8 Best M&A Advisors in Cincinnati for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led exits, family-business successions, PE recapitalizations, and strategic carve-outs — and Cincinnati is the entry in our M&A advisor series where the city's identity should shape who you hire more than in almost any other metro. Most "best Cincinnati M&A advisors" pages either pad the list with wealth managers and insurance asset managers that do not run sell-side deals, or they list a dozen "M&A advisory" firms without telling you which ones are FINRA-registered broker-dealers, which operate under the M&A-broker exemption, and which are something else. At Peony we now serve more than 6,800 customers, and Greater Cincinnati sits right in the heart of the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark.

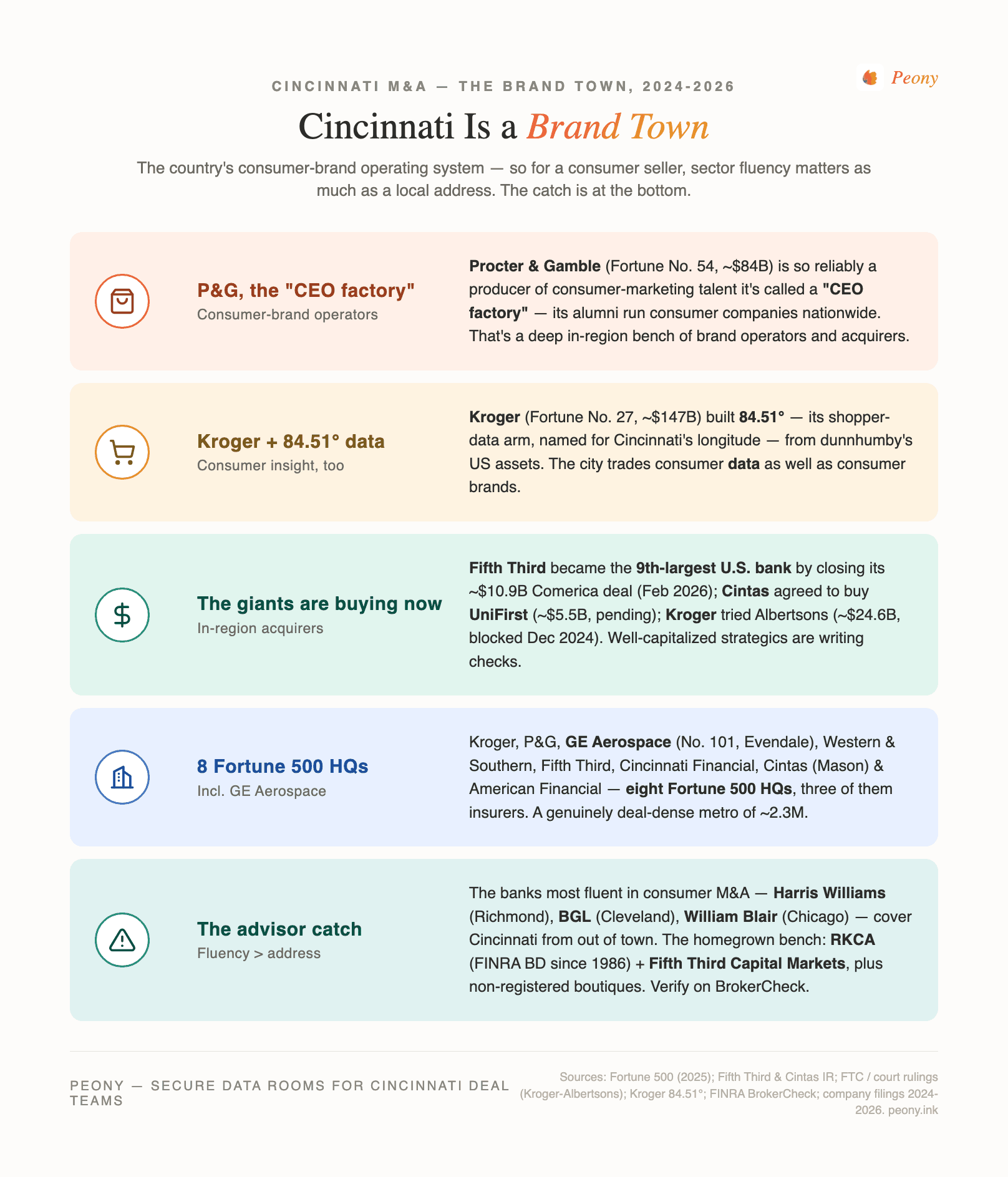

Here is the thesis I want you to internalize before you read another word: Cincinnati is a Brand Town. It is the country's consumer-brand operating system. Procter & Gamble (Fortune 500 No. 54, about $84B in net sales) is so reliably a producer of consumer-marketing talent that it is widely called a "CEO factory," and its alumni run consumer companies across the country. Kroger (No. 27, about $147B) built 84.51°, its shopper-data arm, out of the dunnhumby US data assets — turning Cincinnati into a center of consumer insight as well as consumer brands. Around them sits a dense ecosystem of CPG, food-and-beverage, and personal-care companies, agencies, and operators. No other U.S. metro has quite this concentration of consumer-brand fluency.

That identity changes two things for a seller in a way it would not in Columbus or Cleveland. First, for a consumer, food, or personal-care business, sector fluency matters as much as a local address — and the banks with the deepest rosters of consumer strategic and PE buyers (Harris Williams, Brown Gibbons Lang, William Blair) cover Cincinnati from Richmond, Cleveland, and Chicago, not from a local office. Second, the homegrown giants are net acquirers right now: Fifth Third Bancorp became the ninth-largest U.S. bank in February 2026 by closing its roughly $10.9B acquisition of Comerica, and Cintas agreed in March 2026 to acquire UniFirst for about $5.5B. In-region strategic buyers are unusually real here.

So the homegrown sell-side bench that a $10M-$300M founder actually hires is anchored by two genuine options — RKCA, a Cincinnati FINRA-registered broker-dealer since 1986, and Fifth Third Capital Markets, the investment-banking group inside the city's own bank — plus honest non-registered sell-side boutiques. This post is the working playbook I would hand to a Cincinnati consumer-brand owner weighing a sale, a family-owned manufacturer or aerospace-supplier fielding inbound interest, a food-and-beverage founder, or a business-services owner considering a process. The frames — the Brand Town, the sector-fluency-over-locality rule for consumer deals, the homegrown-giants-as-acquirers signal, the registered-vs-M&A-broker-exemption sorting test, and the Fifth-Third-banking-vs-wealth split — come from cross-referencing the verified 2023-2026 deal record and FINRA BrokerCheck against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in Cincinnati right now for $5M-$300M deals?

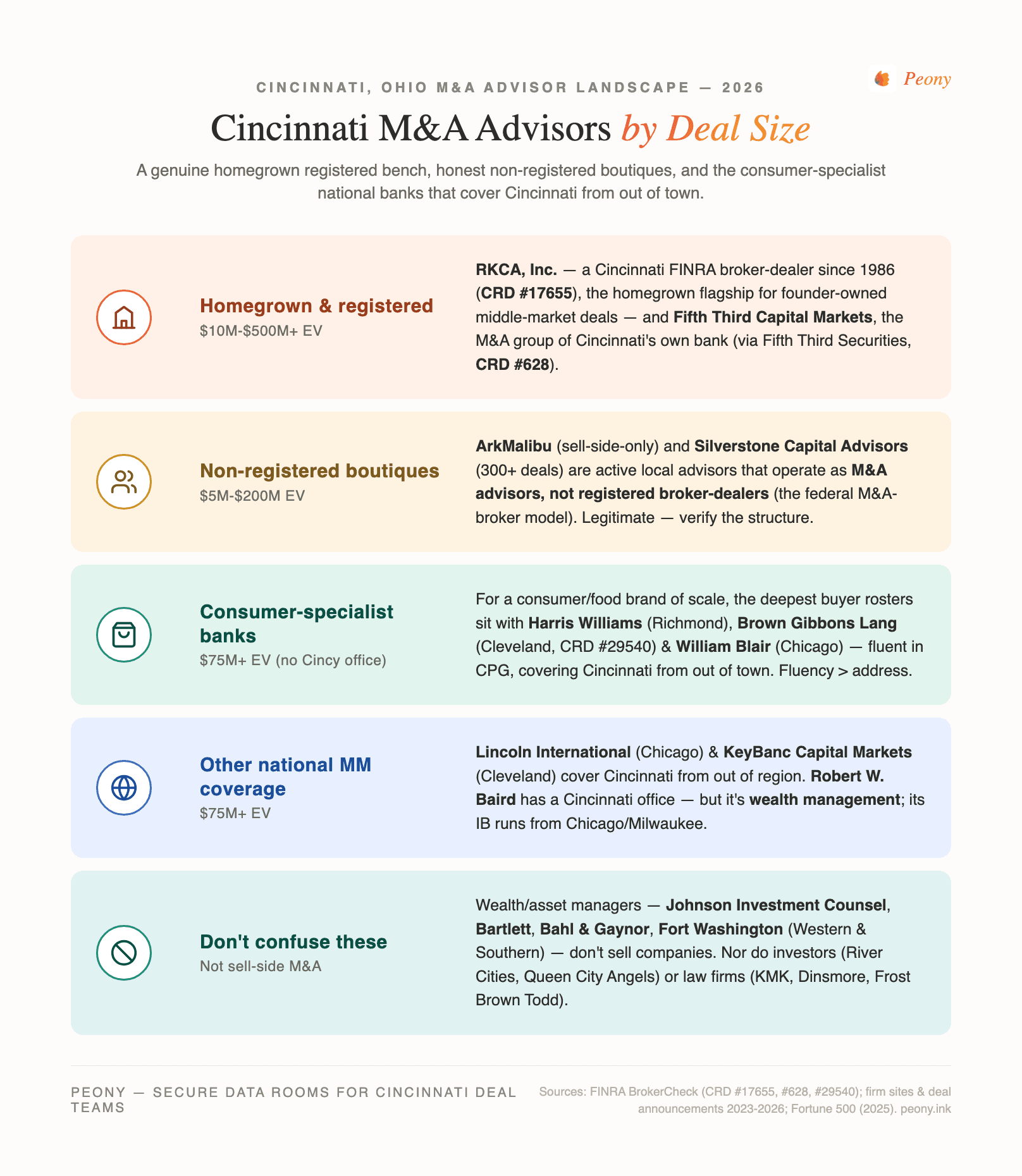

The Greater Cincinnati shortlist for 2026, sorted by tier and deal-size band — with the honesty banner up front: there is no homegrown independent national bank, but there is a genuine homegrown registered boutique (RKCA) and a bank-owned investment bank (Fifth Third Capital Markets); a tier of honest non-registered sell-side advisors; and the national middle-market and consumer-specialist banks that cover Cincinnati from out of town.

| Firm | HQ / Cincinnati presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| RKCA, Inc. ★ (homegrown flagship) | Cincinnati (founded 1986) | $10M-$150M EV | Manufacturing, industrials, tech-enabled, restaurant & consumer | Own FINRA broker-dealer (CRD #17655) |

| Fifth Third Capital Markets | Cincinnati | $25M-$500M+ EV | Middle-market M&A, financial sponsors, consumer & retail, industrials | Transacts through Fifth Third Securities, Inc. (CRD #628) |

| ArkMalibu | Cincinnati | $10M-$200M EV | Sell-side-only national boutique across sectors | M&A advisor (not a registered broker-dealer; M&A-broker model) |

| Silverstone Capital Advisors | Cincinnati | $5M-$100M EV | Lower-middle-market generalist; environmental, healthcare, industrials | M&A advisor (not a registered broker-dealer; M&A-broker model) |

| Harris Williams | Richmond HQ (PNC) — covers Cincinnati, no local office | $100M-$1B+ EV | National consumer & industrials middle-market | Established FINRA broker-dealer |

| Brown Gibbons Lang (BGL) | Cleveland HQ — covers Cincinnati, no local office | $50M-$750M EV | Strong consumer/CPG, industrials, real estate | Own FINRA broker-dealer (CRD #29540) |

| William Blair | Chicago HQ — covers Cincinnati, no local office | $150M-$1B+ EV | National consumer & middle-market for larger processes | Established FINRA broker-dealer |

| Robert W. Baird | Milwaukee HQ — Cincinnati office is wealth only | $75M-$1B+ EV | Employee-owned middle-market; IB run from Chicago/Milwaukee | Established FINRA broker-dealer |

A few notes the table cannot carry. RKCA, Inc. is the homegrown flagship — a Cincinnati FINRA-registered broker-dealer since 1986, with its own broker-dealer registration (CRD #17655) and a steady stream of recent middle-market closings (Johnson Welded Products, a heavy-vehicle component maker, in 2024; Ascent Technologies sold to Edgewater Equity Partners of Boston in January 2024; SimpleVMS, a Cincinnati workforce-management software firm, sold to Avionte in 2024; and the U.S. TGI Fridays operator The Bistro Group sold to Falcons Restaurant Group in 2024). It is the cleanest "genuinely local, genuinely registered" choice for a founder-owned middle-market deal. Fifth Third Capital Markets is the investment-banking and M&A-advisory group inside Cincinnati's own Fifth Third Bancorp — a real middle-market platform with a financial-sponsors group and consumer & retail coverage — though it engages a bit higher up the size curve and is a different thing from the Fifth Third wealth office most owners know (more on that below). It transacts through Fifth Third Securities, Inc. (CRD #628).

Then the tier the honest version of this page has to label clearly: ArkMalibu and Silverstone Capital Advisors are genuinely active Cincinnati sell-side advisors with substantial published deal lists, but they are not FINRA-registered broker-dealers — they operate as M&A advisors, most likely under the federal M&A-broker exemption. That is a legitimate, common model; just verify the status and structure a securities-based sale accordingly. ArkMalibu runs a distinctive sell-side-only practice (its published closings include Cincom and Dominion Electric); Silverstone advertises 300+ lifetime transactions across the lower-middle-market.

And the national banks. Harris Williams (Richmond, owned by PNC) and William Blair (Chicago) are among the deepest consumer and industrials middle-market franchises in the country and routinely win Cincinnati's larger consumer deals — from out of town. Brown Gibbons Lang (Cleveland, CRD #29540) has a strong consumer/CPG practice and covers Cincinnati from Cleveland and Chicago. KeyBanc Capital Markets (Cleveland) and Lincoln International (Chicago) cover the region similarly. Robert W. Baird has a Cincinnati office, but it is a wealth-management branch — Baird's investment banking is run from Chicago and Milwaukee, so do not read its Cincinnati sign as local M&A coverage.

And the critical honesty point on the firms a Cincinnati owner is most likely to already know: Johnson Investment Counsel, Bartlett & Co., Bahl & Gaynor, Foster & Motley, and Fort Washington Investment Advisors are wealth and asset managers, not sell-side M&A advisors; the local private-capital names (River Cities Capital, Roebling Capital Partners, Northcreek Mezzanine, Queen City Angels) are investors, not advisors; and Keating Muething & Klekamp, Dinsmore, and Frost Brown Todd are law firms. More on that sorting test below.

Does Cincinnati have a homegrown investment bank, or do I import one?

The honest answer sits between the two metros people compare Cincinnati to. Unlike St. Louis, Cincinnati has no homegrown independent national investment bank of the Stifel caliber. But unlike Columbus — which has no homegrown registered bank at all and whose best boutiques transact through third-party broker-dealers — Cincinnati has two genuine homegrown options with their own footing.

RKCA, Inc. is a Cincinnati investment bank that has held its own FINRA broker-dealer registration since 1986 (CRD #17655). It is not large, but it is real, local, and registered, and it runs middle-market sell-sides with a current, named deal record. For a founder-owned $10M-$150M business, it is the cleanest "genuinely homegrown and genuinely registered" choice on this page.

Fifth Third Capital Markets is the other homegrown option, and a more institutional one. Cincinnati's Fifth Third Bancorp (Fortune 500 No. 341, and after closing Comerica in February 2026 the ninth-largest U.S. bank) runs a genuine middle-market investment bank — M&A advisory, capital raising, a financial-sponsors group, and industry coverage including consumer & retail — under the Fifth Third Capital Markets name, transacting through Fifth Third Securities (CRD #628). It engages a bit higher up the size curve than a small boutique, and you have to be sure you are talking to its investment bankers rather than its far larger wealth and retail business, but it is a real, local, scaled platform.

Below those, ArkMalibu and Silverstone Capital Advisors are active local sell-side boutiques operating as non-registered M&A advisors. And for a larger or category-specialist process you import a national bank — Harris Williams from Richmond, BGL and KeyBanc from Cleveland, William Blair and Lincoln from Chicago — none of which keeps a deal-executing M&A office in Cincinnati. The practical rule: for a founder-owned deal up to roughly $100M-$150M, RKCA, Fifth Third Capital Markets, or a verified local boutique will usually give you strong senior attention; above that, or for a consumer brand where sector-specialist buyer relationships decide the price, a national bank earns its fee.

What makes Cincinnati a "Brand Town," and does it mean more buyers for my company?

The signature frame for Cincinnati is the Brand Town: it is the country's consumer-brand operating system, and that genuinely shapes the buyer pool for the right kind of seller. Here is the accurate version of each piece.

- Procter & Gamble (Fortune 500 No. 54, about $84B net sales, roughly 107,000 employees) is headquartered downtown and is so consistent a producer of consumer-marketing leadership that it is widely described as a "CEO factory" — its alumni run consumer companies nationwide. That is a real, citable reputation; what it means for you is a deep local bench of consumer-brand operators, advisors, and would-be acquirers.

- Kroger (No. 27, about $147B) is the other anchor, and it made Cincinnati a center of consumer data as well as consumer brands: its 84.51° subsidiary (named for Cincinnati's longitude) was built from the U.S. shopper-data assets of dunnhumby in 2015. A consumer business selling into grocery has unusually sophisticated, in-region counterparties here.

- A dense CPG ecosystem. Around P&G and Kroger sit food-and-beverage, personal-care, and consumer-products companies, plus the agencies and data firms that serve them. For a consumer or food seller, that ecosystem is a genuine source of strategic buyers and sector-fluent advisors.

- Eight Fortune 500 headquarters. Beyond P&G and Kroger: GE Aerospace (No. 101, headquartered in Evendale in the Cincinnati metro, independent since April 2024), Western & Southern (No. 321), Fifth Third Bancorp (No. 341), Cincinnati Financial (No. 348), Cintas (No. 412, in Mason), and American Financial Group (No. 478). Three of those eight are insurers, making Cincinnati a real insurance center as well.

For a seller, the net is genuinely positive — but scope it honestly. The Brand Town identity helps most if you are a consumer, food, or personal-care business, because that is where the in-region fluency and buyer density are deepest. The catch, covered next, is that the banks most fluent in consumer M&A cover Cincinnati from out of town. For an industrials, aerospace-supply, healthcare, or services seller, the consumer-brand halo matters less, and the question reverts to the usual one: which advisor can name your actual best buyers.

Why does sector fluency matter more than a local address for a Cincinnati consumer or food sale?

Because the buyers who pay the most for a consumer brand are reached through sector relationships, not geography — and Cincinnati's paradox is that the city is famous for consumer brands while the banks most fluent in selling them sit elsewhere. Harris Williams (Richmond), William Blair (Chicago), and Brown Gibbons Lang (Cleveland) have among the deepest consumer and CPG practices in the country, with rosters of strategic acquirers and consumer-focused private-equity firms that a generalist local boutique simply cannot match — and all three cover Cincinnati from out of town. So for a consumer or food brand of real scale (roughly $75M+), the right call is often a national consumer-specialist bank, even though it has no Cincinnati office, because it reaches your best buyers.

That does not mean "always go national." Below that scale, a homegrown firm (RKCA or Fifth Third Capital Markets) can run a strong, senior-attention process — provided it can name the specific consumer strategics and CPG sponsors active in your sub-category. That is the exact screening question to ask any advisor pitching your consumer deal: name the last three buyers you placed a business like mine with. A firm that can is fluent; a firm that cannot is the wrong fit regardless of its address. The principle generalizes: in a Brand Town, weight what an advisor knows about your category at least as heavily as where its office is.

Are Cincinnati's big companies buyers right now — and does that help me sell?

Yes — and this is one of the strongest current signals for a Cincinnati seller. The metro's homegrown giants are unusually active acquirers in 2025-2026:

- Fifth Third Bancorp closed its roughly $10.9B all-stock acquisition of Comerica in February 2026, becoming the ninth-largest U.S. bank (about $288-294B in assets).

- Cintas (Mason, OH) agreed in March 2026 to acquire UniFirst for about $5.5B — a deal that, as of mid-2026, is pending and expected to close in the second half of the year.

- Kroger attempted the roughly $24.6B acquisition of Albertsons before it was blocked by a federal court and the FTC in December 2024 (Albertsons then terminated the agreement and sued Kroger for the $600M reverse-termination fee plus damages) — a reminder that the appetite is there even when a specific deal does not clear.

The honest caveat is that these are bulge-bracket mandates — Kroger was advised by Citi and Wells Fargo, not a local boutique — so a giant buying a giant does not directly change who advises your $25M sale. But it does mean well-capitalized strategics headquartered in your own metro are actively writing checks, and a Cincinnati-fluent advisor can point to in-region acquirers and supply-chain consolidators across consumer, industrials, and services. For a seller, in-region strategic interest is a real, current tailwind.

What does it mean that ArkMalibu and Silverstone aren't registered broker-dealers — is that a red flag?

It is not a red flag — it is a legitimate model — but it is worth understanding so you verify the right thing. Both ArkMalibu and Silverstone Capital Advisors are active Cincinnati sell-side M&A advisors with substantial published deal lists, and neither appears as a registered broker-dealer firm on FINRA BrokerCheck. They most likely operate under the federal M&A Broker exemption, added to the securities laws in 2023, which lets a qualifying advisor facilitate the sale of a privately held company without registering as a broker-dealer, subject to size and structure limits.

What this means for you, practically:

- A BrokerCheck search of the advisory name may return zero firm records — that is expected here, not alarming. Verify the individual bankers and ask the firm directly how it is structured.

- For a stock sale that requires a registered broker-dealer in the chain, confirm how the firm handles the securities piece (some non-registered M&A advisors partner with a registered broker-dealer for exactly that).

- The engagement letter should be explicit about the firm's status and your deal's structure.

None of this speaks to deal quality. By contrast, RKCA holds its own broker-dealer registration (CRD #17655), and Fifth Third Capital Markets transacts through Fifth Third Securities (CRD #628). The point is not that registered is better than exempt — both are legitimate — but that you should know which model you are hiring and structure the deal accordingly.

Is Fifth Third Capital Markets the same as the Fifth Third wealth office?

No — and this is the most common Cincinnati mix-up, worth its own section. Fifth Third Bancorp is the city's flagship bank, and most owners know it through its retail branches and its wealth advisors. But Fifth Third also runs a genuine middle-market investment bank under the name Fifth Third Capital Markets (also called Fifth Third Corporate & Investment Banking): M&A advisory, capital raising, a financial-sponsors group covering middle-market private-equity firms, and industry coverage including consumer & retail.

The entity detail: that M&A advisory transacts under the bank and its broker-dealer subsidiary, Fifth Third Securities, Inc. (FINRA CRD #628). The trap is that CRD #628 is overwhelmingly a wealth and retail-brokerage business — the "Fifth Third" person most owners know is a private-client wealth advisor, not an investment banker. They are different groups under one brand. So when you engage Fifth Third to sell your company, you specifically want the Capital Markets / Investment Banking team, and you should ask for its recent middle-market closings in your sector. Used correctly, it is one of the strongest homegrown options on this page; confused with the wealth office, it is a dead end.

Which national middle-market banks cover Cincinnati deals — and do any keep a Cincinnati office?

The national middle-market and consumer-specialist banks that win Cincinnati's larger deals are real options, but the honest answer on local presence is that none keeps a deal-executing M&A office in Cincinnati that I could confirm. They cover the region from Richmond, Cleveland, and Chicago.

- Harris Williams (Richmond HQ, owned by PNC) is one of the deepest middle-market franchises in consumer and industrials, and a frequent choice for Cincinnati's larger consumer and manufacturing deals — covered from Richmond and other hubs.

- Brown Gibbons Lang (Cleveland HQ, CRD #29540) has a strong consumer/CPG and industrials practice and covers Cincinnati from Cleveland and Chicago.

- William Blair (Chicago) is the employee-owned middle-market bank with deep consumer and sector practices — the natural national choice for a clean $150M+ Cincinnati consumer or industrials sell-side, covered from Chicago. (William Blair provided the board fairness opinion on Cincinnati label-maker Multi-Color's 2019 sale, an example of its regional reach.)

- Lincoln International (Chicago) and KeyBanc Capital Markets (Cleveland) both cover Cincinnati from out-of-region hubs.

- Robert W. Baird has a Cincinnati office, but it is a wealth-management branch; Baird's investment-banking M&A is run from Chicago and Milwaukee.

The takeaway: for a larger or category-specialist process, the national banks are credible and often the right answer — especially for a consumer brand — but you are hiring an out-of-town team that will fly in, so weigh them on sector fit and buyer reach, not on a local address. For most founder-owned $5M-$100M deals, a genuinely-homegrown Cincinnati firm gives you more senior attention; the national banks earn their fee as the deal scales or specializes.

Don't mistake a wealth manager, RIA, or insurance asset manager for a deal advisor

This is the most important sorting test in Cincinnati, because the metro is a genuine financial-services center thick with firms that manage money — and almost none of them sells operating companies.

- Johnson Investment Counsel is a large Cincinnati wealth-management RIA and family office. Excellent for your personal and family wealth around a liquidity event; not a firm that markets and sells your company.

- Bartlett & Co. Wealth Management (roots to 1898, roughly $10B AUM), Bahl & Gaynor (an employee-owned RIA), and Foster & Motley are wealth-management RIAs — money management, not sell-side M&A.

- Fort Washington Investment Advisors is the institutional asset-management arm of Western & Southern Financial Group, with roughly $95B AUM; its FW Capital arm is a private-markets investor. Neither is a firm you hire to sell your company.

- Cincinnati's private-capital names — River Cities Capital, Roebling Capital Partners, Northcreek Mezzanine, Queen City Angels — are investors, not advisors. They might buy your company, not sell it for you. (And beware the "Queen City" name collisions: Queen City Capital Management is a wealth RIA, Queen City Angels is a venture investor, and the Queen City Group is a Morgan Stanley wealth team — none is an M&A advisor.)

- The big local law firms — Keating Muething & Klekamp, Dinsmore, Frost Brown Todd — are your legal counsel, not your banker.

The line that separates the two worlds is simple: a wealth manager or asset manager grows and protects capital; an investment bank or registered M&A advisor runs a competitive process to sell a company. Verify on FINRA BrokerCheck which kind of firm you are hiring, and structure a securities-based stock sale through a registered broker-dealer (or a firm whose model and partners cover the securities piece).

Who advises a Cincinnati consumer, food & beverage, or personal-care sale?

This is the Cincinnati sweet spot, and the one place the Brand Town identity should actively shape your shortlist. For a consumer, food & beverage, or personal-care company, weight sector fluency heavily. For a brand of real scale (roughly $75M+), the national consumer-specialist banks — Harris Williams, William Blair, Brown Gibbons Lang — usually reach the deepest pool of strategic and PE consumer buyers, even though they cover Cincinnati from out of town. Below that scale, a homegrown firm (RKCA or Fifth Third Capital Markets, the latter with explicit consumer & retail coverage) can run a strong process if it can name the specific consumer strategics and CPG sponsors active in your sub-category. The screening question is always the same: ask the advisor to name the last three buyers it placed a business like yours with. Cincinnati's consumer ecosystem — P&G's operator bench, Kroger's 84.51° data orbit, the CPG sponsors that cluster here — means in-region buyers are unusually real, but only a sector-fluent advisor can actually reach them.

Who advises a Cincinnati industrial, manufacturing, or aerospace-supply-chain sale?

Cincinnati's industrial base is deep — advanced manufacturing, machining, and the aerospace supply chain feeding GE Aerospace in Evendale — and it is where the homegrown registered bench is strongest. For a founder-owned manufacturer, fabricator, or aerospace-supplier in the roughly $10M-$150M band, RKCA is the natural first call (its recent closings include heavy-vehicle and industrial businesses), with Fifth Third Capital Markets a credible homegrown alternative and ArkMalibu or Silverstone as active non-registered options. As the deal scales past roughly $150M, Harris Williams, BGL, William Blair, or KeyBanc bring deeper institutional buyer pools — at the cost of a fly-in team. The aerospace supply chain is a particular Cincinnati strength: confirm that any advisor you consider can name the specific tier-one and PE consolidators active in your niche.

Who advises a Cincinnati healthcare, med-device, or business-services sale?

Greater Cincinnati has a real healthcare and med-device base (anchored by names like Mason-based AtriCure) and a deep bench of business- and professional-services and logistics companies (the Total Quality Logistics orbit). For these sellers in the $5M-$100M band, the homegrown firms again lead on senior attention: RKCA, Fifth Third Capital Markets, and the non-registered boutiques ArkMalibu and Silverstone all work business services and healthcare-adjacent deals, and Silverstone's published list includes healthcare-services transactions. For a larger or more specialized healthcare process, a national healthcare-focused bank reaches a deeper buyer pool. The screening question does not change: ask for the last three deals the advisor closed in your specific sub-sector and the buyers on the other side.

How do I tell a real FINRA investment bank apart from a business broker in Cincinnati?

Cincinnati has three different kinds of firm that all describe themselves as "M&A advisors," and telling them apart shapes how a securities-based sale should be structured.

- Registered broker-dealers. RKCA holds its own registration (CRD #17655). Fifth Third Capital Markets transacts through Fifth Third Securities (CRD #628). The national banks (Harris Williams, BGL CRD #29540, William Blair, KeyBanc, Baird) are registered too.

- Non-registered M&A advisors (M&A-broker model). ArkMalibu and Silverstone are active local examples — a legitimate, common model, especially for founder-owned sales, where the firm facilitates the deal without holding its own broker-dealer license. Verify the model and how the firm handles any securities piece.

- Wealth managers, asset managers, investors, and law firms — the trap category covered above. None sells your company.

Start with FINRA BrokerCheck. The clean test for any firm: ask for its broker-dealer CRD (or an explicit statement that it operates as a non-registered M&A advisor), three named recent closings with the buyers identified, and which senior person will run your deal. If a firm cannot give you a clear answer on its registration model, that itself is information.

Who handles sub-$5M Main-Street business sales in Cincinnati?

Below roughly $5M of enterprise value, you are usually in business-brokerage territory rather than investment banking, and that is fine — it is a different, legitimate market. National and regional business-broker networks (Sunbelt, Transworld, and independent Cincinnati main-street brokers) handle restaurants, small retail, trades businesses, and owner-operator companies. The economics and process differ from a true sell-side auction: more listing-driven, lower absolute fees, a buyer pool weighted toward individuals and searchers. If your company is genuinely lower-middle-market — say $5M+ of enterprise value with real EBITDA — you have outgrown the main-street model and should be talking to the firms above, where a competitive process across strategic and PE buyers will more than pay for the advisor. The crossover zone (roughly $3M-$8M) is worth a second opinion; the right answer depends on your buyer universe, not just your revenue.

Is now a good time to sell my Cincinnati business?

The honest answer is that timing the macro matters less than your own readiness, but Cincinnati has genuine tailwinds in 2026. In-region strategic buyers are unusually active (Fifth Third and Cintas both writing large checks), the consumer and food ecosystem keeps sponsors and strategics hunting Cincinnati brands, and the industrials and aerospace-supply base is busy. Those are real positives for a prepared seller. The counterweights are the same every seller faces: financing costs, your sub-sector's specific dynamics, and — most of all — whether your financials are clean enough to survive diligence. The single biggest determinant of outcome is not the month you launch; it is whether you walk in with a defensible quality-of-earnings picture, a clean data room, and an advisor who can name your actual best buyers. Get those three in place and Cincinnati's buyer pool is as deep as it has been in years.

What's a reasonable success fee for a $25M Cincinnati sell-side?

For a $25M Cincinnati company, a blended success fee around 3-3.5% is squarely normal, typically a modest monthly retainer plus a success fee at close on a Double Lehman scale (10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% above $5M — about $700K, or roughly 2.8%, on $25M, landing near 3-3.5% once minimums and uncredited retainer are added). Retainers run roughly $5,000-$25,000 per month at a boutique and are often credited against the success fee — but only if the engagement letter says so in writing. Watch three things more than the headline percentage: the base the fee applies to (total enterprise value including assumed debt and earnouts, or just cash at close), the tail period (banks ask for 18-24 months; negotiate toward 12), and any minimum-fee floor. The fee delta between two good advisors is almost always dwarfed by the price delta a competitive auction produces — so optimize for the advisor who can reach your best buyers, not the one who shaves 25 basis points. I walk through the full fee math in the FAQ below.

Which virtual data room should a Cincinnati seller actually use?

I run a data room company, so treat this as informed but interested — and I will be honest about where each tool fits. For a true $500M+ mega-deal with hundreds of bidders, Datasite and Intralinks are the incumbents, and your banker may simply require one. For the sub-$300M enterprise-value band that is the bulk of Greater Cincinnati deal flow — which is to say almost every deal in this article — you do not need an enterprise mega-platform, and you should not pay for one. Peony, iDeals, and FirmRoom all run clean, secure, modern sell-side processes at a fraction of the cost. What actually matters for a Cincinnati lower-middle-market sale: per-buyer permissions so strategics and sponsors see different tiers, dynamic watermarking and screenshot protection so a leaked teaser is traceable, page-level analytics so you can see which buyers are genuinely engaged, and pricing that does not punish you per page or per gigabyte. We serve more than 6,800 customers, many running exactly the kind of founder-owned and family-business sales this article is about. Whatever you choose, set the room up before you go to market — it is the cheapest lever you control.

Bottom line

Cincinnati is a Brand Town — the country's consumer-brand operating system, anchored by P&G's operator academy, Kroger and its 84.51° data arm, and eight Fortune 500 headquarters whose giants are net acquirers right now (Fifth Third just became the ninth-largest U.S. bank by buying Comerica; Cintas is acquiring UniFirst). That identity changes how you should hire. For a consumer, food, or personal-care business, weight sector fluency as heavily as a local address — the most fluent consumer banks (Harris Williams, William Blair, Brown Gibbons Lang) cover Cincinnati from out of town. For the broader middle market, the genuine homegrown bench is real and, unlike Columbus, includes a registered local broker-dealer: RKCA (a Cincinnati FINRA broker-dealer since 1986) and Fifth Third Capital Markets, plus honest non-registered sell-side boutiques in ArkMalibu and Silverstone. Do not mistake the metro's wealth and asset managers — Johnson Investment Counsel, Bartlett, Bahl & Gaynor, Fort Washington — for deal advisors, and make sure that when you call Fifth Third you reach its Capital Markets bankers, not its wealth office. Verify every firm's status on FINRA BrokerCheck, ask for three named recent closings with buyers identified, and build a clean data room before you go to market. In a Brand Town, the advisor who knows your category is worth more than the one down the street.

Frequently asked questions about Cincinnati M&A advisors

Should I hire a local Cincinnati M&A boutique or a national investment bank to sell my company?

Hire a homegrown Cincinnati firm when your deal is in the ~$5M-$100M band and your best buyers are reachable strategics and middle-market sponsors; reach for a national middle-market or consumer-specialist bank once the deal climbs toward $150M-$250M+ or your category is one where sector-specialist buyer relationships decide the price. The Cincinnati nuance is that for a consumer, food, or personal-care business the most fluent buyers often sit with national CPG-specialist banks (Harris Williams, BGL, William Blair) that cover Cincinnati from out of town — sector fluency can matter as much as a local address. For industrials and the broader middle market, the homegrown bench is strong: RKCA (CRD #17655) and Fifth Third Capital Markets, plus non-registered boutiques ArkMalibu and Silverstone. A clean, staged data room with page-level analytics is the cheapest lever you control either way.

Does Cincinnati have a homegrown investment bank, or do I have to bring in a Chicago, Cleveland, or Richmond bank?

Cincinnati has no homegrown independent national investment bank of the Stifel caliber, but it has two genuine homegrown options: RKCA, a Cincinnati FINRA-registered broker-dealer since 1986 (CRD #17655), and Fifth Third Capital Markets, the investment-banking group inside Cincinnati's own Fifth Third Bancorp (transacting through Fifth Third Securities, CRD #628). Below those, ArkMalibu and Silverstone are active non-registered sell-side boutiques. For a larger or category-specialist process you import a national bank — Harris Williams from Richmond, BGL and KeyBanc from Cleveland, William Blair and Lincoln from Chicago — none of which keeps a Cincinnati deal office.

Who sells a Cincinnati consumer-products or food & beverage company — a local boutique or a CPG-specialist bank?

Weight sector fluency as heavily as locality. Cincinnati is the country's consumer-brand operating system (P&G, Kroger, 84.51°), but the banks with the deepest consumer buyer rosters — Harris Williams, Brown Gibbons Lang, William Blair — cover Cincinnati from Richmond, Cleveland, and Chicago. So for a consumer brand of real scale ($75M+), a national consumer-specialist bank often reaches your best buyers better than a generalist local boutique. Below that, a homegrown firm (RKCA or Fifth Third Capital Markets) can run a strong process if it can name the specific consumer strategics and sponsors active in your sub-category — which is exactly the screening question to ask.

I own a ~$25M Cincinnati company — who are the best M&A advisors for a lower-middle-market sale?

The genuinely-homegrown shortlist: RKCA, Inc. (Cincinnati, a FINRA broker-dealer since 1986, CRD #17655 — the homegrown flagship), Fifth Third Capital Markets (the M&A group of Cincinnati's Fifth Third Bancorp, fishing a bit higher up the size curve), and the active non-registered sell-side boutiques ArkMalibu and Silverstone Capital Advisors. RKCA holds its own broker-dealer registration; ArkMalibu and Silverstone operate as M&A advisors — verify and structure accordingly. Ask each for the last three deals it closed in your sub-sector and the buyers; RKCA can point to named, dated 2024 closings (Johnson Welded Products; Ascent Technologies to Edgewater Equity Partners; SimpleVMS to Avionte).

What does it mean that ArkMalibu and Silverstone aren't registered broker-dealers — is that a red flag?

No — it is a legitimate, common model. Both are active Cincinnati sell-side advisors that do not appear as registered broker-dealer firms on BrokerCheck; they most likely operate under the federal M&A Broker exemption (2023), which lets a qualifying advisor sell a privately held company without registering as a broker-dealer, subject to limits. Implications: a BrokerCheck search of the advisory name may return zero firm records (expected, not alarming); for a stock sale needing a registered broker-dealer in the chain, confirm how the firm handles the securities piece; and the engagement letter should state the firm's status. By contrast, RKCA holds its own registration (CRD #17655) and Fifth Third Capital Markets transacts through Fifth Third Securities (CRD #628). Know which model you are hiring.

Is Fifth Third Capital Markets the same as the Fifth Third wealth or brokerage office?

No. Fifth Third runs a genuine middle-market investment bank — Fifth Third Capital Markets (Corporate & Investment Banking): M&A advisory, capital raising, a financial-sponsors group, and consumer & retail coverage — transacting through Fifth Third Securities, Inc. (CRD #628). The trap is that CRD #628 is overwhelmingly a wealth and retail-brokerage business, so the "Fifth Third" person most owners know is a private-client wealth advisor, not an investment banker. When you engage Fifth Third to sell your company, ask specifically for the Capital Markets / Investment Banking team and its recent middle-market closings in your sector.

Are Cincinnati's big companies actually buyers right now, and does that help me sell?

Yes. Fifth Third Bancorp closed its $10.9B acquisition of Comerica in February 2026, becoming the ninth-largest U.S. bank ($288-294B assets); Cintas agreed in March 2026 to acquire UniFirst for ~$5.5B (pending, H2 2026); and Kroger attempted the ~$24.6B Albertsons deal before it was blocked in December 2024. The caveat: these are bulge-bracket mandates (Kroger was advised by Citi and Wells Fargo), so a giant buying a giant does not change who advises your $25M sale — but it shows well-capitalized strategics in your own metro are writing checks, and a Cincinnati-fluent advisor can point to active in-region acquirers across consumer, industrials, and services.

How do I tell a real Cincinnati investment bank apart from a wealth manager, RIA, or insurance asset manager?

Start with FINRA BrokerCheck. A securities-based stock sale should run through a registered broker-dealer: RKCA is CRD #17655 and Fifth Third Securities is CRD #628; ArkMalibu and Silverstone operate as non-registered M&A advisors. The trap category is the wealth and asset-management names an owner knows — Johnson Investment Counsel, Bartlett & Co., Bahl & Gaynor, Foster & Motley (wealth RIAs), and Fort Washington (Western & Southern's asset manager) — none of which runs a sell-side auction. The local private-capital names (River Cities Capital, Roebling, Northcreek Mezzanine, Queen City Angels) are investors, and KMK/Dinsmore/Frost Brown Todd are law firms. Ask any firm for its broker-dealer CRD (or non-registered statement), three named recent closings with buyers, and which senior person runs your deal.

How does a sell-side M&A process work for a Cincinnati company, and how long does it take from advisor hire to close?

A Cincinnati sell-side runs in five overlapping stages and typically takes 6-9 months from engagement letter to close: 4-8 weeks of preparation (clean financials, quality-of-earnings, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA from a blind teaser; 3-5 weeks to collect indications of interest; 4-6 weeks of management meetings and the LOI stage; then 8-12 weeks of confirmatory diligence and definitive-agreement negotiation. The advisor's job throughout is to manufacture competitive tension across strategic and PE buyers. Cincinnati's buyer pool is unusually deep on the consumer and food side and increasingly active on industrials and services. The biggest timeline risk is unprepared financials — a clean, staged data room built before launch is the most reliable way to compress the back half.

What do buyers diligence, and how do I set up a data room before going to market with my Cincinnati company?

Buyers diligence the things that prove durable, transferable cash flow — normalized EBITDA and its quality, revenue and customer concentration, gross-margin trend, working capital, contract assignability, and (for consumer sellers) brand, channel, and customer data; (for manufacturers and aerospace suppliers) equipment, capacity, certifications, and labor. Build the data room around the eight workstreams those feed: financial, corporate/legal, commercial, operations/technical, HR, IP and IT, tax, and insurance/compliance. The two documents that do the most work up front are a defensible quality-of-earnings file and the CIM. The discipline that protects you is staged disclosure: a blind teaser first, the named CIM only after an NDA, and sensitive material (customer names, pricing, formulations, rosters) held back for a short list. A room with per-buyer permissions, page-level analytics, and dynamic watermarking makes that enforceable — stage strategics and sponsors as separate visitor groups.

What does an M&A advisor cost to sell a $25M Cincinnati company — is a 3 to 3.5% success fee normal, and how does Double Lehman plus a retainer work?

For a $25M Cincinnati company, expect a monthly retainer plus a success fee at close, with a 3-3.5% blended rate squarely normal. The common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% above $5M — which on $25M is about $700K (roughly 2.8%); add uncredited retainer and any minimum-fee floor and the effective rate lands near 3-3.5%. Retainers run roughly $5,000-$25,000 per month at a boutique and are frequently credited against the success fee — but only if the engagement letter says so. Watch the base the fee applies to (enterprise value including assumed debt and earnouts vs cash at close), the tail period (cap it at 12 months vs the 18-24 banks ask for), and the minimum floor. The fee delta between two good advisors is almost always dwarfed by the price delta a competitive auction produces. On the data-room line item, flat per-admin pricing keeps the cost predictable against a six-figure advisory fee.

Related resources

- The State of M&A Data Rooms — our 283-deal platform benchmark on how sell-side processes actually run.

- How to Build an M&A Data Room — the staged-disclosure playbook every Cincinnati seller should run before going to market.

- How to Write a CIM — the confidential information memorandum your advisor builds after the teaser.

- Best Industrial M&A Advisors — the national sector view for Cincinnati's manufacturing and aerospace-supply sellers.

- Best Insurance M&A Advisors — the national agency-and-brokerage bench for a metro that lives with insurance (Great American and Western & Southern are headquartered downtown): the consolidator teaser decode, real 2026 multiples, and the carrier-consent mechanics.

- Best M&A Advisors in Columbus — the central-Ohio metro with the inverse setup: capital migrating in, but no homegrown registered bank.

- Best M&A Advisors in Cleveland — home to KeyBanc and Brown Gibbons Lang, the Cleveland banks that cover Cincinnati deals.

- Best M&A Advisors in Chicago — where William Blair and Lincoln International (and much of the consumer-bank coverage of Cincinnati) are headquartered.

- Best M&A Advisors in Kansas City — the Ownership Town two states west: roughly $60B of revenue in family, ESOP, and co-op hands that never sells, one Fortune 500 HQ, and a flagship advisor that just changed its name (Turnstone, fka CC Capital Advisors).

- Best M&A Advisors in Baltimore — the First Bank Town: the famous financial brands (T. Rowe Price, Brown Advisory, Alex. Brown) all manage money rather than sell companies — the same brand-vs-function test the Brand Town teaches, applied to the advisors themselves.

- Best M&A Advisors in Milwaukee — the Upper-Midwest maker economy that kept a national-caliber homegrown bank (employee-owned Robert W. Baird) even after selling M&I to BMO.

Footnotes and sources

- FINRA BrokerCheck (brokercheck.finra.org) — verified entity registrations and CRD numbers: RKCA, Inc. (CRD #17655), Fifth Third Securities, Inc. (CRD #628), Brown, Gibbons, Lang & Company Securities, LLC (CRD #29540). ArkMalibu and Silverstone Capital Advisors return no broker-dealer firm records (consistent with operating as non-registered M&A advisors under the federal M&A-broker exemption).

- RKCA, Inc. — firm site and published transaction list (Johnson Welded Products; Ascent Technologies to Edgewater Equity Partners; SimpleVMS to Avionte; The Bistro Group to Falcons Restaurant Group, all 2024).

- Fifth Third — Capital Markets / Corporate & Investment Banking and M&A advisory pages; Comerica acquisition press release (announced October 6, 2025) and completion release (closed February 2, 2026; ninth-largest U.S. bank).

- Cintas — UniFirst acquisition announcement (~$5.5B, March 11, 2026; pending).

- Kroger / Albertsons — FTC and court rulings blocking the ~$24.6B merger (December 10, 2024); Albertsons termination and Delaware Court of Chancery suit seeking the $600M reverse-termination fee.

- GE Aerospace — independent company since April 2, 2024, headquartered in Evendale (Cincinnati metro).

- Fortune 500 (2025) — Cincinnati-metro headquarters ranks: Kroger (No. 27), Procter & Gamble (No. 54), GE Aerospace (No. 101), Western & Southern (No. 321), Fifth Third Bancorp (No. 341), Cincinnati Financial (No. 348), Cintas (No. 412), American Financial Group (No. 478).

- Kroger 84.51° — built from dunnhumby's US shopper-data assets (2015). U.S. Census — Cincinnati OH-KY-IN metro population (~2.3 million).

This article reflects my views as of June 2026 and is informational, not legal, tax, or investment advice. Firm registrations and ownership change — verify current status on FINRA BrokerCheck before engaging any advisor. I am the co-founder of Peony, a data room company; where I mention Peony I have flagged the interest.