verify it before it goes to a counterparty. An answer with no citation is a liability — you cannot send a fund a confident-sounding statement about your grid position that you can't trace to the offer.

- Zero-retention model access. Your room contains your most sensitive commercial terms — grid capacity, PPA pricing, pre-let economics. You do not want those training a third-party model or being retained. Check that AI access to your documents is zero-retention.

Where Peony sits, honestly: Peony's AI Q&A runs only against the models you connect, with zero retention — you bring the model, your documents are not retained, and the answers draw from what is in the room. That is the right posture for confidential deal documents. And the honest concession: Datasite and Intralinks ship deal-team-scale AI suites — broader, more integrated, built for large syndicated processes — at enterprise price points. If you are running a £1bn+ bank-led deal, that tooling is part of what you are paying for. For a sponsor-run sub-£1bn raise, AI Q&A against your own connected model, with citations and zero retention, is the feature that matters and the price that fits. See Smart Q&A for how the Q&A workflow runs.

How much does a virtual data room cost for a project finance raise?

For a sub-£1bn raise, a full data room costs in the low hundreds of dollars total — because per-admin SaaS pricing has replaced the per-page and per-GB models that made VDRs expensive. This is the single biggest change in the economics of running a raise as a small sponsor, and it is worth being precise about.

Peony's pricing is per admin seat:

- Business — $30 per admin per month (annual billing).

- Data Room — $52 per admin per month (annual billing), adding dynamic watermarking and unlimited rooms — the tier most raises want, because watermarking is what makes the model and grid documents traceable.

A 3-to-6-month raise typically runs with two to four admins, and every recipient is free — every fund, every lender, every adviser you invite. So the total for the whole raise lands in the low hundreds of dollars, bounded by your own small team rather than by how many documents you load or how many counterparties you invite.

Compare that with legacy per-page or per-GB enterprise quotes, which land in the $15K to $68K range (these figures are site pricing canon):

- Datasite — around $68K on annual enterprise deals.

- iDeals — roughly $500 to $1,000 per month depending on scope.

- DealRoom — around $12K per year (a flat ~$1,000/month).

Those platforms are built and priced for mega-syndicated deals with a bank's procurement behind them, and at that altitude the enterprise contract is the reality. But for a self-run infrastructure raise, per-page pricing punishes exactly the shape of your deal: a document-heavy raise (large model, technical reports, EPC contracts, full consents pack) with a growing counterparty list. The per-admin model breaks that link — 500 documents or 5,000, five funds or thirty, the bill is the same. For the full pricing-model comparison across the market, see the Virtual Data Room Cost Guide. The one number to remember: recipients are always free, which is what makes an institutional-grade room cost a rounding error against a raise.

Who sits across the table: infra funds, PE, family offices, and lenders — and what each reads first?

Four counterparty types read your room, and each opens it at a different folder. Building the room well means understanding what each one is actually looking for, because they are underwriting genuinely different questions from the same documents.

Infrastructure funds and private equity read for platform potential as much as the single asset. A specialist infra fund is often thinking beyond this one project — is this a sponsor and a site that could become a repeat platform, a pipeline, a fund-scale relationship? They read the model for the return and the sensitivities, the commercial folder for the demand story, and the governance terms for control and follow-on rights. The single asset has to hold up, but the upside they are pricing is frequently the platform.

Family offices are the counterparty most misunderstood, so here the numbers matter. The UBS Global Family Office Report 2025 (published 21 May 2025, surveying 317 family offices with an average of around US$1.1bn in assets under management and around US$2.7bn average net worth) puts infrastructure at just ~1% of strategic asset allocation — so do not overstate how much family-office money is already in infrastructure; the headline weight is small. What makes them relevant is direction and behaviour, not current weight: family offices deploy heavily through direct deals (direct private equity is a large share of the ~21% PE allocation in the same report), and a development JV — tangible, cash-yielding, inflation-linked — fits the direct, patient-capital appetite. (Allocation percentages are worth confirming against the report itself before you quote them onward.) A family office reads your room for power certainty, anchor-counterparty covenant, cost certainty, and downside — and often co-invests alongside a specialist developer rather than originating solo. The Family Offices solution page covers how that buy-side workflow runs.

Lenders read for cover ratios and the EPC wrap first, every time. Their return is fixed, so their entire discipline is downside: they go to the model's debt-service and loan-life coverage ratios, then to the contracts that protect them — the EPC wrap (is construction cost and delivery genuinely wrapped by a creditworthy contractor?), the grid agreement, the offtake. A lender will generally not commit construction financing until power is committed and major consents are secured, which is why the grid offer and planning pack are the fulcrum of the whole room. They read the corporate and legal folders for structure and security, but the coverage ratios and the EPC wrap are the first things they open.

The practical consequence: one room, four sightlines. Folder-level permissions let each class see what it needs — lenders deep in contracts and coverage, equity in the model and control terms, family offices across power and covenant — without any of them seeing each other. For the energy-asset-class specifics that sit underneath these reads, the Energy solution page carries the sector detail.

The sponsor's credibility problem

Here is the situation more infrastructure sponsors are in than anyone admits: a three-person developer raising £100M or more. The team is small, often pre-revenue, sometimes pre-first-deal, and the ask is enormous relative to the headcount. In that gap between the size of the team and the size of the raise, the room is the first work product a counterparty sees — and it carries a disproportionate share of the credibility the team hasn't yet earned through a track record.

This is not hypothetical; it is the shape of the market right now. Consider the archetypes (anonymised, and I'll keep them that way):

- A US GPU-cloud operator financing 30MW sites through SPVs — a lean, C-suite-led team raising off-balance-sheet capital against GPU clusters and data-centre capacity, whose entire pitch is that the SPV structure, the off-take contracts and the model hold together. The room is where the capital-markets rigour has to show.

- A UK data-centre developer preparing a gigawatt-scale JV raise — often an owner-operator with brand-new entities and no filed accounts, courting institutional infrastructure money against a grid position, land control and a masterplan. With no track record, the room is the credibility signal; institutional-grade controls matter disproportionately precisely because nothing else vouches for the team yet.

- A family office underwriting its first direct data-centre deal — on the buy-side of the same table, needing discretion, granular view-controls and a clean, IC-ready structure to organise diligence it is doing for the first time.

In every one of these, a small team is asking a large counterparty to take it seriously, and the room does that work. A numbered skeleton, a single current model, watermarked crown jewels, folder-level permissions and a logged Q&A thread say "this sponsor has run a process" before anyone has met the team. A flat folder dump says the opposite, and no amount of a good project survives a room that reads as amateur.

I run Peony, a data room company, and I'll be plain about where it fits and where it doesn't. Peony gives a small sponsor the controls a fund's IC expects — NDA gating, dynamic watermarks, folder-level permissions, page-level analytics, AI Q&A against a model you connect with zero retention, instant revocation and exportable audit logs — at $30-$52 per admin per month with every recipient free, which is why 5,900+ customers run controlled sharing on it without the bill scaling with the audience. The UK is Peony's second-largest market — 140+ customers across the UK and Europe — and the platform has held 99.96% uptime since August 2025 with a median setup time of 4 minutes 19 seconds, so a small team can stand up an institutional-looking room the afternoon it decides to raise. What Peony does not do is make your project bankable — that is your grid offer, your consents and your model. It makes the room that proves it bankable look like it was run by a team three times your size. For a three-person developer raising £100M against a promise, that is precisely the leverage the room exists to give. With 5,900+ customers behind it across M&A, fundraising and real assets, it is built for the sponsor who has to look institutional before they've had the chance to become it.

Frequently asked questions

We're raising JV equity + development debt for a 100MW project — which data room do infrastructure funds expect to see?

Funds care about room discipline far more than the logo on it. What an infrastructure fund's investment committee actually judges is whether the index is institutional: a clean top-level folder structure that mirrors the diligence workstreams, strict version control so nobody is reading last month's model, a real Q&A process instead of a scatter of emails, and permission hygiene that keeps counterparties from seeing each other. The VDRs they have seen most are the legacy enterprise ones — Datasite and Intralinks — because those have dominated large project finance for years. But a modern per-admin room is fully accepted when the index looks the part; funds are underwriting your project and your professionalism, not your software vendor. Institutional-looking, concretely, means: a numbered folder skeleton, a single current model behind a stable link, watermarked sensitive documents, folder-level permissions per counterparty class, and a logged Q&A thread. Get those right and the room reads as institutional regardless of brand.

We're a 20-person developer prepping a £50m raise — do I actually need a virtual data room, or is Google Drive enough?

For a raise of that size you need a real room, and here is the honest reason. A shared drive has no NDA gate, no per-viewer watermark, no folder-level permissions per counterparty, and no page-level analytics — so you cannot stop two competing funds from seeing each other, you cannot trace a leaked model, and you cannot tell who actually opened the grid offer. An infrastructure fund reading a Google Drive link also reads a signal: this sponsor has not run a process before. The room is the first work product a counterparty sees, and on a £50m project-finance raise it is doing real work — gating the crown-jewel documents, staging disclosure, and giving you engagement data to re-forecast the raise. A dedicated room does all of that, and on a per-admin plan it costs a rounding error against the raise. Google Drive is fine for internal drafting; it is the wrong tool for institutional diligence.

For our project-finance raise, how do iDeals, Datasite, Ansarada and Intralinks compare?

They are the incumbents, and they are genuinely strong for large syndicated deals. Datasite and Intralinks are the enterprise defaults — deal-team-scale tooling, AI suites, and the brand procurement teams expect on a £1bn+ raise — priced accordingly; site pricing canon puts Datasite around $68K on annual enterprise deals. iDeals sits in the mid-market at roughly $500 to $1,000 per month depending on scope, and Ansarada brings a deal-workflow and Q&A heritage. All four are per-page or per-user or per-project in shape, which is the thing to watch: a document-heavy infrastructure raise with a large model, technical reports and a growing counterparty list is exactly where per-page and per-user meters run up. For a sub-£1bn raise run by a small sponsor team, a per-admin room — you pay for internal admin seats, recipients are free — usually fits the shape better. The honest split: enterprise VDRs for the mega-syndicated deal, a per-admin room for the mid-market raise where the meter, not the feature list, is the deciding factor.

We're a small infra sponsor — what's the cheapest institutional-grade data room versus an enterprise VDR like Datasite?

The cheapest institutional-grade option is a per-admin room, and the gap versus an enterprise VDR is large. Peony's Data Room plan is $52 per admin per month (Business is $30), and recipients — every fund, lender and adviser you invite — are always free. Run a 3-to-6-month raise with two to four admins and your total is in the low hundreds of dollars. Compare that with enterprise contracts that land in the $15K to $68K range: Datasite around $68K on annual enterprise deals, DealRoom around $12K a year, iDeals roughly $500 to $1,000 a month. What you give up at the low end is not the diligence-grade controls — watermarking, folder-level permissions, page analytics, NDA gating, audit logs are all there — it is the deal-team-scale AI suite and the enterprise procurement footprint that a mega-deal needs. For a small sponsor on a sub-£1bn raise, institutional-grade and cheap are not in tension; the per-admin model is how you get both.

We're structuring an infrastructure project-finance raise — how should I structure the data room and how many top-level folders should it have?

Use a numbered skeleton of roughly ten to twelve top-level folders, sequenced so the kill-question documents come first. A working structure: 01 Corporate & structure (the SPV/HoldCo chart), 02 Land & real estate (options, title, surveys), 03 Consents & planning (permissions, s.106/CIL or the local equivalent, environmental), 04 Grid & utilities (the connection offer or agreement — the crown jewel for energy-adjacent assets — plus water and fibre), 05 Power strategy (PPA and hedging), 06 Technical (feasibility, design basis, EPC or D&B contracts, programme), 07 Commercial (offtake, pre-lets, LOIs, market studies), 08 Financial model & assumptions, 09 ESG & sustainability, 10 Insurance, 11 Legal & disputes, and 12 Q&A. The number matters less than the sequencing logic: an infrastructure fund does not read front to back, it goes straight to the four things that can kill the deal — grid, planning, land control and model integrity — so those folders sit at the top where they are found in one click. Numbered folders also keep the index stable as you add documents, so a returning reviewer never has to relearn the room.

Our equity and debt counterparties need different views — how do I give lenders and equity investors different access in one data room?

You run one room with folder-level permission groups, one group per counterparty class, and attach only the folders each class needs. Lenders and equity are underwriting different questions: a lender wants the contracts and the cover ratios — the grid agreement, the EPC wrap, the offtake, the model's debt-service coverage — while equity wants the upside and the control terms — the return sensitivities, the platform potential, the shareholders' agreement. So the debt group sees the contract and model folders in full; the equity group sees the model and commercial folders plus the governance terms; neither sees the other's correspondence, and no counterparty sees a competing counterparty. Sensitive items — the full model, the grid documents — can stay staged behind a later unlock even within an approved group. The mechanism is visitor groups plus folder-level permissions, and because recipients are free you can give ten funds and four lenders their own isolated views without the bill moving. One room, many sightlines, each mapped to what that party actually reads.

Investors keep asking us for documents by email instead of using the data room — how do we run Q&A without email chaos?

The fix is to make the room the only channel and give it a real Q&A process. When investors email you for documents, it is usually because the room is hard to navigate or the answer is not obviously in it — so first, tighten the index so the kill-question documents are one click from the front, then route every question through a logged Q&A folder or thread rather than your inbox. That gives you one place where a question, its answer, and any document released in response all live together, visible to the counterparty who asked and auditable later. It also stops the same question being answered three different ways to three different funds. Page-level analytics close the loop: if a fund is emailing you instead of opening the model, the analytics tell you they never got past the teaser, which is a process conversation, not a document one. The discipline — everything in the room, Q&A logged, no side-channel — is exactly what an institutional counterparty expects to see, and it is what separates a run process from a scramble.

We're a small development team — how do we make our data room look institutional to infrastructure funds and control who sees the financial model?

Institutional is a function of discipline, not headcount, and the model is the document you stage most carefully. To look institutional: build the numbered folder skeleton, keep a single current model behind a stable link so version control is visible, watermark the sensitive documents, run Q&A through a logged thread, and set folder-level permissions per counterparty so nobody sees anyone else. That is what a fund's IC reads as a run process, and a three-person team that does it looks as credible as a fifty-person one that does not. For the model specifically, you control who sees it with a staged unlock: the teaser and headline metrics are open to an approved group, but the full model with its assumptions sits behind a later release, watermarked to each viewer, so it only opens once a counterparty is genuinely progressing. Page-level analytics then tell you who opened the model and how long they spent in it — the clearest signal you have of which fund is real. Control plus visibility is the whole game.

For a 3-6 month infrastructure raise, how much does a virtual data room cost?

On a per-admin plan, a full raise costs in the low hundreds of dollars — a fraction of a legacy per-page or per-GB quote. Peony is priced per admin seat: Business is $30 per admin per month and the Data Room plan, which adds dynamic watermarking and unlimited rooms, is $52 per admin per month, both on annual billing. A typical 3-to-6-month raise runs with two to four admins, and every recipient — every fund, lender and adviser — is free, so your total is bounded by your own small team, not by how many counterparties or how many gigabytes you load. That is the structural difference from enterprise VDRs, which quote per page, per GB, or per project and land in the $15K to $68K range: Datasite around $68K on annual enterprise deals, iDeals roughly $500 to $1,000 a month, DealRoom around $12K a year. Those are built and priced for mega-syndicated deals. For a sub-£1bn infrastructure raise, per-admin plus free recipients is what makes an institutional-grade room cost a rounding error against the transaction.

We're weighing pricing models for a document-heavy £20m-£1bn raise — flat-fee or per-page, and is per-page worth it?

For a document-heavy raise, per-page is the model that punishes you and per-admin flat pricing is the one that does not. Per-page and per-GB pricing was designed for an era when the meter matched the work; the problem is that an infrastructure raise is precisely the document-heavy case — a large financial model, technical and feasibility reports, EPC contracts, a full consents pack — so the page and storage counts run up fast, and a big counterparty list multiplies the exposure if you are also paying per user. A per-admin flat model breaks that link entirely: you pay for your internal admin seats, recipients are free, and it does not matter whether you load 500 documents or 5,000, or invite five funds or thirty. So is per-page worth it? For a mega-syndicated deal with a bank's procurement behind it, the enterprise VDR is the reality. For a self-run £20m-to-£1bn raise, per-page is rarely worth it — the flat per-admin model is both cheaper and more predictable, which is what you want when the raise, not the room, is the thing you are trying to manage.

We're organising grid-connection, planning, land and EPC contracts plus the financial model — how do I lay these out in the data room?

Give each its own numbered top-level folder and order them by how likely they are to kill the deal. Grid connection is the crown jewel for any energy-adjacent asset, so 04 Grid & utilities holds the connection offer or agreement — read for firm versus indicative status, capacity in MW/MVA, connection date and milestones — alongside water and fibre. Planning sits in 03 Consents & planning: the permission or its status, s.106/CIL or local-equivalent obligations, and the environmental statement. Land control lives in 02 Land & real estate: option agreements, title, surveys, and the percentage of the site actually under control. The EPC or design-and-build contract belongs in 06 Technical with the feasibility work, design basis and programme. And 08 Financial model & assumptions holds a single current model behind a stable link, with its assumptions alongside so a reviewer can test it. The four an IC checks first — grid status, planning status, land-control percentage, and model integrity — should each be one click from the front of the room. Everything else can sit deeper; those four cannot.

Related resources

- Data Center Data Room — the operating-asset acquisition case, organised around energisation risk

- Renewable Energy Data Room — the solar, wind and battery-storage project room with ITC/PTC and interconnection specifics

- UK Data Centre Due Diligence — the UK development-diligence detail: NESO grid queue, NSIP/DCO, planning

- Data Room Security Questionnaire — how to answer the residency, hosting and security questions a counterparty asks

- Commercial Property Due Diligence — the underlying property process, contingency clock and re-trade dynamics

- Virtual Data Room Cost Guide — how VDR pricing models compare across the market

- Data Centers solution — the digital-infrastructure solution page

- Energy solution — the energy and renewables solution page

- Family Offices solution — the buy-side direct-investment workflow

- Page Analytics — see which fund opened the model and which never got past the teaser

- Smart Q&A — run investor Q&A in the room instead of your inbox

- Visitor Groups — folder-level permissions per counterparty class

You might also like

May 6, 2026

Oil and Gas Data Room Checklist: What Goes in (42 Docs, 2026)

Jul 16, 2026

7 Best M&A Advisors in Raleigh-Durham for $5M–$500M Deals (2026)

Jul 16, 2026

UK Data Centre Due Diligence: The Grid-First Guide for Developers and Investors (2026)