10 Best M&A Advisors in St. Louis for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

10 Best M&A Advisors in St. Louis for $5M-$300M Deals (2026)

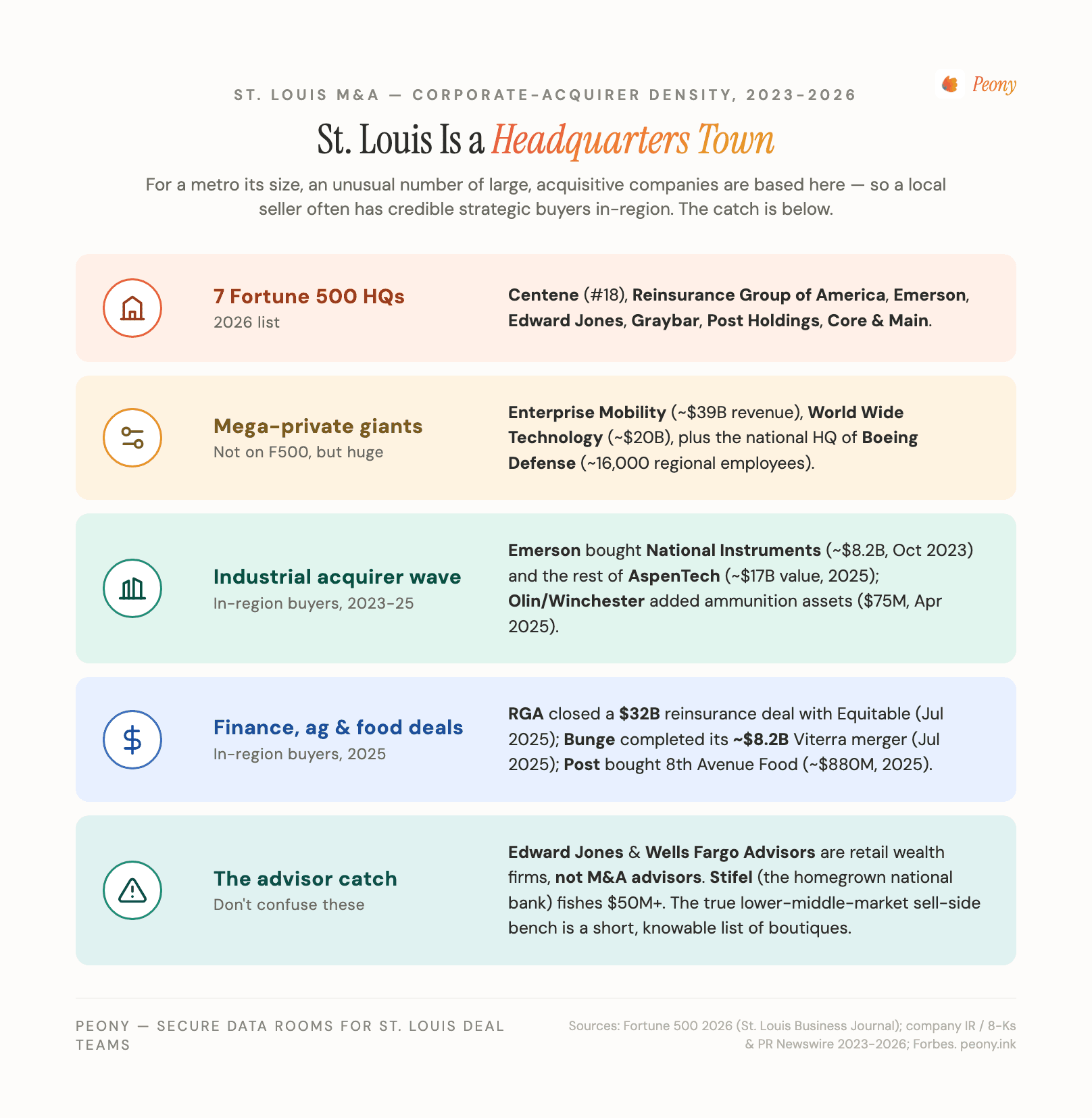

Quick answer: After sitting on the document side of enough Midwest sell-side processes, here is the 10-firm St. Louis shortlist for 2026 — and the framing most lists miss. St. Louis is the opposite of a thin-advisor metro: it is a Headquarters Town. Seven Fortune 500 companies are headquartered here on the 2026 list (Centene, Reinsurance Group of America, Emerson, Edward Jones, Graybar, Post Holdings, Core & Main) (St. Louis Business Journal via Fox2Now, June 2026), two of America's largest private companies call it home (Enterprise Mobility ~$39B; World Wide Technology ~$20B), and it is the headquarters of Boeing Defense — so a local seller often has credible strategic buyers 20 minutes away. It is also home to a genuine national investment bank: Stifel (Stifel, Nicolaus & Company, FINRA CRD #793). The catch: the two financial brands everyone in St. Louis knows — Edward Jones and Wells Fargo Advisors — are retail wealth firms, not corporate M&A advisors, and the true lower-middle-market sell-side bench is a short, knowable list of boutiques: Benjamin F. Edwards (its own broker-dealer, CRD #146936; Surdex → Bowman, $44M, closed April 4, 2024), Nolan & Associates (founded 1976; affiliate BD Middle Market Transactions, CRD #133062), R.L. Hulett (Clayton, founded 1981, 275+ deals), and The Fortune Group (its own subsidiary broker-dealer, FG Capital LC, CRD #125229) — each with its own or an affiliated FINRA broker-dealer. The signature frame below — the Corporate-Acquirer Density Map — explains how a 2023-2026 wave of in-region acquisitions (Emerson–NI $8.2B; RGA–Equitable $32B reinsurance; Bunge–Viterra ~$8.2B; Post–8th Avenue ~$880M) shapes which advisor wins which deal.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led exits, family-business successions, PE recapitalizations, and strategic carve-outs — and St. Louis is the entry in our M&A advisor series where the story most lists tell and the story a seller actually needs diverge in an unusual way. Most "best St. Louis M&A advisors" pages either pad the list with wealth managers who do not run sell-side deals, or they default to the national-bank names without telling you which ones keep a real deal team in town. At Peony we now serve more than 6,800 customers, and St. Louis sits right in the heart of the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark.

Here is the thesis I want you to internalize before you read another word: St. Louis is a Headquarters Town. For a metro its size, it punches far above its weight in large-company headquarters — seven Fortune 500 companies on the 2026 list, two of the largest private companies in the United States (Enterprise Mobility and World Wide Technology), the national headquarters of Boeing Defense, and a deep agtech and plant-science cluster anchored by Bayer Crop Science and the Donald Danforth Plant Science Center. That density is a genuine advantage for a seller, because so many credible strategic acquirers — Emerson, Post Holdings, Graybar, Core & Main, Olin, Spire — are headquartered right here and have been actively buying. Your best buyer might be twenty minutes up the road.

But two things follow that most lists get wrong. First, St. Louis is also a national center of retail financial advice — Edward Jones and Wells Fargo Advisors are both headquartered here, along with a deep bench of wealth RIAs (Moneta, Plancorp, Matter Family Office) — and none of those is a corporate sell-side M&A advisor. The wealth giant you already know is the wrong firm to sell your company. Second, the city does have a genuine homegrown national investment bank in Stifel, but Stifel's institutional M&A group fishes mostly at $50M and up (its bank-M&A arm, KBW, is a different and dominant story). For the $5M-$75M founder-owned business that is the heart of this market, the right lead is usually one of a short, knowable list of local boutiques — and a recurring detail you should know going in is that several of them transact through a hosted, third-party FINRA broker-dealer rather than their own. That is fine; it just needs to be verified.

This post is the working playbook I would hand to a St. Louis manufacturer or distributor weighing a sale, a family-owned food or consumer business fielding inbound interest, an agtech founder near the 39 North district, a Boeing-orbit defense supplier, or a Missouri community bank considering strategic alternatives. The frames — the Headquarters Town, the Corporate-Acquirer Density Map, the Stifel Gap, the hosted-broker-dealer reality, and the wealth-giant sorting test — come from cross-referencing the verified 2023-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in St. Louis right now for $5M-$300M deals?

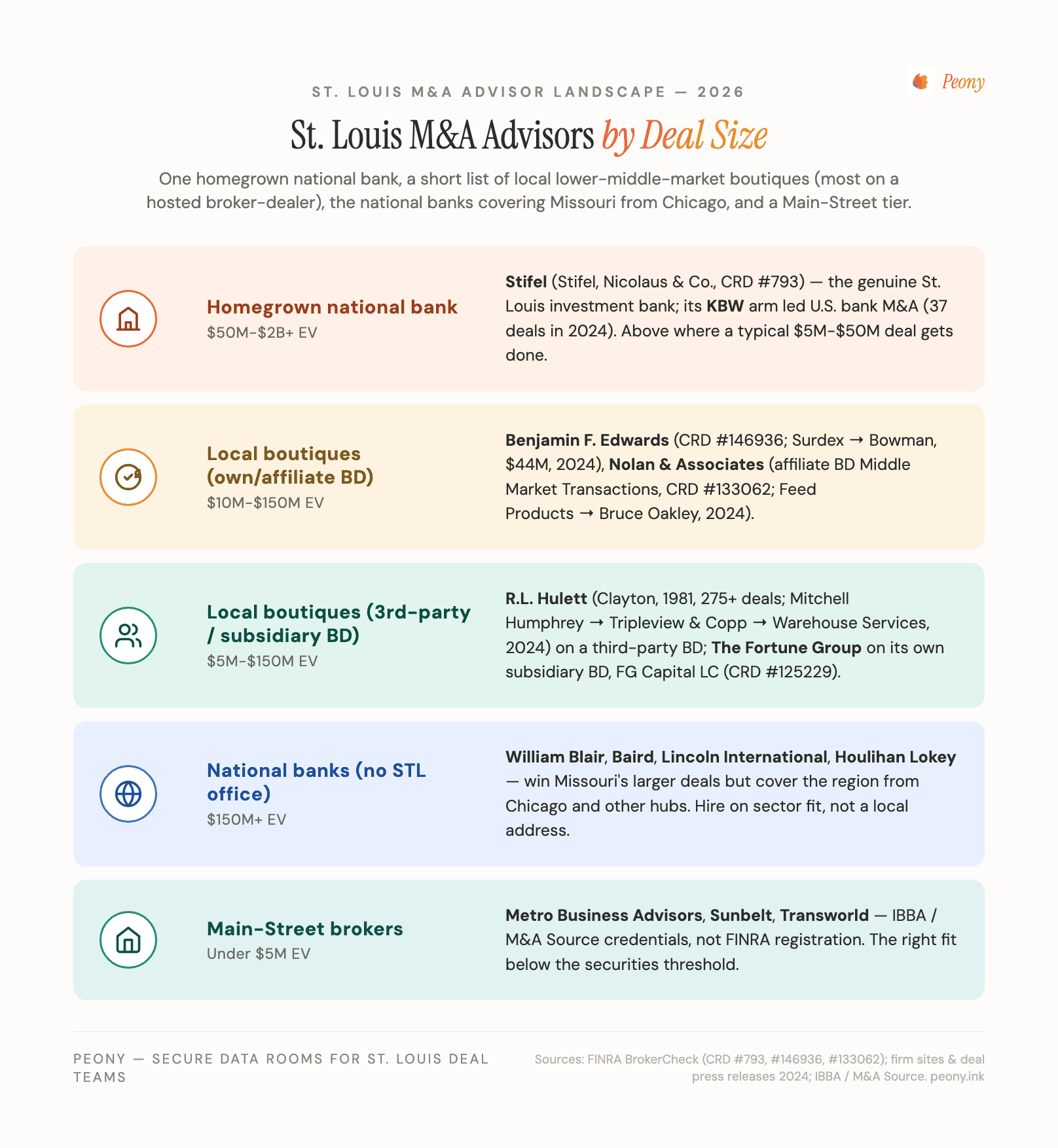

The St. Louis-metro shortlist for 2026, sorted by tier and deal-size band — with the honesty banner up front: the homegrown bench splits into one genuine national bank (Stifel, which engages higher up the size curve), a short list of local lower-middle-market boutiques, and a Main-Street broker tier, while the national middle-market banks cover Missouri from out of town.

| Firm | HQ / St. Louis presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| Stifel ★ (homegrown national) | Downtown St. Louis (since 1890) | $50M-$2B+ EV | Mid/upper-middle-market; financial-institution M&A via KBW | Own FINRA broker-dealer (Stifel, Nicolaus, CRD #793) |

| Benjamin F. Edwards & Company | St. Louis | $10M-$100M+ EV | Middle-market sell-side & capital raising | Own FINRA broker-dealer (CRD #146936) |

| Nolan & Associates | St. Louis (founded 1976) | $10M-$150M EV | Building products, transport, industrial, business services | Affiliate BD Middle Market Transactions (CRD #133062) |

| R.L. Hulett & Company | Clayton, MO (founded 1981) | $10M-$150M EV | Generalist middle-market; 275+ deals over 40 years | Uses a third-party FINRA broker-dealer (not its own) |

| The Fortune Group | St. Louis (founded 1987) | $5M-$50M EV | Lower-middle-market generalist | Own BD via subsidiary FG Capital LC (CRD #125229) |

| Forvis Mazars (transaction advisory) | St. Louis office (national HQ) | $10M-$150M EV | Accounting-firm transaction advisory & investment banking | National firm; transaction-advisory practice |

| William Blair | Chicago HQ — covers Missouri, no STL deal office | $150M-$1B+ EV | National middle-market for larger/institutional processes | Established FINRA broker-dealer |

| Robert W. Baird | Milwaukee HQ — covers Missouri, no STL deal office | $75M-$1B+ EV | Employee-owned middle-market, industrials & consumer | Established FINRA broker-dealer |

| Lincoln International | Chicago HQ — covers Missouri, no STL deal office | $75M-$1B+ EV | Global mid-market sell-side & private capital | Established FINRA broker-dealer |

| Metro Business Advisors | St. Louis | Under $5M EV | Main-Street → lower-LMM business brokerage (up to ~$20M rev) | Business broker (IBBA / M&A Source — not a FINRA BD) |

A few notes the table cannot carry. Stifel is the headline name — the genuine homegrown national investment bank, and the reason a St. Louis seller of real scale is not automatically forced to ship the mandate to Chicago or New York — but its institutional M&A group realistically engages at $50M+, so it is not a peer of the lower-middle-market boutiques for a typical founder-owned deal. Benjamin F. Edwards is the standout genuinely-local boutique — its own FINRA broker-dealer (CRD #146936) and a clean, recent, in-band closing to point to (Surdex → Bowman, $44M, April 2024). Nolan & Associates (affiliate BD Middle Market Transactions, CRD #133062) and R.L. Hulett (a third-party FINRA broker-dealer, 275+ deals over 40 years, with named 2023-2026 closings including Mitchell Humphrey → Tripleview, October 2024, and Copp → Warehouse Services, 2024) are the two other local boutiques with verifiable recent, named transactions. The Fortune Group transacts through its own subsidiary broker-dealer, FG Capital LC (FINRA CRD #125229) — a real regulatory credential, though I could not verify a 2023-2026 named closing for it this pass. Forvis Mazars is a national accounting firm with a St. Louis office and a transaction-advisory/investment-banking practice — useful, but not a homegrown boutique. William Blair, Robert W. Baird, and Lincoln International are the national middle-market banks (along with Houlihan Lokey) that win Missouri's larger deals but cover the region from out of town with no deal-executing St. Louis M&A office that I could confirm.

A note on what I left off the ranked list, and why — because the honest version of a "best advisors" page should say what it could not stand behind. Two long-operating local names, Clayton Capital Partners (founded 2001) and The Douglas Group (founded 1991), are genuinely in the St. Louis market, but I could not verify either a FINRA broker-dealer or a named, dated recent transaction for them from a primary source this pass, so I have not ranked them. That is not an accusation — many legitimate lower-middle-market advisors run asset sales that never produce a public tombstone — but it is the line between "verified" and "take it on faith," and a buyer's guide should keep that line visible. If you are considering either, ask directly for their broker-dealer registration and three named recent closings with buyers, exactly as you would for any firm on this page.

And the critical honesty point on the famous local names: Edward Jones, Wells Fargo Advisors, Moneta Group, Plancorp, and Matter Family Office are wealth-management and retail-brokerage firms, not corporate M&A advisors — more on that sorting test below.

Is there actually a homegrown St. Louis investment bank, and is Stifel too big for my deal?

Yes — St. Louis has a genuine, homegrown, nationally significant investment bank in Stifel, and that is unusual for a metro this size. The honest nuance is about fit: Stifel is the right call for a $50M+ sale or for any bank or specialty-finance company, but for a sub-$50M non-financial business it usually sits above where the deal gets done.

Stifel Financial Corp. (NYSE: SF) has been headquartered in downtown St. Louis since 1890, at One Financial Plaza on North Broadway. It is a full-service wealth manager and middle-market investment bank with ~$5.5B in 2025 net revenue and nearly 10,000 associates (Stifel 2025 results). M&A is executed through Stifel, Nicolaus & Company, Incorporated (FINRA CRD #793) — and the bench was built largely by acquisition: KBW (Keefe, Bruyette & Woods, financial institutions, closed February 2013), Miller Buckfire (restructuring, 2012), Eaton Partners (fund placement, 2016), Torreya Partners (life sciences, closed March 1, 2023), and Bryan, Garnier & Co. (European technology and healthcare, completed June 2, 2025).

Where it fits: Stifel's own M&A deal showcase runs roughly $92.5M to $2.2B in enterprise value — squarely core- and upper-middle-market. It does not publish a hard minimum, but the public record makes clear the institutional M&A group anchors well above the $5M-$50M lower-middle-market band. For a $25M manufacturer, distributor, or services business, a local boutique will give your deal more senior attention at a lower fee.

The one big exception for St. Louis sellers: financial institutions. Through KBW, Stifel is the dominant U.S. bank-M&A advisor — KBW led the financial-services sector by deal volume in 2024 with 37 deals, and Stifel disclosed that KBW advised on roughly 84% of all bank-and-thrift deals by disclosed value since January 1, 2025 (Stifel disclosure, July 2025). KBW will advise sub-$100M community banks on strategic alternatives — a recent example: KBW acted as exclusive financial advisor to Burke & Herbert Financial Services on its ~$354M acquisition of LINKBANCORP (announced December 2025). So a Missouri community bank or specialty-finance company should put KBW at the top of the list at almost any size; a non-financial lower-middle-market business should weigh it against the local boutiques.

Which national middle-market banks cover Missouri deals — and do any keep a St. Louis deal office?

The national middle-market banks that win Missouri's larger deals — William Blair, Robert W. Baird, Lincoln International, Houlihan Lokey — are real options for a $150M+ or specialized process, but the honest answer on local presence is that none of them keeps a deal-executing M&A office in St. Louis that I could confirm. They cover the region from Chicago and other hubs.

- William Blair (Chicago HQ) is the employee-owned middle-market bank with deep sector practices; it has no St. Louis office (confirmed on its own locations page) and covers the Midwest from Chicago. It is the natural national choice for a clean $150M-$1B Missouri sell-side.

- Robert W. Baird (Milwaukee HQ) is another strong employee-owned middle-market bank covering the region; I could not confirm a dedicated St. Louis investment-banking deal office.

- Lincoln International and Houlihan Lokey (the latter the #1 global M&A advisor by deal count) both cover Missouri from Chicago and other hubs rather than a local deal team.

The takeaway: for a larger or more complex process, these are credible, but you are hiring a Chicago-based team that will fly in — there is no national-bank "St. Louis office" advantage to be had, so weigh them on sector fit and buyer reach, not on a local address. For most founder-owned $5M-$75M deals, a genuinely-local boutique gives you more senior attention; the national banks earn their fee as the deal scales.

Don't mistake a wealth giant for a deal advisor: Edward Jones, Wells Fargo Advisors, and the RIA trap

This is the most important sorting test in St. Louis, because the city is a national capital of retail financial advice — and none of those famous firms runs corporate sell-side M&A.

- Edward Jones (Edward D. Jones & Co., headquartered in Des Peres) is one of the largest retail brokerages in the country — ~15,000 branch offices, ~$2.2T in client assets — built on the one-advisor branch model. It manages individuals' investment portfolios. It does not run sell-side auctions for operating companies.

- Wells Fargo Advisors (headquartered downtown, built on the old St. Louis firm A.G. Edwards) is the wealth-management arm of Wells Fargo. Corporate M&A at Wells Fargo lives in a separate corporate and investment bank, not in Wells Fargo Advisors. The St. Louis wealth office is not a middle-market M&A shop.

- The big St. Louis wealth RIAs — Moneta Group (~$42B AUM), Plancorp, Matter Family Office, Buckingham Strategic Wealth — are excellent at managing a business owner's personal and family wealth (and a good wealth advisor is genuinely valuable around a liquidity event, for the proceeds). But they are not the firm you hire to market and sell the company.

- The commercial banks — Commerce Bancshares, Enterprise Financial, Stifel Bank — lend and take deposits; they are not sell-side M&A advisors. (Note that Stifel Bank is a separate subsidiary from the Stifel Nicolaus M&A practice; do not conflate the two.)

There are also two name traps to avoid: "Focus Partners Wealth" in St. Louis is an unrelated wealth manager, not the national boutique FOCUS Investment Banking (Vienna, VA); and Greenwich Capital Group is a Michigan middle-market bank with no St. Louis office, despite the generic name. Selling a company is a distinct discipline — it belongs to an M&A advisor or investment bank, not a wealth manager, a commercial banker, or a similarly-named firm.

What's the "Headquarters Town," and which in-town strategics actually buy?

The signature frame for St. Louis is the Corporate-Acquirer Density Map: for a metro its size, an unusual number of large, acquisitive companies are headquartered here, which means a local seller frequently has credible strategic buyers in-region — and the 2023-2026 deal record proves they are active.

The headquarters base, on the 2026 Fortune 500 list, includes Centene (#18, managed care), Reinsurance Group of America (life/health reinsurance, Chesterfield), Emerson Electric (industrial automation, #239), Edward Jones / Jones Financial (#268), Graybar (employee-owned electrical/comm distribution, #373), Post Holdings (consumer food, #458), and Core & Main (water/infrastructure distribution, #483) (Fox2Now, June 2026). Add two of the largest private companies in the country — Enterprise Mobility ($39B revenue, Taylor-family owned) and World Wide Technology ($20B, IT services) — plus the national headquarters of Boeing Defense, Space & Security (~16,000 regional employees, building the F-15, F/A-18, T-7A, and MQ-25), and a deep agtech cluster (Bayer Crop Science, the Donald Danforth Plant Science Center, the 39 North district).

Now the part that matters for a seller — these companies buy:

- Emerson acquired National Instruments for ~$8.2B (completed October 2023) and the remaining shares of AspenTech in a deal valuing it at ~$17B (2025).

- Reinsurance Group of America closed a $32B reinsurance transaction with Equitable Holdings (closed July 31, 2025).

- Bunge (St. Louis corporate HQ) completed its ~$8.2B merger with Viterra (closed July 2, 2025).

- Post Holdings is a textbook serial acquirer, buying 8th Avenue Food & Provisions for ~$880M (2025) and Potato Products of Idaho the same cycle.

- Olin/Winchester acquired small-caliber ammunition manufacturing assets for $75M (completed April 2025).

- BJC HealthCare merged with Kansas City's Saint Luke's to form a $10B, 28-hospital system (closed January 1, 2024).

For a middle-market seller, this density is a real edge: a St. Louis-fluent advisor who can name the in-region corporate-development teams and the active national sponsors in your sector has a genuine buyer map to work, not just a generic outreach list. It also cuts the other way on confidentiality — many of your most logical buyers travel in the same circles as your competitors, which is exactly why staged disclosure and a permissioned, watermarked data room matter here.

Who advises a St. Louis food, consumer, or agtech sale?

For a food, consumer, or agtech business, the lane is sector-relationship-driven, and St. Louis's strategic-buyer base is unusually deep. Post Holdings alone is one of the most active food-and-CPG acquirers in the country, and the region adds Nestlé Purina, Anheuser-Busch, and Schnucks on the consumer side, plus the Bayer Crop Science / Danforth / 39 North agtech ecosystem on the plant-science side.

For a $5M-$75M founder-owned food or consumer business, a relationship-rich local boutique (Benjamin F. Edwards, Nolan & Associates, R.L. Hulett, The Fortune Group) can run a tight, confidential process and pull in-region strategics in by name, then layer national consumer-focused private-equity platforms on top. For a larger or more specialized process ($150M+), a national consumer/food-and-beverage banking desk earns its fee on buyer reach. Agtech and plant-science deals add IP, formulation, and regulatory diligence that reward a sector specialist and a tightly permissioned data room — recipes, trait data, and field-trial results are exactly the material you stage behind an NDA and release only to a short list.

Who advises a St. Louis industrial, manufacturing, or distribution sale?

This is the bread-and-butter of the St. Louis lower-middle-market, and the local boutique bench is built for it. Nolan & Associates explicitly covers building products, transportation and logistics, industrial, and distribution, and has a recent, named, in-band closing to point to — it was sell-side advisor to Feed Products & Service Company on its 2024 sale to Bruce Oakley, Inc. R.L. Hulett is a generalist middle-market firm with 275+ closed deals over 40 years and a recent industrial-services closing (Copp of St. Louis to Warehouse Services, Inc., 2024). Benjamin F. Edwards brings its own broker-dealer and a recent technical-services deal (Surdex Corporation, a geospatial firm, to Bowman Consulting, $44M, April 2024). The Fortune Group, which transacts through its own subsidiary broker-dealer FG Capital LC (FINRA CRD #125229), rounds out the verified local bench.

The buyer map is the advantage: in-region distribution consolidators (Graybar, Core & Main) and industrial acquirers (Emerson, Olin) are realistic strategic buyers, and a St. Louis-fluent advisor will know which corporate-development teams are active this cycle. Industrial diligence is heavy on working capital, environmental and safety, equipment condition, and customer concentration — prepare those workstreams early, because they are the most common source of re-trading late in a deal.

Who advises a Missouri community bank or specialty-finance sale?

If you are a bank, thrift, credit union, or specialty-finance company, the answer is unusually clear in St. Louis: KBW, A Stifel Company is the dominant U.S. financial-institution M&A advisor, and it is headquartered under the same St. Louis roof as Stifel. KBW led the financial-services sector by deal volume in 2024 (37 deals) and advised on roughly 84% of bank-and-thrift deal value since January 2025. It runs strategic-alternatives mandates for community banks well below $100M, so size is rarely a barrier here. For a Missouri financial institution, KBW is the call; for everything else, weigh the local boutiques and national middle-market banks above.

What's the difference between a business broker, a boutique investment bank, and a national bank in St. Louis — and which do I need?

The three tiers map cleanly to deal size and the licensing line:

- Business brokers (Metro Business Advisors, Sunbelt Business Advisors of St. Louis, Transworld) handle Main-Street and very-lower-middle-market deals — typically under $5M, sometimes up to ~$20M in revenue. They operate under business-brokerage credentials (the IBBA's CBI, the M&A Source's M&AMI), not FINRA registration, which is appropriate for an asset sale below the securities threshold.

- Boutique investment banks / M&A advisors (Benjamin F. Edwards, Nolan & Associates, R.L. Hulett, The Fortune Group) run competitive sell-side auctions in the ~$5M-$200M band. A securities-based stock sale should run through a FINRA-registered broker-dealer — some of these firms have their own (Benjamin F. Edwards, CRD #146936), some use an affiliate (Nolan via Middle Market Transactions, CRD #133062), and some use a hosted third-party broker-dealer. Verify which, but do not treat a hosted broker-dealer as a red flag — it is a common, legitimate model.

- National banks (Stifel for $50M+ and all financial-institution deals; William Blair, Baird, Lincoln for $150M+) bring institutional buyer networks and capital-markets muscle that matter as the deal scales.

The rule of thumb: under ~$5M, a broker; ~$5M-$150M, a local boutique; $150M+ or a financial institution, a national bank. The deal-size bands overlap, so the real test is buyer reach and senior-banker attention, not the label.

Who handles sub-$5M Main-Street business sales in St. Louis?

For a genuinely Main-Street business — a sub-$5M restaurant, services firm, franchise, or small distributor — the right intermediary is a business broker, not an investment bank. In St. Louis the recognized names include Metro Business Advisors (which serves companies up to ~$20M in revenue and adds valuation and exit planning), Sunbelt Business Advisors of St. Louis, Transworld Business Advisors (St. Peters and St. Charles), Murphy Business, and Premier Business Brokers. These operate under IBBA / M&A Source credentials rather than FINRA registration, which is the correct fit below the securities threshold. The economics differ from an investment-bank engagement — typically a success fee on a simpler scale and a smaller (or no) retainer — and the process is lighter, but the confidentiality discipline still matters: even a $2M business benefits from a blind teaser, an NDA gate, and a simple permissioned data room rather than emailing financials to every tire-kicker.

Is now a good time to sell my St. Louis business?

The honest answer is that "the market" matters far less than your own readiness and the strength of your specific buyer pool. For St. Louis sellers in 2026, the structural backdrop is favorable in one important way: the in-region strategic-acquirer base is demonstrably active (Emerson, RGA, Bunge, Post, Olin, and BJC all closed significant deals in the 2023-2026 window), and private-equity dry powder remains substantial and looking for quality middle-market platforms and add-ons. Industrial, distribution, food, healthcare-services, and financial-institution assets with clean financials and durable cash flow are in demand.

What actually determines your outcome is preparation. A business with a clean, defensible quality-of-earnings picture, low customer concentration, transferable contracts, and a documented growth story sells faster and at a higher multiple regardless of the macro headlines — and one that goes to market with messy books invites re-trading no matter how good the year is. The single most reliable thing you control is being ready before you launch: clean financials, a real CIM, and a staged data room. If those are in place and you have a credible buyer map, 2026 is a reasonable year to run a process; if they are not, the highest-return move is to spend two quarters getting them in order first.

What's a reasonable success fee for a $25M St. Louis sell-side, and how do fees vary?

For a $25M St. Louis company, expect a monthly retainer plus a success fee at close, with a blended success rate around 3-3.5% squarely in the normal range. The most common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M — which on a $25M deal computes to about $700K, roughly 2.8%; add the uncredited slice of the retainer plus any minimum-fee floor and the effective rate usually lands near 3-3.5%. That tracks national middle-market data: success fees run ~3-4% in the $25M band and decline toward 1.5-2% by $100M.

Retainers (work fees) run roughly $5,000-$25,000 per month at a small boutique, often credited against the success fee at closing — but only if the engagement letter says so in writing. A minimum-fee floor (commonly ~$150K at the small end, $500K-$1.5M at true middle-market banks) appears in most letters but rarely binds on a $25M deal. What matters more than the headline percentage is the base the fee applies to (total enterprise value including assumed debt and earnouts, or just cash at close) and the tail period — banks ask for 18-24 months; negotiate it to 12. And keep perspective: the fee delta between two good advisors is almost always dwarfed by the price delta a competitive, well-run auction produces.

Which virtual data room should a St. Louis seller actually use?

Match the room to the deal. For a $500M+ mega-deal where counterparty expectations demand a legacy brand, Datasite or Intralinks are the default — and you will pay legacy per-page or per-project pricing for the signaling. For the sub-$300M enterprise-value band that is the bulk of St. Louis lower-middle-market deal count, a modern flat-rate platform — Peony, iDeals, or FirmRoom — gives you the same core security and analytics without the per-page premium.

I run Peony, so I will be direct about what matters for a sell-side and disclose my bias: the controls that protect a confidential process are per-buyer permissions (so strategics, sponsors, and in-region competitors each see only their tier), dynamic per-viewer watermarks and screenshot protection (so a leaked page traces back to the exact viewer), and page-level analytics (so you know which buyer's CFO actually read your financials and for how long). On Peony, watermarks, screenshot protection, and granular per-file permissions live on the Data Room tier at a flat $52 per admin per month; NDA gating and analytics start lower, and there are no per-page or per-GB fees — a predictable line item against an advisory fee that runs into six figures. Whatever you choose, the principle is the same: stage your disclosure, gate it behind an NDA, and make every page traceable.

Bottom line

St. Louis is the rare metro that is rich in both corporate headquarters and financial-services brands — and the honest version of this list separates the two. The genuinely homegrown national investment bank is Stifel (Stifel, Nicolaus & Company, FINRA CRD #793), formidable on $50M+ sales and dominant in financial-institution M&A through KBW — but realistically above where a typical $5M-$50M founder-owned deal gets done. The genuinely-local lower-middle-market sell-side bench is a short, knowable list: Benjamin F. Edwards (its own broker-dealer, CRD #146936; Surdex → Bowman, $44M, 2024), Nolan & Associates (affiliate BD Middle Market Transactions, CRD #133062; Feed Products → Bruce Oakley, 2024), R.L. Hulett (Clayton, founded 1981, 275+ deals; Mitchell Humphrey → Tripleview and Copp → Warehouse Services, 2024), and The Fortune Group (its own subsidiary broker-dealer FG Capital LC, CRD #125229). Two long-operating local names, Clayton Capital Partners and The Douglas Group, are also in the market, but I could not verify a FINRA broker-dealer or a recent named deal for either this pass, so I have not ranked them.

For a $5M-$75M industrial, distribution, food, consumer, or services sale, start with the local boutiques and weigh their buyer map. For a $150M+ or institutional process, bring in Stifel, William Blair, or Baird — none keeps a deal-executing St. Louis office, so hire them on sector fit, not a local address. For a Missouri community bank, call KBW. For a Main-Street deal under ~$5M, an IBBA-credentialed broker (Metro Business Advisors, Sunbelt, Transworld). And do not mistake the famous St. Louis financial brands — Edward Jones, Wells Fargo Advisors, Moneta, Plancorp, Matter Family Office — for M&A advisors; they manage wealth, they do not sell companies.

The single most important advisor-selection question for a St. Louis seller: which firm has the deepest documented relationship with the in-region strategics and the PE platforms in your sub-sector, and can show recent closings in your band? In a Headquarters Town this dense with potential buyers, that verification is the whole edge. We serve 6,800+ customers on the data-room side of exactly these deals, and the prep you do before you pick an advisor — clean financials, a defensible quality-of-earnings file, a staged data room, a tight buyer thesis — compounds everything the advisor does next. I run Peony, a data room company, and the Data Room tier gives you dynamic per-viewer watermarks, page-level analytics, and visitor groups at a flat $52 per admin per month — no per-page or per-GB fees, the predictable line item against a six-figure advisory fee.

Frequently asked questions about St. Louis M&A advisors

I'm selling my St. Louis manufacturing or distribution company — should I hire a local St. Louis M&A boutique or a national investment bank?

For a St. Louis manufacturing or distribution sale, hire a local boutique when your deal is in the ~$5M-$75M band and your best buyers are reachable strategics and middle-market sponsors; reach for a national bank (William Blair, Baird, or the homegrown national bank Stifel) once the deal climbs toward $150M+ or needs a wide institutional buyer pool. Price comes from competitive tension, not from a banker's zip code, so the real question is where your best buyers sit and who already has those relationships — and St. Louis has an unusual structural advantage here. This is a Headquarters Town: a dense set of acquisitive in-region companies (Emerson, Graybar, Core & Main, Post Holdings, Olin, World Wide Technology) means a local seller frequently has credible strategic buyers headquartered within the metro, and a genuinely St. Louis-fluent boutique can name them. The genuinely-local sell-side bench is short but real: Benjamin F. Edwards (its own FINRA broker-dealer, CRD #146936), Nolan & Associates (through affiliate Middle Market Transactions, CRD #133062), R.L. Hulett (founded 1981, 275+ deals), and The Fortune Group (its own subsidiary broker-dealer, FG Capital LC, CRD #125229). Above ~$150M you bring in Stifel or a Chicago-based middle-market bank. On the document side, the prep is the same either way — I run Peony, a data room company used by 6,800+ customers, and a clean, staged data room with page-level analytics is the cheapest lever you control before you even pick the banker.

I own a ~$25M family business in St. Louis — who are the best M&A advisors in St. Louis for a lower-middle-market sale?

For a ~$25M St. Louis family-business sale, the genuinely-local shortlist is short and knowable, and you should be told so plainly: Benjamin F. Edwards & Company (St. Louis, with its own FINRA broker-dealer, CRD #146936), Nolan & Associates (founded 1976, transacting through its affiliated broker-dealer Middle Market Transactions, Inc., CRD #133062), R.L. Hulett & Company (Clayton, founded 1981, 275+ closed deals over 40 years), and The Fortune Group (its own subsidiary broker-dealer FG Capital LC, CRD #125229) are the core boutiques that run lower-middle-market sell-sides in this band. The homegrown national bank, Stifel, is headquartered downtown, but its institutional M&A group realistically anchors at $50M+ — for a $25M non-financial business it usually sits above where the deal gets done, unless you are a bank or specialty-finance company (then its KBW arm is the call at almost any size). The screening test for any boutique: ask the banker to name the last three deals they closed in your sub-sector and the buyers on the other side. Benjamin F. Edwards can point to a named, dated, in-band closing (Surdex Corporation's $44M sale to Bowman Consulting, April 2024); Nolan can point to Feed Products & Service Company's 2024 sale to Bruce Oakley; R.L. Hulett to Copp of St. Louis's 2024 sale to Warehouse Services — that kind of recent, named track record is what separates a real fit from a directory listing. We serve 6,800+ customers on the data-room side of exactly these deals, and the firms that read every page of a teaser — you can see it in page-level analytics — are usually the ones genuinely working your file.

For a $25M St. Louis sale, what are the pros and cons of a local boutique vs the homegrown national bank (Stifel) vs a national bank covering from Chicago?

For a $25M St. Louis sale, a local boutique gives you senior-banker attention, in-region strategic relationships, and a boutique fee; Stifel gives you a national-bank brand and balance sheet but realistically engages higher up the size curve; and a Chicago-based middle-market bank (William Blair, Baird, Lincoln International) gives you a deep institutional buyer network that matters more as the deal gets larger. The boutique case: at $25M you are below the size where Stifel's institutional M&A group or a William Blair will staff its A-team, so a firm like Benjamin F. Edwards, Nolan & Associates, R.L. Hulett, or The Fortune Group can put a senior banker on every buyer call and run a tight, confidential process — and in a Headquarters Town the local relationships reach real buyers. The Stifel case: Stifel (Stifel, Nicolaus & Company, FINRA CRD #793) is the genuine homegrown national investment bank, formidable on $50M+ sales and the clear national leader in bank and specialty-finance M&A through its KBW arm — but its public deal showcase runs ~$92.5M to $2.2B, so a $25M non-financial business is below its sweet spot. The Chicago-bank case: at $150M+ a national middle-market desk's reach is worth the higher fee, but none keeps a deal-executing M&A office in St. Louis — they cover Missouri remotely. The honest read for a $25M deal: a relationship-rich local boutique usually wins on attention and fee, provided it can name your actual best buyers. We serve 6,800+ customers on the data-room side, and you can use visitor groups to run a strategics-vs-sponsors split as separate permissioned tiers in one room regardless of which advisor you pick.

Is Stifel the right M&A advisor to sell my St. Louis company, or is it too big for a sub-$50M deal?

Stifel is the right M&A advisor for your St. Louis company if you are selling for roughly $50M or more, or if you are a bank, thrift, or specialty-finance company of almost any size — but for a sub-$50M non-financial business it usually sits above where the deal actually gets done, and a local boutique is the more realistic lead. Here is the honest framing. Stifel is genuinely St. Louis's homegrown national investment bank — headquartered downtown since 1890, ~$5.5B in 2025 net revenue, nearly 10,000 associates, with M&A executed through Stifel, Nicolaus & Company, Incorporated (FINRA CRD #793). Its bench was built by acquisition: KBW (financial institutions, 2013), Miller Buckfire (restructuring, 2012), Eaton Partners (fund placement, 2016), Torreya (life sciences, 2023), and Bryan Garnier (European tech/healthcare, 2025). Its public M&A deal showcase runs roughly $92.5M to $2.2B in value — squarely mid- and upper-middle-market, not $5M-$50M lower-middle-market. The one exception that matters for St. Louis: through KBW, Stifel dominates U.S. financial-institution M&A (37 financial-services deals in 2024, the volume leader; ~84% of bank-and-thrift deal value since January 2025), and KBW will advise sub-$100M community banks on strategic alternatives. So: a Missouri community bank, yes, call KBW; a $25M manufacturer or distributor, a local boutique will give your deal more senior attention at a lower fee. On the document side, I run Peony, a data room company, and a clean room with page-level analytics is the cheapest lever you control before you pick between them.

I own a St. Louis food, consumer, or agtech company — who should advise the sale, and are in-town strategics like Post or Emerson realistic buyers?

For a St. Louis food, consumer, or agtech sale, you want an advisor with sector relationships and a documented buyer map — and yes, in-town and in-region strategics are realistic buyers, which is one of St. Louis's genuine structural advantages as a seller. The Headquarters Town density is real: Post Holdings is a textbook serial acquirer in food and consumer products (it bought 8th Avenue Food & Provisions for ~$880M in 2025 and Potato Products of Idaho the same cycle), Nestlé Purina and Anheuser-Busch anchor consumer and pet, and the agtech ecosystem around Bayer Crop Science, the Donald Danforth Plant Science Center, and the 39 North district makes St. Louis a credible plant-science buyer hub. For a $5M-$75M founder-owned food or consumer business, a relationship-rich local boutique (Benjamin F. Edwards, Nolan & Associates, R.L. Hulett, The Fortune Group) can run a tight process and pull those in-region strategics in by name, then layer national consumer-focused sponsors on top. For a larger or more specialized process ($150M+), a national consumer or food-and-beverage banking desk earns its fee on buyer reach. The advisor-fit test is the same in every sector: can the banker name the active strategic and PE acquirers in your specific niche and the last comparable deal they closed? Because consumer and agtech diligence is recipe-, formulation-, and IP-sensitive, a data room with dynamic per-viewer watermarking and screenshot protection matters — I run Peony, a data room company, and those controls live on our Data Room tier.

How does a sell-side M&A process work for a St. Louis company, and how long does it take from advisor hire to close?

A St. Louis sell-side runs in five overlapping stages and typically takes 6-9 months from signing the engagement letter to close, longer if the financials need cleanup first. The rough timeline: 4-8 weeks of preparation (clean financials, a quality-of-earnings build, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA, starting from a blind teaser; 3-5 weeks to collect indications of interest and build a short list; 4-6 weeks of management meetings and the lead-bid/LOI stage; then 8-12 weeks of confirmatory due diligence and definitive-agreement negotiation to close. The advisor's job through all of it is to manufacture competitive tension — running a real auction across both strategic buyers (in St. Louis that often means in-region consolidators like Post, Emerson, Graybar, or Core & Main plus national strategics) and private-equity platforms, so no single bidder feels unchallenged. Industrial and distribution deals can move quickly when a strategic already knows the market, but slower through working-capital, environmental, and customer-concentration diligence. The single biggest timeline risk is unprepared financials — sellers who walk in without a clean, defensible quality-of-earnings picture add months. A clean, staged data room prepared before launch is the most reliable way to compress the back half of the schedule; I run Peony, a data room company used by 6,800+ customers, and the sellers who set up the room before going to market consistently close faster than the ones who scramble after the first LOI.

What do buyers diligence, and how do I set up a data room before going to market with my St. Louis company?

Buyers diligence a St. Louis lower-middle-market company on the things that prove durable, transferable cash flow — normalized EBITDA and its quality, revenue and customer concentration, gross-margin trend, working-capital needs, contract assignability, and (for industrial and manufacturing sellers) environmental, safety, and equipment condition — and you set up the data room around the eight diligence workstreams those feed. The workstreams: financial (3-5 years of statements plus a quality-of-earnings build), corporate/legal (cap table, org chart, bylaws, minutes), commercial (customer and supplier contracts, concentration analysis), operations/technical (facilities, equipment, environmental, safety), HR (org chart, key-employee and non-compete agreements), IP and IT (patents, trademarks, systems), tax (returns, nexus, credits), and insurance and compliance. The two documents that do the most work up front are a defensible quality-of-earnings file and the CIM your advisor builds. The discipline that protects you is staged disclosure: a blind teaser first, the named CIM only after an NDA, and sensitive material (customer names, pricing, employee rosters) held back to later stages and released only to a short list. A data room with per-buyer permissions, page-level analytics, and dynamic watermarking is what makes that enforceable — each viewer sees only their tier, and every page they open carries their identity so a leak is traceable. I run Peony, a data room company used by 6,800+ customers, built for exactly this kind of tiered, watermarked release, and you can stage strategics and sponsors as separate visitor groups in one room.

How do I keep my sale confidential in St. Louis's tight-knit business community where owners, bankers, and competitors all know each other?

Confidentiality is run through staged disclosure and tight access control — and in St. Louis, where the owner, banker, and corporate-development circles are small and overlapping, it is one of the main reasons to hire an intermediary rather than shop the business yourself. The standard playbook: the advisor markets a blind teaser first (sector, size, and headline numbers with no name); interested buyers sign an NDA before receiving the named CIM; and sensitive material (customer names, pricing, employee rosters, supplier terms) is held back until later diligence stages and released only to a short list. A data room with per-buyer permissions and dynamic per-viewer watermarking is what makes this enforceable — each viewer sees only their tier, and every page they open carries their identity, so a leaked teaser is traceable back to the exact person who leaked it. That deterrence matters in a Headquarters Town: many of your most logical strategic buyers are in-region companies whose corporate-development teams move in the same circles as your competitors, and a key employee or a competing owner might be one shared advisor away. Tell your advisor explicitly that no competitor or in-region party on your do-not-contact list should ever receive even the blind teaser, and put that list in the engagement letter. I run Peony, a data room company used by 6,800+ customers, built for exactly this kind of tiered, watermarked release — dynamic per-viewer watermarks and screenshot protection are how you make a small-market sale leak-resistant, and page-level analytics tell you who actually opened what.

Can a local St. Louis boutique actually reach national PE and strategic buyers, or will I leave value on the table vs a national bank?

Yes — a good local St. Louis boutique can reach national PE and strategic buyers, but only if it can prove the relationships, and St. Louis's structural advantage actually helps because so many credible acquirers are headquartered in-region. The proof is in the buyer list: ask the advisor to produce a list that mixes 8-15 named strategics with 15-30 named sponsors specific to your sub-sector, with a contact at each. A genuinely St. Louis-fluent boutique can do that and can name the in-region consolidators (Post Holdings, Emerson, Graybar, Core & Main, Olin, World Wide Technology) that have actually been buying in 2023-2026; a generalist who cannot name them is the wrong fit. The honest caveat: for a true national or cross-border buyer pool at $150M+, a boutique should co-advise with or hand off to a national bank (Stifel, William Blair, Baird) rather than pretend it owns relationships it does not have. You leave value on the table not by hiring local, but by hiring an advisor — local or national — who cannot reach your actual best buyers, so the verification matters more than the zip code. And one St. Louis-specific check: confirm the boutique transacts through a registered broker-dealer (its own or a hosted one) for a securities-based sale, since several local shops use a third-party FINRA broker-dealer rather than their own. We serve 6,800+ customers on the data-room side, and visitor groups let you run the strategics-vs-sponsors split as separate permissioned tiers in one data room.

What red flags should I watch for, and isn't my Edward Jones or Wells Fargo Advisors contact enough to sell my St. Louis business?

Your Edward Jones or Wells Fargo Advisors contact is almost certainly not the right person to sell your business — those are retail wealth-management and brokerage firms, not corporate sell-side M&A advisors, and confusing the two is the single most common St. Louis mistake. Both are headquartered here (Edward Jones in Des Peres, Wells Fargo Advisors downtown, the latter built on the old A.G. Edwards), and both are excellent at managing your personal investment portfolio — but neither runs competitive sell-side auctions for operating companies, and the same is true of the big St. Louis wealth RIAs (Moneta Group, Plancorp, Matter Family Office) and the commercial banks (Commerce, Enterprise, Stifel Bank). Selling your company is the job of an M&A advisor or investment bank, a different discipline entirely. Beyond that sorting, vet any advisor on three things: registration status (a securities-based sale should run through a FINRA-registered broker-dealer — check BrokerCheck, e.g., Stifel is CRD #793, Benjamin F. Edwards CRD #146936, Nolan's affiliate Middle Market Transactions CRD #133062; some boutiques use a hosted broker-dealer, which is fine if disclosed), named recent closings in your sub-sector with the buyers identified, and a written commitment on which senior banker will actually run your deal. Red flags: a large upfront fee with a vague success structure; a valuation that sounds too good to be true; reluctance to name the lead banker; emailing sensitive financials instead of using a permissioned data room; and an 18-24 month tail period they refuse to negotiate. I run Peony, a data room company, and a telling early signal is whether the advisor insists on a real data room with page-level analytics rather than emailing your financials around.

What does an M&A advisor cost to sell a $25M St. Louis company — is a 3 to 3.5% success fee normal, and how does Double Lehman plus a retainer work?

For a $25M St. Louis company, expect a monthly retainer plus a success fee at close, with a 3-3.5% blended success rate squarely in the normal range. The most common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M — which on a $25M deal computes to about $700K, roughly 2.8%; add the slice of retainer that is not credited back plus any minimum-fee floor and the effective blended rate usually lands near 3-3.5%. That tracks national middle-market data: a $25M deal sits in the band where independent fee tables put blended success fees around 3-4%, declining toward 1.5-2% by $100M, so quote ~3-4% as the practical range. Retainers (work fees) in this band run roughly $5,000-$25,000 per month at a small boutique (more at a mid-market bank), and they are frequently credited against the success fee at closing — but only if the engagement letter says so in writing, so negotiate the credit explicitly. A minimum-fee floor (commonly around $150,000 at the small end, $500K-$1.5M for true middle-market banks) appears in most letters; on a $25M deal the percentage fee normally exceeds the small-end floor, so it rarely binds at this size. What matters more than the headline percentage is the base it applies to (total enterprise value including assumed debt and earnouts, or just cash at close) and the tail period — banks ask for 18-24 months; cap it at 12. The fee delta between two good advisors is almost always dwarfed by the price delta a competitive, well-run auction produces. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — a predictable cost against an advisory fee that runs into six figures.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this St. Louis shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- Best Industrial M&A Advisors — the sector hub for manufacturing, distribution, and industrial sellers, the bulk of the St. Louis deal flow

- Best Financial Services M&A Advisors — the FIG sector hub, the lane where KBW (A Stifel Company) dominates

- Best Accounting Firm M&A Advisors — the national CPA-firm deal bench: who actually runs firm sales and mergers, what the private-equity platforms pay, and the practice-broker tier for smaller books

- M&A Data Room: Setup and Workstream Mapping — the data room setup playbook for sell-side prep

- Best Data Room for a Small M&A Deal (sub-$30M sale) — right-sized VDR selection and setup for a sub-$30M sale, the band where most St. Louis founder exits land

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep including vendor DD, which matters more in an industrial, defense, or regulated footprint

- How to Write a CIM (Confidential Information Memorandum) — the authoring playbook for the offering document your advisor will build for the sale

- State of M&A Data Rooms: 2026 Benchmark — the 283-deal Peony platform benchmark

- Virtual Data Room Cost Guide — what a VDR actually costs, and how flat per-admin pricing compares to per-page models

- Best M&A Advisors in Chicago — the Midwest hub where William Blair, Baird, and Lincoln run the larger Missouri deals

- Best M&A Advisors in Indianapolis — the closest strategic-acquirer-density comparator, also anchored by a real in-state investment bank

- Best M&A Advisors in Minneapolis — Upper-Midwest comparator with a deep industrial and food base

- Best M&A Advisors in Nashville — Mid-South growth-market comparator

- Best M&A Advisors in Kansas City — the cross-state "Ownership Town" counterpart: no homegrown national bank, $86B of public giants sold out of town (Sprint, Cerner, KCS), and the Animal Health Corridor running on vertical-specialist rules

- Best M&A Advisors in Baltimore — the First Bank Town: America's first investment bank was founded there in 1800, and Stifel's 2005 purchase of Legg Mason Capital Markets (up to $95M, ~500 people) is the deal that made Baltimore this hometown bank's East Coast institutional home

- Best M&A Advisors in Milwaukee — the closest peer to St. Louis's story: another Midwest metro that grew and kept a homegrown national bank, employee-owned Robert W. Baird

Footnotes and sources

- Stifel — firm overview, 2025 results, and M&A practice; FINRA BrokerCheck — Stifel, Nicolaus & Company, CRD #793; KBW (A Stifel Company) financial-institution M&A leadership (37 deals in 2024; ~84% of bank-and-thrift deal value since January 2025)

- Benjamin F. Edwards & Company — investment-banking practice; FINRA CRD #146936; exclusive sell-side advisor to Surdex Corporation on its $44M sale to Bowman Consulting Group, closed April 4, 2024

- Nolan & Associates — middle-market M&A; securities offered through affiliate Middle Market Transactions, Inc., FINRA CRD #133062; sell-side advisor to Feed Products & Service Company on its 2024 sale to Bruce Oakley, Inc.

- R.L. Hulett & Company — middle-market M&A, founded 1981, 275+ closed transactions; sell-side advisor to Copp of St. Louis on its 2024 sale to Warehouse Services, Inc.; securities offered through an independent FINRA-registered broker-dealer

- The Fortune Group — St. Louis lower-middle-market M&A advisory (founded 1987); securities offered through its subsidiary broker-dealer FG Capital LC, FINRA CRD #125229

- St. Louis 2026 Fortune 500 companies — seven regional Fortune 500 headquarters (Centene #18, Reinsurance Group of America, Emerson, Edward Jones, Graybar, Post Holdings, Core & Main)

- Emerson completes acquisition of NI — ~$8.2B, completed October 2023; Emerson–AspenTech remaining-shares acquisition (2025)

- RGA closes $32B reinsurance transaction with Equitable — closed July 31, 2025

- Bunge and Viterra complete merger — ~$8.2B, closed July 2, 2025

- Post Holdings to acquire 8th Avenue Food & Provisions — ~$880M (2025)

- Olin/Winchester completes acquisition of small-caliber ammunition assets — $75M, completed April 2025

- BJC and Saint Luke's complete merger — $10B integrated health system, closed January 1, 2024

- Edward Jones and Wells Fargo Advisors — retail wealth-management and brokerage firms headquartered in the St. Louis area (NOT corporate M&A advisors); Moneta Group, Plancorp, and Matter Family Office are wealth-management RIAs

- Peony — data room platform serving 6,800+ customers; pricing, page-level analytics, dynamic watermarks, visitor groups