12 Best Accounting Firm M&A Advisors & CPA Practice Brokers (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

12 Best Accounting Firm M&A Advisors & CPA Practice Brokers (2026)

Quick answer: For a mid-size CPA firm (roughly $5M-$50M revenue) weighing a sale, merge-up, or internal succession, the advisor bench is not investment banks — it is a small set of specialist consultants plus practice brokers, each right at a different size. Category-defining CPA-firm M&A consultants run the mid-market firm-to-firm and firm-to-PE deals: Koltin Consulting Group (Allan Koltin, Chicago — the single most-cited dealmaker in the profession), Whitman Advisory (formerly Whitman Transition Advisors, New York), The Visionary Group, Accountants Advisory Group, and Carl George Advisory. A minority of larger, institutional sell-side mandates run through registered mid-market banks — Capstone Partners, Berkery Noyes (CRD #155918), and Republic Capital Group (CRD #334963) — each with honest caveats below. For a sub-$2M practice selling to an individual buyer, the venue is a practice broker: Accounting Practice Sales (APS), Poe Group Advisors, ProHorizons, or Accounting Biz Brokers. Match the advisor to your size and situation, not to the biggest logo. Peony does not advise on deals — pick your advisor first.

This is the CPA-firm-only cut. For the general question of which intermediary type sells a company — advisor vs broker vs investment bank — see our M&A advisor vs broker vs investment bank hub, and for the adjacent financial-services bench (where wealth, insurance, and fintech sellers go) see Best Financial Services M&A Advisors. This page goes deep on the one thing those hubs do not cover at resolution: the specialist bench for selling an accounting firm specifically, and the structural machinery — the alternative practice structure, partner-comp normalization, rollover, and the second bite — that makes a CPA-firm offer so easy to misread.

Last updated: July 2026

TL;DR: The thesis of 2026 is that the multiple arrived before the succession plan. About 75% of CPAs are at or near retirement eligibility and fewer than half of firms have a funded succession plan (AICPA) — and exactly then, private equity arrived: roughly half the IPA top 30 took PE money or an alternative practice structure in five years, from TowerBrook/EisnerAmper (Aug 2021) to KKR/Crowe (June 11, 2026). The seller's problem is not finding a buyer — three may already be calling — it is decoding a structurally confusing offer: the alternative practice structure (attest/advisory split), adjusted EBITDA built on partner-comp normalization, rollover equity, and the "second bite." The right advisor for that is not an investment bank; it is a specialist consultant or, for a small practice, a broker. And the traps stale lists repeat are real: "Transition Advisors LLC" no longer exists as a standalone (it is inside Whitman Advisory), CBIZ/Marcum was a strategic deal, not PE, and Rosenberg's $615K is an average, not a median.

Why I wrote this — and how it differs from our other advisor guides

I'm Deqian Jia, co-founder of Peony, a data room company used by 5,900+ customers. I spend most of my time on the part of our product that decides who — and now what — is allowed to read a confidential document, which means I sit on the document side of a lot of professional-services deals, including the wave of accounting-firm sales and mergers that has reshaped the profession since 2021. Selling an accounting firm is the one deal type where the offer is almost designed to be misread: the headline multiple is applied to a number the buyer constructs (adjusted EBITDA after normalizing partner comp), the firm gets legally split in two (the alternative practice structure), and a large part of the "price" is rolled equity and a future "second bite" that may or may not pay. A managing partner who reads "8x adjusted EBITDA" as if it were "8x last year's profit" is off by a wide margin before the first meeting.

We already publish an M&A advisor vs broker vs investment bank hub and sector guides for financial services, software, and technology. This page is the accounting-firm-only cut. It does not re-run the generic advisor-selection decision. Instead it does two things those guides do not: it names the specialist bench that actually sells CPA firms — a set of consultants and brokers, most of which are not investment banks and several of which are not even FINRA-registered (by design, under a 2023 federal exemption) — and it decodes the structural machinery of a modern accounting-firm deal so you can read an offer correctly.

One scope note before the roster. Peony is not an M&A advisor and does not place deals — the firms below do that. Peony is the data-room layer a confidential firm-sale runs on: a room per buyer conversation, staff and client confidentiality, per-viewer watermarking, and engagement analytics. I will flag where that fits at the end, but the advisory firms are the subject here, and the order of operations matters — pick your advisor first.

What's the 2026 landscape — why did private equity arrive exactly when it did?

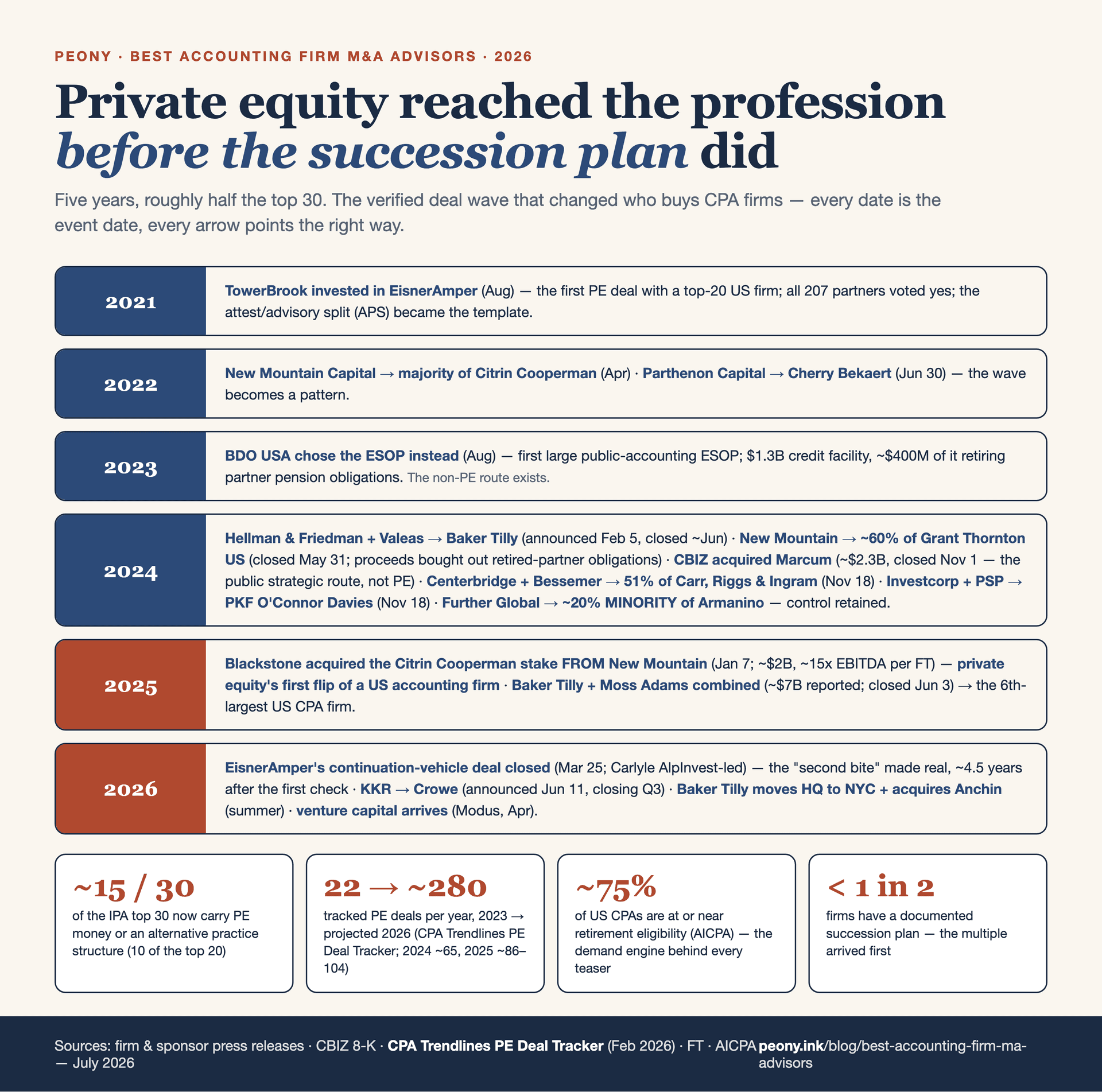

The defining fact of 2026 is a collision between a succession cliff and a capital wave. On the succession side, the AICPA estimates about 75% of today's CPAs are at or near retirement eligibility; at $2M-$10M firms, 65.5% of partners are over 50, and at sole-practitioner and small firms it is 71.1% — yet fewer than half of firms have a succession plan. Into that vacuum came private equity. Roughly half of the IPA / Accounting Today top 30 now carry PE money or an alternative practice structure (about 15 firms), and 10 of the top 20 are PE-backed. The CPA Trendlines "PE Deal Tracker" counts about 250 institutional PE transactions in accounting since 2019 (203 recorded as of its February 16, 2026 update), and the annual cadence has accelerated sharply: roughly 22 deals in 2023, about 65 in 2024, and about 86-104 in 2025 (sources vary — one cites 104 for the full year), with about 280 projected for full-year 2026.

Here is the wave, deal by deal, with directions stated explicitly — because the direction is the fact stale lists most often get wrong:

- Aug 2021 — TowerBrook invested in EisnerAmper, the first PE deal with a top-20 US accounting firm; it split into EisnerAmper LLP (attest) and Eisner Advisory Group (non-attest), and all 207 partners voted unanimously.

- Apr 2022 — New Mountain Capital acquired a majority of Citrin Cooperman (its original PE owner).

- Jun 2022 — Parthenon Capital invested in Cherry Bekaert, splitting Cherry Bekaert LLP (attest) and Cherry Bekaert Advisory LLC.

- Aug 2023 — BDO USA established an ESOP — the first large public-accounting-firm ESOP and an employee-ownership alternative to PE — backed by a $1.3B credit facility, roughly $400M of it earmarked to cover retired-partner pension obligations. CEO Wayne Berson framed it as getting "all the benefits of private equity, without giving up control."

- ~Jun 2024 (closed) — Hellman & Friedman, with Valeas, acquired a majority of Baker Tilly US — the largest US CPA PE deal to that date.

- May 2024 (closed) — New Mountain acquired ~60% of Grant Thornton's non-audit business (with CDPQ and OA Private Capital as minority co-investors); proceeds went partly to buy out retirement obligations from former partners.

- Jul 2024 — Charlesbank Capital Partners invested in Aprio (its first institutional capital).

- Nov 2024 (closed) — CBIZ acquired Marcum — a public-company strategic deal, not PE — for about $2.3B in cash and stock, creating a roughly $2.8B-revenue combination.

- Oct 2024 (closed) — Further Global took a ~20% minority stake in Armanino, which retained control (the only top-20 firm doing a minority PE deal).

- Nov 2024 — Centerbridge Partners, with Bessemer Venture Partners, took a combined 51% voting interest in Carr, Riggs & Ingram (CRI).

- Nov 2024 — Investcorp, with PSP Investments, made a strategic growth investment in PKF O'Connor Davies — with Capstone Partners as sole financial advisor to PKFOD.

- Jan 7, 2025 (announced) — Blackstone acquired the Citrin Cooperman stake FROM New Mountain Capital — reportedly PE's first "flip" of a US accounting firm, valued around $2B (about 15x EBITDA per the Financial Times).

- Jun 2025 (closed) — Baker Tilly and Moss Adams combined (H&F-backed), forming the 6th-largest US CPA firm.

And the freshest 2026 developments, which is why this guide carries a July-2026 date:

- Mar 25, 2026 (closed) — EisnerAmper completed a TowerBrook continuation-vehicle transaction (Carlyle's AlpInvest led, Hamilton Lane co-led) — the "second-bite" liquidity event for the original fund's investors, delivered about 4.5 years after the first check. EisnerAmper is now the 13th-largest US firm, with over $1.2B in revenue and 27 add-on acquisitions since 2021.

- Apr 2026 — Modus raised the first VC-led accounting-platform round (Lightspeed and YC-affiliated investors) — venture capital, not just PE, entering the category.

- Jun 11, 2026 (announced) — KKR agreed to make a "significant equity investment" in Crowe (closing expected Q3 2026), forming Crowe Advisory LLC alongside Crowe LLP.

- Summer 2026 (expected close) — Baker Tilly is acquiring Anchin (a top-100 New York firm founded in 1923) and relocating its HQ from Chicago to New York City.

The takeaway for a managing partner: you are selling into the most active buyer market the profession has ever seen, but "active market" is not the same as "good offer." The next four sections decode what an offer in this market actually means.

Who are the best accounting-firm M&A advisors? (the tiered bench)

For a CPA firm, the advisor bench splits into three tiers, and — this is the part that surprises sellers — the top tier is not investment banks. It is a small set of specialist consultants who have run most of the profession's marquee firm-to-firm and firm-to-PE deals. Below them sit a few registered mid-market banks that run a minority of the largest institutional mandates, and below those are the practice brokers who serve sub-$2M practices selling to individual buyers. The table is the map; each firm is profiled beneath it.

| Firm | HQ | Tier | Registration status | The tell (who it's for) |

|---|---|---|---|---|

| Koltin Consulting Group | Chicago, IL | 1 — consultant | NOT FINRA-registered (M&A-broker exemption) | The most-cited dealmaker in the profession; marquee firm-to-PE deals |

| Whitman Advisory LLC | New York, NY | 1 — consultant | NOT FINRA-registered (M&A-broker exemption) | Largest by raw firm-count; succession + M&A + lateral-partner talent |

| The Visionary Group | US (accounting-only) | 1 — consultant | Unregistered consultant | Top-20 firms down to $2M practices; pairs deals with growth advisory |

| Accountants Advisory Group | New York, NY | 1 — consultant | Unregistered consultant | Deal work plus partner-comp / performance redesign |

| Carl George Advisory | US (professional services) | 1 — consultant | Unregistered consultant | Ex-CLA CEO; governance, succession, partner mentoring |

| Capstone Partners | Boston, MA | 2 — registered bank | FINRA member (Huntington company); no printed CRD | Institutional CPA-firm sell-side; publishes the sector's banker research |

| Berkery Noyes & Co. | New York, NY | 2 — registered bank | Berkery Noyes Securities, CRD #155918 | Registered, capable; core is info/software/HCM — confirm CPA-firm flow |

| Republic Capital Group | New York, NY | 2 — registered bank | CRD #334963 | Registered, reputable; verified deal flow is wealth/RIA, not CPA firms |

| Accounting Practice Sales (APS) | US (national) | 3 — practice broker | NOT FINRA-registered (business-broker model) | The volume marketplace for sub-$2M individual-buyer sales |

| Poe Group Advisors | Charleston, SC | 3 — practice broker | Business-broker/intermediary | The most educational broker; firms up to ~$10M / ~50 staff |

| ProHorizons | San Mateo, CA | 3 — practice broker | Business-broker/intermediary | West-Coast tax/accounting practices, ~$80K to several $M |

| Accounting Biz Brokers | US (national) | 3 — practice broker | Business-broker/intermediary | Small/solo practice listing-and-match (thin public detail) |

A quick note on registration before the profiles, because it looks alarming and is not. I print a CRD only for Berkery Noyes (#155918) and Republic Capital (#334963) — the two firms whose registration I verified on BrokerCheck. Koltin, Whitman, and APS are not FINRA-registered, and that is deliberate on their part: they operate under the federal M&A-broker exemption that took effect March 29, 2023, which lets an intermediary facilitate the sale of a privately held company (within statutory size limits) without registering as a broker-dealer, as long as no public securities offering is involved. For a firm-to-firm or firm-to-PE accounting deal, that exemption fits — so "not on BrokerCheck" is not a red flag here; it is the expected status for these specialists. The right move is to confirm which basis a firm operates under and get it in writing.

Tier 1 — The category-defining CPA-firm M&A consultants

Koltin Consulting Group (led by Allan D. Koltin, based in Chicago) is the single most-cited dealmaker in the accounting profession and the name to know first. Koltin has advised on more than 250 M&A deals in accounting with combined value exceeding $5B, and he is the connective tissue of the PE era — retained by both the top-30 firms and the PE sponsors buying them. His verified deal record reads like the wave itself, with directions stated: he advised on Blackstone's acquisition of the Citrin Cooperman stake FROM New Mountain (announced Jan 7, 2025), on Citrin Cooperman's merger-in of Berdon LLP (2022, primary advisor to both), on the CBIZ/MHM combination with Somerset (2023, both sides), and on Marcum's merger-in of Melanson (both sides). He has been an Accounting Today Top 100 Most Influential figure for 26 consecutive years (#2 in 2023 and 2024) and a Crain's Chicago Notable M&A Dealmaker in 2025. On registration: Koltin is not FINRA-registered (BrokerCheck returns zero registered firms under "Koltin," verified July 2026) — he operates under the M&A-broker exemption. For a firm fielding platform-level PE interest and trying to read the market correctly, Koltin is the reference name.

Whitman Advisory LLC (CEO Phil Whitman, New York) is the largest of these firms by raw firm-count — its principals have been "involved in the acquisition, sale, and/or merger of over 1,000 CPA firms" — and it is also the firm at the center of the profession's most common stale-list error. The name matters: in 2022, Transition Advisors LLC (Joel Sinkin and Terry Putney) merged with Whitman Business Advisors to form Whitman Transition Advisors, and in 2026 it rebranded to Whitman Advisory LLC. "Transition Advisors LLC" no longer exists as a standalone firm — Sinkin and Putney are now Whitman partners — so any list that still names it separately is out of date. Whitman covers succession, M&A, practice sales, and, distinctively, lateral-partner recruiting and fractional-CFO services, which makes it a natural fit when a firm's succession problem is really a talent problem. It is not FINRA-registered (M&A-broker exemption).

The Visionary Group (President Bob Lewis, an Accounting Today Top 100 Most Influential figure) is the accounting-only consultancy that spans the widest size range — "top-20 firms to emerging $2M practices" — with about 30 years in the sector. Its distinctive move is pairing deal facilitation (sell-side, upward mergers, and buy-side searches for acquirers) with "Chief Growth Officer" and outsourced-advisory engagements, so it is a strong fit for a firm that wants growth help alongside a transaction, or one that is as likely to buy as to sell. It is an unregistered consultant (no CRD located).

Accountants Advisory Group (New York-centric) runs direct M&A work — candidate identification, diligence, negotiation, valuation, and contracts — but its differentiator, and the reason it belongs on this list for your situation specifically, is that it also does strategic and succession planning and partner-compensation design. Its advisors are CPAs with CPA-industry executive backgrounds, so it speaks the partner-comp-normalization language natively — which is the single most confusing part of an accounting-firm valuation. (A trap worth clearing up: there is no CPA-firm M&A advisor called "Ashford Advisors" — that name belongs to an unrelated Oregon CPA firm and a Guardian Life insurance agency. The genuine consultancy people are reaching for is Accountants Advisory Group.) It is an unregistered consultant.

Carl George Advisory, LLC (founded 2013 by Carl R. George) is the operator-turned-advisor on this bench. George was CEO of Clifton Gunderson and led it through the merger that created CliftonLarsonAllen (CLA) — meaning he has sat in the managing-partner seat through a top-tier combination, which most advisors never have. His practice is governance and structure, strategic and succession planning, CEO and partner mentoring, and M&A consulting — the right call when the hardest part of your decision is the internal one (partner alignment, governance, and whether the next generation can carry the firm) rather than sourcing a buyer. He is an unregistered consultant (40+ years in the profession).

Tier 2 — Registered mid-market banks running a minority of CPA-firm mandates

Capstone Partners (Boston; part of Capstone Partners, a Huntington Bancshares company) is the registered bank that most genuinely runs institutional CPA-firm sell-side work — it has a dedicated Accounting Services M&A practice and publishes the sector's most-cited banker research (the "Accounting Services M&A Update"). Its verified mandate: Capstone served as sole financial advisor to PKF O'Connor Davies on the strategic growth investment it received from Investcorp and PSP Investments (announced Nov 18, 2024). The registration nuance is that the parent's IB arm is a FINRA member, but I could not pin the exact broker-dealer entity and CRD, so — consistent with the honesty rule of this guide — I do not print a Capstone CRD; verify it directly. (Name-collision trap: this Boston IB is not "Capstone Accounting and Tax," an unrelated Oregon CPA firm that itself took PE from Seaside Equity in April 2025, nor Capstone Wealth Partners or Capstone CPA Group.) For a scaled firm that wants a true banker-run process, Capstone is the strongest Tier-2 name.

Berkery Noyes & Co. (New York) is a legitimate, registered middle-market investment bank — Berkery Noyes Securities, LLC, CRD #155918 (verified active on BrokerCheck, July 2026) — founded in 1983, with 500-plus sell- and buy-side deals since 1988. The honest caveat: Berkery Noyes's core is information, software, and human-capital-management deals, and no specific recent CPA-firm mandate was verified this cycle. So include it as capable and registered but confirm active CPA-firm deal flow before you assume it is the right fit — do not overclaim it as an accounting-firm specialist.

Republic Capital Group (New York) is likewise registered and reputable — CRD #334963 (verified active, July 2026), an independent IB founded in 2015 with about $150B in client assets transacted since 2022 and a 2023 "Boutique Investment Banking Firm of the Year" award (M&A Advisor). It lists accounting firms among its verticals — but its verified deal flow is heavily wealth- and asset-management / RIA work, and no specific CPA-firm transaction was verified. Treat it as a possible fit worth a conversation, not a proven accounting-firm desk, and ask directly for CPA-firm references.

One reference-and-trap note that belongs here rather than in a profile: Houlihan Lokey and William Blair are the wrong mandate type for this seller. Houlihan Lokey's Business Services group covers "accounting and legal services" and it runs a large Transaction Advisory Services (quality-of-earnings / financial-due-diligence) practice — but that is diligence support and coverage of accounting-services companies broadly, not a "sell my $12M CPA firm" desk; William Blair's accounting-adjacent work is similarly wealth- and asset-management-oriented. Do not shortlist either as your sell-side advisor for a firm this size.

Tier 3 — Practice brokers (sub-$2M practices) — honest size framing

These four are the right call for a sole practitioner or a sub-$2M firm selling to an individual buyer, and a mismatch for a $12M, 8-partner firm fielding PE interest. I frame them by size honestly rather than pretending they compete for platform deals.

Accounting Practice Sales (APS) is the volume marketplace of the small-practice world — it markets itself as "#1 in Sales & Acquisitions," reports about $2B in cumulative deals closed, 301 practices sold in 2025, and 140,000+ registered buyers over 25-plus years, on a listing-and-commission model (the rate is not published). It is not FINRA-registered (verified zero on BrokerCheck) — an exempt business-broker model — and it is the right venue for a small firm or sole practitioner selling to an individual, and the wrong one for a firm that needs a competitive process among PE platforms. Note that APS does not publish a multiple table — it markets a free valuation questionnaire — so any revenue multiple you see attributed to it is third-party inference, not its own number.

Poe Group Advisors (Charleston, SC; founded ~2003 by Brannon Poe, CPA, ex-Big-Four) is the most educational broker — it publishes a valuation blog and runs an "Accounting Practice Academy," and it targets practices under ~50 employees / up to ~$10M revenue. Poe is worth reading even if you do not hire him, because he openly argues the market has shifted away from the old "1x gross revenue" rule of thumb toward EBITDA- and profitability-based pricing — citing owner-dependent firms at roughly 3x-6x EBITDA versus scalable PE-platform targets at roughly 4x-7.5x EBITDA and up. That reframing is exactly right, and it is the antidote to the revenue-rule-of-thumb trap.

ProHorizons (San Mateo, CA; broker Ken Berry) has brokered West-Coast accounting and tax practices since 1995, covering practices from about $80K to several million in revenue — a straightforward regional practice brokerage for the small end of the market.

Accounting Biz Brokers is a national small- and solo-practice brokerage on a listing-and-match model. Public detail is thin, so I include it for completeness with a low-confidence flag on specifics rather than overstating what is verifiable.

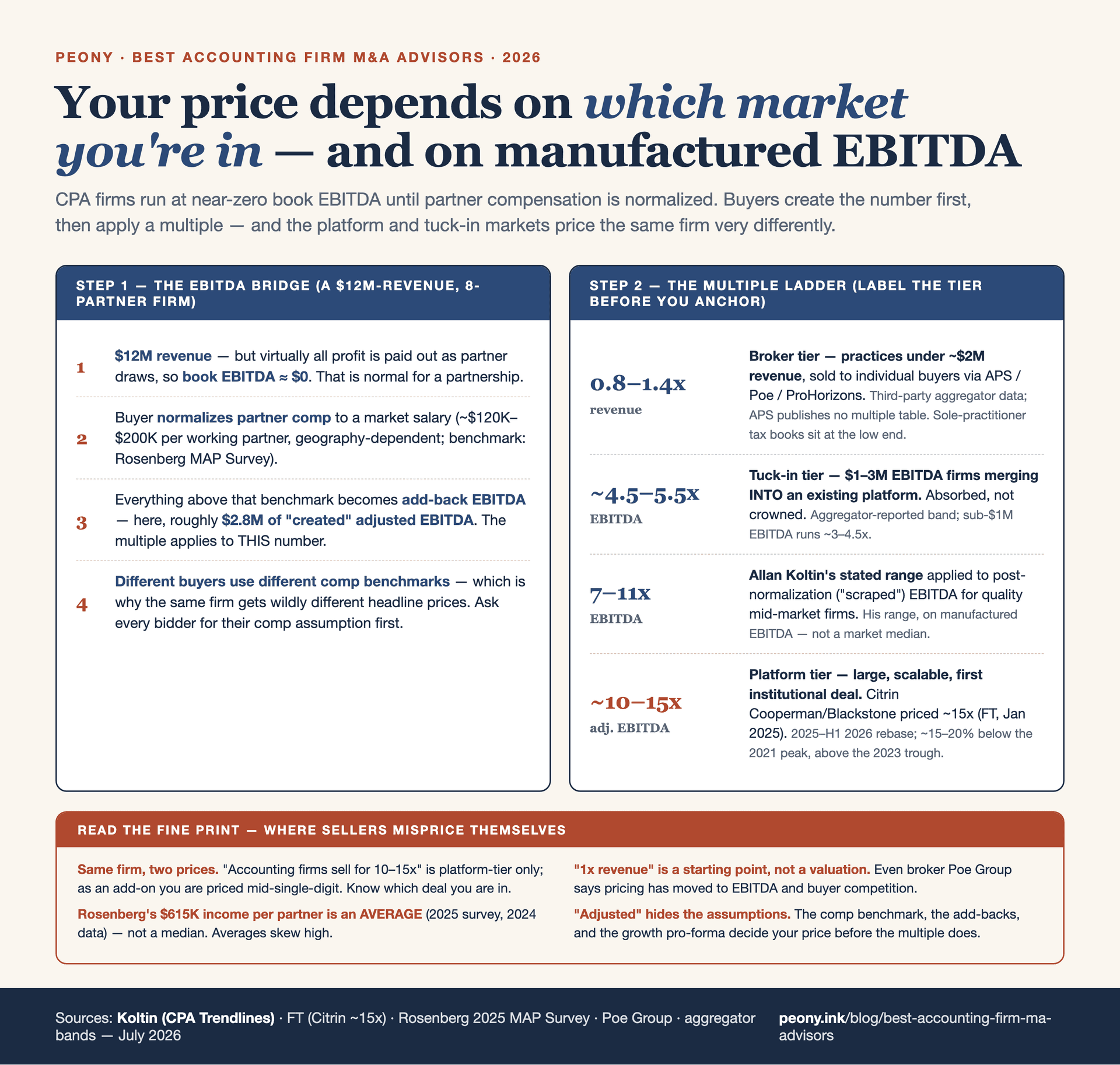

What multiple are accounting firms selling for in 2026 — and why is it two different markets?

The most important discipline in reading 2026 accounting-firm valuations is that there is no single multiple — there are two markets, and which one you are in changes your number more than any negotiation will. The chart below is the whole picture; the labeled anchors follow.

Here are the anchors, each labeled by whose data it is and what kind of figure it is:

- Platform tier — ~10x-15x adjusted EBITDA (range-reported for large, scalable, first-PE-deal firms across 2025-H1 2026). The Citrin Cooperman stake Blackstone bought was valued around 15x EBITDA per the Financial Times. This is the number that makes headlines — and it applies to platforms, not to most firms.

- Tuck-in tier — mid-single-digit EBITDA. A $5M-$20M firm merging INTO an existing platform prices far lower than the platform headline — because the buyer is absorbing you as an add-on, not acquiring a standalone platform. Same firm, different multiple, depending on the role you play in the deal.

- Koltin's stated range — 7x-11x applied to the manufactured (post-comp-scrape) EBITDA, with general PE valuations he cites around 8x-10x. Label this as Koltin's own stated range, not a market-wide constant.

- Practice-broker tier — ~0.8x-1.4x annual gross revenue for sub-$2M practices. Critically, this is third-party aggregator data (e.g., CT Acquisitions, Auxo), NOT APS's own published table — APS publishes no multiple. Sole-practitioner tax practices sit at the low end (~0.5x-0.8x); multi-partner advisory-heavy practices higher.

- Rosenberg (MAP) Survey — $615K income per partner (2025 survey on 2024 data). This is an AVERAGE, never a median — the distinction matters because a handful of large firms pull the average up.

Two calibrations. First, where the market sits versus its peak: platform multiples peaked around 12x-15x in 2020-2022, compressed during the 2023-2024 rate shock (the Fed reached 5.25%-5.50% by July 2023), and rebased to roughly 10x-15x in 2025-H1 2026 after rate cuts — broadly ~15-20% below the 2021 peak and ~10-15% above the 2023 trough. Second, and most important for you: your number depends on whether you are a platform or a tuck-in, and on your normalized EBITDA — not on a revenue rule of thumb. That is what the next section unpacks.

The mechanic that decides your price: partner-comp normalization

This is the #1 seller confusion, and it is worth its own explainer because it moves your headline more than the multiple does. CPA firms historically show near-zero EBITDA — the profit is paid out as partner compensation, so there is little "earnings" left on the books. A buyer therefore normalizes partner comp: it resets each working partner's pay to a market-rate salary (roughly $120K-$200K, depending on role and geography, benchmarked to surveys like Rosenberg's MAP Survey) and treats the excess above that benchmark as add-back EBITDA. Koltin's blunt version: firms "traditionally have zero EBITDA and need to create it through partner-compensation 'scrape' strategies," and a multiple is then applied to that manufactured number.

The consequence is the thing to internalize: different buyers apply different fair-comp assumptions, which produces wildly different headline prices for the exact same firm. Two platforms can both quote "you a strong multiple" and land millions apart purely because one assumed a $150K fair salary and the other assumed $180K. So the multiple is only half the conversation — the comp assumption underneath it is the other half, and you cannot compare two offers until you have rebuilt both on the same normalized base.

What does "adjusted EBITDA" hide — a worked example with your numbers

"Adjusted EBITDA" is where the price is really set, so let me run it with the persona's numbers to make the machinery concrete. Say your firm does $12M in revenue and, after normalizing partner comp, shows about $2.8M in normalized EBITDA. That $2.8M did not come off your tax return — it was built by the normalization above, plus the usual add-backs (owner perks, one-time costs, non-market rent to a partner-owned entity). At an 8x headline that is about $22.4M of enterprise value.

Now watch how sensitive that is to a single assumption. Suppose a buyer's "fair comp" figure for a working partner is $30K per partner higher than another buyer's. Across 8 partners, that is $240K less add-back, so normalized EBITDA drops from $2.8M to about $2.56M — and at 8x, the headline falls by roughly $1.9M, from about $22.4M to about $20.5M. Nothing about your firm changed — only the comp assumption did. That is what "adjusted" hides: not fraud, but a set of judgment calls, each of which is negotiable and each of which moves real money.

The practical defense is simple and it is the same one every good advisor will run: get every add-back and the exact partner-comp assumption in writing, and rebuild the bridge with your own advisor so you are comparing offers on an identical normalized base. An offer is not "8x" — it is "8x of a number the buyer chose," and the number is where you negotiate.

How does the alternative practice structure (APS) work — and what happens to your audit practice?

When PE buys a CPA firm, it cannot simply buy the whole thing, because CPA-ownership rules forbid it — so the firm is split in two, and that split is the alternative practice structure (APS). The mechanism: the firm divides into a licensed attest entity (audits, reviews, and other attest work) that must stay majority-owned by CPAs who actively participate, and a separate advisory / non-attest entity (tax, advisory, outsourcing) that receives the PE capital. Partners generally roll their equity into the PE-owned advisory entity, while the attest entity is carved out under CPA control.

The reason it is forced is regulatory: the AICPA Code (the Independence Rule and the Form-of-Organization-and-Name Rule) and state boards require attest firms to be majority CPA-owned and independent — Illinois, for instance, requires 51% of a CPA firm's owners to be CPAs who actively participate — and SEC/PCAOB independence rules bear on any public-company audit clients. Every PE deal in the wave used this shape: EisnerAmper LLP + Eisner Advisory Group, Baker Tilly US LLP + Baker Tilly Advisory Group, Cherry Bekaert LLP + Cherry Bekaert Advisory LLC, and, in the June 2026 KKR deal, Crowe LLP + the newly formed Crowe Advisory LLC.

The part to watch, because it is live and moving: the AICPA was updating its APS ethics rules in 2025 (open for comment), and state boards are actively scrutinizing arrangements where PE exercises effective control despite a nominal CPA majority. So do not treat the APS as settled boilerplate. Have counsel confirm three things specifically: what your partners actually sign, who legally owns what, and whether your particular attest clients — especially any public-company or PCAOB-registered work — create independence constraints that the structure has to accommodate. For a firm with meaningful attest work, the APS is not a formality; it is the center of the deal.

Is rollover equity and the "second bite" real money, or a sales pitch?

It can be real — there are disclosed examples where it paid — but it is genuinely at risk and it is not the same mechanic in every deal, so treat the second-bite projection as a range, not a promise. The typical structure: you take cash at close on part of the price and roll the rest into equity in the PE-owned advisory entity, then receive a "second bite" when the sponsor recapitalizes or sells again. Koltin frames the arc as a day-one check, a second bite in years three to four, and a larger recap or sale in years four to seven.

Two real, disclosed outcomes show the two distinct shapes — and it is important to keep them separate:

- EisnerAmper — the continuation-vehicle second bite, sponsor STAYED. TowerBrook invested in August 2021; on March 25, 2026, EisnerAmper completed a continuation-vehicle transaction (Carlyle's AlpInvest led, Hamilton Lane co-led) that delivered liquidity to the original fund's investors roughly 4.5 years after the first check, after the firm grew past $1.2B in revenue with 27 add-ons. The sponsor remained in the business through a new fund vehicle.

- Citrin Cooperman — the "flip," sponsor CHANGED. Blackstone acquired the stake FROM New Mountain Capital (announced January 7, 2025), valued around $2B / ~15x EBITDA per the Financial Times. Here the sponsor changed hands — a different mechanic entirely from a continuation vehicle, even though both delivered a "second" liquidity event.

Do not conflate the two: one is the same sponsor extending its hold and cashing out its fund; the other is one sponsor selling to another. What to do about your own rollover: value the deal on the cash you are certain to receive at close, model the second bite as upside contingent on the sponsor hitting its growth plan, and ask specifically how your rollover is valued, what governance and drag/tag rights attach, and whether it is common or preferred equity — because those terms determine whether the second bite is a real claim or a soft one.

Partner economics: after-tax mechanics, deferred comp, and the partner vote

Three partner-level realities sit underneath every headline, and they are where a "good multiple" turns into what each partner actually keeps.

After-tax, at a high level (model it with your advisor — this is not tax advice). The headline enterprise value is reduced, in order, by the cash/rollover/earnout split (broker-tier deals often run 70-80% cash at close with a 20-30% retention holdback over two to three years; platform deals roll a meaningful slice into the advisory entity), then by any deferred-comp or retired-partner obligations the proceeds must retire first, then allocated unequally across partners under your partnership agreement, and only then taxed at each partner's own rate and gain character. The point is that price-divided-by-partners is not a real number — build a per-partner waterfall from actual cash at close, with your tax counsel.

The unfunded-deferred-comp driver — often the real reason firms sell. Because these obligations are unfunded (a promise to pay retiring partners from future earnings, with no assets set aside), they compete directly with the money the next generation would use to fund an internal buyout — which is why an outside capital event is frequently the cleaner way to retire them. The precedent is explicit: Grant Thornton used deal proceeds partly to buy out retirement obligations from former partners, and BDO earmarked roughly $400M of its $1.3B ESOP facility for retired-partner pensions. One structural wrinkle: under ERISA, a PE fund owning 80% or more of a portfolio company can inherit certain pension liabilities, which is one reason some sponsors deliberately cap at a minority stake (Armanino's investor took about 20%).

The partner vote. Partnership sales typically require a supermajority or near-unanimous vote, which means the deal cannot proceed until the economics are laid out clearly enough that skeptical partners can see their own outcome. The reason EisnerAmper's 207 partners voted unanimously is that the structure and payouts were worked out before the vote, not during it — which is the template for resolving a split partner group: model per-partner outcomes and evaluate internal succession and a PE deal on the same page, so the vote is about economics rather than personalities.

What are the alternatives to a PE sale?

Selling to a PE platform is one option, not the only one — and a good advisor will make you weigh it against these before you sign anything.

- Internal succession. Keep ownership with the next generation, funded out of future firm cash flow over 5-10 years. The honest constraint is that this money collides with unfunded deferred comp — which is exactly why so many firms that lack a funded plan end up selling instead.

- ESOP (employee ownership). BDO USA established the first large public-accounting-firm ESOP in August 2023, backed by a $1.3B facility, with CEO Wayne Berson framing it as "all the benefits of private equity, without giving up control." An ESOP can provide partner liquidity and retire retirement obligations without handing control to an outside sponsor — a real alternative for firms philosophically opposed to PE.

- The "stay independent with capital" platforms. Ascend (launched 2023 by Alpine Investors, roughly 14 sector deals) offers firms in the ~$10M-$50M range an "operating system" of shared services while letting them stay independent with capital — a middle path between full sale and going it alone. Springline Advisory (Trinity Hunt Partners, with MarksNelson as the founding firm) and Crete Professionals Alliance (a ~$500M AI-first roll-up backed by Thrive, ZBS, and Bessemer) are variants of the same mid-market platform model.

- The strategic route. A public-company strategic buyer is a distinct path from PE — CBIZ acquired Marcum in a roughly $2.3B cash-and-stock deal (closed November 2024), a strategic combination rather than a sponsor recap, with a different governance and currency (public stock) than a PE deal.

- IPO. None has happened yet in this wave — but Koltin predicts up to three IPOs of significant accounting/consulting firms in 2026-2027. Label that as his prediction, not a done deal; it is a watch-item, not an option you can pursue today.

Who NOT to call — and what stale lists get wrong

Every directory-style "best accounting firm M&A advisor" list repeats the same avoidable errors. Here are the traps that matter, with the correct facts:

- "Transition Advisors LLC" no longer exists as a standalone firm. It merged into Whitman in 2022 and the combined firm rebranded to Whitman Advisory LLC in 2026. Stale lists still name it separately — do not shortlist a firm that is now part of another.

- "Ashford Advisors" is not a CPA-firm M&A advisor. That name belongs to an unrelated Oregon CPA firm and a Guardian Life insurance agency. The genuine consultancy is Accountants Advisory Group.

- There are two different "Capstone Partners." The Boston investment bank (which ran the PKFOD mandate) is not "Capstone Accounting and Tax," an unrelated Oregon CPA firm that itself took PE from Seaside Equity in April 2025 — nor Capstone Wealth Partners or Capstone CPA Group.

- Republic Capital Group is a wealth/asset-management deal shop first. It is registered (CRD #334963) and reputable, but its verified deal flow is RIA and wealth, not CPA-firm sales. Possible mismatch — verify a current CPA-firm mandate before assuming fit.

- Houlihan Lokey and William Blair are the wrong mandate type. Their accounting-adjacent work is quality-of-earnings / financial-due-diligence support and financial-services coverage — not "sell my $12M CPA firm" desks.

- Brokers topping out at sub-$2M are a mismatch for a $12M+ firm. APS, ProHorizons, and Accounting Biz Brokers excel at sole-practitioner-to-few-$M individual-buyer sales, not competitive processes among PE platforms.

- Big Four independence conflicts. A Big Four firm cannot advise on your sale where it audits a counterparty — and it does not run mid-market CPA-firm sale mandates anyway.

- "Practice-management consultants/coaches" are not deal-runners. Confirm any advisor will actually quarterback diligence, valuation, and negotiation, not just coach the practice.

- Berkery Noyes is registered and capable, but its core is information/software/HCM. Confirm active CPA-firm deal flow before treating it as an accounting-firm specialist.

- The "revenue rule of thumb" is itself a trap. Even Poe says pricing has moved to EBITDA — anchoring on "1x revenue" mis-prices a firm that a platform values on normalized EBITDA.

What do these advisors charge?

There is no published fee schedule for the CPA-firm consultants, so I will not invent one — instead, here is how the fee models work across the three tiers, matched to which advisor you need. The Tier 1 consultants (Koltin, Whitman, The Visionary Group, Accountants Advisory Group, Carl George) typically work on a negotiated consulting basis — a retainer and/or a success component — but none publishes a standard percentage, so any specific number attributed to them is inference. The Tier 2 registered banks (Capstone, Berkery Noyes, Republic Capital) run institutional sell-side mandates and are generally paid a success fee at close, often tiered, plus a work fee — the standard lower-middle-market pattern. The Tier 3 brokers (APS, Poe, ProHorizons, Accounting Biz Brokers) work the sub-$2M market on a listing-and-commission model, and even there the rate is not publicly posted.

Two things move the real number more than the headline rate, on any deal: the minimum fee (on a smaller deal the floor, not the percentage, can set the bill) and the definition of transaction value (a broad definition that sweeps in rollover and earnout inflates the base on the same headline price — which matters enormously here, because rollover is a large part of an accounting-firm deal). Get the fee structure, the minimum, the transaction-value definition, and the tail in writing from every advisor. For the full mechanics — Modified-Lehman and Double-Lehman math, retainer credits, and the engagement-letter clauses that quietly inflate the base — see our M&A advisor fees guide.

Where does Peony fit in an accounting-firm sale?

Whichever advisor wins your mandate, the process runs out of a data room — and a firm sale carries unusually sensitive material: partner-level compensation and capital accounts, client-level revenue and retention data, engagement letters, and the details of who is retiring and what they are owed. We built Peony, a data room company used by 5,900+ customers, to be the confidential-process layer under whichever advisor you hire: a separate data room per buyer conversation so competing platforms and consolidators see only what they should, per-viewer watermarks on every render so a leaked page is traceable to the party that leaked it, dynamic NDA gating before access, and page-level analytics that show your advisor which buyers actually read the confidential memorandum and which held back. In a firm where 55% of revenue is recurring compliance work and a leak could spook the very clients and staff the deal is built to retain, that confidentiality is not a nicety — it is how you keep the asset intact through a months-long process.

Two honest scoping notes, in the same spirit as the rest of this guide. Peony is not an M&A advisor and does not place deals — the firms above do that; Peony is the layer that makes the diligence run cleanly once you have hired one, and I want to be explicit that we take no side in the sell-versus-succeed decision. And the order of operations matters: pick your advisor first, then stand up the room. For the room buildout, see our M&A data room playbook and sell-side due diligence guide; for reading buyer intent during a targeted process, our data-room analytics guide covers the engagement signals that separate serious buyers from tire-kickers. Peony serves 5,900+ customers on exactly this document layer.

The bottom line

Accounting-firm M&A in 2026 is defined by one fact: the multiple arrived before the succession plan. With about 75% of CPAs near retirement, fewer than half of firms carrying a funded succession plan, and roughly half the IPA top 30 already holding PE capital, the seller's problem is not finding a buyer — it is reading the offer. And the machinery is genuinely confusing: the price is applied to a constructed adjusted-EBITDA number (partner-comp normalization moves it more than the multiple does), the firm is split in two under the alternative practice structure, and a large part of the "price" is rolled equity and a second bite that may or may not pay. The advisor for that is not an investment bank — it is a specialist consultant (Koltin, Whitman Advisory, The Visionary Group, Accountants Advisory Group, Carl George Advisory), or, for a small practice, a broker (APS, Poe, ProHorizons, Accounting Biz Brokers), with the registered banks (Capstone, Berkery Noyes, Republic Capital) running a minority of the largest mandates. Model internal succession, ESOP, and a PE deal on the same page; get every add-back and the partner-comp assumption in writing; and remember the direction of the deals stale lists get wrong (Blackstone bought Citrin from New Mountain; CBIZ/Marcum was strategic, not PE; Rosenberg's $615K is an average). Pick your advisor first; the data room comes after.

Related resources

- Best M&A Advisors in Chicago — the geo cut for Allan Koltin's home market, the single most-cited dealmaker in accounting-firm M&A

- Best Financial Services M&A Advisors — the adjacent sector bench: where wealth-management, insurance, and RIA sellers go (and where Republic Capital's real deal flow sits)

- M&A advisor vs broker vs investment bank — the decision that comes before this shortlist: which of the three intermediary types should sell your firm

- M&A advisor fees: what you actually pay — Modified-Lehman and Double-Lehman math, retainer credits, minimum-fee floors, and the transaction-value definition that inflates the base when rollover is involved

- Sell-side due diligence: how to prepare — tying out your normalized-EBITDA bridge and partner-comp add-backs before a buyer's quality-of-earnings review

- M&A data room: setup and workstream mapping — the general sell-side data-room playbook for a confidential firm sale

- Data-room analytics: how to spot serious buyers — reading buyer intent from engagement data during a targeted process

- How to write a CIM — the confidential memorandum a specialist builds around your recurring-revenue base and normalized economics

- Best Software M&A Advisors and Best Technology & Software M&A Advisors — the sector cuts for software and tech sellers, if your firm's value is really its technology

- City guides: Milwaukee, Detroit, St. Louis, and Houston — geo benches for owners who want a locally grounded advisor conversation

Frequently asked questions

I run a $12M, 8-partner CPA firm with no funded succession plan — should we sell to private equity or fund an internal buyout?

There is no default answer — the honest one is that this is a math-and-timeline decision, not a values decision, and you should model both paths before you talk to a single buyer. The mechanism: an internal buyout keeps ownership with the next generation of partners but has to be funded out of future firm cash flow, which is exactly the money your two retiring partners' roughly $6M of unfunded deferred comp is already claiming — that collision is why fewer than half of firms have a funded succession plan (AICPA) and, per Allan Koltin, is often the real reason a firm sells. A PE or platform sale puts outside capital on the table now, typically as cash at close plus rolled equity into a PE-owned advisory entity, and platform-tier deals in 2025-H1 2026 have been reported around 10x-15x adjusted EBITDA — but only after your partner comp is normalized to market salary, which changes the number more than the multiple does (see the valuation section). What to do: build two side-by-side models — internal succession funded over 5-10 years versus a PE deal with a stated cash/rollover split — and have a specialist consultant (Koltin, Whitman Advisory, The Visionary Group, Accountants Advisory Group, or Carl George Advisory) and your tax advisor pressure-test both before you let an inbound offer set the agenda. Peony is not an M&A advisor and takes no side in that choice — pick your advisor first; we are only the data-room layer the confidential process later runs on.

The teaser we got says "8x adjusted EBITDA" — what does "adjusted" actually hide?

"Adjusted" is where most of the price is actually decided, and the single biggest adjustment for a CPA firm is partner-compensation normalization — so read the teaser as a claim about a number the buyer constructed, not a number off your tax return. Here is what is actually happening: accounting firms historically show near-zero EBITDA because the profit is paid out as partner comp, so a buyer normalizes each working partner's pay down to a market-rate salary (roughly $120K-$200K depending on role and geography, benchmarked to surveys like Rosenberg) and counts the excess as add-back EBITDA. Koltin puts it bluntly: firms "traditionally have zero EBITDA and need to create it through partner-compensation 'scrape' strategies," and a multiple is then applied to that manufactured number. On a $12M firm with about $2.8M of normalized EBITDA, an 8x headline is roughly $22.4M of enterprise value — but change the assumed fair-comp figure by $30K a partner across 8 partners and you move EBITDA by about $240K and the headline by roughly $1.9M at 8x, on the exact same firm. What to do: before you react to any multiple, ask the buyer to show its partner-comp assumption and every add-back in writing, and rebuild the bridge with your own advisor so you are comparing offers on the same normalized base — because two buyers can quote wildly different prices for your firm purely by choosing different comp assumptions.

What multiple are accounting firms actually selling for in 2026?

There is no single multiple — there are two markets, and which one you are in matters far more than the exact number. Platform-tier PE deals (a large, scalable firm taking its first institutional capital) have been reported in a roughly 10x-15x adjusted EBITDA range across 2025 and the first half of 2026; the Citrin Cooperman stake Blackstone bought was valued at about 15x EBITDA per the Financial Times. Tuck-in deals (a $5M-$20M firm merging into an existing platform) price far lower — mid-single-digit EBITDA — for the same underlying firm, because the buyer is absorbing you rather than acquiring a standalone platform. Koltin's own stated range is 7x-11x applied to the manufactured (post-comp-scrape) EBITDA, with general PE valuations he cites around 8x-10x. For sub-$2M practices the market is different again: third-party aggregators (not APS's own published table, which does not exist) put it near 0.8x-1.4x of annual gross revenue. What to do: figure out honestly whether you are a platform or a tuck-in — a $12M, 8-partner firm fielding platform interest can be either depending on the buyer — and treat every multiple you are quoted as attached to a specific normalized-EBITDA base and a specific buyer role, never as a market-wide fact.

How does the alternative practice structure work when PE buys a CPA firm — and what happens to our audit practice?

The alternative practice structure (APS) splits your firm in two so that private-equity money can come in without violating CPA-ownership rules, and your attest practice is the piece that stays CPA-controlled. The mechanism: the firm divides into a licensed attest entity (audits, reviews, and other attest work, which must stay majority-owned by CPAs who actively participate — Illinois, for example, requires 51% CPA ownership) and a separate advisory/non-attest entity (tax, advisory, outsourcing) that receives the PE capital. Partners generally roll their equity into the PE-owned advisory entity, while the attest entity is carved out under CPA control to satisfy the AICPA Code (the Independence and Form-of-Organization rules) and state-board and SEC/PCAOB independence requirements. Every 2021-2026 PE deal used this shape — EisnerAmper LLP plus Eisner Advisory Group, Baker Tilly US LLP plus Baker Tilly Advisory Group, and the newly formed Crowe Advisory LLC alongside Crowe LLP in the June 2026 KKR deal. Practically: treat the APS as a live regulatory area, not settled boilerplate — the AICPA was updating its APS ethics rules in 2025 and state boards are actively scrutinizing structures where PE holds effective control despite a nominal CPA majority — so have counsel confirm what your partners actually sign, who owns what, and whether your specific attest clients (especially any public-company or PCAOB-registered work) create independence constraints.

Is rollover equity and the "second bite of the apple" real money, or a sales pitch?

It can be real, and there are disclosed examples where it paid — but it is genuinely at risk, and it is not the same thing in every deal, so treat the projection as a range, not a promise. The mechanism: in a typical deal you take cash on part of the price at close and roll the rest into equity in the PE-owned advisory entity, then get a "second bite" when the sponsor recapitalizes or sells again — Koltin frames the arc as a day-one check, a second bite in years three to four, and a larger recap or sale in years four to seven. Two real, disclosed outcomes show both shapes: EisnerAmper's rolled investors got liquidity through a TowerBrook continuation-vehicle transaction that closed March 25, 2026, roughly 4.5 years after the first 2021 check and after the firm grew past $1.2B in revenue with 27 add-ons — and the sponsor stayed. Citrin Cooperman was the other shape, a "flip": Blackstone acquired the stake FROM New Mountain Capital (announced January 7, 2025, valued around $2B / ~15x EBITDA per the FT), so the sponsor changed. What to do: value the deal on the cash you are certain to receive at close, model the second bite as upside that depends on the sponsor hitting its growth plan, and ask specifically how your rollover is valued, what governance and drag/tag rights attach to it, and whether it is common or preferred equity.

With 8 partners, how much does each of us actually clear after tax in a sale?

Nobody can give you a per-partner after-tax number without your allocation and your tax situation — and any advisor who quotes one from the headline price is skipping the four things that actually determine it. The mechanism: the headline enterprise value is reduced, in order, by (1) how the price splits across cash-at-close versus rolled equity and earnout — broker-tier deals often run 70-80% cash at close with a 20-30% retention holdback over two to three years, and platform deals roll a meaningful slice into the advisory entity; (2) any unfunded deferred comp or retired-partner obligations the proceeds have to retire first (Grant Thornton explicitly used deal proceeds to buy out retirement obligations; your roughly $6M is a first claim on the money); (3) how the total is allocated among your 8 partners under your partnership agreement, which is rarely equal; and (4) the character of the gain and each partner's own tax position. So a $22M headline is not $2.75M a partner — it is the headline minus rollover, minus the deferred-comp buyout, allocated unequally, then taxed. The move: do not anchor on price-divided-by-partners; have your advisor and tax counsel build a per-partner waterfall from actual cash at close, and model it as "cash now versus rolled equity at risk" for each partner rather than one blended figure. This is high-level structure, not tax advice — retain your own tax counsel.

Two of our partners retire within four years — what happens to ~$6M of unfunded deferred comp in a sale?

Unfunded deferred comp does not disappear in a sale — it gets addressed explicitly in the deal, and it is frequently the reason the deal happens at all. Why: because the obligation is unfunded (a promise to pay retiring partners out of future firm earnings, with no set-aside assets behind it), it competes directly with the internal-buyout money the next generation would otherwise use — which is why an outside capital event can be the cleaner way to retire it. Real precedent: Grant Thornton used proceeds from the New Mountain deal partly to buy out retirement obligations from former partners, and BDO earmarked roughly $400M of its $1.3B ESOP facility for retired-partner pensions. One structural wrinkle worth knowing: a PE fund owning 80% or more of a portfolio company can, under ERISA, inherit certain pension liabilities, which is one reason some sponsors deliberately cap at a minority stake (Armanino's PE investor took about 20%). What to do: put the roughly $6M on the table early as a defined use of proceeds, get clarity on whether it is retired from cash at close or assumed by the buyer, and make sure your two retiring partners understand whether their payout is fixed cash or partly tied to the same rollover and retention terms as everyone else — because how that obligation is settled changes what the continuing partners actually keep.

Our partner group is split on selling — how do firms actually resolve this?

A split partner group is the norm, not a crisis, and the firms that get through it resolve it with a defined decision process and honest side-by-side economics rather than by letting the loudest partner or the freshest inbound offer decide. The reality: most partnership agreements require a supermajority or near-unanimous vote to sell, which means a deal cannot proceed until the economics are laid out clearly enough that skeptics can see their own after-tax outcome — the reason EisnerAmper's 207 partners could vote unanimously was that the structure and payouts were worked out before the vote, not during it. The split usually tracks age and tenure: partners near retirement weigh a certain cash exit against their unfunded deferred comp, while younger partners weigh rolled equity and a longer runway under a new owner, so a single blended "is this a good deal" question papers over genuinely different situations. What to do: bring in a specialist consultant (Koltin, Whitman Advisory, The Visionary Group, Accountants Advisory Group, or Carl George Advisory — several explicitly do partner-alignment and governance work) to model per-partner outcomes and run a structured decision, and evaluate internal succession and a PE deal on the same page so the vote is about economics, not personalities.

What do M&A advisors charge to sell an accounting firm?

There is no published fee schedule for the CPA-firm consultants, so the honest answer is to describe the fee models rather than quote a rate — and to match the model to which tier of advisor you actually need. The mechanism: the category-defining consultants (Koltin, Whitman, The Visionary Group, Accountants Advisory Group, Carl George) typically work on a negotiated consulting basis — a retainer and/or success component — but none publishes a standard percentage, so any specific number you see attributed to them is inference, not fact. Registered mid-market banks (Capstone Partners, Berkery Noyes, Republic Capital Group) run institutional sell-side mandates and are generally paid a success fee at close, often on a tiered structure, plus a work fee — the same lower-middle-market pattern our fee guide details. Practice brokers (APS, Poe, ProHorizons, Accounting Biz Brokers) work the sub-$2M market on a listing-and-commission model, and even there the rate is not publicly posted. The move: since none of these firms publish a fee schedule, do not accept invented benchmarks — get the fee structure, the minimum fee, the definition of transaction value (does it sweep in rollover and earnout?), and the tail in writing from each advisor — and read our M&A advisor fees guide for the Modified-Lehman and Double-Lehman mechanics and the engagement-letter clauses that quietly inflate the base.

Three buyers already approached us — do we even need an advisor, or can we negotiate directly?

In almost every case yes, you still need an advisor — and three inbound approaches is precisely the situation where one pays for itself, because until those buyers are competing against each other on a clock, you have three separate one-on-one negotiations, which is the structure most likely to give up value you could have kept. Here is the conflict: the two PE platforms and the regional consolidator who approached you negotiate firm sales every month; you will do this exactly once. A specialist advisor turns inbound interest into a real process — quietly adding the other platforms and consolidators active in your category, setting a bid deadline so the parties compete, and negotiating not just price but the structure that actually determines your outcome: the cash/rollover split, how partner comp is normalized, the deferred-comp treatment, and the retention terms. The narrow case for going direct is a single trusted buyer offering a genuine premium plus a fairness check from your own counsel and a quality-of-earnings accountant — but even then, quiet competitive tension usually improves the terms. What to do: engage a specialist consultant or, at institutional scale, a registered bank before you respond substantively to any of the three, and see our M&A advisor vs broker vs investment bank guide for which intermediary type fits your size.

What actually happens to our staff and clients after a PE platform buys the firm?

In the near term, usually less visible change than staff fear — the platform's economic thesis depends on keeping your clients and people — but the honest answer is that incentives and obligations shift, and the retention terms in your own deal are where that plays out. The mechanism: platforms buy accounting firms for their recurring compliance base and their people, so day-one continuity is typically the plan, and payouts beyond closing are commonly tied to client-retention guarantees and performance benchmarks — which means the deal itself gives the buyer (and you) a direct incentive to hold the client base. That is also the pressure point: retention holdbacks and earnouts put real money on keeping clients and key staff through the transition, and your roughly 55% recurring compliance revenue is exactly the asset the structure is built to protect. The move: negotiate the staff and client terms as deliberately as the price — retention packages for key people, what the platform's shared-services "operating system" will and will not change about how your team works, and how client-retention guarantees are measured — and use the confidential pre-close period to control who inside the firm knows and when, because a leak is the thing most likely to spook the clients and staff the deal is trying to keep. That confidentiality is the layer we build at Peony; the deal terms are your advisor's job.

How long does it take to sell an accounting firm from first conversation to close?

For a well-prepared mid-size firm, plan on roughly six to twelve months from the first serious conversation to close, with the biggest swing factors being how clean your normalized financials are and how much competitive tension the process generates. The mechanism: the arc runs through preparation and partner alignment (assembling the normalized-EBITDA bridge, resolving the deferred-comp question, and getting the partner group to a decision), a targeted outreach process behind confidentiality protections, indications of interest and management meetings, then confirmatory due diligence and exclusivity — where a quality-of-earnings review and deep verification of your partner-comp add-backs happen — followed by legal negotiation of the APS split and the equity documents and close. The two things that most often add time are a partner group that is not actually aligned before buyers are engaged, and a normalized-EBITDA picture that does not survive the buyer's quality-of-earnings scrutiny. What to do: the cheapest lever you control on both timeline and price is walking into diligence with your comp normalization already defensible, your deferred-comp plan already decided, and a data room staged before outreach — so build the room and tie out the numbers before you start, not after a buyer asks. See our sell-side due diligence guide and the M&A data room playbook for the buildout.

Sources

- AICPA — succession-cliff and retirement-eligibility data (~75% of CPAs at/near retirement; 65.5% of partners over 50 at $2M-$10M firms; 71.1% at small/sole firms; fewer than half of firms have a succession plan) and the Independence / Form-of-Organization rules underlying the alternative practice structure

- CPA Trendlines — PE Deal Tracker (February 16, 2026 update: ~250 institutional PE transactions since 2019, 203 recorded; ~22 deals 2023, ~65 in 2024, ~86-104 in 2025, ~280 projected 2026) and Allan Koltin commentary (7x-11x on manufactured EBITDA; the partner-comp "scrape"; the day-one / second-bite / recap arc; the IPO prediction for 2026-2027)

- Rosenberg (MAP) Survey, 2025 (on 2024 data) — average income per partner of $615K (an average, not a median), and partner-comp normalization benchmarks

- Financial Times — Citrin Cooperman / Blackstone valuation (~$2B, ~15x EBITDA)

- Journal of Accountancy — KKR / Crowe (announced June 11, 2026); Baker Tilly / Moss Adams; Citrin Cooperman / Blackstone

- Company and sponsor releases — TowerBrook / EisnerAmper (2021) and the March 25, 2026 continuation-vehicle transaction (AlpInvest lead, Hamilton Lane co-lead); New Mountain / Grant Thornton (

60%, proceeds partly to retire retirement obligations); New Mountain / Citrin Cooperman (2022); Parthenon / Cherry Bekaert; Hellman & Friedman + Valeas / Baker Tilly; Charlesbank / Aprio; CBIZ 8-K on the Marcum acquisition ($2.3B, closed November 2024, strategic); Further Global / Armanino (~20% minority); Centerbridge + Bessemer / Carr, Riggs & Ingram (51%); Investcorp + PSP / PKF O'Connor Davies (Capstone Partners sole advisor) - BDO USA — August 2023 ESOP ($1.3B facility, ~$400M for retired-partner pensions; CEO Wayne Berson quote)

- Ascend / Alpine Investors, Springline Advisory / Trinity Hunt Partners, and Crete Professionals Alliance — "stay independent with capital" and roll-up platform models; Modus (April 2026, first VC-led accounting-platform round)

- FINRA BrokerCheck — registration verification (Berkery Noyes Securities, LLC, CRD #155918; Republic Capital Group, CRD #334963; zero registered firms under "Koltin," Whitman, or APS, consistent with the March 29, 2023 federal M&A-broker exemption)

- Firm sources — Koltin Consulting Group, Whitman Advisory LLC, The Visionary Group, Accountants Advisory Group, Carl George Advisory, Capstone Partners (Accounting Services M&A Update), Accounting Practice Sales, Poe Group Advisors (owner-dependent ~3x-6x vs scalable platform ~4x-7.5x EBITDA), ProHorizons, Accounting Biz Brokers

Disclosure: I am the co-founder of Peony, a data room company, so I have a commercial interest in the data-room layer discussed in the Peony section — the advisory firms above are independent and are not Peony partners or clients by virtue of appearing here. Firm facts, deals, and registrations were verified as of July 2026 and can change; confirm current registration on FINRA BrokerCheck or with your state securities regulator before engaging any advisor. Multiples are labeled by source and by type (average vs median vs stated range); deal directions are stated explicitly. Self-reported superlatives are attributed to the firms that make them. Nothing here is investment, legal, tax, or financial advice — retain your own M&A counsel, legal counsel, and a quality-of-earnings accountant before acting.

About the author: Deqian Jia is the co-founder of Peony, the data room platform used by 5,900+ customers across M&A, fundraising, and private-deal workflows. He spends most of his time on the access-control and analytics layer that decides who — and now what — is allowed to read a confidential document. Contact: hello@peony.ink.