10 Best M&A Advisors in Cleveland for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

10 Best M&A Advisors in Cleveland for $5M-$300M Deals (2026)

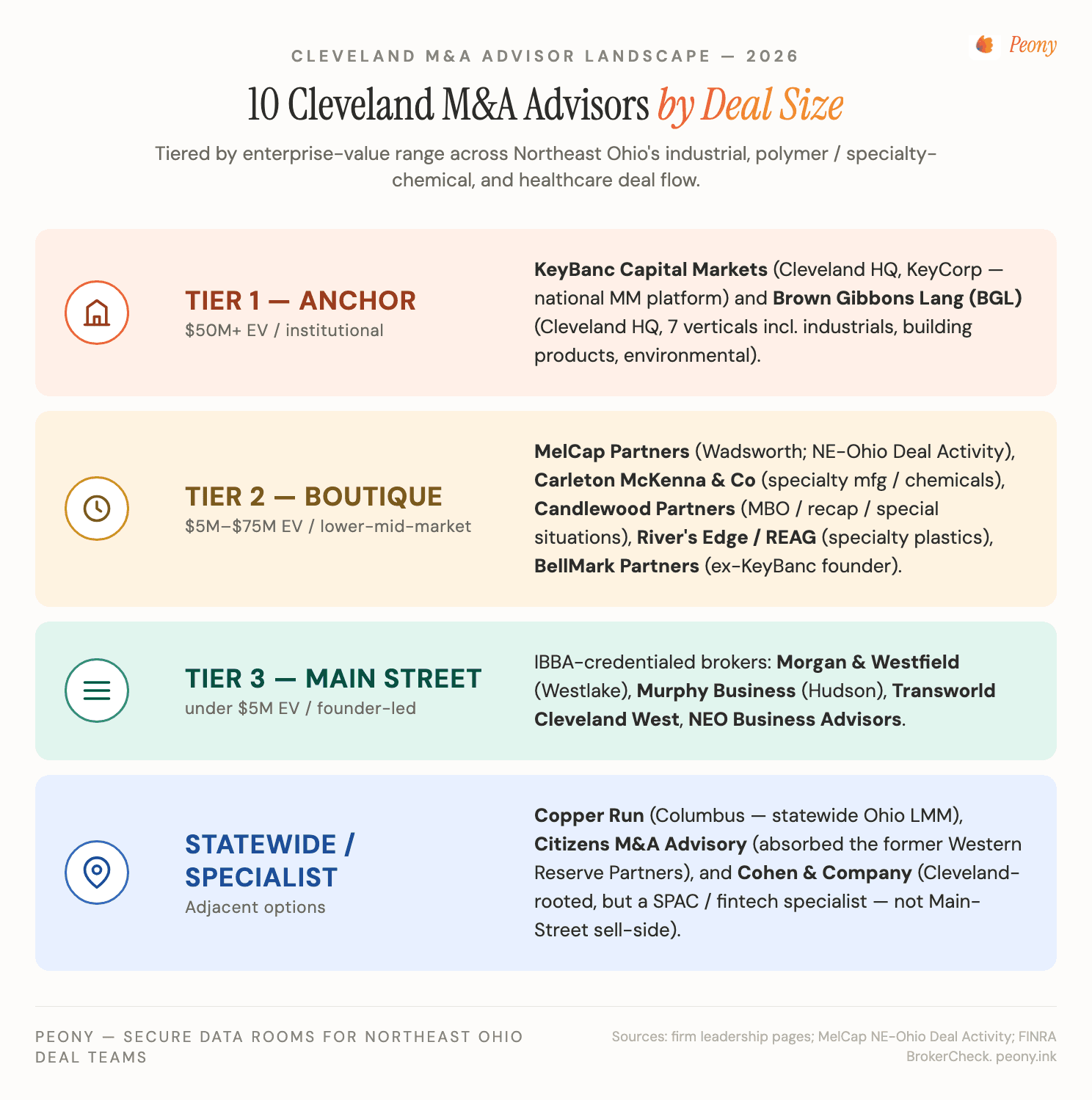

Quick answer: After running and watching enough Northeast Ohio sell-side and buy-side processes, here is the 10-firm Cleveland shortlist for 2026. Two Cleveland-headquartered middle-market investment banks lead it — KeyBanc Capital Markets and Brown Gibbons Lang (BGL) — backed by a deep boutique bench: MelCap Partners, Carleton McKenna & Co, Candlewood Partners, River's Edge Alliance Group, and BellMark Partners, plus Citizens M&A Advisory (which absorbed the former Western Reserve Partners), statewide Copper Run, and the SPAC/fintech specialist Cohen & Company. What makes Cleveland different from the other 21 cities in this series is the buyer pool: the metro is home to an unusually dense cluster of acquisitive Fortune-500 strategics — Eaton, Parker Hannifin, Sherwin-Williams, Lincoln Electric, Cleveland-Cliffs, Nordson, RPM, Materion, Applied Industrial, Timken — that closed or announced more than $20B of acquisitions in 2024-2026. The five proprietary frames below explain how that density, the Akron-Cleveland Polymer Valley, and the Cleveland Clinic / University Hospitals ecosystem decide which advisor wins which deal.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led sales, PE recapitalizations, strategic carve-outs, and venture-stage exits — and Cleveland keeps showing up as one of the most underrated industrial M&A markets in the country. At Peony we now serve more than 5,900 customers, and Northeast Ohio sits right in the heart of the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark. This is the 22nd city in our M&A advisor series, and structurally it is one of the most distinctive.

Most "best M&A advisors" lists are interchangeable directory pages. This one is not, because Cleveland is not interchangeable. The metro has two things almost no other US city its size can claim at once: a Cleveland-headquartered middle-market investment bank bench (KeyBanc Capital Markets and Brown Gibbons Lang both run national practices from downtown Cleveland), and an in-backyard pool of large, acquisitive public strategics. When a Northeast Ohio industrial owner sells, several of the most logical strategic buyers are headquartered within a 30-minute drive — and that changes everything about how you pick an advisor.

This post is the working playbook I would hand to a Cleveland manufacturing owner weighing retirement, a Polymer Valley specialty-chemical founder fielding inbound interest, a healthcare-services operator inside the Cleveland Clinic ecosystem, or a private-equity partner sourcing Northeast Ohio carve-outs. The five frames — Strategic-Acquirer Density, Polymer Valley Advisor-Fit, Eds-and-Meds Buyer Gravity, the KeyBanc/BGL Alumni Bench, and the Reshoring Exit-Timing Window — come from cross-referencing the verified 2024-2026 deal record against the region's structural specifics.

What's the Cleveland / Northeast Ohio M&A advisor landscape for $5M-$300M deals in 2026?

The Cleveland-metro shortlist for 2026, sorted by deal-size band and tier:

| Firm | Founded | HQ / NE-Ohio office | Sweet spot | Specialty |

|---|---|---|---|---|

| KeyBanc Capital Markets | 1990s brand (KeyCorp roots 19th c.) | Cleveland HQ | $50M-$1B+ EV | Industrials, consumer, healthcare, tech, real estate, energy |

| Brown Gibbons Lang (BGL) | 1989 | Cleveland HQ | $25M-$500M+ EV | Industrials, consumer, healthcare, infrastructure, services, tech, RE |

| Citizens M&A Advisory | (Western Reserve absorbed 2017) | Cleveland | $25M-$500M EV | Mid-market sell-side + buy-side; industrials, services |

| MelCap Partners | 2000 | Wadsworth (Medina County) | $5M-$100M EV | LMM generalist — industrials, distribution, business services |

| Carleton McKenna & Co | 2001 | Downtown Cleveland | $5M-$75M EV | Specialty manufacturing + chemicals, cybersecurity, B2B services |

| Candlewood Partners | 2001 | Cleveland | $5M-$50M EV | MBOs, recapitalizations, special situations, niche industrials |

| River's Edge Alliance Group (REAG) | 2004 | Cleveland (multi-office) | $5M-$50M EV | Distribution, building products, chemicals, specialty plastics |

| BellMark Partners | 2009 | Boston + Cleveland | $20M-$200M EV | Services, consumer, industrials, healthcare |

| Copper Run | 2008 | Columbus (statewide OH) | $10M-$250M EV | LMM generalist across Ohio incl. Northeast Ohio |

| Cohen & Company Capital Markets | — | Cleveland-rooted | (specialist) | SPACs, digital assets, fintech — not Main-Street sell-side |

A few notes the table can't carry. KeyBanc Capital Markets and BGL are the only two nationally significant middle-market investment banks headquartered in Cleveland, and they anchor the top of the market. Citizens M&A Advisory is where the old Cleveland boutique Western Reserve Partners now lives (Citizens acquired it in 2017) — if you are pointed to "Western Reserve," that is the platform you are actually hiring. And Cohen & Company is Cleveland-rooted but is a capital-markets/SPAC specialist, not a $5M-$300M Main-Street sell-side shop — I include it for completeness, not as a default option for an industrial seller. For genuinely Main-Street businesses (under ~$5M), the right call is an IBBA-credentialed broker — Morgan & Westfield (Westlake), Murphy Business of Hudson, Transworld Business Advisors Cleveland West, or NEO Business Advisors — covered in the hire-by-size section below.

The two Cleveland-headquartered investment banks

KeyBanc Capital Markets is the investment-banking arm of Cleveland's KeyCorp and a true national middle-market platform run from downtown Cleveland. Its coverage spans industrials, industrial technology, consumer and retail, healthcare, technology, real estate, and energy, with a deep financial-sponsors group. It recently acted as sell-side advisor on TerraSource Holdings' sale to Astec Industries (July 2025). For a Northeast Ohio seller above ~$75M EV who wants league-table credibility and national sponsor reach, KeyBanc is the obvious local heavyweight; ask which Cleveland managing director will personally staff the process.

Brown Gibbons Lang (BGL), founded in 1989, is the other Cleveland-headquartered middle-market investment bank, organized into seven verticals (consumer, healthcare and life sciences, industrials, infrastructure, services, technology, and real estate). BGL is led today by co-CEOs Andrew K. Petryk and Effram E. Kaplan; founder Michael E. Gibbons passed away in 2025 and the firm carries his legacy forward. Recent sell-side work includes Frontier Waste Solutions' sale to GFL Environmental (April 2026) and Boston Valley Terra Cotta's sale to RAF Equity (February 2026). BGL is the strongest independent option for a Cleveland industrial, building-products, or environmental-services seller in the $25M-$500M band.

The Cleveland boutiques

MelCap Partners, founded in 2000 by Albert D. Melchiorre and based in Wadsworth (Medina County, in the Akron-Cleveland corridor), is a lower-middle-market generalist (FINRA-registered through broker-dealer M&A Securities Group) covering industrials and manufacturing, distribution, business services, consumer, and healthcare. MelCap also publishes the monthly Northeast Ohio Deal Activity report — the single best public read on the local market — which makes its bankers unusually fluent on regional deal cadence.

Carleton McKenna & Co, founded in 2001 and based in downtown Cleveland, is led by founder Paul H. Carleton and managing partner Christopher J. McKenna. It is the boutique most explicitly positioned for specialty manufacturing and chemicals, with additional strength in cybersecurity, B2B services, and construction — a natural fit for Polymer Valley sellers.

Candlewood Partners (Cleveland, 2001) specializes in management buyouts, recapitalizations, and special situations / restructuring for lower-middle-market companies, including niche industrials. It is the right call for owners pursuing a partial-liquidity recap or a complex, distressed-tinged situation rather than a clean full exit.

River's Edge Alliance Group (REAG), co-founded in 2004 by Scott Mashuda, is a Cleveland-rooted lower-middle-market firm (now multi-office, including Pittsburgh) whose stated verticals — distribution and logistics, building products, chemicals, manufacturing and fabrication, and specialty plastics — map almost perfectly onto Northeast Ohio's industrial base. It is a strong specialty-plastics and chemicals fit alongside Carleton McKenna. REAG operates as an M&A Source-credentialed M&A brokerage rather than a FINRA Series-79 broker-dealer, which fits the lower-middle-market band it serves.

BellMark Partners (founded 2009, with offices in Boston and Cleveland) is led by Dave Gesmondi, a former senior M&A banker at KeyBanc Capital Markets in Cleveland — the clearest single piece of evidence for the KeyBanc/BGL alumni bench frame below. BellMark advised Parker Hannifin on the divestiture of Filter Resources to Motion & Control Enterprises, exactly the kind of in-metro strategic carve-out that defines the Cleveland market.

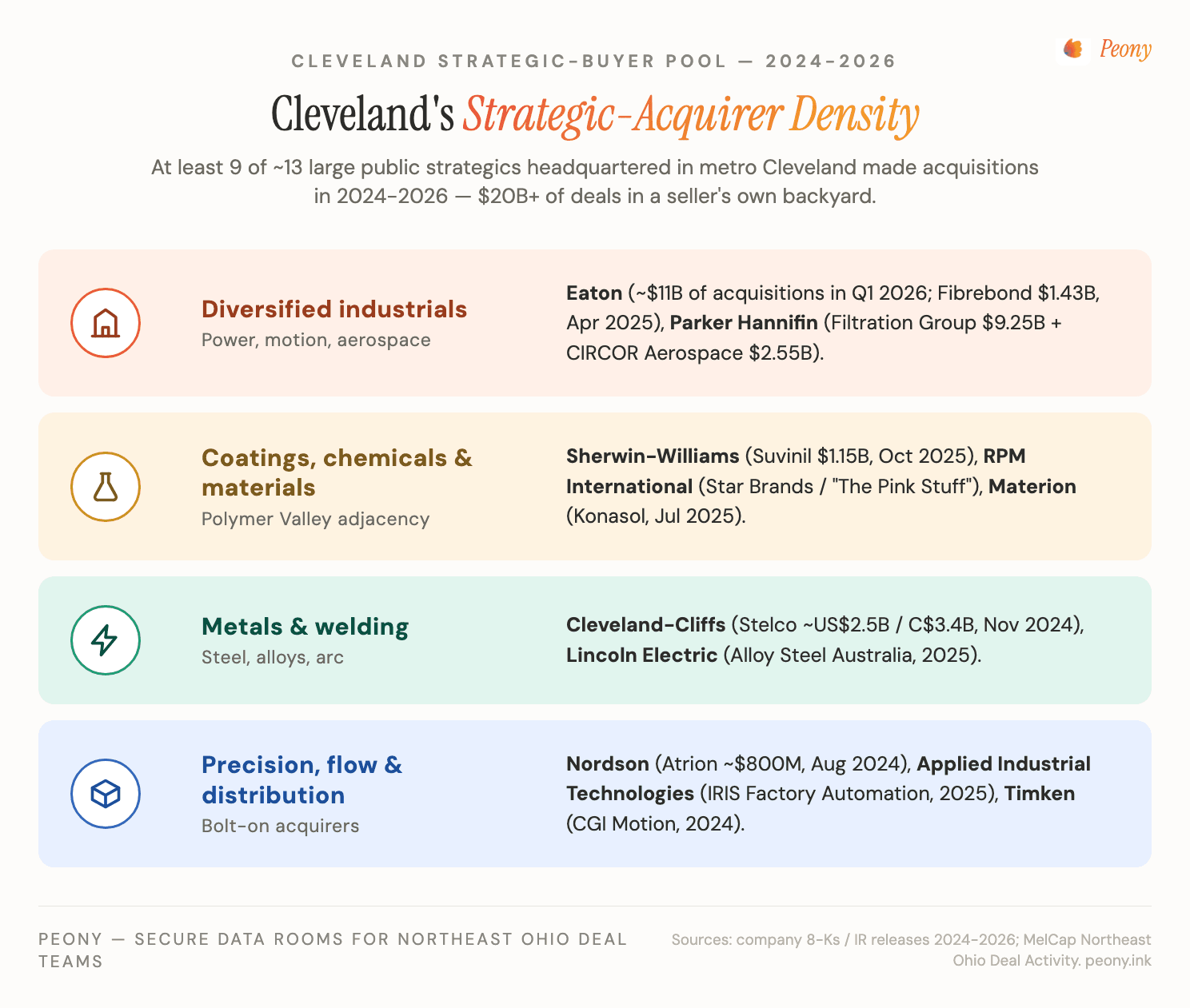

Why does Cleveland's strategic-acquirer density change your buyer pool?

Cleveland's signature M&A advantage is that an unusually large share of credible strategic buyers for industrial, materials, and many healthcare-services targets are headquartered inside the metro — so a Cleveland sell-side process can run a serious strategic-buyer track without the seller ever leaving Northeast Ohio.

The evidence is in the 2024-2026 deal record. Of roughly thirteen large public strategics headquartered in metro Cleveland, at least nine closed or announced acquisitions in the period:

- Eaton (operations in Beachwood) deployed roughly $11B of acquisitions in Q1 2026, after buying Fibrebond (modular power enclosures for data centers) for $1.43B in April 2025.

- Parker Hannifin (Mayfield Heights) announced Filtration Group for $9.25B (November 2025) and CIRCOR Aerospace for $2.55B, and closed Curtis Instruments in September 2025.

- Sherwin-Williams (Cleveland) bought BASF's Suvinil Brazilian architectural-paints business for $1.15B (closed October 2025).

- Cleveland-Cliffs (Cleveland) closed Stelco for about US$2.5B (C$3.4B) (November 2024).

- Nordson (Westlake) acquired Atrion (medical) for roughly $800M (August 2024).

- RPM International (Medina), Materion (Mayfield Heights), Lincoln Electric (Euclid), Applied Industrial Technologies (Cleveland), and Timken (Canton) all stayed acquisitive across 2024-2026.

For an advisor, this density is the whole game. The right Cleveland banker does not just own a generic buyers list — they know which of these corporate-development teams is actively buying in your category this quarter and can get your CIM in front of the right VP within weeks. The screening test for any advisor pitching a Northeast Ohio industrial: ask them to name, off the top of their head, the in-metro strategics most likely to bid on your business and the last deal each of those buyers closed. A genuinely Cleveland-fluent advisor will not hesitate.

One honest caveat: in-metro strategics are not always the highest bidder, and the biggest deals still draw national banks — the Avtron Power Solutions sale to France's Legrand ($1.125B, closed November 2025) was run by Harris Williams, not a local firm. The point of the density frame is not "always sell local"; it is that a Cleveland process should always include a credible local-strategic track, because few metros let you build one so easily.

How does the Polymer Valley change advisor selection for polymers and specialty-chemicals sellers?

If your business touches polymers, elastomers, coatings, or specialty chemicals, hire a banker who can speak feedstock and plug you into the Akron-Cleveland materials cluster — a generalist will leave multiple on the table.

Northeast Ohio is one of the densest polymer and specialty-chemical regions in the United States: roughly 820 polymer and materials companies, about 26,000 polymer workers, and Ohio ranks number one among US states for plastic and rubber product-manufacturing employment (Team NEO). Akron's history as the rubber capital of the world seeded the cluster; today it benefits from a feedstock tailwind as Utica and Marcellus shale natural-gas liquids feed regional chemical production, and Case Western Reserve anchors one of the country's leading polymer-engineering programs.

That depth means both specialist buyers and specialist advisors exist locally. The live deal flow is real: Goodyear sold its synthetic-rubber and chemicals business to Gemspring Capital for about $650M (closed October 2025), and Cleveland-headquartered coatings giant Sherwin-Williams paid $1.15B for BASF's Suvinil. Among the boutiques, Carleton McKenna & Co explicitly covers specialty manufacturing and chemicals, and River's Edge Alliance Group lists chemicals and specialty plastics as core verticals; for larger mandates, BGL's industrials practice and KeyBanc Capital Markets both carry materials coverage. The advisor-fit test for a chemicals or polymers seller: can the banker name the strategic and financial buyers active in your specific chemistry, and have they closed a comparable materials deal in the last 24 months?

How does Cleveland's Eds-and-Meds buyer gravity shape healthcare advisor selection?

Beyond industry, Cleveland's other defining economic anchor is healthcare — and the gravitational pull of the Cleveland Clinic and University Hospitals turns Northeast Ohio into a natural hub for health-services and health-tech sellers.

These two systems are among the largest employers in the region and sit at the center of a dense ecosystem of providers, payers, device makers, and health-IT companies. Healthcare is also a named hot sector for 2026 in MelCap's regional outlook. For a healthcare-services seller (physician practices, post-acute, behavioral health, outsourced services), that ecosystem means a deeper bench of both strategic acquirers and private-equity platforms doing roll-ups in the region than a metro Cleveland's size would otherwise support.

A note on rigor: I am framing this as buyer-gravity rather than citing a specific recent Cleveland Clinic or University Hospitals acquisition — the ecosystem effect is real and well-documented, but a seller should test it deal by deal. The advisor pattern for a Northeast Ohio healthcare seller: pair a boutique that can reach the regional health systems and the local PE healthcare platforms (BGL's healthcare and life-sciences vertical is the strongest local option at scale) with national buy-side reach if the asset is large enough to attract coastal healthcare PE. Ask the advisor to document at least three healthcare closings in your sub-sector in the last 24 months.

Why is Cleveland's boutique bench essentially a KeyBanc/BGL alumni tree?

A useful, slightly insider read on the Cleveland market: much of the boutique layer is staffed by alumni of the two big Cleveland-headquartered investment banks, KeyBanc Capital Markets and BGL. The metro effectively grew its own middle-market banker talent tree, which means even the smaller shops often carry bulge-adjacent training and relationships.

The clearest data point is BellMark Partners, founded in 2009 by Dave Gesmondi after a senior M&A career at KeyBanc Capital Markets in Cleveland. The broader pattern — that Cleveland boutiques are disproportionately founded and staffed by people who trained at KeyBanc or BGL — is my read from watching the market rather than a published statistic, so weigh it as informed analysis. But it has a practical implication for sellers: when you hire a Cleveland boutique, you are frequently getting a banker with institutional-platform pedigree at boutique attention levels and boutique fee structures. The diligence question that operationalizes this: ask a boutique banker where they trained and which platform relationships they carried over. A KeyBanc or BGL lineage usually translates into a faster, warmer path to both the in-metro strategics and the national sponsors.

Is now the reshoring exit-timing window for Northeast Ohio industrials?

For owners of Northeast Ohio industrial businesses, the macro backdrop in 2026 is about as favorable as it gets — supply-chain reshoring, record strategic-buyer cash, and the Baby-Boomer succession wave are stacking demand at the same time.

The reshoring signal is concrete: Team NEO reported that 2025 was one of its busiest business-attraction years on record, with more than 60 companies evaluating Northeast Ohio capital investment by mid-year, 53% of them global companies seeking a US foothold or supply-chain diversification. Ohio manufacturing GDP rose 8.5% and manufacturing employment 5.8% from 2020-2023 (Team NEO), and Intel's central-Ohio semiconductor campus has reframed the state as an advanced-manufacturing destination (a statewide rather than strictly Northeast-Ohio effect, but it lifts the whole regional narrative).

On the seller side, the demographic wave is just as real: Baby Boomers hold more than half of America's $163.1 trillion in wealth (UBS Global Wealth Report 2025, cited by MelCap) while making up roughly a fifth of the population, and are projected to be largely out of the workforce by about 2035 — a durable owner-succession pipeline. And the market is already moving: MelCap's Northeast Ohio Deal Activity report showed 2025 volume up about 6% over 2024, with December 2025 up roughly 14% year over year, against a national backdrop where December 2025 was the highest December monthly US deal total since 2021. The exit-timing read: industrial owners who have been waiting for "a better year" are arguably in one now, and the advisor conversation is worth starting 6-9 months before you want to be in market.

What's a reasonable success fee for a $25M Cleveland sell-side, and how do fees vary?

Cleveland M&A advisors price the way the broader US lower-middle-market does: a monthly retainer or fixed work fee plus a success fee at close, with the success rate declining as deal size grows.

For a $25M enterprise-value deal, the most common structure is a Double Lehman scale (10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% of everything above $5M), which computes to about $700K — roughly 2.8%. Add the slice of retainer that is not credited back plus any minimum-fee floor and the effective blended rate usually lands near 3-3.5%, consistent with national data showing success fees around 4.8% at $5M, 3.4% at $25M, and 2.0% at $100M+. Lehman-style declining formulas are not obsolete — a declining-rate Lehman structure is still the single most common arrangement (about 44% of engagements), versus roughly 26% flat-rate and 20% accelerators.

The variation by advisor type in Cleveland:

- Boutiques (MelCap, Carleton McKenna, Candlewood, River's Edge) typically run Double Lehman or a negotiated flat 2.0-2.75% at $25M-$75M, with a $25,000-$75,000 retainer.

- The investment banks (KeyBanc, BGL) carry higher retainer floors ($75,000-$150,000+) given their cost structures, and reach for standard Lehman with capital-markets add-ons on larger deals.

- Main-Street brokers on sub-$2M businesses often charge a flat 8-12% or Double Lehman where the minimum fee dominates.

Across all of them, roughly five of six advisors charge a retainer, about 72% credit it against the success fee, and a minimum-fee floor (commonly $50K-$250K) appears in about two-thirds of engagement letters (the granular 67%/72% figures are from the 2021-22 Fee Guide survey; the headline curve and structure split are current). The full math — including the engagement-letter clauses that quietly inflate the bill — is in our M&A advisor fees hub.

What does the Cleveland M&A deal cadence look like over the past 12 months?

A representative slate of verified 2024-2026 Northeast Ohio transactions — both the local-advisor closings and the big in-metro strategic deals that define the buyer pool:

| Target (HQ) | Acquirer | Date | Approx value | Sector | Advisor (if known) | | ------------------------------------------------- | ---------------------------- | ----------------- | ----------------- | ------------------------------- | ---------------------------- | --- | -------------------- | ---------------- | -------- | ----------- | -------------------- | ----------------------------------- | | Avtron Power Solutions (Cleveland) | Legrand (France) | Nov 2025 (closed) | $1.125B | Power equip / data-center infra | Harris Williams (sell-side) | | Goodyear synthetic-rubber & chemicals (Akron R&D) | Gemspring Capital | Oct 2025 (closed) | ~$650M | Polymers / specialty chemicals | undisclosed | | Country Pure Foods (Akron) | Peterson Brands | Dec 2025 | undisclosed | Food & beverage | (Blue Point Capital, seller) | | Stelco Holdings (Canada) | Cleveland-Cliffs (Cleveland) | Nov 2024 (closed) | ~US$2.5B (C$3.4B) | Steel / metals | — | | Frontier Waste Solutions | GFL Environmental | Apr 2026 | undisclosed | Environmental / waste | BGL (sell-side) | | Boston Valley Terra Cotta | RAF Equity | Feb 2026 | undisclosed | Building products | BGL (sell-side) | | Fibrebond Corp | Eaton (Beachwood ops) | Apr 2025 | $1.43B | Modular power / data centers | — | | TerraSource Holdings | Astec Industries | Jul 2025 | undisclosed | Industrial equipment | KeyBanc Capital Markets (sell-side) | | Suvinil (BASF, Brazil) | Sherwin-Williams (Cleveland) | Oct 2025 (closed) | $1.15B | Coatings / chemicals | — | | Star Brands / "The Pink Stuff" (UK) | RPM International (Medina) | Apr 2025 | undisclosed | Consumer cleaning | — | | Atrion Corp | Nordson (Westlake) | Aug 2024 (closed) | ~$800M | Medical devices | — |

The pattern worth internalizing: local boutiques and the two Cleveland banks carry the verified sell-side mandates in the $20M-$300M industrial range (BGL, KeyBanc, BellMark, MelCap), while the eye-catching billion-dollar headlines are mostly in-metro strategics buying — which is exactly why the Strategic-Acquirer Density frame matters so much for how you choose an advisor.

Which Cleveland advisor should I hire for a sub-$10M sell-side? What about a $25M-$100M one?

The right advisor scales with deal size, and Cleveland has a clean ladder.

Under ~$5M (Main-Street): Use an IBBA- or M&A Source-credentialed business broker, not an investment bank — at this size a Series-79 bank's minimum-fee floor ($50K-$250K) eats too much of the proceeds. In Northeast Ohio the options include Morgan & Westfield (Westlake, businesses under ~$10M revenue), Murphy Business of Hudson, Transworld Business Advisors Cleveland West, and NEO Business Advisors. Expect a flat percentage (often 8-12%) or a Double Lehman where the minimum dominates.

$5M-$25M EV (lower middle market): This is the boutique sweet spot. MelCap Partners, Carleton McKenna & Co, Candlewood Partners, and River's Edge Alliance Group all run deals in this band with senior bankers personally on buyer calls. Match by sector: Carleton McKenna or River's Edge for chemicals/specialty manufacturing; Candlewood for an MBO or recap; MelCap as the broad generalist.

$25M-$100M EV (core middle market): Here the boutiques (especially BellMark and MelCap at the top of their range, and Carleton McKenna for chemicals) compete with the two Cleveland investment banks. BGL is the strongest independent for industrials, building products, and environmental services; KeyBanc Capital Markets adds sponsor coverage and capital-markets capability. The deciding factor is usually whether your best buyers are local strategics (favor a relationship-rich boutique or BGL) or a broad national sponsor pool (favor KeyBanc's platform).

$100M-$300M+ EV: KeyBanc Capital Markets and BGL lead, often with a national co-advisor on very large or cross-border processes. Above ~$300M, expect national banks (Harris Williams, Lincoln International, William Blair, Baird) to compete for the mandate alongside the Cleveland banks — as the Avtron-Legrand deal showed.

Honest comparison: which Cleveland advisors fit which lane?

| Sub-vertical | $5M-$25M EV | $25M-$100M EV | $100M-$300M EV | $300M+ EV |

|---|---|---|---|---|

| Industrial / manufacturing | MelCap + Carleton McKenna + Candlewood | BGL + BellMark + MelCap | KeyBanc + BGL | KeyBanc + BGL + national |

| Polymers / specialty chemicals | Carleton McKenna + River's Edge | Carleton McKenna + BGL | KeyBanc + BGL | National materials specialists |

| Building products / industrial distribution | River's Edge + MelCap | BGL + BellMark | KeyBanc + BGL | KeyBanc + BGL |

| Healthcare services | MelCap + Carleton McKenna | BGL + BellMark | BGL + KeyBanc | National healthcare IBs |

| Business services / consumer | MelCap + Candlewood + Copper Run | BellMark + BGL | KeyBanc + BGL | Coastal generalists |

| Special situations / MBO / recap | Candlewood | Candlewood + BGL | BGL + KeyBanc | National |

| Main-Street (under $5M) | Morgan & Westfield / Murphy / Transworld | — | — | — |

The honest limits to flag:

- Above $500M EV — bulge-bracket and large-national capabilities matter, and Datasite or Intralinks become the dominant data-room choices given pre-existing relationships with QoE providers, law firms, and R&W underwriters. We built Peony for the sub-$500M band, which is where most Northeast Ohio deals live.

- Cross-border buyer outreach (European or Asian strategics) — pair a Cleveland boutique with a national or global platform for buyer-pool extension; the local-only structure underperforms here.

- Cleared / defense-exposed deals (CFIUS, ITAR) — Cleveland has limited defense-banker capacity; route to specialists.

- Music, media, or pure-tech software — outside the region's industrial/healthcare core; a sector-specialist advisor elsewhere will usually beat a Cleveland generalist.

For the deals that do fit — the $5M-$300M industrial, polymer, building-products, and healthcare-services businesses that make up the bulk of Northeast Ohio M&A — a Cleveland-fluent advisor with a documented in-metro relationship map is hard to beat, and a clean data room prepared before launch is the cheapest lever you control on both timeline and price.

Bottom line

Cleveland is one of the most underrated industrial M&A markets in the country, and its advisor landscape is shaped by one rare asset: a dense cluster of acquisitive Fortune-500 strategics — Eaton, Parker Hannifin, Sherwin-Williams, Lincoln Electric, Cleveland-Cliffs, Nordson, RPM, Materion, Applied Industrial, Timken — headquartered inside the metro, which closed or announced more than $20B of acquisitions in 2024-2026. That in-backyard buyer pool, plus the Akron-Cleveland Polymer Valley and the Cleveland Clinic / University Hospitals ecosystem, is what should drive advisor selection.

Two Cleveland-headquartered middle-market investment banks lead the market — KeyBanc Capital Markets and Brown Gibbons Lang — backed by a genuinely deep boutique bench (MelCap Partners, Carleton McKenna & Co, Candlewood Partners, River's Edge Alliance Group, BellMark Partners) that is disproportionately staffed by KeyBanc and BGL alumni. For specialty chemicals and polymers, weight toward Carleton McKenna and River's Edge; for an MBO or recap, Candlewood; for the broad lower-middle-market, MelCap; and for Main-Street deals under ~$5M, an IBBA-credentialed broker rather than a bank.

The single most important advisor-selection question for a Northeast Ohio seller: which firm has the deepest documented relationship with the named in-metro strategics and the PE platforms in your sub-sector, and can show at least three closed transactions with those buyers in the last 24 months? In a metro where so many logical buyers are headquartered down the road, that relationship map is the whole edge. We serve 5,900+ customers on the data-room side of exactly these deals — the prep you do before you pick an advisor (clean financials, a staged data room, a tight buyer thesis) compounds everything the advisor does next.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Cleveland shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- M&A Due Diligence: 6-Phase Playbook + 8 Workstreams — what your buyer is actually doing once you sign the LOI

- M&A Data Room: Setup and Workstream Mapping — the data room setup playbook for sell-side prep

- Best Data Room for a Small M&A Deal (sub-$30M sale) — right-sized VDR selection and setup for a sub-$30M sale, the band where most Northeast Ohio industrial and Polymer Valley founder exits land

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep including vendor DD

- State of M&A Data Rooms: 2026 Benchmark — the 283-deal Peony platform benchmark

- Best M&A Advisors in Detroit — the closest Midwest industrial comparator (automotive and manufacturing)

- Best M&A Advisors in Columbus — the other major Ohio metro, where the capital arrived (Intel, $15B+ of data centers) before the homegrown bankers did, and where KeyBanc and Brown Gibbons Lang cover deals from Cleveland

- Best M&A Advisors in Cincinnati — southern Ohio's consumer-brand "Brand Town," where BGL's CPG practice covers deals from Cleveland and the giants (Fifth Third, Kroger, Cintas) are active acquirers

- Best M&A Advisors in Pittsburgh — Rust Belt industrial and robotics comparator

- Best M&A Advisors in Minneapolis — Upper-Midwest medtech, industrial, and AgTech comparator

- Best M&A Advisors in Chicago — the Midwest's largest M&A hub

- Best M&A Advisors in St. Louis — Midwest strategic-acquirer-density comparator: a "Headquarters Town" anchored by the homegrown national bank Stifel, with a deep industrial and distribution base

- How to Write a CIM (Confidential Information Memorandum) — the authoring playbook for the offering document your advisor will build for the sale

Footnotes and sources

- MelCap Partners — Northeast Ohio Deal Activity reports (monthly; regional deal-volume figures)

- Team NEO — Northeast Ohio polymers & materials cluster data (820 polymer companies, ~26,000 workers, Ohio #1 plastic/rubber employment; 2025 business-attraction figures)

- Brown Gibbons Lang (BGL) — firm overview, co-CEOs Petryk and Kaplan, Frontier Waste and Boston Valley Terra Cotta transactions

- KeyBanc Capital Markets — firm overview; TerraSource / Astec transaction

- MelCap Partners — firm overview; Albert D. Melchiorre

- Carleton McKenna & Co — firm overview; Paul Carleton, Christopher McKenna

- Candlewood Partners — firm overview

- River's Edge Alliance Group (REAG) — firm overview; specialty plastics / chemicals verticals

- BellMark Partners — firm overview; Dave Gesmondi; Parker Hannifin / Filter Resources advisory

- Sherwin-Williams completes acquisition of Suvinil ($1.15B, October 2025)

- Parker Hannifin to acquire Filtration Group ($9.25B announced November 2025)

- Eaton Q1 2026 acquisitions and Fibrebond ($1.43B, April 2025)

- Cleveland-Cliffs completes acquisition of Stelco (~US$2.5B / C$3.4B, November 2024)

- Harris Williams advises on Avtron Power Solutions sale to Legrand ($1.125B, November 2025)

- Goodyear divests chemicals business to Gemspring (~$650M, October 2025)

- UBS Global Wealth Report 2025 (Boomer wealth share, via MelCap)

- Firmex / Axial M&A Fee Guide 2024-25 (success-fee curve, Lehman structure split, retainer and minimum-fee survey data)