14 Best Energy M&A Advisors in the US for $25M-$1B Deals (2026 Guide)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

14 Best Energy M&A Advisors in the US for $25M-$1B Deals (2026 Guide)

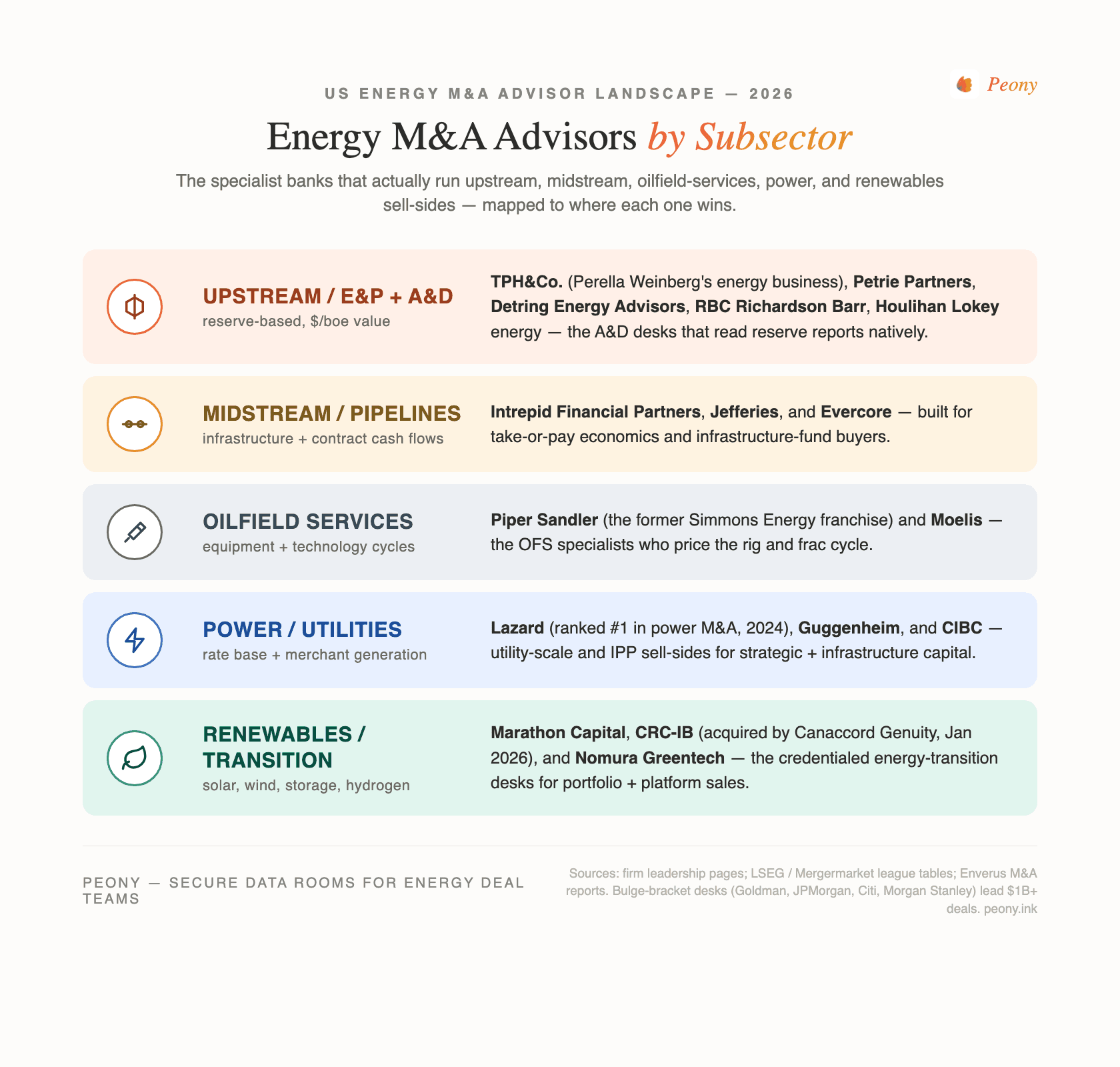

Quick answer: Energy M&A does not have one "best advisor" — it has five subsector benches. For upstream / E&P, the strongest names in the $25M-$1B band are Petrie Partners, Detring Energy Advisors, RBC Richardson Barr, Houlihan Lokey, and TPH&Co. (Tudor, Pickering, Holt — Perella Weinberg's energy business). For midstream, Intrepid Financial Partners, Jefferies, and Evercore. For oilfield services, Piper Sandler (the former Simmons Energy franchise) and Moelis. For power & utilities, Guggenheim, Lazard, and CIBC. For renewables / energy transition, Marathon Capital, CRC-IB (now part of Canaccord Genuity), CIBC, and Nomura Greentech. The bulge brackets — Goldman, JPMorgan, Citi, Morgan Stanley — own the $1B+ value league tables but are usually the wrong call below that. Pick by subsector and asset type, not by logo.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — upstream divestitures, midstream carve-outs, oilfield-services exits, renewables platform sales, and the occasional billion-dollar corporate combination — and energy is the one sector where picking the wrong type of advisor costs you the most. A generalist banker who runs an EBITDA-multiple process on a reserve-heavy upstream package, or who has never valued an interconnection queue on a solar portfolio, leaves real money on the table. At Peony we now serve more than 5,900 customers, and a large share of our energy deals live in exactly the $25M-$1B band this guide covers.

Most "best energy M&A advisor" lists are interchangeable directory pages that rank firms one through ten as if a single league table existed. It does not. Energy M&A splits into at least five distinct benches — upstream / E&P (including the A&D specialists), midstream / pipelines, oilfield services, power and utilities, and renewables / energy transition — and the firm that dominates one is often irrelevant in another. This post is organized the way the market actually works: by subsector, with each firm mapped to its lane, its deal-size band, and a verified credential or deal. The five proprietary frames — the Reserve-Report-to-Banker-Fit Matrix, the A&D-Boutique-vs-Bulge-Bracket Gate, the Commodity-Cycle Timing frame, the Energy-Transition Crossover Test, and the Datacenter-Offtake Premium frame — come from cross-referencing the verified 2024-2026 deal record against the structural realities of each subsector.

Two framing notes before the roster. First, the A&D distinction. Acquisitions-and-divestitures (A&D) specialist boutiques sell asset packages — PDP / PUD reserves, acreage, producing wellbores — through engineering-and-geology-led managed processes, with a $50M-$500M sweet spot. Full-service and corporate-M&A banks sell whole companies — corporate combinations, take-privates, $1B+ mergers. A&D boutiques live on subsurface technical credibility; corporate-M&A banks live on balance-sheet relationships and equity-story packaging. Second, honest framing on the bulge brackets. They are not the answer for most readers of this guide, but they own the value league tables, so I name them at the end to frame the ceiling. And Peony is not an advisor — it is the data-room layer sellers and bankers use to run the process; I will flag where that fits, but the advisory firms are the subject here.

What's the energy M&A advisor landscape by subsector in 2026?

The roster below is organized by subsector. Each firm is profiled in depth in its section; this table is the map.

| Firm | HQ | Deal-size band | Subsector focus | Credential / verified deal |

|---|---|---|---|---|

| Petrie Partners | Denver + Houston | $100M-multi-billion | Upstream corporate M&A | Advised Pioneer on $59.5B sale to ExxonMobil |

| Detring Energy Advisors | Houston | $25M-$500M (A&D) | Pure upstream A&D | 175 transactions / ~$6.5B closed |

| RBC Richardson Barr | Houston | $50M-$500M+ | Upstream / midstream A&D | RBC led O&G M&A by volume + value Q1-Q3 2025 (16 deals / $32.7B) |

| Houlihan Lokey (Energy) | Houston (energy) | $25M-$500M+ | Mid-market A&D + restructuring | Tied #1 by O&G deal volume Q1 2026 |

| TPH&Co. (PWP energy business) | Houston | $250M+ | Full value chain, corporate M&A | Most recognized pure-energy brand; ~130-company research footprint |

| Intrepid Financial Partners | New York | $100M-$2B+ | Midstream infrastructure | Founder-led midstream merchant bank (McGee) |

| Jefferies (Energy) | New York + Houston | Mid-cap-$5B+ | Full energy + financing | Best-ever advisory quarter 2025; #5 O&G volume Q1 2026 |

| Evercore (Energy / P&U) | New York + Houston | $1B+ | Energy + power + LNG | Advised Calpine and Woodside on Louisiana LNG 2025 |

| Piper Sandler (ex-Simmons) | Houston (energy) | $25M-$1B+ | Oilfield services & equipment | The category-defining OFS desk (Simmons legacy) |

| Moelis (Energy & Clean Tech) | New York + Houston | Mid-cap-large-cap | Upstream / midstream + clean tech | Hired Stephen Trauber to chair energy, 2024 |

| Guggenheim Securities | New York | $1B+ | Power & utilities | Recognized leader in utility M&A; $200B+ advised |

| Lazard (Power, Energy & Infra) | New York + Houston | $1B+ | Power, utilities, infra, transition | #1 power M&A advisor 2024 (23 deals / $22.8B) |

| CIBC (Energy, Infra & Transition) | New York + Houston | Mid-cap-large-cap | Power, utilities, renewables | #2 North American renewables advisor since 2017 |

| Marathon Capital | Chicago | Project-platform | Pure-play renewables / transition | IJ Global Financial Adviser of the Year N.A. 2023 |

A few notes the table cannot carry. Petrie, Detring, RBC Richardson Barr, and Houlihan Lokey are the working core for a $25M-$1B upstream seller — the A&D and mid-market specialists most readers of this guide actually need. TPH&Co. is the most recognized pure-energy brand, but its best fit is $250M and above. Piper Sandler carries the former Simmons Energy franchise and is the category-defining oilfield-services desk. And the renewables specialists — Marathon Capital, CRC-IB (now part of Canaccord Genuity), CIBC, and Nomura Greentech — solve a different problem than the O&G shops, because renewables value lives in the interconnection queue and the tax-credit stack. The two energy-transition firms beyond Marathon are profiled in the renewables section below.

Who are the best upstream / E&P (oil & gas) M&A advisors?

For an upstream sale, the right advisor is a function of whether you are selling an asset package or a whole company — and of how much of your value lives in the reserve report. The five firms below cover the $25M-$1B upstream band, from pure A&D boutiques to the corporate-M&A brand names.

Petrie Partners is the dean of US upstream M&A. Founded in 2011 by Jon Hughes, Mike Bock, and Andy Rapp — all alumni of the legendary Petrie Parkman & Co. (which merged into Merrill Lynch in 2006) — and chaired since 2012 by Thomas A. Petrie himself, it is a small founder-led boutique of roughly ten to twelve partners that punches far above its headcount. It is predominantly sell-side and strategic-advisory, mid-cap to large-cap ($100M to multi-billion). Petrie advised Pioneer Natural Resources on its sale to ExxonMobil — the all-stock deal valued at $59.5B equity / ~$64.5B enterprise value that closed in May 2024 — and has advised on a series of 2025 strategic transactions including a Civitas Resources combination. For a whole-company sale or a board that wants gravitas, Petrie is the reference boutique.

Detring Energy Advisors is the specialist's specialist — a pure upstream A&D shop founded in September 2014 by Derek Detring (ex-Merrill Lynch, then Wells Fargo A&D). Detring explicitly works the gap that is too large or technically complex for online auction sites but not large enough to attract the biggest banks, with a track record the firm cites at 175 transactions and roughly $6.5B closed. Its product is reserve-report-grade technical marketing of asset packages, often run in partnership with PetroDivest Advisors. For a private operator selling a defined producing or undeveloped package in the $25M-$500M range, Detring is best-in-class.

RBC Richardson Barr gives you A&D-boutique technical depth inside a global bank. Richardson Barr & Co. was founded in 2003 and acquired by RBC Capital Markets in 2008 (its Calgary sister team is RBC Rundle). It covers upstream, midstream, and energy-transition A&D and corporate M&A, typically on $50M-$500M asset deals but with RBC's balance sheet available for larger corporate mandates. The verified credential is striking: RBC Capital Markets led oil & gas M&A advisory in both volume and value in Q1-Q3 2025 — 16 deals worth $32.7B — up from #3 by volume and #7 by value a year earlier. It pairs engineering-and-geology-led marketing with financing and cross-border reach.

Houlihan Lokey's energy / oil & gas group is the leading middle-market M&A house with a differentiator that matters in a downcycle: a deep restructuring bench. The energy team is anchored in Houston (an A&D team hired in from 2015 and expanded in 2021), and the natural home for the $25M-$1B band is its middle-market coverage. The verified credential: Houlihan Lokey was tied for #1 by oil & gas deal volume in Q1 2026 (four deals, alongside Evercore). When oil prices fall and distressed E&P sales appear, the firm's restructuring capability is a real edge no pure A&D boutique can match.

TPH&Co. — Tudor, Pickering, Holt & Co., the energy business of Perella Weinberg Partners — is the most recognized pure-energy brand on the Street. The energy practice launched in 2007 and combined with Perella Weinberg Partners (PWP) in 2016; TPH now operates as PWP's energy arm, with research covering roughly 130 energy companies and 100-plus banking professionals across seven offices. It runs both buy- and sell-side corporate M&A plus capital markets across the full value chain, and its best fit is $250M and above, routinely on multi-billion-dollar deals. A clarification worth making because it is widely misstated: TPH&Co. is not an independent boutique — it is PWP's energy business, which means it brings PWP's independent-advisory balance sheet behind the energy brand.

Reserve-Report-to-Banker-Fit Matrix. The right upstream advisor is a function of how much of your value lives in the subsurface engineering versus the corporate equity story. Map what you are selling to the banker type — and hire the banker who can read your reserve report (or your interconnection queue), not just your income statement.

| What you're selling | Value driver | Best advisor type | Examples |

|---|---|---|---|

| PDP-heavy producing package | Current cash flow / decline curves | A&D boutique (engineering-led) | Detring, RBC Richardson Barr, PetroDivest |

| PUD / acreage-heavy, undeveloped inventory | Drilling inventory & well economics | A&D boutique with reservoir bench | Detring, RBC Richardson Barr |

| Whole private E&P company | Equity story + balance sheet + inventory | Corporate-M&A boutique / bank | Petrie, Jefferies, TPH&Co. |

| $1B+ public-company merger | Strategic fit, synergies, stock | Bulge bracket / top independent | Goldman, Evercore, JPMorgan, TPH&Co. |

| Gas package near a datacenter corridor | Offtake / PPA optionality (not just strip) | Midstream / power-literate bank | Intrepid, Lazard, Morgan Stanley |

| Renewables developer / portfolio | Interconnection queue + tax credits | Renewables specialist | Marathon Capital, CRC-IB, CIBC, Nomura Greentech |

Who advises on midstream and pipeline M&A?

Midstream is a contracted-cash-flow and infrastructure game, so the right advisor values long-term firm-transportation and minimum-volume commitments, rights-of-way, and — increasingly — datacenter and power offtake, not just commodity strip. Three firms lead for a $25M-$1B midstream seller.

Intrepid Financial Partners is the standout midstream boutique. Founded in 2015 by Hugh E. "Skip" McGee III (the former head of investment banking at Barclays and Lehman) and Christopher F. Winchenbaugh, Intrepid is an independent merchant bank that both advises and invests, with midstream infrastructure as its genuine center of gravity (plus upstream and energy transition), in a $100M-$2B+ growth-and-yield band. Very few boutiques truly lead with midstream; Intrepid is one of them. As a notable prior mandate, Intrepid represented itself in Shell USA's $1.96B acquisition of Shell Midstream Partners, announced July 25, 2022 — older than this guide's usual recency window, so I flag the date, but it illustrates the firm's midstream pedigree.

Jefferies brings bulge-bracket-scale energy coverage inside an independent investment bank, with a large Houston energy presence spanning upstream, midstream, oilfield services, and energy transition — and, crucially, the leveraged-finance muscle to pair M&A with debt financing for sponsors. The context credential: Jefferies posted one of its strongest advisory quarters on record in 2025 and ranked #5 by oil & gas deal volume in Q1 2026. For a midstream seller whose buyer pool includes sponsors needing acquisition financing, Jefferies's ability to staple M&A advice to debt is a structural advantage.

Evercore is a top-tier independent advisor that sits at the upper end of the band — large-cap, routinely $1B+, across upstream, midstream, power, LNG infrastructure, and energy transition. Its verified 2025 mandates show the franchise's reach: Evercore advised Calpine on its sale to Constellation Energy (~$16.4B equity / ~$26.6B net purchase price; closed January 7, 2026) and advised Woodside Energy on its $5.7B sale of a 40% interest in Louisiana LNG Infrastructure to Stonepeak (April 2025). Evercore was also tied for #1 by oil & gas deal volume in Q1 2026 (four deals) and #2 by value ($64.4B). For a midstream or infrastructure asset approaching the top of the $25M-$1B band, Evercore is a credible independent.

Who are the top oilfield services (OFS) M&A advisors?

Oilfield services is its own world — cyclical, with customer-concentration and technology / IP value that a generalist misreads — and it has a category-defining desk.

Piper Sandler carries the former Simmons Energy franchise, the single most storied oilfield-services advisory practice in the world. Simmons & Company, founded in 1974, became "Simmons Energy | A Division of Piper Sandler" and was then folded fully into Piper Sandler in July 2021 — so the current, correct name is simply Piper Sandler (the former Simmons Energy franchise), not "Simmons & Company" or "Simmons Energy" as a standalone. The energy team is headquartered in Houston, with Aberdeen and London for international OFS, covering energy services and equipment plus upstream, midstream, and downstream, across a middle-market-through-large-cap band ($25M-$1B+). For an oilfield-services or equipment seller, this is the category-defining desk, and Piper Sandler has been expanding its E&P coverage with recent hires.

Moelis & Company built a top-tier energy franchise aggressively through 2024 senior hires. The headline move: Moelis hired Stephen Trauber as Chairman and Global Head of Energy & Clean Technology — a banker with 35-plus years who has advised on more than $700B of energy deals over his career — alongside managing directors Muhammad Laghari (formerly head of North American upstream IB at Guggenheim) and Alexander Burpee. Moelis covers upstream and midstream oil & gas plus clean technology and energy transition on an independent-advisory model, mid-cap through large-cap. The franchise is now a credible choice for an OFS or upstream seller who wants a Trauber-led independent process; I am leading with the franchise build-out rather than a specific named mandate, because the strongest recent signal here is the team Moelis assembled.

Who are the best power and utilities M&A advisors?

Power and utilities M&A is a regulated, large-cap business — rate base, state PUC and FERC approvals, and large-cap process management are the table stakes — and three firms lead.

Guggenheim Securities is a recognized league-table leader in utility M&A. The firm states it has advised on $200B+ of energy M&A and positions itself as a Wall Street leader in utility M&A, and it continues to hire senior power and renewables advisors. For a regulated-utility combination at the $1B+ end, Guggenheim is a default name; I am leading with that verified credential rather than naming an unconfirmed recent mandate.

Lazard combined its Power, Energy & Infrastructure practice with its Oil & Gas Advisory team into roughly 60 US bankers co-located in Houston and New York, and it also publishes the influential annual Levelized Cost of Energy+ (LCOE+) report. The verified credential is strong: Lazard ranked #1 as an M&A financial adviser in the power sector in 2024 (23 deals / $22.8B), up from #9 by volume the year before. Verified 2025 mandates include advising on Oncor Electric Delivery corporate M&A ($9.45B, March 2025) and advising Invenergy on a $3B strategic growth capital raise (January 2025). Lazard's annual M&A review is also citable thought leadership for market context.

CIBC's Energy, Infrastructure & Transition (EIT) group is the bank that genuinely bridges conventional power and renewables — useful for the energy-transition crossover buyer. Its US energy team sits in New York and Houston (with Calgary, London, and Bogotá), covering conventional power, regulated utilities, renewables, midstream, upstream, and infrastructure. The verified credential: CIBC has been the #2 North American renewables M&A advisor since 2017 by both gross deal value and number of transactions closed, and was named North American Financial Advisor of the Year in 2023. For a power seller whose asset mix straddles conventional generation and renewables, CIBC is purpose-built.

Who are the best renewables and energy-transition M&A advisors?

Renewables is the subsector where specialist credentials matter most, because value lives in the two scarcest currencies of 2025-26 — interconnection-queue position and transferable tax credits — not in conventional EBITDA. Four firms lead, three of which are profiled here (CIBC, the conventional-power bridge, is covered in the power section above).

Marathon Capital is one of the longest-running independent renewables-only advisors. Founded in 1999 by Ted Brandt and Gregg Elesh and headquartered in Chicago (with New York, San Francisco, Houston, and London offices), it is a pure-play clean-energy and energy-transition shop — renewable power (solar, wind), storage, sustainable infrastructure, low-carbon molecules — offering M&A, debt and equity capital markets, tax-credit advisory, and offtake advisory, sell-side-heavy on developer and portfolio sales. It has been named M&A Advisor of the Year multiple times by Power, Finance & Risk and IJ Global's Financial Adviser of the Year — North America (2023). Verified recent deals: Marathon advised Pacifico Energy on the sale of a co-located solar-plus-storage portfolio (27 MWdc solar / 25 MWh BESS) to CleanCapital (announced June 2025), and advised Redeux Energy on the sale of a 450 MW solar portfolio to Pine Gate Renewables and on a 200 MWdc solar-plus-storage development sale to Scout Clean Energy. For a renewables developer selling a project or portfolio, Marathon is a reference name.

CRC-IB (now part of Canaccord Genuity) is the highest-deal-count renewables shop. The brand chain matters and is worth getting right: founded in 2008 as CohnReznick Capital, rebranded CRC-IB in November 2023, taken partner-owned via a buyout from CohnReznick in November 2024, and acquired by Canaccord Genuity Group on January 14, 2026 — it now operates as the "Energy Transformation group" inside Canaccord's US Sustainability platform. It covers renewable energy and energy transition — wind, solar, storage, carbon capture — across M&A, project finance, capital raising, and tax-credit transfer, from project-level through corporate. CRC-IB positions itself as the #1 renewable-energy investment bank by transaction count, with roughly 415 transactions and ~$91B cumulative cited in the January 2026 Canaccord acquisition announcement, and about 75% repeat clients. For a renewables seller who wants the deepest deal-count bench, this is it.

Nomura Greentech is an energy-transition specialist with the balance sheet and global footprint of a major bank. It originated as Greentech Capital Advisors and was acquired by Nomura and rebranded Nomura Greentech in 2020 (the brand is current — there has been no recent rename). Headquartered in New York and San Francisco with global offices including Houston, London, Paris, Frankfurt, Zurich, Tokyo, Hong Kong, and Singapore, it covers sustainable technology and infrastructure / energy transition, fully integrated within Nomura's global investment bank, mid-cap to large-cap and cross-border. For a climate-tech or energy-transition mandate that needs a major bank's reach across borders, Nomura Greentech is the strongest fit; I am leading with that positioning rather than a specific named mandate.

Energy-Transition Crossover Test. A traditional oil & gas seller should add — or switch to — a renewables-credentialed advisor when a meaningful slice of value is in molecules or assets the buyer wants for power or carbon, not for refining. You've crossed over if any of these is true:

- You're selling gas assets whose premium buyer is a datacenter / hyperscaler or a power developer — value is offtake, not commodity. Pick a midstream / power-literate bank (Intrepid, Lazard, Morgan Stanley, CIBC).

- Your base includes CCS, geothermal, lithium-from-brine, or RNG optionality a pure O&G A&D shop will under-credit. Pick a crossover bank (Nomura Greentech, CRC-IB, Marathon Capital).

- You want the widest buyer universe in a thin oil-weighted market — transition banks bring IPPs, infrastructure funds, and strategics O&G-only firms don't cover.

If a meaningful slice of your value is in molecules the buyer wants for power or carbon — not for refining — you've crossed over, and your banker shortlist should too.

When does a $1B+ deal call for a bulge-bracket energy desk?

For most readers of this guide, the bulge brackets are not the answer — their minimums and attention favor $1B+ — but they own the value league tables because they advise the mega-mergers, and a seller should understand the ceiling.

The Q1 2026 oil & gas league tables tell the story: Goldman Sachs ranked #1 by deal value (~$64.7B), driven largely by advising on the Devon-Coterra merger (≈$58B combined enterprise value; Enverus counts ≈$25.4B of it as Q1 2026 upstream transaction value), jumping from #9 a year earlier; JPMorgan was #3 by value (~$58.5B) and sits atop the broad FY2025 league tables alongside Goldman; Barclays was #4 by oil & gas value (~$7.9B). Power is its own table: Citi leapt to #1 in power M&A by value in Q1 2026 (from #21 a year earlier — all four of its Q1 2026 deals were billion-dollar-plus, including one $10B+ mega-deal), and Morgan Stanley led power M&A by volume in both Q1 2025 and Q1 2026, notably combining its upstream-oil and power teams to chase integrated LNG-to-power and grid-storage mandates.

A&D-Boutique-vs-Bulge-Bracket Gate. A clean decision gate by deal size and asset type. The paradox: bulge brackets dominate the value tables but are the wrong call for most $25M-$1B sellers.

| Deal size (EV) | Default choice | Why | Watch-out |

|---|---|---|---|

| $25M-$150M asset package | A&D boutique (Detring, RBC Richardson Barr, PetroDivest) | Below bulge-bracket attention / minimums; technical marketing wins; Double-Lehman economics | A bulge bracket will under-resource you or decline |

| $150M-$500M | A&D boutique OR mid-market bank (Houlihan Lokey, Piper Sandler, Jefferies) | Enough size for a real bank; still wants technical depth | Confirm the senior banker, not a junior, runs it |

| $500M-$1B | Top independent (Jefferies, Evercore, TPH&Co., Petrie) | Corporate process, financing access, buyer breadth | Fees compress; negotiate the % and tail |

| $1B+ | Bulge bracket / top independent (Goldman, Evercore, JPMorgan; Citi for power) | Mega-buyer relationships, stock-deal mechanics | Not the audience for this guide |

The bank at the top of the league table by value is usually the wrong bank for a $25-150M asset sale — that deal needs a reserve engineer with a Rolodex, not a logo.

Is now a good time to sell energy assets? The commodity-cycle frame

Energy M&A is uniquely cycle-gated, and the advisor choice should flex with where the cycle sits — auction tension is a function of the strip, so timing the banker to the cycle matters almost as much as timing the sale.

The Enverus quarterly series quantifies it. US upstream M&A ran about $17B in Q1 2025 (the second-best start since 2018, with Diamondback driving roughly half the value), then fell to ~$13.5B in Q2 2025 — making the first half of 2025 about $30.5B, down roughly 60% versus the first half of 2024 — and slid again to $9.7B in Q3 2025 on weak crude. Then it rebounded: $23.5B in Q4 2025 (gas-weighted, led by Haynesville and Gulf Coast gas, with the Permian only a minor portion) for a full-year 2025 total of about $65B, and $38B in Q1 2026, where the ~$25.4B Devon-Coterra merger alone drove about two-thirds of the value and only eight deals topped $100M (a post-2020 low). Over the past six months through Q1 2026, more than $60B of upstream M&A changed hands. Enverus's Andrew Dittmar framed it in May 2026: "the case for higher-for-longer oil prices is strengthening and creating the setup for an M&A rebound."

Commodity-Cycle Timing frame. Match the advisor to the cycle:

- Trough / weak prices (buyers "in the dugout"): fewer bidders, longer processes — favor an A&D boutique that runs a targeted (not broad-auction) process with direct lines to the handful of active acquirers (refunded PE, international entrants). Distressed? Add a restructuring-capable bank (Houlihan Lokey).

- Recovery / firming prices: competitive tension returns — a broader process and a brand-name bank can extract a premium; private operators should move before the "final divestiture window" closes on scarce premium inventory.

- Gas-vs-oil divergence (current): gas-weighted (Haynesville / Gulf Coast / Appalachia)? You're in the hot part of the cycle (LNG + datacenters) — pick a gas / LNG / power-literate advisor. Oil-weighted Permian non-core? You're in the broadening tail — pick a technical A&D shop that finds regional and private buyers.

The 2026 story underneath the numbers: high consolidation over the last few years has left few attractive private companies for the public E&Ps to target, so market gravity is broadening to gas-weighted plays and non-core regional opportunities. Remaining premium Permian inventory is scarce, which means some private operators may view their current holdings as a final opportunity for meaningful divestiture proceeds — and the leftover deals are smaller, more technical, non-core packages. That is precisely why the A&D boutiques matter now.

Why does the datacenter-offtake premium change which banker you hire?

In 2026, the most valuable thing about some gas assets isn't the gas — it's the zip code's proximity to a datacenter corridor. A gas asset's value is increasingly bifurcated between commodity-strip value and offtake-optionality value: the premium a hyperscaler or power developer pays for firm, behind-the-meter supply near a datacenter corridor in Northern Virginia, Texas, or Ohio.

The demand backdrop is real. Data-centre electricity demand rose roughly 17% in 2025 and is set to double by 2030, with AI-specific demand tripling (IEA). US data-center grid-power demand rose about 22% in 2025 and is tracking toward roughly 75.8 GW by 2026, 108 GW by 2028, and 134.4 GW by 2030 (S&P Global and industry estimates). Natural gas is the swing supply: planned gas capacity rose from about 11.1% of additions in 2024 to roughly 18.1% in 2026, and powering AI may require an extra 10-15% of US gas production by the early 2030s. The new commercial model is midstream-to-hyperscaler direct deals and on-site behind-the-meter gas generation that bypasses multi-year utility interconnection queues.

The canonical template is Williams Companies' "Socrates" project — roughly $1.6B for about 500 MW of behind-the-meter gas generation in New Albany, Ohio, anchored by a 10-year fixed-price PPA with Meta (440 MW), with Williams committing $5.1B+ to a broader power-innovation model.

Datacenter-Offtake Premium frame. If your acreage or gas can underpin a datacenter PPA:

- Pick an advisor who can quantify and market the offtake optionality, not just run a PDP economics model — midstream / power-literate (Intrepid, Lazard, Morgan Stanley; Williams-type strategics as buyers).

- Expect a different buyer universe — utilities, IPPs, infrastructure funds, hyperscalers — than a vanilla E&P A&D process.

Hire a banker who prices the PPA, not just the strip.

What does an energy M&A advisor charge in 2026?

Energy M&A advisors price like the broader lower-middle-market — a retainer or work fee plus a success fee at close — with the success rate declining as deal size grows, but with energy-specific nuances on top.

The baseline curve, from the Firmex / Axial M&A Fee Guide 2024-25 (the 8th annual edition, surveying 456 middle-market professionals): an effective success fee of roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M. Lehman-style declining-rate formulas are not obsolete — a declining Lehman structure is the single most common arrangement at about 44% of engagements (versus ~26% flat-rate and ~20% accelerators). In the lower middle market you will most often be quoted the Double Lehman (10-8-6-4-2): on a $20M deal that computes to $600,000 (3.0%). Retainers run $5,000-$10,000/month (or a fixed $25K-$75K), about 72% are credited against the success fee if the letter says so in writing (2021-22 Fee Guide survey), and minimum-fee floors of $50K-$250K appear in about two-thirds of letters — on a small deal the floor, not the percentage, sets the bill.

| Deal size (EV) | Typical structure | Blended success fee | Energy-specific note |

|---|---|---|---|

| $25M-$50M asset package | Double Lehman (10-8-6-4-2) | ~2.5%-3.5% | Retainer often partly funds the technical marketing package |

| $50M-$150M | Double Lehman or negotiated flat | ~2.0%-2.5% | A&D fees skew to the percentage end; confirm senior staffing |

| $150M-$500M | Lehman with flat tier above threshold | ~1.5%-2.0% | Top of A&D, bottom of corporate; fees compress |

| $500M-$1B | Negotiated flat / stepped | ~1.0%-1.5% | Corporate-M&A territory; negotiate % and tail hard |

Four energy-specific fee realities. First, A&D asset deals price off the reserve report, not EBITDA — the banker is marketing a reserve / acreage package, a fundamentally technical sell, so retainers and work fees are common and often partly fund building the engineering, mapping, and data-room package (analogous to the generic "the data room is a reimbursed expense line" point, but heavier because the technical package is the product). Second, A&D success fees skew toward the percentage end because the deals are smaller and the marketing process is labor-intensive. Third, corporate energy M&A at $1B+ compresses to well under 1% — bulge brackets on a $20-60B merger earn fractions of a percent on enormous bases — which means the $25M-$1B reader sits in the 2.0%→~1% transition zone at the top and the 3-5%+ Double-Lehman zone at the bottom. Fourth, the tail bites harder in A&D: a named strategic that passed can resurface 12-18 months later when commodity prices move, so negotiate the named-buyer-list defense (the banker must deliver the contacted-buyer list within ~10 days of termination or the tail is void). The full mechanics — including how a broad "transaction value" definition can put the fee base above the cash you actually pocket — are in our M&A advisor fees hub.

Honest comparison: which energy advisor fits which lane?

No single firm wins every energy mandate. This matrix maps subsector and deal size to the firms that genuinely fit — and concedes where a bulge bracket or a relationship-driven generalist is the better call than a boutique.

| Subsector | $25M-$150M | $150M-$500M | $500M-$1B | $1B+ |

|---|---|---|---|---|

| Upstream / E&P (asset / A&D) | Detring + RBC Richardson Barr | RBC Richardson Barr + Houlihan Lokey | Jefferies + Petrie + TPH&Co. | Goldman + Evercore + JPMorgan |

| Upstream / E&P (whole company) | Houlihan Lokey + Petrie | Petrie + Jefferies | Petrie + TPH&Co. + Evercore | TPH&Co. + Goldman + JPMorgan |

| Midstream / pipelines | Intrepid | Intrepid + Jefferies | Jefferies + Evercore + Intrepid | Evercore + Morgan Stanley + bulge |

| Oilfield services | Piper Sandler | Piper Sandler + Moelis | Piper Sandler + Moelis + Evercore | Evercore + bulge |

| Power / utilities | (boutique scarce — regional) | CIBC + Lazard | Lazard + Guggenheim + Evercore | Citi + Morgan Stanley + Guggenheim |

| Renewables / energy transition | Marathon + CRC-IB | Marathon + CRC-IB + CIBC | CIBC + Nomura Greentech + Evercore | Nomura Greentech + bulge |

The honest limits to flag:

- Above $1B EV — bulge-bracket and top-independent capabilities (mega-buyer relationships, stock-deal mechanics) matter, and this guide's $25M-$1B band is no longer the right frame. Goldman, JPMorgan, Citi (power), Morgan Stanley, and the top independents lead there.

- A single dominant strategic buyer with a deep existing relationship — if your CEO or board already has the relationship that will set the price, a trusted generalist with that strategic relationship, or even a direct negotiation with a fairness opinion, can beat a specialist's broad process. Competition moves price; the specialist's value is creating it where it does not already exist.

- Power and utilities below ~$150M — there is no deep pure-play power boutique bench at the small end; a regional advisor or a generalist with utility experience often fits better than forcing a large-cap power desk.

- Pure financial restructuring in a downcycle — if the situation is distressed, weight toward a restructuring-capable house (Houlihan Lokey) over a pure A&D shop.

For the energy deals that do fit this guide — the $25M-$1B upstream, midstream, oilfield-services, power, and renewables sellers who make up the bulk of the market — a subsector specialist with a documented buyer-relationship map and the right technical literacy is hard to beat, and a clean, staged data room prepared before launch is the cheapest lever you control on both timeline and price.

Bottom line

Energy M&A does not have one league table — it has five, and the firm that dominates one subsector is often irrelevant in another. For a $25M-$1B seller, the working core is the upstream A&D and mid-market bench — Petrie Partners, Detring Energy Advisors, RBC Richardson Barr, Houlihan Lokey, and TPH&Co. — plus the subsector specialists: Intrepid, Jefferies, and Evercore for midstream; Piper Sandler (the former Simmons Energy franchise) and Moelis for oilfield services; Guggenheim, Lazard, and CIBC for power and utilities; and Marathon Capital, CRC-IB (now part of Canaccord Genuity), CIBC, and Nomura Greentech for renewables and energy transition. The bulge brackets — Goldman, JPMorgan, Citi, Morgan Stanley — own the $1B+ value tables but are usually the wrong call below that.

The single most important advisor-selection question for an energy seller: which firm can read the part of my value that is technical — the reserve report, the contract stack, the interconnection queue — and name the five buyers, strategic and financial, it will call first for my specific asset in my specific basin or sub-vertical? In a sector this cycle-gated and this technical, that combination of subsurface (or queue) literacy and a current buyer Rolodex is the whole edge. We serve 5,900+ customers on the data-room side of exactly these deals — and the prep you do before you pick an advisor (a current reserve report, clean title, a staged and watermarked data room, a tight buyer thesis) compounds everything the advisor does next.

Related resources

- M&A advisor vs broker vs investment bank — the decision that comes before this energy shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- 16 Best Healthcare M&A Advisors by Subsector — the sibling national sector cut: healthcare M&A advisors mapped by subsector, with the 2026 Regulatory-Overhang Discount and the CMS-moratorium scarcity frame

- 13 Best Technology & Software M&A Advisors — the sibling national sector cut: SaaS, infrastructure & data/AI, cybersecurity, fintech, and IT-services M&A advisors mapped by subsector, with the Rule-of-40 Banker-Fit Matrix

- Best data rooms for oil and gas companies — the energy-specific data-room buildout behind a sale, scored

- Upstream oil & gas divestiture data room: 12-month timeline — the process and timeline for an upstream asset sale, step by step

- Best M&A Advisors in Houston — the geo cut of this national hub: where most energy A&D boutiques are headquartered

- Best M&A Advisors in Dallas — the North Texas geo cut for energy and diversified sellers

- Best M&A Advisors in Denver — the Rockies / DJ-Basin geo cut, anchored by Petrie Partners and the Front Range energy bench

- M&A Data Room: setup and workstream mapping — the general sell-side data-room playbook

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, where the room and its cost have to fit a smaller deal

- State of M&A Data Rooms: 2026 benchmark — the Peony platform deal benchmark

Frequently asked questions

Who are the best energy M&A advisors for selling an oil & gas company in 2026?

The best energy M&A advisor depends on your subsector and deal size, not a single ranking. For an upstream / E&P sale in the $25M-$1B band, the strongest options are the pure-play A&D boutiques and corporate-M&A specialists: Petrie Partners (Denver / Houston, the dean of US upstream M&A, advised Pioneer on its $59.5B sale to ExxonMobil), Detring Energy Advisors (Houston, a pure acquisitions-and-divestitures shop with 175 transactions / ~$6.5B closed), RBC Richardson Barr (A&D technical depth inside a global bank — RBC Capital Markets led oil & gas M&A in both volume and value in Q1-Q3 2025 with 16 deals / $32.7B), Houlihan Lokey's energy group (the leading middle-market house, tied for #1 by oil & gas deal volume in Q1 2026, with a restructuring bench that matters in a downcycle), and TPH&Co. — Tudor, Pickering, Holt, the energy business of Perella Weinberg Partners (the most recognized pure-energy brand on the Street, best fit at $250M and above). For midstream, look at Intrepid Financial Partners, Jefferies, and Evercore; for oilfield services, Piper Sandler (the former Simmons Energy franchise) and Moelis; for power and utilities, Guggenheim, Lazard, and Citi; for renewables and energy transition, Marathon Capital, CRC-IB (now part of Canaccord Genuity), CIBC, and Nomura Greentech. The honest filter: ask each firm to name the five buyers they would call first for your specific asset, and how many deals they have closed in your basin or sub-vertical in the last 18 months. We run Peony, a data room company that has served 5,900+ customers, and across hundreds of energy and divestiture processes the firms that genuinely engage are the ones that can answer that question without hesitating. The intermediary-tier decision is covered upstream in our M&A advisor vs broker vs investment bank guide.

Which advisors specialize in midstream, oilfield services, power, or renewables M&A?

Each energy subsector has its own specialist bench. For midstream / pipelines, the standout boutique is Intrepid Financial Partners (founded 2015 by former Barclays IB head Skip McGee — one of the few boutiques that genuinely leads with midstream infrastructure), alongside Jefferies, Evercore, and CIBC; these firms can value long-term contracted cash flows, firm-transportation commitments, and rights-of-way. For oilfield services and equipment, Piper Sandler carries the former Simmons Energy franchise (Simmons & Company, founded 1974, was rebranded fully into Piper Sandler in July 2021) — the single most storied OFS advisory practice in the world — with Moelis and Evercore also credible after Moelis's 2024 hire of Stephen Trauber to chair its energy practice. For power and utilities, Guggenheim Securities is a recognized leader in utility M&A ($200B+ advised), Lazard ranked #1 in power-sector M&A in 2024 (23 deals / $22.8B), and CIBC is a strong conventional-power-plus-renewables bridge. For renewables / energy transition, the specialists are Marathon Capital (one of the longest-running renewables-only advisors), CRC-IB (now part of Canaccord Genuity after its January 2026 acquisition — positioned as the #1 renewable-energy bank by transaction count, ~415 deals / ~$91B), CIBC (#2 North American renewables advisor since 2017), and Nomura Greentech. The bulge brackets — Goldman, JPMorgan, Citi, Morgan Stanley — span all of these but are built for $1B+ mandates. The subsector roster below maps each firm to its lane, and our city guides cover the geo cut: Houston, Dallas, and Denver.

Do I need an energy-specialist banker, or can a generalist M&A advisor sell my company?

For most energy sellers, a sector specialist beats a generalist — but the reason is specific, not snobbery. Energy value is technical in ways a generalist process does not capture: an upstream asset is priced off a reserve report (PDP, PUD, probable / possible reserves run through engineering), a midstream asset off contracted cash flows and rights-of-way, a renewables platform off its interconnection-queue position and transferable tax credits. A generalist banker who runs an EBITDA-multiple process will under-credit the parts of your value that live in the subsurface, the contract stack, or the queue — and, just as costly, will not have direct lines to the handful of active acquirers in your subsector (right now in upstream that is refunded private-equity teams, a few public consolidators, and new international entrants like Mitsubishi). The exception worth naming honestly: if your most likely buyer is a single strategic with whom your CEO or board already has a deep relationship, a trusted generalist or even a direct negotiation can sometimes beat a specialist's broad process — competition, not the banker's logo, is what moves price. But in a thin, cycle-gated market, the specialist's buyer Rolodex and technical credibility are usually worth more than the fee. The deeper distinction between an A&D boutique, a full-service investment bank, and a business broker is in our M&A advisor vs broker vs investment bank hub.

Does my M&A banker really need to understand reserve reports and PDP/PUD?

For an upstream oil & gas sale, yes — reserve-report literacy is the single most important technical qualification, because your asset value is set by the reserve report, not by an income statement. A&D (acquisitions and divestitures) boutiques live and die on subsurface credibility: they market a reserve / acreage package by valuing PDP (proved developed producing) reserves off decline curves and current cash flow, PUD (proved undeveloped) and probable / possible reserves off drilling inventory and well economics, usually run through a third-party reserve engineer on an SPE-PRMS or SEC reserve case. A banker who cannot read your reserve report cannot defend your $/boe or $/flowing-barrel against a sophisticated strategic or PE buyer, and will lose value in negotiation. This is the core of our Reserve-Report-to-Banker-Fit Matrix: a PDP-heavy producing package and a PUD / acreage-heavy undeveloped package both want an engineering-led A&D boutique (Detring, RBC Richardson Barr), while a whole-company sale wants a corporate-M&A specialist (Petrie, TPH&Co.) and a renewables platform wants a banker who reads interconnection queues and tax-credit transfers instead. The branded line I use: hire the banker who can read your reserve report — or your interconnection queue — not just your income statement. The screening question for any upstream advisor: ask them to walk through how they would value your PUD inventory, and whether they will commission an independent reserve report before launch.

A&D boutique vs full-service investment bank vs bulge bracket — which do I need for an energy sale?

It maps almost entirely to deal size and asset type. For a $25M-$150M asset package (a defined producing or undeveloped reserve / acreage package), the default is a pure A&D boutique — Detring, RBC Richardson Barr, or a PetroDivest-style shop — because that deal is below the attention and minimums of a bulge bracket, the win comes from technical marketing of the reserves, and the economics run on Double Lehman. For $150M-$500M you have a choice between an A&D boutique and a mid-market bank (Houlihan Lokey, Piper Sandler, Jefferies) — enough size for a real bank, but you should confirm a senior banker (not a junior) runs it. For $500M-$1B, a top independent (Jefferies, Evercore, TPH&Co., Petrie) brings a corporate process, financing access, and broader buyer reach — and fees compress, so negotiate the percentage and the tail. Only at $1B+ does a bulge bracket (Goldman, Evercore, JPMorgan, or Citi for power) become the default, for mega-buyer relationships and stock-deal mechanics. The league-table paradox to understand: bulge brackets dominate the value tables because they advise the $20-60B mega-mergers, but that is exactly why they are usually the wrong call for a $25-150M asset sale — that deal needs a reserve engineer with a Rolodex, not a logo. Our advisor-vs-bank selection hub walks the full intermediary decision.

Is my $50M energy company too small for an energy investment bank?

No — a $50M energy company is squarely in the sweet spot for the A&D boutiques and the mid-market energy banks, and is at the lower end of what a top independent will take. A $50M upstream package is exactly the gap Detring describes as too large or technically complex for auction sites but not large enough to attract the biggest banks — the home turf of a specialist A&D shop. Houlihan Lokey's energy group, Piper Sandler, and Jefferies will all run a $50M energy deal with senior bankers on buyer calls, and an oilfield-services seller at $50M is a natural Piper Sandler (ex-Simmons) mandate. Where you are genuinely too small for a full-service energy bank is below roughly $25M of value, where a bank's minimum-fee floor ($50K-$250K) consumes an outsized share of proceeds — at that size a pure A&D boutique or a regional advisor that runs a targeted process is the better economic fit. The honest filter for a $50M energy seller: a focused A&D boutique with a real buyer relationship map will almost always beat a bulge bracket that treats your deal as its smallest mandate of the quarter, and a generalist with no subsurface credibility. Ask each pitching bank, in writing, which senior banker will be on every buyer call.

What do energy M&A advisors charge — and are Lehman / Double Lehman fees still standard in 2026?

Both are still standard. Energy M&A advisors price like the broader lower-middle-market — a monthly retainer or work fee plus a success fee at close — with the success rate declining as deal size grows: roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex / Axial M&A Fee Guide 2024-25, the 8th annual edition, N=456). Lehman-style declining-rate formulas are not obsolete — a declining Lehman structure is the single most common arrangement at about 44% of engagements (versus ~26% flat-rate and ~20% accelerators). In the lower middle market you will most often be quoted the Double Lehman (10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% of everything above $5M): on a $20M deal that computes to $600,000, or 3.0%. Energy A&D fees skew toward the percentage end with retainers common, because the technical marketing package (well files, logs, decline curves, title, seismic) is labor-intensive and the retainer often partly funds building it. Retainers run $5,000-$10,000/month (or a fixed $25K-$75K) and about 72% are credited against the success fee if the letter says so in writing (2021-22 Fee Guide survey); minimum-fee floors ($50K-$250K) appear in about two-thirds of letters. One energy-specific clause to negotiate hard: the tail bites harder in A&D, because a named strategic that passed can resurface 12-18 months later when commodity prices move — limit the tail to a named-buyer list the banker must deliver within ~10 days of termination. Full mechanics and the Boutin Jones $780K-fee-on-$2.5M-net cautionary tale are in our M&A advisor fees hub.

How much does it cost to sell a $100M-$250M energy company?

For a $100M-$250M energy company you are in the fee-compression zone — expect a blended success fee around 1.5%-2.0% at the bottom of the range, falling toward ~1%-1.5% as you approach $250M, plus a retainer of roughly $75K-$150K and capped expenses. On a $100M deal a Double Lehman computes to about $1.9M (1.9%); on a $250M deal a straight Double Lehman would overpay the advisor, so banks negotiate a flat or stepped structure with a ~1.25%-1.5% blended target. The base matters more than the rate: confirm whether transaction value is defined on equity, on enterprise value (including assumed debt), and how earnouts and contingent payments are counted — a broad definition can add hundreds of thousands of dollars on the same headline price. At this size you are paying a top independent or a mid-market energy bank (Evercore, Jefferies, TPH&Co., Houlihan Lokey, Piper Sandler), and the senior-banker question becomes critical because a $100-250M deal can be staffed thin inside a large bank. The fee delta between two credible advisors is almost always dwarfed by the price delta a competitive, well-run process produces — so negotiate the percentage and the tail, but choose on buyer reach and subsurface or sector credibility. The worked Lehman / Double Lehman math is in our fee hub.

How do I find a banker who reaches both strategic majors and PE / infrastructure buyers?

Test it directly: ask each pitching banker to produce a buyer list that mixes named strategics with named financial buyers specific to your subsector, and to show recent closings into both groups. The best energy advisors run a dual-track process that puts your asset in front of strategic acquirers (the public consolidators and majors — ExxonMobil, Chevron, Diamondback, Devon, ConocoPhillips in upstream; utilities and IPPs in power; hyperscalers and developers for datacenter-adjacent gas) and financial buyers (energy private equity such as EnCap, Riverstone, Quantum, NGP, ArcLight, EIG, plus infrastructure funds and, increasingly, international entrants like Mitsubishi). A firm that only knows one side leaves competition — and price — on the table. In a thin oil-weighted market, transition-credentialed banks (Marathon Capital, CRC-IB / Canaccord, CIBC, Nomura Greentech) add a buyer universe that pure O&G shops do not cover: IPPs, infrastructure funds, and strategics chasing molecules for power or carbon. The verification question: how many of your last ten closed deals went to a strategic versus a financial buyer, and can you name the corporate-development team and the fund partner you would call first for my asset? A genuinely connected energy banker answers without hesitation. On the document side, Peony's visitor groups let your advisor run strategics and sponsors as separate permissioned tiers in one data room, so the senior banker can see at a glance which of each is genuinely engaged — useful across the 5,900+ customers we have supported on exactly these processes.

I'm an oil & gas seller pivoting to renewables — do I need an energy-transition-credentialed banker?

Often yes — and there is a clean test for it, what I call the Energy-Transition Crossover Test. You have crossed over (and should add or switch to a transition-credentialed advisor) when a meaningful slice of your value is in molecules or assets the buyer wants for power or carbon rather than for refining. Three trigger conditions: (1) you are selling gas assets whose premium buyer is a datacenter / hyperscaler or a power developer, where the value is offtake optionality, not commodity strip — pick a midstream / power-literate bank (Intrepid, Lazard, Morgan Stanley, CIBC); (2) your asset base includes CCS, geothermal, lithium-from-brine, or RNG optionality, which a pure O&G A&D shop will under-credit — pick a crossover bank (Nomura Greentech, CRC-IB / Canaccord, Marathon Capital); (3) you want the widest possible buyer universe in a thin oil-weighted market, where transition-credentialed banks bring IPPs, infrastructure funds, and strategics that O&G-only firms do not cover. The two scarcest currencies in 2025-26 renewables deals are interconnection-queue position and transferable tax credits (the tax-credit transfer market reached ~$60B in 2025, up from ~$52B in 2024) — so ask a renewables advisor specifically how they value your interconnection position and your transferable credits. If your transaction is still a straightforward producing-asset divestiture with no transition upside, a traditional A&D boutique remains the right call — do not over-pay for a transition skill set you will not use.

When is the best time in the commodity cycle to sell oil & gas assets?

Energy M&A is uniquely cycle-gated, so timing the banker to the cycle matters almost as much as timing the sale — auction tension is a function of the strip. The data shows it: US upstream M&A ran about $30.5B in the first half of 2025, down roughly 60% year-over-year as weak crude kept buyers in the dugout, then rebounded to a gas-weighted $23.5B in Q4 2025 and $38B in Q1 2026 (with the ~$25.4B Devon-Coterra merger alone driving about two-thirds of Q1 2026 value). Enverus analyst Andrew Dittmar noted in May 2026 that the case for higher-for-longer oil prices is strengthening and creating the setup for an M&A rebound. The practical read: in a trough with weak prices, bidders are few and processes are longer, so favor an A&D boutique that runs a targeted process with direct lines to the handful of active acquirers (and add a restructuring-capable bank like Houlihan Lokey if the situation is distressed); in a recovery with firming prices, competitive tension returns and a broader process can extract a premium. The structural nuance in 2026 is the gas-versus-oil divergence: if you are gas-weighted (Haynesville, Gulf Coast, Appalachia) you are in the hot part of the cycle thanks to LNG and datacenter demand — pick a gas / LNG / power-literate advisor; if you are oil-weighted Permian non-core, you are in the broadening tail where private operators may view current holdings as their final meaningful divestiture window — pick a technical A&D shop that can find regional and private buyers. The process mechanics for an upstream sale are in our upstream oil & gas divestiture data room timeline.

What should be in my data room before I take energy assets to market?

An energy data room is more technical than a generic M&A room, and getting it right before launch is the cheapest lever you control on both timeline and price. For an upstream / E&P asset, buyers expect: a current third-party reserve report (PDP / PUD / probable / possible on an SPE-PRMS or SEC case), production and decline-curve histories, well files, logs, and completion data, AFE and LOE / operating-cost detail, lease and title documents with division-of-interest and ownership confirmation, seismic and geologic mapping, marketing and transportation / gathering contracts, environmental and regulatory permits, and any plugging-and-abandonment liability schedule. Midstream rooms add firm-transportation and minimum-volume-commitment contracts, rights-of-way, FERC filings, and interconnection agreements; renewables rooms add interconnection-queue position, PPA / offtake terms, and tax-credit transfer documentation. The room should be staged: a teaser and high-level summary behind a clickthrough NDA, then a full technical room (well-level data, title, seismic) released only to NDA-signed bidders, with sensitive title and contract detail held to a short list after indications of interest. We built Peony — used by 5,900+ customers — for exactly this kind of tiered, watermarked release: per-bidder watermarks on every page render, staged folder permissions, and page-level analytics that show your banker which bidders are genuinely working the file. For the energy-specific buildout, see our best data room for oil and gas companies guide and the upstream divestiture timeline.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 5,900+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, industrials, and energy in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Contact: sean@peony.ink • LinkedIn.

You might also like

May 23, 2026

13 Best Boutique M&A Advisors in Denver for $5M-$200M Deals (2026)

Jun 16, 2026

18 Best Financial Services & FIG M&A Advisors for $25M-$1B Deals (2026)

Jun 15, 2026

22 Best Industrial & Manufacturing M&A Advisors for $25M-$1B Deals (2026)