15 Best Insurance M&A Advisors for Agency & Brokerage Sales (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

15 Best Insurance M&A Advisors for Agency & Brokerage Sales (2026)

Quick answer: For selling an independent P&C agency or brokerage, the national sell-side specialists to know first are Sica | Fletcher (New York — #1 by combined closed deal count on S&P Global since 2017) and MarshBerry (Woodmere, OH — #1 sell-side advisor 2008-2025 per S&P Global, now part of Lincoln International): the two hold different number-one titles on different metrics, and both are true. Round out the national bench with Reagan Consulting (perpetuation and valuation), OPTIS Partners (lower-middle-market, publisher of the quarterly deal report), and Dowling Hales (distribution and carriers). In New York and the tri-state, the boutiques are Insurance Advisory Partners, Mystic Capital, Merger & Acquisition Services (the MGA/program specialist), Philo Smith (Stamford), and Sherman & Company. For a carrier, MGA, or reinsurance deal — a different animal — KBW, Piper Sandler, and Houlihan Lokey (now home to the former Waller Helms) take over. At the small end, Agency Brokerage Consultants and Springtree Group serve the sub-scale tier honestly. The one thing every teaser hides: the consolidator who called you is not your advisor. Pick your banker first.

This is the insurance-distribution deep dive. For banks, RIAs, specialty finance, and the full FIG map, see our financial-services M&A advisors guide — that hub keeps the cross-subsector bench (KBW and Piper Sandler for banks, Berkshire Global and Echelon for RIAs, and the rest). This guide goes deep on insurance distribution: the agency and brokerage sell-side specialists a $1M-$10M-EBITDA owner actually shortlists, the consolidator buyer pool and how it computes a teaser, the EBITDA-versus-EBITDAC decode, and the New York agency-versus-carrier approval distinction no generic listicle explains. No firm here is ranked against banks or RIAs; it is ranked against your agency and your deal.

Last updated: July 2026

TL;DR: Insurance-distribution M&A splits by deal size and by what you are selling — an agency is not a carrier. The specialist map above is the whole game. What the map cannot show is the traps: MarshBerry is not Marsh, the two "#1" firms measure different metrics (combined closed count vs sell-side completed count), Waller Helms is now Houlihan Lokey, the consolidator's in-house caller represents the buyer, and a teaser "10x" all-in on pro-forma EBITDA is not the guaranteed cash-at-close multiple on your trailing actual EBITDA. Only two boutiques on this page carry a printed CRD, and that is deliberate.

Why I wrote this — and how it differs from our financial-services hub

I'm Sean Yu, co-founder of Peony, a data room company used by more than 5,900 customers. I've sat on the document side of a lot of insurance-distribution deals — family-owned P&C agency sales, benefits-agency roll-ups, MGA and program-business transactions, and the occasional carrier process — and insurance distribution is a corner of financial services where the choice of advisor moves the price more than almost anywhere I've watched, because so much of the "price" is contingent by design and buried in how EBITDA is defined.

We already publish a broad financial-services & FIG M&A advisors hub that maps six subsector benches — banks and thrifts, insurance distribution, insurance carriers and insurtech, asset and wealth management and RIAs, specialty finance and BDCs, and broker-dealers. This page is the insurance-distribution cut of that hub. For banks, RIAs, and the full FIG map, see the financial-services guide; this guide goes deep on insurance distribution. It does not re-run the cross-subsector map — instead it goes deeper on the agency and brokerage sell-side bench, the consolidator buyer pool that is calling you weekly, the teaser-versus-real multiple decode, and the mechanics of actually getting a New York agency sold. If you own a bank, an RIA, or a specialty lender, the hub is your starting point, not this page.

One framing note before the roster, and it is the spine of this whole guide: the consolidator who called you is not your advisor. The insurance-distribution buyer pool has consolidated hard — OPTIS Partners counts about 95 unique buyers in 2025, down from 104 in 2024, falling every year since 2021 — and roughly 72-73% of deals are done with private-equity money behind them. Those buyers call agency owners weekly, and they lead with an all-in teaser multiple computed on pro-forma adjusted EBITDA, while the guaranteed cash-at-close multiple on your trailing actual EBITDA is materially lower. The dedicated sell-side bench exists precisely to close that gap — Sica | Fletcher's own data puts advised deals about 25% higher on average (their stat). And to be clear about scope: Peony is not an M&A advisor and does not place deals — the firms below do that. I build the secure room the process runs in, which is exactly why I care which banker you hire.

What's the 2026 insurance M&A market — deal counts, buyers, and the mega-deal wave?

The 2026 market has two headline facts an agency owner needs to hold at once: deal count at the agency level is at a decade low, while the dollar value of the sector is concentrated at the very top in a handful of mega-deals. Reading only one of those tells you the wrong story.

Start with the count, and mind the source — because two respected datasets point in opposite directions and count different universes. OPTIS Partners (US and Canada agent-and-broker M&A, the quarterly benchmark) counted 695 deals in 2025, down about 12% year over year, with Q4 2025 the lowest quarter since 2019 — "the story of 2025 is more like 2019 than any year since," in the words of OPTIS's Steve Germundson. MarshBerry, tracking a broader distribution universe with different counting rules, counted 854 announced US brokerage transactions in 2025, up about 1% and its third-highest on record. Those are not contradictory — they measure different things — but you must attribute each by name and never blend them into a single "market" number. The direction that matters for a seller is OPTIS's: fewer deals, done by fewer buyers.

That buyer concentration is the second fact. The 2025 acquirer table (OPTIS Partners) reads:

| 2025 rank | Acquirer | 2025 deals | 2024 deals | Note |

|---|---|---|---|---|

| 1 | BroadStreet Partners | ~69 (OPTIS-reported)¹ | 90 | Led the table; down year over year |

| 2 | Hub International | 49 | 61 | PE-backed platform |

| 3 | Inszone | 45 | 48 | PE-backed platform |

| 4 | Leavitt Group | 29 | — | Only privately held broker in the top 10 |

¹ BroadStreet's 2025 figure is OPTIS-reported and carries slight source variance (one read put it materially lower); the majority of sources and the year-over-year comparison support roughly 69, down from 90.

Behind the leaders, World Insurance Associates and Keystone Agency Partners grew year over year, and ten firms did 20 or more deals in 2025 — but the pool is shrinking: about 95 unique buyers in 2025 versus 104 in 2024, down every year since 2021, and 72-73% of all deals went to PE-backed or hybrid buyers (OPTIS). MarshBerry's cut is consistent in thrust: private-capital-backed buyers were about 70.8% (605 of 854) of its universe. Privately held brokers were down about 9% year over year; public brokers down about 27%. The consolidator watch-list an owner will actually hear from: BroadStreet, Hub, Inszone, World, Alkeme, Trucordia (rebranded from PCF Insurance Services on October 24, 2024 — not 2025), Keystone, Leavitt, Higginbotham, and Patriot Growth, plus the platforms now inside strategics (Risk Strategies/One80 under Brown & Brown; AssuredPartners under Gallagher).

Now the mega-deal wave — the transactions that made the sector's dollar value soar even as agency-level count fell. Keep the dates, values, and status exact:

| Deal | Value | Status | Note |

|---|---|---|---|

| Aon acquires NFP | ~$13.4B announced² | Closed Apr 25, 2024 | ~$7.0B cash + ~$6.0B / 19M shares (SEC filings ~$13.0B EV) |

| Marsh McLennan acquires McGriff | $7.75B cash | Closed Nov 15, 2024 | Folded into Marsh McLennan Agency |

| Arthur J. Gallagher acquires AssuredPartners | $13.45B cash | Closed mid-Aug 2025 | Largest sale of a US broker to a strategic in history |

| Brown & Brown acquires Accession Risk Mgmt | $9.825B gross | Closed Aug 1, 2025 | RSC Topco (Risk Strategies + One80); ~$8.55B cash + ~$1.045B stock |

² "$13.4B" is announced consideration; SEC filings imply roughly $13.0B enterprise value and about $9.1B on a GAAP preliminary basis — cite it as announced, not as a precise EV.

The reason all four are worth naming is scale-setting, not comparability: these are strategic-to-strategic transactions that frame the ceiling, while your agency sale runs in a completely different band. The Gallagher/AssuredPartners deal is also the cleanest public illustration of the EBITDAC point below — it was quoted at 11.3x EBITDAC net of synergies versus 14.3x gross.

Finally, the turn that matters most for 2026 pricing: the commercial P&C market went soft in Q1 2026. Average premiums declined about 1.2% across account sizes — the first broad decline in roughly nine years and the end of a 33-quarter streak of increases — with some property lines seeing double-digit rate decreases on the back of a quiet 2025 hurricane season and record reinsurance capital. Softening matters to agency multiples because it removes the rate-driven revenue tailwind that lifted agency growth for years. When premiums stop rising on their own, organic growth carries the multiple: agencies with 90%+ retention and genuine high-single- or double-digit organic growth still command a premium, while agencies whose growth was mostly rate get compressed. That same pressure has pushed public-broker valuations to a decade low (around 12-13x EBITDA), and that flows down into private-platform pricing.

Who are the best insurance M&A advisors for an agency or brokerage sale?

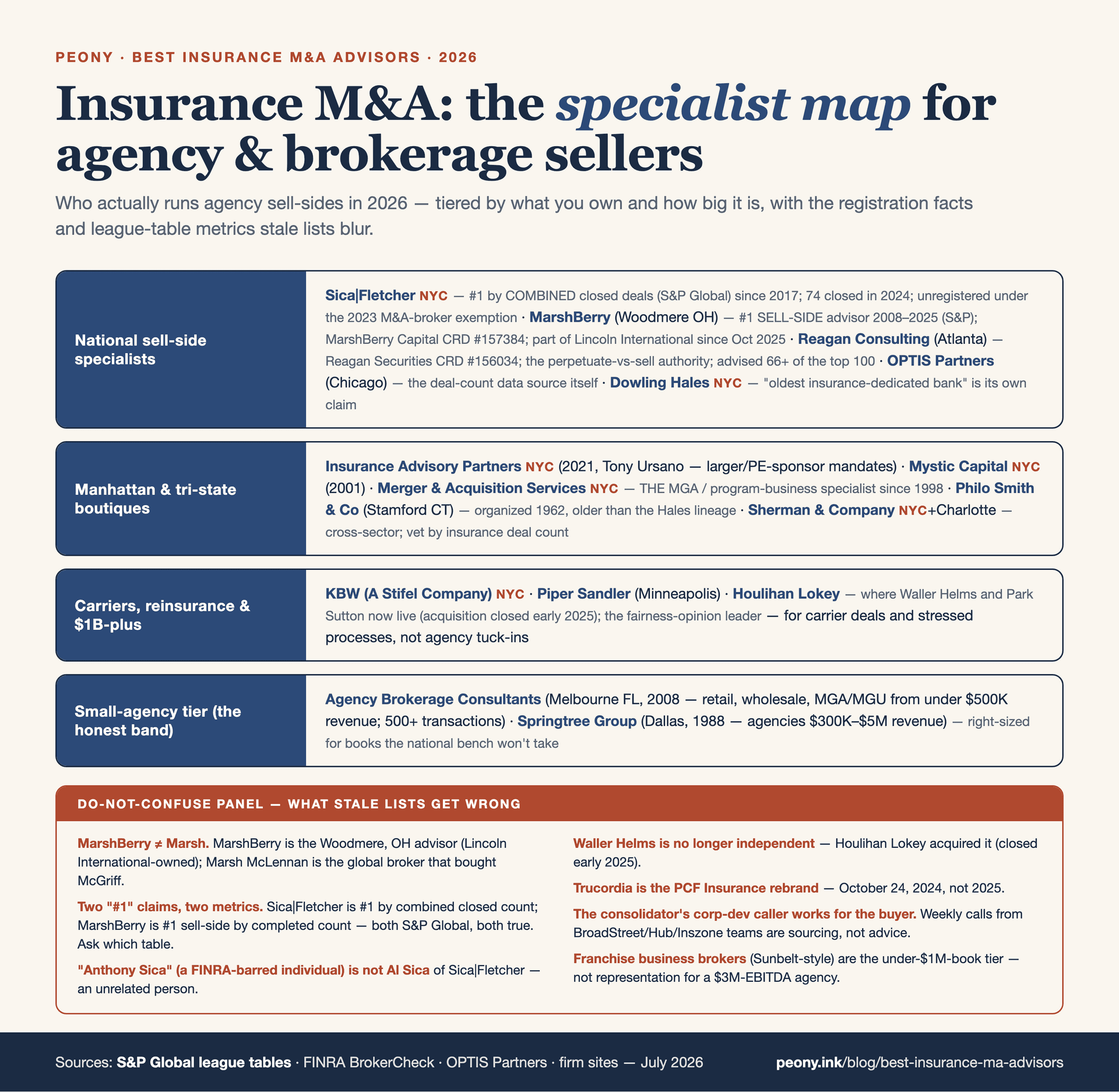

For an independent P&C agency or brokerage, the working core is a set of national, insurance-distribution sell-side specialists — firms whose entire practice is selling agencies, who live inside agency economics and the consolidator buyer pool, and who can make that pool compete. The five firms below are that core; the NY/tri-state boutiques, the carrier crossover, and the small-agency tier come after. Where I can print a verified CRD I do; where I cannot, I say so plainly.

Sica | Fletcher (Manhattan — 250 West Street; founded 2014) is the firm most agency owners should know first, and it is the most active advisor on sub-$500M deals. Its practice spans P&C agencies, employee benefits, MGAs and wholesalers, and insurtech distribution, on both the sell-side and buy-side, and it has closed more than $19B since inception. On the league tables, Sica | Fletcher is #1 by combined closed deal count (buy-side and sell-side together) on S&P Global, a position it has held since 2017 — 74 closed deals in 2024, 31 ahead of the number-two firm, with H1 2025 running 17 sell-side plus 20 buy-side. It publishes the widely cited SF Index. Verified recent mandates, with direction: it advised The Murphy Insurance Group on its sale to Highstreet Insurance Partners (May 15, 2025); advised Meyer & Rosenbaum on its sale to Hub International Midwest (March 31, 2025); advised Becker Benefit Group on its sale to ALKEME (April 8, 2025); and advised Cross Coastal Advisors on its sale to Highstreet (April 14, 2025). On registration: Sica | Fletcher operates as an unregistered M&A advisory under the federal M&A-broker exemption (effective March 29, 2023), not as a FINRA member — one tight explainer on what that means is in the vetting section below. Principals are Al Sica and Michael Fletcher. (Naming trap: Al Sica is not the separate, FINRA-barred "Anthony Sica.")

MarshBerry (Woodmere, OH; founded 1981 as Marsh, Berry & Co) is the deepest agency sell-side bench in the country and the other holder of a "#1" title — a different one. MarshBerry is #1 sell-side advisor from 2008 through 2025 per S&P Global (a completed sell-side-only metric, distinct from Sica | Fletcher's combined count — both are true, and the difference matters, so I state the metric explicitly). It pairs M&A advisory with consulting, valuation, and benchmarking across the agency sector, works deals from roughly $25M to $1B+, and completed 139 total M&A transactions in 2025. On registration, MarshBerry is one of only two firms on this page whose entity I can cite with a verified CRD: securities and M&A advisory run through MarshBerry Capital, LLC — FINRA CRD #157384 (SEC-registered plus 45 states). Ownership has changed twice: an Atlas Merchant Capital growth investment in January 2022, and then a full acquisition by Lincoln International, completed October 31, 2025 — so MarshBerry now operates as part of Lincoln International. For an agency owner selling into the consolidator wave, it is still the reference sell-side name. (Trap: MarshBerry is not Marsh, the global broker inside Marsh McLennan that bought McGriff.)

Reagan Consulting (Atlanta, GA) is the perpetuation-and-valuation authority for high-quality agencies — the firm to call when you are genuinely weighing a sale against staying independent. It has advised more than 66 of the top-100 US agents and brokers, combining M&A advisory with valuation, capital raising, and perpetuation planning (the internal-succession alternative to a sale), and it publishes the quarterly Organic Growth & Profitability survey and co-develops the Big "I" Best Practices Study. It works roughly $25M-$500M. Registration: Reagan's broker-dealer affiliate is Reagan Securities, Inc. — FINRA CRD #156034 (the second, and only other, verified CRD on this page). Reagan's own 2025 data is a useful market read: record 10.7% organic growth, with the best tier ($5-10M revenue) at 11.3% — a reminder that organic growth is now the multiple driver.

OPTIS Partners (Chicago, IL) owns the lower-middle market and is the firm whose data the whole sector quotes: it publishes the quarterly US and Canada agent-broker M&A deal report that this guide's market section draws on. Its practice is LMM P&C agency M&A plus valuation, principals Timothy J. Cunningham and Steve Germundson, working roughly $25M-$300M. OPTIS operates as an advisory firm under the M&A-broker exemption; I do not print a CRD for it because I could not verify one this pass. For a smaller agency that wants an advisor deeply embedded in the deal-count reality of the market, OPTIS is a natural fit.

Dowling Hales (Manhattan, plus Chicago, Boston, Vero Beach, and Farmington) works across both distribution and carriers, which makes it the bridge firm on this bench. It was formed in 2011 when Dowling & Partners acquired Hales & Company (founded 1973), and it dates its lineage to 1972; it has done more than 250 transactions since 2010, over $10B aggregate, and publishes The Hales Report. It bills itself as the oldest investment bank specializing in insurance — attribute that as a self-claim, because Stamford's Philo Smith & Co, organized 1962, predates it. It works roughly $50M-$1B. I do not print a CRD for Dowling Hales (unverified this pass). For an owner whose business straddles distribution and underwriting, Dowling Hales' dual coverage is the tell.

What's the insurance M&A advisor landscape in 2026? (the map)

The table below is the map for the whole insurance-distribution bench this guide covers — the national specialists, the NY/tri-state boutiques, the carrier crossover, and the small-agency tier. Each firm is profiled in its section; this is the at-a-glance routing. The registration column is deliberately conservative: I print a CRD only for the two firms I can verify, and "verify on BrokerCheck" everywhere else is the honest instruction, not a knock.

| Firm | HQ | Focus / band | Registration status | The tell (who it's for) |

|---|---|---|---|---|

| Sica | Fletcher | New York, NY (Manhattan) | Agencies/MGAs, sub-$500M sweet spot | Unregistered (M&A-broker exemption) | #1 combined closed deal count (S&P Global) since 2017; SF Index |

| MarshBerry | Woodmere, OH | Agencies, ~$25M-$1B+ | MarshBerry Capital, LLC — FINRA CRD #157384 | #1 sell-side advisor 2008-2025 (S&P Global); Lincoln-owned |

| Reagan Consulting | Atlanta, GA | High-quality agencies, ~$25M-$500M | Reagan Securities, Inc. — FINRA CRD #156034 | Perpetuation-vs-sale + valuation authority |

| OPTIS Partners | Chicago, IL | LMM agencies, ~$25M-$300M | Verify on BrokerCheck (M&A-broker exemption) | Owns the LMM; publishes the quarterly deal report |

| Dowling Hales | New York, NY (Manhattan) | Distribution + carriers, ~$50M-$1B | Verify on BrokerCheck | The distribution-and-carrier bridge; publishes The Hales Report |

| Insurance Advisory Partners (IAP) | New York, NY (Manhattan) | Insurance/insurtech M&A + capital | Verify on BrokerCheck | Ex-Willis Capital Markets pedigree; larger/sponsor mandates |

| Mystic Capital Advisors Group | New York, NY (Manhattan) | Distribution + carriers | Verify on BrokerCheck | Founded 2001 out of The Hartford; long track record |

| Merger & Acquisition Services | New York, NY (Manhattan) | Wholesale/retail, MGAs, programs | Verify on BrokerCheck | THE MGA/program-business specialist |

| Philo Smith & Co | Stamford, CT | Insurance/financial-services IB | Verify on BrokerCheck | Organized 1962 — the older-line CT tri-state cut |

| Sherman & Company | Charlotte + New York, NY | Cross-sector incl. insurance | Verify on BrokerCheck | Cross-sector; vet by insurance-distribution deal count |

| KBW (A Stifel Company) | New York, NY (Manhattan) | Carriers, reinsurance, FIG | Verify on BrokerCheck | Carrier/insurtech/reinsurance — not agency tuck-ins |

| Piper Sandler | Minneapolis, MN | Carriers + specialty finance | Verify on BrokerCheck (NYSE: PIPR) | Carrier tier; Financial Services Group |

| Houlihan Lokey | Global | Carriers, cross-bench, ~$1B+ | Verify on BrokerCheck (NYSE: HLI) | Now home to the former Waller Helms / Park Sutton |

| Agency Brokerage Consultants | Melbourne, FL | Under $500K to over $50M revenue | Verify on BrokerCheck | Small-agency tier, honestly framed |

| Springtree Group | Dallas, TX | $300K-$5M revenue agencies | Verify on BrokerCheck | Sub-scale business-broker band |

A few notes the table cannot carry. Sica | Fletcher and MarshBerry are the two names an agency owner should shortlist first — but for different reasons and on different metrics, so match the title to your need rather than treating "#1" as one crown. Reagan is the call if you are genuinely undecided between selling and perpetuating internally. The carrier tier (KBW, Piper Sandler, Houlihan Lokey) is a different animal entirely — those firms price carriers on loss ratios, combined ratios, and statutory capital, not agency EBITDA, so they belong on your list only if you own a carrier, an MGA underwriting risk, or a reinsurance book. And Houlihan Lokey is where "Waller Helms" now lives — the old standalone boutique was acquired, a change the market is still catching up to (and one our financial-services hub reflects in its current form).

Which insurance M&A advisor fits my situation — the NY/tri-state boutiques and the specialist tiers

This is the part the broad FIG hub does not do at agency resolution: matching your specific situation — where you are, what you sell, how big you are — to the right sub-bench. The national five above cover most agency owners; the firms below fill in the geography, the MGA/program niche, the carrier crossover, and the honest small-agency tier.

Who are the best New York and tri-state insurance M&A boutiques?

The New York thread runs through this whole guide, and it is worth pulling together, because a striking share of the insurance-distribution bench is Manhattan-based. Sica | Fletcher (250 West Street), Dowling Hales, and the carrier desk at KBW all sit in Manhattan, and the tri-state boutiques cluster around them. For local-bench context beyond insurance, our New York M&A advisors guide carries the broader city roster.

Insurance Advisory Partners (IAP) (Manhattan; founded 2021) was built by Antonio "Tony" Ursano — founder and former CEO of Willis Capital Markets, former president of TigerRisk, and former FIG vice-chairman at Bank of America — and it covers insurance and insurtech M&A, capital raising, and fairness and valuation opinions. It has done roughly 17 deals to date and advised sponsors like Stone Point Capital and Lee Equity Partners. Position it honestly: IAP's pedigree points toward larger and PE-sponsor mandates, so for a $1M-$10M-EBITDA agency it is a better fit at the top of that range than at the bottom.

Mystic Capital Advisors Group (Manhattan, plus London, Miami, Charlotte, and Denver; founded October 2001 by a team out of The Hartford, led by managing director Kevin P. Donoghue) covers both distribution and carriers and claims more than 1,000 transactions over 20-plus years. It is a long-track-record tri-state option across the agency and carrier spectrum.

Merger & Acquisition Services, Inc. (Manhattan; incorporated 1998, CEO Jason C. Murgio) is the specialist to call if your business is an MGA, MGU, program administrator, TPA, or program-business placement — it is an insurance-specialist investment bank for wholesale and retail agencies and the program-business market specifically, having served more than 500 insurance companies and agencies. If "agency" undersells what you actually are, this is your firm.

Philo Smith & Co (Stamford, CT; organized 1962) is the older-line boutique and the Connecticut tri-state cut — one of the longest-running insurance and financial-services investment banks, and, notably, older than Dowling Hales despite the latter's "oldest" self-claim. It offers M&A advisory alongside investment management and research.

Sherman & Company (Charlotte, NC, with a New York office; founded 2004) is a boutique investment bank spanning insurance, healthcare, technology, and asset and wealth management, with more than $11B closed. Because it is genuinely cross-sector, vet it specifically on its insurance-distribution deal count rather than its total volume — a firm that also does healthcare and tech is not automatically an agency specialist.

Who advises on insurance carriers, MGAs, and reinsurance (the larger-cap crossover)?

Insurance carriers — underwriting companies, life, annuity, and P&C insurers, MGAs and MGUs that carry risk, and reinsurers — are a different bench from agency distribution, priced on loss ratios, combined ratios, and statutory capital rather than agency EBITDA. If you own an agency, this tier is not for you; if you own a carrier or an underwriting MGA, it is exactly the tier you want.

Keefe, Bruyette & Woods (KBW), a Stifel company (Manhattan), is the definitive FIG franchise (since 1962; Stifel-owned since 2013) and runs dedicated insurance-carrier and reinsurance desks — the right call for carrier M&A, MGA/MGU sales, and reinsurance transactions, not for agency tuck-ins. Piper Sandler (Minneapolis; NYSE: PIPR) covers insurance carriers and specialty finance through its Financial Services Group (built on the former Sandler O'Neill), another carrier-tier option. And Houlihan Lokey (global; NYSE: HLI), the #1 global M&A fairness-opinion advisor over 25 years, is the call above roughly $1B or for a stressed or cross-bench situation — and, critically for anyone who remembers the old bench, Houlihan Lokey acquired Waller Helms Advisors (the Chicago insurance-and-wealth boutique) and Park Sutton, closing around the end of 2024 into early 2025 and roughly doubling its Financial Services Group; Waller Helms co-founders John Waller and David Helms joined as managing directors, and James Anderson is now global co-head of the FSG. So a seller who was going to call "Waller Helms" should now call Houlihan Lokey. For the full carrier-and-insurtech treatment and where an insurtech priced on recurring revenue belongs instead, see the financial-services hub.

What's the honest tier for a small agency — the business-broker band?

Below the scale the national specialists work, the economics flip: a full sell-side process, with its retainer and minimum fee, consumes too much of the proceeds, and the right venue is a firm that lives in the small-agency band. The important honesty here is that these are valuation-and-brokerage shops, not managed-auction investment banks — which is exactly right for a sub-scale agency and exactly wrong for a $9M-revenue agency that needs a competitive process.

Agency Brokerage Consultants (Melbourne, FL; founded 2008) provides valuation and sell-side representation across retail agencies, wholesalers, MGAs/MGUs, and program administrators, from under $500K to over $50M in revenue, with more than 500 M&A transactions and 3,000-plus valuations to its name. Springtree Group (Dallas/Carrollton, TX; established 1988) works agencies in the $300K-$5M revenue band, pairing M&A with lending and financial-performance consulting through a network of sell-side business brokers. Both serve the small tier honestly — and both are the honest alternative to the business-broker franchises (Sunbelt, Transworld) that work sub-$1M books and are not built for a $1M-$10M-EBITDA agency at all.

What insurance agency multiples are realistic in 2026 — and whose data says so?

The single most important discipline in reading 2026 agency multiples is to label every number with whose data it is and whether it is a mean or a band — because there is no one "market" multiple, and a headline quoted without its source is a negotiating trap. Here are the anchors, labeled explicitly.

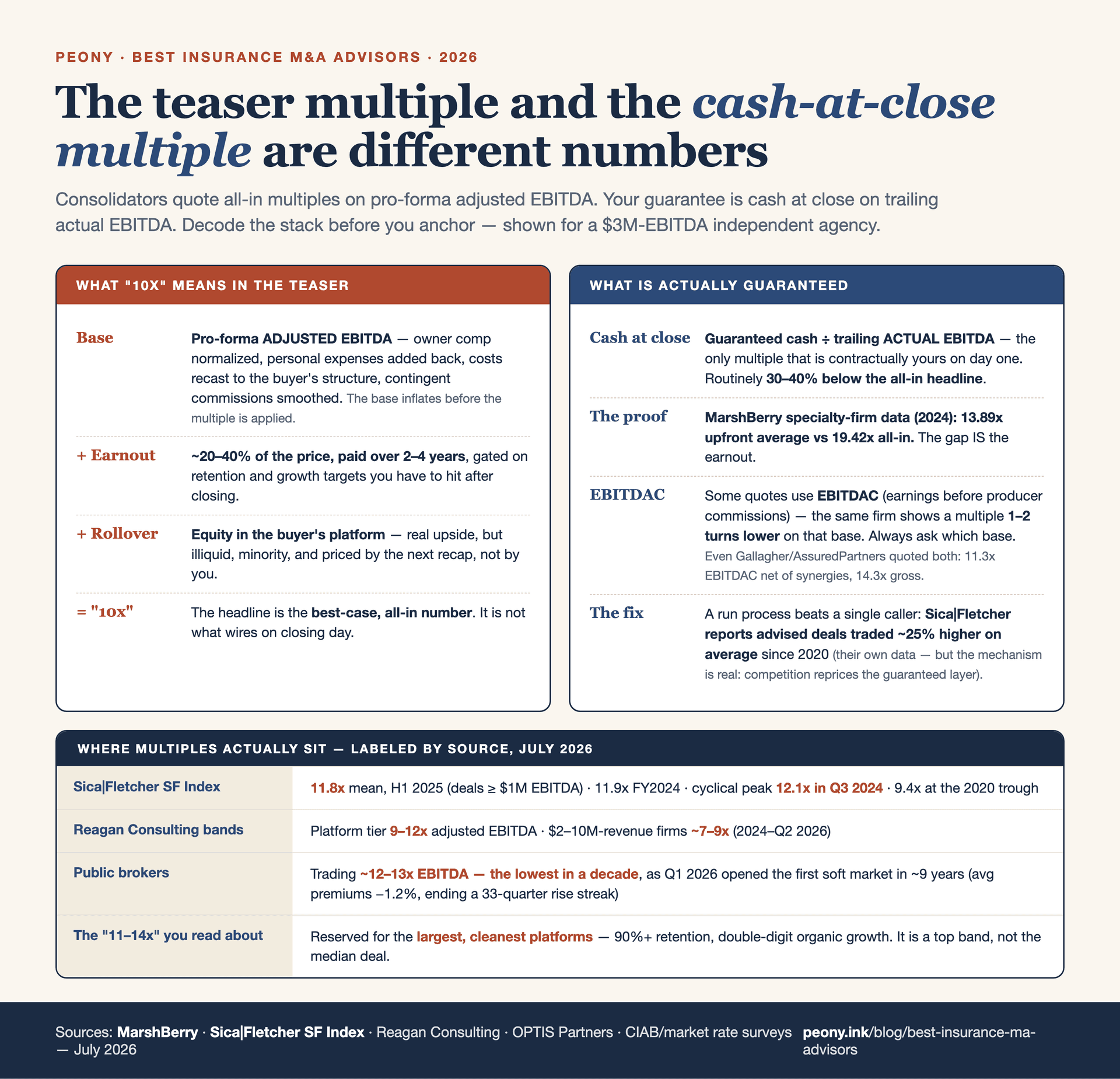

- Sica | Fletcher SF Index (deals of at least $1M of EBITDA; a blended mean): about 11.8x in H1 2025, 11.9x for full-year 2024, a cyclical peak around 12.1x in Q3 2024, up from a 9.4x trough in 2020. This is the best single read on where blended agency deals cleared — but it is a mean, pulled up by the largest and cleanest platforms.

- Reagan Consulting: the LMM platform band has stabilized in the 9x-12x adjusted-EBITDA range, with $2-10M-revenue firms closer to 7x-9x. (A "12.5x" figure sometimes quoted for high-quality $3-10M-revenue brokers traces to a Q3 2023 vintage — use the current 9-12x band and label it.)

- The "11-14x" ceiling: reserved for the largest and cleanest platforms only — consistent with what our financial-services guide says for the top of the band, and not the number a $9M-revenue agency should plan around.

- Public brokers: trading around 12-13x EBITDA — the lowest in a decade — as slowing organic growth (public retail broker average organic growth around 3.2%; Marsh's FY2025 organic 4%, down from 7% in 2024), soft pricing, and AI uncertainty weigh on the group.

For a $9M-revenue, $3M-EBITDA agency, the honest planning anchor is the blended mean (roughly 11-12x per Sica | Fletcher and Reagan), not the platform ceiling — and even that assumes clean books, 90%+ retention, and real organic growth. Sub-$10M-revenue tuck-ins closer to 7x-9x are the more common reality for smaller or less-clean agencies.

How do I read a consolidator teaser — EBITDA vs adjusted EBITDA vs EBITDAC?

This is the emotional core of an agency sale, so I'll take it slowly. A teaser multiple hides two moving parts — what number the multiple is applied to, and how much of the price is actually guaranteed — and the whole art of not being taken advantage of is separating them.

The base. There are three different earnings numbers, and they are not interchangeable:

- EBITDA — earnings before interest, taxes, depreciation, and amortization: your baseline profit.

- Adjusted EBITDA — EBITDA plus add-backs a buyer considers non-recurring or owner-specific: above-market owner compensation normalized, discretionary and personal expenses removed, one-time costs stripped, and contingent/profit-share commissions smoothed to a rolling average (then often underwritten at a lower forward run-rate). Adjusted EBITDA is almost always higher than reported EBITDA — which is exactly why buyers quote multiples on it.

- EBITDAC — earnings before interest, taxes, depreciation, amortization, and commissions: producer commissions treated as an add-back variable cost. Because EBITDAC is a bigger base number, the same purchase price expressed as an EBITDAC multiple looks one to two turns lower than the same price expressed as an EBITDA multiple. An "11.3x EBITDAC" offer is not cheaper than a "13x EBITDA" offer — they can be the identical dollar amount (the Gallagher/AssuredPartners deal was quoted at 11.3x EBITDAC net of synergies versus 14.3x gross). Never compare two offers until both are expressed on the same base.

The guarantee. The headline is almost always an all-in multiple that includes the full earnout. The guaranteed cash you actually receive at close is a lower multiple applied to your trailing actual EBITDA. The MarshBerry specialty-firm data frames the spread: about 13.89x upfront versus 19.42x all-in in 2024 — meaning roughly 30-40% of the "price" is contingent.

A worked example on your $3M of EBITDA. Suppose a teaser says "10x." Decode it:

- If "10x" is computed on pro-forma adjusted EBITDA that the buyer marks up from $3M actual to, say, $3.6M, the implied enterprise value is about $36M, not $30M — the adjustment did the work.

- But if that "10x" is the all-in figure and the guaranteed-cash multiple is materially lower (the MarshBerry pattern implies the upfront can be roughly 70% of all-in), the cash you're guaranteed at close might be closer to 7x — on the order of $21M-$25M depending on the base — with the remaining $11M-$15M riding on earnout targets over the next two to four years.

Neither number is a lie; they measure different things. The two questions to put in writing before you sign: what EBITDA figure is this multiple applied to (actual or pro-forma adjusted, EBITDA or EBITDAC), and how much is guaranteed cash at close versus earnout. A specialist advisor asks both on your behalf before the first handshake — and re-bases the number in your favor.

How is an agency sale structured — cash, earnout, rollover, and the carrier landmine?

Insurance-agency consideration almost always comes in three parts: guaranteed cash at close, an earnout, and sometimes rollover equity. Getting the split and the definitions right is where an advisor earns the fee.

Earnouts typically run about 20-40% of total price, spread over two to four years, tied to retention, revenue, or EBITDA-growth targets. The risk is rarely outright non-payment — it is that once you sell, you no longer fully control the levers (the buyer sets budgets, may reassign accounts or producers, and defines how the metric is measured), so the definition matters more than the size: specify the metric, the measurement method, the accounting, and your operational authority during the earnout period, and insist retention is measured on terms you can actually influence.

Rollover equity — reinvesting 20-40% of proceeds into the buyer's platform — is a genuine "second bite" if the platform grows, but its value lives entirely in the fine print (common vs preferred, where you sit relative to the sponsor's preferred stack and debt, tag-along and drag-along rights, and how your basis is set versus the sponsor's). It concentrates your wealth in a single illiquid sponsor-controlled asset, so model it as its own risk line, not a number bolted onto the multiple.

Retention math is the through-line: 90%+ book retention supports a premium multiple; 80-90% is acceptable; under 80% triggers heavy earnout and compression. The levers you control are book quality, producer non-solicits, and carrier appointments. Producer non-solicitation and employment agreements are standard, because buyers underwrite producer continuity directly.

Asset sale vs stock sale — and the carrier-appointment landmine. An asset sale is the norm for smaller and tuck-in deals (liability avoidance plus a stepped-up basis for the buyer), but it carries a specific consequence: carrier appointments do not transfer automatically — the buyer must be or become appointed by each carrier, and the book is assigned or novated. A stock sale keeps the entity intact, but carriers generally retain change-of-control termination rights, so appointment survival is a matter of carrier forbearance, not law. Either way, the #1 closing-condition landmine is the carrier-contract consent: agency-company agreements carry notice-and-consent provisions on change of control, with notice periods ranging from 30 days up to six months for major carriers, and a carrier may consent, renegotiate, or terminate. A specialist sequences those consents into the closing timeline; a generalist discovers them in the eleventh hour.

How do I run a confidential agency sale — and protect my producers and carriers?

Confidentiality in an agency sale is not a nicety, because your most sensitive assets — your producers and their books, your carrier appointments, your named accounts — are exactly what walks out the door if the process leaks. This is the Peony-native part of the guide, so I'll be concrete about the mechanics and honest about where the room ends and the advisor begins.

Staged, curated disclosure is the whole game. A quiet process protects staff, carrier, and producer information through four levers: a tight, curated buyer list rather than a broad auction; staged disclosure behind NDAs (a blind teaser with no agency name first, then identity and the full room only after a strong NDA, then the crown-jewel material — producer-level books, carrier-appointment detail, named-account and commission data, key-employee comp — released only as a bidder advances past its indication of interest); a strict internal need-to-know circle (often just you, your CFO or controller, and one trusted person) with diligence calls scheduled off-hours; and per-bidder controls in the data room so competing bidders never see each other's questions or your most sensitive files early.

On carriers specifically: carrier appointments and change-of-control consents come at signing and closing, not at exploration. You do not tell your carriers you are "thinking about selling." You address their contractual consents once you have a signed deal and a specific, approvable buyer — which is also why sequencing (the advisor's job) and traceable document control (the room's job) matter so much.

This is where a modern data room earns its keep. Peony is SOC 2 Type II certified and used by more than 5,900 customers, and for an agency sale the model is purpose-built: a room per buyer conversation via visitor groups that wall each bidder into their own view, producer-safe permissions so sensitive producer and carrier detail only unlocks for advanced bidders, per-viewer watermarks and screenshot protection that make any leaked page traceable to the one party that leaked it, dynamic NDA gating before access, redaction to mask account and producer names until you choose to reveal them, and page-level analytics that show which bidder is genuinely engaged. To be clear about scope: Peony is not an M&A advisor and does not place deals — your banker runs the human side of confidentiality; the room enforces the document side. See how analytics spot the serious buyers and the M&A data room playbook.

What's the New York angle — selling a NY agency vs a NY carrier?

Here is a distinction no generic listicle explains, and it changes how a New York seller should think about timing: selling a NY-domiciled agency is a light-touch, administrative event, while selling a NY-domiciled carrier is a heavy, regulator-gated one. They are not the same transaction, and conflating them is a common and costly error.

Selling a NY agency or brokerage (a licensed producer entity) is light-touch. There is no Form A and no DFS change-of-control approval for the sale of a licensed producer. The mechanics are administrative: the entity reports owner and officer changes to the Department of Financial Services by letter; the buyer ensures its own producer licenses and carrier appointments are in place (an appointing insurer files its notice of appointment within 15 days); and non-resident producer status is updated through NIPR and DFS. Crucially, an appointment is not a license — carrier appointments have to be re-papered even though licenses travel — and this re-papering, administered through ALiS, the DFS portal, and NIPR, is the real work of closing a NY agency deal. No regulator sign-off gates the sale itself. That is genuinely good news for a NY agency owner: your timeline is driven by the process and the carrier consents, not by a state approval clock.

Selling a NY carrier is heavy. If what you own is an underwriting company (or an MGU tied to one), a change of control runs through New York Insurance Law §1506 and Regulation 52 — a Form A filing with the Superintendent (with disclaimer-of-control mechanics under §1501(c) and DFS Circular Letter 5 of 2022), administered via DFS Connect/ALiS, on a roughly two-to-six-month timeline. That is the same regulatory gate our financial-services hub describes for carriers — and it is why the carrier tier (KBW, Piper Sandler, Houlihan Lokey) sequences the deal around approval, while an agency sale does not need to.

The practical upshot: the Northeast is core consolidator hunting ground — the 2025 Sica | Fletcher mandates above (Massachusetts, Maryland, and tri-state agencies going to Highstreet, Hub, and ALKEME) show the pattern — and a New York agency owner fields the same weekly calls as everyone else while sitting closest to the deepest advisor bench in the country. The Manhattan roster (Sica | Fletcher on 250 West Street, Dowling Hales, IAP, Mystic Capital, Merger & Acquisition Services, KBW) plus Philo Smith in Stamford means the specialists are, quite literally, down the street. For the broader city bench, see our New York M&A advisors guide.

What do insurance M&A advisors charge in 2026?

The honest answer is that there is no published fee schedule for insurance-distribution advisors — the sell-side specialists do not post rate cards — so I'll describe the models qualitatively and give you the one number sellers actually report. Agency owners commonly report being quoted roughly 2-4% as a success fee on the transaction (a range sellers report, not a published schedule), with the rate declining as deal size grows, typically alongside a monthly retainer or work fee credited against the success fee, and a tail covering named buyers for a period after the engagement ends.

Two things move the real bill more than the headline rate. The first is the minimum fee — on a smaller deal the floor, not the percentage, can set the number. The second is the definition of transaction value: a broad definition that sweeps in the earnout and rollover inflates the base on the same headline price, so pin down whether the fee runs on guaranteed cash, total consideration, equity value, or enterprise value. Weigh whatever you are quoted against the uplift the specialists publish (roughly 20-25% on average, their own data) — on a $3M-EBITDA agency, that math usually clears the fee comfortably. For the full mechanics — including how declining-rate Lehman and Double-Lehman structures work across lower-middle-market M&A generally — see our M&A advisor fees guide, exactly as our financial-services hub does.

What are the traps an agency seller should watch for?

Insurance-distribution M&A is full of near-misses that a careful seller can sidestep. The panel below is the one I'd tape to the wall before taking a single consolidator call.

- MarshBerry is not Marsh. MarshBerry is the Woodmere, Ohio sell-side advisor (now Lincoln-owned); Marsh is the global broker inside Marsh McLennan that bought McGriff. Different companies entirely.

- The two "#1" claims measure different things. Sica | Fletcher is #1 by combined closed deal count (buy + sell) on S&P Global since 2017; MarshBerry is #1 sell-side advisor 2008-2025 on S&P Global. Both are true; neither is "the #1 firm" without the metric attached.

- Al Sica is not "Anthony Sica." The FINRA-barred "Anthony Sica" is a different individual from Al Sica of Sica | Fletcher. Do not merge the identities.

- "Oldest" is a self-claim. Dowling Hales bills itself as the oldest insurance-dedicated bank, but Philo Smith & Co (organized 1962) predates it. Attribute the claim; don't assert it.

- Waller Helms is now Houlihan Lokey. The standalone Waller Helms boutique was acquired by Houlihan Lokey (closed end-2024/early-2025), along with Park Sutton. If a source still lists it as independent, that source is stale.

- The consolidator's caller represents the buyer. In-house corporate-development teams at Hub, BroadStreet, and the rest are not advisors — they are buying your agency for their employer.

- Sunbelt and Transworld are the wrong tier. Those business-broker franchises work sub-$1M books, not $1M-$10M-EBITDA agencies. Agency Brokerage Consultants and Springtree serve the small tier honestly; the national specialists serve the rest.

- Trucordia rebranded October 24, 2024 — from PCF Insurance Services, not in 2025. Small detail, but a tell for whether your source is current.

- OPTIS and MarshBerry count different universes. OPTIS's 695 deals (down 12%) and MarshBerry's 854 (up ~1%) are not contradictory — they measure different things. Attribute each; never blend them.

- EBITDAC runs one to two turns lower than EBITDA. A teaser's all-in EBITDAC number is not the guaranteed cash-at-close EBITDA multiple. Get both offers on the same base before you compare.

- "$13.4B" for Aon/NFP is announced consideration, not a precise enterprise value (SEC filings imply ~$13.0B EV / ~$9.1B GAAP). Don't over-precise a headline.

- Cross-sector boutiques need an insurance-specific check. A firm that also does healthcare, tech, and wealth (like Sherman & Company) may be excellent, but vet it on its insurance-distribution deal count, not its total volume.

The bottom line

Insurance-distribution M&A isn't one league table — and the consolidator calling you weekly isn't your advisor. For a national process, the two names to shortlist first are Sica | Fletcher and MarshBerry (each #1 on a different, clearly labeled metric), with Reagan Consulting if you're weighing sale against perpetuation, OPTIS Partners for the lower-middle market, and Dowling Hales if you straddle distribution and carriers. In the tri-state, the boutiques — IAP, Mystic Capital, Merger & Acquisition Services, Philo Smith, and Sherman & Company — cluster within blocks of each other in Manhattan and Stamford. If you own a carrier rather than an agency, that's the KBW / Piper Sandler / Houlihan Lokey bench, priced on a different currency and gated by a Form A. Whoever you hire, the moves that defend your price are the same: decode the teaser (what base, how much guaranteed), run a curated competitive process so two or three buyers set your terms instead of one, sequence the carrier consents from day one, and walk in with clean, normalized numbers sitting in a staged, walled data room. That preparation — more than the logo on the engagement letter — is what closes the gap between the teaser and the check.

Related resources

- Best financial-services & FIG M&A advisors — the parent hub this guide carves from: banks and thrifts, RIAs, specialty finance, broker-dealers, and the insurance-carrier bench, matched to subsector and deal size.

- Best M&A advisors in New York — the local bench for the Manhattan/tri-state insurance boutiques above, in the broader city context.

- Best M&A advisors in Tampa — the home-city guide for the Baldwin Group and Florida's consolidator ecosystem, a natural read when a consolidator comes calling.

- Best M&A advisors in Cincinnati and best M&A advisors in Columbus — the Ohio insurance corridor, home turf for MarshBerry (Woodmere) and a deep agency ecosystem.

- M&A advisor fees and advisor vs. broker vs. investment bank — what advisors charge and which intermediary tier fits your size.

- Sell-side due diligence and the M&A due diligence process guide — packaging producer continuity, retention, and normalized EBITDA before you go to market.

- M&A data room, investment banking data room, best data room for a small M&A deal, and how analytics spot serious buyers — running the confidential, competitor-bidder process.

Frequently asked questions

A consolidator has been calling me for months — should I hire a sell-side advisor or just negotiate with them directly?

In almost every case, hire the advisor — because the consolidator who has been calling you is not your advisor; they are the buyer's corporate-development team, and their job is to buy your agency for as little as the market will let them. That is not a knock on them; it is the structure. Until two or three consolidators are bidding against each other on a clock, a friendly weekly call is a one-on-one negotiation, and a one-on-one negotiation is the single structure guaranteed to leave money on the table. A sell-side insurance advisor turns that inbound interest into a real process: it quietly adds the other PE-backed platforms and strategics buying agencies in your region, runs them behind an NDA on a bid deadline, and negotiates not just the headline multiple but the structure — the split between guaranteed cash at close, earnout, and rollover equity, the retention math, the producer non-solicits, and the carrier-appointment consents that decide whether the deal even closes. The advisors publish their own uplift data: Sica | Fletcher reports that agencies it advised sold for about 25% higher on average than non-advised deals since 2020 (their own stat), and MarshBerry cites a client that improved on its initial offer by 23% after a select-buyer process. The narrow case for going direct is a single trusted strategic offering a genuine premium where speed and confidentiality matter more than the last dollar — but even then, quiet competitive tension usually improves the terms. I run Peony, a data room company used by 5,900+ customers, so I see the document side of these processes — but pick your banker first. For banks, RIAs, and the full FIG map, see our financial-services M&A advisors guide.

How much more does an agency actually sell for with an advisor versus going direct?

The honest answer is that the sell-side specialists publish their own uplift numbers, and they cluster around 20-25% on average — label them as advisor-reported, not an independent guarantee. Sica | Fletcher reports that deals it advised traded about 25% higher on average than non-advised deals since 2020 (their own data), and MarshBerry cites a specific client that improved 23% over its initial offer after running a select-buyer process. The mechanism is more useful than the percentage. A single unsolicited consolidator offer is anchored on the low combination — a guaranteed-cash multiple applied to your trailing actual EBITDA. A run process moves you toward the high combination — an all-in multiple (including earnout) applied to a pro-forma adjusted EBITDA, with two or three bidders competing to set it. The MarshBerry specialty-firm data shows how wide that gap can be: about 13.89x upfront versus 19.42x all-in in 2024. An advisor does not conjure the difference out of nothing — it captures it by creating competition and by re-basing the EBITDA the multiple is applied to. Weigh that against the fee (sellers report being quoted roughly 2-4%, described qualitatively below), and on a $3M-EBITDA agency the uplift math usually clears the fee comfortably. Our M&A advisor fees guide has the full mechanics.

The teaser on my $3M EBITDA agency says "10x" — is that real or adjusted-EBITDA games?

Treat "10x" as a question, not a price, because a teaser multiple hides two moving parts: what number the multiple is applied to, and how much of the price is guaranteed. First, the base. A consolidator will compute "10x" on pro-forma adjusted EBITDA — your reported EBITDA after add-backs (owner compensation normalized, discretionary expenses removed, contingent commissions smoothed and often underwritten at a lower forward run-rate) and after the buyer's own cost structure is layered in. If those adjustments lift your $3M of actual EBITDA to, say, $3.6M pro-forma, then "10x" is really $36M of enterprise value, not $30M. Second, the guarantee. That headline is almost always an all-in multiple that includes the full earnout. The guaranteed cash you receive at close is computed on a lower multiple applied to your trailing actual EBITDA. The MarshBerry specialty-firm gap between upfront and all-in multiples (the exact 2024 figures are in the valuation section above) frames the spread starkly — a "10x all-in" can mean something closer to 7x guaranteed, with the rest riding on hitting earnout targets over the next two to four years. Ask two questions in writing: what EBITDA figure is this multiple applied to (actual or pro-forma adjusted, and is it EBITDA or EBITDAC), and how much is guaranteed cash at close versus earnout. A specialist advisor decodes both before you ever sign. See the worked example in the valuation section above.

What's the difference between EBITDA, adjusted EBITDA, and EBITDAC in an agency valuation?

These are three different numbers, and conflating them is the most common way an agency owner mis-reads an offer. EBITDA is earnings before interest, taxes, depreciation, and amortization — your baseline profit. Adjusted EBITDA takes that and adds back items a buyer considers non-recurring or owner-specific: above-market owner compensation, personal or discretionary expenses run through the business, one-time costs, and often a smoothing of contingent and profit-share commissions to a rolling average that is then underwritten at a lower forward run-rate. Adjusted EBITDA is almost always higher than reported EBITDA, which is why buyers quote multiples on it. EBITDAC is earnings before interest, taxes, depreciation, amortization, and commissions — it treats producer commissions as a variable cost added back. The critical consequence: because EBITDAC is a larger base number, the same purchase price expressed as an EBITDAC multiple looks one to two turns lower than the same price expressed as an EBITDA multiple. So an offer quoted as "11.3x EBITDAC" is not cheaper than one quoted as "13x EBITDA" — they can be the identical dollar amount (the Gallagher/AssuredPartners deal, for scale, was quoted at 11.3x EBITDAC net of synergies versus 14.3x gross). Never compare two offers until you have both expressed on the same base. Sica | Fletcher, for instance, computes target margins excluding contingent commissions precisely so the base is defensible. Ask every bidder to state the base explicitly.

What are independent P&C agencies actually selling for in 2026 — are multiples really down from 2021?

Yes, multiples softened from the peak, but the more accurate framing is that the cyclical high was more recent than 2021 for private agencies, and the current level is still historically strong. On Sica | Fletcher's SF Index (deals of at least $1M of EBITDA, a blended mean), the market ran about 11.9x for full-year 2024, peaked around 12.1x in Q3 2024, and eased to about 11.8x in the first half of 2025 — well above the 9.4x trough of 2020. So the honest statement is not "multiples crashed since 2021" but "they set a cyclical high in late 2024 and have softened modestly since" (label that as Sica | Fletcher's mean). Reagan Consulting frames the platform band as having stabilized in the 9x-12x adjusted-EBITDA range, with smaller $2-10M-revenue firms closer to 7x-9x. The "11-14x" you may have read is defensible only for the largest and cleanest platforms — it is not the median, and it matches the top-of-band framing in our financial-services guide. Public brokers, a useful reference point, are trading around 12-13x EBITDA — the lowest in a decade — as slowing organic growth, soft pricing, and AI uncertainty weigh on the group, and that pressure flows down into private-platform pricing. For a $9M-revenue, $3M-EBITDA agency, plan around the blended mean, not the platform ceiling.

Should I sell my agency now or wait for multiples to recover?

This is a genuine judgment call, and the honest answer is that it depends on your organic growth more than on the multiple cycle — but two 2026 facts should shape the decision. First, the buyer pool is shrinking: OPTIS Partners counts about 95 unique buyers in 2025, down from 104 in 2024, and falling every year since 2021, with total agent-broker deal count at a decade low (OPTIS: 695 deals in 2025, down 12%, with Q4 the lowest quarter since 2019). Fewer buyers doing fewer deals is not a reason to panic, but it is a reason not to assume the window widens on its own. Second, and more important for pricing, the commercial P&C market turned soft in Q1 2026 — average premiums fell about 1.2%, ending a 33-quarter streak of increases, with some property lines seeing double-digit rate decreases. Soft pricing removes the rate-driven revenue tailwind that lifted agency growth for years, which means organic growth now carries the multiple. If your agency is growing organically at a healthy clip with 90%+ retention, you screen as a premium asset regardless of the cycle, and you have leverage now. If your growth was mostly rate-driven, waiting risks watching your own numbers soften alongside the market. The strongest move is usually to prepare a clean process now and let a competitive bench — not the cycle — set your price. Our sell-side due diligence guide covers how to package that.

Hub, Acrisure, BroadStreet and the other consolidators keep calling — does it matter which one buys us?

It matters enormously — and the fact that several are calling is precisely the argument for running them against each other rather than picking one. The 2025 acquirer table (OPTIS Partners) shows how concentrated and how varied this pool is: BroadStreet Partners led with about 69 deals (OPTIS-reported, with some source variance in the exact figure), down from 90 in 2024; Hub International did 49 (down from 61); Inszone 45; and Leavitt Group 29 — notable as the only privately held broker in the top 10, when about 72-73% of all deals went to PE-backed or hybrid buyers. Those buyers differ in ways that hit you directly: how they compute pro-forma EBITDA, how much they guarantee as cash at close versus earnout, whether they want you and your producers to stay and roll equity, how they treat your brand and staff post-close, and how their carrier relationships mesh with yours. A platform desperate to enter your region pays differently from one adding a tuck-in to an existing hub. Two names to keep straight: Trucordia rebranded from PCF Insurance Services on October 24, 2024, and the largest platforms sit under strategics now (AssuredPartners under Gallagher, Risk Strategies/One80 under Brown & Brown). A sell-side advisor knows which platforms are hungry this quarter and makes them compete — that competition, not the logo, sets your terms.

How do Sica Fletcher, MarshBerry, and the other big insurance M&A advisors actually differ?

The most important thing to understand is that the two headline firms hold different number-one titles measured on different metrics — and any advisor who blurs that is selling you a slogan. Sica | Fletcher (New York, founded 2014) is #1 by combined closed deal count on S&P Global league tables — buy-side and sell-side transactions together — and has held that spot since 2017 (74 closed deals in 2024, 31 ahead of the number-two firm); it publishes the SF Index and has closed more than $19B since inception. MarshBerry (Woodmere, Ohio, founded 1981) is #1 sell-side advisor from 2008 to 2025 per S&P Global — a completed sell-side-only metric — and pairs its M&A bench with deep consulting, valuation, and benchmarking; it is now part of Lincoln International (acquired October 31, 2025). Both claims are true; they simply count different things, so match the metric to your need. Beyond those two: Reagan Consulting (Atlanta) is the perpetuation-and-valuation authority for high-quality agencies weighing sale against staying independent; OPTIS Partners (Chicago) owns the lower-middle market and publishes the quarterly deal report; and Dowling Hales (New York) covers distribution and carriers and bills itself as the oldest insurance-dedicated bank (a self-claim — Stamford's Philo Smith & Co, organized 1962, predates it). One naming trap: MarshBerry is not Marsh (the global broker inside Marsh McLennan), and Al Sica of Sica | Fletcher is not the separate, FINRA-barred "Anthony Sica." Vet each firm on deals closed in your size band in the last 18 months, not on the league-table headline.

Is rollover equity in a PE-backed platform actually worth anything?

Sometimes it is worth more than the cash — and sometimes it is worth far less than the headline implies; the difference is in terms you have to read carefully rather than in the pitch. When a PE-backed consolidator asks you to roll 20-40% of your proceeds into equity in their platform, they are offering you a "second bite": if the platform grows and sells or recapitalizes in a few years, your rolled stake can appreciate meaningfully, and rolling is often how the highest headline multiples get justified. But the value is entirely a function of the fine print. Ask: is it common equity or preferred, and where does it sit relative to the sponsor's preferred stack and any debt (you can be diluted or subordinated)? What are the tag-along and drag-along rights, and can you be forced to sell — or blocked from selling — at the sponsor's timing? How is the rollover valued going in versus how the sponsor's own basis is set? What happens to your stake if the platform underperforms or the next recap is a down round? Rollover concentrates your wealth in a single, illiquid, sponsor-controlled asset right after you have sold your diversified, cash-generating business — so it is not free money, it is a leveraged bet on that specific platform. A specialist advisor and an M&A attorney model the rollover as its own line item with its own risk, not as a number bolted onto the multiple. Treat a high all-in multiple that leans heavily on rollover as a claim to stress-test.

How often do earnouts actually pay out in agency sales?

There is no published universal payout rate, so the honest framing is structural: earnouts are a large slice of agency deals — typically about 20-40% of total price, spread over two to four years and tied to retention, revenue, or EBITDA-growth targets — which means a meaningful share of your "price" is contingent by design, and whether it pays depends on targets you partly stop controlling the day you sell. The MarshBerry specialty data (the upfront-versus-all-in gap in the valuation section above) implies roughly 30-40% of total value sitting in the earnout. The risk is not usually outright non-payment; it is that post-close you no longer fully control the levers — the buyer sets budgets, may reassign accounts or producers, changes carrier relationships, and defines how the target metric is measured. That is why the definition matters more than the headline: insist that the earnout metric, the measurement method, the accounting, and your operational authority during the earnout period are all specified precisely in the agreement, and that retention is measured on terms you can actually influence. Retention is the through-line — 90%+ book retention supports a premium and a payable earnout; under 80% triggers compression and puts the earnout at risk. A sell-side advisor negotiates the earnout definition, not just its size, and that negotiation is often worth more than a fraction of a turn on the headline multiple.

How do I keep a sale process confidential from my 25 staff — and from my carriers?

Confidentiality is a process-design problem, and in an agency it is acute because a leak can spook producers, staff, and carriers before you have signed anything. Four levers do most of the work. First, a tight, curated buyer list rather than a broad auction — the fewer parties who know, the lower the leak risk. Second, staged disclosure behind NDAs: a blind teaser (no agency name) goes out first; your identity and the full data room open only to bidders who have signed a strong NDA; and the most sensitive material — producer-level books, carrier-appointment detail, named-account and commission data, key-employee compensation — is held back until bidders have advanced past indications of interest. Third, a strict internal need-to-know circle (often just you, your CFO or controller, and maybe one trusted person) with diligence calls scheduled off-hours and a cover story for unusual activity. Fourth — and this is the carrier point specifically — carrier appointments and change-of-control consents come at signing and closing, not at exploration; you do not notify carriers that you are "thinking about selling," you address their contractual consents once you have a signed deal and a specific buyer. This is where the data room earns its keep: Peony — used by 5,900+ customers — gives you visitor groups that wall each bidder into their own view, per-viewer watermarks and screenshot protection that make a leaked page traceable to one party, dynamic NDA gating before access, redaction to mask names until you choose to reveal them, and page-level analytics. Your advisor manages the human side; the room enforces the document side.

How do I keep my top producers from bolting mid-process?

Producer flight is the agency seller's single biggest self-inflicted risk, and the defense is part legal, part informational, and part timing. On the legal side, the durable protection is contractual: producer employment agreements with non-solicitation covenants and clear book-ownership terms, in place before you go to market, so a buyer can underwrite that the producers — and the accounts they service — stay. Buyers price in worst-case attrition unless you can prove the book is sticky and the producers are bound; retention above 90% supports a premium multiple, while retention slipping under 80% triggers earnout compression. On the informational side, the same need-to-know discipline that protects confidentiality protects your producers: the fewer people who know a process is running, the less rumor churns, so keep the circle tight and let staged disclosure control what leaks. On the timing side, plan how and when you tell key producers — usually late, and usually paired with retention incentives the buyer funds (stay bonuses, rollover participation, or new producer agreements), so the news arrives with an upside attached rather than as a threat. Document producer non-competes, book ownership, and persistency before the buyer asks, because unprotected producers are exactly the risk a buyer will discount hardest. Our sell-side due diligence guide covers how to package producer continuity, and Peony's page-level analytics show which bidder is seriously engaged so you only expose sensitive producer detail to real buyers.

You might also like

Jun 16, 2026

18 Best Financial Services & FIG M&A Advisors for $25M-$1B Deals (2026)

Jul 17, 2026

9 Best M&A Advisors in Las Vegas for $5M–$500M Deals (2026)

Jul 16, 2026

7 Best M&A Advisors in Raleigh-Durham for $5M–$500M Deals (2026)