7 Best M&A Advisors in Milwaukee for $5M–$500M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: July 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. Before Peony I ran M&A deals as a banker at Nomura and invested at Target Global and Backed VC, so I have sat on both sides of the table — and now, on the document side, I watch hundreds of deals a year move through our platform, from founder-led exits and family-business successions to PE recapitalizations and strategic carve-outs. Milwaukee is the entry in our M&A advisor series where the metro's defining fact is not its industry mix or its deal volume but a single structural inheritance: it is the city that kept its investment bank. Most "best Milwaukee M&A advisors" pages fail a simple currency test. They still describe Cleary Gull as an independent Milwaukee investment bank (it has been CIBC's Milwaukee middle-market team since 2019). They still list "Schenck M&A Solutions" (which became the independent Taureau Group in January 2019). They list Grace Matthews as the broker-dealer (the registered entity is its affiliate, GM Securities). And they routinely file Northwestern Mutual — a life insurer — under "M&A advisors." At Peony we now serve more than 5,900 customers, and Milwaukee sits squarely in the sub-$500M enterprise-value band that makes up the bulk of the deals we see in our state-of-the-market benchmark.

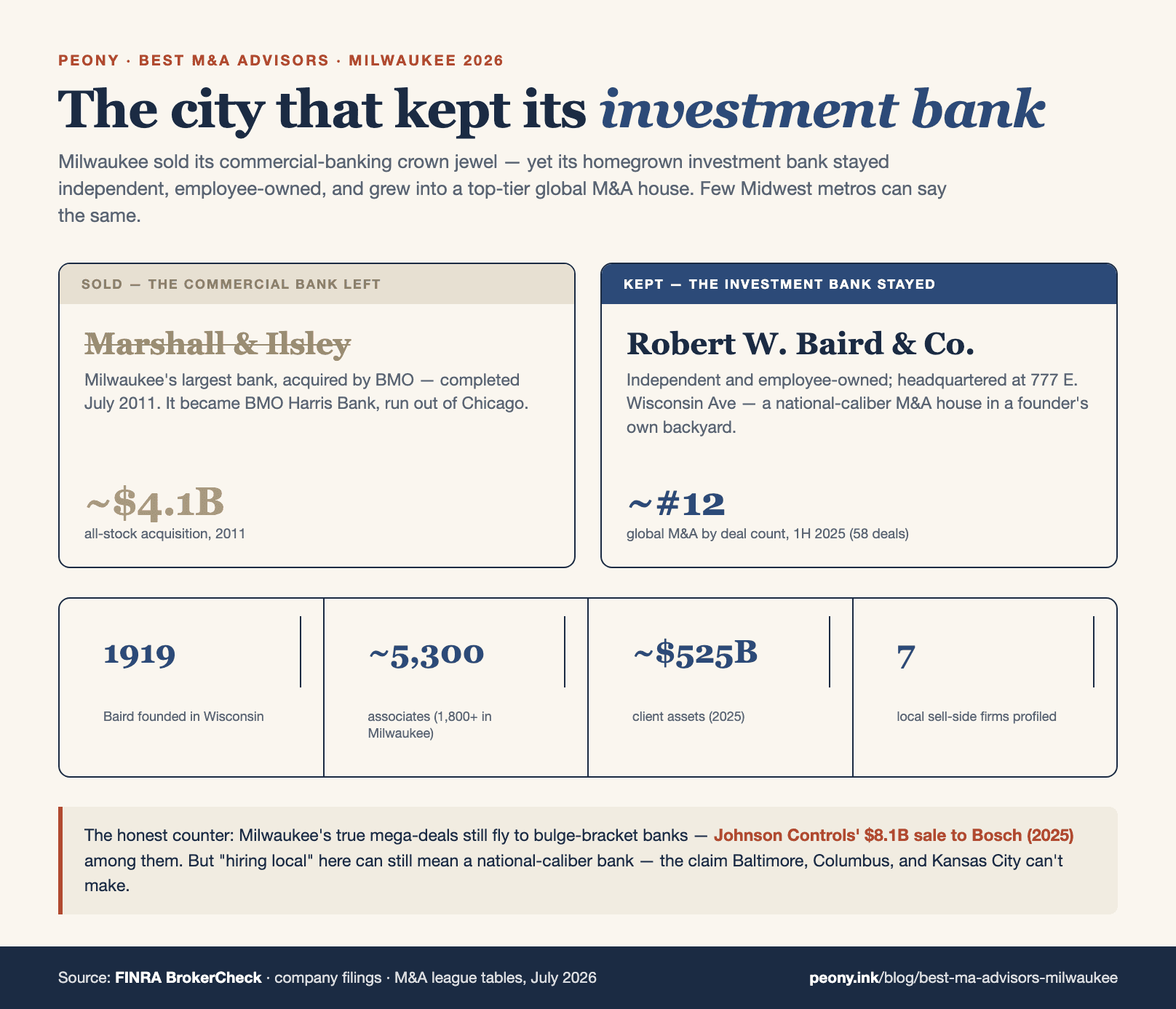

Here is the thesis I want you to internalize before you read another word: Milwaukee kept its investment bank when it sold its commercial bank. In 2011 the metro parted with Marshall & Ilsley — its commercial-banking crown jewel — to BMO. But employee-owned Robert W. Baird & Co. stayed independent, stayed headquartered on E. Wisconsin Avenue, and scaled into one of the roughly twelve largest M&A houses in the world. That single fact reorganizes the whole advisor decision. Unlike Baltimore, which invented American investment banking and then sold every homegrown heir, or Kansas City and Columbus, where no homegrown investment bank ever scaled, a Southeast-Wisconsin founder weighing a sale gets a choice almost no peer metro can offer: hire the national-caliber bank in your own backyard, or hire a smaller local boutique that will focus entirely on you.

That is not a marketing line — it is a real fork with real trade-offs, and I will walk through both sides honestly, including the counter that matters most: Milwaukee's true mega-deals (Johnson Controls' $8.1B sale to Bosch is the current example) still fly to bulge-bracket banks, and "keeping it local" with Baird really means hiring a national bank that happens to be headquartered locally. This post is the working playbook I would hand to a Milwaukee manufacturer weighing a sale, a family-business owner weighing succession against an ESOP, or a specialty-chemicals CEO fielding inbound interest. The frames come from cross-referencing FINRA BrokerCheck, the firms' own disclosures, and the verified 2025-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in Milwaukee right now for $5M-$500M deals?

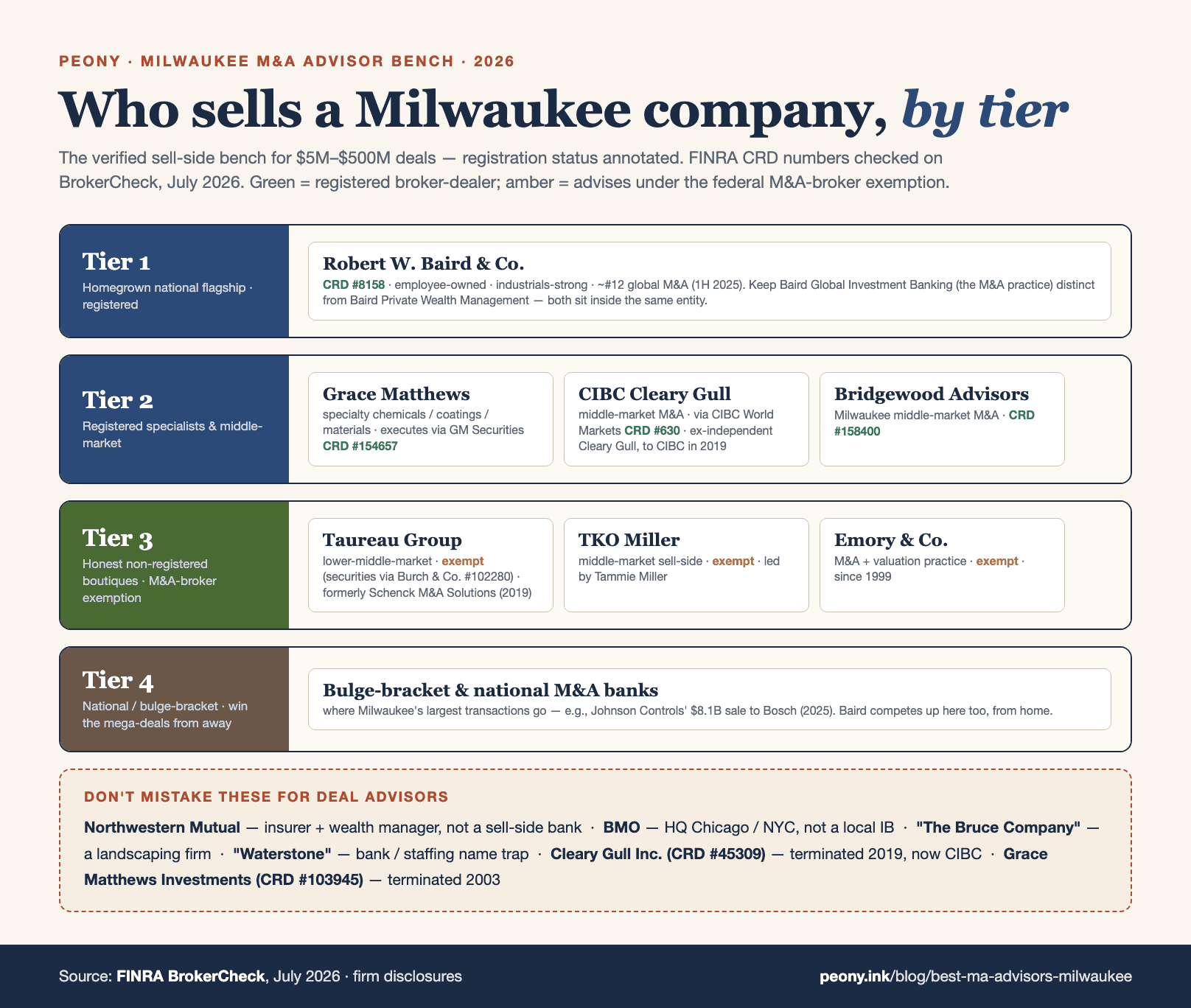

The Milwaukee shortlist for 2026, sorted by tier and deal-size band — with the honesty banner up front: this is the rare Midwest metro whose genuinely-local bench includes both a national-caliber flagship (Robert W. Baird) and a credible set of registered and exempt boutiques, matched unusually well to the region's maker economy. The verification wrinkle is different from most cities: the traps here are not dead firms so much as renamed and re-homed ones — Cleary Gull is now CIBC's team, Schenck M&A Solutions is now Taureau, and Grace Matthews executes through GM Securities.

| Firm | HQ / Milwaukee presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| Robert W. Baird & Co. ★ | 777 E. Wisconsin Ave, Milwaukee (formed 1919, employee-owned) | $75M-$500M+ EV | Industrials and core-middle-market M&A on a global platform (~#12 by M&A deal count, 1H25) | Registered broker-dealer (CRD #8158) |

| Grace Matthews (via GM Securities) | Milwaukee, 833 E. Michigan St (founded 1999) | $25M-$300M EV | Specialty chemicals, coatings, materials science (150+ transactions) | Registered broker-dealer — GM Securities, LLC (CRD #154657) |

| CIBC Cleary Gull | Milwaukee branch of CIBC (NYC HQ; ex-Cleary Gull, to CIBC 2019) | $50M-$300M EV | Middle-market M&A plus private capital raising | Registered broker-dealer — CIBC World Markets Corp. (CRD #630) |

| Bridgewood Advisors Inc. | 111 E. Wisconsin Ave, Milwaukee (formed 2011) | $10M-$100M EV | Milwaukee middle-market M&A | Registered broker-dealer (CRD #158400) |

| Taureau Group (fka Schenck M&A Solutions) | Milwaukee (independent since Jan 1, 2019) | $10M-$250M EV | Closely-held / family-owned; mfg, services, healthcare, food and bev, packaging | M&A advisor (non-registered; securities via Burch & Company, CRD #102280) |

| TKO Miller | Milwaukee (founded 2016) | $10M-$150M EV | Middle-market; recent water-technology and packaging sell-sides | M&A advisor (not a registered broker-dealer; M&A-broker model) |

| Emory & Co. | Milwaukee (formed 1999) | $5M-$75M EV | M&A plus a heavy valuation practice (135+ deals, 1,400+ valuation projects) | M&A advisor (not a registered broker-dealer; M&A-broker model) |

| National / bulge-bracket banks | New York / Chicago — no Milwaukee M&A office | $500M+ EV | Win Milwaukee's mega-deals from out of town (JCI's $8.1B sale to Bosch); Baird competes here too | Established FINRA broker-dealers |

A few notes the table cannot carry. Robert W. Baird & Co. is the reason this page reads differently from every other city in the series: it is a genuinely homegrown, employee-owned bank — formed in Wisconsin in 1919, headquartered at 777 E. Wisconsin Avenue, with roughly 5,300 associates and about $525B in client assets — whose global investment-banking arm ranked around #12 in worldwide M&A league tables in the first half of 2025 (58 M&A deals, per ION Analytics/Mergermarket league tables). The nuance you must hold, covered in its own section below, is that "Baird" contains two very different businesses inside one legal entity: the global investment bank that would sell your company, and Baird Private Wealth Management, the retail advisors who manage individuals' money. Both live inside CRD #8158.

Grace Matthews is the sleeper strength of this metro — a specialty-chemicals, coatings, and materials-science M&A boutique that punches at national weight in its niche, executing through its affiliated broker-dealer GM Securities, LLC (CRD #154657). CIBC Cleary Gull is the former independent Cleary Gull, now the Milwaukee-resident team of CIBC's US middle-market investment bank (CRD #630) — a real local presence backed by a national bank's balance sheet. Bridgewood Advisors (CRD #158400) rounds out the registered boutique bench. Then the honest non-registered tier — Taureau Group (the former Schenck M&A Solutions), TKO Miller, and Emory & Co. — operates under the federal M&A-broker exemption, a legitimate and common model for private-company sales.

And the critical honesty point on the firms a Milwaukee owner is most likely to already know: Northwestern Mutual is a life insurer and wealth manager, not an M&A advisor; BMO's investment bank is in New York and its retail bank in Chicago, not Milwaukee, whatever the M&I heritage suggests; and the name-alikes ("The Bruce Company," "Waterstone") are not advisors at all. More on the sorting test below.

Why is Milwaukee "the city that kept its investment bank"?

Every metro in this series has a structural signature. St. Louis is a Headquarters Town that grew and kept a national bank in Stifel. Baltimore is the First Bank Town that invented American investment banking and then sold every homegrown heir. Kansas City is the Ownership Town, where the crown jewels are built never to sell and no homegrown investment bank ever scaled. Milwaukee's signature is the cleanest inversion of Baltimore's: it sold the commercial bank and kept the investment bank.

The commercial-bank half of the story is Marshall & Ilsley. For generations, M&I was Milwaukee's dominant bank — the commercial-banking crown jewel of the state. In 2011 it was acquired by BMO (Bank of Montreal) in an all-stock deal, completed July 5, 2011, valued at roughly $4.1B; M&I was merged with Harris Bank to create BMO Harris Bank, headquartered in Chicago. From that day, the deposit-taking, branch-banking core of Milwaukee finance answered to Toronto and Chicago. If the story ended there, Milwaukee would read like Baltimore or Cleveland — a proud industrial city whose financial institutions were absorbed by outsiders.

But the story does not end there, because the investment-bank half stayed home. Robert W. Baird & Co. — employee-owned, formed in Wisconsin in 1919, headquartered on E. Wisconsin Avenue — never sold. Instead it compounded: roughly 5,300 associates, about $525B in client assets, and a global M&A practice that now ranks among the dozen or so largest in the world by deal count. Employee ownership is the mechanism: with no outside shareholder pressing for a sale and no parent to fold into, Baird could reinvest for decades. The result is the fact almost no peer metro can claim — a founder in Waukesha or Menomonee Falls can hire a top-tier global M&A bank whose headquarters is a twenty-minute drive away.

What does that mean for you, a founder selling a $5M-$500M company? Three things. First, the local-versus-national decision is a genuine choice here, and it arrives higher on the size curve than in most cities. In a metro with no homegrown bank you import a national firm the moment your deal gets serious; in Milwaukee you can keep it local much further up. Second, the boutique bench is unusually sector-fluent, because it grew up serving a maker economy — precision manufacturing, specialty chemicals and coatings, packaging and plastics, water technology, food and beverage, and industrial distribution — rather than a services or tech economy. Grace Matthews in coatings, TKO Miller in water and packaging: these are specialists, not generalists with a local address. Third, and this is the honest counter you must hold alongside the thesis: keeping it local with Baird still means hiring a national bank. The very-largest Milwaukee deals — Johnson Controls' $8.1B sale to Bosch is the clearest recent case — go to bulge-bracket advisors, and even Baird competes for those as a national player, not as a hometown favor. The "kept its bank" advantage is real, but it is an advantage of access, not of discount.

What happened to Marshall & Ilsley — and why does the BMO sale still shape Milwaukee deals?

To understand why Milwaukee's advisor market looks the way it does, you have to understand the bank it lost. Marshall & Ilsley was, for generations, the financial center of gravity in Wisconsin — the commercial bank where the state's manufacturers kept their operating accounts, drew their revolvers, and financed their expansions. When BMO acquired M&I in an all-stock transaction completed July 5, 2011, at roughly $4.1B, and folded it together with Harris Bank into BMO Harris Bank, the metro's lead commercial-banking relationship moved out of state for good. Today BMO Harris Bank is headquartered in Chicago, and BMO's capital-markets and investment-banking arm — BMO Capital Markets Corp. (CRD #16686) — is run primarily out of New York. So despite the deep M&I heritage that older Milwaukee owners still feel, BMO is not a local Milwaukee investment-banking option; treating it as one is a common mistake.

Why does a 2011 bank sale still shape how you sell a company in 2026? Because it clarifies what Milwaukee did and did not keep. A commercial bank and an investment bank do different jobs. The commercial bank lends against your balance sheet and runs your treasury; the investment bank sells your company. Milwaukee exported the first function and kept the second — which is exactly backwards from most industrial metros, and exactly why the advisor decision here is unusual. Your lending relationship may now sit with an out-of-state institution (BMO Harris, or one of the regionals and community banks that filled the gap), but your sell-side options are richer at home than almost anywhere in the Midwest.

There is a second, subtler lesson in the M&I story, and it is the one that recurs throughout this page: in Milwaukee, the firm you think you know may have quietly changed hands or names. M&I became BMO. Cleary Gull became CIBC's team. Schenck M&A Solutions became Taureau. The letterhead persists in memory long after the ownership changes underneath it. For a seller, that means the single most valuable habit is currency — verify the current entity, its current owner, and its current registration before you sign anything, rather than trusting the reputation a name carried a decade ago. The rest of this article is, in a sense, an exercise in exactly that verification.

Should I hire Robert W. Baird or a smaller Milwaukee boutique to sell my company?

This is Milwaukee's signature question — the fork few peer metros can even offer — so it deserves a real framework rather than a slogan. The short version: size, complexity, and buyer geography decide it, not loyalty.

Reach for Baird when your deal is big enough or complex enough that a global platform changes the outcome. Concretely, that usually means roughly $75M-$100M+ of enterprise value, a buyer universe that is national or global rather than regional, a competitive process where a top-12 M&A brand adds credibility with sophisticated counterparties, or a carve-out or cross-border angle that rewards a bank with offices and coverage bankers everywhere. Baird's industrials franchise is genuine and deep, its sponsor relationships are broad, and its league-table position (around #12 globally by M&A deal count in the first half of 2025) is not a vanity metric — it reflects the density of buyer relationships that manufactures competitive tension on a large process.

Reach for a smaller Milwaukee boutique — Grace Matthews, Taureau Group, TKO Miller, Bridgewood, Emory & Co., or CIBC Cleary Gull's local team — when your deal is in the ~$5M-$75M band and what you value most is senior attention. At a boutique, the managing director who pitched you is the person who runs your process, reads every buyer, and negotiates your LOI; at a national bank, a $30M deal is staffed accordingly and much of the day-to-day falls to junior bankers. For a founder-owned company where the sale is the defining financial event of a lifetime, that attention gap is worth real money — often more than any difference in buyer reach, because a good boutique with a focused buyer list can create just as much tension in the sub-$75M market as a bulge-bracket bank would.

The honest nuances that decide close calls: (1) Baird fishes higher up the curve, so on a genuinely small deal you may find its attention stretched — ask directly who will staff you and how often you will see the senior banker. (2) Sector fluency can trump platform size. If you make coatings, a Grace Matthews already knows your ten most likely strategic buyers by name; a generalist national bank has to go learn them. (3) The two are not mutually exclusive in spirit — the right test is the same for both: named senior staffing, three named recent closings in your sub-sector, and the actual buyers on the other side. Run Baird and your best boutique through the identical screen and let the answers decide. Price comes from competitive tension and preparation, not from the size of the logo on the engagement letter — a point I make in nearly every city, but which lands differently in the one metro where the local option is itself a national bank.

Baird Global Investment Banking vs Baird Private Wealth Management — which one actually sells my company?

This confusion trips up more Milwaukee owners than any other, and it is worth its own section because both businesses live inside the same legal entity — Robert W. Baird & Co. Incorporated, FINRA CRD #8158 — so checking the CRD alone will not tell them apart. The distinction is functional, not legal.

Baird Private Wealth Management is the retail side: financial advisors who manage individuals' and families' investment portfolios, retirement assets, and financial plans. If you have a Baird advisor today, this is almost certainly who you know. They are very good at what they do — but what they do is grow and protect capital, not run a competitive sale of an operating company. Baird Global Investment Banking is a different discipline entirely: sector-focused M&A bankers who prepare a company, build the CIM, run the auction, and negotiate the deal. When people say "Baird is a top-12 M&A bank," they mean this group, not the wealth advisors.

Why does the distinction matter to you? Because the pathway in is different. Walking into your local Baird wealth branch and asking to sell your $40M manufacturer will not, by itself, connect you to the investment bank; you (or your attorney or accountant) need to reach the investment-banking coverage team for your sector. And the reverse is the productive sequence most successful sellers run: the investment bank creates the liquidity by selling the company, and then a wealth manager — Baird's or anyone's — plans what happens to the proceeds. You want both functions, sequenced, not substituted.

There is a useful tell here for evaluating any advisor, not just Baird. Ask the person across the table a blunt question: "Will you be building a data room, running a buyer auction, and negotiating the purchase agreement — or are you managing the money afterward?" A wealth advisor will (honestly) describe the second; a deal banker will describe the first. The same either/or separates Northwestern Mutual's advisors, the wealth arms of every regional bank, and the RIAs from the firms that actually sell companies. Inside Baird the line runs through one CRD, which is precisely why you have to ask about function rather than firm.

Did Baird buy Cleary Gull — and is Cleary Gull still an independent Milwaukee investment bank?

No, and no — and getting this wrong is the most common single error on stale Milwaukee advisor lists, so let me be precise. Baird did not buy Cleary Gull. Cleary Gull's investment-banking business was acquired by CIBC (the Canadian Imperial Bank of Commerce), announced in 2019 and closed that year. Today those bankers operate as CIBC Cleary Gull, the Milwaukee-resident team of CIBC's US Middle Market Investment Banking group, transacting through CIBC World Markets Corp. (CRD #630) — a broker-dealer headquartered in New York, with Milwaukee as a branch office.

So Cleary Gull is no longer an independent Milwaukee investment bank. It is a national bank's middle-market team that happens to sit in Milwaukee — which is a genuine local presence and a real advantage (national balance sheet, national buyer relationships, resident senior bankers), but it is a different animal from the independent boutique that older directories describe. The old independent entity, Cleary Gull Inc. (CRD #45309), was terminated in 2019. Any list still presenting "Cleary Gull Inc." as an active, independent firm is describing something that no longer exists.

Why do so many sources get this wrong, and why does the Baird confusion in particular persist? Two reasons. First, Baird and the former Cleary Gull were both Milwaukee middle-market names for years, so memory blurs them. Second, the internet is full of pre-2019 content that was never updated. The correction matters practically: if you want the former Cleary Gull bankers, you should understand that you are hiring CIBC — with CIBC's fee structure, CIBC's conflict-check process, and CIBC's platform — not a small independent shop. That may be exactly right for your deal; just go in with clear eyes.

The generalizable discipline is the one this whole page keeps returning to: verify the current entity on FINRA BrokerCheck before you sign. For the former Cleary Gull, the registration you care about is CIBC World Markets Corp., CRD #630 — not the terminated CRD #45309, and certainly not Baird's CRD #8158. Currency is the whole game in a metro where three of the best-known names have changed hands or labels in the past several years.

Who advises the sale of a Milwaukee industrial, manufacturing, or specialty-chemicals company?

The short answer: Robert W. Baird for a broad industrial or precision-manufacturing sale, and Grace Matthews (via GM Securities, CRD #154657) for specialty chemicals, coatings, and materials science. This is Milwaukee's home turf, and the fit between the local bench and the local economy is almost suspiciously good. Southeast Wisconsin runs on making things — precision manufacturing (Rockwell Automation, Regal Rexnord, A.O. Smith, the Briggs & Stratton orbit), specialty chemicals and coatings, packaging and plastics, water technology, and industrial distribution — and the advisors here grew up serving exactly that economy.

For a broad industrial or precision-manufacturing sale, Robert W. Baird's global investment bank has a genuine industrials franchise, and it is headquartered here; for a large or global-buyer process, that combination of local presence and national reach is hard to beat. For specialty chemicals, coatings, and materials science specifically, the standout is Grace Matthews — a Milwaukee boutique founded in 1999 that has closed 150+ transactions in the vertical and executes through its affiliated broker-dealer GM Securities, LLC (CRD #154657). This is the clearest example on the page of a specialist that happens to be local rather than a local generalist: Grace Matthews' recent record includes advising Lindau Chemicals on its 2025 sale to South Coast Terminals and Diamond Vogel on the 2026 sale of certain architectural paint-store locations to JC Licht. Those are real, recent, in-vertical mandates — the kind of proof you should demand from any specialist.

For general lower-middle-market manufacturing and business services, the bench is deep: Taureau Group (closely-held and family-owned companies roughly $10M-$250M), TKO Miller (middle-market, with recent water-technology and packaging sell-sides), Bridgewood Advisors (registered, CRD #158400), and Emory & Co. (M&A plus a heavy valuation practice) all run credible processes for founder-owned industrials.

The rule that matters here is the fluency-over-address rule that governs the whole series, with a Milwaukee twist. In a concentrated vertical like coatings, specialty chemicals, or precision components, the specialist's buyer list beats the generalist's local address — because the specialist already knows, by name, the ten strategic acquirers and the handful of sector-focused sponsors who will actually pay a premium multiple, and has probably sold to several of them before. A local generalist has to go build that map from scratch during your process, on your clock. So the screening question for an industrial or chemicals sale is not "are you local?" (in Milwaukee, several good options are) but "show me your last three closings in my sub-sector, with the buyers named." For the national context on this category, our best industrial M&A advisors guide maps the specialist landscape beyond Wisconsin.

Who advises a Milwaukee packaging, water-technology, or food-and-beverage sale?

Beyond broad industrials, three sub-sectors — packaging and plastics, water technology, and food and beverage — deserve their own note, and the local bench has genuine, recent proof in each: TKO Miller in packaging and water technology, and Taureau Group across packaging and food and beverage.

Packaging and plastics. Milwaukee and its orbit host a dense cluster of packaging, converting, and plastics manufacturers, and this is one of TKO Miller's demonstrated lanes: its 2026 sell-sides include SÜDPACK's U.S. operations to PPC Flex — a clean example of a Wisconsin-based flexible-packaging asset trading to a strategic consolidator. Taureau Group also names packaging among its target sectors. The buyer universe for packaging is national and heavily sponsor-driven (packaging has been a private-equity roll-up favorite for a decade), so the advisor's job is to reach the platform buyers and the strategics who are actively consolidating — which, again, argues for demonstrated sector deal flow over a generic local relationship.

Water technology. Milwaukee has deliberately built itself into a global water-technology hub — the region's Water Council cluster anchors a concentration of water-treatment, metering, filtration, and flow-control companies, and marquee local names like A.O. Smith (water heating and treatment) sit at its center. The deal proof is current: TKO Miller advised on the 2026 sale of Complete Filtration Resources to Integrated Water Services, and A.O. Smith itself extended its water-temperature-control line by acquiring Leonard Valve Company for $470M (announced November 2025, closed January 2026). For a water-tech founder, the important nuance is that your best buyers are often strategics in adjacent water categories or specialist sponsors — a buyer set an advisor either knows or does not.

Food and beverage. Wisconsin's food-and-beverage economy is enormous (dairy, protein, ingredients, and a deep co-packing base), and Taureau Group names food and beverage among its core sectors. As in most metros, branded consumer and larger food assets tend to draw national consumer-specialist banks, while lower-middle-market food-and-beverage and ingredients companies are well served by the local bench provided it proves reach to the national strategic and sponsor buyers who dominate the category.

The through-line across all three: Milwaukee's economic identity (packaging, water, food) and its advisory market line up better than in most cities, but the buyers in every one of these categories are national. So the discipline is unchanged — hire the firm that can name and reach your actual buyers, and make any generalist prove it can.

What happened to Schenck M&A Solutions — and is Taureau Group the same team?

Same team, new name, new independence — and the confusion is compounded by a simultaneous accounting-firm merger, so let me untangle both threads. Taureau Group is the former Schenck M&A Solutions, the M&A practice that used to sit inside the Schenck accounting firm. Its managing directors, Ann Hanna and Corey Vanderpoel, bought out Schenck's stake and launched Taureau Group as an independent firm effective January 1, 2019. The deal team did not disappear; it became independent under a new name.

Here is the part that trips up stale lists. At almost the same time, Schenck's accounting practice merged into CLA (CliftonLarsonAllen). So two different things happened to "Schenck" in 2019: the M&A team spun out as Taureau Group, and the accountants joined CLA. Directories that half-remember the news sometimes report that "Schenck's M&A group went to CLA" — that is wrong. The M&A group is Taureau; CLA got the audit-and-tax practice. (And CLA's own investment bank, CLA Meridian Capital, is Seattle-based and joined CLA in April 2026 — it is not a Milwaukee M&A shop, a separate trap covered below.)

Today Taureau Group is a Milwaukee lower-middle-market M&A advisor focused on closely-held and family-owned companies roughly $10M-$250M in enterprise value, across manufacturing, business services, healthcare, food and beverage, and packaging — a sector list that maps neatly onto the region's maker economy and its founder-and-family ownership base. It is not a broker-dealer; securities are offered through Burch & Company, Inc. (member FINRA/SIPC, CRD #102280), a common and legitimate structure for M&A boutiques. As always, verify the model and understand which entity carries the securities work on a stock sale.

The lesson mirrors the Cleary Gull one: a well-known Milwaukee name changed form years ago, and the old label lingers in search results. If a "best Milwaukee M&A advisors" page still lists "Schenck M&A Solutions" as a going concern, it has not been updated since 2018 — which tells you something about the rest of its facts, too.

Is an ESOP a realistic exit for my Wisconsin company — and who advises one?

Yes — and in a maker economy full of multi-generational, closely-held manufacturers, the employee stock ownership plan deserves a serious look rather than a footnote. An ESOP is a genuine alternative exit, not a consolation prize, and Wisconsin's founder-and-family ownership base makes it a natural fit for owners who care about legacy and workforce as much as headline price.

The mechanics, honestly stated. An ESOP sells your stock to a trust for your employees at fair market value determined by an independent appraisal — not the strategic premium a competitive auction can clear, and that gap is the core tradeoff. In exchange, the structure offers real advantages: sellers of C-corp stock can defer capital gains under Section 1042 by rolling proceeds into qualified replacement securities; a company that becomes a 100% ESOP-owned S-corp pays no federal income tax, which is why the structure compounds so powerfully in stable, cash-generative manufacturing and services businesses; you control the timing and can sell in stages; and the company's identity, management, and workforce stay in place — no small thing for a founder who does not want to hand a lifetime's work to a distant strategic or a sponsor with a five-year clock.

The costs are real too. An independent trustee negotiates against you to protect the employees. The transaction stack — feasibility study, valuation, trustee counsel, plan design — runs into the low-to-mid six figures, though it is typically smaller in total than a success fee on the same company. And the company takes on an annual repurchase obligation to buy back departing employees' shares over time, which must be planned for. An ESOP is governance-heavy and permanent in a way an outright sale is not.

Who advises one: an ESOP transaction is a specialist discipline, so alongside a sell-side advisor you will engage ESOP-focused financial advisors and trustee-side counsel, and the trustee's independent appraiser matters as much as anyone. Several of Milwaukee's boutiques can help you weigh the ESOP against a market process, and a good advisor can run the two in parallel as a real market check — feasibility-testing the ESOP while quietly gauging strategic interest — so you make the legacy-versus-premium decision with actual numbers rather than a guess. Either way, the diligence is identical in kind: the trustee's appraiser wants the same clean financial picture and the same staged data room a strategic buyer would. If your priorities rank legacy, workforce, tax efficiency, and control of timing above the last dollar of headline price, feasibility-test an ESOP before — or alongside — running a full auction.

Are Milwaukee's big companies actually buyers right now — and does that help me sell?

Yes — the 2025-2026 record is unusually active for a metro this size, and reading it correctly tells you a lot about how deals actually get done here. Start with the headline, which is instructive precisely because it was a sale, not a purchase: Johnson Controls sold its Residential and Light Commercial HVAC business — plus its stake in the JCI-Hitachi joint venture — to Bosch for $8.1B, completed July 31, 2025. It was Bosch's largest-ever acquisition, generated roughly $5.0B of net cash for JCI, and funded a roughly $5.0B buyback. (A note on why JCI does not appear on lists of "Wisconsin's Fortune 500": its operational headquarters is in Glendale, in metro Milwaukee, but the company is legally domiciled in Cork, Ireland.)

On the buy-and-tuck-in side, the clearest recent example is A.O. Smith (Milwaukee), which acquired Leonard Valve Company for $470M — announced November 12, 2025, closed January 2026 — extending its water-temperature-control line. A.O. Smith itself, at roughly $3.9B in revenue, is a serial acquirer of water-technology assets even though it is not a Fortune 500 company.

The metro's actual Fortune 500 anchors are a genuine buyer engine in their own categories. Milwaukee's six Fortune 500 headquarters, by approximate rank: Northwestern Mutual (around #109), Fiserv (now headquartered downtown after relocating from Brookfield, around #215), ManpowerGroup (around #247), Kohl's (Menomonee Falls, around #289), WEC Energy Group (around #424), and Rockwell Automation (around #467). Rockwell in particular is a persistent acquirer of industrial-automation, software, and cybersecurity assets. Beyond the Fortune 500 sit large public acquirers like A.O. Smith, Harley-Davidson (around $5B in revenue), and Regal Rexnord (around $6B), plus private giants Kohler Co. and Briggs & Stratton (owned by KPS Capital Partners since 2020), and GE HealthCare, which is headquartered in Chicago but is consolidating its large Milwaukee-area operations into a Waukesha campus by 2026.

One clarification, because it is easy to misread: Harley-Davidson's most prominent recent news is strategic, not M&A. Artie Starrs was named president and CEO effective October 1, 2025 (succeeding Jochen Zeitz, amid pressure from activist H Partners, which held around 9%, and continued losses at the LiveWire electric unit). That is a leadership-and-strategy story, not a deal — do not let a stale list convert it into an "acquisition."

What it means for a seller: there is genuine in-region and strategic demand for industrial, water-technology, components, packaging, and services assets, and the local strategics are real buyers of tuck-ins in the size band this page covers. But the marquee-scale transactions flow to and from bulge-bracket banks, so your process still needs to prove national buyer reach — the local buyer next door is a bonus, not a strategy. Once buyers are in the room, page-level analytics will tell you which of them actually engaged past the teaser and which are just kicking tires.

Which national banks cover Milwaukee — and does any keep a real local office?

More than one does, which again separates Milwaukee from most Midwest metros. The verified 2026 picture:

- Robert W. Baird & Co. is the obvious answer and the whole point of this page: a national-caliber (top-~12 global) M&A bank headquartered in Milwaukee, with resident senior bankers, deep industrials coverage, and a global buyer network. For most purposes it is both the local option and the national one.

- CIBC Cleary Gull keeps a genuine Milwaukee team — CIBC's US Middle Market Investment Banking group, resident in Milwaukee, transacting through CIBC World Markets Corp. (CRD #630). This is a national bank with actual deal professionals living in the metro, focused on the middle market.

- The bulge-bracket and elite-boutique banks — Goldman Sachs, Morgan Stanley, and the like — cover Milwaukee from New York and Chicago and show up only on the largest mandates (the JCI-scale deals). They keep no Milwaukee M&A office, and for a founder-owned company they are neither reachable nor appropriate.

- The national middle-market specialists — William Blair, Lincoln International, Harris Williams, Houlihan Lokey, Jefferies, and their peers — cover Milwaukee primarily from Chicago and the coasts. They are the right call as deals scale past roughly $150M or into a specialist vertical with a global buyer set, and several have deep industrials and specialty-chemicals franchises that compete directly with Baird and Grace Matthews at the top of the local size range.

- Piper Sandler, headquartered up the road in Minneapolis, covers the Upper Midwest broadly and is strong in specific verticals, though I could not verify a dedicated Milwaukee M&A deal office — ask directly if it pitches you.

The practical rule mirrors the rest of the series, with the Milwaukee twist that the "local option" reaches unusually far up the size curve. For a founder-owned deal up to roughly $75M-$100M, the homegrown firms (Baird for larger and more complex, the boutiques for focused senior attention) give you as much as an imported bank would, closer to home. Past that, or in a specialist vertical where a particular national bank owns the buyer relationships, importing the specialist earns its fee. The test never changes: named buyers, named closings, named senior staffing — run the local and national options through the identical screen.

Is my Northwestern Mutual advisor able to sell my business — or do I need an investment bank?

You need an investment bank or a registered M&A advisor. Your Northwestern Mutual advisor manages wealth — and this mix-up matters more in Milwaukee than almost anywhere, because Northwestern Mutual is the metro's most famous financial brand and a Fortune 500 company (around #109), so owners understandably assume it does everything a financial institution could do. It does not sell operating companies.

Be precise about what Northwestern Mutual is. It is a life insurer and wealth manager — one of the largest mutual life insurers in the country, with an enormous financial-planning and investment-advisory business. Its investing arm, Northwestern Mutual Capital, does principal private debt and equity investing — meaning it deploys the company's own capital into deals as an investor, and might in principle sit on the buy side of a transaction — but it is not a sell-side M&A brokerage that will run a competitive auction to sell your business. Neither your NM financial advisor nor NM Capital is the firm that prepares your company, builds your CIM, runs your buyer process, and negotiates your purchase agreement.

The clean division of labor is the same one I drew for Baird's two halves: an investment bank or registered M&A advisor creates the liquidity by selling the company; a wealth manager plans what happens to the proceeds afterward. You want both, sequenced, not substituted. The sellers who get the sequence right — bank first to maximize the number, wealth manager second to steward it — walk into the wealth conversation with materially more to manage. Running it backwards (asking your wealth advisor to "help sell the business") leaves money on the table, because managing a portfolio and manufacturing competitive tension among strategic acquirers are simply different skills.

A telling early signal, from the document side where I sit: whether the "advisor" pitching you insists on a real, permissioned data room. Deal people build rooms — staged, watermarked, access-controlled — because that is how a competitive process is actually run and protected. Wealth managers email PDFs, because that is appropriate for what they do. If the person promising to "handle your sale" has never set up a data room, you are talking to the wrong kind of advisor for this job.

Which Milwaukee "financial" names are not M&A advisors? A do-not-claim list

Every metro has firms whose names get miscataloged as M&A advisors; Milwaukee has a particularly rich set because its most famous financial brands are an insurer and a departed bank. Here is the clearly-marked do-not-claim list — legitimate, often excellent firms, but the wrong number for selling your operating company.

- Northwestern Mutual — the metro's most famous financial brand and a Fortune 500 company (around #109), but a life insurer and wealth manager, not a sell-side M&A advisor. Its Northwestern Mutual Capital arm invests the firm's own capital as a principal; it does not broker the sale of your company. (Full treatment in the section above.)

- BMO — despite inheriting M&I in 2011, BMO is not a local Milwaukee investment-banking option. BMO Harris Bank is headquartered in Chicago (commercial and retail banking), and BMO Capital Markets Corp. (CRD #16686) — the investment bank — is run primarily out of New York. The M&I heritage is emotional history, not a local deal team.

- "The Bruce Company" — a Middleton, Wisconsin landscaping company. It is a real business with a similar-sounding name; it is not an M&A advisor. If a search surfaces it, it is a name trap.

- "Waterstone" — a name shared across banking, staffing, and RIA businesses, with no Milwaukee M&A broker-dealer behind it. There is no "Waterstone" investment bank running Milwaukee sell-sides; treat any such reference as a name confusion.

- CLA (CliftonLarsonAllen) — the accounting firm that absorbed Schenck's audit-and-tax practice in 2019. CLA is a major professional-services firm, but its investment bank, CLA Meridian Capital, is Seattle-based (it joined CLA in April 2026) — not a Milwaukee M&A shop. Do not confuse "the firm the Schenck accountants joined" with "a Milwaukee investment bank."

- The dead entities stale lists still cite — Cleary Gull Inc. (CRD #45309) was terminated in 2019 (the bankers are now CIBC's team), and Grace Matthews Investments LLC (CRD #103945) was terminated in 2003 (the active broker-dealer behind Grace Matthews is GM Securities, LLC, CRD #154657). Any list presenting either terminated CRD as an active firm is out of date — and, to repeat the correction that matters most: Baird did not buy Cleary Gull; CIBC did.

The point of the list is not to disparage anyone — most of these are fine institutions at what they actually do. The point is the sorting discipline. Before you take a firm's pitch as a sell-side advisor, confirm three things: that it is a registered broker-dealer (with a live CRD) or explicitly operates under the M&A-broker exemption; that it can name three recent closings with the buyers identified; and that a specific senior person will run your deal. Insurers, departed banks, accounting affiliates, and name-alikes will fail that test quickly.

How do I tell a real FINRA-registered investment bank from an M&A advisor under the broker exemption in Milwaukee?

Milwaukee's bench splits three ways, and knowing which group a firm belongs to is the foundation of hiring well. Start every evaluation at FINRA BrokerCheck.

-

Registered broker-dealers. These firms (or their affiliates) hold FINRA registrations and can handle securities transactions directly. In Milwaukee that includes Robert W. Baird & Co. (CRD #8158); GM Securities, LLC (CRD #154657), the broker-dealer behind Grace Matthews; CIBC World Markets Corp. (CRD #630), behind CIBC Cleary Gull; and Bridgewood Advisors (CRD #158400). The national and bulge-bracket banks are all registered as well.

-

Non-registered M&A advisors operating under the federal M&A-broker exemption. In 2023 Congress codified a federal exemption allowing qualified M&A brokers to facilitate the sale of privately held companies without full broker-dealer registration, subject to size and structure limits. This is a legitimate, common, and appropriate model for lower-middle-market private-company sales. In Milwaukee it includes Taureau Group (which offers securities through Burch & Company, CRD #102280 when a transaction needs it), TKO Miller, and Emory & Co. The exemption is not a red flag; it is a sensible fit for the deals these firms run. The one thing to confirm: for a stock sale (as opposed to an asset sale), ask exactly how the securities piece will be handled and through which entity.

-

Everyone who sounds like an advisor but is not one. Wealth managers (Northwestern Mutual), departed or out-of-market banks with no local M&A team (BMO Harris — investment bank in New York and Chicago), accounting affiliates whose banks sit elsewhere (CLA Meridian in Seattle), and name-alikes ("The Bruce Company," "Waterstone"). None of these runs a competitive sale of your company.

The clean, universal test for any firm across all three groups: ask for its CRD number (or an explicit statement that it operates as a non-registered M&A advisor under the exemption), three named recent closings with the buyers identified, and the senior person who will actually run your deal. A real advisor answers all three in one breath. And remember the Milwaukee-specific currency lesson: check the current record, because the three best-known local names all changed form in recent years — a directory written before 2019 will point you to firms that no longer exist as described.

How do I keep my sale confidential in Milwaukee's tight-knit manufacturing community?

You keep it confidential with staged disclosure — a blind teaser first, the named CIM only after an NDA, and the most sensitive material held for a short list — enforced by a permissioned data room. That discipline bites harder in Milwaukee than in a big anonymous market, because Southeast Wisconsin's manufacturing world is tight-knit: your competitors, your best customers, your key suppliers, and your top employees often know each other, sit on the same association boards, and drink at the same industry events. A leak that your company is "for sale" can spook a major customer, embolden a competitor to poach staff, or unsettle the workforce — all before you have a signed deal. So confidentiality is not paranoia here; it is process discipline.

The structural defense is staged disclosure, and a good advisor runs it as a matter of course:

- A blind teaser first. The initial one- or two-page marketing document describes the business — sector, size, financial profile, investment highlights — without naming it, so a recipient cannot identify the company (or realize it is their competitor down the road) from the teaser alone.

- The named CIM only after an NDA. The full confidential information memorandum, which does name the company and disclose real detail, goes only to buyers who have signed a non-disclosure agreement — and the advisor curates that list to exclude the parties most likely to misuse it.

- The most sensitive material held for a short list. Customer names, specific pricing, chemical formulations, employee rosters, and detailed contracts are released only to a small set of serious, later-stage bidders — never in the first wave.

The tooling has to enforce all of that, which is where the document side I work on comes in. A modern data room lets you run tiered access so strategics and financial buyers see different things; dynamic watermarking stamps each viewer's identity across every page so a leaked document is traceable to its source; screenshot protection raises the cost of casual copying; and page-level analytics show you exactly who opened what and when — so if a rumor starts, you have a record of who had access. In a vertical this concentrated, remember the rule from the industrial section: your buyer list is also your competitor list. Treat every disclosure as if it might reach a rival, because in Milwaukee manufacturing it plausibly could. I run Peony precisely to make this kind of staged, watermarked, permissioned release the default rather than a scramble.

Who handles sub-$5M Main-Street business sales in Milwaukee?

Below roughly $5M of enterprise value, you are generally in business-brokerage territory rather than investment-banking territory, and it is a legitimate, different market. Milwaukee and its suburbs support a deep bench of business brokers and franchise-network offices handling restaurants, trades, small distribution, service businesses, and owner-operator companies — listing-driven, weighted toward individual buyers, with lower absolute fees than a middle-market process. Emory & Co. and other boutiques on this page work down into the lower part of this range, but for a genuine Main-Street business a specialized broker is often the right fit.

Two Milwaukee-specific notes. First, the crossover zone — roughly $3M-$8M of enterprise value — rewards a second opinion. A company with $1M+ of real, defensible EBITDA and clean financials can often "graduate" from the individual-buyer market to a true competitive process at a boutique like Taureau, TKO Miller, or Emory, where strategic and private-equity tension routinely outbids the individual-buyer pool by more than the difference in fees. If you are near the top of the Main-Street band, get both kinds of firm to weigh in before you list.

Second, in this maker economy, even smaller manufacturers and industrial-services firms with a strong second layer of management can attract sponsor and strategic interest that a generic brokerage listing would never reach — because a search fund, an independent sponsor, or a strategic add-on buyer values a real management team and transferable operations, not just the owner's personal book of business. So the honest test is not your revenue but your transferability: if the business runs without you and the numbers hold up under scrutiny, you have likely outgrown the Main-Street model even at a modest size, and should act like it.

Is now a good time to sell my Milwaukee business?

The honest answer is that timing the macro matters less than your own readiness — but Milwaukee's 2026 conditions are genuinely favorable for a prepared industrial or manufacturing seller. The demand signals are real: strategic acquirers in the region and nationally are actively buying tuck-ins (A.O. Smith's $470M Leonard Valve deal is a clean recent example), private-equity platforms remain hungry for quality manufacturing, packaging, water-technology, and industrial-services assets, and the metro's Fortune 500 anchors (Rockwell especially) keep consolidating in their categories. The maker economy's fundamentals — durable niches, real assets, defensible margins — are exactly what sponsors and strategics pay up for when rates and financing conditions cooperate.

The counterweights are honest and worth naming. Financing costs still shape sponsor bids, so highly leveraged buyers are more disciplined than they were at the 2021 peak. Some industrial end-markets are cyclical, and a buyer will scrutinize where you sit in your cycle. And the very-largest local deals continue to flow to bulge-bracket banks (JCI's $8.1B Bosch sale), which is a reminder that scale changes the whole process, not just the advisor.

Net: for a prepared seller in industrials, specialty chemicals, packaging, water technology, food and beverage, or business services, this is a genuinely good window — the buyer engine is running and the local advisory bench is deep. For a seller whose financials need a year of cleanup, the window matters less than the cleanup, because unprepared financials cost more in a discounted price and a dragged-out process than any market timing gains you. The single biggest determinant of outcome is the same in every cycle: a defensible quality-of-earnings picture, an advisor who can name your actual best buyers, and a clean data room built before you go to market — the three things you control regardless of where rates go next.

What does an M&A advisor cost to sell a $30M Milwaukee company?

For a $30M Milwaukee company, expect a monthly retainer plus a success fee at close, with a 3-3.5% blended success fee squarely in the normal range. The most common structure is a Double Lehman scale — 10% of the first $1M of consideration, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $4M. Run that on $30M and the arithmetic is: $100K + $80K + $60K + $40K on the first $4M, then 2% of the remaining $26M ($520K), for about $800K — roughly 2.7%. Add the slice of retainer that is not credited back, plus any minimum-fee floor, and the effective blended rate usually lands near 3-3.5%. That tracks national middle-market data: a $30M deal sits in the band where independent fee studies put blended success fees around 3-4%, declining toward 1.5-2% by $100M and lower still on a $500M process (which is part of why the largest deals can economically support a bulge-bracket bank).

Retainers (work fees) run roughly $5,000-$25,000 per month at a boutique and are frequently credited against the success fee at closing — but only if the engagement letter says so in writing, so negotiate the credit explicitly rather than assuming it. Three terms deserve more attention than the headline percentage:

- The base the fee applies to. Is it total enterprise value (including assumed debt and earnouts) or just cash at close? On a deal with a meaningful earnout or rollover, this distinction is worth real money.

- The tail period. Banks often ask for 18-24 months, meaning they collect if you sell to an introduced buyer after the engagement ends. Negotiate toward 12 months and a tight, named buyer list.

- The minimum-fee floor. Many boutiques set a floor (say, $250K-$500K) that governs on smaller deals — reasonable, but know the number.

One comparison worth running: an ESOP swaps the success-fee model for a fixed stack of professional fees (feasibility, valuation, trustee counsel, plan design) that usually totals less than a success fee on the same company — in exchange for a fair-market-value price rather than an auction premium. Run both models on your actual numbers before anchoring on either. And keep the whole cost conversation in proportion: the fee delta between two good advisors is almost always dwarfed by the price delta a competitive process produces. I walk through the full fee math and the ESOP comparison in the FAQ below.

Which virtual data room should a Milwaukee seller actually use?

I run a data room company, so treat this as informed but interested — and I will be honest about where each tool fits. For a true $500M-plus mega-deal with hundreds of bidders and a bulge-bracket bank running the process, Datasite and Intralinks are the incumbents, and your banker may simply require one; their enterprise pricing typically starts around $50,000 or more per deal, which is rational at that scale and overkill below it. For the sub-$500M enterprise-value band that is the bulk of Milwaukee lower-middle-market deal count — which is to say almost every deal in this article — you do not need an enterprise mega-platform, and you should not pay for one. Peony, iDeals, and FirmRoom all run clean, secure, modern sell-side processes at a fraction of that cost.

What actually matters for a Milwaukee manufacturing or specialty-chemicals sale:

- Per-buyer permissions so strategics and financial buyers — and, in an ESOP, the trustee's advisors — see different tiers of information, staged as separate visitor groups in one room.

- Dynamic watermarking and screenshot protection so a leaked teaser or CIM is traceable — essential when your buyer list is your competitor list in a tight-knit industrial community.

- Page-level analytics so you can see which buyers genuinely engaged (and which never opened the CIM), which sharpens your advisor's follow-up and your read on real interest.

- Pricing that does not punish you per page or per gigabyte. Peony runs flat per-admin pricing (from $0 up to $52 per admin per month), so a document-heavy manufacturing diligence process does not inflate the bill.

We serve more than 5,900 customers, many running exactly the kind of founder-owned and family-business sales this article is about. If you want the full cost comparison across providers, our virtual data room cost guide breaks down the pricing models. Whatever you choose, set the room up before you go to market — it is the cheapest lever you control, and the one that most reliably compresses the back half of the timeline.

Bottom line

Milwaukee is the city that kept its investment bank. It sold its commercial-banking crown jewel — Marshall & Ilsley to BMO in 2011 — but employee-owned Robert W. Baird & Co. stayed independent and scaled into a top-~12 global M&A house headquartered on E. Wisconsin Avenue. For a founder, the practical consequence is a choice few peer metros can offer: hire the national-caliber bank in your backyard, or a focused local boutique that will run your deal personally — and the fork lands higher on the size curve here than anywhere in the Midwest. Beneath Baird sits an unusually deep, sector-fluent bench matched to the region's maker economy: Grace Matthews (specialty chemicals, via GM Securities, CRD #154657), CIBC Cleary Gull (CRD #630, the former Cleary Gull — acquired by CIBC, not Baird), Bridgewood Advisors (CRD #158400), and the honest non-registered boutiques Taureau Group (the former Schenck M&A Solutions), TKO Miller, and Emory & Co.

The honest counters, held alongside the thesis: Milwaukee's true mega-deals (Johnson Controls' $8.1B sale to Bosch) still fly to bulge-bracket banks, and "keeping it local" with Baird really means hiring a national bank that happens to be headquartered locally. Do not mistake the metro's most famous financial names for deal advisors — Northwestern Mutual is a life insurer and wealth manager, BMO's investment bank sits in New York and Chicago, and the name-alikes are traps. Verify every firm's current status on FINRA BrokerCheck, because the three best-known local names all changed form in recent years. An ESOP is a first-class exit for a Wisconsin manufacturer, not a consolation prize. And whichever path you choose, build a clean, staged data room before you go to market. In the one metro that kept its investment bank, the sellers who win are the ones who use that rare local access — and still make every advisor prove buyer reach, named closings, and senior attention before they sign.

Frequently asked questions about Milwaukee M&A advisors

Should I hire Robert W. Baird — the national bank in my backyard — or a smaller Milwaukee boutique to sell my company?

Hire Baird when your deal is large or complex enough to need a national platform's buyer reach and league-table credibility — roughly $75M-$100M+ of enterprise value, a broad global buyer universe, or a competitive dynamic that rewards a top-12 M&A brand. Hire a smaller Milwaukee boutique (Grace Matthews, Taureau, TKO Miller, Bridgewood, Emory & Co., or CIBC Cleary Gull's local team) when your deal is in the ~$5M-$75M band and you want the senior banker who pitched you to actually run the process. Milwaukee is one of the very few metros where this is a real choice: it kept its homegrown investment bank when it sold its commercial bank (M&I to BMO in 2011). The honest nuance — Baird fishes higher up the curve, so for a $30M founder sale a specialist boutique often gives more senior attention per dollar, while for a $150M carve-out Baird's platform earns its fee. Price comes from competitive tension, not a zip code. I run Peony, a data room company used by 5,900+ customers, and either way a clean, staged room with page-level analytics is the cheapest lever you control before you pick the banker.

I own a ~$30M Milwaukee-area manufacturing company — who are the best M&A advisors for a lower-middle-market sale?

For a ~$30M Southeast-Wisconsin manufacturing sale, the shortlist is deeper than most Midwest metros. Registered broker-dealers: Robert W. Baird & Co. (CRD #8158, the homegrown national flagship, though it fishes higher up the curve); Grace Matthews (specialty-chemicals and coatings specialist, via its affiliated broker-dealer GM Securities, CRD #154657); CIBC Cleary Gull (CIBC's Milwaukee middle-market team, CRD #630); and Bridgewood Advisors (CRD #158400). Non-registered M&A advisors under the federal M&A-broker exemption: Taureau Group (the former Schenck M&A Solutions, closely-held and family-owned companies roughly $10M-$250M), TKO Miller (recent water- and packaging-sector sell-sides), and Emory & Co. (M&A plus a heavy valuation practice). Verify the split — Baird, GM Securities, CIBC World Markets, and Bridgewood are registered; Taureau, TKO Miller, and Emory operate under the exemption — and structure a securities sale accordingly. The screening test: ask each firm for its last three closings in your sub-sector with the buyers named. We serve 5,900+ customers on the data-room side of exactly these deals.

Did Baird buy Cleary Gull, and is Cleary Gull still an independent Milwaukee investment bank?

No on both counts — this is the most common Milwaukee mistake in stale directories. Baird did not buy Cleary Gull. Cleary Gull's investment-banking business was acquired by CIBC (announced and closed in 2019) and today operates as CIBC Cleary Gull, the Milwaukee-resident team of CIBC's US Middle Market Investment Banking group, transacting through CIBC World Markets Corp. (CRD #630, headquartered in New York, Milwaukee a branch). So Cleary Gull is no longer an independent Milwaukee investment bank; it is a national bank's middle-market team that happens to sit in Milwaukee. The old independent entity, Cleary Gull Inc. (CRD #45309), was terminated in 2019 — any list presenting it as active is out of date. If you want the former Cleary Gull bankers, you are hiring CIBC; and if a directory says "Baird acquired Cleary Gull," it is simply wrong. Verify the current entity on FINRA BrokerCheck before you sign: the registration that matters is CIBC World Markets Corp., CRD #630.

Who advises the sale of a Milwaukee industrial, manufacturing, or specialty-chemicals company?

This is Milwaukee's home turf. For a broad industrial or precision-manufacturing sale, Robert W. Baird's global investment bank has a genuine industrials franchise and is headquartered here. For specialty chemicals, coatings, and materials science specifically, Grace Matthews is the national specialist that happens to be local — a Milwaukee boutique (founded 1999, 150+ transactions) executing through GM Securities (CRD #154657), with recent deals including Lindau Chemicals to South Coast Terminals (2025) and Diamond Vogel's architectural paint-store locations to JC Licht (2026). For general lower-middle-market manufacturing and business services, Taureau Group, TKO Miller, and Bridgewood Advisors all run credible processes. The rule: in a concentrated vertical like coatings, sector fluency and a specialist's buyer list beat a generalist's local address — the specialist already knows the ten strategics who will pay up. See our best industrial M&A advisors guide for the national view. I run Peony, a data room company used by 5,900+ customers, and in a tight vertical dynamic watermarking matters because your buyer list is also your competitor list.

Is my Northwestern Mutual advisor able to sell my business, or do I need an investment bank?

You need an investment bank or a registered M&A advisor — your Northwestern Mutual advisor manages wealth. The mix-up matters more in Milwaukee than almost anywhere, because Northwestern Mutual is the metro's most famous financial brand and a Fortune 500 company (around #109), so owners assume it does everything financial. It does not sell operating companies. Northwestern Mutual is a life insurer and wealth manager; its investing arm, Northwestern Mutual Capital, does principal private debt and equity investing — it may be an investor on the other side of a deal — not sell-side M&A brokerage for your business. The clean division of labor: an investment bank or registered M&A advisor runs the competitive process that sells the company; your wealth manager plans what happens to the proceeds. Sequence, don't substitute — the sellers who get it right walk into the wealth conversation with a bigger number. I run Peony, a data room company, and a telling early signal is whether the "advisor" insists on a real, permissioned data room: wealth managers email PDFs; deal people build rooms.

What happened to Schenck M&A Solutions — is Taureau Group the same team?

Same team, new name, new independence. Taureau Group is the former Schenck M&A Solutions — the M&A practice inside the Schenck accounting firm. Managing directors Ann Hanna and Corey Vanderpoel bought out Schenck's stake and launched Taureau Group as an independent firm effective January 1, 2019. Separately and around the same time, Schenck's accounting practice merged into CLA (CliftonLarsonAllen) — which is why stale lists conflate the two: the M&A team went to Taureau, the accountants went to CLA. Today Taureau is a Milwaukee lower-middle-market M&A advisor focused on closely-held and family-owned companies roughly $10M-$250M across manufacturing, business services, healthcare, food and beverage, and packaging. It is not a broker-dealer; securities are offered through Burch & Company, Inc. (member FINRA/SIPC, CRD #102280) — a common structure, but verify it and know which entity carries the securities work. If a directory still lists "Schenck M&A Solutions," it is describing a firm that renamed more than seven years ago.

How do I tell a real FINRA-registered investment bank from an M&A advisor operating under the broker exemption in Milwaukee?

Start at FINRA BrokerCheck and sort the bench into three groups. Registered broker-dealers: Robert W. Baird & Co. (CRD #8158), GM Securities — behind Grace Matthews (CRD #154657), CIBC World Markets Corp. — behind CIBC Cleary Gull (CRD #630), and Bridgewood Advisors (CRD #158400). Non-registered M&A advisors under the federal M&A-broker exemption (codified in 2023 for private-company sales, subject to size and structure limits): Taureau Group (securities through Burch & Company, CRD #102280), TKO Miller, and Emory & Co. Both models are legitimate; the exemption is common and appropriate, but for a stock deal confirm how the securities piece is handled and through which entity. The third group is everyone who sounds like an advisor but is not: wealth managers (Northwestern Mutual), banks with no local M&A team (BMO Harris — its investment bank is in New York and Chicago), and name-alikes ("The Bruce Company," "Waterstone"). The clean test for any firm: its CRD (or an explicit non-registered statement), three named recent closings with buyers identified, and the senior person who will run your deal. If a firm cannot answer all three crisply, that is your answer.

Are Milwaukee's big companies actually buyers right now, and does that help me sell?

Yes, and the 2025-2026 record is unusually active — though the headline deal shows how the market really works. The biggest was a sale, not a purchase: Johnson Controls sold its Residential and Light Commercial HVAC business (and its stake in the JCI-Hitachi JV) to Bosch for $8.1B, completed July 31, 2025 — Bosch's largest-ever acquisition, funding a roughly $5.0B buyback at JCI. On the buy-and-tuck-in side, A.O. Smith (Milwaukee) acquired Leonard Valve Company for $470M (announced November 2025, closed January 2026). The metro's Fortune 500 anchors — Northwestern Mutual, Fiserv (now downtown), ManpowerGroup, Kohl's, WEC Energy Group, and Rockwell Automation — are active acquirers, and Rockwell in particular is a serial buyer of automation and software assets. (Harley-Davidson's news was strategic, not M&A: Artie Starrs became CEO effective October 1, 2025.) For a seller, that means genuine strategic demand for industrial, water-technology, components, and services assets — but the marquee deals go to bulge-bracket banks, so your process still needs national reach. I run Peony, a data room company, and page-level analytics will tell you which buyers actually engaged past the teaser.

How does a sell-side M&A process work for a Milwaukee company, and how long does it take from advisor hire to close?

Five overlapping stages, typically 6-9 months from engagement letter to close, longer if the financials need cleanup: 4-8 weeks of preparation (clean financials, a quality-of-earnings build, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA from a blind teaser; 3-5 weeks collecting indications of interest and building a short list; 4-6 weeks of management meetings and the lead-bid/LOI stage; then 8-12 weeks of confirmatory diligence and definitive-agreement negotiation. The advisor's job throughout is to manufacture competitive tension across strategic buyers and private-equity platforms — and for a Southeast-Wisconsin manufacturer that means proving reach to the national and often global strategics who buy precision components, coatings, packaging, and water technology, not just the regional buyer down the road. An ESOP alternative runs 4-6 months of feasibility, valuation, and trustee negotiation. The biggest timeline risk is unprepared financials. I run Peony, a data room company, and a clean, staged data room built before launch is the most reliable way to compress the back half.

What do buyers diligence, and how do I set up a data room before going to market with my Milwaukee company?

Buyers diligence durable, transferable cash flow — normalized EBITDA quality, customer concentration, margin trend, working capital, contract assignability — plus the sector layer that defines this maker economy: backlog, equipment, capacity, and skilled-labor retention for manufacturers; formulations, EHS and environmental compliance, and TSCA standing for specialty-chemicals and coatings makers; certifications, co-packer and supply agreements, and food-safety records for packaging and food-and-beverage; IP and product certifications for water technology. Build the room around eight workstreams: financial (3-5 years plus a quality-of-earnings build), corporate/legal, commercial, operations/technical, HR, IP and IT, tax, and insurance/compliance. The two documents that do the most work: a defensible quality-of-earnings file and the CIM. Protect yourself with staged disclosure — blind teaser, NDA-gated CIM, sensitive material (customer names, pricing, formulations) held for the short list. I run Peony, a data room company used by 5,900+ customers, built for exactly this tiered, watermarked release — stage strategics and sponsors as separate visitor groups in one room.

What does an M&A advisor cost to sell a $30M Milwaukee company — is a 3 to 3.5% success fee normal, and how does Double Lehman plus a retainer work?

A 3-3.5% blended success fee is squarely normal for a $30M sale: Double Lehman (10/8/6/4% of the first four $1M increments, 2% above $4M) computes to about $800K (~2.7%) on $30M, landing near 3-3.5% once minimums and uncredited retainer are added. That tracks national data — blended success fees run around 3-4% at $30M, declining toward 1.5-2% by $100M and lower on a $500M process. Retainers run $5,000-$25,000/month at a boutique and are often credited against the success fee — but only if the engagement letter says so in writing. Watch the fee base (enterprise value including debt and earnouts vs cash at close), the tail (cap at 12 months vs the 18-24 asked), and any minimum floor. An ESOP swaps the success-fee model for a fixed professional-fee stack that usually totals less — in exchange for fair market value rather than an auction premium; run both on your numbers. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — predictable against a six-figure advisory fee.

Related resources

- The State of M&A Data Rooms — our platform benchmark on how sell-side processes actually run, across hundreds of deals in the sub-$500M band that covers most of Milwaukee.

- How to Build an M&A Data Room — the staged-disclosure playbook every Milwaukee seller should run before going to market.

- How to Write a CIM — the confidential information memorandum your advisor builds after the blind teaser.

- Best Industrial M&A Advisors — the national sector view for Milwaukee's manufacturing, specialty-chemicals, and industrial-services sellers.

- Best M&A Advisors in Chicago — where William Blair, Lincoln International, and much of the national middle-market coverage of Milwaukee deals is headquartered.

- Best M&A Advisors in Minneapolis — the Upper Midwest neighbor and Piper Sandler's headquarters town.

- Best M&A Advisors in St. Louis — the other Midwest metro that grew and kept a homegrown national bank (Stifel); the closest peer to Milwaukee's "kept its bank" story.

- Best M&A Advisors in Kansas City — the Ownership Town, where no homegrown investment bank ever scaled — the structural contrast to Milwaukee.

- Virtual Data Room Cost Guide — the full pricing comparison across providers for a sub-$500M sell-side.

Footnotes and sources

- FINRA BrokerCheck (brokercheck.finra.org) — verified entity registrations and CRD numbers: Robert W. Baird & Co. Incorporated (CRD #8158, active; formed in Wisconsin 12/29/1919; employee-owned; contains both Baird Global Investment Banking and Baird Private Wealth Management); GM Securities, LLC (CRD #154657, active — the registered broker-dealer affiliated with Grace Matthews, 833 E. Michigan St, Milwaukee); CIBC World Markets Corp. (CRD #630, active — the broker-dealer behind CIBC Cleary Gull; New York HQ, Milwaukee branch); Bridgewood Advisors Inc. (CRD #158400, active; 111 E. Wisconsin Ave, Milwaukee; formed 2011); Burch & Company, Inc. (member FINRA/SIPC, CRD #102280 — the broker-dealer through which Taureau Group offers securities); BMO Capital Markets Corp. (CRD #16686, New York). Terminated entities: Cleary Gull Inc. (CRD #45309, terminated 2019); Grace Matthews Investments LLC (CRD #103945, terminated 2003). Taureau Group, TKO Miller, and Emory & Co. return no broker-dealer firm records (consistent with the federal M&A-broker exemption).

- Robert W. Baird & Co. — firm disclosures: roughly 5,300+ associates and about $525B in client assets (2025); global investment-banking M&A practice ranked approximately #12 worldwide by number of deals in the first half of 2025 (58 M&A deals; per ION Analytics/Mergermarket league tables). Headquartered at 777 E. Wisconsin Avenue, Milwaukee.

- Marshall & Ilsley / BMO — BMO (Bank of Montreal) acquisition of Marshall & Ilsley completed July 5, 2011 (all-stock, approximately $4.1B); M&I merged with Harris Bank to form BMO Harris Bank (Chicago HQ). BMO Harris Bank commercial and retail banking run from Chicago; BMO Capital Markets Corp. (CRD #16686) investment bank run primarily from New York.

- Grace Matthews / GM Securities — Milwaukee specialty-chemicals, coatings, and materials-science M&A boutique (founded 1999; 150+ transactions), executing through GM Securities, LLC (CRD #154657). Recent transactions: advised Lindau Chemicals on its sale to South Coast Terminals (August 2025); advised Diamond Vogel on the sale of certain architectural paint-store locations to JC Licht (May 2026).

- CIBC Cleary Gull — CIBC's US Middle Market Investment Banking team, resident in Milwaukee, operating under CIBC World Markets Corp. (CRD #630). Formerly the independent Cleary Gull, whose investment-banking business was acquired by CIBC (announced 2019, closed Q4 2019). Baird did not acquire Cleary Gull.

- Taureau Group — the former Schenck M&A Solutions; managing directors Ann Hanna and Corey Vanderpoel bought out Schenck's stake and launched Taureau Group as an independent firm effective January 1, 2019; lower-middle-market focus (roughly $10M-$250M; closely-held and family-owned; manufacturing, business services, healthcare, food and beverage, packaging); securities offered through Burch & Company, Inc. (CRD #102280). Schenck's accounting practice separately merged into CLA (CliftonLarsonAllen) in 2019; CLA's investment bank, CLA Meridian Capital, is Seattle-based (joined CLA April 2026).

- TKO Miller — Milwaukee middle-market M&A firm (founded 2016; led by Tammie Miller); recent sell-sides: Complete Filtration Resources to Integrated Water Services (2026); SÜDPACK U.S. operations to PPC Flex (2026). Not a registered broker-dealer.

- Emory & Co. — Milwaukee M&A firm (formed 1999) with a heavy valuation practice (135+ transactions; 1,400+ valuation projects). Not a registered broker-dealer.

- Buyer engine and deal record — Johnson Controls sale of its Residential and Light Commercial HVAC business and JCI-Hitachi JV stake to Bosch ($8.1B, completed July 31, 2025; Bosch's largest-ever acquisition; approximately $5.0B net cash; funded a roughly $5.0B buyback; JCI operational HQ Glendale/Milwaukee, legally domiciled Cork, Ireland). A.O. Smith acquisition of Leonard Valve Company ($470M; announced November 12, 2025; closed January 2026). Harley-Davidson: Artie Starrs named president and CEO effective October 1, 2025 (succeeding Jochen Zeitz; activist H Partners held approximately 9%) — a leadership/strategy development, not an M&A transaction. Historical context (older, not within the ≤12-month window): Kohler Energy to Platinum Equity (closed May 6, 2024; rebranded Rehlko, September 2024); Regal Rexnord Industrial Motors and Generators business to WEG ($400M; closed April 30, 2024; Guggenheim advised); Briggs & Stratton to KPS Capital Partners out of Chapter 11 (2020).

- Fortune 500 in metro Milwaukee (approximate ranks, most recent list): Northwestern Mutual (around #109; life insurer and wealth manager — Northwestern Mutual Capital does principal private investing, not M&A brokerage); Fiserv (around #215; HQ relocated to downtown Milwaukee from Brookfield, opened 2024); ManpowerGroup (around #247); Kohl's (Menomonee Falls, around #289); WEC Energy Group (around #424); Rockwell Automation (around #467). Not Fortune 500: A.O. Smith (approximately $3.9B revenue), Harley-Davidson (approximately $5B), Regal Rexnord (approximately $6B). Private giants: Kohler Co. (Kohler, WI); Briggs & Stratton (KPS-owned since 2020). GE HealthCare: headquartered in Chicago, consolidating Milwaukee/Wauwatosa operations into a Waukesha campus by 2026.

- Fee benchmarks — Double Lehman scale (10/8/6/4/2%) and lower-middle-market blended success-fee ranges (approximately 3-4% at $30M, declining toward 1.5-2% by $100M) per independent middle-market fee studies; retainers approximately $5,000-$25,000/month at boutiques, frequently credited against the success fee. ESOP mechanics — Section 1042 capital-gains deferral for C-corp sellers; federal income-tax exemption for 100% ESOP-owned S-corps; independent trustee, independent valuation, and annual repurchase obligation.

This article reflects my views as of July 2026 and is informational, not legal, tax, or investment advice. Firm registrations, names, and ownership change — in this metro, Marshall & Ilsley became BMO, Cleary Gull became CIBC's team, and Schenck M&A Solutions became Taureau Group — so verify current status on FINRA BrokerCheck before engaging any advisor. I am the co-founder of Peony, a data room company; where I mention Peony I have flagged the interest.