Corporate Divestiture & Carve-Out Data Room (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

I'm Sean Yu, co-founder of Peony, a data room platform used by 6,800+ teams across M&A, private equity, and due diligence processes. Before Peony I worked sell-side and growth processes at Nomura, Backed VC, and Target Global. This guide is about the deal type I think is the most operationally underrated in corporate finance: the divestiture — selling a division, subsidiary, or product line out of a parent — and its hard-mode cousin, the carve-out, where the thing you're selling was never a standalone company to begin with.

Here's why it's worth a dedicated playbook. A whole-company sale prices a clean entity. A carve-out prices a boundary that doesn't exist yet. In a stock sale, the legal entity is the perimeter — everything inside the corporate shell transfers, and your data room is organized around one company. In a divestiture, you're slicing a unit out of a parent that shares contracts, systems, people, IP, and overhead across multiple businesses, so the purchase agreement has to enumerate what's Transferred versus Retained — and the data room's real job is to make every hidden wire between the unit and its parent visible, labeled, and auditable. Get that wrong and the cost doesn't show up in diligence; it shows up after close, when a service silently stops working or a contract turns out to need a consent nobody asked for.

Quick answer: A divestiture or carve-out data room is a separation artifact, not just a diligence archive — it needs six folders a normal M&A room never has (perimeter schedules, carve-out financials, forward and reverse TSA schedules, a contract-by-contract consent tracker, the transferring-employee list, and IT/IP/data-separation plans). The hard parts are specific: carve-out financials exist because audited standalone statements usually don't — the parent only audits the consolidated group — so you build them from directly-attributable costs plus allocated overhead, and the allocation is the estimate (under SEC Reg S-X Rule 3-05 the statements themselves are typically audited). The TSA keeps the unit alive after close — PwC notes a typical exit involves more than 1,500 mostly-interdependent design decisions. And running multiple bidders means walling each off and redacting the retained parent's data out of shared files. Divestitures are not a niche: per Deloitte's 2024 Global Corporate Divestiture Survey, divestitures and spin-offs have made up 13–17% of global M&A volume and 16–22% of value over the six years through 2023. On Peony, per-bidder visitor groups and NDA gates start on the Business plan ($30/admin/month); the Data Room plan ($52/admin/month) — with dynamic watermarks, auto-indexing, and granular per-file permissions — is the anchor for a real carve-out process.

Why are companies divesting and carving out divisions in 2026?

Because divestiture stopped being a sign of weakness and became a recognized way to create value — and the data says focused sellers win. The last three years produced the densest run of large separations in a generation. General Electric finished its three-way breakup, spinning GE HealthCare in January 2023 and then splitting the remainder into GE Aerospace and GE Vernova on April 2, 2024 — all tax-free pro-rata spin-offs. Johnson & Johnson separated its consumer-health business as Kenvue through a carve-out IPO that priced at $22.00 per share in May 2023, raising about $4.24 billion, then split off the rest via a tax-free exchange offer — J&J called it the largest restructuring in the company's 135-year history. Novartis spun Sandoz in a 100% tax-neutral separation in October 2023; 3M spun its health-care business as Solventum on April 1, 2024; Kellogg split into Kellanova and WK Kellogg Co in October 2023; and the wave kept running into Honeywell's planned three-way breakup (its Solstice Advanced Materials spin completed October 30, 2025) and DuPont's spin of Qnity Electronics on November 1, 2025.

Not all of these are spin-offs to shareholders — and the difference matters for the room. Baxter sold its Vantive kidney-care unit to The Carlyle Group for $3.8 billion (announced August 2024, closed January 2025) — a sponsor carve-out that began life in 2023 as a planned spin and was executed as a sale. Emerson sold a majority of its Climate Technologies business (renamed Copeland) to Blackstone in a $14.0 billion deal, then sold its remaining stake later. Spin, carve-out IPO, or sale to a strategic or PE buyer — the exit structure differs, but the separation mechanics underneath are the same, and they're what this post is about.

The strategic logic is now backed by evidence sellers cite in board decks. Bain's study of 2,100 public companies found that focused divestors outperformed inactive companies by about 15% in 10-year total shareholder return, and that the gap widened to nearly 40% for companies that paired divestment with a repeatable M&A model. Bain also found that among the 137 largest divestitures, those done to refocus on the core lifted market cap 7.9% within three months of announcement, versus only 1.4% for cash-driven sales — markets reward strategic clarity, not fire sales. And EY's 2021 Global Corporate Divestment Study found 78% of executives admit they held an asset too long and 79% said their most recent divestment fell short of price expectations — which is exactly the gap a well-run process and a clean room close.

What is a corporate divestiture (or carve-out) data room, and how is it different from an M&A data room?

It's a separation artifact, not just a diligence archive — and the difference is structural, not cosmetic. A standard M&A data room is organized around one company and answers "what is this business worth and what are its risks?" A divestiture room has to answer a prior question first: "where does this business actually end?" Because the unit was embedded in a parent, the room's job is to draw and defend a boundary — and that adds layers a whole-company room never carries.

Concretely, a carve-out room needs six things a normal M&A room doesn't:

- Perimeter schedules — the in-scope vs out-of-scope list of assets, contracts, employees, IP, and data.

- Carve-out / standalone financials — built, not audited-as-an-entity, and labeled as allocated estimates.

- Forward and reverse TSA schedules — what the seller keeps providing post-close, and what flows back.

- A contract-by-contract consent tracker — every agreement with an anti-assignment or change-of-control clause.

- The transferring-employee list — who moves, plus retention agreements for key people.

- IT / IP / data-separation plans — how shared systems, patents, and commingled data get split.

This is also where the divestiture room differs from a sector-specific divestiture playbook. If you're selling a single upstream oil and gas asset, the hard problem isn't entanglement — it's reserves-disclosure tiering, and I wrote that one up separately as the upstream oil and gas divestiture data room timeline (with its sibling, the oil and gas farm-out data room). This guide is the cross-industry corporate carve-out: separating an entangled business unit from a shared parent, whether you're in industrials, healthcare, tech, or consumer. The mechanics below apply to all of them.

Why is defining the perimeter the hardest part of a carve-out? The Perimeter Problem

Because in a carve-out there's no boundary until you draw one, and every undrawn line is a future cost, a missing capability, or a dispute. Call it the Perimeter Problem. In a whole-company sale the legal entity is the perimeter, so most anti-assignment clauses never trip and the financials already exist. In a carve-out, the sale agreement has to literally list which assets, contracts, employees, IP, and data are Transferred versus Excluded — and the genuinely hard cases are the commingled, dual-use items that serve both the unit and the retained parent:

- A master supply agreement covering the whole parent, where only part serves the unit.

- A shared ERP or CRM instance holding both businesses' data.

- A factory or office lease used by multiple divisions.

- A patent family protecting both carved-out and retained products.

- A salesperson who sells across the parent's entire portfolio.

Each one has to be split, assigned, sub-licensed, duplicated, or kept alive under a service arrangement — there's no clean default. And here's the part that breaks first-time sellers: the perimeter is rarely final when the room opens. It's negotiated during diligence, as buyers push to pull in capabilities and sellers push to keep retained-business assets out. So the room can't be a hard-coded folder tree you rebuild every time scope moves; it has to be a stable structure with per-document permissions you flip as items shift in and out. On Peony, granular per-file permissions and visitor groups let you move a document in or out of a bidder's view without re-uploading or re-indexing — so the room tracks a moving perimeter instead of lagging it.

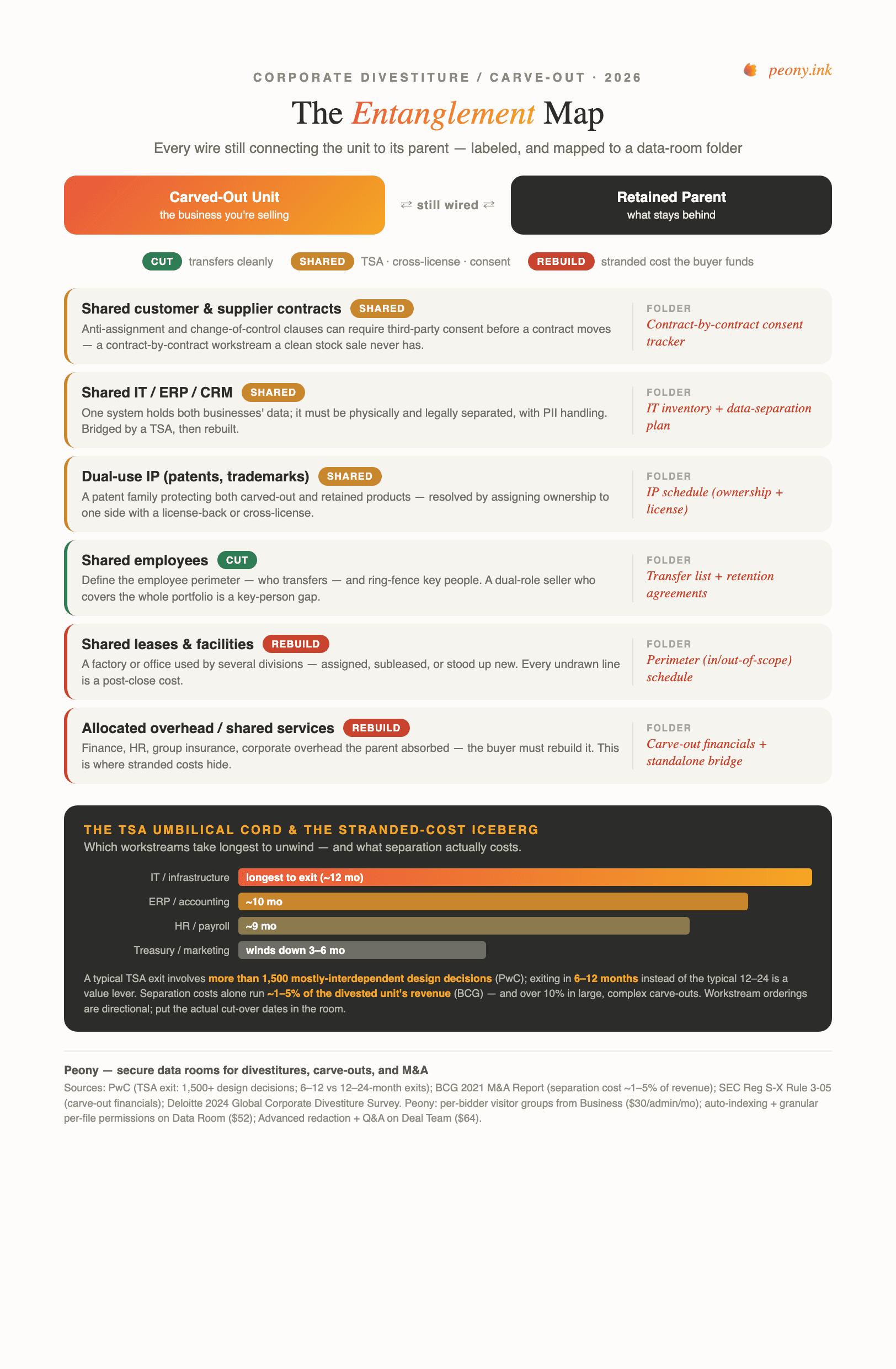

What is the entanglement map, and what folders does a divestiture room need? The Entanglement Map

The single most useful artifact in a carve-out is what I call the Entanglement Map: a map of every wire still connecting the unit to its parent, with each wire labeled Cut (it transfers cleanly), Shared (it needs a TSA, cross-license, or consent), or Rebuild (it's a stranded cost the buyer has to fund). You can't price the deal or close it until every wire has a label — and the beauty of the map is that the data-room folder list falls out of it almost one-to-one. Build the room as the answer to the map:

| Divestiture folder (beyond the normal M&A set) | What the buyer is really underwriting |

|---|---|

| 1. Perimeter schedules (in-scope vs out-of-scope) | Where does the business end? Every ambiguous item is a post-close cost or dispute |

| 2. Carve-out / standalone financials | The unit's real economics — directly-attributable costs plus allocated overhead (the allocation is the estimate) |

| 3. Standalone cost bridge / stranded-cost analysis | What it actually costs to run alone — shared services to rebuild, dis-synergies from lost scale |

| 4. Forward TSA schedule | Services the seller keeps providing (payroll, IT, ERP, accounting) and for how long |

| 5. Reverse TSA schedule | Services the buyer provides back for assets the parent retained |

| 6. Contract-by-contract consent tracker | Every customer/supplier contract with an anti-assignment or change-of-control clause |

| 7. Transferring-employee list + retention agreements | Who moves, who's a key-person risk, who's a dual-role gap |

| 8. IT systems inventory + data-separation plan | How shared ERP/CRM data is physically and legally split, with PII handling |

| 9. IP schedule (ownership + license treatment) | Dual-use patents/trademarks — who owns, who licenses back |

Everything in a normal due diligence data room checklist still applies on top of this — corporate, commercial, tax, litigation, HR. The nine rows above are the separation layer that a whole-company room doesn't have. On Peony, auto-indexing classifies and structures these folders automatically so you're not hand-building the tree, and the data room folder structure guide covers the base layout this extends.

Why don't audited standalone financials exist, and what are carve-out financials?

Because the parent only audits the consolidated group — there was never a separate entity to audit — so for a sub-unit you construct carve-out financials instead. These pull the unit's directly-attributable revenues and costs from the parent's books, then allocate shared corporate overhead (finance, HR, IT, legal, executive) down to the unit, with footnotes stating that the allocation is a reasonable estimate of standalone costs. The precision that matters, and that a sharp buyer's accountant will test: the statements themselves are typically audited under SEC Reg S-X Rule 3-05 — what's an estimate is the overhead allocation, not the audit status. Don't tell a buyer your carve-out numbers are "unaudited estimates"; tell them the allocation is an estimate and the statements are audited.

A few rules shape what has to be in the room:

- Rule 3-05 and the 20% test. For an acquirer that must report a significant acquisition, audited Rule 3-05 carve-out statements plus Article 11 pro-forma financials are mandatory filings. There's a relief valve: under Rule 3-05(e), when the carved business's total assets and revenues are each 20% or less of the seller and the unit was never a separate entity with previously-prepared statements, the SEC permits abbreviated statements — audited statements of assets acquired and liabilities assumed, plus audited statements of revenues and expenses. The 20% test gates the abbreviated relief, not whether carve-out statements are required at all.

- The 2020 modernization. SEC Release 33-10786 (adopted May 20, 2020, effective January 1, 2021) raised the disposition significance threshold from 10% to 20% and replaced the old pro-forma criteria with three adjustment types: transaction-accounting adjustments, autonomous-entity adjustments, and optional management's adjustments. The SEC explicitly declined to codify detailed carve-out requirements, noting that allocation questions can require unique judgments best handled through staff consultation.

- Spin-offs file their own. In a spin-off, the spun-off entity files its own carve-out audited financials (typically in a Form 10) with Article 11 pro-formas. Either way, the room's financial package is a regulatory deliverable, not just a sales aid — which is one more reason to get the allocation defensible before a bidder, or the SEC staff, sees it.

What are stranded costs and dis-synergies, and why do they hide in the financials? The Stranded-Cost Iceberg

Because the allocated overhead a buyer sees is the tip; the real standalone cost sits below the waterline. This is the Stranded-Cost Iceberg. When a unit separates, the costs the parent quietly absorbed — shared services, group insurance, group purchasing scale, corporate overhead — have to be rebuilt by the buyer, and dis-synergies from lost scale pile on top. The trouble is that a simplistic allocation can run lower or higher than true standalone cost, so a buyer who takes the carve-out P&L at face value is underwriting a number that doesn't exist in the real world. The honest seller brings a bridge from the allocated P&L to a true standalone cost model and lets the buyer see it.

How big is the iceberg? Per BCG's analysis of more than 50 divestitures, separation costs alone typically run roughly 1% to 5% of the divested business's revenue, and can exceed 10% in large or complex carve-outs. That's separation spend — the one-time cost to stand the unit up — distinct from the ongoing dis-synergies. A buyer who finds these in the room, quantified and scheduled, prices them in calmly; a buyer who discovers them after signing repricing the deal or walks. The whole point of disclosing the iceberg is that a quantified stranded cost gets financed, while an unquantified one gets a punitive, worst-case discount. The same logic that governs how you structure an earnout applies here: scheduled, evidenced numbers hold their value; vague ones get marked down.

What is a TSA — and a reverse TSA — and how long do they run? The TSA Umbilical Cord

A Transition Service Agreement is the umbilical cord that keeps the carved-out unit alive after close, because the buyer can't breathe on its own on day one. The seller keeps running payroll, IT, ERP, and accounting for the unit for a defined window while the buyer stands up its own functions — and the room has to hold the cord's full anatomy: the forward TSA schedule (what the seller provides, at what service level, until when), the reverse TSA schedule (services that flow back to the parent for retained assets that still depend on the unit's people or systems), and a dependency / exit map with cut-over dates.

Two facts to put in front of a buyer. First, this is genuinely complex: PwC notes a typical TSA exit involves more than 1,500 mostly-interdependent design decisions — which is why a missed dependency means a service silently stops working post-close, and why the schedules belong in the room from day one rather than getting negotiated by email after signing. Second, the duration is a value lever, not an afterthought: TSAs commonly run 3 to 12 months of active service with initial terms often capped around 12 months, and PwC frames completing exits in 6 to 12 months instead of the typical 12 to 24 as a way to unlock deal value. In practice IT and infrastructure are usually the longest workstream to unwind, followed by ERP/accounting and HR/payroll, while treasury and marketing co-use wind down fastest — but treat those orderings as directional, and put the actual per-service exit dates in the room. The tension is structural: the buyer wants a longer cord for runway; the seller wants a shorter one to stop carrying a business it sold.

Which contracts and employees need special handling in a carve-out? The Consent Minefield

Shared contracts are a minefield because each one can carry an anti-assignment or change-of-control clause that requires a third party's prior written consent before the contract can move with the unit — and courts generally enforce comprehensive clauses and treat a change of control without consent as a breach. In a clean stock sale of a whole entity, many of these clauses never trip, because the contracting party doesn't change. In a carve-out — especially an asset deal, where the contract is physically moved to a new entity — assignment is triggered, and you face a contract-by-contract review to flag every agreement that needs consent. Miss one on a key customer and the buyer can lose the revenue the moment the counterparty objects.

So the room needs a consent tracker as a living schedule: contract, counterparty, clause type, consent required (yes/no), status, owner, deadline. The employee side is its own workstream — the employee perimeter defines which headcount transfers, and you ring-fence and retain the key people, because a dual-role employee who sells or operates across the whole parent portfolio is a key-person risk if they don't come with the unit. Org charts, the transfer list, and retention agreements are core room documents, and employee PII in them should be redacted before bidders see it. Running these moving workstreams is exactly what the Advanced Q&A module on Peony's Deal Team plan ($64/admin/month) is for — assignment, deadlines, and an audit trail — and it pairs with the broader data room Q&A discipline of never letting one bidder's questions become visible to another.

How do you separate shared IT, IP, and data — and why is redaction structural?

You separate them with three room artifacts — an IT-systems inventory plus a data-separation plan, an IP schedule with ownership and license treatment, and the transferring-employee list — and you treat redaction as structural, not incidental. Here's why redaction is load-bearing in a divestiture specifically: the shared documents a buyer needs to see will name the retained businesses the buyer has no right to see. A master contract lists all the parent's divisions. A consolidated org chart shows retained-business headcount. A shared-services invoice itemizes costs for units that aren't in the deal. If you share those raw, you've leaked the parent. So the redaction has to be permanent and flattened — not a layer or a black box that can be pulled off or copy-pasted around to re-expose the underlying text.

On the IT and IP mechanics: commingled data inside a shared ERP/CRM must be physically and legally separated, which raises PII and privacy handling and is often the longest pole in the separation tent; dual-use IP gets resolved by assigning ownership to one side with a license-back or cross-license, documented in the IP schedule. Because these separation documents are the most leak-sensitive in the whole room, I run screenshot protection and Screenshield screen-capture blocking on the Data Room plan ($52/admin/month), with permanent redaction (Advanced redaction on Deal Team, $64/admin/month) to strip retained-parent data, and dynamic per-viewer watermarks (Data Room, $52/admin/month) so any leaked page identifies the exact viewer who leaked it.

How do you run one room for multiple bidders without leaking the retained parent? The Two-Audience Wall

You build a Two-Audience Wall — because in a divestiture you're protecting against two audiences at once, not one. In a normal auction you wall bidders off from each other. In a carve-out you also wall every bidder off from the parent's retained-business data baked into shared documents. The design that serves both: one canonical room, each bidder in its own visitor group (isolated documents, its own NDA gate, tracked links, and audit trail, so no bidder can tell another exists), plus permanent redaction of retained-parent data from any shared file. This is the One Room, Many Walls pattern I wrote up for competitive auctions, applied to a separation.

Stage the disclosure as bidders get serious: the perimeter manifest and summary economics to the broad field, then audited carve-out financials and the standalone bridge to the shortlist, then the most sensitive separation detail — stranded-cost analysis, key-employee retention, consent exposure on marquee contracts — to the lead bidder and its clean team. Route every question through a moderated Q&A workflow so nothing one bidder asks is auto-broadcast to another. One honest limit worth stating plainly: if you need physically walled per-bidder Q&A threads inside one room, that's a Peony Enterprise capability — on Business and Data Room the moderated workflow still prevents cross-bidder leakage because answers are never auto-published, but the separate-thread architecture is Enterprise. I'd rather you know that going in than discover it mid-process.

What's the best data room for a divestiture or carve-out?

Segmented honestly, because the right answer depends on who's running your process and how big the deal is:

| Capability | Peony | Datasite | Intralinks | Firmex | Ansarada |

|---|---|---|---|---|---|

| Auto-indexing for carve-out folders | Yes (Data Room) | Partial | Partial | No | Yes |

| Per-bidder isolation (visitor groups) | Yes (Business) | Yes | Yes | Yes | Yes |

| Permanent / flattened redaction | Yes (Deal Team) | Yes | Yes | Limited | Limited |

| Dynamic per-viewer watermarks | Yes (Data Room) | Yes | Yes | Yes | Yes |

| Screen-capture blocking | Yes (Screenshield, Data Room) | Yes | Yes | Limited | Limited |

| Walled per-group Q&A threads | Enterprise | Yes | Yes | Yes | Yes |

| Pricing shape | Flat per admin | Metered per deal | Metered per deal | Per deal | Metered |

| Indicative cost, one process | $52–64/admin/mo | tens of thousands | tens of thousands | ~$5–10K/deal | $479+/mo entry |

How to read it. If a bulge-bracket bank runs your divestiture, it will probably put you on Datasite or Intralinks — they're built for banker-run processes with service teams attached, and the bank's staff already knows the tooling. Pay the metered cost knowingly. (As you compare "alternatives," know that Datasite acquired Firmex in 2021 and Ansarada in 2024 — three of the five logos here are one company.) If a corporate-development team or a boutique advisor runs the process — which describes most mid-market carve-outs — the job is a perimeter-tracking room with per-bidder walls, carve-out-financial staging, and watermark-everything at a flat, predictable price, and that's the lane Peony is built for: SOC 2 Type II certified, used by 6,800+ teams, live the same afternoon. Where Peony honestly loses: walled per-bidder Q&A threads on a standard tier (an Enterprise feature on Peony; Firmex's coordinator workflow is the strongest standard-tier version), and vendor-staffed teams to run a $1B-plus banker-led process for you.

| Your situation | Best choice | Why |

|---|---|---|

| Mid-market carve-out, corp-dev- or boutique-run, 2–8 bidders | Peony (Data Room, $52) | Perimeter-tracking permissions + per-bidder walls + auto-indexing, flat price |

| Banker-run divestiture of a major division, full service team | Datasite / Intralinks | Built for bank-led mega-processes; your bank already runs them |

| Walled per-bidder Q&A threads required on a standard tier | Firmex | Its Q&A coordinator workflow is the strongest standard-tier version |

| Carve-out program with a multi-deal pipeline | Peony (Deal Team, $64) | Flat per-admin across unlimited rooms; one room per target |

| $1B-plus regulated separation with bespoke antitrust workstreams | Datasite / Intralinks | Enterprise compliance tooling and staffing fit the deal size |

These are the same intermediary economics I broke down in M&A advisor fees and the investment banking data room guide — the bank's tooling default travels with the bank's mandate.

How much should the data room cost for a divestiture?

A few hundred dollars a month flat, not five figures — if you avoid metered pricing, because a carve-out is close to the worst-case shape for a meter. The process runs long (often 6 to 24 months once TSA negotiation is included), the document set is large (carve-out financials, contract-by-contract schedules, separation plans), and parallel bidders multiply access — and per-page, per-user, and per-GB models price every one of those variables in. Firmex typically lands around $5,000 to $10,000 per deal; Datasite and Intralinks commonly reach the tens of thousands for a single process; Ansarada's metered entry starts around $479/month ($244 on a 12-month term). Flat-rate removes the variables: Peony's Data Room plan is $52/admin/month (billed annually) with unlimited rooms, storage, and bidders, and the M&A-grade Deal Team plan is $64/admin/month — so two admins on the Data Room plan over a nine-month process spend roughly $940 total. Set that against a separation budget that runs 1% to 5% of the divested unit's revenue, and the room is a rounding error. The full math on why metering punishes long, document-heavy processes is in flat-rate vs per-GB pricing — optimize for predictability and a perimeter-tracking structure, not for the cheapest possible sticker.

Frequently asked questions

I've only ever run whole-company sales — what's actually different about a carve-out data room?

A carve-out data room is a separation artifact, not just a diligence archive. In a whole-company stock sale the legal entity is the perimeter: everything inside the corporate shell transfers, and one company's documents fill the room. In a divestiture you're slicing a division out of a parent that shares contracts, systems, people, IP, and overhead across several units — so there is no pre-existing boundary, and the room's real job is to make every wire still connecting the unit to its parent visible and labeled. That adds six folders a normal M&A room never has: in-scope vs out-of-scope (perimeter) schedules; carve-out / standalone financials labeled as allocated estimates; forward and reverse Transition Service Agreement (TSA) schedules; a contract-by-contract consent tracker; the transferring-employee list with retention agreements; and IT / IP / data-separation plans. I extend the generic folder tree from the M&A data room guide with exactly those layers. On Peony, auto-indexing on the Data Room plan ($52/admin/month) structures those folders automatically, and granular per-file permissions let you release the sensitive separation detail in stages.

I'm in corp-dev prepping a $300M carve-out — do I need carve-out financials before I open the data room?

Usually yes — they are the gating document — but you can stage them. A buyer cannot value a division that has no standalone profit-and-loss, so carve-out financials are the price of entry: the unit's directly-attributable revenues and costs pulled from the parent's books, plus allocated shared overhead (finance, HR, IT, legal, executive), with footnotes disclosing that the allocation is a reasonable estimate of standalone costs. The nuance most first-timers get wrong: under SEC Reg S-X Rule 3-05 these statements are typically audited for a significant acquisition — what is an estimate is the overhead allocation, not the audit status. Practically, you do not need every audited statement before the room opens. Open with the perimeter manifest and summary economics to the broad bidder field, then release the audited carve-out statements and the standalone-cost bridge to the shortlist as they sign deeper NDAs. Peony's granular per-file permissions on the Data Room plan ($52/admin/month) stage exactly that disclosure ladder without spinning up a second room.

We have no audited standalone financials for the division we're selling — what goes in the data room?

That is the normal starting point, not a problem — the parent only audits the consolidated group, so audited standalone statements for a sub-unit usually do not exist, and you construct carve-out financials instead. Put in: the unit's directly-attributable revenues and costs extracted from the parent's books; the allocated shared overhead (finance, HR, IT, legal, executive); and — the part that protects your price — a bridge from that carve-out P&L to a true standalone cost model that shows the stranded costs and dis-synergies a buyer will have to fund. The footnotes should state that the allocation is a reasonable estimate of standalone costs. One relief valve worth knowing: under Rule 3-05(e), when the carved business's total assets and revenues are each 20% or less of the seller and the unit was never a separate entity with previously-prepared statements, the SEC permits abbreviated financial statements — audited statements of assets acquired and liabilities assumed plus audited statements of revenues and expenses. Peony's Data Room plan ($52/admin/month) holds the carve-out package and the standalone bridge as indexed documents the shortlist unlocks together.

Our carve-out perimeter is still being negotiated — how do I keep the data room straight while scope keeps moving?

Treat the perimeter as a live document, not a fixed folder tree — that is the single biggest mindset shift in a carve-out. The sale agreement has to enumerate which assets, contracts, employees, IP, and data are Transferred versus Retained, and that line genuinely moves during diligence as buyer and seller negotiate what is in scope. So build a master in-scope / out-of-scope schedule as the room's index, and when an item shifts in or out of the deal, re-permission it rather than rebuilding the folder structure. The wrong design is a hard-coded folder tree you have to tear down every time the boundary moves; the right one is a stable structure with per-document access you flip. On Peony, granular per-file permissions and visitor groups on the Data Room plan ($52/admin/month) let you move a document in or out of a bidder's view in one click — no re-upload, no re-indexing — so the room tracks the perimeter instead of lagging it. This is also why I tell sellers to open the room before scope is fully locked rather than wait.

I've got five bidders on a divestiture — how do I run them in one data room without leaking the retained parent's data?

One room, many walls — give each bidder its own visitor group and permanently redact the retained parent's data from any shared file. A divestiture carries a risk a clean sale does not: over-disclosure leaks the parent, not just the target. A master supply contract, a consolidated org chart, or a shared-services invoice will name retained businesses the buyer has no right to see. So the discipline is double — isolate each bidder from the others (own documents, own NDA gate, own tracked links, own audit trail, so no bidder learns another exists) and strip retained-parent data from shared documents with permanent, flattened redaction, because layer-based or copy-paste redaction can be reversed and re-expose the parent. One honest constraint on Peony: moderated Q&A prevents cross-bidder leakage because nothing one bidder asks is auto-broadcast, but physically walled per-group Q&A threads are an Enterprise capability — not Business or Data Room. Visitor-group document isolation and NDA gates start on the Business plan ($30/admin/month); granular per-file permissions, dynamic watermarks, and Screenshield are on the Data Room plan ($52/admin/month).

I'm running a carve-out auction — should I set up one data room with permission groups, or a separate room per bidder?

One room with per-bidder visitor groups — not a room per bidder. A separate room for each buyer multiplies version control: the moment your perimeter moves or you re-cut a carve-out schedule (which happens constantly in a divestiture), you have to push the same change into every room and you will eventually miss one, which is how a bidder ends up diligencing a stale standalone P&L. The correct design is one canonical room that is the single source of truth, with each bidder walled into an isolated visitor group so they see only their own documents, NDA status, and audit trail. With unlimited rooms on Peony you technically could spin up one per bidder, but you should not. Note the tier line: the Business plan ($30/admin/month) caps at three rooms per admin and isolates documents by group; the Data Room plan ($52/admin/month) adds unlimited rooms plus granular per-file permissions, which is what lets you stage perimeter-sensitive detail bidder by bidder inside that one room.

My carve-out has a 12-month TSA and dozens of shared contracts — how do I handle the TSA schedules and consents in the data room?

Put both in as living schedules with owners and deadlines, because they are where carve-outs actually slip. The buyer cannot operate the unit on day one, so the seller keeps providing payroll, IT, ERP, and accounting through a Transition Service Agreement — and the room needs three things: the forward TSA schedule, the reverse TSA schedule (services the buyer provides back for assets the parent retained), and a dependency / exit map with cut-over dates. This is not trivial admin: PwC notes a typical TSA exit involves more than 1,500 mostly-interdependent design decisions, and exiting in 6 to 12 months instead of the typical 12 to 24 is a real value lever — a missed dependency means a service silently stops working post-close. Alongside the TSA, maintain a contract-by-contract consent tracker that flags every customer or supplier agreement with an anti-assignment or change-of-control clause requiring third-party consent. On Peony, the Deal Team plan ($64/admin/month) adds the Advanced Q&A module — assignment, deadlines, and a full audit trail — to run the TSA and consent workstreams without exporting them to a side spreadsheet.

The division I'm selling shares our ERP and a patent family — how do I separate IT, IP, and employee data for diligence?

With three room artifacts: an IT-systems inventory plus a data-separation plan, an IP schedule with ownership and license treatment, and a transferring-employee list with retention agreements. Each maps to a real separation problem. Shared ERP/CRM instances hold both businesses' records, so the data must be physically and legally separated — and because that touches employee and customer PII, the separation plan has to address privacy handling, and you should redact PII before bidders see it. Dual-use IP — a patent family protecting both carved-out and retained products — gets resolved by assigning ownership to one side with a license-back or cross-license, so the IP schedule must state who owns what and who licenses what. And the employee perimeter (which headcount transfers, who is a key-person retention risk) is its own negotiation; a dual-role salesperson who sells across the whole parent portfolio is a classic gap. Because these documents are the most leak-sensitive in the room, I run screenshot protection and Screenshield screen-capture blocking (Data Room, $52/admin/month) on them, with dynamic watermarks (Data Room, $52/admin/month) stamping every page with the viewer's identity.

Datasite vs Intralinks — and is there a cheaper alternative for a mid-market carve-out?

For a banker-run mega-divestiture, Datasite or Intralinks are the defensible default; for an owner- or boutique-run mid-market carve-out, a flat-rate room does the same job for a fraction of the cost. Both Datasite and Intralinks are built for bank-led processes with service teams attached and price per deal, which commonly reaches the tens of thousands for a single process. Worth knowing as you compare 'alternatives': Datasite acquired Firmex in 2021 and Ansarada in 2024, so several names on the standard shortlist are one company. The flat-rate lane is where Peony sits: $52/admin/month on the Data Room plan, unlimited rooms and bidders, SOC 2 Type II certified, used by 6,800+ teams, live the same afternoon. Where Peony honestly loses: if you need walled per-bidder Q&A threads on a standard tier (that is an Enterprise feature on Peony, and Firmex's coordinator workflow is genuinely strong), or a vendor-staffed team to run a $1B-plus banker-led process for you. Match the room to who is running the process, not to the biggest logo.

I'm running a 9-month divestiture with several bidders — how much does the data room cost, and is flat-rate cheaper than per-page?

A few hundred dollars a month flat, versus five figures metered — and a divestiture is close to the worst-case shape for a meter. The process runs long (often 6 to 24 months once you include TSA negotiation), the document set is large (carve-out financials, contract-by-contract schedules, separation plans), and multiple bidders multiply access — and per-page, per-user, and per-GB models price every one of those variables in. Firmex typically lands around $5,000 to $10,000 per deal; Datasite and Intralinks commonly reach the tens of thousands for a single process; Ansarada's metered entry starts around $479/month ($244 on a 12-month term). Flat-rate removes the variables: Peony's Data Room plan is $52/admin/month (billed annually) with unlimited rooms, storage, and bidders, and the M&A-grade Deal Team plan is $64/admin/month — so two admins on the Data Room plan over a nine-month process spend roughly $940 total. Set against a separation budget that typically runs 1% to 5% of the divested unit's revenue, the room is a rounding error. The full math on why metering punishes long, document-heavy processes is in flat-rate vs per-GB pricing.

Is Datasite worth it for a single mid-market divestiture, or is a flat-rate room enough?

For a single mid-market carve-out you are running yourself, a flat-rate room is usually enough; pay for Datasite or Intralinks when a bank is running the process with a service team and the deal size justifies the meter. The enterprise platforms earn their cost on banker-led, $1B-plus processes with bespoke compliance workstreams and vendor staffing — that is a real, different product. But for a $50M to $500M division sale run by a corporate-development team or a boutique advisor, the job is a perimeter-tracking room with per-bidder walls, carve-out-financial staging, and watermark-everything at a predictable price — and metered billing actively works against you on a long, document-heavy carve-out. Peony's Data Room plan ($52/admin/month) covers granular per-file permissions, Advanced NDA, Screenshield, auto-indexing, and unlimited bidders; the Deal Team plan ($64/admin/month) adds Advanced redaction and the Advanced Q&A module for the consent and TSA workstreams. With 6,800+ teams on it and SOC 2 Type II certification, it clears the security bar a strategic buyer's diligence team will set.

Related reading

- Upstream oil and gas divestiture data room — the sector-specific sibling: a single E&P asset sale organized around reserves-disclosure tiering, where this post is the cross-industry corporate carve-out

- Best data room for multiple bidders — the One Room, Many Walls playbook for running parallel buyers

- The M&A data room guide — the generic folder tree this post extends with the separation layer

- Data room folder structure guide — the base layout to build the carve-out index on

- Due diligence data room checklist — the full diligence set that sits on top of the separation folders

- Investment banking data room — what changes when a bank runs the process

- Data room for strategic alternatives — when a divestiture is one option in a broader review

- Data room for a distressed asset sale and restructuring — when the separation happens under pressure

- How to structure an earnout — for the contingent value that often bridges a carve-out price gap

- How to set up a data room and how to prepare for due diligence — the readiness sprint before the room opens

- Flat-rate vs per-GB VDR pricing — why metered billing punishes long, document-heavy processes

Draw the boundary before a buyer draws it for you. Open a perimeter-tracking data room on Peony or see how visitor groups wall off each bidder.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 6,800+ teams across M&A, due diligence, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.