16 Best Healthcare M&A Advisors in the US by Subsector (2026 Guide)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

16 Best Healthcare M&A Advisors in the US by Subsector (2026 Guide)

Quick answer: Healthcare M&A does not have one "best advisor" — it splits into a services side and a products / tech / pharma side, each with its own bench. On the services side ($20M-$500M lower-middle and middle market), the strongest names are Cain Brothers (KeyBanc), Provident Healthcare Partners, The Braff Group, VERTESS, Cross Keys Capital, Edgemont Partners, Ziegler, and Physician Growth Partners. On the products / tech / pharma side, Leerink Partners, Centerview, Evercore, Jefferies, Houlihan Lokey, Piper Sandler, William Blair, and Harris Williams. The mega-banks own the multi-billion-dollar biopharma league tables but are usually the wrong call below ~$250M. Pick by subsector and by which advisor can pre-empt your 2026 regulatory exposure — not by logo.

Last updated: July 2026

TL;DR for the cluster: This guide is organized around five proprietary frames — the Subsector-Specialist Gate (healthcare is ~10 markets, not one), the Regulatory-Overhang Discount (CON + Corporate Practice of Medicine + FTC/DOJ/HHS PE-roll-up scrutiny as a discount or delay a specialist pre-empts), the Reimbursement-Mix Multiple Ladder (payor mix is the biggest value lever within any subsector), the Scarcity-Premium-from-Moratorium frame (the CMS hospice/home-health enrollment moratorium makes compliant agencies scarcer), and the Buyer-Universe Depth Test (the one screening question that separates a real specialist from a generalist).

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — multi-site physician practices, behavioral-health and autism platforms, dental DSOs, home-health and hospice agencies, medical-device and healthcare-IT companies, and the occasional multi-billion-dollar biopharma combination — and healthcare is the sector where picking the wrong type of advisor costs you the most. A generalist banker who runs a clean EBITDA-multiple process on a behavioral-health platform, or who has never structured around the Corporate Practice of Medicine on a physician-practice sale, leaves real money on the table and can stall the deal in regulatory review. At Peony we now serve more than 5,900 customers, and a large share of our healthcare deals live in exactly the $20M-$500M band this guide covers.

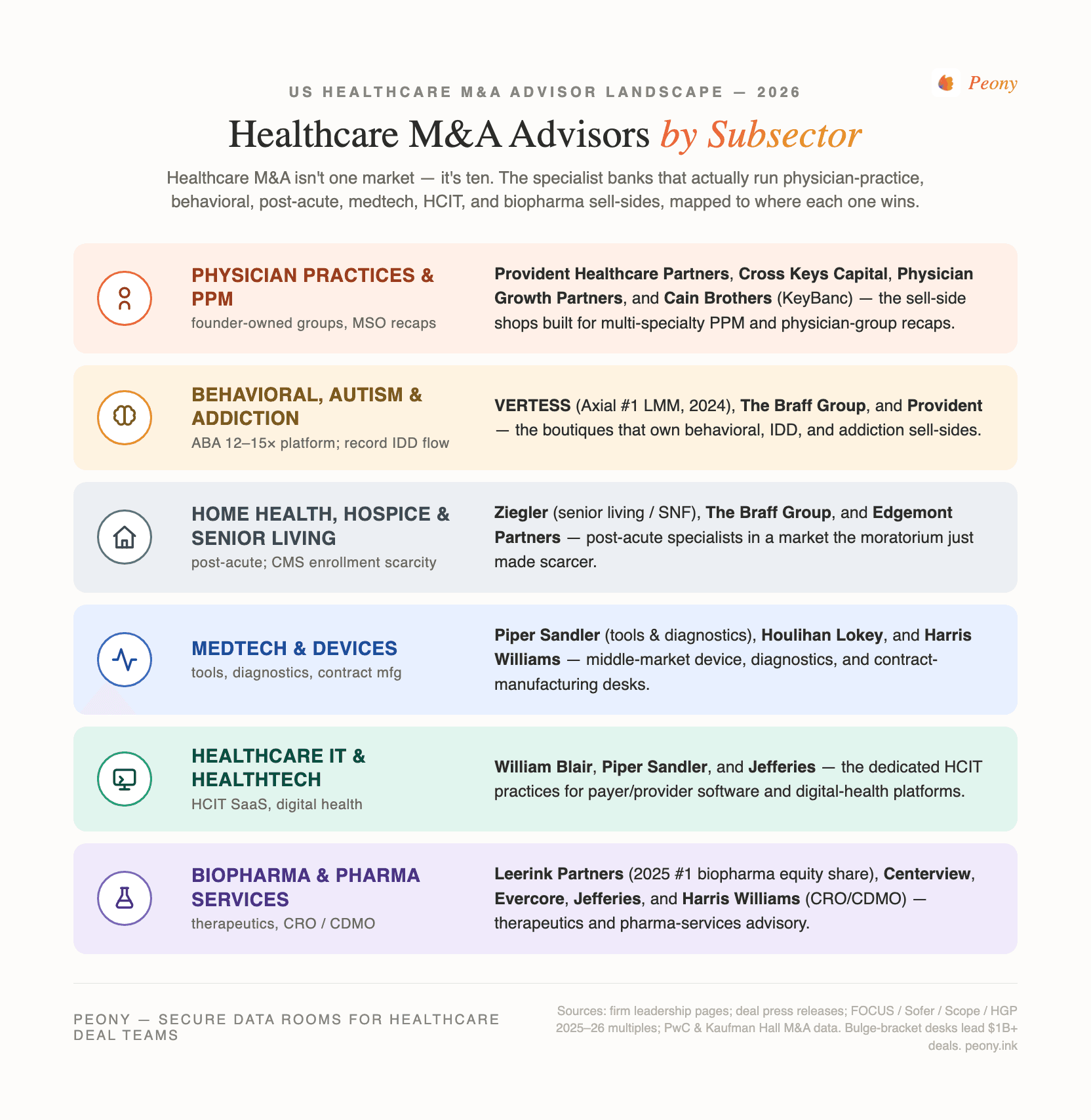

Most "best healthcare M&A advisor" lists are interchangeable directory pages that rank firms one through ten as if a single league table existed. It does not. Healthcare M&A splits into roughly ten distinct sub-markets, which fall into two broad camps: a services side (physician practices and PPM, behavioral health and autism/ABA, dental DSOs, home health and hospice, senior living and post-acute) and a products / tech / pharma side (medical devices, healthcare IT, biopharma, CRO/CDMO and pharma services). The firm that dominates one is often irrelevant in another. This post is organized the way the market actually works — by subsector — with each firm mapped to its lane, its deal-size band, and a verified credential or deal where one exists.

Three framing notes before the roster. First, the services-versus-products split is the master distinction. Services deals are priced off payor mix, recurring contracts, clinical quality, and a buyer set that is mostly healthcare private equity; products and pharma deals are priced off clinical IP, regulatory pathway, and a buyer set that includes strategic acquirers and the largest banks. Second, the regulatory layer is unique to healthcare — Certificate of Need, the Corporate Practice of Medicine, and 2026 FTC/DOJ/HHS scrutiny of PE roll-ups can discount or delay a deal, and the right advisor pre-empts them in process design. Third, honest framing on the mega-banks: Centerview, Evercore, Jefferies, and Leerink own the multi-billion-dollar value league tables, but they are not the answer for most readers of this guide, so I frame them as the ceiling, not the default. And Peony is not an advisor — it is the data-room layer sellers and bankers use to run the process; I will flag where that fits, but the advisory firms are the subject here.

What's the healthcare M&A advisor landscape by subsector in 2026?

The roster below is organized by subsector, split into the services side and the products / tech / pharma side. Each firm is profiled in depth in its section; this table is the map.

| Firm | HQ | Side | Subsector focus | Credential / verified deal |

|---|---|---|---|---|

| Cain Brothers (KeyBanc) | New York | Services | Broadest healthcare-services platform | Advised on FHN-Mercyhealth affiliation (closed Dec 31 2025) |

| Provident Healthcare Partners | Boston | Services | PPM, behavioral, infusion, post-acute, dental | Elder Care Homecare to Rallyday Partners (Aug 2025) |

| The Braff Group | Pittsburgh | Services | Behavioral, home health/hospice, staffing, DME | Sell-side-only; 375+ transactions; founded 1998 |

| VERTESS | Tucson + Dallas-FW | Services | LMM behavioral, IDD, ABA, home care, DME, dental | Axial #1 LMM healthcare sell-side advisor (2024) |

| Cross Keys Capital | Fort Lauderdale | Services | Physician practice management (20+ specialties) | 200+ transactions over the prior decade (firm-reported) |

| Edgemont Partners | New York | Services | Post-acute, healthcare staffing, distribution | Dedicated post-acute / staffing / distribution franchise |

| Ziegler | Chicago | Services | Senior living, skilled nursing, NFP hospitals | Kokoro Assisted Living to Northstar (Sept 1 2025) |

| Physician Growth Partners | Chicago | Services | Physician-practice / PPM sell-side (PE recaps) | 90+ PPM transactions, $3.5B+ enterprise value (confirmed with Director) |

| Leerink Partners | Boston | Products / pharma | Pure-play healthcare bank; biopharma | #1 US biopharma equity-deal share 2025 (Dealogic); advised GSK/IDRx |

| Centerview Partners | New York | Products / pharma | Largest, most complex biopharma M&A | Advised Verona Pharma on ~$10B sale to Merck (closed Oct 2025) |

| Evercore | New York | Products / pharma | Top independent; broad healthcare | Expanded bench in 2025 (Modisett hire from Morgan Stanley) |

| Jefferies | New York | Products / pharma | High-volume biotech ECM + mid-cap M&A | 140+ healthcare bankers; co-advised Intra-Cellular on J&J deal |

| Houlihan Lokey | Los Angeles | Products / pharma | Dominant middle-market by deal count | Middle-market volume leadership + pharma-services depth |

| Piper Sandler | Minneapolis | Products / pharma | Life-science tools & diagnostics; medtech; HCIT | 100+ tools/diagnostics deals since 2012 |

| William Blair | Chicago | Products / pharma | Middle-market HCIT and medtech | Advised Azenta on B Medical Systems sale (US$63M, Dec 2025) |

| Harris Williams | Richmond, VA | Products / pharma | Middle-market healthcare; pharma-services/CDMO | Standout CDMO/CRO franchise serving PE sponsors |

A few notes the table cannot carry. Cain Brothers, Provident, The Braff Group, VERTESS, Cross Keys, and Physician Growth Partners are the working core for a $20M-$500M healthcare-services seller — the specialists most readers of this guide actually need. Ziegler owns senior living and skilled nursing specifically. On the products and pharma side, Houlihan Lokey, William Blair, Piper Sandler, and Harris Williams are the middle-market workhorses, while Leerink, Centerview, Evercore, and Jefferies are built for the large-cap and multi-billion-dollar biopharma deals. Each firm is profiled in its subsector section below.

Who are the best healthcare-services M&A advisors (physician practices, behavioral, dental, home health)?

For a healthcare-services sale, the right advisor is a function of your exact sub-vertical and how much of your value lives in payor mix and recurring contracts versus a clinical brand. The eight firms below cover the $20M-$500M services band, from sell-side-only boutiques to the broadest dedicated platform on the Street.

Cain Brothers, a division of KeyBanc Capital Markets (New York), runs the broadest dedicated healthcare-services platform of any bank, with one of the largest healthcare investment-banking teams anywhere. As part of KeyBanc it pairs boutique healthcare depth with a balance sheet, covering providers, payors, healthcare IT, and pharma services across the lower-middle through large-cap range. Verified recent mandates show the franchise's reach across both not-for-profit and PE-backed deals: Cain Brothers advised on the FHN affiliation with Mercyhealth (signed September 30 2025, closed December 31 2025) and on the US Fertility recapitalization (an L Catterton-led transaction, 2025). For a larger services platform that wants healthcare specialization with a balance sheet behind it, Cain Brothers is the rare specialist that brings both. I am not naming individual managing directors here because the firm's bench is deep and the specific deal team varies by mandate.

Provident Healthcare Partners (Boston) is the founder-owned, sell-side-focused specialist for physician practice management and the broader services landscape — behavioral health and autism, infusion, home-based and post-acute care, dental, and outsourced pharma services. It also publishes the widely read "Trusted Healthcare Advisor" review, useful market thought leadership. Its senior bench includes Robert Ciardi (Managing Partner), Rebecca Leiba (Senior Managing Director), Eric Major (Managing Director), and Kevin Palamara (Managing Director). Verified recent deals span the services map: Provident advised Elder Care Homecare on its sale to Rallyday Partners (August 2025), CPS Infusion on its sale to Seven Hills Capital (September 2025), and Meperia on its sale to Diversis Capital (November 2025). For a founder-owned PPM, behavioral, or post-acute company, Provident's sell-side-only focus — and the market research it publishes — make it a natural first call.

The Braff Group (Pittsburgh) is the purest services specialist on this list: sell-side-only and healthcare-services-only, across behavioral health, home health / home care / hospice, healthcare staffing, home medical equipment (DME), and pharmacy. Founded in 1998 by Dexter Braff, the firm reports more than 375 transactions. Verified recent deals include Beneficial In-Home Care's sale to Family Resource Home Care (announced February 13 2025) and IV Solutions' sale to Singlepoint Healthcare (announced August 14 2025). Its 2025 behavioral-health update reported a record 31 intellectual-and-developmental-disability (IDD) deals and behavioral deal flow up about 17% year over year — a useful read on where services consolidation is hottest. For a behavioral, home-based-care, staffing, or DME seller, no firm here is more narrowly specialized — and on those assets, that single-mindedness is exactly the point.

VERTESS (headquartered in Fort Worth, Texas, and founded in Tucson, Arizona) is a lower-middle-market healthcare M&A firm whose managing directors are operators as well as bankers — covering behavioral health, IDD, autism / ABA, addiction, home care / home health / hospice, DME, pharmacy, urgent care, and dental. Its senior bench includes managing directors Bradley M. Smith and Alan J. Hymowitz, with David E. Coit Jr. leading valuation and financial analysis. VERTESS was named the number 1 lower-middle-market healthcare sell-side advisor by Axial in its 2024 Healthcare Top 50. Verified recent activity: VERTESS closed four sell-side deals between December 2025 and January 2026, including Gammie HomeCare's sale to AdaptHealth (DME) and a Connecticut Mental Health Specialists transaction, and earlier advised Shorehaven (a Maryland IDD provider) on its sale to Sevita (late April 2025). For a sub-$50M services seller who wants operator-led, sub-vertical-deep representation, VERTESS is the shop to beat at the small end.

Cross Keys Capital (Fort Lauderdale, Florida) is the physician-practice-management specialist, advising across 20-plus specialties — ophthalmology, anesthesiology, dermatology, ENT, orthopedics, urology, pain, urgent care, and veterinary — typically on private-equity recapitalizations. The firm reports more than 200 transactions over the prior decade. Its co-founder and Managing Director Bill Britton anchors the healthcare practice. For a multi-specialty or single-specialty physician group weighing a PE recap, Cross Keys lives inside the PPM platform-consolidation wave — that specialty-by-specialty sponsor map is precisely what it sells.

Edgemont Partners (New York) is a healthcare-services-focused independent bank with a dedicated franchise in post-acute care (home health, hospice, personal care), healthcare staffing, and healthcare distribution. Eugene Goldenberg is a Managing Director covering post-acute, staffing, and distribution. Edgemont's value is a deep, current relationship map among the PE platforms and strategics buying in those specific sub-verticals; for a post-acute, staffing, or distribution asset, that live buyer map is what you are actually hiring.

Ziegler (Chicago) is the specialist in senior living / seniors housing, skilled nursing, post-acute care, and not-for-profit hospitals and health systems — a distinct corner of healthcare services with its own buyer universe (regional operators, REITs, and not-for-profit systems) and its own financing needs. Its senior bench includes Dan Revie (Managing Director, Senior Housing & Care Finance), Christopher Utz (Managing Director), and Humair Sabir (Managing Director). Verified recent deals include the sale of BrightStar Senior Living of Mason, Ohio (July 2025), Kokoro Assisted Living's sale to Northstar Senior Living (September 1 2025), and OFFOR Health's sale to Havencrest Capital (April 9 2026). For a senior-living, skilled-nursing, or not-for-profit-hospital seller, Ziegler is the desk the REITs, regional operators, and not-for-profit systems in that niche already know.

Physician Growth Partners (Chicago) is the physician-practice pure-play on this list. Founded in 2017 by Michael Kroin (Founder and Managing Partner) and Ezra Simons (Managing Partner), the firm does one thing: represent independent physician groups, sell-side only, in recapitalizations and sales to private equity and strategic acquirers — with Robert Aprill (Managing Director) on the senior bench. The firm reports more than 90 physician-practice transactions and $3.5B-plus in enterprise value, concentrated in exactly the specialties PE is consolidating: dermatology, eye care, urology, orthopedics, gastroenterology, behavioral health, women's health, allergy/ENT, and oral surgery. Verified recent mandates map that consolidation wave: PGP advised UroPartners (the large Chicago independent urology group) on its private-equity partnership, served as exclusive transaction advisor to Urology America, advised Keystone Urology on its partnership with Solaris Health, and represented psych360 on its sale to MindCare. Its founders are regular voices in the PE-in-healthcare press — quoted in The New York Times and Crain's Chicago Business, with firm research cited by Becker's and KFF Health News. For a founder-owned physician group weighing a PE recapitalization, PGP's practice-only focus and friendly-PC/MSO structuring fluency make it a natural first call alongside Provident and Cross Keys.

Subsector-Specialist Gate. Healthcare M&A is not one market — it is roughly ten, each with a different buyer universe and a different advisor bench. The gate is close to binary: if your entire value story fits on the income statement, a strong generalist clears it — but the moment a material part of your value is sub-vertical-coded (payor mix, recurring-contract quality, clinical IP, an MSO structure, or scarcity under a CON or enrollment-moratorium regime), a generalist leaves that value uncredited and you need the specialist. Map your asset to its lane before you shortlist, and hire for the ability to read the part of your value that does not show up as EBITDA.

| What you're selling | Value driver | Best advisor type | Examples |

|---|---|---|---|

| Behavioral / autism-ABA / addiction platform | Payor mix, clinical quality, scale | Behavioral-focused services boutique | The Braff Group, VERTESS, Provident |

| Dental DSO or physician-practice group | De novo / same-store growth, MSO structure | PPM specialist | Provident, Cross Keys, Physician Growth Partners |

| Home health / hospice / personal care | Census, payor mix, Medicare enrollment | Post-acute specialist | The Braff Group, VERTESS, Edgemont, Cain |

| Senior living / skilled nursing | Occupancy, real estate, operator fit | Senior-living specialist | Ziegler |

| Medical device / medtech | Clinical IP, regulatory pathway, pipeline | Products / medtech bank | Piper Sandler, Houlihan Lokey, William Blair |

| Healthcare IT / HCIT SaaS | ARR, net revenue retention, data assets | HCIT specialist | William Blair, Piper Sandler, Harris Williams |

| Biopharma / therapeutics | Clinical data, patent runway, strategic fit | Pure-play / bulge-bracket biopharma | Leerink, Centerview, Evercore, Jefferies |

| CRO / CDMO / pharma services | Capacity, customer concentration, contracts | Pharma-services bank | Harris Williams, Houlihan Lokey, Cain |

Who advises on medtech and medical-device M&A?

Medical devices are a products business — value lives in clinical IP, the regulatory pathway, and pipeline depth, not in payor contracts — so the right advisor reads a 510(k) or PMA roadmap and reaches both strategic acquirers and device-focused sponsors. Two firms lead the middle market here.

Piper Sandler (Minneapolis) carries one of the deepest life-science tools and diagnostics franchises on the Street — more than 100 deals since 2012 — and extends naturally into medtech and devices, alongside biopharma and healthcare IT. Peter Day is Global Group Head of Healthcare Investment Banking; the firm has been adding senior bench, including Dan Wolf (Managing Director, healthtech, January 2026) and Jason Arnold (Managing Director, tools and diagnostics). For a diagnostics, life-science-tools, or device seller, Piper Sandler's tools-and-diagnostics franchise is the bench to beat. (I lead with the franchise rather than one named device mandate because that is where its edge concentrates.)

Houlihan Lokey (Los Angeles) is the dominant middle-market healthcare advisor by deal count, and its device and medtech coverage benefits from the same volume leadership and capital-solutions / restructuring bench that makes the firm a workhorse across healthcare. Its healthcare practice is led by Mark Francis (Global Head of Healthcare) and Michael Pisani (Co-Head of US Healthcare). For a middle-market device seller who wants sheer deal volume — plus a restructuring bench if the situation turns distressed — Houlihan Lokey closes more healthcare deals than anyone on this list. (I describe it through that volume leadership and its pharma-services depth rather than one named device deal.) (One brand note: Houlihan Lokey's healthcare practice is led by Francis and Pisani, not by the firm-wide corporate-finance leadership sometimes mistakenly cited as its healthcare head.)

Who are the best healthcare IT (HCIT) and healthtech M&A advisors?

Healthcare IT is a software business wearing a healthcare badge — value is recurring revenue, net revenue retention, and the data asset, but the buyer must clear healthcare-specific diligence (HIPAA, interoperability, payor integrations) — so the right advisor blends software-M&A fluency with healthcare relationships. Two middle-market firms lead, with a third strong on the larger end.

William Blair (Chicago) is a leading middle-market HCIT and medtech advisor with a dedicated Healthcare IT investment-banking practice and deep private-equity-sponsor relationships. Joe Schauenberg is a Managing Director and Head of Healthcare IT investment banking. A verified recent mandate shows the medtech-adjacent reach: William Blair advised Azenta on the sale of its B Medical Systems business to THELEMA (US$63M, announced December 29 2025). For a healthtech or HCIT SaaS company in the middle market, William Blair pairs a dedicated HCIT desk with a sponsor network few middle-market rivals can match.

Piper Sandler (profiled above for medtech) is equally credible in HCIT, with healthtech a named coverage area and Dan Wolf's January 2026 arrival reinforcing the bench. Harris Williams (profiled below) also runs a strong HCIT practice, led by Sam Hendler (who rejoined the firm in 2024), and is a natural fit for a larger sponsor-owned healthtech asset. The screening question for any HCIT advisor is the same Buyer-Universe Depth Test: ask which five software-focused and healthcare-focused buyers they would call first, and how many HCIT deals they closed in the last 18 months.

For context, HCIT valuations run on software math, not services math: profitable health-IT companies have traded around 10-14x EV/EBITDA, and SaaS-style HCIT assets are often valued on revenue multiples in the roughly 4-6x range (HGP Health IT Market Review, July 2025 — present these as ranges, because they swing hard with growth and retention).

Who are the best biopharma and therapeutics M&A advisors?

Biopharma is where the largest, most complex healthcare deals happen — value is set by clinical data, patent runway, and strategic fit, and the buyer set is dominated by large-cap pharma — so the leading advisors are the pure-play healthcare bank and the top independents. Four firms lead, and they cluster at the large-cap and multi-billion-dollar end.

Leerink Partners (Boston) is the pure-play healthcare bank. The ownership history is widely misstated, so state it correctly: the firm was formerly SVB Leerink / SVB Securities, and it became independent and employee-owned again via a 2023 Baupost-backed management buyout — it is not owned by SVB today. Its senior bench includes founder and CEO Jeffrey Leerink, Tom Davidson (Co-President / Co-Head of Global Investment Banking), and senior managing directors Grant Curry and Jason Truman (biopharma M&A, who joined in November 2024). Leerink ranked number 1 in US biopharma equity-deal market share in 2025 (Dealogic, per the Boston Globe, February 23 2026), overtaking Jefferies. A verified recent deal: Leerink advised GSK on its acquisition of IDRx ($1B upfront plus up to $150M in milestones, announced January 13 2025). For a therapeutics company that wants the one bank that does nothing but healthcare, Leerink is it.

Centerview Partners (New York) is the pre-eminent independent advisor on the largest, most complex biopharma M&A. Founded in 2006 by Blair Effron and Robert Pruzan, its healthcare practice was built by E. Eric Tokat (Co-President of Investment Banking and founder of the healthcare practice). Verified recent mega-deals show the franchise's altitude: Centerview advised Verona Pharma on its roughly $10B sale to Merck (closed October 7 2025) and advised Intra-Cellular Therapies (alongside Jefferies) on its roughly $14.6B sale to Johnson & Johnson (closed April 2 2025). For a large-cap therapeutics board that wants the most senior independent counsel on the Street, Centerview is where those boards land — well above this guide's lower-middle-market center of gravity, but named here to frame the ceiling.

Evercore (New York) is a top independent advisor that aggressively expanded its healthcare bench in 2025. Its senior bench includes Naveen Nataraj (Co-Head of US Investment Banking), François Maisonrouge (Chairman, global healthcare), and Joe Modisett (Senior Managing Director, who joined in March 2025 from Morgan Stanley, where he was global head of healthcare investment banking). I am describing Evercore through its top-five independent standing and its 2025 senior hires rather than a specific named healthcare mandate; the signal here is the bench it assembled.

Jefferies (New York) runs one of the highest-volume healthcare franchises anywhere — more than 140 healthcare bankers — and is especially strong in biotech equity capital markets and mid-cap M&A. Tommy Erdei is Joint Global Head of Healthcare Investment Banking. Jefferies held the number 1 spot in US biopharma equity-deal share before Leerink overtook it in 2025, and it co-advised Intra-Cellular Therapies on its roughly $14.6B sale to Johnson & Johnson. It also hosts the influential Jefferies Global Healthcare Conference. For a biotech that needs M&A advice and equity-financing muscle under one roof, Jefferies's volume-plus-ECM combination is hard to replicate.

Who advises on CRO / CDMO and pharma-services M&A?

CRO/CDMO and pharma services is a hybrid — part products, part services — where value lives in capacity, customer concentration, and long-term supply contracts, and the buyer set is sponsors and strategics chasing outsourced-pharma scale. One firm stands out, with two more credible at scale.

Harris Williams (Richmond, Virginia) is a premier middle-market healthcare and life-sciences sell-side advisor with a standout pharma-services / contract-manufacturing (CDMO / CRO) franchise serving private-equity sponsors. It is a subsidiary of PNC Financial Services that operates as an independent M&A advisory brand (there has been no 2024-26 rebrand). Its healthcare and life-sciences practice is co-led by Cheairs Porter and Geoff Smith, with Sam Hendler leading HCIT (he rejoined the firm in 2024). For a sponsor-owned CDMO, CRO, or broader pharma-services asset in the middle market, Harris Williams runs one of the deepest contract-manufacturing franchises on the Street. (I describe it through that franchise rather than one named tombstone, because its most recent publicly verifiable healthcare deals skew older — worth confirming with the firm directly.)

Houlihan Lokey (profiled above) carries deep pharma-services capability alongside its middle-market volume leadership, and Cain Brothers (profiled above) covers pharma services within its broad platform. The pharma-services market saw at least one landmark transaction recently — Novo Holdings' roughly $16.5B acquisition of Catalent (a CDMO), valued at about 22.9x EBITDA, which was announced and completed in 2024 (note the year: this was a 2024 deal, not a 2025 one). It is a useful benchmark for the premium multiples a scaled, well-contracted CDMO can command, even if it sits well above the middle-market band most readers occupy.

How do CON, the Corporate Practice of Medicine, and PE scrutiny discount your multiple?

In 2026, three regulatory forces act as what I call the Regulatory-Overhang Discount — a discount or a delay on your multiple if your advisor cannot pre-empt them in process design. This is the single biggest piece of information gain in healthcare M&A advisor selection, because it is where a specialist most clearly out-earns a generalist.

Certificate of Need (CON). In roughly three dozen states, a buyer must obtain or transfer a CON to operate or expand regulated facilities — ambulatory surgery centers, home health agencies, hospital beds, and more. CON cuts both ways: it can slow a deal (the transfer is a closing condition and a timeline risk), but it can also make an already-licensed, compliant asset scarcer and more valuable, because a buyer cannot simply stand up a competing facility. A specialist sequences the CON transfer into the deal timeline and prices the scarcity; a generalist treats it as an afterthought and risks a delayed or repriced close.

The Corporate Practice of Medicine (CPOM). A tightening doctrine in 2026. California's SB 351 (signed October 6 2025) strengthened CPOM against private-equity and hedge-fund control of medical practices, and AB 1415 (signed October 11 2025) expanded pre-close notice to California's Office of Health Care Affordability (OHCA) for PE / MSO "material change" transactions. The practical consequence: a PE-owned physician practice must be structured through a compliant friendly-PC / management-services-organization (MSO) arrangement — the physician entity owns the clinical practice, the MSO provides non-clinical services under a management agreement — or the deal is exposed to enforcement and to a buyer's diligence discount. A specialist designs (or repairs) the MSO structure before launch; a generalist walks a buyer straight into it.

Antitrust and PE roll-up scrutiny. The FTC, DOJ, and HHS issued a joint request for information on healthcare consolidation on March 5 2024 (comment period extended to June 5 2024) that explicitly targets PE "roll-ups" of sub-HSR-threshold acquisitions, cross-market hospital mergers, and cross-ownership. States have layered on their own reviews: Indiana requires healthcare entities to notify the Attorney General 90 days before deals at or above $10M (effective July 1 2024; amended July 1 2025 to exclude provider groups majority-owned by licensed Indiana practitioners), and Oregon's transaction-review program survived a constitutional challenge (a federal appellate decision issued July 3 2025). A specialist positions your deal narrative against the roll-up frame and sequences the state Health Care Transaction (HCT) filings; a generalist underestimates them.

On thresholds: federal HSR review applies above the size-of-transaction threshold, which is re-indexed annually (it was about $126.4M for 2025) — confirm the current-year figure with counsel, because it moves. None of this is legal advice; retain experienced healthcare regulatory counsel early, and treat the structure work as part of the advisor's job, not an afterthought.

Regulatory-Overhang Discount. Three 2026 forces discount or delay a healthcare deal unless the advisor pre-empts them. A specialist structures around each; a generalist walks into them.

- Certificate of Need (CON): transfer is a closing condition and timeline risk — but already-licensed assets are scarcer and can command a premium. Sequence the transfer; price the scarcity.

- Corporate Practice of Medicine (CPOM): California SB 351 + AB 1415 tightened the doctrine; PE deals need a compliant friendly-PC / MSO structure or face a diligence discount.

- FTC / DOJ / HHS + state review: the 2024 RFI targets PE roll-ups; Indiana ($10M AG notice) and Oregon (review regime upheld) add state layers. Position against the roll-up narrative; sequence HCT filings.

A specialist who pre-clears your structure in week one protects both your multiple and your timeline. None of this is legal advice — retain healthcare regulatory counsel early.

How much is your healthcare company worth? The reimbursement-mix multiple ladder

Within any healthcare subsector, the biggest single value lever is payor mix — and this is what I call the Reimbursement-Mix Multiple Ladder. Two otherwise-identical agencies or practices can trade a full turn or more apart on EBITDA purely on the basis of how much of their revenue comes from commercial payors versus Medicare and Medicaid. High commercial-payor assets trade at the top of every subsector range; Medicare/Medicaid-dependent assets trade at the bottom, because the buyer underwrites reimbursement risk, rate pressure, and policy exposure into the price.

The ladder itself is simple — here are the rungs:

| Commercial-payor share of revenue | Where it puts you in your subsector's range | Why the buyer prices it there |

|---|---|---|

| Over 70% commercial | Top of the range, sometimes above it | Rate stability, little policy-cut exposure, real pricing power — buyers pay up for predictable cash flow |

| ~40–70% commercial (balanced) | Middle of the range | Diversified but partly exposed to government rate action — the default underwriting case |

| Under 40% commercial (Medicaid/Medicare-heavy) | Bottom of the range | Buyer underwrites rate-cut risk, policy exposure (reimbursement cuts, moratoria), and payor concentration |

The rungs are not absolute — a government-pay-heavy asset with genuine scale, scarcity (a CON-restricted market, an enrollment moratorium), or clinical differentiation can climb a rung — but as a first-cut rule of thumb, every 10–15 points of commercial-payor mix is worth on the order of a quarter to half a turn of EBITDA within a subsector band. That is why two agencies with identical EBITDA can trade a full turn apart on price.

The subsector ranges below set the broad bands; your position within each band is driven by payor mix, scale, clinical quality, and growth. Treat every figure as an indicative range, not a quote — multiples move with the cycle and with the specific asset.

| Subsector | Indicative 2026 EBITDA multiple range | Source |

|---|---|---|

| Autism / ABA (platform) | ~12-15x | FOCUS Investment Banking, Dec 2025 |

| Mental health (platform / add-on) | ~10-14x platform / ~4-8x add-on | FOCUS Investment Banking, Dec 2025 |

| IDD | ~9-12x | FOCUS Investment Banking, Dec 2025 |

| Addiction treatment | ~8-11x | FOCUS Investment Banking, Dec 2025 |

| Dental DSO | ~9-12x (5-7x sub-$1M EBITDA, 10-12x at $5M+) | FOCUS Investment Banking, Apr 2026 |

| Physician practices | ~6-12x (by specialty and size) | Sofer Advisors, 2025-2026 |

| Home health | ~7.5-9.5x | FOCUS Investment Banking, 2026 |

| Hospice | ~9-12.5x | FOCUS Investment Banking, 2026 |

| Ambulatory surgery centers (ASC) | ~5-8x single-specialty, 6-10x multi, 11-17x ops | Scope Research, 2025 |

| Medtech / devices | ~10-20x EBITDA (broad), ~18x EV/EBITDA NTM marker | Practitioner trackers, 2025 |

| Healthcare IT (profitable) | ~10-14x EV/EBITDA; ~4-6x revenue for SaaS | HGP Health IT Market Review, July 2025 |

Two data points anchor the range. The autism/ABA and IDD segments have been among the hottest — The Braff Group reported a record 31 IDD deals in 2025 and behavioral flow up about 17% year over year, and IDD deal count was up about 113% year over year per FOCUS. And as an illustrative post-acute benchmark, Enhabit Home Health & Hospice's sale to Kinderhook Industries at roughly $1.1B implied about 10.2x — useful as a directional marker for a scaled, multi-line post-acute platform, not a rule for a single small agency.

Reimbursement-Mix Multiple Ladder. Payor mix is the biggest value lever within any subsector — and it moves you rung by rung, not vaguely: >70% commercial sits at the top of the range, 40–70% in the middle, sub-40% / government-heavy at the bottom, with roughly a quarter to half a turn of EBITDA riding on every 10–15 points of commercial mix. Before you go to market, know your mix, defend it with clean billing and coding data, and pick an advisor who positions it — that is where a specialist out-earns a generalist on your actual sale price.

Why does the CMS enrollment moratorium make some agencies more valuable?

In 2026, a regulatory action created a genuine scarcity premium for a specific group of healthcare-services sellers — what I call the Scarcity-Premium-from-Moratorium frame. On May 13 2026, CMS announced and made effective a nationwide six-month moratorium on new Medicare enrollments for Hospice and Home Health Agencies (extendable in six-month increments). Existing, already-enrolled providers are unaffected.

The market consequence is direct: if a buyer cannot stand up a new Medicare-enrolled hospice or home-health agency for at least six months — and possibly longer if the moratorium is extended — then an already-enrolled, compliant agency becomes the only fast way to enter or expand in a market. Scarcity is value. A subsector specialist in home health and hospice (The Braff Group, VERTESS, Edgemont, Cain Brothers) prices that scarcity into the process and uses it to drive competitive tension among the buyers who need enrolled capacity now. There is a deal-structure wrinkle the specialist has to navigate, though: the moratorium reaches not just brand-new enrollments but certain changes in majority ownership, so how the transaction is structured — and whether it preserves the target's existing Medicare enrollment rather than tripping a fresh one — becomes part of the value the advisor protects. A generalist who does not track CMS enrollment policy misses the lever entirely.

This is a clean example of why the advisor's regulatory fluency is not a nice-to-have — it is a direct input into your sale price. The same regulatory layer that creates the Regulatory-Overhang Discount on the wrong deal creates a scarcity premium on the right one, and only an advisor tracking the policy in real time can tell you which side of the line your asset sits on.

What do healthcare M&A advisors charge in 2026?

Healthcare M&A advisors price like the broader lower-middle and middle market — a monthly retainer or work fee plus a success fee at close — with the success rate declining as deal size grows. The mechanics are the same across sectors, so I will keep this tight and point you to the dedicated fee hub for the full math.

The baseline curve puts the effective success fee at roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex / Axial M&A Fee Guide). Lehman is not obsolete — a declining Lehman-style structure is still the single most common arrangement (about 44% of engagements). In the lower middle market you will most often be quoted the Double Lehman (10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% of everything above $5M): on a $20M deal that computes to $600,000, or 3.0%. On a ~$50M healthcare deal, blended success fees commonly land in the roughly 2-4% range depending on structure and subsector; smaller lower-middle-market deals (a single dental group, a small agency) run higher on Double Lehman, while larger middle-market deals blend down toward 1-2%.

| Deal size (EV) | Typical structure | Blended success fee | Healthcare-specific note |

|---|---|---|---|

| $20M-$50M | Double Lehman (10-8-6-4-2) | ~2.5%-4% | Smaller single-site deals sit at the higher end; retainer common |

| $50M-$150M | Double Lehman or negotiated flat | ~2.0%-2.5% | Confirm a senior banker runs it; subsector buyer map is what you pay for |

| $150M-$300M | Lehman with flat tier above threshold | ~1.5%-2.0% | Top of middle market; fees compress |

| $300M+ | Negotiated flat / stepped | ~1.0%-1.5% | Bulge-bracket / top-independent territory; negotiate % and tail |

Retainers commonly run $25,000-$100,000-plus (monthly or a fixed up-front amount), and most are credited against the success fee if the engagement letter says so in writing; minimum-fee floors mean that on a small deal the floor, not the percentage, can set the bill. Two clauses to negotiate hard: how transaction value is defined (equity versus enterprise value including assumed debt, and how earnouts and physician rollover equity count — a broad definition inflates the base on the same headline price), and the tail (limit it to a named-buyer list the banker delivers shortly after termination). The full mechanics — including a worked Lehman-versus-Double-Lehman comparison — are in our M&A advisor fees hub.

What should be in your data room before you take a healthcare company to market?

A healthcare data room is more sensitive than a generic M&A room, and getting it right before launch is the cheapest lever you control on both timeline and price. Beyond the standard corporate, financial, and legal sections, healthcare buyers expect a billing-and-coding section (a sample of claims, denial rates, and a quality-of-earnings analysis that ties to payor data), a payor-contract schedule with commercial-versus-government mix and rate detail, licensure and accreditation (state licenses, Medicare/Medicaid enrollment, CON documentation, Joint Commission or CARF accreditation where relevant), a regulatory and compliance section (HIPAA policies, OIG exclusion checks, any corporate-integrity-agreement history), and — for PE-owned practices — the friendly-PC / MSO structure documents that demonstrate Corporate Practice of Medicine compliance. HCIT rooms add security and interoperability documentation; device and pharma-services rooms add regulatory filings (510(k)/PMA, FDA correspondence) and quality-system records.

The room should be staged: a teaser and high-level summary behind a clickthrough NDA, then the full room released to NDA-signed bidders, with the most sensitive material — detailed payor contracts, physician-compensation detail, patient-level data (de-identified per HIPAA), and litigation files — held to a short list only after indications of interest. This staged, permissioned release is exactly what we built Peony — used by 5,900+ customers — to handle: per-bidder watermarks on every page render, staged folder permissions, and page-level analytics that show your banker which bidders are genuinely working the file. For a biopharma or device seller, the biotech M&A data room and biotech data room guide cover the products-side buildout; the general sell-side mechanics are in our M&A data room and due diligence checklist guides. Peony is the document layer, not the advisor — but a clean, staged room is the prep that makes everything the advisor does next faster and more competitive.

Honest comparison: which advisor fits which lane?

No single firm wins every healthcare mandate. This matrix maps subsector and deal size to the firms that genuinely fit — and concedes where a generalist, a relationship-driven direct deal, or a mega-bank is the better call than a subsector boutique.

| Subsector | $20M-$75M | $75M-$250M | $250M-$500M | $500M+ / mega |

|---|---|---|---|---|

| Behavioral / ABA / addiction | VERTESS + The Braff Group | The Braff Group + Provident | Provident + Cain Brothers | Cain Brothers + bulge |

| Dental DSO / physician practices | Cross Keys + Physician Growth Partners | Provident + Physician Growth Partners | Cain Brothers + Provident | Cain Brothers + bulge |

| Home health / hospice / post-acute | VERTESS + The Braff Group | The Braff Group + Edgemont | Edgemont + Cain Brothers | Cain Brothers + bulge |

| Senior living / skilled nursing | Ziegler | Ziegler | Ziegler + Cain Brothers | Cain Brothers + Ziegler |

| Medtech / devices | William Blair + Piper Sandler | Piper Sandler + Houlihan Lokey | Houlihan Lokey + Piper Sandler | Evercore + bulge |

| Healthcare IT / HCIT | William Blair + Piper Sandler | William Blair + Harris Williams | Harris Williams + Houlihan Lokey | Evercore + Jefferies + bulge |

| Biopharma / therapeutics | (boutique scarce — Leerink early) | Leerink + Jefferies | Leerink + Jefferies + Evercore | Centerview + Leerink + Evercore |

| CRO / CDMO / pharma services | Harris Williams + Houlihan Lokey | Harris Williams + Houlihan Lokey | Houlihan Lokey + Cain Brothers | Centerview + bulge |

The honest limits to flag:

- Above ~$500M EV in biopharma — the mega-banks (Centerview, Evercore, Leerink, Jefferies) and bulge brackets bring the strategic relationships, fairness opinions, and stock-deal mechanics that matter, and this guide's lower-middle-market frame no longer applies.

- A single dominant strategic buyer with a deep existing relationship — if your CEO or board already has the relationship that will set the price (a regional health system that has wanted your practice for years, a strategic that already partners with you), a trusted generalist with that relationship, or a direct negotiation with a fairness opinion, can beat a specialist's broad process. Competition moves price; the specialist's value is creating it where it does not already exist.

- A very small, single-site practice — a solo dental or physician office may be better served by a healthcare-experienced business broker than by a middle-market bank whose minimum-fee floor would consume an outsized share of proceeds.

- A complex regulatory situation — if your deal lives or dies on CON, CPOM, or a state HCT review, weight the choice toward the advisor with the most demonstrated experience structuring around exactly that constraint, even over one with a slightly better headline buyer list.

For the healthcare deals that do fit this guide — the $20M-$500M services, products, tech, and pharma sellers who make up the bulk of the market — a subsector specialist with a documented buyer-relationship map and the regulatory fluency to pre-empt the overhang is hard to beat, and a clean, staged data room prepared before launch is the cheapest lever you control on both timeline and price.

Bottom line

Healthcare M&A does not have one league table — it splits into a services side and a products / tech / pharma side, and within each into roughly ten sub-markets, where the firm that dominates one is often irrelevant in another. For a $20M-$500M seller, the working core on the services side is Cain Brothers, Provident Healthcare Partners, The Braff Group, VERTESS, Cross Keys Capital, Edgemont Partners, Ziegler, and Physician Growth Partners; on the products / tech / pharma side, the workhorses are Houlihan Lokey, William Blair, Piper Sandler, and Harris Williams, with Leerink, Centerview, Evercore, and Jefferies built for the large-cap and multi-billion-dollar biopharma deals that frame the ceiling.

The single most important advisor-selection question for a healthcare seller is the Buyer-Universe Depth Test: which firm can name the five buyers — the specific PE platforms and strategics — it would call first for my exact subsector asset, has closed deals in that niche in the last 18 months, and can pre-empt my regulatory exposure (CON, the Corporate Practice of Medicine, the FTC's roll-up scrutiny) by structuring the deal correctly before launch? In a market this segmented and this regulated, that combination of a current buyer Rolodex and structuring fluency is the whole edge. We serve 5,900+ customers on the data-room side of exactly these deals — and the prep you do before you pick an advisor (a clean quality-of-earnings, a compliant MSO structure, a defensible payor-mix story, a staged and watermarked data room) compounds everything the advisor does next.

Related resources

- M&A advisor vs broker vs investment bank — the decision that comes before this healthcare shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- 16 Best Energy M&A Advisors in the US — the sibling national sector hub: the same subsector-specialist logic applied to upstream, midstream, oilfield services, power, and renewables

- 13 Best Technology & Software M&A Advisors — the sibling national sector cut: SaaS, infrastructure & data/AI, cybersecurity, fintech, and IT-services advisors mapped by subsector

- Biotech M&A data room (2026) — the products-side data-room buildout for a biopharma or device sale

- Biotech data room guide — the life-sciences data-room structure behind a fundraise or sale

- M&A data room: setup and workstream mapping — the general sell-side data-room playbook

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, the right-sized room for a single-site practice or small agency

- Due diligence data room checklist — the document checklist a healthcare buyer will work through

- Best M&A Advisors in Boston — the geo cut of this national hub: the East Coast healthcare-and-life-sciences bench

- Best M&A Advisors in Nashville — the healthcare-services capital geo cut

- Best M&A Advisors in Chicago — the Midwest healthcare and middle-market geo cut

- Best M&A Advisors in NYC — the large-cap and biopharma geo cut

- Best M&A Advisors in Philadelphia — the Mid-Atlantic pharma and life-sciences geo cut

- Best M&A Advisors in San Francisco — the West Coast healthtech and life-sciences geo cut

- Best M&A Advisors in Raleigh-Durham — the Research Triangle geo cut: CRO, pharma-services, and bioanalytical-lab sellers in the market this hub's specialists fly into

Frequently asked questions

Do I need a healthcare-specialist M&A advisor, or will a generalist investment bank do?

For almost every healthcare seller, a subsector specialist beats a generalist — but the reason is specific, not snobbery. Healthcare M&A is not one market; it is roughly ten (physician practices, behavioral health, dental, home health and hospice, senior living, medtech, healthcare IT, biopharma, CRO/CDMO, distribution), and each has a different buyer universe, a different valuation logic, and a different regulatory overhang. This is what I call the Subsector-Specialist Gate: a generalist who runs a clean EBITDA-multiple process will under-credit the parts of your value that live in your payor mix, your recurring-revenue contracts, your clinical IP, or your scarcity under a Certificate-of-Need regime — and, just as costly, will not have direct lines to the dozen or so private-equity platforms and strategics actually buying your exact asset right now. The honest exception: if your most likely buyer is a single strategic your CEO already knows well, a trusted generalist or a direct negotiation can sometimes beat a specialist's broad process, because competition moves price, not the logo on the pitch book. But in a market this segmented and this regulated, the specialist's buyer Rolodex and structuring fluency are usually worth more than any fee difference. The intermediary-type decision sits upstream in our M&A advisor vs broker vs investment bank hub. We run Peony, a data room company that has served 5,900+ customers, and across hundreds of healthcare processes the advisors who genuinely engage are the ones who can name your five most likely buyers without hesitating.

Do I even need a banker to sell my healthcare company, or can I handle a direct PE offer myself?

If a private-equity firm has already made you an unsolicited offer, you almost certainly still need an advisor — and that is exactly the situation where one pays for itself. A single inbound offer is, by definition, a process with no competition, and competition is the thing that moves price. A healthcare-specialist banker turns one bid into several by quietly running the same asset past the other platforms consolidating your subsector, which both tests whether the inbound number is fair and gives you the leverage to improve it on price, structure, rollover equity, and the employment and non-compete terms that matter to a physician owner. The PE buyer who approached you does this for a living and runs dozens of deals a year; most founders sell once. The narrow case where a direct sale can work without a full process is a small, simple practice with a buyer you trust and a fairness check from a healthcare-literate transaction attorney and accountant — but even then, a quality-of-earnings analysis and a tax-structuring review are worth their cost. The deeper distinction between an M&A advisor, an investment bank, and a business broker is in our advisor vs broker vs investment bank guide.

Who are the best M&A advisors for a behavioral health, autism/ABA, or addiction-treatment company?

Behavioral health has its own deep specialist bench, because it is one of the most actively consolidated corners of healthcare and the buyer set is almost entirely behavioral-focused private equity. The standout sell-side specialists are The Braff Group (Pittsburgh, sell-side-only and healthcare-services-only, with behavioral health as a core practice — it reported a record 31 intellectual-and-developmental-disability deals in 2025 and behavioral deal flow up about 17% year over year), VERTESS (Tucson and Dallas-Fort Worth, lower-middle-market behavioral, IDD, autism/ABA and addiction, named Axial's number 1 lower-middle-market healthcare sell-side advisor for 2024), and Provident Healthcare Partners (Boston, with a long autism and behavioral track record). For the buyer-relationship map, the screening question matters: ask each firm how many behavioral deals they closed in your exact sub-vertical — ABA, mental health, IDD, or addiction — in the last 18 months. Subsector multiples vary widely: mental-health platforms have traded around 10-14x EBITDA with add-ons at 4-8x, autism/ABA platforms around 12-15x, IDD around 9-12x, and addiction around 8-11x (FOCUS Investment Banking, December 2025) — though every range depends on payor mix, scale, and clinical quality. The full subsector roster and the products-versus-services split are mapped below.

Which advisor should I use to sell a dental DSO, physician practice, or home health / hospice agency?

Each of these is a distinct services sub-vertical with its own specialist, so match the advisor to the asset. For a dental DSO or a multi-site physician practice, the physician-practice-management (PPM) specialists lead: Provident Healthcare Partners (Boston, deep PPM and dental), Cross Keys Capital (Fort Lauderdale, physician practices across 20-plus specialties including ophthalmology, anesthesiology, dermatology, ENT, orthopedics, urology, and pain), and Physician Growth Partners (Chicago, physician-practice-only sell-side with 90-plus PPM transactions and $3.5B-plus in enterprise value, confirmed with the firm's Director). For home health, hospice, and personal care, the post-acute specialists are The Braff Group (a core home-health/hospice practice), VERTESS (home care, home health, hospice, and DME in the lower middle market), Edgemont Partners (a dedicated post-acute, staffing, and distribution franchise), and Cain Brothers for larger platforms. For senior living and skilled nursing specifically, Ziegler (Chicago) is the reference name. Indicative multiples: dental DSOs roughly 9-12x EBITDA (with smaller sub-$1M-EBITDA practices at 5-7x scaling to 10-12x at $5M-plus); physician practices roughly 6-12x depending on specialty and size; home health about 7.5-9.5x and hospice about 9-12.5x in 2026 (FOCUS Investment Banking; Sofer Advisors). One 2026 wrinkle for home-health and hospice sellers specifically: CMS announced a six-month moratorium on new Medicare enrollments effective May 13 2026, which makes already-enrolled, compliant agencies scarcer — a point a subsector specialist will price in.

Boutique healthcare bank vs a bulge-bracket — which is better for a $50-150M deal?

For a $50-150M healthcare deal, a healthcare-focused boutique or middle-market bank almost always beats a bulge bracket — not because the bulge bracket is bad, but because your deal is below its attention and minimums, so you would be its smallest mandate of the quarter and risk being staffed with juniors. In the $50-150M band the right names are the dedicated healthcare-services boutiques (Provident, The Braff Group, Cross Keys, Physician Growth Partners, Edgemont, Ziegler, Cain Brothers) and the middle-market product/tech specialists (Houlihan Lokey, William Blair, Piper Sandler, Harris Williams), all of which put senior bankers on buyer calls and carry a current buyer Rolodex in your exact sub-vertical. The mega-banks — Centerview, Evercore, Jefferies, Leerink — are built for the multi-billion-dollar biopharma and platform deals where stock mechanics, fairness opinions, and global strategic relationships dominate; below roughly $250M their model is a poor fit on both economics and attention. The honest filter: at $50-150M, choose the advisor with the deepest documented relationships among the specific PE platforms and strategics buying your subsector, and confirm in writing which senior banker will be on every buyer call. The full intermediary decision is in our advisor vs broker vs investment bank hub.

What's the difference between a healthcare M&A advisor, an investment bank, and a business broker?

The three differ by deal size, process sophistication, and — critically in healthcare — regulatory and licensing fluency. A business broker typically handles smaller, often single-location practices (a solo dental or physician office, a small agency), usually on a listing-and-buyer-matching model, and is the right fit at the low end where the buyer pool is local and the deal is simple. An M&A advisor or boutique investment bank runs a competitive, confidential process for lower-middle and middle-market healthcare companies (roughly $20M-$500M of value): a curated buyer list of PE platforms and strategics, a managed data room, multiple bids, and negotiation on price, structure, rollover, and reps. A full-service or bulge-bracket investment bank adds balance-sheet financing, equity capital markets, and the scale for $500M-plus and multi-billion-dollar deals. The healthcare-specific layer that cuts across all three: your intermediary must understand Corporate Practice of Medicine constraints, the friendly-PC/MSO structure, Certificate-of-Need, and the 2026 FTC/DOJ/HHS scrutiny of PE roll-ups — get the structure wrong and you create a regulatory problem that discounts or delays the deal. We walk the full three-way comparison, including the licensing line, in our M&A advisor vs broker vs investment bank hub.

How does a healthcare sell-side process actually work, and how long does it take?

A healthcare sell-side process runs in five broad phases and typically takes six to nine months from kickoff to close — longer when regulatory review is on the critical path. Phase one (four to eight weeks) is preparation: the advisor builds the confidential information memorandum, a quality-of-earnings analysis, and the data room, and — uniquely in healthcare — pressure-tests your corporate structure for Corporate Practice of Medicine compliance and maps which state filings (Certificate-of-Need, state Health Care Transaction notices, HSR) will apply. Phase two (three to five weeks) is outreach to a curated buyer list of PE platforms and strategics, behind a teaser and an NDA. Phase three (four to six weeks) is management presentations and first-round indications of interest. Phase four (six to ten weeks) is confirmatory due diligence with a short list — billing and coding audits, payor-contract review, regulatory and licensure review, and a quality-of-earnings deep dive — running in parallel with purchase-agreement negotiation. Phase five is signing and the gap to close, which in healthcare can stretch on regulatory approvals: HSR, state HCT-review filings, CON transfers, and licensure re-credentialing. The single biggest schedule risk is regulatory sequencing, which is exactly why a subsector specialist who pre-clears the structure in phase one protects your timeline. The data-room mechanics are in our M&A data room and due diligence checklist guides.

How do CON, the Corporate Practice of Medicine, and 2026 FTC/DOJ scrutiny of PE roll-ups affect my sale?

In 2026 these three forces act as a Regulatory-Overhang Discount — a discount or a delay on your multiple if your advisor cannot pre-empt them in process design. First, Certificate of Need (CON): in roughly three dozen states, a buyer must obtain or transfer a CON to operate facilities like ambulatory surgery centers, home health agencies, and hospital beds, which can both slow a deal and, paradoxically, make an already-licensed asset scarcer and more valuable. Second, the Corporate Practice of Medicine (CPOM): a tightening doctrine — California's SB 351, signed October 6 2025, strengthened CPOM against private-equity and hedge-fund control, and AB 1415 (signed October 11 2025) expanded pre-close notice to California's Office of Health Care Affordability — so PE-owned practices must use a compliant friendly-PC / management-services-organization (MSO) structure or the deal is exposed. Third, antitrust and PE scrutiny: the FTC, DOJ, and HHS issued a joint request for information on healthcare consolidation (March 5 2024, comment period extended to June 5 2024) explicitly targeting PE roll-ups of sub-HSR-threshold acquisitions, cross-market hospital mergers, and cross-ownership, and states like Indiana (AG pre-close notice for deals at or above $10M, effective July 1 2024) and Oregon (a transaction-review regime upheld by a federal appellate decision on July 3 2025) have layered on their own reviews. A subsector specialist structures around all three — a CPOM-compliant MSO, sequenced state filings, and a deal narrative positioned against the roll-up frame; a generalist walks into them. None of this is legal advice — retain healthcare regulatory counsel early.

How do I tell if an advisor is a real healthcare specialist — and what are the red flags?

Run what I call the Buyer-Universe Depth Test: ask each advisor to name the five buyers they would call first for your specific subsector asset, and how many deals they have closed in that exact niche in the last 18 months. A genuine specialist answers without hesitation, naming specific PE platforms and the corporate-development teams they actually know; a generalist gives you generic categories or a stale list. The red flags are concrete. First, no recent closings in your exact sub-vertical — a banker with broad healthcare logos but zero ABA or dental or home-health deals in the last year and a half is learning on your dime. Second, a buyer list that is all strategics and no sponsors (or vice versa), which leaves half the competition on the table. Third, no fluency on the regulatory layer — if they cannot explain how Corporate Practice of Medicine or Certificate-of-Need affects your deal, they will not pre-empt the Regulatory-Overhang Discount. Fourth, junior staffing — confirm in writing which senior banker is on every buyer call. Fifth, a quality-of-earnings or billing-audit blind spot, which surfaces late and kills deals. The fee delta between two credible specialists is almost always dwarfed by the price delta a competitive, well-run process produces, so screen hard on buyer reach and subsector closings, not on the lowest quoted percentage.

Are healthcare valuations down in 2026, and will PE scrutiny lower my exit multiple?

The headline is down, but the headline is misleading for most sellers. Health-services M&A fell to roughly 910 deals in 2025 from 1,373 in 2024 (about a 34% drop), with disclosed value around $46B versus $62B (PwC / Fierce Healthcare, 2026) — but that decline is concentrated in hospitals and large-cap platforms, where deal count hit its lowest level since 2011 and a record 43.5% of hospital deals involved a distressed seller (Kaufman Hall, January 2026). The lower-middle-market services segment held up far better, and Q1 2026 hospital M&A re-accelerated. Blended healthcare-services multiples did compress — a median around 11.5x in 2025 versus about 14.5x in 2024 (Sofer Advisors) — so realistic expectations matter, but high-quality assets in actively consolidated niches (autism/ABA, dental, behavioral, home-based care) still command premium multiples. The PE-scrutiny effect is real but specific: it lengthens timelines and adds regulatory conditions rather than uniformly cutting prices, and it bites hardest on the exact roll-up patterns the FTC flagged. The single biggest value lever is not the macro — it is your payor mix, which is the heart of the Reimbursement-Mix Multiple Ladder: high commercial-payor assets trade at the top of every range, Medicare/Medicaid-dependent assets at the bottom. A specialist positions your mix, your scale, and your clinical quality to land high in your subsector's range.

How much do healthcare M&A advisors charge — retainer, and what % on a $50M deal?

Healthcare M&A advisors price like the broader lower-middle and middle market: a monthly retainer or work fee plus a success fee at close, with the success rate declining as deal size grows. Industry benchmarks put the effective success fee around 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex / Axial M&A Fee Guide), so a $50M healthcare deal commonly lands in the roughly 2-4% blended range depending on structure and subsector. Smaller lower-middle-market healthcare deals — a single dental group, a small agency — run higher, often on a Double Lehman formula (10-8-6-4-2% by tranche). Retainers typically run $25,000-$100,000-plus (monthly or a fixed up-front amount), and most are credited against the success fee if the engagement letter says so in writing, with a minimum-fee floor that, on a small deal, can set the bill more than the percentage does. Two clauses to negotiate hard: how transaction value is defined (equity versus enterprise value including assumed debt, and how earnouts and rollover equity count — a broad definition inflates the base), and the tail, which should be limited to a named-buyer list the banker delivers shortly after termination. The full mechanics, including a worked Lehman-versus-Double-Lehman comparison, are in our M&A advisor fees hub.

Is Lehman or Double Lehman standard for healthcare M&A, and are boutique fees worth it?

Lehman is not obsolete — a declining Lehman-style structure is still the single most common arrangement (roughly 44% of engagements), and in the lower middle market you will most often be quoted the Double Lehman: 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M. On a $20M deal that computes to $600,000, or 3.0%; on larger middle-market healthcare deals banks negotiate a flat or stepped structure that blends down toward 1-2%. Whether a boutique's fee is worth it comes down to one question: does the specialist's buyer relationships and subsector fluency produce a higher net price than a cheaper generalist would? In healthcare the answer is usually yes, for two reasons — the specialist reaches the handful of PE platforms actively buying your niche (creating the competition that moves price), and the specialist pre-empts the Regulatory-Overhang Discount by structuring the deal correctly the first time, which protects both your multiple and your timeline. The fee delta between two credible advisors is almost always smaller than the price delta a competitive process produces, so negotiate the percentage and the tail, but choose on buyer reach and regulatory fluency. The full fee math, retainer-credit mechanics, and engagement-letter traps are in our M&A advisor fees hub.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 5,900+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, industrials, and energy in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Contact: sean@peony.ink • LinkedIn.

You might also like

May 19, 2026

14 Best M&A Advisors in Nashville for $5M-$300M Deals (2026)

Jun 16, 2026

18 Best Financial Services & FIG M&A Advisors for $25M-$1B Deals (2026)

Jun 15, 2026

22 Best Industrial & Manufacturing M&A Advisors for $25M-$1B Deals (2026)