Data Room for Restructuring: Which Track Are You On? (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

I'm Sean Yu, co-founder of Peony, a data room platform used by 6,800+ teams across M&A, private equity, and fundraising. Before Peony I ran and supported sell-side and capital-raising processes on the deal side, and "restructuring" is the word I hear most often from companies that are genuinely unsure what they're walking into. Sometimes it means "we're reorganizing and quietly exploring a sale or a new investor." Sometimes it means "our lender is at the table and a §363 sale is on the horizon." Those are two very different situations — and they need two different data rooms.

This is the hub guide to the restructuring data room: what it is, how to tell which of the two tracks you're on, what goes in the room, how to protect your IP and engineering secrets when you have to disclose them at the moment of least leverage, and how to control access across buyers, lenders, and creditors. Where a track needs a deeper, step-by-step build, I link to the dedicated guide.

Quick answer: A restructuring data room is a permissioned, audit-logged room for sharing sensitive material — financials, contracts, cap table, and IP — with the counterparties involved in reorganizing or selling a business. The first decision is which track you're on: a strategic restructuring (exploring a sale, recapitalization, or new investor as a going concern, where you control disclosure) or a distressed restructuring (§363, Chapter 11, or a lender-driven workout, where a court or creditor timeline controls it). The room's mechanics are the same; the governance differs. Whichever track, the rules are constant: stage disclosure in tiers (keep IP and source code gated until a counterparty is serious), wall counterparties into groups (buyers, lenders, creditors each see only their set), watermark and lock down everything sensitive, and prefer flat-rate pricing because a large, months-long, many-party room is the worst case for metered billing. On Peony, per-group isolation starts on the Business plan ($30/admin/month); dynamic watermarking is on the Data Room plan ($52/admin/month), which is the anchor for a serious process.

What is a restructuring data room?

A restructuring data room is a secure, permissioned online room where a company organizes and selectively discloses its most sensitive information to the parties involved in reorganizing or selling the business — potential acquirers, new investors, lenders, creditors, and their advisors. It is the same core tool as an M&A data room or a fundraising data room, but it is used at a moment with a particular kind of pressure: the company often has to disclose a great deal, to people it may not fully trust, while it has less leverage than usual.

That pressure is the defining feature, and it has a name worth keeping in mind throughout this guide — the Disclosure-Under-Duress problem. In a healthy fundraise, you disclose from a position of strength and optionality. In a restructuring, you frequently disclose because you have to: a lender wants diligence, a board wants to test the market, a process is on a clock. The data room is the one part of that situation you can actually control — what goes in, who sees it, when, and whether they can take it with them. Treating the room as a control surface rather than a filing cabinet is the entire game.

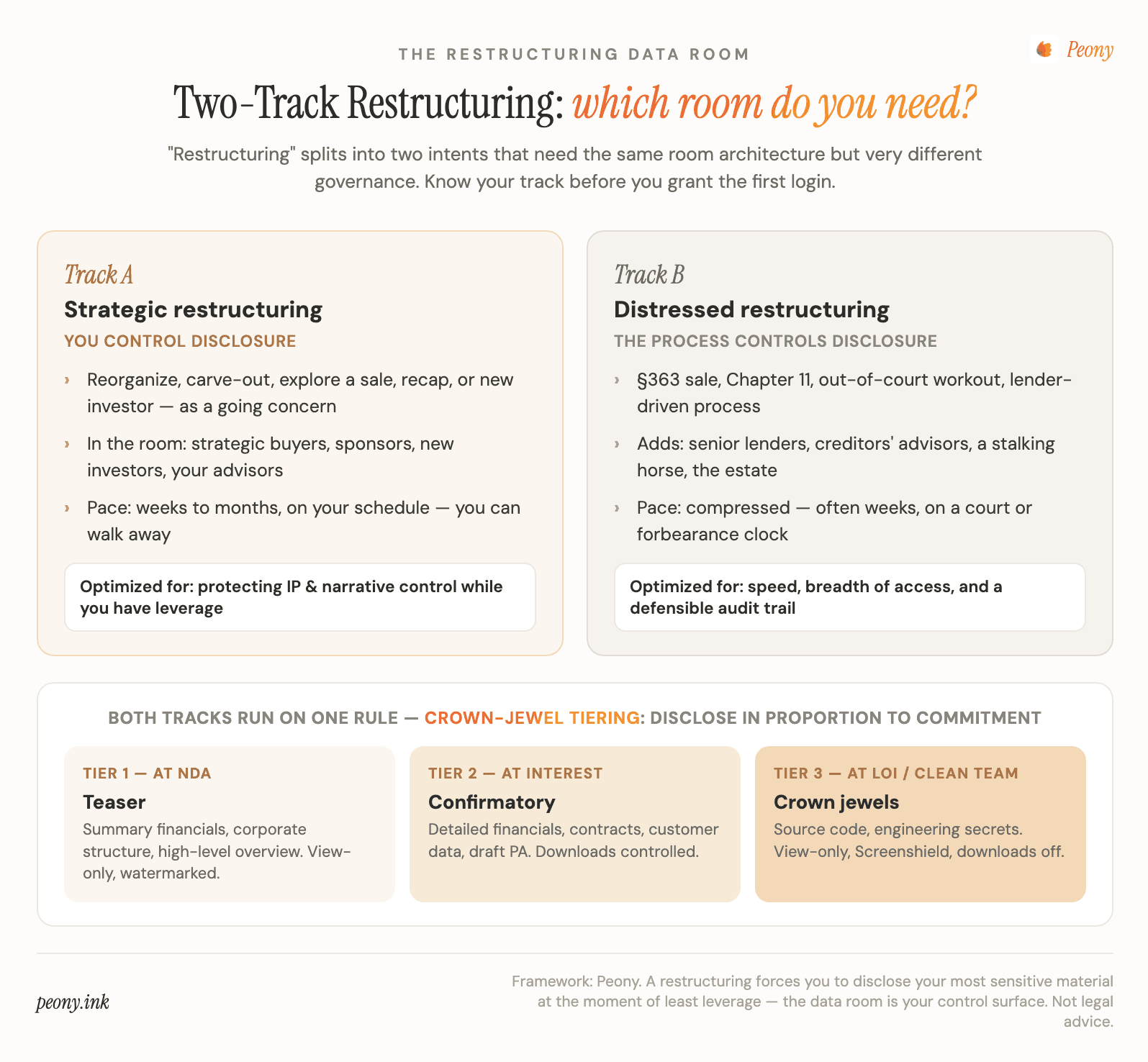

Which restructuring are you in — strategic or distressed?

Before you grant a single login, know which of two tracks you're on, because it changes who controls disclosure. This is the most important decision in the whole process, and it is the one most companies skip. I call it the Two-Track Restructuring model.

| Track A — Strategic restructuring | Track B — Distressed restructuring | |

|---|---|---|

| What it is | Reorganizing, carve-out, exploring a sale, recapitalization, or new investor — as a going concern | §363 sale, Chapter 11, out-of-court workout, lender-driven process |

| Who controls disclosure | You do — your timeline, your access decisions, you can walk away | A court, lender, or creditor committee — process and clock are externally driven |

| Who's in the room | Strategic buyers, financial sponsors, new investors, your advisors | Above, plus senior lenders, creditors' advisors, a stalking-horse bidder, the estate |

| Pace | Weeks to months, on your schedule | Compressed — often weeks, on a court or forbearance clock |

| Room optimized for | Protecting IP and narrative control while you have leverage | Speed, breadth of access, and a defensible, fully logged audit trail |

| Deeper guide | Data room for strategic alternatives | Data room for a distressed asset sale |

Most companies that describe themselves as "restructuring" start on Track A and want to stay there — explore alternatives, find a buyer or an investor, never touch a courtroom. Some slide toward Track B as a lender's patience runs out. The practical implication: build the room for Track A but in a way that survives a move to Track B. A well-organized, tiered, permissioned room is exactly what you want in either case; the difference is governance, not architecture. If you build it as a controllable room from day one, a pivot to a distressed process is a change in who you grant access to and how fast — not a frantic rebuild at the worst possible moment.

Why does restructuring make your data room different from a normal M&A room?

It's the same room doing a harder job, and three things change. First, leverage: you're often disclosing because you have to, not because you chose the moment, so the room has to let you control the pace of disclosure even when you can't control the pace of the process. Second, the cast: a normal sale process has buyers and advisors; a restructuring can add lenders, creditors, a creditors' committee, and their advisors — each with different information rights and different things they should and shouldn't see. Third, scrutiny: in a distressed process especially, the conduct of the sale can be challenged after the fact, so "who saw what, and when" stops being a convenience and becomes a legal record.

The implication is that a restructuring punishes the two shortcuts companies reach for under pressure. Emailing documents or dropping them in a shared drive — the Google Drive or Dropbox habit — gives you no per-party walls, no real revocation, and no defensible log. And a link-tracking deck tool built for sending a pitch is not built for a multi-party, IP-heavy diligence process; it's one of the most common reasons teams switch onto a real permissioned room when a restructuring gets serious. The room you'd casually use to share a deck is not the room you want when a competitor is across the table and a lender is reading over your shoulder.

What goes in a restructuring data room?

Build the index from the due-diligence checklist a buyer or lender will send you, before they send it. Pre-building the room is the single biggest thing you control, and it's the difference between looking organized and looking distressed. The core sections, roughly in the order diligence works through them:

- Corporate — formation documents, cap table, org chart, board and shareholder minutes, prior financing docs.

- Financials — audited statements and management accounts, monthly P&L, balance sheet, projections, debt schedule, and — for a distressed track — a 13-week cash-flow forecast.

- Commercial — top customer and supplier contracts, pipeline, retention/churn, concentration analysis.

- Legal & regulatory — material agreements, litigation, permits, compliance.

- IP & technology — patents, trademarks, domains, the IP assignment chain, and a separate engineering / source-code section that stays gated to the top disclosure tier.

- People — org chart, key employee and contractor agreements, compensation, retention plans.

- Liabilities & claims (distressed track) — debt documents, security/collateral, the creditor matrix, contingent claims.

The art is not the list — it's the permissioning. Build all of it once, then expose it in tiers (next section) so a Tier-1 visitor sees the teaser and summary financials while the source-code folder stays invisible until a counterparty reaches Tier 3. The step-by-step build differs by track; the strategic-alternatives guide covers the going-concern version and the distressed-asset-sale guide covers the §363/creditor version.

How do I protect IP and engineering secrets when I have to disclose them?

Tier your disclosure to commitment — never expose the crown jewels to a party that hasn't earned access. For an IP-heavy company, this is the whole ballgame, and the framework I use is Crown-Jewel Tiering: three tiers of disclosure, each unlocked by a higher level of counterparty commitment.

| Tier | Unlocked by | What's visible | Protection |

|---|---|---|---|

| 1 — Teaser | NDA accepted | Anonymized teaser, summary financials, corporate structure, high-level product overview | Watermarked, view-only |

| 2 — Confirmatory | Indication of interest / shortlist | Detailed financials, customer data, contracts, draft purchase agreement | Watermarked, downloads controlled |

| 3 — Crown jewels | Signed LOI / exclusivity / clean team | Source code, engineering specs, key trade secrets, sensitive customer & employee detail | View-only, Screenshield, downloads off |

The principle is that a counterparty sees your most sensitive IP only after it has demonstrated real commitment — a signed LOI, exclusivity, or a clean-team arrangement that walls the review off from the bidder's operating staff. A competitor running a fishing expedition stalls at Tier 1 or 2 and never reaches the engineering folder. And everything that does load on Tier 3 loads view-only, with per-viewer dynamic watermarks (every page stamped with the viewer's email, IP, and timestamp), download prevention, and screen-capture blocking, so anything seen is hard to take and trivial to trace.

On Peony, screenshot protection and download prevention are on the Business plan ($30/admin/month); dynamic watermarks, Screenshield (advanced screen-capture and screen-recording blocking), and granular per-file permissions are on the Data Room plan ($52/admin/month), the anchor tier for a serious process. No tool can stop a second phone pointed at the screen — but per-viewer watermarking turns a leaked page into a signed confession, which changes the incentive for anyone tempted to leak.

How do I control access across buyers, lenders, and creditors?

Use one room with a walled group per party type — not a pile of separate rooms, and not one shared folder. A restructuring often has more kinds of counterparty than a clean sale: strategic buyers, financial sponsors, senior lenders, a creditors' committee and its advisors. Each needs a different slice of the room. Lenders care about the debt schedule, collateral package, and cash flow; they rarely need your product roadmap. Buyers need the commercial and operating detail. Creditors' advisors need a defined, often narrower set.

The clean way to deliver that is a visitor group per party type — a named container you attach folder- and file-level permissions to, instead of permissioning people one by one. Each group sees only its set, signs its own NDA, gets its own tracked links, and carries its own audit trail; no group can see another's documents or members. This is the same "one room, many walls" architecture I describe in detail for competitive auctions in the multi-bidder guide — restructuring just adds lenders and creditors as additional walls. On Peony, per-group document and access isolation is a Business-plan capability; for fully walled, independent Q&A threads per group — where one party's questions are invisible to another even inside the room — that's an Enterprise capability. (A visitor group isolates documents and access; per-group Q&A-thread isolation is the higher tier. Be precise about which you're buying.)

How do I revoke access and prove what each party saw?

Revoke at the group level in one action, and keep the audit trail as your record. Restructurings end in lots of ways — a bidder drops out, a lender stands down, a process restarts under new advisors — and you need to cut off access cleanly every time. Because access is attached to a visitor group, disabling the group removes every user from that party at once, with no stray live links left behind. This is precisely what shared drives and "anyone with the link" tools can't do reliably, and it's a core reason teams move onto a permissioned room when a restructuring gets real.

The flip side of revocation is proof. A capable room timestamps every view, download, NDA acceptance, and Q&A exchange with user attribution, scoped per group. In a distressed process that audit trail is not optional housekeeping — it's how the conduct of the sale is defended if a creditor or a losing bidder later challenges it. Even in a friendly strategic process, being able to show a board exactly which parties engaged and how deeply is a real asset. Keep everything in the room (no side-channel email answers that never hit the log), and the record reconstructs itself.

How much does a restructuring data room cost?

Prefer flat-rate; a restructuring room is the worst-case shape for metered pricing. The variables a legacy VDR bills against — pages, gigabytes, users, months of access — all run high in a restructuring: years of financials and full contract sets make the room large, the process runs for months, and many counterparties need access. Per-page and per-GB models turn each of those into a line item, which is how an advertised entry price becomes an invoice several times larger by close. (I broke down the mechanics in flat-rate vs per-GB VDR pricing.)

| Platform | Pricing shape | Indicative cost for one restructuring |

|---|---|---|

| Peony — Data Room | Flat, per admin, unlimited storage + rooms | $52/admin/month (annual) |

| Peony — Deal Team (built for M&A) | Flat, per admin (min 4 admins) | $64/admin/month (annual) |

| Firmex | Per deal / per room | ~$5,000–10,000 per deal |

| Datasite | Per deal, usage-metered | tens of thousands per process |

| Intralinks | Per deal, usage-metered | tens of thousands per process |

The takeaway isn't "cheapest wins" — Datasite and Intralinks are powerful platforms that large-cap and high-profile bankruptcy processes use deliberately. It's that a cash-sensitive restructuring is the worst possible time to sign a contract whose bill grows with every document and every party you add. A flat per-admin room with unlimited storage gives you a price you can put in the budget and forget. And because you can own the room rather than rent it inside a bank's platform, your indexed room and audit trail stay portable assets if advisors or processes change.

Strategic or distressed — where should you go deeper?

It depends on which track you're on, and this hub covers what's common to both. The two tracks diverge enough in their build and process that each has its own guide:

- Data room for strategic alternatives — the going-concern playbook: running a quiet process to explore a sale, recapitalization, or new investor while protecting IP and controlling the narrative; the section-by-section build; and why teams move off link-tracking tools when the process gets serious.

- Data room for a distressed asset sale — the §363/creditor playbook: the compressed timeline, stalking-horse dynamics, creditor information rights, and the defensible-audit-trail requirements a distressed process adds on top.

Whichever track you're on, the architecture is the same: build the index once, tier your disclosure, wall counterparties into groups, lock down the crown jewels, and keep one audit trail per party. Get those right and the room does its job — letting you disclose what you must, to whom you choose, on terms you control, at the moment you have the least room for error. That's the difference between a restructuring you run and one that runs you.

Frequently asked questions

We're restructuring but haven't decided between a sale and a Chapter 11 — should I open the data room now or wait?

Open it now, but build it for the track you're most likely on and keep it private until you're ready to grant access. The work of organizing a clean, indexed data room — financials, contracts, cap table, IP schedule, org chart — is identical whether you end up in a strategic sale, a recapitalization, or a distressed process, and doing it early is the single biggest lever you have on speed and leverage. What changes by track is who controls disclosure and how fast counterparties arrive: a strategic process you run on your timeline, a distressed or §363 process compresses diligence into weeks on a court or lender clock. Build the room, stage the sensitive material behind permissions, and you can pivot from "exploring alternatives" to "running a sale" without rebuilding anything. Waiting until a lender demands diligence in two weeks is how companies hand over a disorganized room at the moment of least leverage.

What's actually different between a strategic-restructuring data room and a distressed (363) one?

The mechanics of the room are the same; what differs is who controls disclosure, who's in the room, and how fast it moves. In a strategic restructuring — exploring a sale, recapitalization, or new investor as a going concern — you control the process: you decide who gets in, what they see, and when, and you can walk away. The room optimizes for protecting IP and narrative control while you still have leverage. In a distressed or §363 process, control shifts to a court-supervised or lender-driven timeline: a stalking-horse bidder may get earlier or deeper access, creditors and their advisors have information rights, diligence compresses into weeks, and every access needs to be logged because the estate's conduct can be challenged. Same room, different governance — which is exactly why you should know which track you're on before you grant the first login.

Is it safe to put our source code and engineering secrets in a data room while we're restructuring?

Yes, if the room controls disclosure rather than just storing files — and if you tier what you expose. A capable data room lets you keep source code, engineering documentation, and trade secrets out of the room entirely until a counterparty is serious, then expose them view-only with per-viewer watermarks, download prevention, and screen-capture blocking so anything shown carries the viewer's identity. The mistake is treating restructuring disclosure as all-or-nothing — dumping everything into a shared folder on day one. Stage your crown jewels: keep the most sensitive material gated until a signed LOI or a clean-team arrangement, and disclose the rest in tiers. On Peony, screenshot protection and download prevention are on the Business plan; per-viewer dynamic watermarks and Screenshield (advanced screen-capture/recording blocking) are on the Data Room plan. No tool stops a phone camera, but watermarking turns a leaked page into a signed confession that names the leaker.

How do I stage disclosure so bidders don't see our IP until they're serious?

Map disclosure to commitment using a tiered permission ladder — what I call Crown-Jewel Tiering. Tier 1 (open at first access, NDA-gated): the teaser, summary financials, corporate structure, high-level product overview. Tier 2 (unlocked at indication of interest or shortlist): detailed financials, customer data, contracts, the draft purchase agreement. Tier 3 (gated to a signed LOI, exclusivity, or a clean team): source code, engineering specs, key trade secrets, sensitive customer and employee detail. Each tier is a set of folder permissions you expand for a counterparty as it advances, never a separate room. The crown jewels — the IP that makes a competitor want to mine your room and walk — live on Tier 3 and only ever load view-only, watermarked, with downloads off. You disclose enough to move a deal forward at each stage, and no more.

What if a competitor is one of the bidders — how do I stop them from mining our IP and walking?

Assume any bidder might be a tire-kicker or a competitor on a fishing expedition, and design the room so the cost of looking never exceeds the value of what they can take. Three layers do this. First, gate the crown jewels: keep source code and core IP on the top disclosure tier, released only after a signed LOI or into a clean team — a competitor that won't commit never sees them. Second, make everything they do see view-only with per-viewer watermarks (email, IP, timestamp on every page), download prevention, and screen-capture blocking, so exfiltration is hard and attribution is automatic. Third, watch the audit trail: a "bidder" that downloads nothing, asks no commercial questions, but pages repeatedly through your engineering folder is showing you what it actually wants. You can't make diligence risk-free, but you can make the room expensive to abuse and easy to trace.

Should I run one data room for buyers, lenders, and creditors, or set up separate ones?

Run one room with walled groups, not separate rooms — with one exception. A single room with a visitor group per party type (strategic buyers, financial buyers, senior lenders, creditors' advisors) lets each group see only what it's entitled to, sign its own NDA, and carry its own audit trail, while you maintain one master index and one Q&A queue. Lenders typically need financials, the cap table, and the collateral package but not your product roadmap; buyers need the operating and commercial detail; creditors' advisors need a defined disclosure set. Group-based permissions deliver all of that in one room. The one case for a genuinely separate room is when you need fully walled, independent Q&A threads per group on a plan that doesn't include them — on Peony, per-group document and access isolation is a Business-plan capability, while fully walled per-group Q&A channels are an Enterprise capability.

If a bidder or lender drops out, how do I cut off their access and prove they can't still get in?

Revoke at the group level and keep the log. Because access attaches to a visitor group rather than to scattered individual links, disabling the group cuts off every user from that party in one action — no per-file cleanup, no stray live link. Retain the group's audit trail after revocation: in a restructuring that may later be scrutinized by creditors, a court, or a disappointed bidder, being able to show exactly what a party accessed and that its access was cleanly terminated is part of running a defensible process. The failure mode to avoid is the consumer-cloud pattern — an "anyone with the link" share you can't truly recall — which is one of the main reasons restructuring teams move off link-tracking tools and shared drives onto a permissioned room.

How do I set up a restructuring data room, and what documents actually go in it?

Start from the diligence checklist a buyer or lender will send and pre-build the index so you're never reacting. The core sections: (1) Corporate — formation docs, cap table, org chart, board minutes; (2) Financials — audited and management accounts, monthly P&L, projections, debt schedule, and (for distressed) a 13-week cash flow; (3) Commercial — top customer and supplier contracts, pipeline, churn; (4) Legal — material agreements, litigation, regulatory; (5) IP & Technology — patents, trademarks, the IP assignment chain, and an engineering/source-code section you keep gated to the top tier; (6) People — org chart, key employee agreements, comp; (7) for distressed, a Liabilities & Claims section. Build it once, permission it in tiers, and you can serve a strategic buyer, a new investor, or a lender from the same room. The full section-by-section build differs by track — see the strategic-alternatives and distressed guides linked above.

Can a counterparty screenshot or download our files, and can I see exactly who viewed what?

On a capable room, you control downloading and capture, and you see everything. Set documents to view-only to disable downloads, apply per-viewer dynamic watermarks so any screen that is photographed carries the viewer's email and IP, and enable screen-capture blocking on the most sensitive material. For visibility, the room timestamps every view, download, NDA acceptance, and Q&A exchange with user attribution, so you can see which lender actually opened the debt schedule and which "bidder" spent an hour in the engineering folder. On Peony, view-only, download prevention, and screenshot protection are on the Business plan; dynamic watermarks, Screenshield (advanced capture/recording blocking), and granular per-file permissions are on the Data Room plan. No software stops a second phone pointed at the screen — which is why per-viewer watermarking matters: it makes the leak traceable even when you can't prevent it.

How much does a data room cost for a restructuring, and is flat-rate better than per-page?

For a restructuring, prefer flat-rate — per-page and per-GB pricing punish exactly the shape of a restructuring data room. A restructuring room tends to be large (years of financials, full contract sets, engineering documentation), open for months, and accessed by many counterparties — every variable a metered VDR bills against. Legacy providers that charge per page or per GB can turn an advertised entry price into an invoice several times larger by close. Flat-rate platforms remove that risk: Peony's Data Room plan is $52/admin/month billed annually with unlimited storage, unlimited rooms, and no per-page metering; the M&A-focused Deal Team plan is $64/admin/month. Compare that to Datasite or Intralinks in the tens of thousands per process, or Firmex at roughly $5,000–10,000 per deal. The point isn't "cheapest wins" — it's that a cash-sensitive restructuring is the worst possible time to sign a metered contract whose bill grows with every document and every party you add.

Should I control the data room myself or let our banker or restructuring advisor run it?

Own the room; let your advisor operate inside it. Your banker or chief restructuring officer should absolutely run the day-to-day — managing the index, fielding Q&A, advancing bidders — but the room should sit on an account the company controls, not be locked inside an advisor's or bank's platform you lose when the engagement ends. The reason is continuity and leverage: restructurings change advisors, processes restart, and you want your indexed room, audit trail, and document set to be portable assets you keep, not something you rebuild when a mandate turns over. A flat-rate room you own and grant your advisor admin access to gives you the best of both — professional operation without vendor lock-in or a per-deal bill from the bank's data room.

Related reading

- Data room for strategic alternatives — the going-concern playbook for exploring a sale or recapitalization while protecting IP

- Data room for a distressed asset sale — the §363 / creditor-led playbook and its defensibility requirements

- Best data room for multiple bidders — one room, many walls: isolating competing parties in a single room

- The M&A data room guide — folder structure, staging, and Q&A in context

- How to prepare for due diligence — room setup, team assembly, and turnaround

- Flat-rate vs per-GB VDR pricing — why metered billing punishes large, long, many-party rooms

- Virtual data room vs Google Drive — why shared drives fail a multi-party diligence process

Run your restructuring in a room you control — with per-party walls, tiered disclosure, and a flat price you can budget. See the restructuring data room solution, how visitor groups work, or set up your data room.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 6,800+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.

You might also like

Jun 11, 2026

Distressed Asset Sale Data Room: Speed, Control, Defensibility (2026)

Jun 11, 2026

Data Room for Strategic Alternatives: Sell Without Giving It Away (2026)

Jul 22, 2026

Imaging Center M&A Data Room: Selling a Radiology Group in the Roll-Up Wave (2026)