8 Best M&A Advisors in Baltimore for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led exits, family-business successions, PE recapitalizations, and strategic carve-outs — and Baltimore is the entry in our M&A advisor series where history sets the sharpest trap. Most "best Baltimore M&A advisors" pages fail a simple function test: they rank the city's famous money brands as if they sold companies (one AI-generated "top investment banks in Baltimore" list currently features Fidelity, Morgan Stanley, Truist — and Legg Mason, a firm that ceased to exist as an independent company in July 2020), they never mention that the most storied name in American investment banking is now a wealth-management sign, and they cannot tell you which of the surviving boutiques actually holds a FINRA registration. At Peony we now serve more than 5,900 customers, and Baltimore sits squarely in the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark.

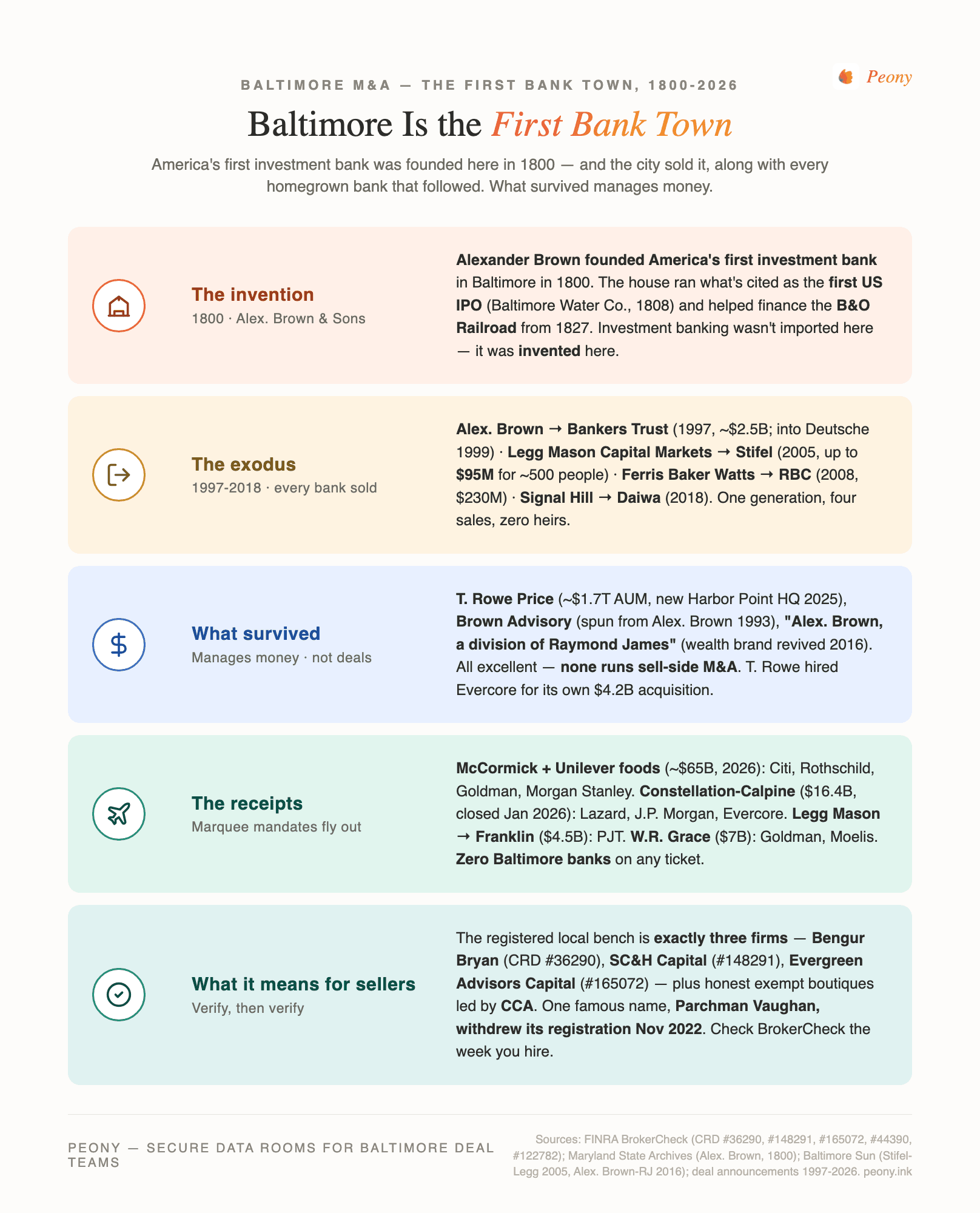

Here is the thesis I want you to internalize before you read another word: Baltimore is the First Bank Town. The American investment bank was invented here — Alexander Brown hung out his shingle in 1800, ran what is generally cited as the first initial public offering in US history (the Baltimore Water Company, 1808), and his sons' house helped finance the B&O Railroad from 1827. For nearly two centuries the city kept a genuine homegrown bench: Alex. Brown & Sons, Legg Mason's capital-markets arm, Ferris Baker Watts (founded 1900). And then, in the span of one generation, Baltimore sold all of it. Alex. Brown went to Bankers Trust in 1997 (~$2.5B in stock by closing) and disappeared into Deutsche Bank in 1999. Legg Mason swapped away its brokerage and sold its capital-markets unit — roughly 500 people — to St. Louis-based Stifel in December 2005 for up to $95 million, a rounding error that became the chassis of Stifel's national institutional business. Ferris Baker Watts went to RBC in 2008 for $230M and the name was retired. Signal Hill Capital, the tech boutique that Alex. Brown veterans founded in 2002 to keep the flame, was absorbed into Daiwa's DC Advisory in 2018. Even the quiet tail continues: Parchman Vaughan, the education-sector boutique founded by Ferris Baker Watts alumni in 1996, withdrew its broker-dealer registration in November 2022.

What survived is remarkable — but it manages money instead of selling companies. T. Rowe Price (founded Baltimore, 1937) runs ~$1.7 trillion and opened a new Harbor Point headquarters in March 2025. Brown Advisory, spun out of Alex. Brown in 1993 and independent via employee buyout in 1998, is a premier wealth and institutional investor. The "Alex. Brown" brand itself was revived in 2016 — as the name of Raymond James's high-net-worth wealth division. The city that invented the sell-side now has, by my count, exactly three FINRA-registered M&A broker-dealers headquartered in the metro, and its marquee corporate mandates — McCormick's ~$65B combination with Unilever's foods business announced this March, Constellation's $16.4B Calpine acquisition closed in January — are run by Citi, Rothschild, Goldman Sachs, Morgan Stanley, Lazard, J.P. Morgan, and Evercore from conference rooms in Hunt Valley and Harbor Point.

That is not a sad story — it is a structural one, and it changes how you should sell a company here. It means brand recognition is actively misleading: the names your neighbors know manage wealth, and the firms that will actually sell your company are ones most owners have never heard of. It means verification does unusual work — the registered bench is three firms, one famous local name is quietly deregistered, and the difference matters the moment your deal involves stock. It means the one vertical where the metro genuinely owns a global table — the Fort Meade cyber corridor — plays by sector-specialist rules rather than local ones. And it means your buyer pool is national by necessity, with the good news being that the buyer engine is running: Constellation is the largest US power producer and restarting Three Mile Island on Microsoft's tab, the Port just posted its second-best year ever and broke ground on a $1.2B container terminal at the old Bethlehem Steel site, and a $65B flavor giant is being assembled in Hunt Valley. This post is the working playbook I would hand to a Baltimore founder weighing a sale, a family-business owner weighing succession against an ESOP, or a corridor cyber CEO fielding inbound interest. The frames come from cross-referencing FINRA BrokerCheck, SEC filings, and the verified 1997-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in Baltimore right now for $5M-$300M deals?

My ranked list for lower-middle-market and middle-market sellers, with the reasoning below:

- Chesapeake Corporate Advisors (CCA) — Harbor East, Baltimore. The most-cited homegrown generalist boutique; founded 2005 by Charlie Maskell; the firm reports 150+ closed transactions; December 2025 marquee: exclusive financial advisor to Burns Engineering in its sale to OceanSound Partners. Non-registered (federal M&A-broker exemption) — fine for most asset/LLC deals; confirm structure fit.

- Bengur Bryan & Co. — Baltimore (Harbor East). The metro's longest-standing registered boutique — FINRA CRD #36290, registered since 1991. Transportation, logistics, industrial, business services; recent closings: Trans/Air Manufacturing → Lippert (March 2025), First Source Electronics → Woodson Equity (October 2024), Dillon Transportation → TFA Logistics (September 2025).

- Evergreen Advisors Capital — Columbia. Registered broker-dealer (CRD #165072; parent firm founded 2001 by Rick Kohr). Growth-company and middle-market coverage on the Baltimore-Washington corridor; recent: Ultimate CNG → Critical Infrastructure Holdings (February 2024).

- SC&H Capital — Columbia/Sparks. Registered broker-dealer (CRD #148291), affiliated with accounting firm SC&H Group. The metro's ESOP and special-situations specialist — Kitware ESOP (May 2024), Wise Consulting → RSM (September 2024). If employee ownership or a distressed/accelerated process is on your menu, start here.

- National Security Capital Advisors (NSCA) — Columbia. The genuine in-corridor national-security merchant bank: founded 2014, targets $10M-$100M-revenue defense/intel/cyber companies, advisory bench of former senior national-security officials. Non-registered.

- Charlesmead Advisors — Baltimore. Telecom and broadband-infrastructure specialist founded by Michael Balhoff, the 16-year head of Legg Mason's telecom equity research — living Legg diaspora. Securities run through BA Securities (a third-party broker-dealer of record) — a properly disclosed hybrid model.

- Parchman Vaughan & Company — Baltimore. The education and workforce-training specialist, founded 1996 by Ferris Baker Watts alumni. Real domain authority — but its FINRA broker-dealer registration (CRD #44390) was withdrawn in November 2022, so it now operates non-registered; structure a securities-based deal accordingly.

- Stifel (Baltimore office) — the bank-owned platform with genuine local lineage: Stifel's 2005 purchase of Legg Mason Capital Markets made Baltimore an institutional home for the St. Louis bank (CRD #793), now consolidating into Harbor Point. For deals climbing past ~$100M, it is the one full-service bank with a real Baltimore capital-markets footprint — and it co-advised (with Piper Sandler) on ZeroFox's $350M take-private, the closest thing to a marquee hometown ticket since 1997.

National names cover Baltimore from elsewhere — Houlihan Lokey, William Blair, Piper Sandler, Guggenheim, Raymond James's defense-and-government team, Lincoln International, Harris Williams — and for specific verticals they are often the right call; the deal receipts below show exactly when. Sub-$5M Main-Street sales are business-broker territory, not this list.

Why is Baltimore the "First Bank Town" — and why does that change how I sell?

Because in Baltimore, the prestige layer and the execution layer split apart a generation ago, and sellers who don't know the history hire the wrong layer.

The prestige layer is real history. Alexander Brown, an Irish linen merchant, founded Alex. Brown & Sons in 1800 — the first investment bank in the United States. The house underwrote what is generally cited as the first US IPO (Baltimore Water Company, 1808); George Brown, Alexander's son, was the founding treasurer of the B&O Railroad, which the family helped finance from 1827. Baltimore did not participate in the invention of American investment banking — Baltimore was the invention. Add Legg Mason (lineage to 1899), Ferris Baker Watts (1900), and T. Rowe Price (1937), and for most of the 20th century the city had a bench most non-New York metros would envy.

The execution layer left in four sales and one swap:

| Year | What happened | Where it went | What it fetched |

|---|---|---|---|

| 1997 | Alex. Brown & Sons sold | Bankers Trust (→ Deutsche Bank, 1999) | ~$1.7B announced; ~$2.5B in stock by close |

| 2005 | Legg Mason swapped its brokerage to Citigroup for Citi's asset-management arm | Citigroup | ~$3.7B total swap |

| 2005 | Legg Mason Capital Markets (the investment bank, ~500 people) sold by Citi | Stifel (St. Louis) | Up to $95M |

| 2008 | Ferris Baker Watts (founded 1900) sold | RBC; name retired | $230M |

| 2018 | Signal Hill Capital (founded 2002 by Alex. Brown veterans) absorbed | Daiwa's DCS/DC Advisory | Undisclosed |

Read that middle row twice, because it is the thesis in one line: in 2005, the operating investment bank of Baltimore's flagship financial firm — research, trading, banking, 22 offices — changed hands for less than one-hundredth of what Franklin later paid for Legg Mason's asset-management business ($4.5B, 2020). Baltimore kept the part that manages money and sold the part that sells companies. Every year since has compounded that choice: the asset managers grew into giants (T. Rowe at ~$1.7 trillion), and the deal bench shrank to a handful of boutiques.

For a seller, three practical consequences:

First, famous ≠ relevant. The financial brands with Baltimore name recognition — T. Rowe Price, Brown Advisory, Alex. Brown — are the wrong doors for a sell-side, however excellent they are at their actual jobs. More below.

Second, the real bench is small, specialized, and verifiable. Three registered broker-dealers, a handful of honest exempt boutiques, one bank-owned office with true local lineage. That's the market. The upside of a short list: you can actually diligence all of it in a week.

Third, national reach is non-negotiable. The First Bank Town's own record proves buyers and banks come from out of town — so whichever local advisor you hire must demonstrate, with named closings, that its buyer outreach isn't regional. The good local firms know this and behave accordingly; the receipts sections below show you how to test it.

Is Alex. Brown still an investment bank in Baltimore?

No. The "Alex. Brown" you see today is "Alex. Brown, a division of Raymond James" — a wealth-management brand. When Deutsche Bank exited its US private-client business in 2016, Raymond James bought the unit and revived the storied name for its high-net-worth franchise (roughly 16 offices, ~600 employees, about 100 of them in Baltimore). It manages portfolios for wealthy families. It does not run sell-side M&A processes.

The confusion is understandable — the same sign once meant the most sophisticated deal shop in America — and it is worth knowing where the deal DNA actually went. When Bankers Trust and then Deutsche absorbed the firm, the M&A talent scattered into three streams: some stayed inside big banks; some founded investment firms (ABS Capital Partners was seeded by Alex. Brown itself in 1990, under former CEO Don Hebb; Brown Advisory spun out of the firm in 1993 and bought its independence in 1998); and some kept banking — Scott Wieler and other Alex. Brown veterans founded Signal Hill Capital in 2002, the closest thing Baltimore had to an heir. Signal Hill built a genuine tech-banking franchise and then it, too, was absorbed — into Daiwa's DC Advisory in 2018, its Baltimore registration ceasing that March. The lineage today survives in fragments: Brown Advisory manages wealth, ABS invests growth equity, Charlesmead's founder carries Legg Mason research DNA into telecom deals, and Stifel's Harbor Point office carries the Legg capital-markets chassis.

The generalizable rule this teaches: in Baltimore, check what a firm does today, not what its name did in 1900. BrokerCheck takes five minutes and settles it.

Can T. Rowe Price or Brown Advisory sell my company? The wealth-brand trap

No — they manage money, and the distinction is worth real dollars, so here is the clean version:

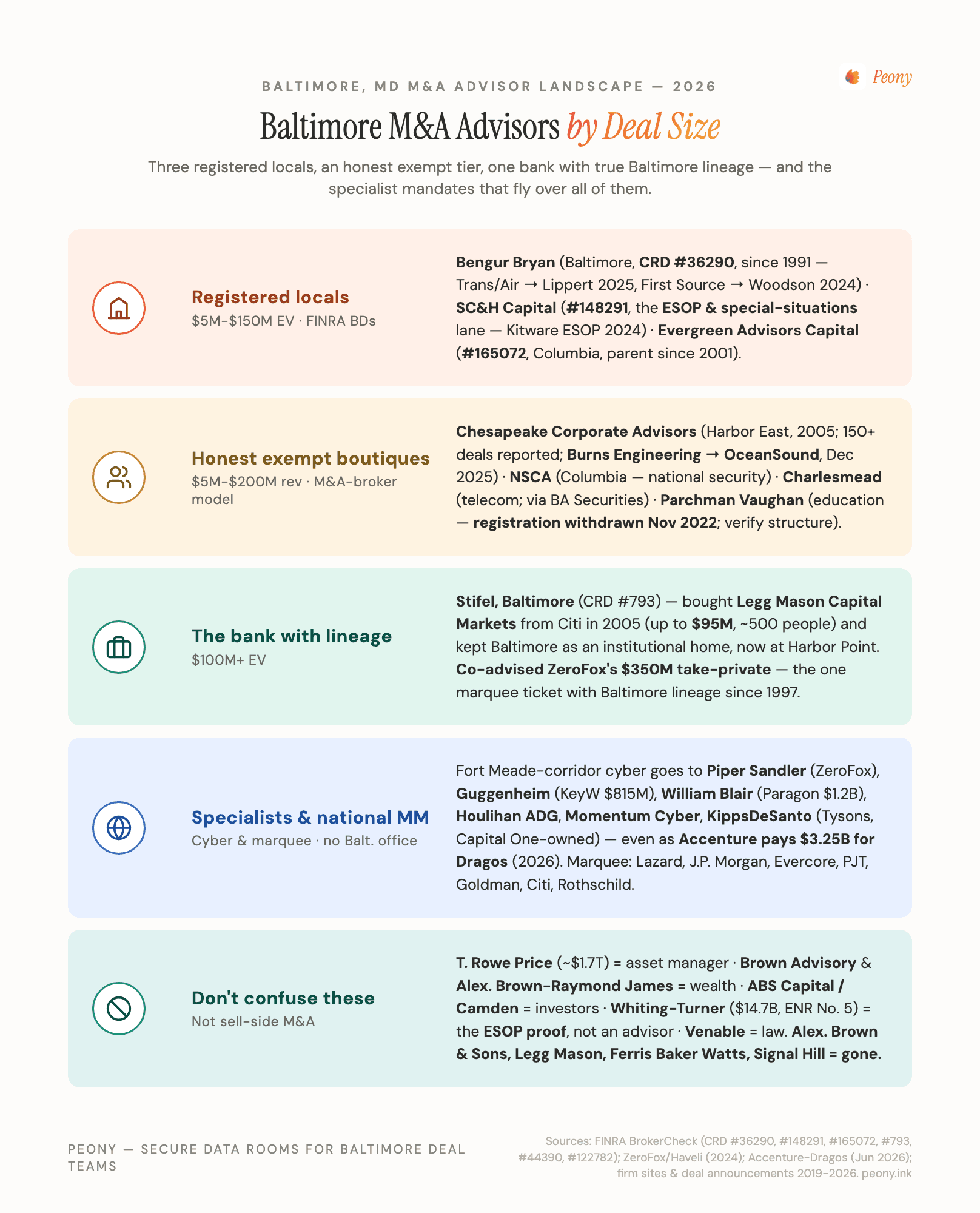

- T. Rowe Price (founded Baltimore 1937; ~$1.7 trillion AUM; moved into its new $278M Harbor Point headquarters in March 2025) is an asset manager. It runs mutual funds and retirement money. The tell: when T. Rowe itself wanted to buy Oak Hill Advisors for up to $4.2B in 2021, it hired Evercore — a New York bank — to advise it. The company whose name is on Baltimore's newest financial headquarters outsources its own M&A advice.

- Brown Advisory (spun out of Alex. Brown 1993; independent via employee buyout 1998) is a wealth and institutional investment firm — a superb one, and a genuine piece of Alex. Brown lineage. It is where sale proceeds go, not what produces them.

- Alex. Brown, a division of Raymond James — wealth management, as above.

- ABS Capital Partners and Camden Partners — growth-equity and private-equity investors. They might buy into your company; they will not run your sell-side. (One precision note, because listicles garble it: ABS is true Alex. Brown lineage — founded 1990 as the firm's investment arm under former CEO Don Hebb. Camden's founder David Warnock came out of T. Rowe Price, not Alex. Brown.)

- Legg Mason — does not exist. Franklin Resources acquired it for $4.5B in cash (announced February 2020, closed July 31, 2020) and retired the brand. Any list still naming Legg Mason as a Baltimore advisor was written by someone — or something — that has not checked in six years.

The division of labor that actually serves you: a registered M&A advisor or investment bank runs the competitive process; your wealth manager plans the proceeds. Sequence them — don't substitute one for the other. The sellers who walk into T. Rowe or Brown Advisory after a well-run auction walk in with a materially bigger number.

Which Baltimore M&A advisors are actually FINRA-registered broker-dealers?

Exactly three, by my BrokerCheck pull for this post — and each anchors a different lane:

Bengur Bryan & Co., Inc. — CRD #36290 — Baltimore (Harbor East). Registered since June 1991, which makes it the metro's longest-standing registered M&A boutique — it has now outlasted every famous name that was on the skyline when it opened. The lane: transportation and logistics, industrials, business services, consumer, with restructuring capability. The receipts are current, not archival: AboveAir Technologies → AirX Climate Solutions (July 2024), Commercial Vehicle Group's First Source Electronics unit → Woodson Equity (October 2024), Trans/Air Manufacturing → Lippert/LCI Industries (closed March 2025), Dillon Transportation → TFA Logistics (September 2025). For a founder-owned industrial, transport, or services company in the $10M-$150M band, this is the registered local flagship.

SC&H Capital — CRD #148291 — registered office Columbia; parent SC&H Group headquartered in Sparks. The broker-dealer arm of a regional accounting-and-advisory firm, formed 2004, and the metro's clear ESOP and special-situations specialist: Kitware's sale to its employee stock ownership plan (May 2024), Carpet & Wood Floor Liquidators → ESOP (March 2024), Wise Consulting Associates → RSM (September 2024). Practice founded by Christopher Helmrath, now co-led by Matthew Roberson and Gregory Hogan. If your exit menu includes employee ownership, a going-concern sale under time pressure, or a court-supervised process, this is the local bench built for it — see the ESOP section for why that menu is unusually relevant here.

Evergreen Advisors Capital — CRD #165072 — Columbia. The broker-dealer of Evergreen Advisors (parent founded 2001 by Rick Kohr; BD entity formed 2012), working the Baltimore-Washington corridor's growth and middle-market companies with both M&A and corporate-finance advisory; recent: Ultimate CNG → Critical Infrastructure Holdings (February 2024), aerospace/defense advisory work for QED Systems (2025). Positioned physically and practically between the Baltimore generalists and the DC-orbit government economy.

Why registration matters (the honest version, not the scare version): a broker-dealer registration governs who may transact securities — so if your deal is a stock sale, includes an equity rollover, or raises capital alongside the sale, a registered advisor (or a firm properly operating through a broker-dealer of record) keeps the structure clean. Since the SEC's 2023 codified M&A-broker exemption, smaller advisors may legally run many private-company sales without registration — which is why a zero result on BrokerCheck is not a scandal. It is, however, a structural fact about what your advisor may do, and you should know it before you sign the engagement letter, not after your buyer proposes a rollover. Ask every candidate: registered, exempt, or through whose broker-dealer? The good firms answer in one sentence.

Which honest non-registered boutiques anchor Baltimore's exempt tier?

Four names, each with a real lane — all operating legally without their own FINRA registration, which is exactly why you should hear the status from them directly:

Chesapeake Corporate Advisors (CCA) — Harbor East, founded 2005 by Charlie Maskell. The most-cited homegrown boutique and the closest thing the metro has to a default first call for a founder-owned company in the $10M-$200M-revenue band. Sector patterns across its record: engineering and construction services, government-adjacent services, healthcare services, IT. The firm reports 150+ closed transactions; the current marquee is exclusive financial advisor to Burns Engineering in its sale to OceanSound Partners (December 2025) — a Philadelphia-headquartered seller, which is itself evidence of reach beyond the harbor. Named local closings include Valley Lighting → Caymus Equity and Fireline → Encore Fire Protection.

National Security Capital Advisors (NSCA) — Columbia, founded 2014. A merchant bank purpose-built for the corridor: national-security, intelligence-community, and cyber companies with $10M-$100M revenue and $1M-$20M EBITDA, with an advisory network of former senior government officials for the buyer-credibility problem unique to this vertical. If your company sells into the Fort Meade economy and you want an advisor who does not need the acronyms explained, this is the local answer — with the honest caveat that the biggest corridor tickets still go to national specialists (receipts in the cyber section).

Charlesmead Advisors — Baltimore. The telecom and broadband-infrastructure specialist, co-founded by Michael Balhoff — who ran Legg Mason's Technology & Telecommunications equity research group for 16 years — and Bradley Williams. A precision instrument: if you own fiber, towers, rural broadband, or telecom services, sector fluency like this is exactly what the "specialist beats generalist" rule is about. Note the properly disclosed structure: securities products run through BA Securities, LLC, a third-party broker-dealer of record — the clean hybrid model, and a live example of Legg Mason DNA still doing deals in Baltimore.

Parchman, Vaughan & Company — Baltimore, founded April 1996 by alumni of Ferris Baker Watts. The education, training, and workforce-development specialist — genuinely rare domain authority, international buyer reach in a niche most banks ignore. And the metro's single most instructive verification lesson: the firm held FINRA registration for a quarter century, then withdrew it effective November 2022 (BrokerCheck shows CRD #44390 as no longer registered). The firm continues to advise — legally, under the exemption — but a directory that copied its 2021 description is now wrong about a fact that matters to deal structure. Check the registry the week you hire, not the year the list was written.

One more category deserves honest handling: hybrids and directory filler. Baltimore-Washington Financial Advisors (BWFA) is a wealth manager that also markets M&A services — if you engage a hybrid, ask exactly who runs the deal and through which broker-dealer. Smaller names that appear in directories (Tower Partners in Columbia, HighBank on the Eastern Shore, Trafalgar Capital Partners) may be perfectly good — apply the same two-question test: BrokerCheck status, and three named closings in your size band. And Chessiecap Securities (CRD #132153) is a real registered tech boutique, but it sits in Bethesda — the DC orbit, forty miles and a different economy away.

What is Stifel's Baltimore office — and is any national bank actually local?

Stifel is the one full-service investment bank with genuine Baltimore capital-markets lineage, and the story is the $95M row from the exodus table. When Citigroup ended up holding Legg Mason's capital-markets business after the 2005 swap, it sold the unit — research, institutional sales and trading, investment banking, roughly 500 associates across 22 offices — to St. Louis-based Stifel for up to $95 million including earnout. That acquisition is widely credited with transforming Stifel from a regional firm into a national one, and Baltimore has remained a core institutional hub ever since: the bank put its name on One South Street downtown and is now consolidating into new space at Harbor Point's Wills Wharf. (For the fuller Stifel story, our St. Louis guide covers the headquarters end of the same firm.)

What that means practically: for deals climbing past ~$100M, or where an industry group and balance-sheet capability start to matter, Stifel is the one bank where "national platform" and "real Baltimore presence" are both true. And it holds a distinction no other bank can claim: when Baltimore-headquartered ZeroFox went private with Haveli Investments for $350M in May 2024, Stifel co-advised the sell-side alongside Piper Sandler — the closest a Legg-descended Baltimore platform has come to a marquee hometown ticket since the 1997 Alex. Brown sale.

Beyond Stifel, be precise about what "in Baltimore" means: the national middle-market banks that show up on Maryland deals — Houlihan Lokey, William Blair, Piper Sandler, Guggenheim, Lincoln International, Harris Williams, Raymond James — cover the metro from New York, Chicago, Minneapolis, Tysons, and St. Petersburg. That is not a criticism; for specialist verticals it is exactly where the buyer relationships live. It just means "we know Baltimore" should be tested with named closings, the same as anyone else.

Who advises a cybersecurity or defense-adjacent sale in the Fort Meade corridor?

Baltimore's one globally significant deal vertical sits twenty minutes south of the harbor. NSA, US Cyber Command, and DISA are all headquartered at Fort Meade in Anne Arundel County — with a $500M+ joint Integrated Cyber Center on post — and the talent that rotates out has built the densest commercial-cyber cluster between New York and Northern Virginia: 2,100+ technology companies in Anne Arundel County alone, ~18,400 information-security analysts employed statewide (the country's deepest per-capita bench), and an institutionalized startup engine in DataTribe, the Fulton "cyber foundry" founded in 2016 by Mike Janke, Bob Ackerman, and Steven Witt that co-founds companies with NSA and national-lab alumni.

The outcomes are not hypothetical:

- Dragos (Hanover; industrial/OT security) — seeded by DataTribe with $1.2M in 2016; $200M Series D at $1.7B (2021); and in June 2026, Accenture agreed to acquire a majority stake at a $3.25B valuation in a bundle of deals worth ~$4.2B. A Fort Meade-alumni company became the anchor asset of a global consultancy's security platform.

- Tenable (Columbia;

$4B market cap) — the corridor's public company, and itself a serial acquirer: Ermetic ($265M, 2023), Eureka Security (2024), Vulcan Cyber ($147M, 2025). - ZeroFox (Baltimore City proper) — de-SPAC'd 2022, taken private by Haveli Investments at ~$350M (closed May 2024).

- Huntress (Ellicott City) — $150M Series D at a $1.5B+ valuation led by Kleiner Perkins (2024). Blackpoint Cyber (Ellicott City) — $190M from Bain Capital and Accel (2023). Sonatype (Fulton) — Vista Equity majority since 2019. Exits to strategics: Terbium Labs → Deloitte (2021), Bricata → OpenText (2021), KeyW (Hanover) → Jacobs ($815M, 2019).

Now the part that matters for a founder: look at the advisor names. ZeroFox's sell-side ran through Piper Sandler (Minneapolis) with Stifel co-advising; KeyW ran through Guggenheim (New York); Paragon Bioservices — the corridor-adjacent biotech CDMO — ran through William Blair (Chicago). The recurring banks in this vertical are Piper Sandler, Guggenheim, William Blair, Houlihan Lokey's aerospace-defense-government group, Raymond James's defense & government team, pure-play Momentum Cyber (Austin), and KippsDeSanto (Tysons — owned by Capital One since 2019). Not one is headquartered in Baltimore. The cyber capital of America, by workforce, imports its cyber bankers.

So the corridor playbook: for a commercial cyber product company (software, platform, recurring revenue), interview the sector specialists first — their buyer relationships at Accenture, Palo Alto, CrowdStrike, Thoma Bravo, and Vista are the price-setters — and use NSCA or a strong local generalist as the relationship-fit comparison. For a cleared government-services business (people-and-contracts, facility clearances), the specialist bench lives in the DC orbit, and the structural issues differ enough that we wrote a separate guide: Best M&A Advisors in Washington DC covers KippsDeSanto, the govcon tier, and cleared-deal mechanics. And whoever you hire: in a vertical where your most probable buyers employ your competitors' product teams, run the data room with dynamic watermarking and per-group permissions from day one — this is the corridor where staged disclosure is not a nicety.

What do Baltimore's marquee deals prove about where the big mandates go?

The receipts, 2019-2026 — every financial advisor on every marquee Baltimore-metro ticket:

| Deal | Size / status | Sell-side advisors | Buy-side advisors |

|---|---|---|---|

| McCormick + Unilever foods business (announced Mar 2026; Hunt Valley keeps HQ) | ~$65B combined; close expected mid-2027 | Goldman Sachs, Morgan Stanley (Unilever) | Citi, Rothschild & Co (McCormick) |

| Constellation Energy–Calpine (closed Jan 7, 2026) | $16.4B equity (~$26.6B with debt) | Evercore, Morgan Stanley, Goldman Sachs, Barclays (Calpine/ECP) | Lazard, J.P. Morgan (Constellation) |

| Legg Mason → Franklin Resources (closed Jul 2020) | $4.5B cash | PJT Partners, J.P. Morgan | Broadhaven, Morgan Stanley, Ardea |

| W.R. Grace (Columbia) → Standard Industries (2021) | $7.0B | Goldman Sachs, Moelis | Citi, J.P. Morgan |

| T. Rowe Price ← Oak Hill Advisors (2021) | Up to $4.2B | J.P. Morgan, M. Klein (OHA) | Evercore (T. Rowe) |

| Paragon Bioservices → Catalent (2019) | $1.2B | William Blair | Centerview |

| KeyW (Hanover) → Jacobs (2019) | $815M | Guggenheim | Barclays |

| ZeroFox → Haveli (closed May 2024) | ~$350M | Piper Sandler + Stifel | BTIG, Evercore |

| Diamond Sports/Sinclair restructuring (emerged Jan 2025) | ~$9B debt → ~$200M | LionTree, Moelis (bankers) | — |

Two honest readings of this table. The first is the obvious one: the First Bank Town's biggest deals are advised from New York, and that is not going to change — a $16B utility deal or a $65B Reverse Morris Trust needs balance sheets and league-table machinery no boutique anywhere has. Your $25M company was never going to hire Lazard anyway, so this is context, not a shopping problem.

The second reading is the useful one: the mid-market tickets show the pattern you actually face. ZeroFox at $350M drew a sector specialist (Piper Sandler) plus the one platform with Baltimore lineage (Stifel). Paragon at $1.2B drew the healthcare mid-market leader (William Blair). KeyW at $815M drew a New York boutique with defense fluency (Guggenheim). At lower-middle-market size the same logic scales down: the winning advisor is the one whose last ten closings put your most probable buyers on a first-name basis — and in Baltimore that is sometimes a Harbor East boutique (Burns Engineering → OceanSound via CCA) and sometimes a specialist three time zones away. Make every candidate — local or national — show you the last three deals they closed with buyers like yours. The zip code is the least predictive line on the pitch book.

Are Baltimore's big companies actually buyers right now — and does that help me sell?

Yes, unusually so — 2025-2026 is the strongest buyer-engine stretch this metro has had in decades, and it matters to you even when the checks are signed elsewhere, because local strategic activity reprices whole supply chains.

Constellation Energy is the engine room. The metro's only Fortune 500 company (#186; ~$86B market cap) closed the $16.4B Calpine acquisition on January 7, 2026 — creating America's largest power producer, run from Harbor Point — and is restarting Three Mile Island Unit 1 as the Crane Clean Energy Center on a 20-year Microsoft power contract, with the restart accelerated to 2027 and a $1B DOE loan (November 2025) behind the $1.6B project. Every megawatt of that story flows through engineering firms, electrical and mechanical contractors, testing outfits, and grid-services companies — the exact kinds of businesses this post's readers own.

McCormick is assembling a ~$65B flavor giant in Hunt Valley — the Reverse Morris Trust combination with Unilever's foods business (announced March 31, 2026, expected to close mid-2027) keeps the McCormick name and the Maryland headquarters and creates ~$20B in revenue. Deals that size reliably shed brands, plants, and business units for years afterward; corporate development teams that just swallowed a whale also buy bolt-ons around it. Consumer, food-services, flavor-adjacent and co-packing sellers should watch this closely.

The Port is compounding. After the Key Bridge collapse (March 2024) the Port of Baltimore posted its second-best year on record in 2025 — ~50M tons, container volume up 21% — and in May 2026 MSC/Terminal Investment broke ground on the ~$1.2B Sparrows Point Container Terminal at Tradepoint Atlantic, one of the largest private container-terminal investments in US history, adding ~70% to the port's container capacity on the site of the old Bethlehem Steel works (where Amazon, Under Armour, Volkswagen, and FedEx already run distribution). Logistics, drayage, warehousing, industrial services, and marine-services companies across the corridor are being repriced by that capacity — this is what inbound-capital tailwinds look like at ground level.

The honest headwinds: Johns Hopkins — the largest university recipient of federal research money every year since 1979 — absorbed an $800M federal-funding hit and announced 2,200+ job cuts in March 2025, the largest layoff in its history (against which Bloomberg's 2024 $1B gift made its medical school tuition-free for most students — both things are true). NIH-dependent research-services sellers should time and position carefully. The Key Bridge rebuild has slipped to ~late 2030 at $4.3-5.2B, with the original contractor dropped — a long construction tailwind, but also years of harbor logistics friction. And Tradepoint's offshore-wind manufacturing tenant is fighting for its federal permit — project-dependent suppliers know who they are. None of this cancels the tailwinds; it tells you which sub-sectors need a sharper story about durability.

Net for a seller: strategic appetite around energy services, defense electronics, cyber, logistics, and consumer/flavor is genuine and current. A good advisor prices this into your launch window — ask each candidate which of these engines their buyer list actually touches.

Is an ESOP a realistic exit for my Baltimore company?

Unusually realistic — Baltimore may be the strongest ESOP-culture metro on the East Coast, and unlike most cities, its ESOP advisory bench is local and registered.

The culture proof is the biggest private company in the metro: Whiting-Turner (Towson), the employee-owned contractor with $14.7B in 2025 revenue, ranked No. 5 on ENR's national Top 400 — proof at maximum scale that employee ownership can build and keep a dominant company in this economy for a century. (SC&H's client list shows the model working at normal scale too: Kitware and Carpet & Wood Floor Liquidators both went to ESOPs through 2024 processes.)

The mechanics, honestly stated: an ESOP sells your company to a trust for your employees at fair market value set by an independent appraisal. Sellers of C-corp stock can defer capital gains under Section 1042 by rolling proceeds into qualified replacement securities; a 100% S-corp ESOP pays no federal income tax, which is why engineering, construction-services, and government-services firms — Baltimore's bread and butter — are structurally overrepresented in the ESOP world. The tradeoffs are equally real: fair market value is not a strategic premium (a competitive auction usually clears higher), the transaction is governance-heavy (trustee, annual valuation, repurchase obligation), and the debt typically funds out over years. The decision framework I'd use: if your priority ranking is legacy-workforce-taxes-timing, feasibility-test an ESOP before running a market process; if it is headline price, run the auction — and know that a good advisor can run the two in parallel as a genuine market check.

Who advises one here: SC&H Capital (CRD #148291) is the registered local specialist with current ESOP closings, and ESOP-specialist trustee counsel and independent appraisers matter as much as the banker. Diligence is identical in kind either way: the trustee's appraiser wants the same clean financial picture a strategic buyer would, staged through the same data room discipline.

Does Maryland deal mechanics matter — the 6% bulk-transfer tax and government-contract novation?

For your buyer list and your valuation: no. For your structure and your closing checklist: yes, in two specific ways that Maryland sellers keep learning at the worst possible moment.

The 6% bulk-transfer trap. In an asset sale, Maryland's bulk-transfer rules can apply the state's 6% sales-and-use tax to the tangible personal property conveyed with the business — machinery, equipment, furniture, vehicles. Equipment-heavy sellers (manufacturers, logistics operators, contractors) can discover a six-figure tax line item in the closing flow if nobody modeled it. A stock sale generally doesn't trigger it; inventory held for resale and intangibles are treated differently; and allocation choices interact with the buyer's tax preferences — which is exactly why the asset-versus-stock conversation should happen with your CPA in month one, not at the closing-checklist call. This is thirty minutes of modeling that protects real money.

Novation cuts the other way. If you sell to or through the federal government — and in this metro, an enormous share of companies touch it — an asset deal triggers novation of your federal contracts (the government's consent process for transferring them, which runs on the government's clock), while a stock deal generally avoids it because the contracting entity survives. So the tax analysis and the novation analysis point in opposite directions for some sellers, and the right structure is a genuine three-way negotiation among tax, contracts, and the buyer's risk appetite. Maryland counsel who close these deals monthly handle this in their sleep; the sellers who get surprised are the ones who operated informally for years and never mapped which contracts sit in which entity. Diligence will find it — so find it first: pull the contracts, the novation-relevant terms, and both tax models into the data room in week one.

How do I tell a real investment bank apart from a business broker in Baltimore?

Ask four questions and BrokerCheck one name — five minutes total:

- "Are you a FINRA-registered broker-dealer, operating under the M&A-broker exemption, or working through a broker-dealer of record?" All three are legitimate; the firm should answer in one sentence. (Local answer key: Bengur Bryan, SC&H, Evergreen = registered; CCA, NSCA = exempt; Charlesmead = through BA Securities; Parchman Vaughan = exempt since November 2022 — a firm that answers this accurately is showing you its integrity.)

- "What were your last three closings in my size band, and who were the buyers?" Named companies, named buyers, dates within ~24 months. In Baltimore's thin market a real firm can name them instantly.

- "Who runs my deal day to day?" Boutique founders sell the A-team; some deliver associates. In a three-registered-firm town, the principal's personal bandwidth is a real constraint — use it as a negotiating point.

- "How will you reach buyers outside the region?" The First Bank Town's whole deal record says your buyer probably isn't local. Listen for named strategics and sponsors, not "our proprietary network."

The tier logic by size: under ~$5M, you want a Main-Street business broker (asset-priced listings, individual buyers — a different craft, honestly practiced by the metro's broker tier); $5M-$150M, the boutiques in this post; $150M+, sector specialists and national banks enter. And a structural note worth repeating: since the 2023 SEC codification, the M&A-broker exemption is a normal, legal way to run private-company sales — the point of the verification is not to disqualify exempt firms, it is to match the structure of your deal (stock? rollover? raise?) to what your advisor may legally execute.

Is now a good time to sell my Baltimore business?

The honest macro answer: 2026 is a seller-friendly window for the metro's core sectors, with sharp sub-sector exceptions. The tailwinds are concrete — Constellation digesting Calpine and rebuilding nuclear (energy services demand), a $65B consumer-flavor combination assembling in Hunt Valley (consumer/food-adjacent strategics active), the port's record recovery plus a $1.2B terminal under construction (logistics/industrial repricing), a cyber corridor where Accenture just validated the whole cluster at $3.25B (strategic and PE appetite for security assets), and an ESOP culture with a registered local bench for owners who prioritize legacy. The headwinds are equally concrete — NIH-dependent research services face a funding regime that cut 2,200+ Hopkins jobs in 2025; offshore-wind suppliers are hostage to a permit fight; bridge-dependent logistics faces 2030 timelines. If you sit in a tailwind sector with clean financials, processes launched in 2026 catch buyers with mandates and dry powder. If you sit in a headwind sub-sector, the work is a durability story — contract diversification, funding-source mix — before launch, which is advisor-selection work too: pick the firm that has sold through your specific weather.

What's a reasonable success fee for a $25M Baltimore sell-side?

The same math as the rest of the country — roughly 3-3.5% at $25M, sliding down as size climbs (toward 1-2% approaching $100M+), often quoted on a Double Lehman scale or a flat percentage with breakpoints, plus a monthly retainer (commonly $10K-$25K at this size, usually creditable against the success fee) that filters unserious sellers and funds the prep months. Minimum fees are the number to watch at the small end: a firm whose minimum is $750K is telling you your $8M deal is not its business — ask directly. Below ~$5M, broker economics run 8-12% instead. What you are actually buying for the fee: buyer-list quality, process discipline that manufactures competitive tension, and a principal who has priced companies like yours through both LOI negotiations and diligence fights. In a metro with a bench this short, fee negotiation is less about the percentage and more about the minimum, the tail (12-24 months is standard; longer deserves pushback), and exactly whose calendar your deal occupies.

Which virtual data room should a Baltimore seller actually use?

The honest tiering, since this is my industry: for $500M-plus mega-deals of the Calpine sort, Datasite and Intralinks are the incumbents and the league-table banks default to them. For the sub-$300M band that is the actual bulk of Baltimore deal count, the modern stack is Peony, iDeals, or FirmRoom — full-strength process tooling (per-group permissions, page-level analytics, dynamic watermarking, Q&A workflow, visitor groups for staging strategics vs sponsors vs the trustee's advisors) at pricing built for founder-led deals rather than bulge-bracket engagement letters. The Baltimore-specific emphasis, one more time because the corridor makes it acute: when your most probable acquirers are also your competitors — the default condition in cyber, defense electronics, and specialized government services — staged disclosure with per-page watermarks and instant access revocation is the difference between running a process and leaking a strategy memo. Whichever platform you choose, build the room before the teaser goes out; our 283-deal benchmark shows prepared rooms compress diligence by weeks.

Bottom line

Baltimore invented the American investment bank in 1800 and spent 1997-2018 selling every homegrown heir — so the famous names manage money now, and the sell-side bench a founder actually hires is short, specialized, and checkable in an afternoon: three registered broker-dealers (Bengur Bryan, CRD #36290; SC&H Capital, CRD #148291; Evergreen Advisors Capital, CRD #165072), an honest exempt tier led by Chesapeake Corporate Advisors with real specialists behind it (NSCA for national security, Charlesmead for telecom, Parchman Vaughan for education — verified current status and all), and Stifel's Legg-descended Harbor Point office when you need a full-service platform with local lineage. Test every candidate — local or national — against the same three receipts: BrokerCheck status stated plainly, three named closings in your size band, and a buyer list that reaches wherever your buyers actually live, which in the First Bank Town has never been down the street. The buyer engine is genuinely running — Calpine closed, a $65B flavor company assembling in Hunt Valley, a $1.2B terminal rising at Sparrows Point, Accenture writing a $3.25B check into the cyber corridor — so the market is doing its part. Prepare the company, verify the advisor, stage the disclosure, and make the competition do the pricing.

Frequently asked questions about Baltimore M&A advisors

Should I hire a local Baltimore M&A boutique or a national investment bank to sell my company?

Hire a genuinely-local firm when your deal is in the ~$5M-$100M band and your best buyers are reachable strategics and middle-market sponsors; go national or sector-specialist once the deal climbs toward $150M+ or your vertical is one where specialist relationships set the price. The Baltimore wrinkles: the famous local brands (T. Rowe Price, Brown Advisory, Alex. Brown) manage money and don't sell companies, only three registered broker-dealers are actually headquartered here (Bengur Bryan, SC&H Capital, Evergreen Advisors Capital), and for Fort Meade-corridor cyber companies the price-setting buyers are reached by sector specialists (Piper Sandler on ZeroFox, Guggenheim on KeyW) wherever they sit. Price comes from competitive tension, not a banker's zip code — and a clean, staged data room with page-level analytics is the cheapest lever you control either way.

I own a ~$25M Baltimore-metro company — who are the best M&A advisors for a lower-middle-market sale?

The genuinely-local shortlist: Bengur Bryan & Co. (registered, CRD #36290, since 1991 — Trans/Air to Lippert in March 2025, First Source Electronics to Woodson in October 2024), Chesapeake Corporate Advisors (Harbor East, the most-cited homegrown boutique, exempt-model, Burns Engineering to OceanSound in December 2025), Evergreen Advisors Capital (registered, Columbia), and SC&H Capital (registered — the ESOP and special-situations lane). Sector specialists: Charlesmead for telecom/broadband, Parchman Vaughan for education (registration withdrawn November 2022 — structure accordingly), NSCA for national-security. Ask every firm for its last three closings in your sub-sector with buyers named.

Is Alex. Brown still a Baltimore investment bank that can sell my company?

No. Alex. Brown & Sons — founded 1800, the first investment bank in the United States — was sold to Bankers Trust in 1997 and absorbed into Deutsche Bank in 1999. The "Alex. Brown" in Baltimore today is a wealth-management division of Raymond James (the brand was revived in 2016 for the high-net-worth business Raymond James bought from Deutsche). It manages portfolios; it does not run sell-side processes. The deal DNA scattered — into Brown Advisory (wealth), ABS Capital (growth equity), Signal Hill (absorbed into Daiwa's DC Advisory in 2018), and Stifel's Baltimore office (via the Legg Mason capital-markets purchase). Check what a firm does today, not what its name did in 1900.

Can T. Rowe Price, Brown Advisory, or my wealth manager sell my business, or do I need an M&A advisor?

You need an M&A advisor; your wealth manager plans the proceeds. T. Rowe Price (~$1.7 trillion AUM) is an asset manager — when it bought Oak Hill Advisors for $4.2B it hired Evercore to advise itself. Brown Advisory is a wealth and institutional investment firm. Alex. Brown is a Raymond James wealth brand. Legg Mason hasn't existed since Franklin absorbed it in July 2020 — yet AI-generated directories still rank it among "Baltimore's top investment banks," which tells you how much of the internet is guessing. Sequence the two disciplines: a registered advisor or bank runs the competitive process; the wealth manager invests what it produces.

Who advises the sale of a cybersecurity or defense-adjacent company in the Fort Meade corridor?

Almost always a sector specialist or national bank: ZeroFox's $350M take-private ran through Piper Sandler (Stifel co-advising), KeyW's $815M sale through Guggenheim, and the recurring corridor banks are Piper Sandler, Guggenheim, William Blair, Houlihan Lokey's aerospace-defense group, Raymond James defense & government, Momentum Cyber, and KippsDeSanto (Tysons, Capital One-owned) — none Baltimore-headquartered, even as Accenture pays $3.25B for Hanover's Dragos. The local exceptions: National Security Capital Advisors (Columbia) is a genuine in-corridor merchant bank for $10M-$100M-revenue national-security companies, and for cleared government-services businesses see our Washington DC guide. Whoever you hire, run diligence with dynamic watermarking — in this corridor your buyer list is your competitor list.

How do I verify a Maryland M&A advisor is FINRA-registered — and which Baltimore firms actually are?

Search the exact legal name on BrokerCheck (brokercheck.finra.org) the week you hire. Registered and headquartered in the metro today: Bengur Bryan & Co. (CRD #36290), SC&H Capital (CRD #148291), Evergreen Advisors Capital (CRD #165072). The instructive trap: Parchman Vaughan held CRD #44390 for a quarter century and withdrew it in November 2022 — the firm still advises, legally, under the SEC's M&A-broker exemption, but a stale directory won't tell you that, and it changes what your advisor may do in a stock sale or rollover. Exempt operation (CCA, NSCA) and broker-dealer-of-record models (Charlesmead via BA Securities) are both legitimate — the test is whether the firm states its status plainly and your deal structure matches it.

Is an ESOP a realistic exit for my Baltimore company, and who advises one?

Unusually realistic: the metro's biggest private company — Whiting-Turner, $14.7B revenue, ENR's No. 5 contractor — is the century-scale proof, and the local specialist bench is registered: SC&H Capital (CRD #148291) closed the Kitware and Carpet & Wood Floor Liquidators ESOPs in 2024. Mechanics: the ESOP trust pays fair market value set by independent appraisal; C-corp sellers can defer gains under Section 1042; a 100% S-corp ESOP pays no federal income tax — which is why engineering and services firms love it. Tradeoffs: no strategic premium, governance-heavy, debt funds out over years. If legacy-workforce-taxes-timing outranks headline price, feasibility-test it — and the trustee's appraiser will want the same clean data room a buyer would.

Are Baltimore's big companies actually buyers right now, and does that help me sell?

Yes — Constellation (the metro's only Fortune 500) closed the $16.4B Calpine deal in January 2026 and is restarting Three Mile Island for Microsoft by 2027; McCormick is assembling a ~$65B flavor giant in Hunt Valley (announced March 2026, closing mid-2027 — megadeals shed units and buy bolt-ons for years); the Port posted its second-best year ever and broke ground on the $1.2B MSC terminal at Sparrows Point in May 2026; and Accenture validated the cyber corridor at $3.25B with Dragos. Honest headwinds: Hopkins cut 2,200+ jobs after federal funding cuts (research-services sellers, time carefully) and the Key Bridge rebuild slipped to ~2030. Energy services, logistics, cyber, defense electronics, and consumer/flavor sellers are in a genuine tailwind window.

How does a sell-side M&A process work for a Baltimore company, and how long does it take from advisor hire to close?

Five overlapping stages, typically 6-9 months: preparation (4-8 weeks — financials, quality of earnings, CIM, data room), outreach under NDA (2-4 weeks), indications of interest (3-5 weeks), management meetings and LOI (4-6 weeks), then confirmatory diligence to close (8-12 weeks). Baltimore wrinkles: government-adjacent sellers should settle stock-vs-asset structure early because asset deals trigger federal contract novation (a months-long consent process) while stock deals generally avoid it; an ESOP alternative runs 4-6 months on its own clock. The biggest timeline risk everywhere is unprepared financials — and a data room built before launch, not after the first LOI, is the most reliable compressor of the back half of the schedule.

What do buyers diligence, and how do I set up a data room before going to market with my Baltimore company?

Buyers underwrite durable, transferable cash flow — normalized EBITDA quality, concentration, margins, working capital, contract assignability — plus Baltimore's sector layer: contract vehicles, clearances, and novation exposure for government-adjacent companies; payer mix for healthcare services; backlog and bonding for construction; leases and equipment for port-orbit logistics. Build the room around eight workstreams: financial, corporate/legal, commercial, operations, HR, IP/IT, tax (including Maryland's bulk-transfer rules), and insurance/compliance. Then enforce staged disclosure: blind teaser first, CIM after NDA, and sensitive material (customer names, pricing, clearance rosters) held for the short list under per-group permissions and dynamic watermarking — non-negotiable in a corridor where buyers and competitors overlap. I run Peony; our 283-deal benchmark shows prepared rooms close weeks faster.

What does an M&A advisor cost to sell a $25M Baltimore company — and do I owe Maryland's 6% bulk sales tax when I sell?

Budget a monthly retainer ($10K-$25K at this size, usually creditable) plus a ~3-3.5% success fee, often on a Double Lehman scale with a minimum-fee floor — and watch the minimum and the tail (12-24 months is standard) more than the headline percentage. The Maryland wrinkle: in an asset sale, the bulk-transfer rules can apply the 6% sales-and-use tax to tangible personal property conveyed with the business (equipment, vehicles, furniture) — a six-figure surprise for equipment-heavy sellers — while a stock sale generally avoids it but triggers different tradeoffs (novation runs the other way for government contractors). Model both structures with your CPA in month one, and put the model in the data room so the fee-and-structure conversation happens on facts.

Related resources

- The State of M&A Data Rooms — our 283-deal platform benchmark on how sell-side processes actually run.

- How to Build an M&A Data Room — the staged-disclosure playbook every Baltimore seller should run before going to market.

- How to Write a CIM — the confidential information memorandum your advisor builds after the teaser.

- Best M&A Advisors in Washington DC — the cleared-govcon and defense-services tier forty miles south: KippsDeSanto, the Beltway specialists, and cleared-deal mechanics for government-services sellers.

- Best M&A Advisors in Philadelphia — the other mid-Atlantic bench Baltimore sellers interview; Burns Engineering's sale (advised from Harbor East) ran in exactly this corridor.

- Best M&A Advisors in St. Louis — the Headquarters Town, and home base of Stifel — the bank that bought Legg Mason's capital-markets arm and kept Baltimore on its institutional map.

- Best M&A Advisors in Kansas City — the Ownership Town: what happens when who holds the equity, rather than who lost the banks, shapes a metro's deal market.

- Best Tech M&A Advisors — the national sector view for corridor software and cyber sellers.

- Best Healthcare M&A Advisors — the national sector view for Hopkins-orbit and healthcare-services sellers.

Footnotes and sources

- FINRA BrokerCheck (brokercheck.finra.org) — verified entity registrations and CRD numbers: Bengur Bryan & Co., Inc. (CRD #36290, Baltimore, formed June 1991); SC&H Capital Corporation (CRD #148291, registered office Columbia, MD; parent SC&H Group, Sparks, MD); Evergreen Advisors Capital, LLC (CRD #165072, Columbia, MD; parent founded 2001); Stifel, Nicolaus & Company (CRD #793); Chessiecap Securities (CRD #132153, Bethesda); BA Securities, LLC (Charlesmead's disclosed broker-dealer of record). Deregistrations verified: Parchman, Vaughan & Company (CRD #44390 — BD registration withdrawn, ceased November 3, 2022; firm continues as a non-registered advisor); Signal Hill Capital Group (CRD #122782 — ceased March 1, 2018; combined with Sagent into Daiwa's DCS Advisory, now DC Advisory; founder Scott Wieler retired from DC Advisory May 2024). Chesapeake Corporate Advisors and National Security Capital Advisors return no broker-dealer firm records (consistent with the federal M&A-broker exemption; SEC codification effective 2023).

- Alex. Brown & Sons history — founded 1800 by Alexander Brown, Baltimore; generally cited as the first investment bank in the United States (Maryland State Archives; standard references); Baltimore Water Company (1808) as the first US IPO; George Brown as founding treasurer of the B&O Railroad (chartered 1827). Sale chain: Bankers Trust merger announced April 1997 (~$1.7B announced; ~$2.5B in stock by the September 1997 close); Deutsche Bank acquired Bankers Trust (completed June 1999); Raymond James acquired Deutsche's US Private Client Services unit and revived "Alex. Brown" as its wealth division (September 2016; ~16 offices, ~600 employees, ~100 in Baltimore, per Baltimore Sun coverage).

- Legg Mason — June 2005 swap with Citigroup (Legg's brokerage and capital markets for Citi's asset management; ~$3.7B; closed December 1, 2005); Legg Mason Capital Markets sold by Citigroup to Stifel (closed December 1, 2005; up to $95M including earnout; ~500 associates; Baltimore Sun and Stifel disclosures); Franklin Resources acquisition ($4.5B all-cash at $50/share; announced February 18, 2020; closed July 31, 2020; advisors: PJT Partners and J.P. Morgan for Legg Mason; Broadhaven, Morgan Stanley, and Ardea for Franklin). Ferris, Baker Watts (founded 1900) — acquired by RBC for $230M, closed 2008, name retired.

- Marquee deal advisors — McCormick-Unilever foods combination (~$65B combined; Reverse Morris Trust; announced March 31, 2026; McCormick name and Hunt Valley HQ retained; ~$20B pro-forma revenue; close expected mid-2027; advisors per the announcement: Citi and Rothschild & Co for McCormick; Goldman Sachs and Morgan Stanley for Unilever). Constellation Energy-Calpine ($16.4B equity,

$26.6B enterprise; announced January 10, 2025; closed January 7, 2026; Lazard and J.P. Morgan for Constellation; Evercore, Morgan Stanley, Goldman Sachs, and Barclays for Calpine/ECP; PJM asset sale to LS Power as regulatory remedy). W.R. Grace (Columbia, MD) to Standard Industries ($7.0B at $70/share; announced April 2021; closed September 2021; Goldman Sachs and Moelis for Grace; Citi and J.P. Morgan for Standard). T. Rowe Price-Oak Hill Advisors (up to $4.2B; closed December 2021; Evercore for T. Rowe Price; J.P. Morgan and M. Klein for OHA). Paragon Bioservices to Catalent ($1.2B; 2019; William Blair sell-side; Centerview for Catalent). KeyW to Jacobs ($815M; 2019; Guggenheim sell-side; Barclays for Jacobs). ZeroFox take-private by Haveli ($350M at $1.14/share; announced February 2024; closed May 13, 2024; Piper Sandler lead and Stifel co-advisor sell-side; BTIG and Evercore for Haveli). Diamond Sports Group restructuring (plan confirmed November 14, 2024; emerged January 2, 2025 as Main Street Sports Group; ~$9B debt reduced to ~$200M; LionTree and Moelis as investment bankers). - Fort Meade cyber corridor — NSA, US Cyber Command (established at Fort Meade 2010), and DISA headquartered at Fort Meade, Anne Arundel County; $500M+ Integrated Cyber Center; Anne Arundel Economic Development Corporation (2,100+ technology companies; 23,000+ tech professionals); Maryland Department of Labor / BLS (~18,400 information-security analysts statewide; mean wage ~$133,630). DataTribe (Fulton; founded 2016 by Mike Janke, Bob Ackerman, Steven Witt; seeded Dragos with $1.2M, 2016). Dragos (Hanover; $200M Series D at $1.7B, October 2021, Koch Disruptive Technologies and BlackRock; $74M extension 2023; Accenture majority-stake agreement at $3.25B valuation announced June 18, 2026, in a ~$4.2B bundle with runZero and NetRise, expected to close fall 2026). Tenable (Columbia; IPO 2018; ~$4B market capitalization July 2026; Ermetic $265M closed October 2023; Eureka Security 2024; Vulcan Cyber ~$147M closed February 2025). Huntress (Ellicott City; $150M Series D at $1.5B+ valuation, led by Kleiner Perkins with Meritech and Sapphire, June 2024). Blackpoint Cyber (Ellicott City; $190M from Bain Capital Tech Opportunities and Accel, June 2023). Sonatype (Fulton; Vista Equity Partners majority, 2019). Terbium Labs acquired by Deloitte (2021); Bricata acquired by OpenText (2021). KippsDeSanto & Co. (Tysons, VA) acquired by Capital One (2019).

- Buyer engine and metro economy — Constellation Energy: Fortune 500 #186 (2025), the Baltimore metro's only Fortune 500 headquarters (Baltimore Sun; T. Rowe Price, McCormick, and Sinclair joined the list in 2021 and have since fallen below the revenue cutoff); ~$86B market capitalization (July 2026); spun off from Exelon February 2022; Crane Clean Energy Center (Three Mile Island Unit 1) restart — 20-year Microsoft PPA announced September 2024, 835 MW, ~$1.6B investment, restart accelerated to 2027, $1B DOE Loan Programs Office loan announced November 2025. Port of Baltimore — Francis Scott Key Bridge collapse March 26, 2024 (six workers killed; ship Dali); 100% federal funding of the rebuild (December 2024 spending law); rebuild estimate $4.3-5.2B with completion

late 2030 and Kiewit's Phase 1 role ending after its estimate ($9B) was rejected (MDTA updates, The Baltimore Banner, CBS Baltimore); 2025 port results — ~50M tons (second-best year), $65.6B cargo value, 1.1M TEU (+21% YoY), record 2,223 vessel calls (Maryland Port Administration / Maritime Executive). Tradepoint Atlantic (Sparrows Point) — ~14M sq ft logistics campus on the former Bethlehem Steel site (tenants include Amazon, Under Armour, Volkswagen, Home Depot, FedEx); Sparrows Point Container Terminal (MSC/Terminal Investment Ltd) — ~$1.2B private investment, groundbreaking May 1, 2026, 168 acres, ~70% container-capacity increase, $39.7M federal PIDP grant (Office of the Governor of Maryland); US Wind monopile facility at risk amid federal permit revocation proceedings (injunction denied December 2025; Maryland Matters). Johns Hopkins — largest university recipient of federal R&D funds every year since 1979; >$1B NIH funding FY2024; 2,200+ position eliminations announced March 2025 tied to ~$800M in federal cuts (CNN, Higher Ed Dive); Bloomberg Philanthropies $1B gift (July 2024) making medical school tuition-free for most students; Johns Hopkins Tech Ventures — 131 portfolio startups, $4.8B raised, 45 exits (2025). Whiting-Turner (Towson) — $14.7B revenue, No. 5 on ENR's 2026 Top 400, employee-owned. Under Armour — Kevin Plank returned as CEO April 1, 2024; MyFitnessPal bought for $475M (2015), sold for $345M (2020). Baltimore-Columbia-Towson MSA — population ~2.86M (2024 Census estimates, 20th-largest US metro); median household income ~$98.7K (2024 ACS), ~20% above the US median. - Maryland deal mechanics — Maryland Tax-General provisions applying the 6% sales-and-use tax to tangible personal property conveyed in bulk transfers (asset sales), with distinct treatment of resale inventory and intangibles (Comptroller of Maryland guidance; consult counsel — this article is not tax advice); FAR Subpart 42.12 novation requirements for transfers of federal government contracts in asset transactions.

- Firm websites and deal announcements — Bengur Bryan (bengurbryan.com; PRWeb deal announcements); SC&H Capital (schgroup.com press releases — Kitware ESOP May 2024; Wise Consulting to RSM September 2024; leadership transition); Evergreen Advisors (evergreenadvisorsllc.com); Chesapeake Corporate Advisors (ccabalt.com; citybiz — Burns Engineering to OceanSound Partners, December 2025); National Security Capital Advisors (nscapitaladvisors.com); Charlesmead Advisors (charlesmead.com — Balhoff biography; BA Securities disclosure); Parchman Vaughan (parchmanvaughan.com); Brown Advisory and ABS Capital Partners (firm histories; Alex. Brown lineage per firm disclosures and standard references; Camden Partners founder background per firm biography — T. Rowe Price, not Alex. Brown).

This article reflects my views as of July 2026 and is informational, not legal, tax, or investment advice. Firm registrations, names, and ownership change — this metro's history is one long proof of that — so verify current status on FINRA BrokerCheck before engaging any advisor. I am the co-founder of Peony, a data room company; where I mention Peony I have flagged the interest.