22 Best Industrial & Manufacturing M&A Advisors for $25M-$1B Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

22 Best Industrial & Manufacturing M&A Advisors for $25M-$1B Deals (2026)

Quick answer: Industrial M&A does not have one "best advisor" — it has six subsector benches. For general industrials, precision components, and metal fabrication in the $25M-$1B band, the deepest names are Harris Williams, Houlihan Lokey, Lincoln International, Robert W. Baird, and William Blair, with regional independents Brown Gibbons Lang, Capstone Partners, Stout, KeyBanc, Stephens, P&M Corporate Finance, and Mesirow. For aerospace & defense, KippsDeSanto, KAL Capital Markets, and The McLean Group. For automotive & aftermarket, Piper Sandler and Stifel. For building products & HVAC, Brentwood Growth (plus Baird, Capstone, and BGL). For specialty chemicals, Grace Matthews and Piper Sandler's Valence Group. The bulge brackets — Goldman Sachs, Morgan Stanley, J.P. Morgan — own the $1B-plus value tables but are usually the wrong call below that. Pick by subsector and deal size, not by logo.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — metal-fabrication and precision-components sales, building-products and HVAC roll-ups, automotive-supplier carve-outs, aerospace and defense tuck-ins, industrial-distribution exits, and specialty-chemicals processes — and industrials is the sector where the type of advisor you pick changes the price the most, because so much of the value is physical and technical. A generalist banker who anchors on a single trailing-EBITDA number for a cyclical business, or who has never had to defend a 40%-concentration customer or a fleet of qualified machinery against a buyer's quality-of-earnings team, leaves real money on the table. At Peony we now serve more than 6,800 customers, and a large share of our deals live in exactly the $25M-$1B band this guide covers.

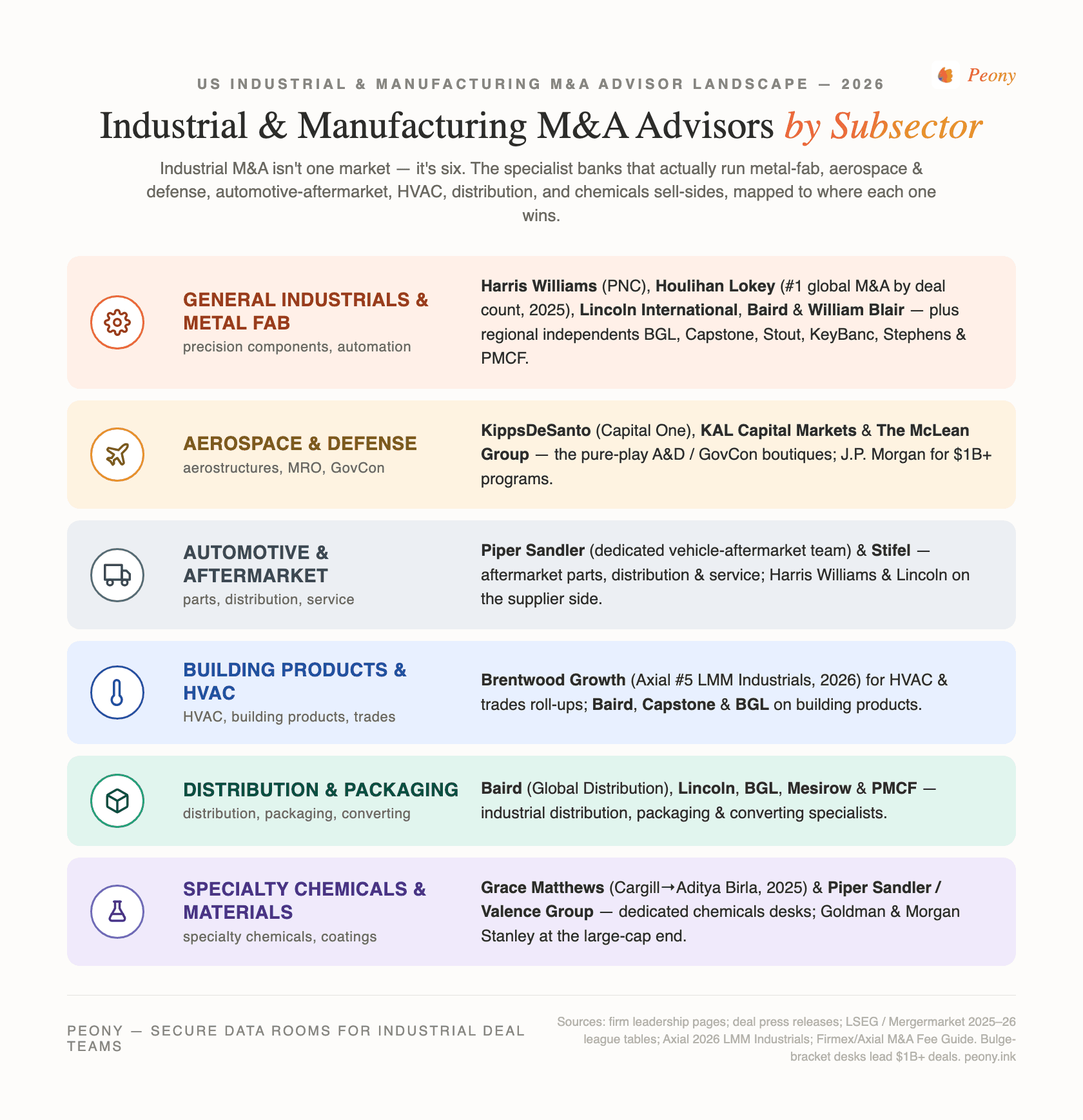

Most "best industrial M&A advisor" lists are interchangeable directory pages that rank firms one through ten as if a single league table existed. It does not. Industrial M&A splits into at least six distinct benches — general industrials and metal fabrication, aerospace & defense, automotive & aftermarket, building products & HVAC, industrial distribution & packaging, and specialty chemicals — and the firm that dominates one is often irrelevant in another. This post is organized the way the market actually works: by subsector, with each firm mapped to its lane, its deal-size band, and a verified credential or recent deal. The five proprietary frames — the Subsector Bench Map, the Tangible-Asset & Certification Translation Gap, Through-Cycle Earnings Normalization, the Customer-Concentration Discount Ladder, and the Strategic-versus-Sponsor Buyer Split — come from cross-referencing the verified 2024-2026 deal record against the structural realities of how industrial businesses get valued and sold.

Two framing notes before the roster. First, the confidentiality reality. In industrials your highest-paying buyers are frequently your direct competitors, so the whole process — teaser, CIM, and staged data room — has to be built to reveal the business case without handing over the keys. Second, honest framing on the bulge brackets. Goldman Sachs, Morgan Stanley, and J.P. Morgan own the value league tables, but they are not the answer for most readers of this guide, so I name them at the end to frame the ceiling. Peony is not an advisor — it is the data-room layer founders and bankers use to run the process; I will flag where that fits, but the advisory firms are the subject here. If you are on the buy side looking for capital to back a manufacturing acquisition rather than an advisor to sell one, that is a different list — see our independent sponsor manufacturing capital partners guide instead.

What's the industrial & manufacturing M&A advisor landscape by subsector in 2026?

The roster below is organized by subsector. Each firm is profiled in depth in its section; this table is the map. Several firms cover more than one subsector — Harris Williams, Houlihan Lokey, Lincoln, Baird, William Blair, BGL, and Capstone all run multiple industrial benches — and are listed under their primary home with cross-coverage noted in the profile.

| Firm | HQ | Deal-size band | Subsector focus | Credential / verified deal |

|---|---|---|---|---|

| Harris Williams | Richmond, VA | $50M-$2B+ EV | General industrials, diversified mfg (PNC-owned) | Dedicated Industrials Group; among the most active mid-market sell-side platforms |

| Houlihan Lokey | Los Angeles, CA | $25M-$5B | Industrials + restructuring bench | #1 global M&A advisor by deal count 2025 (318); #1 global industrials under $5B |

| Lincoln International | Chicago, IL | $50M-$2B+ | Industrials, automation, cross-border | Advised Hidden Harbor on Avtron Power Solutions → Legrand; filed NYSE IPO 2025 |

| Robert W. Baird & Co. | Milwaukee, WI | $50M-$1B+ | ~20 industrial subsectors (employee-owned) | #1 for Industrial PE M&A Exits, Mergermarket Q1 2026 |

| William Blair | Chicago, IL | $150M-$2B+ | Industrial products, advanced materials | Sole advisor to Royston Group on ~$325M sale to LSI Industries (Feb 2026) |

| Brown Gibbons Lang (BGL) | Cleveland, OH | $25M-$500M | Diversified industrials, plastics, building prod | Advised Five Lakes Manufacturing → Valesco (Jul 2025); Industrials Insider research |

| Capstone Partners | Boston, MA | $10M-$500M | Precision mfg, metals processing, HVAC (Huntington) | Nine industrials subsectors; recurring Industrials/HVAC/Aftermarket M&A reports |

| Stout | Detroit / Chicago | $25M-$500M | Metals & specialty manufacturing | Named Metals & Specialty Manufacturing coverage team |

| KeyBanc Capital Markets | Cleveland, OH | $50M-$1B+ | Diversified industrials (KeyCorp) | Advised TerraSource on its sale to Astec Industries (Jul 2025) |

| Stephens Inc. | Little Rock, AR | $50M-$1B | Diversified industrials & services (family-owned) | Family-owned since 1933; Diversified Industrials & Services group for owner-operators |

| P&M Corporate Finance (PMCF) | Detroit area, MI | $25M-$500M | Manufacturing specialist (Plante Moran affiliate) | Dedicated plastics, packaging, automotive & A&D teams; 300+ transactions |

| Mesirow | Chicago, IL | $25M-$500M | Diversified industrials, A&D, distribution | 220+ transactions; employee-owned; building its industrials & A&D bench |

| KippsDeSanto & Co. | Tysons, VA | $50M-$1B | Aerospace, defense & government services | Pure-play A&D/GovCon; publishes quarterly DealView Top-10 A&D report |

| KAL Capital Markets | Long Beach, CA | $25M-$500M | Aerospace & defense (independent) | A&D-only; one of its most active stretches in H1 2025 (7 deals) |

| The McLean Group | Tysons, VA | $25M-$500M | Defense, government & intelligence | DGI team blends bankers with former military/intelligence operators |

| Piper Sandler | Minneapolis, MN | $50M-$1B+ | Vehicle aftermarket; chemicals (Valence) | Dedicated Vehicle Aftermarket team; owns the Valence Group chemicals franchise |

| Stifel | St. Louis, MO | $50M-$1B | Auto aftermarket; diversified industries | Built an auto-aftermarket franchise; publishes an Aftermarket Outlook |

| Brentwood Growth | Berkeley Heights, NJ | $5M-$75M | HVAC, plumbing, trades & home/commercial services | #5 sell-side advisor on Axial's 2026 Lower-Middle-Market Industrials list |

| Grace Matthews | Milwaukee, WI | $25M-$500M | Specialty chemicals & material science | Advised Cargill on a 2025 specialty-chemicals sale to Aditya Birla |

| Goldman Sachs | New York, NY | $1B+ | Large-cap chemicals & diversified industrials | #1 global M&A franchise; mega-cap chemicals carve-outs |

| Morgan Stanley | New York, NY | $1B+ | Large-cap chemicals & materials | Among the deepest large-cap industrials/chemicals franchises |

| J.P. Morgan | New York, NY | $1B+ | Large-cap aerospace, defense & government | Dedicated Aerospace, Defense & Government Services coverage group |

Who are the best general industrial & diversified manufacturing M&A advisors?

For most family-owned manufacturers — precision components, metal fabrication, engineered products, automation — this is the bench that matters, and it is the deepest in the market. The split is between the large mid-market platforms that run wide auctions and the regional independents that win the founder-owned mandates the bigger firms overlook.

Harris Williams (Richmond, VA) is one of the most active dedicated mid-market industrials sell-side platforms in the country. Owned by PNC Financial Services Group since 2005 but operated as a standalone brand, it runs broad, polished, highly competitive processes and carries the deepest private-equity-sponsor relationships of any firm on this list — the right call when you want a wide auction. Its industrials practice spans diversified manufacturing, automation, specialty distribution, building products, and chemicals.

Houlihan Lokey (Los Angeles, NYSE: HLI) was the #1 global M&A advisor by deal count in 2025 with 318 transactions (LSEG), and its Industrials Group ranked #1 for global industrials deals under $5B. Independent and public, it pairs that reach with the deepest restructuring bench on the Street — which is exactly what you want if your business is cyclical, leveraged, or selling into a downturn.

Lincoln International (Chicago) is a global, independent mid-market bank with one of the deepest industrials benches and heavy cross-border sponsor flow; it filed for a NYSE IPO in 2025. On the deal record, it advised Hidden Harbor Capital Partners on the sale of Avtron Power Solutions to Legrand and has a record of packaging and automation closings across the mid-market.

Robert W. Baird & Co. (Milwaukee) is employee-owned and runs a Global Industrial group spanning roughly 20 industrial subsectors — diversified manufacturing, engineered products, automation, building products, and more. Baird ranked #1 for Industrial PE M&A Exits in Mergermarket's Q1 2026 table and reports 360-plus M&A transactions since 2017. Its named Defense & Government team (LinQuest → KBR, Applied Insight → CACI) and Thermal & Climate Technologies team make it a genuine multi-subsector platform.

William Blair (Chicago), also employee-owned, is a high-volume sponsor M&A franchise with deep industrial-products and advanced-materials coverage. It was sole financial advisor to Royston Group on its roughly $325M sale to LSI Industries, announced February 2026 at about 8x EBITDA — and it ran Driven Brands' US car-wash divestiture and the sale of United Building Solutions to AE Industrial Partners.

The regional independents are where many family manufacturers should start:

- Brown Gibbons Lang & Company (BGL) (Cleveland) is a partner-owned, heartland-rooted independent with a dedicated Diversified Industrials and Plastics practice and the recurring Industrials Insider research. It was exclusive advisor to Five Lakes Manufacturing on its July 2025 sale to Valesco Industries, and it added a managing director to lead packaging coverage in mid-2025.

- Capstone Partners (Boston, owned by Huntington Bancshares since 2022) runs nine industrials subsectors with explicit precision-manufacturing and metals-processing coverage, plus the most prolific recurring sector research in the lower-middle market — Industrials, HVAC Services, and Automotive Aftermarket reports. It absorbed TM Capital from Janney to deepen the bench.

- Stout (Detroit / Chicago) is one of the few mid-market banks with an explicitly named Metals & Specialty Manufacturing coverage team — directly on point if your business is metal fabrication or precision components.

- KeyBanc Capital Markets (Cleveland, part of KeyCorp) runs a long-standing Diversified Industrials franchise with strong family-business and sponsor coverage and full-service financing alongside M&A; it advised TerraSource on its July 2025 sale to Astec Industries.

- Stephens Inc. (Little Rock) is one of the largest privately held, family-owned full-service banks (since 1933), with a Diversified Industrials & Services group built for owner-operators and dedicated building-controls and smart-building-technology coverage — a natural fit for a multi-generational manufacturer that wants a banker with staying power rather than a revolving deal team.

- P&M Corporate Finance (PMCF) (Detroit area) is an affiliate of Plante Moran built specifically for manufacturers, with dedicated plastics, packaging, automotive, and A&D teams and 300-plus transactions — one of the most explicitly manufacturing-focused mid-market banks in the country.

- Mesirow Investment Banking (Chicago) is 100% employee-owned and actively building its diversified-industrials and aerospace/defense bench, with deep automotive-supplier and distribution coverage across 220-plus transactions.

Most of these firms anchor the geo cut of our city guides — see Chicago, Detroit, Cleveland, and Pittsburgh for where each bench sits.

Who are the best aerospace & defense (A&D) M&A advisors?

Aerospace and defense is its own world, with classified work, government-contract novation, and qualified-supplier status that a generalist cannot diligence. The specialists here are defined by their concentration in the sector and, often, by bankers who came out of it.

KippsDeSanto & Co. (Tysons, VA) is one of the most recognized pure-play A&D and government-services boutiques, owned by Capital One since 2019. Its senior team has advised on 200-plus transactions totaling $17B-plus, and it publishes the widely cited quarterly DealView Top-10 A&D report and an annual A&D / Government Services M&A survey — the market data most bankers in the sector quote.

KAL Capital Markets (Long Beach, CA) is a fast-growing, independent aerospace-and-defense-only boutique focused on the aerospace supply chain — aerostructures, MRO and aftermarket, OEM, space, and unmanned systems — for privately held lower- and middle-market sellers. It runs a high deal cadence relative to its size, with one of its most active stretches in the first half of 2025.

The McLean Group (Tysons, VA) is a long-standing independent boutique whose Defense, Government & Intelligence team blends bankers with former military and intelligence operators — useful when the buyer universe is cleared and the value is in a contract backlog.

Two cross-coverage notes: Robert W. Baird's named Defense & Government team is a credible large-mid-market option (LinQuest → KBR at $737M; Applied Insight → CACI), and Mesirow and P&M Corporate Finance both carry A&D benches. At the very top — programs above roughly $1B, prime-contractor carve-outs, and public-company mechanics — J.P. Morgan's dedicated Aerospace, Defense & Government Services coverage group is the bulge-bracket option; below that, a specialist boutique runs a better process. Our defense data-room solution covers the access-control and ITAR-sensitivity layer these deals demand.

Who are the best automotive & auto-aftermarket M&A advisors?

Automotive splits cleanly in two: the OEM-tied Tier 1/Tier 2 supplier world (cyclical, program-driven, capital-intensive) and the auto-aftermarket (parts, distribution, service — recurring, recession-resilient, and consolidating fast). The aftermarket is where most of the deal volume and the highest multiples sit, with 194-plus deals tracked into late 2025.

Piper Sandler (Minneapolis, NYSE: PIPR) runs a dedicated Vehicle Aftermarket Products & Services banking team spanning the full value chain — parts suppliers, distributors and jobbers, remanufacturers, installers and service providers, and powersports and commercial-vehicle aftermarket. It is the most clearly franchised aftermarket bench in the mid-market.

Stifel (St. Louis, NYSE: SF) built an auto-aftermarket franchise and publishes a recurring Aftermarket Outlook within its specialty-distribution coverage; note that its lead aftermarket banker departed in late 2024, so confirm current senior bench depth when you pitch it.

On the supplier side, Harris Williams (a dedicated transportation and heavy-duty aftermarket group) and Lincoln International are the deepest cross-coverage options, and Mesirow carries Tier 1/Tier 2 supplier and aftermarket coverage. For the OEM-tied supplier seller, the Detroit bench is decisive — see our Detroit M&A advisors guide.

Who are the best building products, HVAC & industrial-services M&A advisors?

Building products and HVAC are two of the hottest industrial subsectors in 2026, driven by an aging US housing stock, the return of strategic buyers, and a private-equity roll-up wave. Private equity closed a record 55 HVAC deals in 2024 (up 72% year over year), and HVAC-services M&A reached roughly 149 transactions through 2025 — with high-margin, maintenance-heavy platforms changing hands north of ~10x EBITDA.

Brentwood Growth (Berkeley Heights, NJ) is a dedicated lower-middle-market sell-side specialist in the trades — HVAC, plumbing, electrical, roofing, restoration, and home and commercial services — and one of the core advisors driving the HVAC roll-up, with relationships across thousands of PE, institutional, and strategic buyers. It was ranked #5 sell-side M&A advisor in the US on Axial's 2026 Lower-Middle-Market Industrials list (up from #6 in 2025).

On the building-products and equipment side, the larger benches dominate: Robert W. Baird runs a named Thermal & Climate Technologies team, Capstone Partners publishes the most-tracked HVAC Services M&A data and runs the deals behind it, William Blair advised on United Building Solutions → AE Industrial Partners, Brown Gibbons Lang runs a Building Products Insider franchise, and Stephens covers building controls and smart-building technology. For an HVAC or services platform under ~$75M, start with a trades specialist; above that, a building-products bench runs the broader process.

Who advises on industrial distribution & packaging M&A?

Industrial distribution and packaging trade on a blend of recurring volume, supplier relationships, and working-capital discipline, and the strongest coverage here is cross-coverage from the diversified platforms rather than standalone boutiques.

Robert W. Baird runs a dedicated Global Distribution group and packaging coverage; Lincoln International posted a record run of packaging transactions and carries deep specialty-distribution coverage; Brown Gibbons Lang added a managing director in 2025 to lead packaging; Mesirow runs a named Paper, Plastics & Packaging team alongside its Distribution & Supply Chain group; and P&M Corporate Finance carries dedicated plastics-and-packaging coverage built for converters and manufacturers. Harris Williams' specialty-distribution group rounds out the large-mid-market bench. The selection rule is the same as elsewhere: pick the firm that can name the specific strategic and PE consolidators active in your product category, not just the firm with "distribution" on a slide.

Who are the best specialty chemicals & materials M&A advisors?

Specialty chemicals is a technical, regulation-heavy subsector where formulation know-how, EHS posture, and customer qualification drive value — and it has its own dedicated bench.

Grace Matthews (Milwaukee) is one of the longest-standing dedicated chemicals M&A boutiques, advising across the full chemicals and material-science value chain — specialty chemicals, coatings, adhesives, and formulated products. It advised Cargill on the 2025 sale of a specialty-chemicals (formulated resins) facility to the Aditya Birla Group and closed 11 transactions in 2024.

Piper Sandler's chemicals group — the former Valence Group (acquired in 2020, rebranded under Piper Sandler in 2021) — is widely regarded as the largest wholly dedicated chemicals M&A advisor, having brought a 29-professional, all-chemicals team into the bank. For mid-market specialty-chemicals sellers, these two are the specialists to shortlist.

At the large-cap end — mega-cap petrochemicals deals and corporate carve-outs — the bulge brackets dominate. Goldman Sachs and Morgan Stanley were both advisers on the headline 2025 transaction, the $13.4B sale of NOVA Chemicals to Borouge Group International (ADNOC/OMV) announced in March 2025 (advisory sides per deal reports), and J.P. Morgan rounds out the large-cap chemicals bench. Below roughly $500M, a dedicated chemicals boutique runs a better, more confidential process.

How much is your manufacturing company worth? The 2026 industrial multiple ladder

Most mid-market industrial and manufacturing businesses trade in a roughly 6-10x EBITDA range in 2026, and the spread is driven less by sector than by quality. The ladder runs roughly like this:

- Sub-6x: commoditized job shops, single-process fabricators, heavily cyclical or capacity-constrained businesses, and companies with one customer above ~40% of revenue and no contractual protection.

- 6-8x: solid diversified manufacturers with a stable customer base, reasonable margins, and a clean balance sheet — the broad middle of the market.

- 8-10x: differentiated businesses with proprietary products or designs, qualified-supplier or sole-source positions, diversified blue-chip customers, and above-sector margins.

- 10x-plus: high-margin, maintenance-heavy, recurring-revenue niches — HVAC and industrial-services platforms most of all, which is why the PE roll-up has pushed those above ~10x.

Two levers move you within the ladder more than anything else, and both are where a specialist earns the fee. The first is Through-Cycle Earnings Normalization: a buyer will anchor on whichever trailing-twelve-month EBITDA suits it, so a specialist builds a normalized, through-cycle bridge — adjusting for one-time tooling, owner compensation, related-party rent, commodity swings, and non-recurring program costs — and defends it in the quality-of-earnings review. The second is the Tangible-Asset & Certification Translation Gap: the replacement value of your machinery, its remaining useful life, your AS9100 / IATF 16949 / Nadcap certifications, and your qualified-supplier status are real value a pure-EBITDA lens misses. The advisor's job is to translate iron and quality records into a higher multiple before the buyer's accountants translate them down.

What do industrial M&A advisors charge in 2026?

Industrial M&A is priced like the rest of the lower-middle market — a monthly retainer or work fee plus a success fee at close — and the "nobody uses Lehman anymore" line is a myth. A declining-rate Lehman-style formula is the single most common structure, used in about 44% of engagements (2024-25 M&A Fee Guide). In the lower-middle market you will most often be quoted the Double Lehman (10% of the first $1M of transaction value, 8% of the second, 6% of the third, 4% of the fourth, and 2% above $5M): on a $20M deal that is $600,000, or 3.0%, and on a $50M deal about 2.4%. The blended effective success-fee curve declines as deals grow — roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex/Axial M&A Fee Guide, 8th edition, N=456).

Three terms move the bill more than the headline rate, and all three are negotiable:

- The retainer credit. Expect a $5,000-$15,000/month work fee; confirm in writing that it is credited dollar-for-dollar against the success fee (about 72% are, per the 2021-22 Fee Guide survey — silence usually means you pay it on top).

- The fee base. Confirm whether "transaction value" is defined on equity or on enterprise value including assumed debt, and how earnouts, rollover equity, and seller notes are counted — a broad definition can add hundreds of thousands of dollars on the same headline price.

- The tail. Cap it to a named-buyer list the banker must deliver within ~10 days of termination, not a blanket 18-24 month claim on any buyer.

The single most underused lever is simply getting two or three competing proposals — only about 17% of sellers run a banker bake-off (2021-22 Fee Guide survey), and it is the cheapest leverage you will ever have. The worked Lehman and Double Lehman math, the retainer-credit traps, and the cautionary fee cases are in our M&A advisor fees hub, and the pricing for the data room itself sits on our pricing page.

What are the proprietary frames in this guide — and how do I use them?

These are the five Peony-original lenses this post is built on. Each turns a public fact into a decision you can act on.

- Subsector Bench Map (above): industrial M&A is six benches, not one league table. The firm that dominates HVAC is irrelevant in chemicals; the firm that runs $1B carve-outs is the wrong call for a $40M fabricator. Match the firm to your subsector and deal size first, then compare within that bench.

- Tangible-Asset & Certification Translation Gap: an equipment-heavy business carries value a pure-EBITDA process misses — machinery replacement value and remaining life, AS9100 / IATF 16949 / Nadcap certifications, and qualified-supplier status. The specialist's job is to translate balance-sheet iron and quality records into a higher multiple before a buyer's accountants translate them down to maintenance capex.

- Through-Cycle Earnings Normalization: manufacturing is cyclical, so whoever controls the earnings baseline controls the price. A generalist hands the buyer a single trailing-twelve-month number; a specialist builds and defends a normalized, through-cycle EBITDA bridge so a trough year does not cap your price and a peak year does not invite a "not sustainable" discount.

- Customer-Concentration Discount Ladder: a 40%-of-revenue top customer is not automatically a value killer. The ladder runs from raw concentration (a buyer's worst case) up through contract tenure, switching costs, sole-source or designed-in status, and program longevity — and the advisor's job is to surface the embeddedness evidence before the buyer prices in the worst case.

- Strategic-versus-Sponsor Buyer Split: strategics (often competitors) pay for synergy, capacity, and taking a rival off the board; PE platforms pay a disciplined, cash-flow-anchored price and want you to roll equity and stay. Run a dual-track process that makes both compete — and, because your strategic buyers are often direct competitors, build the data room for staged, walled disclosure from day one.

What's the honest take on the bulge brackets for industrials?

They own the value league tables, and below ~$1B they are usually the wrong call — but it is worth knowing the ceiling. Goldman Sachs runs the #1 global M&A franchise by value and the deepest large-cap chemicals and diversified-industrials bench, advising the mega-cap carve-outs and take-privates. Morgan Stanley carries one of the deepest large-cap industrials and chemicals franchises on the Street. J.P. Morgan pairs a top global M&A platform with a dedicated Aerospace, Defense & Government Services coverage group for the largest A&D mandates. All three were on the headline 2025 chemicals deal — NOVA Chemicals' $13.4B sale to Borouge — and that is exactly the kind of transaction they are built for.

The reason these are the wrong default for a $25M-$300M manufacturer is not quality — it is fit. Their economics, attention, and process are built for billion-dollar mandates, so your deal becomes their smallest of the quarter, staffed thin. A focused mid-market bank or regional independent with a real, current map of the strategic and PE consolidators in your subsector will run a tighter, more confidential process and put senior bankers on every buyer call — which, at this size, is what actually moves the price.

How does this compare to other sectors — and where does Peony fit?

If you are weighing an industrial sale against how other capital-intensive sectors run, two of our sector hubs are useful references: the best energy M&A advisors guide (how a reserve-report-driven sector picks advisors) and the best healthcare M&A advisors guide (regulatory-overhang and subsector-specialist dynamics). The best technology & software M&A advisors guide shows the same pattern in a recurring-revenue sector. The common thread across all four is identical: the firm that wins your value is the one that can speak your subsector's specific value language — reserves in energy, regulatory posture in healthcare, net revenue retention in software, and normalized through-cycle earnings plus certified capacity in industrials.

On the document side, the through-line is also constant — and in industrials it is unusually sharp, because your most likely buyers are direct competitors. Whoever you hire, your advisor will run the process out of a data room, and that room carries customer-level revenue, supplier terms, engineering drawings, process documentation, and certification records you cannot afford a competitor-bidder to walk away with. We built Peony, a SOC 2 Type II certified data room company used by 6,800+ customers, for exactly this kind of tiered, walled release: per-bidder visitor groups so a competitor sees only its tranche, per-page watermarks stamped with the viewer's identity on every render, screenshot protection on the most sensitive drawings, redaction to mask customer names until you choose to reveal them, and page-level analytics that show your banker which bidders are genuinely working the file. To be clear about scope: Peony is not an M&A advisor and does not place deals — the advisory firms above do that. Peony is the layer that makes the diligence run cleanly once you have hired one. See our manufacturing and M&A solution pages for the industrial setup, and our data-room analytics guide for reading buyer intent from engagement data.

The bottom line

Industrial M&A is not one league table — it is six subsector benches, and the right advisor for a $25M-$1B manufacturer is a function of your subsector and your deal size, not a logo. For general industrials and metal fabrication, start with Harris Williams, Houlihan Lokey, Lincoln, Baird, and William Blair, with BGL, Capstone, Stout, KeyBanc, Stephens, PMCF, and Mesirow as the regional independents that win family-owned mandates. For aerospace & defense, KippsDeSanto, KAL Capital, and The McLean Group; for automotive & aftermarket, Piper Sandler and Stifel; for building products & HVAC, Brentwood Growth plus Baird and Capstone; for specialty chemicals, Grace Matthews and Piper Sandler's Valence Group. Run a dual-track process so a strategic and a sponsor compete — and because your strategics are often competitors, walk in with normalized through-cycle earnings, a customer-concentration story, and a staged, walled data room before you launch. That preparation, not the banker's logo, is the cheapest lever you control on both timeline and price.

Related resources

- M&A advisor vs broker vs investment bank — the decision that comes before this shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- 14 Best Energy M&A Advisors by Subsector — the first national sector cut in this series, showing how a reserve-driven sector picks advisors

- 16 Best Healthcare M&A Advisors by Subsector — a sibling national sector cut: healthcare M&A advisors mapped by subsector

- 22 Best Technology & Software M&A Advisors by Subsector — the software sector cut, for recurring-revenue businesses

- How to write a CIM — the confidential information memorandum that tells your normalized-earnings and capacity story to buyers

- M&A due-diligence process guide — the full diligence arc buyers will run on a manufacturer

- Sell-side due diligence — the quality-of-earnings and normalization prep that defends your multiple

- M&A Data Room: setup and workstream mapping — the general sell-side data-room playbook, built for competitor-bidder confidentiality

- Industrial data room: the room that survives the buyer's engineer — selling the building, not the company: the spec-organized data room for an industrial property deal (clear height, ESFR, IOS zoning), distinct from the company-sale advisor selection in this guide

- Best data room for a small M&A deal — VDR selection for a sub-$30M sale, the right-sized room for a lower-mid-market manufacturer

- Data-room analytics: how to spot serious buyers — reading buyer intent from engagement data during a dual-track process

- Corporate divestiture data room — for carving a division or product line out of a larger industrial parent

- Best M&A Advisors in Columbus — the central-Ohio geo cut for manufacturers riding the Intel and data-center supply-chain buildout, where the homegrown boutiques (Copper Run, Footprint Capital) lead the lower-middle-market bench

- Best M&A Advisors in Cincinnati — the southern-Ohio geo cut for manufacturers and aerospace-supply sellers (the GE Aerospace orbit in Evendale), anchored by the homegrown registered bank RKCA

- Best M&A Advisors in Chicago, Detroit, Cleveland, and Pittsburgh — the industrial-heartland geo cuts of this national hub

Frequently asked questions

As a third-generation manufacturing owner exploring a sale, who are the best M&A advisors for selling a family-owned industrial company in 2026?

There is no single ranking — the best industrial M&A advisor depends on your subsector and deal size. For a diversified industrial, precision-components, or metal-fabrication business in the $25M-$1B range, the deepest mid-market benches are Harris Williams (owned by PNC since 2005, one of the most active industrials sell-side platforms), Houlihan Lokey (the #1 global M&A advisor by deal count in 2025 at 318 deals, and #1 for global industrials deals under $5B), Lincoln International (Chicago, which advised Hidden Harbor Capital Partners on the sale of Avtron Power Solutions to Legrand), Robert W. Baird (Milwaukee, employee-owned, ranked #1 for industrial PE M&A exits in Mergermarket's Q1 2026 table), and William Blair (Chicago, sole advisor to Royston Group on its ~$325M sale to LSI Industries in February 2026). Regional independents like Brown Gibbons Lang (Cleveland), Stephens (Little Rock, family-owned since 1933), and P&M Corporate Finance (a Plante Moran affiliate built specifically for manufacturers) win family-owned mandates the bigger banks overlook. The honest filter for a third-generation owner: ask each firm to name the five buyers it would call first for your specific product line, how many deals it has closed in your subsector in the last 18 months, and whether those went to strategics or to private equity. I run Peony, a SOC 2 Type II certified data room company that has served 6,800+ customers, and across hundreds of industrial diligence processes the firms that genuinely engage are the ones that can answer that without hesitating. The intermediary-tier decision sits upstream in our M&A advisor vs broker vs investment bank guide.

Selling my family-owned manufacturer, should I hire a sector-specialist industrial boutique or can a generalist M&A advisor handle it?

For most industrial sellers, a sector specialist beats a generalist — and the reason is concrete, not snobbery. A manufacturing business is priced off things a generalist process tends to flatten: normalized through-cycle EBITDA (not a single trough or peak year), the replacement value and remaining life of your machinery, your certifications and qualified-supplier status (AS9100 for aerospace, IATF 16949 for automotive, Nadcap for special processes), and the embeddedness of your top customer relationships. A generalist who runs a blunt trailing-EBITDA process will under-credit exactly what drives an industrial premium — long-tenured customer designs, switching costs, and domestic capacity a strategic acquirer wants. Just as important, a specialist already knows the active buyers in your niche: the PE platforms rolling up HVAC, distribution, or aftermarket parts, and the short list of strategics that would pay up to close a capability or capacity gap. The exception worth naming honestly: if your single most likely buyer is a strategic your family already knows well, a trusted generalist or even a direct negotiation can sometimes match a specialist's broad process — competition, not the banker's logo, is what moves price. But where the buyer universe is concentrated and the value drivers are technical, the specialist's Rolodex and subsector fluency usually outweigh the fee. The deeper distinction between a sector boutique, a full-service bank, and a business broker is in our M&A advisor vs broker vs investment bank hub.

Weighing my options for a $150M industrial sale, how do firms like Harris Williams, Lincoln International, and Houlihan Lokey compare for industrial M&A?

At a ~$150M enterprise value you are in the heart of the mid-market, where all three are credible but optimize differently. Harris Williams (Richmond, owned by PNC since 2005) runs broad, highly competitive sell-side processes with one of the deepest dedicated industrials groups and the strongest private-equity-sponsor coverage — a good fit if you want a wide auction and a polished process. Houlihan Lokey (the #1 global M&A advisor by deal count in 2025 at 318 transactions, and #1 for global industrials deals under $5B) pairs that reach with the Street's deepest restructuring bench, which matters if your business is cyclical or carrying leverage. Lincoln International (Chicago, independent, which filed for a NYSE IPO in 2025) brings heavy cross-border sponsor flow and a deep industrials team — it advised Hidden Harbor Capital Partners on the sale of Avtron Power Solutions to Legrand. The practical test at $150M is not the league-table logo but the deal team: insist on knowing which managing director (not a second-year associate) will personally run your process, and ask each to name the five most likely buyers and show two closings in your exact subsector in the last 18 months. For the geo cut, our city guides cover where these benches sit — Chicago, Detroit, Cleveland, and Pittsburgh.

As a Midwest factory owner, should I use a boutique investment bank or a bulge-bracket bank — and does a regional advisor reach national PE and strategic buyers?

For a Midwest manufacturer in the $25M-$1B range, a boutique or mid-market bank is almost always the right call, and a good regional advisor absolutely reaches national buyers — that worry is the most common and most mistaken one I hear. The active buyers for your business are a defined, national set: the private-equity platforms rolling up your category and the handful of strategics that want your capacity or customer base, and a credible mid-market bank already has those relationships regardless of where it is headquartered. Firms like Brown Gibbons Lang (Cleveland), Robert W. Baird (Milwaukee), William Blair (Chicago), KeyBanc Capital Markets (Cleveland), and P&M Corporate Finance (Detroit area) run national and cross-border processes from the industrial heartland every week. A bulge bracket (Goldman Sachs, Morgan Stanley, J.P. Morgan) only becomes the default above roughly $1B in enterprise value, where public-company mechanics, stock consideration, and mega-buyer relationships justify their minimums — below that, your deal becomes their smallest mandate of the quarter and gets staffed thin. The real question is not regional-vs-national but whether the senior banker pitching you will still be on every buyer call after you sign. Our advisor-vs-bank selection hub walks the full intermediary decision by deal size.

Preparing to take my manufacturing company to market, how does the sell-side process work start to finish and how long does it take to close?

An industrial sell-side runs the standard six-stage arc, and a well-run mid-market process typically takes about six to twelve months from launch to close. Roughly: (1) preparation and positioning (4-8 weeks) — normalize your through-cycle EBITDA, document your machinery, certifications, and customer contracts, build a clean data room, and draft the confidential information memorandum (CIM); (2) buyer outreach behind a teaser and a clickthrough NDA (3-5 weeks) — a focused list weighted toward the PE platforms and strategics actually active in your niche; (3) management meetings and indications of interest (4-6 weeks); (4) bid evaluation and selecting a lead party or short list; (5) confirmatory due diligence and exclusivity (6-10 weeks) — where a quality-of-earnings review, environmental and equipment diligence, and a working-capital study happen; and (6) purchase-agreement negotiation and close. The two things that most often add time are a messy or peak-/trough-distorted earnings picture that fails to reconcile in quality-of-earnings, and a thin buyer list that produces too little competitive tension. The single cheapest lever you control on both timeline and price is walking in with a diligence-ready data room and a CIM that already tells the normalized-earnings story — our how to write a CIM guide and M&A due-diligence process guide cover both.

Since my most likely buyers are direct competitors, how do I run a confidential sale and what should go in the data room or CIM?

This is the defining tension of an industrial sale: your highest-paying buyers are often the competitors you least want browsing your customer list, pricing, and process know-how. You manage it with staged disclosure, not by hiding the ball. Start with a no-name teaser, move to a CIM only behind a signed NDA, and release the most sensitive material — customer-level revenue, supplier terms, drawings, and process documentation — only to a short list of bidders after indications of interest, with the crown-jewel detail held until late confirmatory diligence under a clean-team arrangement. Your data room should be organized so a competitor-bidder sees the business case without the keys to it: financials and a normalized EBITDA bridge, an equipment and capacity schedule, certifications and quality records, a redacted customer-contract set (names masked until late), environmental and safety records, and the standard legal, HR, and tax sections. The tooling matters here more than in almost any other sector. We built Peony — a SOC 2 Type II certified data room used by 6,800+ customers — for exactly this: per-bidder visitor groups so a competitor sees only its tranche, per-page watermarks stamped with the viewer's identity on every render, screenshot protection on the most sensitive drawings, and redaction to mask customer names until you choose to reveal them. The full sell-side room buildout is in our M&A data room guide.

Before I sign an engagement letter to sell my factory, how do I vet an industrial M&A advisor and what questions should I ask?

Vet on subsector evidence and engagement-letter terms, in that order. On evidence, ask each firm in writing to: name the five buyers it would call first for your specific product line; list the deals it has closed in your exact subsector (metal fabrication, building products, aftermarket, A&D, chemicals) in the last 18-24 months, with the buyer type; identify the managing director who will personally run your process and be on every buyer call; and explain how it would normalize your through-cycle earnings and frame your customer concentration to a skeptical buyer. A real specialist answers without hesitating; a generalist reframes the question. On terms, read the engagement letter like a contract: confirm whether 'transaction value' is defined on equity or on enterprise value including assumed debt (a broad base quietly inflates the fee), whether the retainer is credited dollar-for-dollar against the success fee (about 72% are, per the 2021-22 M&A Fee Guide survey — only if the letter says so), and cap the tail to a named-buyer list the banker must deliver within ~10 days of termination rather than a blanket 18-24 month claim. The single most underused lever is simply getting two or three competing proposals — only about 17% of sellers run a banker bake-off (2021-22 Fee Guide survey), and it is the cheapest leverage you will ever have. The full engagement-letter mechanics are in our M&A advisor fees hub.

Worried about my equipment-heavy, cyclical business, will a generalist advisor undervalue an asset-heavy manufacturing company?

Often, yes — and the gap usually shows up in two places that a specialist defends and a generalist concedes. The first is earnings normalization. Manufacturing is cyclical, so a generalist who anchors on a single trailing-twelve-month EBITDA hands the buyer the year that suits the buyer — a trough year caps your price, and even a peak year invites a 'this isn't sustainable' discount. A specialist builds a through-cycle, normalized EBITDA bridge — adjusting for one-time tooling, owner compensation, related-party rent, commodity swings, and non-recurring program costs — and defends it in the quality-of-earnings review. The second is the asset and capability story. An equipment-heavy business carries value a pure-EBITDA lens misses: the replacement cost and remaining life of your machinery, your certifications and qualified-supplier status, spare capacity a strategic can fill, and long-tenured customer designs with real switching costs. I call the difference the Tangible-Asset & Certification Translation Gap — the specialist's job is to translate balance-sheet iron and quality records into a higher multiple before a buyer's accountants translate them down. The screening question for any advisor: ask them to walk through exactly how they would normalize your earnings across the cycle and how they would present your machinery and certifications as value rather than as maintenance capex. Our sell-side due-diligence guide covers the quality-of-earnings preparation that wins that argument.

With one customer at 40% of revenue and only $35M in sales, will customer concentration kill my valuation and am I too small for a real investment bank?

Neither is fatal, but both need to be managed, not hidden. On size: a $35M-revenue manufacturer (very roughly $25M-$70M EV at a mid-market multiple) is squarely in the sweet spot for the regional independents and lower-mid-market specialists — Brown Gibbons Lang, P&M Corporate Finance, Stephens, Capstone Partners, and Stout all build senior-led processes for businesses your size, and several will out-hustle a bulge bracket that would treat your deal as its smallest of the quarter. You are genuinely too small for a full-service bank only below roughly $10M-$15M EV, where a minimum-fee floor (commonly $50K-$250K, in about 67% of letters per the 2021-22 Fee Guide survey) eats an outsized share of proceeds. On concentration: a 40%-of-revenue top customer is a real discount risk, but a specialist reframes it. The Customer-Concentration Discount Ladder I use runs from 'raw concentration' (a buyer's worst case) up through contract tenure, switching costs, sole-source or designed-in status, and program longevity — the same 40% looks very different if it is a ten-year sole-source aerospace program under a long-term agreement than if it is a spot-buy relationship. The advisor's job is to surface the embeddedness evidence — contracts, design wins, requalification cost to the customer — before the buyer prices in the worst case. Ask any banker how they have handled a 30%-plus concentration account in a recent close; a specialist has a playbook, a generalist has a worry.

Deciding who buys my family manufacturer, is a strategic competitor or a private equity buyer likely to pay more, and is 2026 a good time to sell given reshoring and tariffs?

Run a process that puts both in competition, because in industrials the answer genuinely splits — this is the Strategic-versus-Sponsor Buyer Split. A strategic acquirer (often a competitor or an adjacent manufacturer) typically pays the highest price when your business closes a specific capability, capacity, or geographic gap or takes a competitor off the board — synergies it can underwrite let it stretch on price, though it may absorb your team and brand and can walk if the synergy case wobbles. A private-equity platform tends to pay a disciplined, cash-flow-anchored price, frequently wants the owner or management to roll equity and stay, and offers a structured path to a 'second bite' at the next exit — attractive if you want partial liquidity now and believe in the next chapter. PE-owned strategics (add-ons to an existing platform — common in HVAC, distribution, and aftermarket) blend both. On timing: the 2026 backdrop genuinely favors well-run domestic manufacturers, as reshoring and tariff pressure push strategic acquirers to value US capacity and supply-chain resilience — but treat that as a qualitative tailwind, not a guaranteed premium, and let competitive tension rather than a single inbound set your price. To read which bidders are actually working your file once the process is live, our data-room analytics guide covers the engagement signals that separate serious buyers from tire-kickers.

Budgeting the cost of selling my mid-market manufacturing company, what success fee do advisors charge and is the Double Lehman formula still standard in 2026?

Yes, Lehman-style formulas are still standard — the 'nobody uses Lehman anymore' line is a myth. A declining-rate Lehman structure is the single most common fee format, used in about 44% of engagements (2024-25 M&A Fee Guide), and in the lower-middle market you will most often be quoted the Double Lehman: 10% of the first $1M of transaction value, 8% of the second, 6% of the third, 4% of the fourth, and 2% on everything above $5M. On a $20M deal that computes to $600,000, or 3.0%; on a $50M deal, about 2.4%. The blended effective success-fee curve declines as deals get bigger — roughly 4.8% at $5M, 3.4% at $20M, and 2.0% at $100M (Firmex/Axial M&A Fee Guide, 8th edition, N=456). Expect a monthly retainer or work fee of about $5,000-$15,000 on top, and confirm in writing that it is credited dollar-for-dollar against the success fee (about 72% are, per the 2021-22 Fee Guide survey — silence usually means you pay it on top). The detail that moves the bill more than the rate is the base: confirm whether transaction value is defined on equity or on enterprise value including assumed debt, and how earnouts, rollover equity, and seller notes are counted — a broad definition can add hundreds of thousands of dollars on the same headline price. The worked Lehman and Double Lehman math, plus the cautionary fee cases, are in our M&A advisor fees hub.

Setting valuation expectations for my fabrication business, what EBITDA multiple can I expect in 2026 and is a sector-specialist's fee worth it versus a generalist?

On valuation: most mid-market industrial and manufacturing businesses trade in a roughly 6-10x EBITDA range in 2026, with the spread driven less by sector than by quality — sub-6x for commoditized, cyclical, or heavily concentrated job shops, and 9-10x-plus for differentiated businesses with proprietary products, recurring aftermarket revenue, strong margins, and diversified blue-chip customers. High-margin, maintenance-heavy niches run hotter: HVAC and industrial-services platforms have changed hands north of ~10x EBITDA, which is why private equity closed a record 55 HVAC deals in 2024 (up 72% year over year). On whether a specialist's fee is worth it: the math usually favors the specialist. A sector advisor who lifts your multiple by even half a turn of EBITDA creates far more value than the difference between a 2-3% and a 3-4% fee — and the specialist is the one who normalizes your through-cycle earnings, reframes your customer concentration, and runs the competitive process that actually moves the number. The fee is the visible cost; the invisible cost is the multiple a generalist leaves on the table. Set expectations with a real advisor against your specific margins, customer mix, and product differentiation, and compare two or three proposals before you sign — our M&A advisor fees hub shows how to read them side by side.