14 Best M&A Advisors in Detroit for $5M-$500M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

14 Best M&A Advisors in Detroit for $5M-$500M Deals (2026)

Quick answer: I have run M&A diligence across enough Detroit-metro mandates and watched enough Front Range buy-side and sell-side processes to have firm conclusions on which advisors win which deals. The 14-firm shortlist for 2026: Houlihan Lokey, Lincoln International, BMO Capital Markets, Cascade Partners (Rajesh Kothari healthcare), PMCF / Plante Moran Corporate Finance (Southfield industrial specialist), Plante Moran, TD Cowen Middle Market (Quarton Birmingham legacy), Angle Advisors (Birmingham A&D + auto), Donnelly Penman & Partners (Grosse Pointe Woods auto Tier-2 specialist), Cendrowski Corporate Advisors (Prosperity Partners-acquired August 11 2024), Strength Capital Partners (Birmingham PE buyer context), EdgePoint Capital Advisors (Beachwood OH coverage), Amherst Partners (Birmingham IMAP network), and FINNEA Group (Tim Leuliette unique simultaneous M&A + restructuring). Detroit fragments into four structurally different verticals — auto / mobility, mortgage / fintech, defense-industrial, and healthcare — anchored by Rocket Companies-Mr. Cooper $14.2B (closed October 1 2025), ABC Technologies-TI Fluid Systems $2.4B (closed April 15 2025), AAM → Dauch Corporation-Dowlais $1.44B (closed February 3 2026; rebrand effective January 26 2026; NYSE: DCH from February 5 2026), Stellantis €22.2B H2 2025 charges (February 6 2026), Henry Ford Health-Ascension Michigan $12B joint venture (closed September 30 2024, HFH 80% / Ascension 20%, 8 hospital campuses + ~17,000 employees integrated), and Corewell-Beaumont post-merger divestiture cycle. Six proprietary frames below distinguish the right advisor by sub-vertical.

Last updated: May 2026

Why I wrote this

I have run buy-side and sell-side diligence on hundreds of deals across founder-led sales, PE recapitalizations, strategic acquisitions, and venture-stage exits. At Peony we now serve more than 5,900 customers, and Detroit is one of the most structurally distinct mid-market clusters in our platform's deal-room telemetry. The Tier A US M&A Mega cluster series has now shipped 19 city posts (NYC, Boston, Philadelphia, DC, Atlanta, Charlotte, Miami, Chicago, Dallas, Houston, LA, SF, Seattle, Phoenix, San Diego, Nashville, Minneapolis, Denver, Austin). Detroit is the 20th — and structurally different from the prior 19 because the metro fragments across four structurally distinct verticals (auto / mobility, mortgage / fintech, defense-industrial, healthcare) to a degree no other US metro matches.

Detroit's M&A landscape concentrates differently than any other Tier A US city. The auto / mobility cluster anchors at Stellantis (Auburn Hills MI HQ), General Motors (Detroit Renaissance Center HQ), and Ford Motor Company (Dearborn HQ) plus the Tier-1 / Tier-2 supplier base (BorgWarner, Lear, Adient, American Axle / Dauch Corporation, Magna USA operations, ZF North America). Stellantis announced ~€22.2B in charges for H2 2025 on February 6 2026 — largely reflecting "the cost of over-estimating the pace of the energy transition" per the 6-K filing — and that announcement has reshaped the entire Tier-2 capacity rationalization cycle.

The mortgage / fintech cluster anchors at Rocket Companies (NYSE: RKT, Renaissance Center) and Ally Financial (Detroit HQ). Rocket closed its $14.2B equity-value acquisition of Mr. Cooper Group on October 1 2025 — the largest independent mortgage deal in US history — and acquired Redfin on July 1 2025 (announced March 10 2025; 63% premium over 30-day VWAP). Detroit is now the second-largest US mortgage / consumer-credit M&A advisory hub by per-capita advisory volume after NYC.

The defense-industrial cluster anchors at the Sterling Heights / Warren corridor — BAE Combat Vehicles Sterling Heights and General Dynamics Land Systems Sterling Heights are the only two US tracked-vehicle assembly plants. The 2025 BAE Sterling Heights ACV-30 contract awards ($184M for 30 turreted amphibious combat vehicles + $181M for 31 ACV medium-caliber cannon variants) anchor a multi-year Section 232/301 tariff-driven onshoring M&A cycle.

The healthcare cluster anchors at Corewell Health (largest Michigan system, 22 hospitals, ~64,000 employees, ~$200M annual synergy capture from the February 1 2022 Beaumont-Spectrum merger), Henry Ford Health (closed a $12B joint venture with Ascension Michigan on September 30 2024 — HFH 80% / Ascension 20%; 8 hospital campuses + ~17,000 employees integrated), Trinity Health Michigan, and the residual Ascension Michigan minority-stake entity.

This post is the working playbook I would hand to a Detroit-area Tier-2 auto supplier founder reading the Stellantis €22.2B cascade and weighing exit timing, a mortgage / fintech founder mapping the Rocket-Mr. Cooper template, a BAE-Sterling-Heights-orbit defense-industrial Tier-2/3 supplier reading the Section 232/301 onshoring wave, a Detroit-metro healthcare services CEO mapping post-Corewell-merger and post-HFH-Ascension buyer pool reshuffling, a Birmingham / Bloomfield family-office principal navigating the Michigan Tax Stack + FL/NV migration sequence, or a distressed Tier-2 founder considering dual-track M&A + restructuring. The six proprietary frames (Stellantis Tier-2 Cascade Effect, Detroit Mortgage M&A Velocity, Defense Industrial Onshoring Wave, Corewell Spinout Cycle, Michigan Tax Stack + FL/NV Migration, OEM-Tier-Dependency Whipsaw) come from cross-referencing the 2024-2026 deal record with Detroit's structural specifics.

What's the Detroit M&A advisor landscape for $5M-$500M deals in 2026?

The 14-firm Detroit-metro shortlist for 2026, sorted by deal-size band and specialty:

| Firm | Founded | HQ / Detroit office | Sweet spot | Specialty |

|---|---|---|---|---|

| Houlihan Lokey | 1972 | LA HQ (Detroit auto coverage from Chicago/NY) | $50M-$500M+ EV | Auto / industrial / #1 global Chapter 11 restructuring |

| Lincoln International | 1996 | Chicago HQ (Detroit auto coverage from Chicago) | $50M-$500M EV | Auto & Mobility Tech specialty group |

| BMO Capital Markets US M&A | 1989 (BMO Cap Mkts) | Toronto / Chicago / NY | $50M-$500M+ EV | North American cross-border industrial / metals / food-ag |

| Cascade Partners | 2012 | Southfield MI | $10M-$150M EV | Healthcare services (largest practice) + industrials |

| PMCF (Plante Moran Corporate Finance) | 1995 | Southfield MI | $25M-$300M EV | Industrial manufacturing + plastics + packaging + medtech |

| Plante Moran | 1924 (PMCF 1995) | Southfield MI | $10M-$200M EV | Accounting-integrated sell-side prep + QoE + tax |

| TD Cowen Middle Market (Quarton legacy) | 2008 (Quarton Partners) | Birmingham MI (legacy) | $25M-$500M EV | Cross-border industrial (DACH / Italy / UK buyer access) |

| Angle Advisors | 2009 | Birmingham MI | $10M-$200M EV | Aerospace & defense + automotive + industrial |

| Donnelly Penman & Partners | September 2000 | Grosse Pointe Woods MI | $10M-$150M EV | Auto Tier-2 specialty (4 confirmed 2024 closes); community banks |

| Cendrowski Corporate Advisors | 1983 | Bloomfield Hills MI (Prosperity-acquired Aug 11 2024) | $5M-$75M EV | Tax-integrated valuation + family office + dispute advisory |

| Strength Capital Partners (BUYER context) | 2000 | Birmingham MI | Equity $10M-$50M / EBITDA $4M-$25M | PE sponsor manufacturing + distribution roll-up |

| EdgePoint Capital Advisors | 2000 | Beachwood OH (Detroit cross-border) | $10M-$100M EV | Industrials + distribution + transportation |

| Amherst Partners | 1994 | Birmingham MI | $10M-$150M EV | IMAP network diversified middle market |

| FINNEA Group | May 2011 | Birmingham MI | $10M-$200M EV | Unique simultaneous M&A + restructuring (Tim Leuliette) |

Excluded with rationale:

- W.Y. Campbell & Co. — DORMANT. Comerica (NOT BMO) acquired W.Y. Campbell in 1995; founders left 2010 after Comerica-employee buyback talks failed; last advised deal was 2010 (Interstate Waste Services). PrivCo lists $4M revenue / 0 employees. Removed from any active Detroit advisors listing.

- Headwaters MB — Detroit's auto specialist is not Headwaters; Headwaters was a Denver-area firm absorbed by Capstone Partners 2018 → Huntington Bancshares 2022.

- Hennessy Capital — Zephyr Cove NV, not Detroit.

Firm profiles

1. Houlihan Lokey — Detroit-area Auto / Industrial Coverage

Houlihan Lokey (NYSE: HLI, Los Angeles HQ, founded 1972 by Richard Houlihan and O. Kit Lokey — both ex-PwC) covers Detroit-area auto mandates from its Chicago and New York offices — the firm does NOT maintain a standalone Detroit office. The Auto Mobility group is led by Mark Hammond (Co-Head of Global Auto), Phillip Pierce (Managing Director, Industrials / Automotive), and Brad Beuter (Senior Advisor, Auto Mobility). Houlihan topped both volume and value tables for 2024 auto M&A per the Just-Auto industry league table.

Beyond auto, Houlihan carries the #1 global Chapter 11 restructuring book — a critical capability in the post-Stellantis-€22.2B cycle when distressed Tier-2 suppliers need a banker who can run M&A and restructuring with the same senior team. Deal-size band $50M-$500M+ EV; routine on $1B+ auto transactions. The October 2 2025 Strength Capital Partners acquisition of Grand Equipment Company (Hudsonville MI construction equipment distributor) — where Houlihan advised Strength Capital on the buy-side — is a Detroit-relevant 2025 tombstone.

Why founders pick them: When the deal crosses $200M EV and includes cross-border PE buyers, Houlihan delivers the world's top auto-M&A franchise by 2024 volume/value tables. The Lokey restructuring book gives them a unique edge on distressed Tier-2 suppliers — a critical capability in the post-Stellantis-€22.2B cycle.

2. Lincoln International — Detroit Auto / Mobility Coverage

Lincoln International (Chicago HQ, founded 1996, 25+ offices across North America with 850+ professionals in 15 countries) runs its Auto & Mobility Tech investment banking specialty group out of Chicago — covering Detroit from there. Senior leadership includes Aamir Rehman, Jim Lawson (founding partner), and John Gnuse on the Auto Group. Lincoln advised the Android Industries / Avancez merger with Detroit Manufacturing Systems creating Voltava in 2024 — one of the largest minority-owned automotive businesses in Michigan.

Deal-size band $50M-$500M EV with a middle-market specialty. Sector focus spans Auto & Mobility Tech (named specialty group), Industrials, Tech & Services, Healthcare, and Consumer.

Why founders pick them: When the founder wants global cross-border buyer access (especially European or Asian auto Tier-1s buying into US Tier-2s) without paying NY-bracket fees, Lincoln is the default Chicago-based middle-market choice with deep auto / mobility specialization.

3. BMO Capital Markets US M&A

BMO Capital Markets US M&A operates from Toronto / Chicago / New York; the firm does not maintain a standalone Detroit M&A office and Detroit-area mandates are run out of BMO Chicago + NY. Critical correction to widely-cited but incorrect aggregator data: [W.Y. Campbell & Co. was acquired by Comerica in 1995, NOT BMO, and W.Y. Campbell has been effectively dormant since founder departures in 2010.

BMO's US Mid-Market group covers diversified middle market with specialty in metals & mining, food & ag, industrial, and healthcare. Deal-size band $50M-$500M+ EV.

Why founders pick them: Detroit founders who want a North American bracket bank (US-Canada cross-border buyer pool) but with middle-market deal team responsiveness pick BMO over the US bulge brackets. Auto Tier-1 buyer access through both Chicago and Toronto.

4. Cascade Partners — Southfield Healthcare + Industrials Boutique

Cascade Partners (Southfield MI, founded 2012 by Rajesh Kothari Managing Director with ~30 years experience as investor + financial advisor + entrepreneur) is the most-cited Michigan healthcare M&A boutique. Healthcare services is the largest practice; sector coverage extends to industrials, business services, and technology. Deal-size band $10M-$150M EV.

Representative 2023-2026 deals: DeGarA acquired by American Physician Partners October 2023 (Cascade sell-side advisor; APP later filed Chapter 11 July 2024 — Cascade-advised sale closed before that); First Care Medical (FCM, Utah) acquired Advanced Spine & Rehabilitation (ASR) 2024 (Cascade buy-side). Cascade publishes the 2025 North American Healthcare M&A Update and 2024-2025 industrial M&A commentary — credible sector thought-leadership.

Why founders pick them: Lower-middle-market healthcare services and industrial founders who want sector-specialized boutique attention without paying bracket-bank fees. Kothari is the most-cited Michigan healthcare M&A voice — strong fit for physician practices, behavioral health, and ambulatory surgical centers.

5. PMCF / Plante Moran Corporate Finance — Southfield Industrial Specialist

PMCF (3000 Town Center Suite 100, Southfield MI 48075; phone 248.223.3300; offices in Chicago, Detroit, and Denver) is the trade name for PMCF Advisors LLC plus P&M Corporate Finance LLC (FINRA-registered broker-dealer / SIPC member). The "P&M" in "PMCF" stands for "Plante & Moran" — PMCF is an affiliate of Plante Moran (one of the nation's largest professional services firms, founded 1924, Southfield-HQ accounting/consulting firm) per pmcf.com/about/affiliations/plante-moran/.

Deal-size band $25M-$300M EV; 300+ transactions completed since 1995 inception. Sector specialty in industrial manufacturing, plastics & packaging, medical technology, diversified industrials, and industrial services & distribution. PMCF publishes quarterly Industrial Manufacturing M&A Pulse reports — the single most-cited proprietary sector dataset on US Midwest industrial M&A. Q3 2025: 77 US industrial M&A transactions, down 34.2% YoY from 117 in Q3 2024 — a key Stellantis-cascade indicator. PMCF's Q3 2025 Pulse reports a trailing-12-month deal count of 1,039 as of September 2025.

Why founders pick them: PMCF is the default Midwest middle-market industrial manufacturing advisor. The Plante Moran integration lets founders consolidate sell-side accounting / tax / QoE work under one professional services umbrella — uniquely useful for Detroit-area family businesses where the same family CFO has used Plante Moran for tax for decades.

6. Plante Moran — Accounting-Integrated M&A Front-End

Plante Moran (27400 Northwestern Hwy, Southfield MI 48034; 25+ offices nationally; founded 1924 by Frank Moran and Elmer Plante) is the parent professional services firm of PMCF. As a standalone advisor, Plante Moran provides transaction services on the front end (sell-side prep, QoE, valuations, tax restructuring); PMCF handles M&A execution. Deal-size band best fit $10M-$200M for the integrated Plante Moran + PMCF model. 59 deals as general advisor per PitchBook, most recently advising The Anderson Group in 2025.

Why founders pick them: The same Plante Moran partner who has handled the founder's tax and audit for 10+ years can now hand off to a PMCF banker down the hall. Lowest-friction sell-side prep in the Midwest for $10M-$50M companies.

7. TD Cowen Middle Market — Quarton Birmingham Legacy

TD Cowen Middle Market is the post-2023 brand for the former Quarton Partners / Quarton International franchise. Cowen acquired Quarton International on January 2 2019; TD Securities (Toronto-Dominion Bank's investment banking arm) acquired Cowen in March 2023. The Quarton legacy spans Quarton Partners (founded 2008) and Quarton International (formed 2015 by combining Quarton Partners with Blue Corporate Finance for DACH / Switzerland / Austria / UK coverage). Pre-acquisition track record: 500+ transactions in 30 countries with total volume exceeding $15B.

Birmingham MI office status post-2023 integration is unverified — likely consolidated into broader TD Securities NYC footprint, though specific Detroit-area MDs may still source mandates from the Birmingham address. Deal-size band $25M-$500M EV with diversified middle-market industrials and cross-border M&A specialty. Email domains are ambiguous post-integration: first.last@td.com (TD Securities) and first.last@tdcowen.com (TD Cowen brand) are both possible.

Why founders pick them: Cross-border European-Asian-US industrial buyer access through the TD bank platform. Best fit for Detroit-area industrial owners selling to a German Mittelstand or Italian family-office buyer.

8. Angle Advisors — Birmingham Auto / A&D Boutique

Angle Advisors (280 N Old Woodward Ave, Birmingham MI 48009, founded 2009 by co-founders Clifton Roesler and Kevin Marsh) is a 310+ closed-deal boutique with named specialty in aerospace & defense, automotive, vehicular (truck / heavy equipment), industrial components, capital equipment, electronics, metals, consumer products, packaging, and residential services. Roesler led Tier-2 auto sell-side for 20+ years prior to founding the firm. Deal-size band $10M-$200M EV.

Why founders pick them: When the seller is a $30M-$100M Detroit-area Tier-2 auto supplier or A&D component manufacturer and wants a boutique with deep industry rolodex, Angle is the default below-bracket pick. The A&D specialty is the closest like-for-like Detroit alternative to Houlihan Lokey industrials on sub-$100M defense supplier sell-sides.

9. Donnelly Penman & Partners — Grosse Pointe Auto Tier-2 Specialist

Donnelly Penman & Partners (20902 Mack Avenue Suite 200, Grosse Pointe Woods MI 48236; phone 313.446.9900; founded September 2000) is the Detroit-rooted auto Tier-2 specialist with the deepest 2024 sell-side track record in the metro. Co-founders John Donnelly (Senior Managing Director) and Robert Penman built an employee-owned firm with 275+ transactions since inception and 110+ years of combined banker experience. Deal-size band $10M-$150M EV.

Four confirmed 2024 closes establish the franchise: AMI Industries acquired Fluid Handling Technology Inc. July 1 2024 (Donnelly Penman exclusive sell-side advisor; AMI = Tier I/II fluid handling supplier across agriculture, construction, automotive, heavy truck, defense, marine); OKE Group GmbH acquired Global Enterprises July 1 2024 (Donnelly Penman exclusive sell-side advisor to Global, a manufacturer of technical extruded profiles + seating / interior assemblies for global automotive industry); The Shyft Group acquired Independent Truck Upfitters July 25 2024 (Donnelly Penman exclusive advisor to Shyft, a work-trucks / specialty vehicles platform); Lock Joint Tube affiliate acquired JEMS of Litchfield 2024 (Donnelly Penman exclusive sell-side to JEMS, a trailer hitch / towing components supplier to OEM / aftermarket). Sector focus extends to industrial and financial institutions (community banks).

Why founders pick them: Detroit-rooted (Grosse Pointe Woods is 15 minutes from the Renaissance Center) automotive specialist with the deepest Tier-2 supplier rolodex in the metro. When a $30M Michigan auto supplier wants discreet local representation with an OEM call-down list, Donnelly Penman beats every Chicago / NY bracket option.

10. Cendrowski Corporate Advisors (CCA) — Bloomfield Hills Tax-Integrated Advisory

Cendrowski Corporate Advisors (Bloomfield Hills MI primary office plus secondary Chicago office, founded 1983 by Harry Cendrowski CPA / ABV / CFF / CFE, former Touche Ross / Deloitte) was acquired by Prosperity Partners (Chicago-based PE-backed accounting consolidator) on August 11 2024 per Crain's Detroit Business. CCA's Bloomfield Hills HQ remains open with all 20 employees; Harry Cendrowski continues as Managing Partner. Deal-size band $5M-$75M EV for advisory / valuation / QoE work — not lead M&A execution.

Sector focus: boutique tax consulting + family office services + business valuation + dispute advisory + forensic accounting. Family-office-led carve-outs and physician-practice valuations dominate the deal book.

Why founders pick them: Detroit-area family-office founders selling closely-held businesses where tax basis, family equity dynamics, and post-close family-office structure matter MORE than maximum-price banker hustle. Best fit for founders selling to family-office buyers or doing inter-generational transfers.

11. Strength Capital Partners — Birmingham PE Sponsor (BUYER context)

Strength Capital Partners (Birmingham MI primary office plus Cincinnati OH and Denver CO offices, founded 2000 by Mark McCammon and Mike Bergeron — Harvard Business School classmates) is a PE sponsor and BUYER, not a pure advisor — included here because Detroit founders should know about active strategic acquirers. Equity checks $10M-$50M per platform targeting EBITDA $4M-$25M companies in manufacturing, distribution, infrastructure, and industrial services with Central US focus.

Track record: $500M+ equity capital deployed across 70+ transactions / 32 platforms with 54 add-on acquisitions and 16% IRR since inception. Most recent transaction: acquired Grand Equipment Company (Hudsonville MI construction equipment distributor across Western Michigan) October 2 2025 from Cognitive Capital Partners; Houlihan Lokey advised Strength on the buy-side and TM Capital advised Cognitive on the sell-side; PNC Bank, Northcreek Mezzanine, Longwater, and IBC Funds provided financing.

Why founders pick them: Detroit-area founders selling to a PE buyer pick Strength Capital when they want a buyer who will partner on long-term build-out (54 add-ons across 32 platforms = clear roll-up strategist), keep management in place, and finance growth from a Midwest LP base.

12. EdgePoint Capital Advisors — Beachwood OH Detroit Coverage

EdgePoint Capital Advisors (2000 Auburn Drive Suite 330, Beachwood OH 44122 single office, founded 2000) covers Detroit cross-border from its Cleveland-area base. Deal-size band $10M-$100M EV (lower-middle market); 181+ deals per Mergr. Recent senior hires: Chuck Aquino joined as Managing Director, Business Services January 2024; Tom Stafford also joined as Managing Director.

Sector focus: industrials (largest practice), distribution, transportation, business services, healthcare. Representative deals include Thor Precision, Inc. acquired by STAR Turbine (Mangrove Equity Partners portfolio company) — EdgePoint exclusive financial advisor.

Why founders pick them: Detroit-area founders selling industrial / transportation / distribution businesses pick EdgePoint when they want Cleveland-based fee economics (15-20% lower than Detroit boutiques) plus a Midwest-rolodex sale process. Best fit when founder is open to Ohio / Indiana / Western PA buyers as well as Michigan.

13. Amherst Partners — Birmingham Diversified Mid-Market

Amherst Partners (255 E Brown Suite 120, Birmingham MI 48009, founded 1994 by Scott Eisenberg co-founder) is a 14-professional diversified middle-market boutique. Deal-size band $10M-$150M EV; 36 total deals as of June 2025. Long-time member of IMAP (the world's largest M&A advisor network) — giving the firm cross-border buyer access disproportionate to its 14-person size.

Sector focus: automotive, building materials, business services, consumer, retail, food/beverage, financial services, healthcare, industrials, IT, software, transportation.

Why founders pick them: Smallest-shop discretion for $20M-$100M deals — 14 professionals means the senior MD actually runs the process (no junior-banker hand-off). IMAP network gives surprising international buyer reach for a 14-person Birmingham shop.

14. FINNEA Group — Birmingham Restructuring + M&A + FP&A

FINNEA Group (Birmingham MI, founded May 2011 by combining three predecessor firms: Leuliette Partners + LonePine Capital Advisors + The Novak Group) is the only Detroit shop where the same banker can advise on M&A execution AND restructuring / turnaround / FP&A consulting simultaneously. The four co-founders bring distinct depth:

- Jim Klunk (Senior Managing Director) founded LonePine Capital Advisors prior; 25+ years M&A / valuations / capital markets; MBA from Ross Michigan; began at Ernst & Young Corporate Finance 1996, later Macquarie Capital USA.

- Tim Leuliette (Senior Managing Director) — auto industry veteran (Iacocca era through Visteon CEO); 43+ year career.

- Tom McDonald (Senior Managing Director) — 30+ years investment banking / corporate finance; formerly Macquarie Capital (USA).

- Joe Novak (Senior Managing Director) — founded The Novak Group (restructuring boutique); leads FINNEA's Restructuring + FP&A practices; 25+ years operational / financial / strategic consulting.

Deal-size band $10M-$200M EV. Especially strong in distressed industrial / auto. Per PRNewswire 121882818, the May 2011 founding combined the three predecessor firms specifically to address the simultaneous M&A + restructuring + FP&A need that Detroit Tier-2 supplier founders consistently face.

Why founders pick them: When the Detroit auto Tier-2 founder is BOTH considering a sale AND facing covenant pressure / restructuring decisions, FINNEA is the only Detroit shop that can advise on M&A and restructuring simultaneously with the same banker. Tim Leuliette's auto-industry depth (former Visteon CEO) is unique.

Sector deep-dives

Auto / Mobility — Stellantis €22.2B Cascade + Tier-2 Roll-Up

The Detroit auto / mobility cluster fragments into three sub-segments: OEM-direct M&A, Tier-1 / Tier-2 supplier consolidation, and mobility tech (autonomous, EV, software).

OEM-direct: Stellantis (Auburn Hills HQ) announced ~€22.2B in charges for H2 2025 on February 6 2026, largely reflecting "the cost of over-estimating the pace of the energy transition" per the 6-K filing. General Motors (Detroit Renaissance Center HQ) continues to consolidate its mobility / autonomous portfolio post-Cruise integration. Ford (Dearborn HQ) is running active EV-bet rationalization.

Tier-1 / Tier-2 supplier deals 2024-2026:

| Date | Buyer | Target | Value | Advisors |

|---|---|---|---|---|

| Apr 15 2025 (close) | ABC Technologies (Apollo / Oaktree-backed) | TI Fluid Systems | £1.83B / ~$2.4B EV | Lazard (lead to ABC); Citi, TD Securities, Scotiabank (additional) |

| Jan 29 2025 (announce); closed Feb 3 2026; rebrand effective Jan 26 2026 | American Axle → Dauch Corporation | Dowlais Group plc | $1.44B cash-and-stock | J.P. Morgan + J.P. Morgan Cazenove (sole to AAM) |

| 2024 | Detroit Manufacturing Systems → Voltava | Android Industries + Avancez | Undisclosed | Lincoln International (Houlihan also referenced; verify primary) |

| Oct 2 2025 (close) | Strength Capital Partners | Grand Equipment Company | Undisclosed | Houlihan Lokey (buy-side); TM Capital (sell-side) |

| Jul 1 2024 | AMI Industries | Fluid Handling Technology Inc. | Undisclosed | Donnelly Penman (exclusive sell-side) |

| Jul 1 2024 | OKE Group GmbH | Global Enterprises | Undisclosed | Donnelly Penman (exclusive sell-side to Global) |

| Jul 25 2024 | The Shyft Group | Independent Truck Upfitters | Undisclosed | Donnelly Penman (exclusive to Shyft) |

| 2024 | Lock Joint Tube affiliate | JEMS of Litchfield | Undisclosed | Donnelly Penman (exclusive sell-side) |

| 2025-2026 (in process) | Various global investment firms | Magna International Lighting + Rooftop Systems | ~$1.1B aggregate 2025 sales | (TBD per Magna disclosure) |

Why Detroit matters in auto M&A: Stellantis + GM + Ford anchor a 4-state Midwest supplier ecosystem; the Detroit-metro Tier-2 buyer pool is concentrated within 30 miles of the Renaissance Center; ABC Technologies' rebrand to TI Automotive (Auburn Hills HQ, $5.4B revenue, 34,600 employees across 26 countries) plus AAM's rebrand to Dauch Corporation (NYSE: DCH from Feb 5 2026) re-shapes the strategic-buyer set.

Mortgage / Fintech — Rocket-Mr. Cooper Template

Detroit is the second-largest US mortgage / consumer-credit M&A advisory hub by per-capita advisory volume after NYC. Rocket Companies (NYSE: RKT, Renaissance Center) closed the $14.2B equity-value acquisition of Mr. Cooper Group on October 1 2025 — the largest independent mortgage deal in US history. J.P. Morgan advised Rocket; Citigroup advised Mr. Cooper. Rocket separately acquired Redfin (announced March 10 2025; closed July 1 2025; 63% premium over 30-day VWAP; Morgan Stanley advised Rocket; Goldman Sachs advised Redfin).

Ally Financial (Detroit HQ) is in active divestiture mode: $2.3B credit card business sold to CardWorks / Merrick Bank (agreement announced January 22 2025, closed April 1 2025; J.P. Morgan advised Ally); separately, Ally Lending point-of-sale financing business divested to Synchrony Financial (~$2.2B receivables, early 2024); Ally exited mortgage origination January 2025.

Why Detroit matters in mortgage M&A: Per-capita advisory volume now exceeds NYC for sub-$5B mortgage / servicing / fintech mandates. The bracket banks running Detroit mortgage deals (JPM, Citi, Morgan Stanley, Goldman) operate from Chicago / NY desks; Detroit founders should ask which senior MD has done a Rocket-adjacent or Ally-adjacent deal in the last 24 months.

Defense-Industrial — Sterling Heights / Warren Corridor

BAE Combat Vehicles Sterling Heights and General Dynamics Land Systems (GDLS) Sterling Heights are the only two US tracked-vehicle assembly plants. 2025 BAE Sterling Heights ACV-30 contract awards: $184M for 30 turreted amphibious combat vehicles + $181M for 31 ACV medium-caliber cannon variants (representing 5% of ACV-30 work share). Northrop Grumman Mission Systems, L3Harris, and Raytheon all have Detroit-area engineering presence.

Why Detroit matters in defense-industrial M&A: Section 232 (steel/aluminum) + Section 301 (China-origin) tariffs effectively block foreign-origin tracked-vehicle components from the supply chain — driving Tier-2/3 onshoring M&A multiples elevated through 2026-2028. The Detroit boutique with the deepest A&D bench is Angle Advisors (Birmingham; A&D is a named specialty). For mandates above $100M EV requiring DCAA / DCMA / FCL workflows, layer Angle with Houlihan Lokey industrials or Lincoln International.

Healthcare — Corewell + Henry Ford-Ascension

Two simultaneous integrations are reshuffling Michigan's hospital-system buyer pool. Corewell Health (the February 1 2022 Beaumont Health + Spectrum Health merger; HQ Grand Rapids MI post-merger but Southfield retains Beaumont-brand campuses) is the largest Michigan system at 22 hospitals and ~64,000 employees with ~$200M annual synergy capture (per Fierce Healthcare JPM24 coverage). Henry Ford Health and Ascension Michigan closed a $12B joint venture (HFH 80% / Ascension 20%) on September 30 2024, integrating 8 Ascension Michigan hospital campuses and ~17,000 employees into HFH's system — meaningfully reducing (but not eliminating) Ascension Michigan as an independent regional acquirer given the retained 20% ownership stake.

The Detroit-metro healthcare sell-side cadence: Cascade Partners advised DeGarA / American Physician Partners October 2023 (Cascade sell-side); Cascade also ran First Care Medical / Advanced Spine & Rehabilitation 2024 buy-side. DaVita Integrated Kidney Care risk-arrangement model (62,100 patients = $5.2B annualized medical spend as of March 31 2025) is the dialysis-adjacent strategic-buyer reference outside Michigan systems.

Why Detroit matters in healthcare M&A: The Corewell Spinout Cycle creates a 5-year downstream sell-side pipeline for sub-$50M EV Detroit-metro healthcare services. Cascade Partners is the most-cited Michigan healthcare M&A boutique; for tax-integrated valuation + sell-side prep work pair with Cendrowski Corporate Advisors.

Family Office + Tax-Driven Migration

Michigan's 6% flat corporate income tax + Detroit city income tax (2.4% resident / 1.2% non-resident) + property tax stack drives Detroit-headquartered owner-operators toward sell-before-relocate patterns. Florida / Nevada / Texas / Tennessee / Wyoming migration is the canonical post-close sequence — typically a 24-36 month effort to establish residency before the eventual close. Tax-integrated advisors (PMCF, Plante Moran, Cendrowski Corporate Advisors) coordinate the residency planning with the IB execution.

Proprietary frames

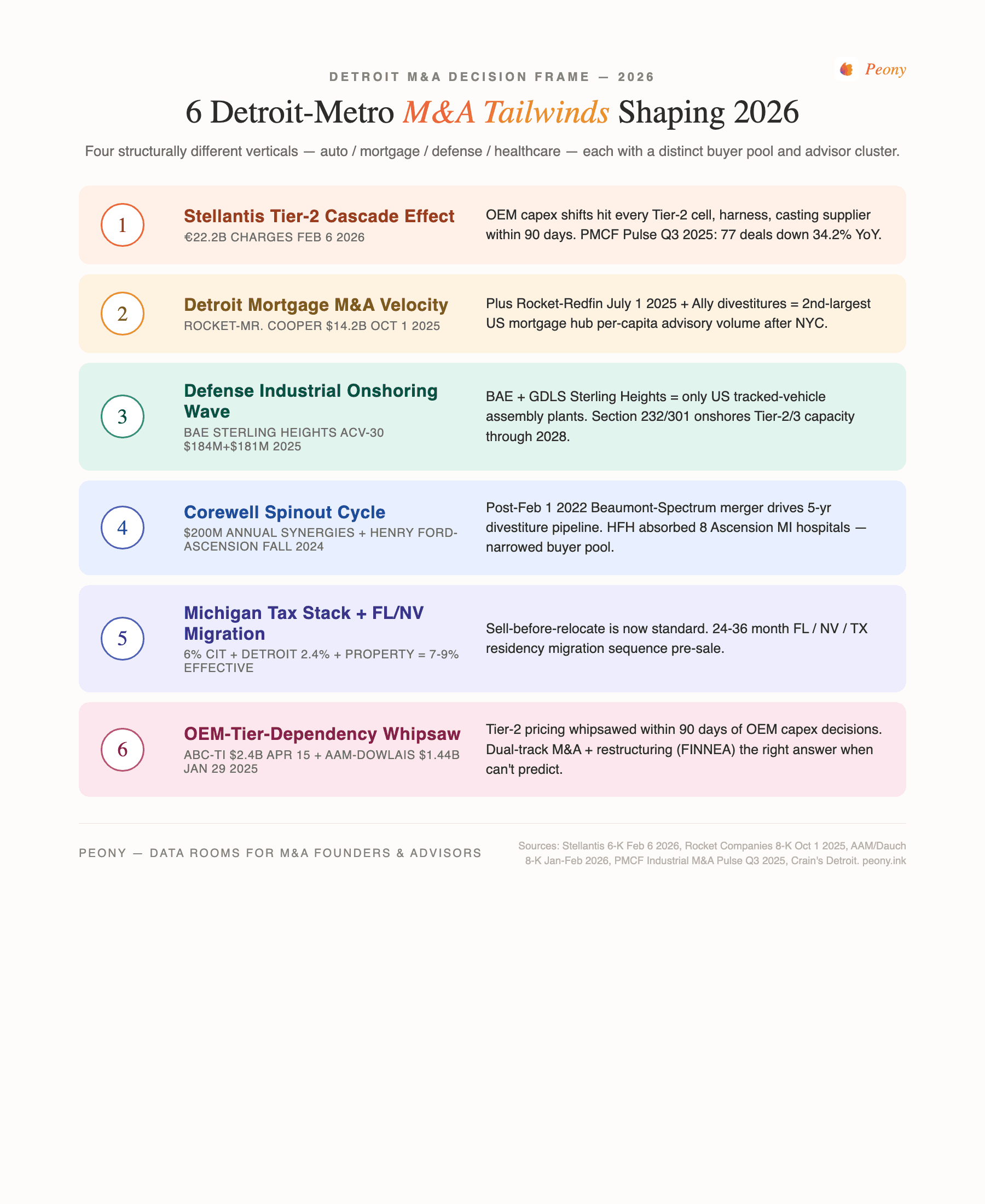

Frame 1: Stellantis Tier-2 Cascade Effect

When an OEM the size of Stellantis books €22.2B in H2 2025 charges, the cascade through every Tier-2 supplier — cells, harnesses, castings, optronics, propellant subsystems — hits within 90 days. Stellantis's February 6 2026 disclosure ("the cost of over-estimating the pace of the energy transition") is the canonical 2026 forward-cycle indicator: ICE Tier-2 capacity will continue to rationalize while EV-adjacent Tier-2 capacity faces multiple compression as the OEMs reset assumptions. PMCF's Q3 2025 Industrial Manufacturing M&A Pulse (77 US transactions, down 34.2% YoY from 117 in Q3 2024) confirms the cascade is already visible in transaction counts.

Founder action: For $30M-$150M revenue Detroit Tier-2 founders, the binary 2026 decision is sell NOW (Q2-Q3 2026) at partial multiple compression OR wait 12-18 months with covenant risk if you carry variable-rate debt. Advisors with OEM corp-dev rolodexes (Donnelly Penman, Angle Advisors, Lincoln Auto & Mobility) outperform generalists on these mandates.

Frame 2: Detroit Mortgage M&A Velocity

Rocket Companies' two 2025 mega-deals ($14.2B Mr. Cooper closed October 1 2025; Redfin closed July 1 2025) plus Ally Financial's active divestiture cycle establish Detroit as the second-largest US mortgage / consumer-credit M&A advisory hub by per-capita volume after NYC. The advisor pool routes through national bracket banks (JPM, Citi, Morgan Stanley, Goldman) operating from Chicago / NY desks — but the per-capita deal density means Detroit-area mortgage / fintech founders raising sub-$500M EV exits have unusual depth of competitive bidder interest.

Founder action: For $20M-$200M EV mortgage / fintech / consumer-credit sell-sides, ask each pitching bank which senior MD has done a Rocket-adjacent or Ally-adjacent deal in the last 24 months, and which GSE / FHA / VA agency rolodex they actually have versus claim.

Frame 3: Defense Industrial Onshoring Wave

BAE Combat Vehicles Sterling Heights + GDLS Sterling Heights are the only two US tracked-vehicle assembly plants. The Section 232 (steel/aluminum) + Section 301 (China-origin) tariff regime effectively onshores Tier-2/3 supplier capacity — meaning component suppliers in transmission cases, armor plate, optronics, propellant subsystems, harness assemblies, and avionics integration face elevated M&A multiples through 2026-2028 as primes and PE roll-up platforms compete for capacity.

Founder action: Detroit-area $15M-$100M defense-industrial Tier-2 founders should run a 2026-2027 process while multiples are elevated. Specialist advisor: Angle Advisors (Birmingham A&D). For DCAA / DCMA / FCL clearance work, layer with national defense banks.

Frame 4: Corewell Spinout Cycle

The February 1 2022 Beaumont-Spectrum merger that created Corewell Health continues to produce ~$200M annual synergies — and synergy capture at that scale creates a downstream 5-year divestiture pipeline of non-core service lines, real estate, and physician practice JVs. Combined with Henry Ford Health's Fall 2024 acquisition of 8 Ascension Michigan hospitals, the Michigan strategic-buyer pool for sub-$50M EV healthcare services sellers narrows materially.

Founder action: Detroit-metro healthcare services founders at $10M-$80M EV face a narrowed Michigan-system buyer pool (Corewell, HFH, Trinity, Ascension residual) plus PE roll-up platforms. Engage Cascade Partners (Rajesh Kothari) for sector-specialist sell-side execution.

Frame 5: Michigan Tax Stack + FL/NV Migration

Michigan's 6% flat CIT + Detroit 2.4% city tax + property tax stack adds 7-9% effective state + local burden on net proceeds for $20M-$200M EV sellers. The 24-36 month pre-sale Florida / Nevada / Texas / Tennessee / Wyoming residency migration sequence is now standard practice for Detroit-area founders — but requires careful Michigan Department of Treasury risk management.

Founder action: Engage tax-integrated advisors (PMCF, Plante Moran, Cendrowski Corporate Advisors) 24-36 months pre-sale to coordinate residency planning with eventual IB execution. Cendrowski's Bloomfield Hills HQ post-August 2024 Prosperity Partners acquisition retains Harry Cendrowski as Managing Partner — continuity matters for multi-year planning.

Frame 6: OEM-Tier-Dependency Whipsaw

Tier-2 supplier M&A pricing is whipsawed by OEM capex decisions within 90 days. The pattern: OEM announces capex shift → Tier-1 reprices supplier contracts within 30-45 days → Tier-2 covenant pressure shows up within 60-90 days → Tier-2 M&A multiples reset within 90-120 days. When you can't predict whether to push for sale OR negotiate covenant relief, dual-track M&A + restructuring becomes the right answer.

Founder action: FINNEA Group is the only Detroit shop where the same senior team can advise on M&A AND restructuring in parallel — Tim Leuliette's former-Visteon-CEO depth plus Joe Novak's restructuring book (Novak Group lineage) creates uniquely flexible dual-track capability. Houlihan Lokey is the national alternative for $100M+ EV distressed Tier-2 mandates given the #1 global Chapter 11 restructuring book.

FAQ

What's the difference between a Detroit M&A boutique and a bulge-bracket bank like Goldman or Morgan Stanley for a $50M sell-side?

For Detroit-metro sellers in the $5M-$500M EV band, the structural difference is amplified by Detroit's four-vertical specialization. Bulge-bracket banks are built around $200M+ engagements where senior MD time goes to the largest fee-payers; at $50M EV you get VP and associate staffing with senior MD only on kickoff. Detroit-anchored boutiques (Donnelly Penman, Angle Advisors, Cascade Partners) are built around the $5M-$500M EV band where senior bankers run buyer calls personally. Houlihan Lokey sits in a useful middle position with no standalone Detroit office (Auto Mobility group runs from Chicago/NY) but topped both 2024 auto M&A tables per Just-Auto plus carries the #1 global Chapter 11 restructuring book — critical for distressed Tier-2 work post-Stellantis-€22.2B cascade.

I'm a Detroit Tier-2 auto supplier founder — how does the Stellantis €22.2B charges announcement change my sell-side timing in 2026?

See Frame 1 above. Stellantis announced ~€22.2B in H2 2025 charges on February 6 2026 reflecting energy-transition pace over-estimate. The Tier-2 Cascade Effect: OEM capex shifts hit every cell, harness, and casting supplier within 90 days. Binary 2026 decision: sell now at partial multiple compression OR wait 12-18 months with covenant risk. Donnelly Penman (4 confirmed 2024 closes), Angle Advisors (Birmingham A&D + auto), Lincoln International (Chicago Auto & Mobility), and FINNEA Group (dual-track M&A + restructuring) cover the Tier-2 sell-side pool. Before launching, prepare a defensible sell-side QoE + customer concentration package per the sell-side due diligence playbook — buyers in the cascade window will reprice on any weak DD signal, so the operational DD workstream matters more than usual.

Which Detroit advisors handled the Rocket Companies-Mr. Cooper $14.2B mortgage deal — and what does that tell me about Detroit mortgage M&A capacity?

Rocket closed the $14.2B equity-value Mr. Cooper acquisition October 1 2025 (announced March 31 2025 at $9.4B equity; gap reflects RKT share appreciation). J.P. Morgan advised Rocket; Citigroup advised Mr. Cooper. Rocket-Redfin (closed July 1 2025) was Morgan Stanley to Rocket / Goldman Sachs to Redfin. Detroit is now the second-largest US mortgage / consumer-credit M&A hub by per-capita volume after NYC. Mortgage / fintech sell-sides route through these national bracket banks via Chicago / NY desks.

I'm a defense-industrial Tier-2 supplier near BAE Sterling Heights or GDLS — how does the Section 232/301 onshoring wave change my M&A timing?

See Frame 3 above. BAE Combat Vehicles Sterling Heights + GDLS Sterling Heights are the only two US tracked-vehicle assembly plants. The 2025 BAE Sterling Heights ACV-30 contract awards ($184M + $181M) anchor a multi-year DoD program backed by tariffs that onshore Tier-2/3 supplier capacity. Multiples elevated through 2026-2028. Angle Advisors is the default Detroit boutique pick; layer with Houlihan Lokey or Lincoln International for $100M+ EV mandates requiring DCAA / DCMA / FCL workflows.

I'm a Detroit healthcare services founder — how do the Corewell post-merger divestiture cycle and Henry Ford Health's Ascension acquisition change my buyer pool?

See Frame 4 above. Corewell's Feb 1 2022 Beaumont-Spectrum merger produced ~$200M annual synergies and a 5-year divestiture pipeline. Henry Ford Health and Ascension Michigan closed a $12B joint venture September 30 2024 (HFH 80% / Ascension 20%) integrating 8 Ascension Michigan hospital campuses + ~17,000 employees — meaningfully reducing Ascension's standalone Michigan footprint without fully eliminating it given the 20% retained stake. Combined effect: narrowed Michigan strategic-buyer pool for sub-$50M EV healthcare services sellers. Cascade Partners (Rajesh Kothari) is the most-cited Michigan healthcare M&A boutique.

How does the Michigan Tax Stack work — and what does the FL/NV/TX migration pattern mean for my $50M Detroit sale planning?

See Frame 5 above. Michigan 6% flat CIT + Detroit 2.4% city + property = 7-9% effective state + local burden on net proceeds for $50M EV sellers. 24-36 month pre-sale FL / NV / TX residency migration is standard. Tax-integrated advisors (PMCF, Plante Moran, Cendrowski Corporate Advisors post-Aug 2024 Prosperity acquisition) coordinate residency planning with IB execution.

TD Cowen acquired Quarton in 2019 then TD Securities acquired Cowen in 2023 — is the Birmingham MI office still operational?

Birmingham MI office status post-2023 integration is unverified — likely consolidated into broader TD Securities NYC footprint. The cross-border value proposition (Quarton International's 500+ pre-acquisition transactions in 30 countries) still exists through the TD Securities platform. For authentic Birmingham-resident senior-MD attention with European cross-border buyer access, Amherst Partners (founded 1994 by Scott Eisenberg, IMAP network member) is the closer like-for-like alternative.

When is FINNEA Group's simultaneous M&A + restructuring capability the right choice?

See Frame 6 above. FINNEA is the only Detroit shop where the same banker can advise on M&A AND restructuring with the same senior team. Tim Leuliette's former-Visteon-CEO operating perspective + Joe Novak's Novak Group restructuring lineage make FINNEA uniquely flexible in OEM-Tier-Dependency Whipsaw scenarios. Use FINNEA when you can't predict whether to push for sale or negotiate covenant relief and want to run both tracks in parallel.

What's a reasonable success fee for a $50M Detroit M&A sell-side mandate?

1.5%-2.5% blended success fee + $50K-$150K retainer + 12-24 month tail. Standard Lehman (5/4/3/2/1) = ~1.4% blended on $50M = $700K floor. Auto Tier-2 specialists (Donnelly Penman, Angle Advisors): 2.0-2.75% blended. Healthcare (Cascade Partners): 2.0-2.75% blended. Defense (Angle + Houlihan Lokey): 2.5-3.5%. Dual-track M&A + restructuring (FINNEA Group): hybrid $200K-$500K flat + 1.0-1.5% transaction value. Peony Business at $30 per admin per month replaces $15K-$50K per-deal data room expense.

I get inbound calls from Stellantis / GM / Ford corp-dev a few times a year — should I take the call directly or run through a Detroit advisor?

Take the call but never sell off it. Inbound IOIs after screening calls are structurally below competitive-process pricing. Log the inbound, ask qualifying questions, don't share financials, engage a Detroit sell-side advisor (Donnelly Penman / Angle Advisors for auto Tier-2; PMCF for diversified industrial; Cascade Partners for healthcare; Houlihan Lokey / Lincoln International for $100M+ cross-border). Route the inbound into your eventual process as one of 8-15 qualified buyers.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Detroit shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- M&A due diligence process guide — master DD framework

- Sell-side due diligence — preparing for buyer scrutiny

- Operational due diligence — operations + supply chain workstream

- HR due diligence — people-side workstream

- M&A data room checklist — what your data room should contain

- Best data room for a small M&A deal — picking a right-sized VDR for a sub-$30M sale, the band most Detroit-metro Tier-2 and family-office sell-sides start in

- Due diligence timeline — week-by-week DD critical path

- Hard vs soft due diligence — integration-risk pair

- Sibling city posts: NYC · LA · SF · Chicago · Boston · Houston · Dallas · Atlanta · Minneapolis · Nashville · Denver · Austin · Cleveland · Columbus · Cincinnati · Pittsburgh · Indianapolis