7 Best M&A Advisors in Raleigh-Durham for $5M–$500M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: July 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. Before Peony I ran M&A deals as a banker at Nomura and invested at Target Global and Backed VC, so I have sat on both sides of the table — and now, on the document side, I watch hundreds of deals a year move through our platform, from founder-led exits and family-business successions to PE recapitalizations and strategic carve-outs. Raleigh-Durham is the entry in our M&A advisor series where the metro's defining fact is not a homegrown bank it kept or sold, but the kind of company it produces: the Research Triangle is a university deal engine, and the exits it mints are so specialized that the advice leaves town. Most "best Raleigh M&A advisors" pages fail a simple test — they either pad a list with wealth managers and banks that do not run sell-side processes, or they imply a deep local investment-banking bench that does not exist. The honest picture is more useful, and more flattering to the few real local players: a thin, knowable bench, one genuine Raleigh-rooted national specialist, and a set of sector experts who fly in. At Peony we now serve more than 5,900 customers, and the Triangle sits squarely in the sub-$500M enterprise-value band that makes up the bulk of the deals we see in our state-of-the-market benchmark.

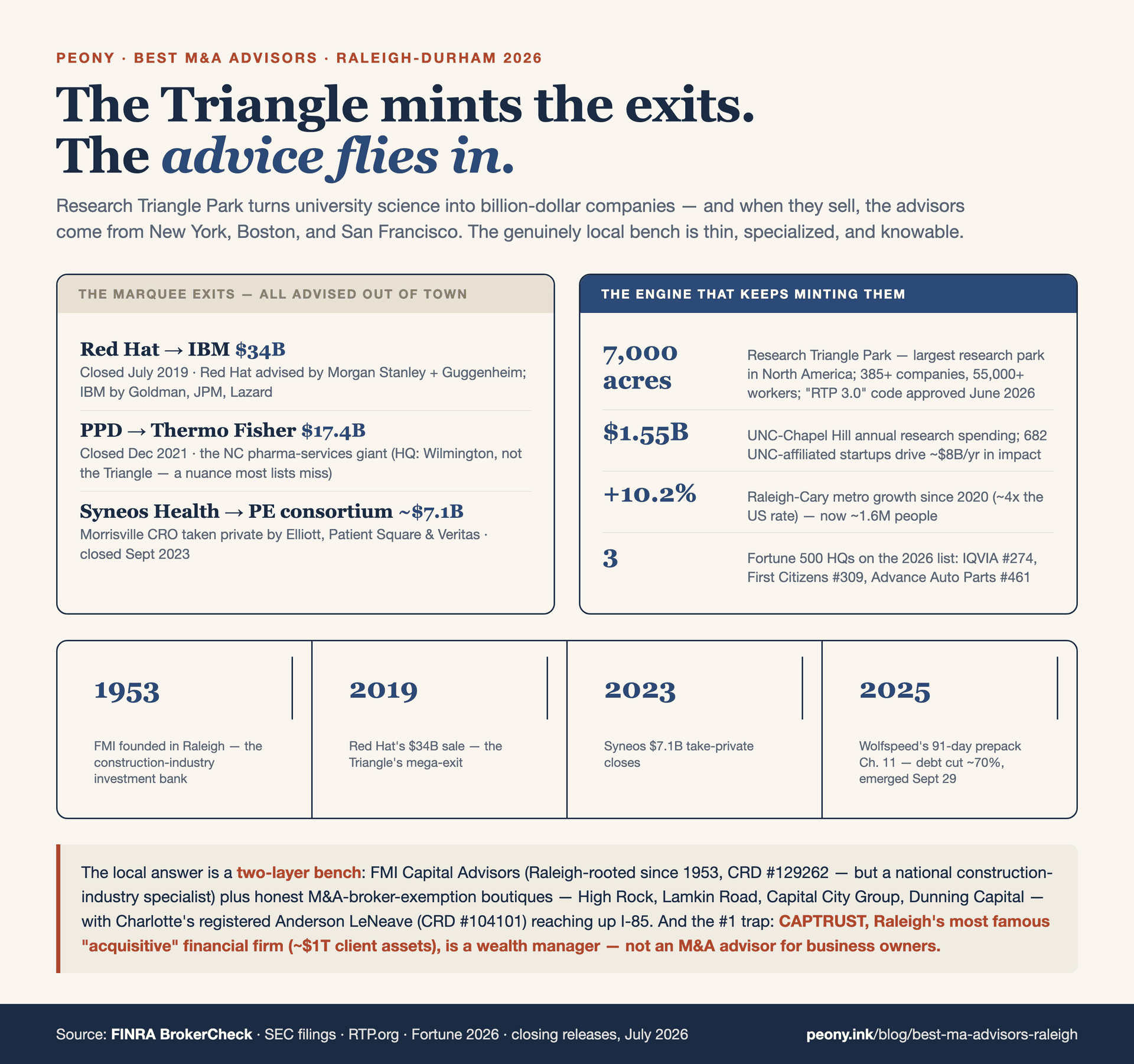

Here is the thesis I want you to internalize before you read another word: the Triangle mints science and software exits out of the Duke, UNC, and NC State research complex, but the marquee deals leave town for the advice. Red Hat sold to IBM for $34B (closed July 2019), advised by Morgan Stanley and Guggenheim — not by anyone in Raleigh. PPD sold to Thermo Fisher for $17.4B in 2021 (and PPD is really a Wilmington company, on the coast). Syneos Health of Morrisville sold to an Elliott/Patient Square/Veritas consortium for about $7.1B in 2023. None of those were local mandates, and none could have been — deals at that scale and specialization go to bulge-bracket banks and dedicated sector franchises, wherever they sit.

That single fact reorganizes the whole advisor decision here, and it comes with a counterintuitive payoff for the persona I wrote this for: a PhD scientist-founder with a ~$22M-revenue bioanalytical lab, weighing an unsolicited approach from a PE-backed consolidator. Unlike Richmond, which built its own dedicated mid-market flagship in Harris Williams, or Milwaukee, which kept a homegrown national bank in Robert W. Baird, Raleigh's bench is thin precisely because its exits are so specialized that the specialists fly in — the fluency-over-address rule at maximum strength. This post is the working playbook I would hand to that founder. The frames come from cross-referencing FINRA BrokerCheck, the firms' own disclosures, and the verified 2025-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in Raleigh-Durham right now for $5M-$500M deals?

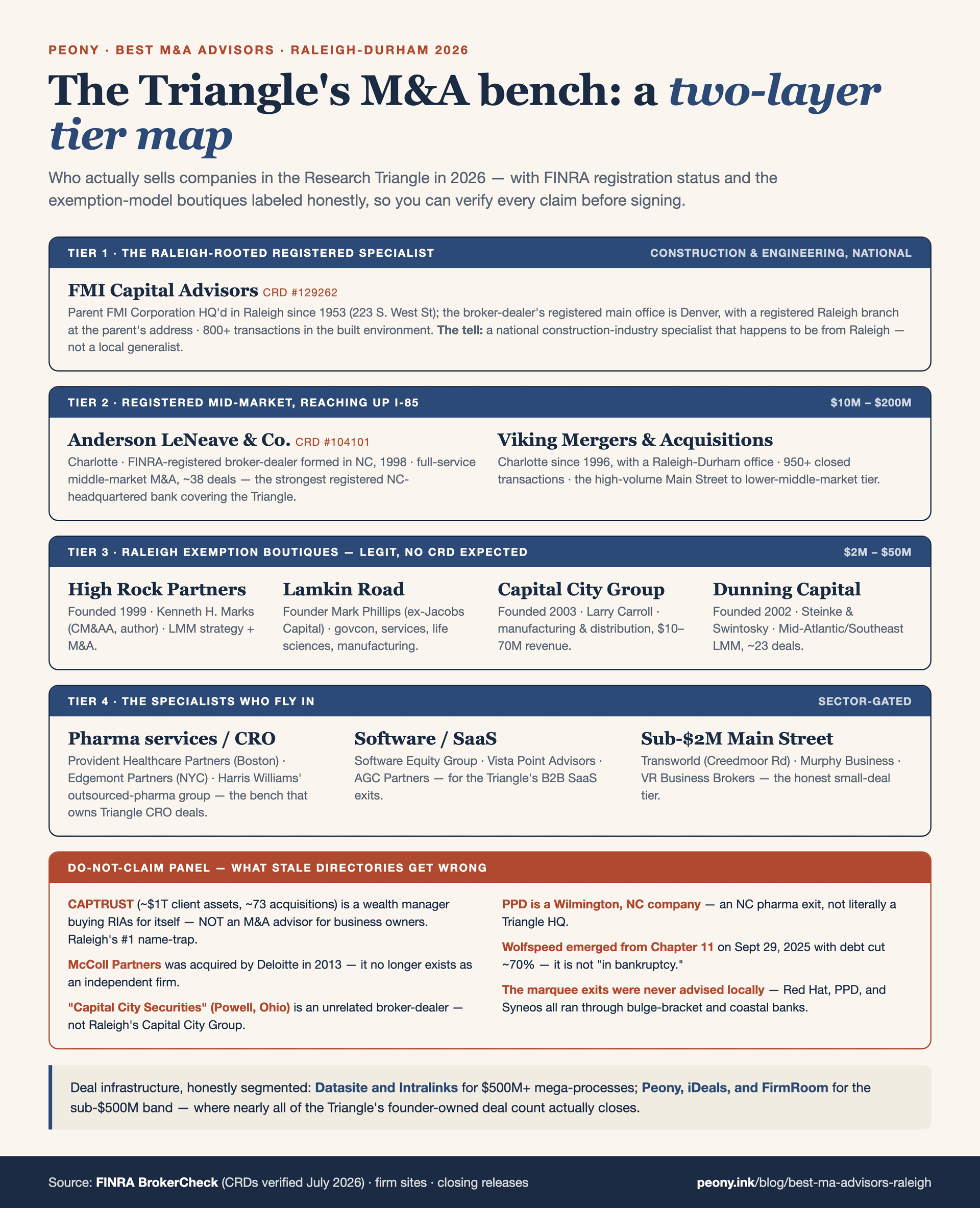

The best M&A advisor in the Triangle depends on your deal's size and sector, and the honest segmented answer is the whole point of this page. For a construction, engineering, or built-environment company, the standout is FMI Capital Advisors (CRD #129262) — a national specialist whose parent is Raleigh-headquartered, the one genuine Triangle-rooted investment bank. For a pharma-services, CRO, or bioanalytical-lab company — the Triangle's signature export — the best advisors are the sector specialists who fly in: Provident Healthcare Partners, Edgemont Partners, and Harris Williams' Outsourced Pharma Services group. For a software or SaaS company, the specialist banks are Software Equity Group, Vista Point Advisors, and AGC Partners. For a general lower-middle-market manufacturer, business-services company, or government contractor, the local M&A-broker-exemption boutiques — High Rock Partners, Lamkin Road, Capital City Group, and Dunning Capital — run true sell-side processes. And when you want a registered NC-headquartered mid-market bank, Charlotte's Anderson LeNeave & Co. (CRD #104101) reaches up I-85. The one name to be careful with: CAPTRUST (CRD-registered, but as a wealth manager) manages roughly $1 trillion of client assets and is famously acquisitive — but it buys RIAs for itself; it is not a sell-side M&A advisor for a business owner.

Here is the 2026 shortlist, sorted by tier and deal-size band. The verification wrinkle in the Triangle is different from most cities: the trap is not a graveyard of dead firms so much as a wealth-management giant miscataloged as an advisor, a construction specialist mistaken for a local generalist, and a set of name collisions that send you to the wrong company.

| Firm | HQ / Triangle presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| FMI Capital Advisors ★ | Parent FMI Corporation, 223 S. West St, Raleigh (since 1953); Denver-registered BD, registered Raleigh branch | $10M-$300M+ EV, sector-specific | Construction, engineering, built environment (800+ transactions); sell-side, buy-side, ESOP, valuations | Registered broker-dealer (CRD #129262) |

| High Rock Partners | Raleigh (founded 1999) | $5M-$75M EV | Lower-middle-market strategy + M&A; founder Kenneth H. Marks (CM&AA, author) | M&A advisor (non-registered; M&A-broker exemption) |

| Lamkin Road | Raleigh | $5M-$100M EV | Business services, govcon, healthcare/life sciences, manufacturing, technology | M&A advisor (non-registered; M&A-broker exemption) |

| Capital City Group | Raleigh (founded 2003) | $10M-$70M revenue | Manufacturing, wholesale distribution ($1M+ EBITDA); founder Larry Carroll | M&A advisor (non-registered; M&A-broker exemption) |

| Dunning Capital | Raleigh (founded 2002) | $5M-$75M EV | Mid-Atlantic/Southeast LMM; manufacturing, consumer, healthcare, IT | M&A advisor (non-registered; M&A-broker exemption) |

| Anderson LeNeave & Co. | Charlotte (formed in NC Aug 4, 1998) — reaches up I-85 | $25M-$250M EV | Full-service middle-market M&A (~38 deals) | Registered broker-dealer (CRD #104101) |

| Viking Mergers & Acquisitions | Charlotte (since 1996); Raleigh/Durham office | $1M-$25M EV | Main Street to lower-LMM (950+ deals) | M&A advisor / business brokerage (see body) |

| Fly-in sector specialists | Boston / New York / San Francisco — no Triangle office | $25M-$500M+ EV, sector-specific | Pharma services & CROs (Provident, Edgemont, Harris Williams OPS); software (SEG, Vista Point, AGC) | Established FINRA broker-dealers |

A few notes the table cannot carry. FMI Capital Advisors is the reason this page has a genuine local anchor at all: its parent, FMI Corporation, has been headquartered at 223 S. West St in Raleigh since 1953, and the broker-dealer subsidiary (CRD #129262) maintains a registered Raleigh branch at that address even though its main registered office is in Denver. But hold the nuance precisely — Raleigh-headquartered parent, Denver-registered broker-dealer, registered Raleigh branch, and a construction-industry specialist, not a local generalist. FMI will run a superb sell-side for an engineering or built-environment company anywhere in the country; it is not the firm that sells your bioanalytical lab.

High Rock Partners, Lamkin Road, Capital City Group, and Dunning Capital are the honest lower-middle-market bench — legitimate Raleigh boutiques that operate under the federal M&A-broker exemption rather than holding their own broker-dealer registration. Anderson LeNeave & Co. (CRD #104101) is the strongest registered NC-headquartered mid-market bank in the coverage set, reaching the Triangle from Charlotte down I-85, and Viking Mergers & Acquisitions covers the Main Street and lower-lower-middle-market band from a Raleigh/Durham office. Above all of them, for the science and software exits that define this metro, sit the specialists who fly in — because in a concentrated vertical the specialist's buyer list beats any local address.

And the critical honesty point on the name a Triangle owner is most likely to encounter and misread: CAPTRUST is a wealth manager, not an M&A advisor. More on the sorting test below.

Why is the Research Triangle a "university deal engine"?

Every metro in this series has a structural signature. Richmond is the Wall Street of the South that sold its banks and rebuilt itself as a mid-market M&A capital. Milwaukee is the city that kept its investment bank when it sold its commercial bank. Columbus is the capital where the money flew in and no homegrown bank ever scaled. Raleigh-Durham's signature is different from all of them: it is a university deal engine — a metro whose defining economic output is science and technology companies spun out of a world-class research complex, whose most valuable exits are therefore highly specialized, and whose advisory needs are met by specialists who fly in rather than by a deep homegrown bank.

The engine is real and measurable. Three research universities — Duke, the University of North Carolina at Chapel Hill, and NC State — anchor the region; UNC's research spending alone topped $1.55B, and per a TEConomy analysis, 87% of North Carolina's in-state R&D concentrates in UNC, Duke, and NC State. UNC counts 682 affiliated startups generating roughly $8B a year of economic impact. At the center sits Research Triangle Park — 7,000 acres, 385-plus companies, 55,000-plus workers, the largest research park in North America — and the region just approved a "RTP 3.0" development code in June 2026 to redevelop it for a denser, mixed-use future. The biotech capital keeps flowing: roughly $4B of North Carolina life-sciences investment in 2025, Durham's Hatteras Venture Partners closing $200M-plus across two funds, Novartis committing $771M to a Durham/Wake expansion, and Genentech committing $700M to Holly Springs. This is a metro built to produce IQVIA, Red Hat, PPD, Syneos, SAS, and Epic Games — not one built to produce investment banks.

That distinction is the whole point. A metro that mints Red Hats and PPDs produces exits that are (a) large and (b) so sector-specific that only a dedicated franchise can value and sell them well. So the marquee deals do not just happen to leave town — they must, because a $34B software-infrastructure sale or a $17B CRO sale belongs to the handful of banks in the world that run those processes. Red Hat's sale to IBM was advised by Morgan Stanley and Guggenheim. PPD's sale to Thermo Fisher and Syneos's sale to its PE consortium were bulge-bracket-and-specialist affairs. None of that reflects any deficiency in Raleigh; it reflects the physics of specialization.

What does that mean for you, a founder selling a $5M-$500M company? Three things. First, the local-versus-national question is really a generalist-versus-specialist question, and for a science or software company the specialist wins even when it flies in — because sector fluency, not geography, sets your price. Second, the genuine local bench is thin but knowable — one construction-industry national specialist (FMI), a handful of exemption boutiques for general lower-middle-market deals, and a registered NC bank reaching in from Charlotte. Third, and this is the honest counter you must hold alongside the thesis: the metro's headline companies are not your comps or your advisors. SAS is private and not for sale; Epic Games is private and controlled; the Fortune 500 names here are a bank holding company and a retailer mid-turnaround. The university deal engine is a genuine advantage — it means real strategic and PE demand for Triangle science and tech assets — but it is an advantage of buyer interest, not of a deep local advisory bench.

Are there any real M&A advisors based in Raleigh-Durham?

Yes, but the bench is thin and specialized — and the most useful thing I can do is name exactly who is genuinely local, who reaches in, and who flies in, rather than pad a list to look deep. This is the question the persona for this page asks first and most often, so let me answer it precisely.

The one genuine Triangle-rooted investment bank is FMI Capital Advisors (CRD #129262). Its parent, FMI Corporation, has been headquartered in Raleigh since 1953, and the broker-dealer subsidiary keeps a registered Raleigh branch — but it is a national construction, engineering, and built-environment specialist, not a local generalist. If you are in the built environment, it may be the best advisor for you in the country and it happens to be down the street. If you are not, it is a landmark, not an option.

The genuine local lower-middle-market bench is a short list of exemption boutiques: High Rock Partners (founded 1999 by Kenneth H. Marks, who holds the CM&AA credential and has written on middle-market M&A), Lamkin Road (led by Mark Phillips, formerly of Jacobs Capital, with a team that includes ex-Baird government and defense M&A talent), Capital City Group (founded 2003 by Larry Carroll, focused on manufacturing and wholesale distribution), and Dunning Capital (founded 2002, principals Paul Steinke and David Swintosky, covering the Mid-Atlantic and Southeast lower middle market). These are legitimate, focused firms that run true sell-side processes for general manufacturers, business-services companies, and government contractors in the roughly $5M-$100M range. What they are not is registered broker-dealers — they operate under the federal M&A-broker exemption, which is a normal and appropriate model I explain in its own section below.

The registered NC bank reaching in is Anderson LeNeave & Co. (CRD #104101), a Charlotte full-service middle-market broker-dealer formed in North Carolina in 1998 — the strongest registered NC-headquartered mid-market option in the coverage set, and a natural call for a Triangle seller who wants a registered bank with a genuine NC footprint. Viking Mergers & Acquisitions covers the smaller end (Main Street to lower-lower-middle-market) from a Raleigh/Durham office.

And the specialists fly in. For the pharma-services, CRO, and lab exits the Triangle is famous for, the best advisors are dedicated sector banks — Provident Healthcare Partners, Edgemont Partners, and Harris Williams' Outsourced Pharma Services group — headquartered elsewhere. For software and SaaS, it is Software Equity Group, Vista Point Advisors, and AGC Partners. That is not a gap in the local market; it is the correct answer for a specialized business.

So the honest, complete answer to "are there any real M&A advisors here" is: yes — one local national specialist, a handful of local exemption boutiques for general LMM deals, a registered NC bank reaching in from Charlotte, and the sector specialists who fly in for the science and software exits. Thin, but knowable — and, for most sellers, sufficient once you match the firm to the deal.

Should I hire a local Triangle advisor or an out-of-town pharma-services specialist to sell my CRO-adjacent business?

For a CRO-adjacent, pharma-services, or bioanalytical-lab business, hire the sector specialist even if it flies in — and be clear-eyed that this is the one metro in the series where "go local" is most often the wrong instinct. The reason is sector fluency, not geography: the Triangle's science exits are so specialized that a generalist, however local and however competent, simply cannot match a dedicated pharma-services banker who already knows the strategic consolidators and the PE platforms rolling up labs and CROs, and who has probably sold to several of them before.

Reach for an out-of-town pharma-services specialist — Provident Healthcare Partners (Boston), Edgemont Partners (New York), or Harris Williams' Outsourced Pharma Services group — when your company is the science: a bioanalytical lab, a CRO or CRO-adjacent services business, a specialty pharma-services platform. These firms live in the vertical (Provident publishes quarterly CRO M&A updates), speak the language of backlog and book-to-bill and GLP compliance, and carry the buyer relationships that manufacture competitive tension among the exact acquirers who will pay a premium for your capabilities. Category names like Cain Brothers (now part of KeyBanc), Ziegler, and Capstone round out the healthcare specialist landscape. The plane ticket is irrelevant next to the buyer list.

Reach for a local Triangle boutique — High Rock Partners, Lamkin Road, Capital City Group, or Dunning Capital — when your business is more general than science: a manufacturer, a business-services company, a government contractor, a distributor. There the buyer universe is broader, a good generalist can run a full competitive process, and senior local attention is worth real money. Lamkin Road in particular spans healthcare and life sciences alongside govcon and manufacturing, so for a services-heavy life-sciences company (rather than a deeply technical lab) it is worth a conversation. And if you want a registered NC bank, Anderson LeNeave & Co. (CRD #104101) reaches the Triangle from Charlotte.

The honest nuances that decide close calls: (1) specialization scales with technical depth — the more your value lives in GLP-validated methods, regulatory standing, and scientific differentiation, the more the specialist's fluency matters; a broad services business tilts back toward a capable generalist. (2) The test is identical for local and fly-in — named senior staffing, three named recent closings in your exact sub-sector, and the buyers on the other side. Run your best local option and your best specialist through the same screen and let the answers decide. (3) Distance is not the cost you think it is — video diligence, data rooms, and travel make a Boston banker as reachable as a Raleigh one; the real cost is hiring someone who has to learn your buyer map on your clock. For the national view of the category, our best healthcare M&A advisors guide maps the specialist landscape. Price comes from competitive tension and sector fluency, not from the zip code on the engagement letter.

How are bioanalytical labs and pharma-services companies valued — backlog, book-to-bill, and GLP compliance?

Bioanalytical labs and pharma-services companies are valued primarily on a multiple of normalized EBITDA, but the multiple itself is set by a sector-specific fluency test that a generalist can fail — and failing it costs you real money. This is the persona's core anxiety, and it is well founded: a science business is not valued like a widget maker, and the advisor who does not know the drivers will let a buyer chip your price down.

Start with normalized EBITDA. A buyer takes your trailing and forward EBITDA and normalizes it — adding back owner compensation, one-time costs, and non-recurring items — with one sector-specific wrinkle that trips up generalists: in CRO and lab models, pass-through costs (reimbursed investigator fees, third-party expenses) can distort both revenue and margin, so they must be stripped out to see true service EBITDA. Miss that and your margins look wrong in either direction.

Then the multiple, which is driven by a handful of science-business metrics:

- Backlog. Contracted-but-unrecognized revenue is the single most scrutinized asset in a services-science business. Buyers want to see its size, its composition (which sponsors, which studies), and its quality (how cancellable, how likely to convert). A deep, high-quality backlog supports a premium; a thin or concentrated one invites a discount.

- Book-to-bill. New bookings divided by revenue over a period; above 1.0 signals a growing order book, below 1.0 a shrinking one. Yours near 1.1 is a genuine selling point — but only if your banker knows to lead with it and defend how it is calculated.

- Revenue quality and concentration. Recurring and contracted revenue beats one-off projects; a diversified sponsor base beats client concentration (a single sponsor at 40% of revenue is a discount you will have to argue against).

- The regulatory and quality layer. GLP status, FDA inspection history (Form 483 observations and, critically, how you resolved them), data-integrity practices, and accreditations gate the whole valuation. A clean inspection record is worth defending as a premium driver; unresolved findings are a live discount a specialist buyer will press.

On the number itself: your hoped-for 8-11x is not unreasonable for a well-run, growing lab with clean compliance and durable backlog — but I am deliberately not publishing a precise multiple range as though it were a fact for your business, because pharma-services multiples vary widely by sub-sector, scale, and growth, and false precision would mislead you. A specialist banker with current comps will give you a defensible range for your exact profile. The durable truth is that the valuation is won or lost on how well your backlog, book-to-bill, and compliance record are documented and defended — which makes it a preparation problem before it is a negotiation problem. When you interview advisors, ask each one to walk you through how they would value your backlog, normalize your book-to-bill, and defend your GLP record; the fluency of the answer tells you whether you are talking to a specialist or a generalist. And build the data room around exactly those drivers, so a buyer confirms your story quickly instead of discounting the parts it cannot verify.

A PE-backed consolidator approached me unsolicited — do I still need an advisor?

Yes — and counterintuitively, an unsolicited approach from a PE-backed consolidator is the moment you most need one. A consolidator that contacts a founder directly is trying to buy the company without competition, which is entirely rational for the buyer and potentially expensive for you. These firms roll up fragmented sectors — labs, CROs, home services, SaaS — for a living; approaching founders bilaterally is their standard playbook precisely because it avoids an auction. Without a competing bid you have no leverage on price or terms, and a first-time seller rarely knows whether the offered multiple is generous or a lowball dressed up as a compliment ("we love the science, let's move fast, exclusively"). The flattery is real; so is the incentive to buy you cheap.

An M&A advisor's job is to convert that single inbound into a competitive process. The advisor runs a curated set of other credible strategics and sponsors against the party that called — under NDA, from a blind teaser, so your identity stays protected — and lets price be set by the market rather than by the one buyer at the table. That competitive tension typically moves the outcome by far more than the advisor's fee: on a lower-middle-market deal, the delta between a bilateral first offer and a competitively bid price is routinely a meaningful fraction of enterprise value, while the advisor's success fee is low-single-digit percent. The math favors the process.

An advisor also protects you on the things a first-time seller cannot see coming and a repeat buyer uses routinely: the structure of the LOI, the earnout and equity-rollover mechanics (a consolidator often wants you to roll meaningful equity into its platform — a decision with its own valuation and governance consequences), the exclusivity and no-shop provisions that, once signed, hand the buyer leverage to re-trade the price during diligence, and the confirmatory-diligence gauntlet itself. In the Triangle, a local boutique (High Rock, Lamkin Road, Dunning Capital) can run this play for a general business, and a pharma-services specialist should run it for a science company.

One honest caveat: if the unsolicited offer is genuinely extraordinary, the buyer is uniquely strategic, and you have independent reason to trust the number, a full auction is not always mandatory. But even then, an advisor — or at minimum a strong deal attorney — should pressure-test the offer and the terms before you sign exclusivity. The default should be a process; the exception should be deliberate, not accidental. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects you — staged disclosure through a permissioned room — is identical whether one buyer called or ten did.

Is the first unsolicited PE offer usually too low?

More often than not, yes — a single unsolicited offer is a starting point, not a fair price, and treating it as the ceiling is the most common way founders in this position leave money on the table. Price on a private company is not a fixed number; it is whatever a motivated buyer will pay when they know another motivated buyer is in the room. A PE-backed consolidator that reached out did so precisely because it hopes to transact bilaterally, without that pressure — and it has every incentive to anchor you low while the offer still feels like validation of your life's work.

A tight, confidential process against a curated short list does three things at once:

- It tests the offer against real alternatives. You learn what the market actually thinks your company is worth, rather than accepting one buyer's self-interested estimate.

- It moves price and terms in your favor. Competitive tension is the single most powerful lever in M&A — buyers bid more, and concede more on terms, when they know they can lose the deal.

- It disciplines the original buyer. The firm that called now knows it cannot slow-walk diligence or re-trade the price after signing without risking the whole deal to a competitor.

The objection founders raise — especially in a small industry — is confidentiality: "I don't want the whole Triangle to know I'm for sale." That is a legitimate concern and a fully solvable one, and I treat it at length in the next section. The short version: a good advisor markets from a blind teaser under NDA and stages disclosure through a permissioned data room, so only serious, vetted buyers ever learn your identity, and even they see sensitive material only in the final wave. You are not choosing between "run a process" and "stay confidential"; a well-run process is confidential by construction.

Weigh the costs honestly. Running a process costs you a few months and a success fee; not running one often costs a materially lower price and weaker terms — a far larger number on a deal in your range. The only real exception is a genuinely exceptional bilateral offer you have independently pressure-tested, and even then you should get an advisor's read before signing exclusivity. I run Peony, a data room company used by 5,900+ customers, built for exactly this kind of staged, confidential release.

How do I sell confidentially when everyone at RTP knows everyone?

You keep it confidential with staged disclosure enforced by a permissioned data room: a blind teaser first, the named CIM only after a signed NDA, and the most sensitive material held back for a small short list of serious, later-stage bidders. This discipline bites harder in the Research Triangle than in almost any market, because the science and technology community here is genuinely small and interconnected — your competitors, your largest sponsors, your principal investigators, and the PE firms circling your sector may all know each other, sit on the same boards, and see each other at the same conferences and RTP events. A leak that you are "for sale" can spook a sponsor mid-study, embolden a competitor to poach your key scientists, or unsettle staff — all before you have a signed deal. Confidentiality here is not paranoia; it is process discipline.

The structural defenses, which a good advisor runs as a matter of course:

- A blind teaser first. The initial one- or two-page document describes the business — sector, size, financial profile, capabilities, investment highlights — without naming it, so a recipient (including a competitor who happens to receive it) cannot identify you from the teaser alone.

- The named CIM only after an NDA. The full confidential information memorandum, which names your company and discloses real detail, goes only to buyers who have signed a non-disclosure agreement — and your advisor curates that list to exclude the parties most likely to misuse it.

- Crown-jewel material held for the short list. Client and sponsor names, specific pricing, validated methods and proprietary protocols, key-scientist rosters, and detailed contracts are released only to a small set of serious, late-stage bidders — never in the first wave.

The tooling has to enforce all of that, which is where the document side I work on comes in. Dynamic watermarking stamps each viewer's identity across every page, so a leaked document is traceable to its source and buyers know it. An NDA gate blocks access to the CIM until the agreement is signed. Page-level analytics show exactly who opened what and when — so if a rumor starts, you have a record of who had access. And per-buyer permissions let you stage strategics and financial buyers as separate groups seeing different tiers in one secure room. In a community this interconnected, remember the rule that governs the whole series: your buyer list is often also your competitor list. Treat every disclosure as if it might reach a rival, because at RTP it plausibly could. I run Peony, a data room company used by 5,900+ customers, precisely to make this staged, watermarked, permissioned release the default rather than a scramble.

What's the difference between a business broker and an M&A advisor for a $22M company?

A business broker lists smaller, owner-operated businesses to a pool weighted toward individual buyers on a listing-and-commission model; an M&A advisor or investment bank runs a confidential, competitive, curated process for a middle-market company, marketing to strategic acquirers and private-equity firms and manufacturing tension among them. For a $22M-revenue company with roughly $4.5M of EBITDA, you are squarely in M&A-advisor territory, not business-brokerage territory — and getting this distinction right is the difference between a clean competitive exit and leaving money on the table.

The practical differences that matter for a Triangle seller:

- How your company is marketed. A broker often posts a semi-public or public listing that anyone can browse; an M&A advisor markets from a blind teaser under NDA and does not name your company until a buyer is vetted and committed. For a science-company founder terrified of sponsors and competitors finding out, that difference alone is decisive.

- Who the buyer is. A broker's buyer is usually an individual, an owner-operator, or a small local acquirer; an M&A advisor's buyer is an institution — a strategic consolidator in your sector or a PE platform — that pays on multiples of EBITDA and can move on a deal in your range.

- How the fee works. A broker typically charges a flat commission on a listing; an M&A advisor charges a monthly retainer plus a success fee scaled to the deal (see the fee section below).

- What "the process" even means. A broker matches a willing buyer to a willing seller; an advisor engineers competition — running multiple credible buyers against each other to move price and terms.

In the Triangle, genuine business brokers — Transworld Business Advisors (4509 Creedmoor Rd, Raleigh), Murphy Business, and VR Business Brokers — are the right fit below roughly $2M of enterprise value. A science company with $4.5M of real EBITDA has long outgrown that model; your best buyers are institutions that will never see a broker's listing, and reaching them confidentially is the entire job. For the full taxonomy — advisor vs. broker vs. investment bank — see our dedicated guide. The tell I use from the document side: deal people build a permissioned data room and stage disclosure; brokers email a listing sheet.

Is a $22M-revenue company too small for a real healthcare investment bank?

Not too small for the right healthcare bank, but likely too small for the biggest ones — and knowing where you fit saves you a wasted cycle pitching firms that will politely pass. A $22M-revenue company with roughly $4.5M of EBITDA and an 8-11x hoped-for multiple implies an enterprise value somewhere in the $35M-$50M range, which is genuine middle-market territory, not brokerage territory.

The banks that advised the Triangle's marquee healthcare exits — the bulge-bracket and elite franchises behind Syneos and PPD — fish far above you and are neither reachable nor appropriate for a deal your size. But that is not the whole healthcare bench. Dedicated pharma-services and healthcare boutiques routinely take deals in your band: Provident Healthcare Partners and Edgemont Partners work the lower and core middle market of the sector, and Harris Williams' Outsourced Pharma Services group, while it leans larger, is worth a conversation to learn where its floor sits. The mistake is assuming that because the famous names won't take you, no specialist will — the sector's boutique bench exists precisely for companies your size.

So your realistic shortlist, in order: a pharma-services specialist boutique (fly-in) as first choice, because sector fluency sets your price; a strong registered NC mid-market bank like Anderson LeNeave & Co. (CRD #104101) as a local-generalist alternative; and the Triangle exemption boutiques (High Rock, Lamkin Road, Dunning Capital) if your business is more services than deep science. The screening move is the same for all of them: ask directly what the firm's typical and minimum deal sizes are, and for three recent closings near your size in your sub-sector. A firm that regularly does deals your size answers in one breath; one that does not will tell you (honestly) that you are below its floor — which is useful information, not a rejection. I run Peony, a data room company used by 5,900+ customers, on the document side of exactly these lower-middle-market healthcare deals.

Which Triangle "financial" names are not M&A advisors? A do-not-claim list

Every metro has firms whose names get miscataloged as M&A advisors; the Triangle's version is dominated by one enormous wealth manager and a cluster of name collisions, so this list matters more here than the usual graveyard-of-dead-firms version. These are, in each case, the wrong number for selling your operating company.

- CAPTRUST — the number-one trap on this page. CAPTRUST is a Raleigh-headquartered giant with roughly $1 trillion of client assets, ranked number one on Financial Advisor magazine's 2025 billion-dollar-plus RIA ranking, and it is famously acquisitive (on the order of 73 acquisitions). But it is a wealth manager and RIA that buys other RIAs for its own book — it is not a sell-side M&A advisor that will run a competitive auction to sell your business. Owners see "Raleigh's biggest financial firm, and it does tons of M&A" and misread it; the M&A it does is buying wealth-management practices for itself, which is the opposite of what you need.

- First Citizens BancShares — a Raleigh-headquartered bank holding company (Fortune 500 #309). It is a bank, not your sell-side advisor. It may lend to your business or, through its capital arms, invest — but it does not run a founder-exit auction.

- Private-equity firms — regional sponsors such as Plexus Capital and SharpVue Capital are buyers and investors, not advisors. If one approaches you, that is a bid to evaluate, not an advisor to hire; the whole point of hiring an advisor is to run firms like these against each other.

- Capital City Securities LLC (Powell, Ohio) — an unrelated broker-dealer whose name collides with Raleigh's Capital City Group. If you search "Capital City" and land on the Ohio firm, you have the wrong company.

- Falls River Group — despite the North-Carolina-sounding name (Falls River is a Raleigh neighborhood), this firm is headquartered in Naples, Florida. A name-geography trap.

- Hexagon Capital Alliance (Orange County, California) and Preston Todd (Boston) — more name-alikes with no Triangle M&A presence.

- McColl Partners — a firm stale lists still cite that no longer exists as an independent. McColl Partners was acquired by Deloitte Corporate Finance in June 2013; do not list it as a standalone Charlotte/NC advisor.

The point of the list is the sorting discipline, not disparagement — CAPTRUST and First Citizens are excellent at what they actually do. Before you take any firm's pitch as a sell-side advisor, confirm three things: that it is a registered broker-dealer (with a live CRD) or explicitly operates under the M&A-broker exemption; that it can name three recent closings with the buyers identified; and that a specific senior person will run your deal. Wealth managers, banks, sponsors, and name-alikes fail that test fast.

How do I check whether a Triangle M&A advisor is a registered broker-dealer — and what is the M&A-broker exemption?

Go to FINRA BrokerCheck (brokercheck.finra.org) and search the firm's exact legal name — it returns the CRD number, registration status, business lines, office locations, and any disclosure events. This is free, authoritative, and the single most valuable ten minutes of diligence you will do before signing an engagement letter. For the Triangle's bench, that means confirming FMI Capital Advisors (CRD #129262) and Anderson LeNeave & Co. (CRD #104101) as registered broker-dealers — and understanding why several of the legitimate local boutiques will return no broker-dealer record at all.

That absence is expected, not a red flag. High Rock Partners, Lamkin Road, Capital City Group, and Dunning Capital operate under the federal M&A-broker exemption, which took effect March 29, 2023. It lets qualified M&A brokers facilitate the sale of privately held companies without full broker-dealer registration, subject to size and structure limits — broadly, target companies with EBITDA under $25M or revenue under $250M (your business fits comfortably). This is a normal, appropriate, and common model for pure sell-side advisory: most boutiques that only sell companies (rather than underwrite securities) fit it. So when you pull one of these firms on BrokerCheck and find nothing, that is consistent with the exemption, not evidence of a problem. What you should do — exactly as I advise in every city — is confirm they operate under the exemption rather than red-flag them, and, if your deal is structured as a stock sale rather than an asset sale, ask specifically how the securities piece will be handled and whether a host broker-dealer is involved.

Then watch for the Triangle-specific name collisions, which are this metro's version of the "dead entity" trap:

- "Capital City Securities LLC" (Powell, Ohio) is a different, unrelated broker-dealer — not Raleigh's Capital City Group. Pull the wrong one and you are researching a company two states away.

- Falls River Group is in Naples, Florida, despite the NC-sounding name; Hexagon Capital Alliance is in Orange County, California; and Preston Todd is in Boston — none is a Triangle firm.

- McColl Partners was absorbed into Deloitte Corporate Finance in June 2013 and is not a firm you can hire as an independent.

The generalizable discipline is the one this series always returns to: verify the current entity, its current owner, and its current registration before you sign anything, and confirm the model (registered broker-dealer versus exemption boutique) rather than assuming the absence of a CRD is disqualifying. In a metro where the real bench is small and the name collisions are many, a careful ten minutes on BrokerCheck is the cheapest diligence you will ever do.

Are the Triangle's big companies actually buyers right now, and does that help me sell?

Yes — the university deal engine produces not just sellers but a genuine ecosystem of acquirers, and 2025-2026 gave real signals of strategic and PE demand in exactly the categories a Triangle founder sells into. But read the headline names correctly, because several of the metro's most famous companies are not what a stale list assumes.

Start with the Fortune 500 reality, because it is easy to misread. The Triangle has three Fortune 500 headquarters on the 2026 list: IQVIA (Durham, #274) — a genuine global life-sciences and data giant (~$16.6B TTM revenue, ~88,000-93,000 employees) and a real acquirer in its categories; First Citizens BancShares (Raleigh, #309) — a bank holding company, not an advisor; and Advance Auto Parts (Raleigh, #461) — which fell from #389 and is mid-turnaround (700-plus store closures, and it divested its Worldpac business to Carlyle for about $1.5B, closed November 1, 2024), so do not read its presence as strength. Martin Marietta (Raleigh) narrowly missed the list at #532 — it is not a Fortune 500 member. Statewide, North Carolina counts 12 Fortune 500 companies in 2026.

The living giants are mostly private or controlled, which is why they are not exit comps:

- SAS Institute (Cary) is private (founder Jim Goodnight, founded 1976). Its IPO pledge has softened with no date, and the 2021 Broadcom acquisition rumor was denied and is not live — do not describe SAS as being for sale. (It is, however, an acquirer: it bought UK synthetic-data firm Hazy in November 2024.)

- Epic Games (Cary) is private and controlled by Tim Sweeney (Tencent has held ~40% since 2012; Disney invested $1.5B in February 2024 for ~9% at a $22.5B valuation — a down round from the 2022 peak). Not for sale.

- Lenovo runs its US/Americas HQ from Morrisville; Wolfspeed (Durham) filed a prepackaged Chapter 11 on June 30, 2025 and emerged September 29, 2025, cutting debt roughly 70% (about $6.7B to $2.1B) — it is out of bankruptcy and restructured, not in it, a nuance stale coverage gets wrong. Teamworks (Durham) raised a $235M Series F in June 2025 at a $1B-plus valuation and is a Triangle serial acquirer; Pendo (Raleigh) reached a $2.6B valuation in 2021.

Where a lower-middle-market founder actually sees demand is in the recent, verifiable deal flow — the persona's real world. HVAC and home-services roll-ups are hot: the Raleigh-area Maynor Service Co went to Centre Partners and Baldwin Creek to form TruTemp Holdings (September 2025); Durham's PlumbV (2022) and Happy Home Services (2021) joined the Charlotte PE-backed platform NearU Services; Durham's Alternative Aire went to The Chill Brothers — all against a backdrop of global PE add-ons in HVAC up about 88% year over year through mid-2025. SaaS tuck-ins closed too: Morrisville's Tactyc to Carta, Durham's WorkDove to Quantum Workplace, Morrisville's PlayMetrics taking a stake from Blue Star Innovation Partners. And on the science side, WEP Clinical (Morrisville) was itself a buyer, acquiring Netherlands-based Siron Clinical — a Triangle CRO consolidating, not selling.

The takeaway for a seller: there is real strategic and PE demand for Triangle science, tech, and services assets, and the buyer engine is running. But the marquee names are traps or non-comps, and the biggest deals still fly to bulge-bracket banks — so your process needs national buyer reach through the right specialist, not a bet on a local logo. Once buyers are in the room, page-level analytics will tell you which of them actually engaged past the teaser and which are just kicking tires.

What does an M&A advisor cost to sell a $22M Triangle company?

For a $22M Triangle company, expect a monthly retainer plus a success fee at close, with a blended success fee in the low-single-digit percent. Independent middle-market data — the Axial/Firmex M&A Fee Guide 2024-25 (N=456) — puts blended success fees at roughly 4.8% at a $5M deal, about 3.4% at $20M, and around 2.0% by $100M, so a sale in your range sits in the low-3s percent on the success fee alone. Here is how the pieces work.

The formula. A declining-rate, Lehman-style structure is still the single most common, used in about 44% of engagements (versus roughly 26% flat-rate and 20% with an accelerator that raises the rate on higher tranches) — so do not believe anyone who tells you "nobody uses Lehman anymore." The modern default is Double Lehman (10-8-6-4-2%): 10% of the first $1M of consideration, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $4M. Run that on smaller checkpoints: a $10M deal computes to $400K (4.0%), a $20M deal to $600K (3.0%). The older Classic Lehman (5-4-3-2-1) is about half that.

The retainer. Roughly five of six advisers charge one, typically $5,000-$10,000 per month (some charge a fixed $25K-$75K instead), and about 72% credit it against the success fee at closing (per a 2021-22 fee-guide survey) — but only if the engagement letter says so in writing, so negotiate the credit explicitly.

The minimum fee — the number that actually governs a deal your size. Minimum fees appear in about 67% of engagement letters (2021-22 survey) and typically run $200K-$600K on $5M-$30M deals. On a deal in your range, it is often the floor, not the percentage, that sets the bill — a firm with a $400K minimum on your deal is charging a different effective rate than the Lehman math implies, so ask for the minimum first.

Three more terms deserve scrutiny:

- The fee base. Is the success fee on total enterprise value (including assumed debt and earnouts) or just cash at close? With a consolidator that wants you to roll equity or take an earnout, this distinction is worth real money.

- The tail period. Advisers often ask for 18-24 months, during which they collect if you sell to a buyer they introduced after the engagement ends. Negotiate toward 12 months, and require a named-buyer list within 10 days of termination — your best defense against paying a tail on a buyer the advisor never actually sourced (including the consolidator that approached you first).

- Exclusivity (6-12 months) and expense caps ($25K-$50K typical).

Keep the whole cost conversation in proportion: the fee delta between two good advisors is almost always dwarfed by the price delta a competitive process produces — which is exactly why paying a specialist to run your consolidator against the market pays for itself. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — a predictable cost against an advisory fee that runs into six figures.

Which virtual data room should a Triangle seller actually use?

I run a data room company, so treat this as informed but interested — and I will be honest about where each tool fits. For a true $500M-plus mega-deal with hundreds of bidders and a bulge-bracket bank running the process (the Red Hat and PPD tier), Datasite and Intralinks are the incumbents, and your banker may simply require one; their enterprise pricing typically starts around $50,000 or more per deal, which is rational at that scale and overkill below it. For the sub-$500M enterprise-value band that is the bulk of Triangle deal count — which is to say essentially every deal in this article, and certainly a $35M-$50M science-company sale — you do not need an enterprise mega-platform and should not pay for one. Peony, iDeals, and FirmRoom all run clean, secure, modern sell-side processes at a fraction of that cost.

What actually matters for a Triangle science, tech, or services sale:

- Per-buyer permissions so strategics and financial buyers see different tiers of information, staged as separate access groups in one secure room — essential for the tiered disclosure a confidential process requires.

- Dynamic watermarking so a leaked teaser or CIM is traceable to the viewer who leaked it — critical when the likeliest bidders are the same companies and sponsors you see at every RTP event.

- An NDA gate so nobody sees the named CIM until the agreement is signed.

- Page-level analytics so you can see which buyers genuinely engaged (and which never opened the CIM), which sharpens your advisor's follow-up and your read on real interest.

- Pricing that does not punish you per page or per gigabyte — a document-heavy diligence process (and science businesses are document-heavy: methods, validations, regulatory files) should not inflate the bill.

We serve more than 5,900 customers, many running exactly the kind of founder-owned and family-business sales this article is about, and the Triangle's lower-middle-market deals sit right in that band. For the full solution view, see our M&A data room solution; for the pricing comparison across providers, our virtual data room cost guide breaks down the models. Whatever you choose, set the room up before you go to market — it is the cheapest lever you control, and the one that most reliably compresses the back half of the timeline.

Bottom line

The Research Triangle mints science and software exits out of the Duke, UNC, and NC State research complex — and when those companies sell, the mandate has always gone to whoever is most fluent in the asset, wherever they sit. Red Hat → IBM ($34B, 2019), PPD → Thermo Fisher ($17.4B, 2021), and Syneos → its Elliott/Patient Square/Veritas consortium (about $7.1B, 2023) were bulge-bracket-and-specialist affairs, never local mandates — and they could not have been, because deals that large and that specialized belong to the handful of franchises in the world that run them. That is not a deficiency in Raleigh; it is the physics of specialization, and it defines the whole advisor decision here.

For a founder, the practical consequence is a two-layer answer plus fly-in specialists. The one genuine Triangle-rooted investment bank is FMI Capital Advisors (CRD #129262) — Raleigh-headquartered parent, Denver-registered broker-dealer, registered Raleigh branch, and a construction-industry specialist through and through. The honest local lower-middle-market bench is a short list of M&A-broker-exemption boutiques — High Rock Partners, Lamkin Road, Capital City Group, and Dunning Capital — with Anderson LeNeave & Co. (CRD #104101) reaching in from Charlotte as the strongest registered NC bank and Viking M&A covering the smaller end. And for the science and software exits that define this metro, the best advisors are the sector specialists who fly in — Provident, Edgemont, and Harris Williams' Outsourced Pharma Services group for pharma services and CROs; Software Equity Group, Vista Point, and AGC for software.

The honest counters, held alongside the thesis: the metro's famous names are traps or non-comps — CAPTRUST (~$1T assets) is a wealth manager buying RIAs for itself, not your sell-side advisor; First Citizens is a bank holding company; SAS and Epic are private and not for sale; and the marquee exits are neither your comps nor your mandates. Verify every firm's current status on FINRA BrokerCheck, confirm the exemption boutiques rather than red-flagging them, and watch the name collisions (Capital City Securities of Ohio, Falls River of Naples, the defunct McColl Partners). And whichever path you choose, build a clean, staged data room before you go to market. In the metro where the specialists fly in, the sellers who win are the ones who match the advisor to the exit — a construction bank for the built environment, a pharma-services specialist for the lab, a capable local boutique for the general business — and still make every firm prove buyer reach, named closings, and senior attention before they sign.

Frequently asked questions about Raleigh-Durham M&A advisors

Are there any real M&A advisors based in Raleigh-Durham, or do I have to go out of town?

There are real ones, but the bench is thin and specialized — which is the honest, verified answer, not a dodge. The biggest genuinely-Triangle-rooted investment bank is FMI Capital Advisors (FINRA CRD #129262): its parent, FMI Corporation, has been headquartered at 223 S. West St in Raleigh since 1953, and while the broker-dealer subsidiary is registered mainly out of Denver, it maintains a registered Raleigh branch at the parent's address. The catch is that FMI is a national construction, engineering, and built-environment M&A specialist with 800-plus transactions — not a local generalist who will sell your bioanalytical lab. Beneath it sit legitimate lower-middle-market boutiques that operate under the federal M&A-broker exemption (no broker-dealer of their own): High Rock Partners, Lamkin Road, Capital City Group, and Dunning Capital, all Raleigh-based. Charlotte's registered banks reach up I-85 — Anderson LeNeave & Co. (CRD #104101) is the strongest registered NC-headquartered mid-market bank in the coverage set. And for a pharma-services or software company, the best advisors fly in from Boston, New York, and San Francisco, because the Triangle's exits are so specialized that sector specialists own the flow. So the real answer is a two-layer bench plus fly-in specialists — knowable, but not a deep local roster. I run Peony, a data room company used by 5,900+ customers, and whichever you pick, a clean, staged room with page-level analytics is the cheapest lever you control before you even sign an engagement letter.

Should I hire a local Triangle advisor or an out-of-town pharma-services specialist to sell my CRO-adjacent business?

For a CRO-adjacent or pharma-services company, hire the sector specialist even if it flies in — this is the fluency-over-address rule at maximum strength. The Triangle's science exits are so specialized that a generalist, however local and however competent, cannot match a dedicated pharma-services banker who already knows, by name, the strategic consolidators and the PE platforms actively rolling up CROs and lab-services businesses. Those specialists are not in Raleigh: Provident Healthcare Partners (Boston) publishes quarterly CRO M&A updates and lives in the vertical; Edgemont Partners (New York) runs a dedicated pharma-services practice; and Harris Williams' Outsourced Pharma Services group covers the category from a national platform. A local Triangle boutique is the right call for a manufacturer, a business-services company, or a government contractor — where the buyer universe is broader and a good generalist can run a full competitive process. But for a bioanalytical lab with backlog, book-to-bill, and GLP/FDA-compliance nuances that define value, the specialist's buyer list is worth far more than a local address. The test is identical either way: named senior staffing, three named recent closings in your exact sub-sector, and the buyers on the other side. For the national view of the category, see our best healthcare M&A advisors guide. I run Peony, a data room company used by 5,900+ customers, and in a small, interconnected vertical dynamic watermarking matters because your buyer list is also your competitor list.

Can a generalist M&A advisor actually value a science business — backlog, book-to-bill, GLP compliance?

A good generalist can run the process, but valuing a science business correctly takes sector fluency a generalist usually does not have — and getting the valuation drivers wrong costs you real money. A bioanalytical lab or CRO-adjacent business is not valued like a widget maker: buyers underwrite backlog (contracted-but-unrecognized revenue) and its quality, book-to-bill ratio (new bookings divided by revenue — above 1.0 signals growth, and yours near 1.1 is a genuine selling point), the mix of recurring versus project revenue, client concentration among sponsors, cancellation and pass-through-cost terms, and the regulatory and quality layer that gates everything — GLP status, FDA inspection history (Form 483s and their resolution), data integrity, and accreditations. A banker who does not speak that language will let a buyer discount your backlog, misread your book-to-bill, or fail to defend the premium a clean GLP inspection record deserves. This is exactly why, for a pharma-services or CRO deal, the specialist bankers who fly in (Provident, Edgemont, Harris Williams' Outsourced Pharma Services group) tend to clear higher valuations than a generalist — they know which metrics a sophisticated strategic will pay up for and which objections to preempt. Ask any advisor to walk you through how they would value your backlog and normalize your book-to-bill before you sign; the answer tells you everything. I run Peony, a data room company used by 5,900+ customers, and a data room organized around those diligence drivers is what lets a buyer confirm your numbers quickly instead of discounting them.

How are bioanalytical labs and pharma-services companies valued in a sale?

Bioanalytical labs and pharma-services companies are valued primarily on a multiple of normalized EBITDA, with the multiple set by the durability and visibility of that EBITDA — which in this sector means backlog, book-to-bill, and the quality of the sponsor relationships behind them. The mechanics: a buyer starts from your trailing and forward EBITDA, normalizes it (adding back owner compensation, one-time costs, and non-recurring items, and scrutinizing pass-through costs, which in CRO models can distort margins if not stripped out), then applies a multiple driven by growth (book-to-bill above 1.0), revenue quality (recurring and contracted versus one-off projects), client concentration (a single sponsor at 40 percent of revenue is a discount; a diversified base is a premium), therapeutic-area and modality mix, and the regulatory record (GLP status and a clean FDA inspection history support the multiple; unresolved 483s erode it). Scale matters too — larger, more diversified platforms command higher multiples than sub-scale single-site labs, which is part of why strategic consolidators pay up to add capabilities. I am not going to publish a precise multiple range as if it were a fact for your specific business, because pharma-services multiples vary widely by sub-sector, scale, and growth, and a false-precision number would mislead you; a specialist banker with current comps will give you a defensible range for your exact profile. What I can say with confidence is that the valuation is won or lost on how well your backlog, book-to-bill, and compliance record are documented and defended — which is a preparation problem before it is a negotiation problem. I run Peony, a data room company used by 5,900+ customers, and the sellers who defend their multiple are the ones who walk in with the diligence file already built.

A PE-backed consolidator approached me unsolicited — do I still need an advisor?

Yes — and an unsolicited approach from a PE-backed consolidator is precisely the moment you most need one, because it means a professional, repeat buyer has decided your company is worth acquiring before you have run any process to learn what it is worth. Consolidators roll up fragmented sectors (labs, CROs, home services, SaaS) for a living; they approach founders directly specifically to buy without competition, and they are very good at making a below-market bilateral offer feel flattering and urgent ("we love what you've built, let's move fast, exclusively"). A first-time seller has no way to know whether the multiple is generous or a lowball dressed up as a compliment. An M&A advisor's job is to convert that single inbound into a competitive process — running a curated set of other credible strategics and sponsors against the party that called, under NDA and from a blind teaser, so price is set by the market rather than by the one buyer at the table. That competitive tension typically moves the outcome by far more than the advisor's fee. An advisor also protects you on the mechanics a repeat buyer uses routinely and you will encounter once: the LOI structure, the earnout and equity-rollover terms, the exclusivity and no-shop clauses that hand the buyer leverage to re-trade during diligence, and the confirmatory-diligence gauntlet itself. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects you — staged disclosure through a permissioned room — is the same whether one buyer called or ten did.

Is the first unsolicited offer usually below what my company is worth?

More often than not, yes — a single unsolicited offer is a starting point, not a fair price, and treating it as the ceiling is how founders leave money on the table. Price on a private company is not a fixed number; it is whatever a motivated buyer will pay when they know another motivated buyer is in the room. A PE-backed consolidator that reached out did so precisely because it hopes to transact bilaterally, without that pressure, and it has every incentive to anchor you low while the offer still feels like validation. The only way to know whether the number is at, above, or below market is to test it — and running even a tight, confidential process against a curated short list does three things at once: it benchmarks the offer against real alternatives, it moves price and terms in your favor through competitive tension, and it disciplines the original buyer, who now knows it cannot slow-walk diligence or re-trade the price without risking the deal to a rival. The objection founders raise is confidentiality, especially in a small industry — and it is solvable: a good advisor markets from a blind teaser under NDA and stages disclosure through a permissioned data room, so only serious, vetted buyers ever learn your identity. The cost of running a process is measured in months and a success fee; the cost of skipping it is often a materially lower price. I run Peony, a data room company used by 5,900+ customers, built for exactly this kind of staged, confidential release.

How do I sell confidentially when everyone at RTP knows everyone?

You keep it confidential with staged disclosure enforced by a permissioned data room: a blind teaser first, the named confidential information memorandum only after a signed NDA, and the most sensitive material (client names, sponsor contracts, pricing, key-scientist rosters) held back for a small short list of serious, later-stage bidders. This matters acutely in the Research Triangle, where the science and technology community is genuinely small — your competitors, your largest sponsors, your key scientists, and the PE firms circling your sector may all know each other, sit on the same boards, and see each other at the same conferences. A leak that you are "for sale" can spook a sponsor mid-study, embolden a competitor to poach your principal investigators, or unsettle staff before you have a signed deal. The structural defenses: the initial teaser describes the business (sector, size, financial profile, capabilities) without naming it, so a recipient — including a competitor — cannot identify you from it; the full CIM goes only to NDA-signed buyers your advisor has curated to exclude the parties most likely to misuse it; and the crown-jewel material is released only in the final wave. The tooling has to enforce all of that: dynamic watermarking stamps each viewer's identity across every page so a leaked document is traceable to its source, an NDA gate blocks access until the agreement is signed, and page-level analytics show exactly who opened what and when. I run Peony, a data room company used by 5,900+ customers, precisely to make this staged, watermarked, permissioned release the default rather than a scramble — because at RTP your buyer list is almost certainly also your competitor list.

What's the difference between a business broker and an M&A advisor for a $22M company?

A business broker lists smaller, owner-operated businesses (typically under about $5M of enterprise value) to a pool weighted toward individual buyers, on a listing-and-commission model; an M&A advisor or investment bank runs a confidential, competitive, curated process for a middle-market company, marketing to strategic acquirers and private-equity firms and manufacturing tension among them. For a $22M-revenue company with roughly $4.5M of EBITDA, you are squarely in M&A-advisor territory, not business-brokerage territory — your best buyers are strategic consolidators and PE platforms who will never see a broker's public listing, and reaching them confidentially is the entire job. The practical differences that matter: a broker often posts a semi-public listing anyone can browse, while an advisor markets from a blind teaser under NDA and never names your company early; a broker's buyer is usually an individual or a small operator, while an advisor's buyer is an institution that pays on multiples of EBITDA; and a broker's fee is a flat commission, while an advisor charges a retainer plus a success fee scaled to the deal. In the Triangle, business brokers like Transworld, Murphy Business, and VR Business Brokers are the right fit below roughly $2M of enterprise value; a science company with $4.5M of real EBITDA has long outgrown that model. For the full taxonomy, see our M&A advisor vs broker vs investment bank guide. I run Peony, a data room company; the tell is simple — deal people build a permissioned data room, brokers email a listing.

Is a $22M-revenue company too small for a real healthcare investment bank?

Not too small for the right healthcare bank, but likely too small for the biggest ones — and knowing where you fit saves you a wasted cycle. A $22M-revenue company with roughly $4.5M of EBITDA and an 8-11x hoped-for multiple implies an enterprise value somewhere in the $35M-$50M range, which is real middle-market territory, not brokerage territory. The bulge-bracket and elite healthcare franchises (the banks that advised Syneos and PPD) fish far above you and will pass. But dedicated pharma-services and healthcare boutiques routinely take deals in your band: Provident Healthcare Partners and Edgemont Partners work the lower and core middle market of the sector, and Harris Williams' Outsourced Pharma Services group, while it leans larger, is worth a conversation to learn where its floor sits. The mistake is assuming that because the famous names won't take you, no specialist will — the sector's boutique bench exists precisely for companies your size. Your realistic shortlist is a pharma-services specialist boutique (fly-in) as first choice, a strong registered NC mid-market bank like Anderson LeNeave & Co. (CRD #104101) as a local-generalist alternative, and the Triangle exemption boutiques if your business is more services than science. Ask each firm directly what its typical and minimum deal sizes are, and for three recent closings near your size in your sub-sector. I run Peony, a data room company used by 5,900+ customers, on the document side of exactly these lower-middle-market healthcare deals.

What do M&A advisors charge to sell a $22M company?

For a $22M company, expect a monthly retainer plus a success fee at close, with a blended success fee in the low-single-digit percent. Independent middle-market data — the Axial/Firmex M&A Fee Guide 2024-25 (N=456) — puts blended success fees at roughly 4.8% at a $5M deal, about 3.4% at $20M, and around 2.0% by $100M, so a sale in your range sits in the low-3s percent on the success fee alone. The most common structure is still a declining-rate, Lehman-style formula: the modern default, Double Lehman (10-8-6-4-2%), charges 10% of the first $1M of consideration, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $4M — which computes to $400K on a $10M deal (4.0%) and $600K on a $20M deal (3.0%); the older Classic Lehman (5-4-3-2-1) is roughly half that. Two numbers matter more than the headline percentage on a deal this size. First, the minimum fee: minimums appear in about two-thirds of engagement letters (per a 2021-22 fee-guide survey) and typically run $200K-$600K on $5M-$30M deals — so on a smaller deal it is often the floor, not the percentage, that sets the bill. Second, the retainer: roughly five of six advisers charge one ($5,000-$10,000 per month, or a fixed $25K-$75K), and about 72% credit it against the success fee — but only if the engagement letter says so in writing, so negotiate the credit explicitly. Also scrutinize the tail (18-24 months asked; negotiate toward 12) and the fee base (enterprise value including debt and earnouts, or just cash at close). I run Peony, a data room company with flat per-admin pricing, a predictable line item against a six-figure advisory fee.

What EBITDA multiple do pharma-services and CRO-adjacent companies sell for, and how long does it take?

Pharma-services and CRO-adjacent companies trade on a multiple of normalized EBITDA that varies widely by sub-sector, scale, growth, and — above all — the quality of backlog and book-to-bill, so the honest answer is that a specialist banker with current comps must set your range rather than a blog quoting one number. What I can say is what moves the multiple: a book-to-bill above 1.0 (yours near 1.1 helps), a diversified sponsor base rather than heavy client concentration, recurring and contracted revenue over one-off projects, a clean GLP status and FDA inspection history, differentiated capabilities or therapeutic-area focus, and scale — larger, multi-capability platforms command more than sub-scale single-site labs, which is why strategic consolidators pay up to add what they lack. Your hoped-for 8-11x is not unreasonable for a well-run, growing lab with clean compliance and durable backlog, but it has to be earned in the diligence file and defended by a banker who speaks the sector's language; a generalist can let a buyer chip it down. On timing: plan on roughly 6-9 months from signing the engagement letter to close, longer if the financials need cleanup first — 4-8 weeks of preparation (clean financials, a quality-of-earnings build, the CIM, and a data room), 2-4 weeks of buyer outreach under NDA, 3-5 weeks to collect indications of interest, 4-6 weeks of management meetings and the LOI stage, then 8-12 weeks of confirmatory diligence and definitive-agreement negotiation. The single biggest timeline risk is unprepared financials. I run Peony, a data room company used by 5,900+ customers, and a clean, staged data room built before you go to market is the most reliable way to compress the back half of the schedule.

Related resources

- The State of M&A Data Rooms — our platform benchmark on how sell-side processes actually run, across hundreds of deals in the sub-$500M band that covers most of the Triangle.

- How to Build an M&A Data Room — the staged-disclosure playbook every Triangle seller should run before going to market.

- How to Write a CIM — the confidential information memorandum your advisor builds after the blind teaser.

- M&A Advisor vs Broker vs Investment Bank — the taxonomy every first-time seller should read before hiring anyone.

- Hard vs Soft Due Diligence — what buyers actually scrutinize in the confirmatory phase where deals slow down or die.

- Best Healthcare M&A Advisors — the national sector view for the pharma-services, CRO, and lab specialists who fly in to run the Triangle's science exits.

- Best Software M&A Advisors — the specialist bench (Software Equity Group, Vista Point, AGC) for the Triangle's SaaS and software sellers.

- Best M&A Advisors in Charlotte — the registered bank bench down I-85 that reaches into the Triangle (Anderson LeNeave and Viking both cover Raleigh-Durham from there).

- Best M&A Advisors in Richmond — the neighbor 150 miles northeast, and the structural contrast: Richmond built its own dedicated mid-market flagship (Harris Williams) instead of relying on specialists who fly in.

- Best M&A Advisors in Nashville — a Southeastern peer market for a lower-middle-market seller.

- Best M&A Advisors in Atlanta — the region's largest deal hub and the nearest metro with a deep homegrown investment-banking bench.

- Virtual Data Room Cost Guide — the full pricing comparison across providers for a sub-$500M sell-side.

Footnotes and sources

- FINRA BrokerCheck (brokercheck.finra.org) — verified entity registrations and CRD numbers: FMI Capital Advisors, Inc. (CRD #129262, active; broker-dealer subsidiary of FMI Corporation; main registered office in Denver, CO, with a registered branch at 223 S. West St, Ste 1200, Raleigh — the parent's address); Anderson LeNeave & Co. (CRD #104101, active; Charlotte, NC; formed in North Carolina August 4, 1998; full-service middle-market broker-dealer). High Rock Partners, Lamkin Road, Capital City Group, and Dunning Capital return no broker-dealer firm records, consistent with operating under the federal M&A-broker exemption (effective March 29, 2023, for privately held targets with EBITDA under $25M or revenue under $250M). Name-collision traps: "Capital City Securities LLC" (Powell, OH) is an unrelated broker-dealer, not Raleigh's Capital City Group.

- The genuinely-local bench — FMI Capital Advisors: parent FMI Corporation headquartered at 223 S. West St, Raleigh, since 1953; national construction, engineering, and built-environment M&A specialist; 800+ transactions across sell-side, buy-side, ESOP, and valuations; broker-dealer subsidiary CRD #129262 (Denver main office, registered Raleigh branch). High Rock Partners: Raleigh, founded 1999; founder Kenneth H. Marks (CM&AA credential-holder and author on middle-market M&A); lower-middle-market strategy plus M&A (~29 tracked deals). Lamkin Road: Raleigh; founder/managing director Mark Phillips (ex-Jacobs Capital); team includes former Baird government/defense M&A talent; sectors: business services, government contracting, healthcare/life sciences, manufacturing, technology. Capital City Group: Raleigh, founded 2003; founder Larry Carroll; targets $10M-$70M revenue and $1M+ EBITDA in manufacturing and wholesale distribution. Dunning Capital: Raleigh, founded 2002; principals Paul M. Steinke and David A. Swintosky (~23 tracked deals); Mid-Atlantic/Southeast lower middle market across manufacturing, consumer, healthcare, and IT. All four are urged to be verified on BrokerCheck and asked how securities-involving (stock) deals are handled.

- Charlotte reaching up I-85 — Anderson LeNeave & Co. (CRD #104101), Charlotte full-service middle-market broker-dealer, formed in NC August 4, 1998 (~38 deals) — the strongest registered NC-headquartered mid-market bank in the coverage set. Viking Mergers & Acquisitions: Charlotte since 1996; 950+ deals; has a Raleigh/Durham office; Main Street to lower-lower-middle-market tier. Trap: McColl Partners was acquired by Deloitte Corporate Finance in June 2013 and no longer exists as an independent firm.

- The specialists who fly in — pharma services and CROs: Provident Healthcare Partners (Boston; publishes quarterly CRO M&A updates), Edgemont Partners (New York; dedicated pharma-services practice), Harris Williams' Outsourced Pharma Services group; category names Cain Brothers (part of KeyBanc), Ziegler, Capstone. Software/SaaS: Software Equity Group, Vista Point Advisors, AGC Partners. Business brokers (sub-$2M): Transworld Business Advisors (4509 Creedmoor Rd, Raleigh), Murphy Business, VR Business Brokers.

- Marquee Triangle exits (bulge-bracket / specialist advised, never local mandates) — Red Hat to IBM ($34B, $190/share, closed July 9, 2019; IBM advised by Goldman Sachs, JPMorgan, Lazard; Red Hat advised by Morgan Stanley and Guggenheim). PPD to Thermo Fisher ($17.4B; $47.50/share plus

$3.5B debt; closed December 8, 2021; PPD is headquartered in Wilmington, NC — a coastal NC pharma-services exit, not literally a Triangle company). Syneos Health (Morrisville) to a consortium of Elliott Investment Management, Patient Square Capital, and Veritas Capital ($7.1B including debt; $43.00/share; closed September 28, 2023). Advance Auto Parts (Raleigh) sold Worldpac to Carlyle (~$1.5B, ~$1.2B net; closed November 1, 2024) — a Raleigh corporate divestiture at bulge-bracket tier. Prometheus Group (Raleigh) to Genstar was May 2019 (not recent). - The buyer engine / city economy — Fortune 500 2026 (Axios Raleigh, June 3, 2026): IQVIA (Durham) #274 (~$16.6B TTM revenue, ~88,000-93,000 employees); First Citizens BancShares (Raleigh) #309 (a bank holding company, not an advisor); Advance Auto Parts (Raleigh) #461 (fell from #389, mid-turnaround: 700+ store closures, Worldpac divested). Martin Marietta (Raleigh) narrowly missed at #532 (not an F500 member). North Carolina: 12 Fortune 500 companies in 2026. Private giants: SAS Institute (Cary, private; founder Jim Goodnight; founded 1976; IPO pledge softened with no date; 2021 Broadcom acquisition rumor denied, not live; acquired UK synthetic-data firm Hazy November 2024); Epic Games (Cary, private; Tencent ~40% since 2012; Disney invested $1.5B February 2024 for ~9% at a $22.5B valuation, a down round; Sweeney retains control); Lenovo (US/Americas HQ in Morrisville). Wolfspeed (Durham): filed prepackaged Chapter 11 June 30, 2025 and emerged September 29, 2025 — debt cut

70% ($6.7B to ~$2.1B); it is out of bankruptcy, restructured. Pendo (Raleigh, $2.6B Series F valuation July 2021, ~$100M ARR at the 2021 raise). Teamworks (Durham): $235M Series F June 2025 led by Dragoneer at $1B+ — a Triangle serial acquirer. - The university deal engine — Research Triangle Park: 7,000 acres, largest research park in North America, 385+ companies, 55,000+ workers; "RTP 3.0" development code approved June 2026. Universities: UNC research spending topped $1.55B; 682 UNC-affiliated startups (~$8B/yr impact); 87% of NC's in-state R&D concentrated in UNC + Duke + NC State (per TEConomy). Biotech capital 2025: ~$4B NC life-sciences investment; Hatteras Venture Partners (Durham) closed $200M+ across two funds; Novartis $771M Durham/Wake expansion (380 jobs); Genentech $700M Holly Springs (420 jobs). Metro growth: Raleigh-Cary +10.2% since 2020 to ~1.6M (~4x national rate); City of Raleigh passed 500,000 in 2024; Durham-Chapel Hill +6.6% to ~621k.

- Verified 2021-2026 lower-middle-market deal flow (the persona's world) — HVAC/home-services roll-ups: Maynor Service Co (Apex, founded 1996) to Centre Partners + Baldwin Creek to form TruTemp Holdings (September 2025); PlumbV (Durham, 2022) and Happy Home Services (Durham, 2021) to NearU Services (Charlotte PE-backed platform); Alternative Aire (Durham) to The Chill Brothers; context: global PE add-ons in HVAC +88% YoY through mid-2025. SaaS: Tactyc (Morrisville) to Carta; WorkDove (Durham) to Quantum Workplace; PlayMetrics (Morrisville) to Blue Star Innovation Partners (stake). CRO as buyer: WEP Clinical (Morrisville) acquired Siron Clinical (Netherlands).