18 Best Financial Services & FIG M&A Advisors for $25M-$1B Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

18 Best Financial Services & FIG M&A Advisors for $25M-$1B Deals (2026)

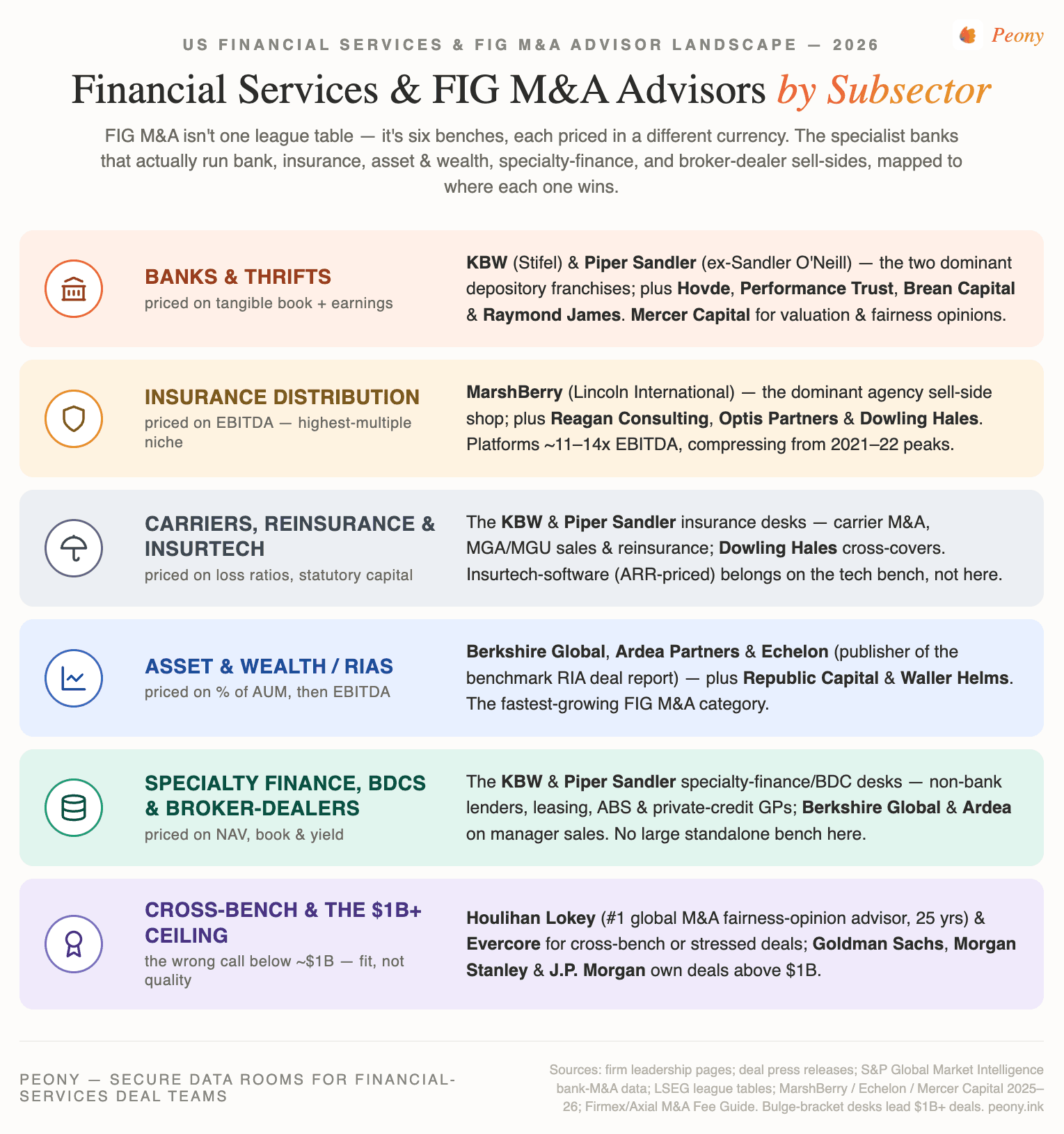

Quick answer: Financial-services (FIG) M&A does not have one "best advisor" — it has six subsector benches, each priced on a different metric. For banks & thrifts (priced on price-to-tangible-book, not EBITDA — acquirers paid a median of about 150% of tangible book as of September 2025, up from 131% in 2024), the dominant names are KBW (a Stifel company), Piper Sandler (the former Sandler O'Neill), Hovde Group, Performance Trust, Brean Capital (which absorbed Janney's FIG team in February 2026), and Raymond James, with Mercer Capital as the valuation and fairness-opinion authority. For insurance distribution — the highest-multiple FIG niche at roughly 11–14x EBITDA for platforms in 2025, compressing from the 2021–22 peaks — MarshBerry, Reagan Consulting, Optis Partners, and Dowling Hales. For asset & wealth / RIAs (priced on a percentage of AUM, then EBITDA), Berkshire Global, Ardea Partners, Echelon Partners, Republic Capital, and Waller Helms. For a cross-bench mandate or a stressed seller, Houlihan Lokey (the #1 global M&A fairness-opinion advisor over 25 years) and Evercore. The bulge brackets — Goldman Sachs, Morgan Stanley, J.P. Morgan — own the $1B-plus value tables but are usually the wrong call below that. For a fintech or payments company priced on ARR and take-rate, see our best technology & software M&A advisors guide (FT Partners); this guide covers regulated financial institutions. Pick by subsector and deal size, not by logo.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I've sat on the document side of hundreds of deals — community-bank sales, insurance-agency roll-ups, RIA and wealth-manager sales, specialty-finance and BDC processes, and the occasional broker-dealer deal — and financial services is the sector where the choice of advisor moves the price more than anywhere else I've watched. Two reasons. First, your value is quoted in a subsector-specific currency: a bank in tangible book, an insurance agency in EBITDA, an RIA in a percentage of AUM. Pick an advisor who flattens all of that to a generic multiple and you get under-credited. Second, a FIG deal lives or dies at a regulatory gate that no generalist sequences for — signing a purchase agreement is the start of the approval clock, not the finish line.

This guide ranks 18 advisors across six benches for sellers in the $25M–$1B band: banks & thrifts, insurance distribution, insurance carriers & insurtech, asset & wealth management / RIAs, specialty finance & BDCs, and broker-dealers. Along the way I lean on five frames I use when I'm helping a founder think about who should run their process: the FIG Subsector Bench Map, the Regulatory-Approval Gate, the Tangible-Book-versus-Earnings Multiple Split, the Net-Flows & Client-Retention Defense, and the Strategic-versus-Sponsor Buyer Split. More than 6,800 customers run their data rooms on Peony, so I see how these processes actually play out on the document side.

Two framing notes before the roster. First, confidentiality is not optional in FIG: your highest-paying buyers are frequently direct competitors, and a leak triggers deposit runoff, producer flight, or client attrition before you've signed anything. Second, an honest word on the bulge brackets — Goldman Sachs, Morgan Stanley, and J.P. Morgan own the value tables above $1B, but below that they're usually the wrong call on fit, not quality. And one scope note: Peony is not an M&A advisor and does not place deals — I build the secure room these processes run in, which is exactly why I care which banker you hire.

If your business is a fintech or payments software company priced on ARR, take-rate, and net revenue retention — where the asset is code, not a balance sheet — that's a different bench; see our best technology & software M&A advisors guide (FT Partners and the SaaS boutiques). This guide covers regulated financial institutions. And if you want the advisors near you rather than the national specialist bench, our city guides carry the local FIG and insurance tiers — Charlotte, Miami, Philadelphia, and New York.

What's the financial-services (FIG) M&A advisor landscape by subsector in 2026?

This table is the map. Find your subsector, then compare within that bench — the lead specialists are listed first, with the cross-bench and bulge-bracket ceiling last.

| Firm | HQ | Deal-size band | Subsector focus | Credential / verified deal |

|---|---|---|---|---|

| Keefe, Bruyette & Woods (KBW) | New York, NY | $50M–$5B+ | Banks & thrifts (+ insurance, broker-dealers) (Stifel-owned) | The definitive FIG franchise since 1962; "KBW, A Stifel Company" since 2013 |

| Piper Sandler | Minneapolis, MN | $50M–$3B | Banks & thrifts + diversified FIG (NYSE: PIPR) | Financial Services Group built on Sandler O'Neill (acquired 2020) |

| Hovde Group | Inverness, IL | $25M–$1B | Banks & thrifts (community-bank specialist) | Independent FIG specialist since 1987 |

| Performance Trust Capital Partners | Chicago, IL | $25M–$750M | Banks & thrifts (community depositories) | Largest full-service bank focused on community depository institutions |

| Brean Capital | New York, NY | $25M–$1B | Banks & thrifts + insurance distribution | Acquired Janney's depository & insurance IB team (completed Feb 2026) |

| Raymond James | St. Petersburg, FL | $50M–$2B | Banks & thrifts + diversified FIG (NYSE: RJF) | Deep depository franchise; Howe Barnes Hoefer & Arnett heritage |

| Mercer Capital | Memphis, TN | Valuation / advisory | Banks & thrifts — valuation & fairness opinions | Leading financial-institution valuation firm; publishes Bank Watch |

| MarshBerry | Woodmere, OH | $25M–$1B | Insurance distribution (Lincoln International-owned) | Top insurance-brokerage sell-side advisor by completed deal count |

| Reagan Consulting | Atlanta, GA | $25M–$500M | Insurance distribution + valuation | Advised 66+ of the top-100 US agents & brokers |

| Optis Partners | Chicago, IL | $25M–$300M | Insurance distribution (lower-mid-market) | Publishes the quarterly agent-broker M&A deal report |

| Dowling Hales | New York, NY | $50M–$1B | Insurance distribution + carriers | Bills itself as the oldest insurance-dedicated bank |

| Berkshire Global Advisors | New York, NY | $50M–$2B | Asset & wealth management / RIAs | Leading dedicated advisor to investment & wealth managers |

| Ardea Partners | New York, NY | $250M–$2B+ | Asset & wealth + cross-border FIG | Elite boutique founded by four former Goldman Sachs partners |

| Echelon Partners | Manhattan Beach, CA | $25M–$1B | Asset & wealth management / RIAs | 500+ engagements; publishes the benchmark RIA M&A Deal Report |

| Republic Capital Group | New York, NY | $25M–$500M | Asset & wealth management / RIAs | RIA-dedicated middle-market M&A advisory |

| Waller Helms (Houlihan Lokey) | Chicago, IL | $25M–$750M | Insurance + asset & wealth (cross-bench) | Acquired by Houlihan Lokey (closed early 2025); absorbed Park Sutton in 2022 |

| Houlihan Lokey | Los Angeles, CA | $50M–$5B+ | Cross-bench FIG + restructuring (NYSE: HLI) | #1 global M&A fairness-opinion advisor over 25 years (LSEG) |

| Evercore | New York, NY | $500M–$5B+ | Elite-boutique FIG ceiling (NYSE: EVR) | Building FIG with senior bulge-bracket hires; record 2025 revenue |

A few notes the table cannot carry. Several firms cross-cover: KBW and Piper Sandler run dedicated insurance-carrier and specialty-finance/BDC desks in addition to banks; Houlihan Lokey and Evercore cover every bench and are the call above ~$1B or when a seller is stressed; and Waller Helms straddles insurance and wealth management. The bulge brackets — Goldman Sachs, Morgan Stanley, and J.P. Morgan — sit above this table for $1B-plus deals and are discussed honestly at the end.

Who are the best community-bank and thrift M&A advisors?

The best community-bank advisors are the pure-play depository franchises — KBW and Piper Sandler at the top, with Hovde, Performance Trust, Brean Capital, and Raymond James rounding out the bench, and Mercer Capital as the valuation authority. Bank M&A is its own world: it runs on price-to-tangible-book and forward earnings, never an EBITDA multiple, and it closes only after the regulators approve.

Keefe, Bruyette & Woods (KBW) (New York, NY) is the reference name in financial-institutions M&A. Founded in 1962 and operating as "KBW, A Stifel Company" since Stifel acquired it in 2013, it covers banks, thrifts, insurance, broker-dealers, specialty finance, and asset managers across research, M&A, and capital markets — the deepest single FIG franchise on the Street. For a community or regional bank running a competitive sale, KBW is the default first call.

Piper Sandler (Minneapolis, MN; NYSE: PIPR) runs one of the two dominant depository franchises through its Financial Services Group, built on the former Sandler O'Neill, which Piper acquired in 2020 and which had long been the leading community-bank M&A advisor. The combined platform remains a top-ranked bank-M&A and bank-capital advisor.

Hovde Group (Inverness, IL) is an independent community-bank specialist that has focused on US bank and thrift M&A and capital markets since 1987 — a strong fit for a closely held community bank that wants a dedicated team rather than a line in a big bank's league table.

Performance Trust Capital Partners (Chicago, IL) describes itself as the largest full-service investment bank focused on community depository institutions, and it pairs M&A with balance-sheet and fixed-income advisory — useful when the sale decision is intertwined with capital and interest-rate positioning.

Brean Capital (New York, NY) is now home to one of the most active community-bank teams in the country: in a deal completed in February 2026, Brean acquired Janney Montgomery Scott's Depository and Insurance Investment Banking, Equity Research, and Institutional Equity Sales businesses — a roughly 50-person group whose roots trace to the old FIG Partners franchise. As of 2026 that depository team sits at Brean Capital, not Janney.

Raymond James (St. Petersburg, FL; NYSE: RJF) runs a deep depository franchise — built in part through its earlier Howe Barnes Hoefer & Arnett acquisition — covering bank stocks from community to multinational, with several hundred FIG transactions completed since 2000.

Mercer Capital (Memphis, TN) belongs on this list as the financial-institution valuation and fairness-opinion authority — not a sell-side auction bank. Founded in 1982 and publisher of the widely cited Bank Watch, it's the firm you bring in for a defensible valuation, a fairness opinion, or transaction advisory, and a key data source on bank-M&A pricing. (Don't confuse it with Mercer Advisors, an RIA aggregator, or Mercer, the Marsh McLennan consulting firm.)

The Regulatory-Approval Gate. Unlike most M&A, a financial-institution sale does not close when the purchase agreement is signed — it closes when the regulator says yes. A specialist sequences the deal around that gate and pre-clears the buyer's standing before you ever sign; a generalist treats signing as the finish line and gets a nasty surprise in month four.

| FIG subsector | Lead regulator(s) | Approval mechanism | Typical window |

|---|---|---|---|

| Banks & thrifts | Federal Reserve + OCC or FDIC + state | Bank Holding Company Act / Bank Merger Act applications | ~3–6 months |

| Insurance carriers | State insurance department(s) | Form A in each state of domicile | ~2–6 months |

| Broker-dealers | FINRA | Continuing-membership application (Rule 1017) | ~3–6 months |

| RIAs | SEC / state securities regulator | Advisers Act change-of-control (assignment) consent | Weeks to months |

For the advisors near you rather than the national bench, our Charlotte and Philadelphia guides carry the regional bank tiers.

Who are the best insurance brokerage and agency M&A advisors?

For an insurance agency or brokerage, the sell-side specialists are MarshBerry, Reagan Consulting, Optis Partners, and Dowling Hales. Insurance distribution is the highest-multiple FIG niche — the largest, cleanest platform agencies traded around 11–14x EBITDA in 2025, while public brokers now trade near 12–13x EBITDA, the lowest in a decade — so price your business on current comps, not 2021 nostalgia. This section is the map; for the full ranked bench — including the New York boutique tier, the EBITDAC teaser math consolidators quote, and the carrier-consent mechanics that decide whether an agency deal closes — see our dedicated best insurance M&A advisors guide.

MarshBerry (Woodmere, OH) is the dominant insurance-brokerage sell-side advisor, consistently ranked at or near the top by completed deal count, and it pairs M&A with consulting and valuation across the agency sector. MarshBerry took a growth investment from Atlas Merchant Capital in January 2022, and in a deal completed October 31, 2025, Lincoln International acquired the firm — so as of 2026 MarshBerry operates as part of Lincoln International rather than as a standalone partner-owned advisory. For an agency owner selling into the consolidator wave, it's still the deepest sell-side bench.

Reagan Consulting (Atlanta, GA) has advised more than 66 of the top-100 US agents and brokers, combining M&A advisory with valuation, capital raising, and perpetuation planning — a strong fit for a high-quality agency weighing a sale against an internal perpetuation.

Optis Partners (Chicago, IL) focuses on the lower-middle-market agent-and-broker segment and publishes a widely followed quarterly agent-broker M&A deal report — useful market intelligence and a sign of how deep they sit in the niche.

Dowling Hales (New York, NY) bills itself as the oldest investment bank dedicated to insurance, working across both distribution and carriers. (Confirm current ownership and any affiliation before relying on specific historical deal figures.)

A cross-coverage note: KBW and Piper Sandler both run dedicated insurance-carrier and reinsurance desks, covered in the next section. For the regional agency-rollup buyer pool, our Charlotte insurance tier is a useful geo cut.

Who advises on insurance carriers, reinsurance, and insurtech M&A?

Insurance carriers — underwriting companies, MGAs and MGUs, life, annuity, and P&C insurers, and reinsurers — are a different bench from agency distribution, priced on loss ratios, combined ratios, and statutory capital rather than agency EBITDA. The deepest coverage here runs through the KBW and Piper Sandler insurance desks, which handle carrier M&A, MGA/MGU sales, and reinsurance transactions, with Dowling Hales cross-covering carriers as well.

This is also where I'll draw the FIG-versus-fintech line clearly. An insurtech belongs on this bench only when the asset is a regulated, balance-sheet business — a carrier or MGA underwriting risk. If your insurtech is a software platform priced on recurring revenue, take-rate, and net revenue retention, that's the tech bench, and the advisor set is different: see our best technology & software M&A advisors guide. The carriers and MGAs here are valued on statutory capital and loss ratios, not ARR — get on the right bench before you pick a banker.

Who are the best asset & wealth management and RIA M&A advisors?

RIA and wealth-management M&A is the fastest-growing FIG category, and it has a dedicated bench: Berkshire Global Advisors, Ardea Partners, Echelon Partners, Republic Capital Group, and Waller Helms Advisors (since early 2025 part of Houlihan Lokey). These firms are screened on a percentage of AUM and closed on EBITDA — a different currency again from banks and agencies.

Berkshire Global Advisors (New York, NY) is the leading dedicated M&A advisor to investment and wealth managers, with more than 40 years advising the sector and particular depth in alternative and traditional asset-management transactions.

Ardea Partners (New York, NY) is an elite cross-border FIG boutique founded in 2016 by four former Goldman Sachs partners, with a strong asset-management focus. It runs a senior, relationship-driven model; treat it as a top-tier team for a larger or cross-border mandate rather than a high-volume shop.

Echelon Partners (Manhattan Beach, CA) is wealth-management-dedicated, with several hundred completed engagements and the industry's benchmark annual RIA M&A Deal Report — the source most of the sector quotes for deal counts. For an RIA founder, Echelon's deal flow and market data are hard to match.

Republic Capital Group (New York, NY) is an RIA-focused middle-market advisory firm — a credible specialist for a wealth-management seller; confirm a recent comparable with them directly.

Waller Helms Advisors (Chicago, IL) built its franchise spanning insurance, wealth, and financial technology, and absorbed the RIA-M&A boutique Park Sutton Advisors in 2022. Note the 2024–25 update: Houlihan Lokey acquired Waller Helms (agreed August 2024, closed by early 2025), so the Waller Helms and Park Sutton benches now operate inside Houlihan Lokey's Financial Services Group rather than as an independent boutique — a seller who remembers either name should route the conversation there.

The Net-Flows & Client-Retention Defense. In FIG the asset can walk out the door during the sale — an RIA loses AUM to attrition, a wealth firm loses clients who followed one advisor, a bank loses deposits, an agency loses producers. The defensible value is sticky, contractually protected, multi-relationship business. Document persistency — net-flow trends, client-tenure cohorts, advisor and producer non-competes, book ownership — before the buyer prices in the worst case.

| Buyer type | What they pay for | Price posture | What they want from you | Best when… |

|---|---|---|---|---|

| Strategic (acquiring bank, national broker, aggregator) | Synergy, scale, taking a competitor off the board | Highest headline price | Your deposits / book / AUM and advisors; integration | You want maximum value and a clean exit |

| New PE platform | A scarce, well-run platform to build around | Disciplined, cash-flow- or AUM-anchored | You and your team to lead and roll equity | You want a second bite and to keep running it |

| PE add-on / aggregator add-on | Tuck-in scale into an existing platform | Programmatic, multiple-driven | Smooth integration; key producers/advisors to stay | You're sub-scale and want speed and certainty |

A staged, walled data room is how you make a strategic and a sponsor compete without either seeing your crown-jewel client data early — roll equity is usually the sponsor's ask, and the M&A data room is where the dual track runs. For the local wealth-management buyer pool, see our Miami and New York guides.

Who advises on specialty finance, BDCs, and broker-dealer M&A?

This sixth bench is the most cross-covered. Specialty finance and BDCs — non-bank lenders, leasing platforms, ABS originators, BDCs, and direct-lending managers — are priced on NAV, book value, and yield, and the specialist set is the KBW and Piper Sandler specialty-finance/BDC desks, with Berkshire Global Advisors and Ardea Partners strong on private-credit-manager and GP sales. Broker-dealers and diversified-FIG businesses are likewise covered by the KBW and Piper Sandler franchises (a broker-dealer sale also runs through the FINRA approval gate above). If you're selling a specialty lender or a credit manager, the right team is one of the FIG desks paired with an asset-management boutique — there's no large standalone bench here, which is itself worth knowing.

How much is your financial-services company worth? The 2026 FIG multiple ladder

There is no single FIG multiple — there's a ladder per subsector, because each is priced in its own currency. This is the Tangible-Book-versus-Earnings Multiple Split, and getting it right is the difference between a defensible number and a generalist's guess:

- Banks & thrifts — price-to-tangible-book plus forward earnings, never EBITDA. Acquirers paid a median of about 150% of tangible book as of September 2025 (up from 131% in 2024 and 124% in 2023). Community banks in the $2–10B asset range traded around 1.3x tangible book and ~11x forward earnings, with average takeover premiums near 30%. 2025 saw roughly 176 announced bank deals, a second consecutive annual rise.

- Insurance distribution — EBITDA / EBITDAC. Platform agencies 11–14x, tuck-ins 7.5–12x, small agencies 5–8x, public brokers 16–18x EV/EBITDA, with the whole band compressing from the 2021–22 peaks through 2025.

- Asset & wealth / RIAs — a percentage of AUM as a first screen (roughly 0.5–1.5% for traditional books, higher for alternatives), then EBITDA: ~10–15x for $500M–$3B AUM platforms, into the high-teens to low-20s for the largest, with blended deals landing near 10x EBITDA in 2025.

- Specialty finance / BDCs — NAV, book value, and yield.

The second value lever is the Net-Flows & Client-Retention Defense: a buyer discounts headline AUM or deposits for expected runoff unless you prove persistency. Package both — a tangible-book bridge or AUM-persistency story plus a clean sell-side diligence file — and you defend the top of your range.

What do financial-services M&A advisors charge in 2026?

FIG advisors charge a success fee on close, usually on a declining-rate Lehman scale, plus a retainer. The declining-rate Lehman is not obsolete — it's the single most common structure, used in about 44% of engagements — and Double Lehman (10/8/6/4/2% on successive $1M tranches) is the lower-middle-market standard. On a $20M deal that's roughly $600K (about 3.0%); the blended effective success-fee curve runs near 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (from a sample of 456 engagements).

Three terms move the bill more than the headline rate:

- The retainer. Expect $5–15K/month, credited against the success fee in about 72% of letters — so it's mostly a timing question, not extra cost. Smaller deals carry a minimum-fee floor of $50–250K.

- The fee base. Equity value versus enterprise value (including assumed debt) can swing the number materially; for a bank, confirm whether the fee runs on aggregate consideration or equity value.

- The tail. A list of named buyers stays covered for a period after the engagement ends — keep it tight and specific.

The cheapest lever you have is competition: only about 17% of sellers run a banker bake-off, and it routinely pays for itself. Our M&A advisor fees guide has the full math, and advisor versus broker versus investment bank covers which intermediary tier fits your size.

What are the proprietary frames in this guide — and how do I use them?

Five frames, each turning a public fact into a decision:

- FIG Subsector Bench Map — there is no single "best FIG advisor"; match the firm to your subsector (banks, insurance, asset & wealth, specialty finance, broker-dealer) first, then compare within that bench.

- Regulatory-Approval Gate — signing isn't closing; pick an advisor who sequences the Fed/OCC/FDIC, state-insurance Form A, FINRA, or Advisers Act approval and pre-clears your buyer's standing.

- Tangible-Book-versus-Earnings Multiple Split — get priced in your subsector's native currency (tangible book for banks, EBITDA for agencies, % of AUM for RIAs, NAV/yield for specialty finance), not a flattened EBITDA multiple.

- Net-Flows & Client-Retention Defense — document deposit, AUM, or producer persistency before the buyer prices in worst-case runoff.

- Strategic-versus-Sponsor Buyer Split — run a dual track so a strategic (paying for synergy) and a sponsor (paying a disciplined price and wanting you to roll equity and stay) compete.

What's the honest take on the bulge brackets and elite boutiques for FIG?

The bulge brackets and elite boutiques own the value tables above $1B — and below that they're usually the wrong call on fit, not quality.

Houlihan Lokey (Los Angeles, CA; NYSE: HLI) is the #1 global M&A fairness-opinion advisor over the past 25 years (by transaction count, per LSEG) and runs the Street's leading restructuring bench — so it's the call when a FIG seller is stressed, needs a defensible opinion, or sits in a complex cross-bench situation. Evercore (New York, NY; NYSE: EVR) is the elite-boutique FIG option, actively building the practice with senior bulge-bracket hires and coming off record firm revenue in 2025; reach for it on a larger, advisory-led mandate. PJT Partners appears on FIG advisory and restructuring league tables alongside the other elites.

Above roughly $1B — public-company mechanics, carrier carve-outs, mega-cap bank deals — the bulge brackets Goldman Sachs, Morgan Stanley, and J.P. Morgan have the deepest large-cap FIG coverage and are the right default. Below that line, they tend to staff a mid-market FIG seller thin, and you're not the priority account. That's the ceiling, not the recommendation.

How does this compare to other sectors — and where does Peony fit?

The through-line across every sector cut is the same: hire the advisor who speaks your value language. In energy it's reserves and PDP; in healthcare it's reimbursement and regulatory posture; in industrials it's normalized through-cycle earnings; in tech and software it's ARR and net revenue retention; and in FIG it's tangible book, EBITDA, and AUM persistency, subsector by subsector.

Peony is where the document side of these deals runs. It's not an M&A advisor and doesn't place deals — it's the data room your banker's process lives in, and it's SOC 2 Type II certified and used by more than 6,800 customers. For a FIG sale, the security model matters more than usual, because your crown jewels are exactly what a competitor-bidder would love to walk away with: customer deposit and loan tapes, producer and book-of-business schedules, AUM and client rosters. Peony's visitor groups wall each bidder into their own view, dynamic watermarks and screenshot protection trace any leak to one party, redaction masks names until you choose to reveal them, and page-level analytics show which bidder is seriously engaged. For private equity buyers and sell-side teams alike, that's the difference between a controlled process and a leak. See how analytics spot the serious buyers.

The bottom line

Financial-services M&A isn't one league table — it's six benches. For a bank or thrift, hire KBW, Piper Sandler, Hovde, Performance Trust, Brean Capital, or Raymond James, with Mercer Capital for the valuation. For an insurance agency, MarshBerry, Reagan Consulting, Optis, or Dowling Hales. For an RIA or wealth manager, Berkshire Global, Ardea, Echelon, Republic Capital, or Waller Helms. For a cross-bench or stressed situation, Houlihan Lokey or Evercore; above $1B, the bulge brackets. Whatever your subsector, run a dual-track process so a strategic and a sponsor compete, sequence the regulatory gate from day one, and walk in with the cheapest lever already pulled: a tangible-book bridge or AUM-persistency story, priced in your own currency, sitting in a staged, walled data room. That preparation, more than the logo on the engagement letter, is what defends the top of your range.

Related resources

- The MGA Data Room: Selling Underwriting Authority — staged disclosure for the two audiences who can kill an MGA sale: carriers holding change-of-control consent and producers holding the relationships

- Best energy M&A advisors, best healthcare M&A advisors, best industrial M&A advisors, best technology & software M&A advisors, and best software M&A advisors — the sibling national sector cuts, the last one the software/SaaS-only carve where the fintech-software specialist tier lives.

- Best insurance M&A advisors — the insurance-distribution deep dive off this guide's insurance bench: the full 15-firm map, the New York boutique tier, and the teaser-decode math for agency sellers.

- M&A advisor fees and advisor vs. broker vs. investment bank — what advisors charge and which intermediary tier fits your size.

- Investment banking data room and M&A data room — running the sell-side process.

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, the right-sized room for a smaller community-bank, agency, or RIA transaction.

- How to write a CIM, sell-side due diligence, and the M&A due diligence process guide — preparing the materials.

- Data room Q&A and how analytics spot serious buyers — running confidential, competitor-bidder diligence.

- City geo-cuts: Charlotte, Miami, Philadelphia, and New York.

Frequently asked questions

As a community-bank owner exploring a sale, who are the best M&A advisors for selling a community bank in 2026?

For a community bank, the specialist bench is Keefe, Bruyette & Woods (KBW, a Stifel company), Piper Sandler (which absorbed Sandler O'Neill's depository franchise), Hovde Group, Performance Trust, Brean Capital (which acquired Janney's depository investment-banking team in February 2026), and Raymond James — with Mercer Capital as the valuation and fairness-opinion authority rather than an auction banker. The reason to use a financial-institutions specialist is that a bank is not priced or sold like a normal company: value runs on price-to-tangible-book and forward earnings, not an EBITDA multiple, and the deal closes only when the Federal Reserve, OCC, and/or FDIC approve the change of control. This is the FIG Subsector Bench Map in action — the firm that dominates bank M&A is usually irrelevant to an insurance or RIA sale. Vet any advisor by asking for five buyers they would call, the bank deals they have closed in the last 18 months, and whether they would run a strategic-versus-sponsor dual track. I run Peony, a data room company used by more than 6,800 customers, so I see the document side of these processes — but pick your banker first.

Selling my family-owned insurance brokerage, who are the best investment banks and advisors for an insurance-agency sale?

For an insurance agency or brokerage, the sell-side specialists are MarshBerry, Reagan Consulting, Optis Partners, and Dowling Hales — firms that live inside agency economics and the consolidator buyer pool. Insurance distribution is the highest-multiple FIG niche: it is priced on EBITDA (or EBITDAC), with platform agencies trading around 11–14x in 2025 and smaller agencies 5–12x, though multiples compressed over the year from their 2021–22 peaks. That is the Tangible-Book-versus-Earnings Multiple Split — your agency is an EBITDA business, unlike a bank seller down the hall priced on tangible book. The buyer universe is dominated by a handful of PE-backed brokerage consolidators plus a few strategics, so a specialist who runs them against each other is how you capture the multiple rather than taking the first call. If your business is actually an insurtech software platform priced on recurring revenue, that is a different bench — see our tech and software M&A advisors guide. For everyone else, a dedicated insurance advisor is worth the fee. Peony is used by more than 6,800 customers to run these confidential processes.

Deciding who sells my RIA, which advisors specialize in wealth-management and RIA M&A versus bank or insurance deals?

RIA and wealth-management M&A has its own dedicated bench — Berkshire Global Advisors, Ardea Partners, Echelon Partners, Republic Capital Group, and Waller Helms Advisors — and it is genuinely separate from the bank and insurance benches. This is the FIG Subsector Bench Map: the firm that leads community-bank M&A does not sell RIAs, and Echelon, which publishes the industry's benchmark RIA deal report, does not sell banks. RIAs are screened on a percentage of AUM and then closed on EBITDA, with platform firms in the $500M–$3B AUM range trading roughly 10–15x EBITDA in 2025 and the largest books reaching the high-teens to low-20s. The buyer pool is mostly RIA aggregators and PE-backed platforms who want your advisors and clients to stay, so retention terms matter as much as headline price. Vet an advisor by their RIA deal count, not their general M&A volume. Peony is SOC 2 Type II certified and used by more than 6,800 customers, so the client rosters and AUM detail stay walled until late diligence.

Weighing my options for a $200M bank sale, do I need a FIG-specialist investment bank or can a generalist M&A advisor handle it?

For a $200M bank, use a financial-institutions specialist — this is the one sector where a generalist most reliably leaves money on the table or stalls the deal. Two reasons. First, the Tangible-Book-versus-Earnings Multiple Split: a bank is priced on price-to-tangible-book and forward earnings, not an EBITDA multiple, and a generalist who reaches for EBITDA simply mis-prices you. Second, the Regulatory-Approval Gate: a bank sale does not close at signing — it closes when the Federal Reserve, OCC, and/or FDIC approve the change of control, a 3–6 month window a specialist sequences and a generalist treats as an afterthought. The specialist set at this size is KBW, Piper Sandler, Hovde, Performance Trust, Brean Capital, and Raymond James. The honest exception: if you already have one obvious strategic acquirer and just need execution and a fairness opinion, a leaner mandate (or a valuation firm like Mercer Capital) can work. For a competitive process, a FIG banker earns the fee. See our guide on advisor versus broker versus investment bank.

Comparing advisors for my community-bank sale, how do KBW, Piper Sandler, and Stephens compare for bank and thrift M&A?

KBW and Piper Sandler are the two dominant pure-play depository franchises. KBW — Keefe, Bruyette & Woods, a Stifel company since 2013 — has been the reference name in bank, thrift, and broader FIG M&A since 1962, with research, M&A, and capital-markets depth across the sector. Piper Sandler's Financial Services Group was built on the former Sandler O'Neill (acquired in 2020), historically the leading community-bank M&A advisor, and remains a top-ranked depository franchise. Stephens, the family-owned Little Rock investment bank, covers financial institutions as part of a diversified franchise rather than as a pure-play depository shop, so it is a credible option — especially for a relationship-driven seller — but for a competitive bank auction the pure-play bench (add Hovde, Performance Trust, Brean Capital, and Raymond James) is where the deepest buyer relationships sit. The real test is which managing director actually runs your deal and the bank transactions they closed in the last 18 months. Compare on deal team and recent comparables, not logo.

As a mid-size bank owner, should I use a FIG boutique or a bulge-bracket bank, and will a regional advisor still reach national buyers?

Below roughly $1B, a FIG boutique or specialist is almost always the better call, and yes — a credible specialist reaches the national buyer set regardless of where it sits. The buyer universe for a community or mid-size bank is a defined, knowable list: acquiring banks building scale in your region, a few out-of-market strategics, and PE-backed bank-holding platforms. A specialist like KBW, Piper Sandler, or Hovde already covers every one of them. A bulge-bracket bank (Goldman Sachs, Morgan Stanley, J.P. Morgan) has the deepest large-cap FIG coverage, but below ~$1B it tends to staff you thin and you are not the priority account — that is fit, not quality. This is also where the Strategic-versus-Sponsor Buyer Split matters: a specialist runs an acquiring bank (paying for deposits and scale) against a PE platform (paying a disciplined price and wanting management to stay) so they compete. Reserve the bulge brackets for genuine $1B-plus, public-company-mechanics deals. See our advisor-versus-broker-versus-investment-bank guide for the size thresholds.

Preparing to sell my community bank, how long does the process take and what Fed, OCC, and FDIC regulatory approvals are required?

Plan on roughly 6–12 months or more, because in banking signing is not closing — the Regulatory-Approval Gate is. After you sign a definitive agreement, the buyer (and sometimes you) must obtain change-of-control approval: a bank holding company acquisition runs through the Federal Reserve under the Bank Holding Company Act; a bank-level merger runs through the OCC (for national banks) or the FDIC (for state non-member banks) under the Bank Merger Act; and your state banking department weighs in. That approval window commonly runs 3–6 months on top of diligence and signing, and a clean buyer with strong capital and CRA standing moves faster than a troubled one. A FIG specialist pre-clears the buyer's regulatory standing before you pick them, so you are not six months into a process with a buyer who cannot get approved. Build the data room for a long, staged process from day one — our M&A due diligence process guide and CIM guide walk through the sequence.

Since my likely buyers are competitors, how do I run a confidential bank or insurance sale and what belongs in the data room?

In FIG your highest-paying buyers are usually direct competitors, so confidentiality is not a nicety — a leak triggers deposit runoff, producer flight, or client attrition before you even sign. Run staged disclosure: a no-name teaser first, then an NDA-gated CIM, then walled tranches of detail released only as a bidder advances, with the most sensitive material (customer-level deposit and loan tapes for a bank, producer and book-of-business schedules for an agency, client and AUM rosters for an RIA) masked until late confirmatory diligence under a clean-team arrangement. This is the confidentiality side of the Strategic-versus-Sponsor Buyer Split: competing strategics must never see each other's questions or your crown-jewel data early. A modern data room is built for exactly this — Peony is SOC 2 Type II certified and used by more than 6,800 customers, with visitor groups for per-bidder walls, dynamic watermarks and screenshot protection to trace leaks, and redaction to mask names until you choose to reveal them. See our M&A data room and data room Q&A guides.

Worried about losing my book of business, how do I prevent deposit runoff, AUM attrition, or producer flight while I'm selling?

This is the Net-Flows and Client-Retention Defense, and it is the FIG seller's single biggest value lever. In financial services the asset can walk out the door during the sale: a bank bleeds deposits, an RIA shows negative net flows, an agency loses producers and their books, a wealth firm loses clients who followed one advisor. Buyers price in worst-case runoff unless you prove the business is sticky — so document persistency before they ask. For a bank, show deposit beta and the core-versus-brokered mix; for an RIA, show net-flow trends and client-tenure cohorts; for an agency, show producer non-competes and who actually owns the book. Keep your team focused and your numbers clean through the process, and stage the disclosure so departures are not triggered by a premature leak. The defensible value is contractually protected, multi-relationship business — not headline AUM or deposits. Our sell-side due diligence guide covers how to package this, and Peony's page-level analytics show which bidder is seriously engaged.

Setting price expectations for my bank, is it valued on tangible book value or an EBITDA multiple, and how is an insurance agency or RIA valued differently?

A bank is valued on price-to-tangible-book plus forward earnings — never an EBITDA multiple. Applying a generic EBITDA multiple to a bank is a category error, because banks do not report EBITDA in a comparable way; their currency is tangible common equity and earnings. As of September 2025, acquirers paid a median of roughly 150% of tangible book for banks, up from 131% in 2024, and community banks in the $2–10B asset range traded around 1.3x tangible book and about 11x forward earnings, with average takeover premiums near 30%. That is the Tangible-Book-versus-Earnings Multiple Split: each FIG subsector is priced in a different currency. An insurance agency is an EBITDA business (platforms ~11–14x in 2025, compressing from 2021–22 peaks). An RIA is screened on a percentage of AUM and closed on EBITDA (roughly 10–15x for $500M–$3B AUM books). Specialty finance trades on NAV and yield. A specialist prices you in your subsector's native currency and defends it. See our M&A advisor fees guide for how that value drives the fee.

Budgeting the cost of selling my financial-services company, what success fee do FIG advisors charge and is the Double Lehman formula still standard in 2026?

Yes — the declining-rate Lehman structure is alive and is the single most common fee format, used in about 44% of engagements per the 2024–25 fee data, and Double Lehman (10/8/6/4/2% on successive $1M tranches) remains the lower-middle-market standard. On a $20M deal Double Lehman works out to roughly $600K, about 3.0%; the blended effective success-fee curve runs near 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (from a sample of 456 engagements). Expect a monthly retainer of roughly $5–15K (credited against the success fee in about 72% of letters), a minimum-fee floor of $50–250K on smaller deals, and a tail covering named buyers for a period after the engagement ends. Only about 17% of sellers run a competitive banker bake-off, which is the cheapest lever you have on the fee. For banks priced on tangible book, confirm whether the fee base is aggregate consideration or equity value. Our M&A advisor fees guide has the full math.

Benchmarking my 2026 valuation, what price-to-tangible-book multiple are banks selling for, and what EBITDA or AUM multiples apply to insurance agencies and RIAs?

Three different yardsticks, one per subsector. Banks: acquirers paid a median of roughly 150% of tangible book as of September 2025 (up from 131% in 2024), with community banks in the $2–10B asset range around 1.3x tangible book and ~11x forward earnings and average premiums near 30% — 2025 saw about 176 announced bank deals, a second straight annual rise. Insurance agencies: EBITDA-based, with platforms ~11–14x and tuck-ins 7.5–12x in 2025, compressing from the 2021–22 peaks (public brokers now trade near 12-13x EBITDA, the lowest in a decade). RIAs: screened on a percentage of AUM (roughly 0.5–1.5% for traditional books, higher for alternatives) and closed on EBITDA, around 10–15x for $500M–$3B AUM platforms and into the high-teens to low-20s for the largest. This is the Tangible-Book-versus-Earnings Multiple Split — get priced in your own currency. See our sell-side due diligence and advisor fees guides to turn these into a defensible number.

You might also like

Jul 19, 2026

15 Best Insurance M&A Advisors for Agency & Brokerage Sales (2026)

Jun 15, 2026

22 Best Industrial & Manufacturing M&A Advisors for $25M-$1B Deals (2026)

Jun 7, 2026

13 Best Technology & Software M&A Advisors for $25M-$1B Deals (2026)