Distressed Asset Sale Data Room: Speed, Control, Defensibility (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

I'm Sean Yu, co-founder of Peony, a data room platform used by 6,800+ teams across M&A, private equity, and restructuring. Before Peony I worked on the deal side, and distressed processes are the ones where the data room stops being a convenience and becomes part of the legal record. A §363 sale or a creditor-driven workout asks the room to do two things that pull in opposite directions — move fast and never lose control — while producing a record that can withstand a challenge in open court.

This guide is the operator's view of a distressed asset sale data room: how to onboard many bidders on a compressed timeline without losing control, how to handle stalking-horse asymmetry and creditor information rights, and how to build the kind of defensible audit trail a sale hearing rewards. It's the distressed track of our restructuring data room hub; if you're a going concern quietly exploring a sale instead, the strategic-alternatives guide is the one you want. One caveat throughout: I'm describing data-room mechanics, not giving legal advice — your counsel owns the legal standard for your case.

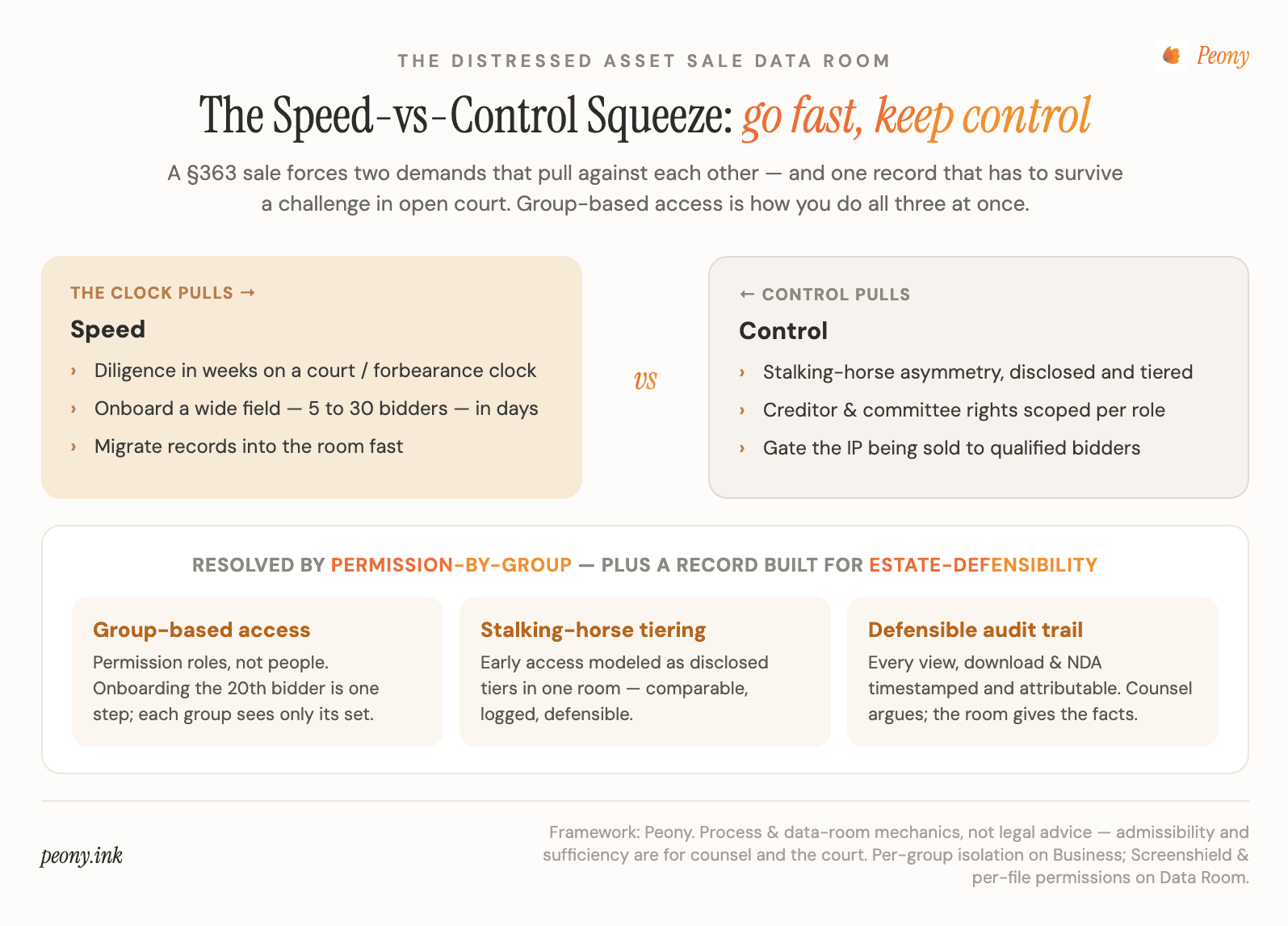

Quick answer: A distressed asset sale data room has to resolve the Speed-vs-Control Squeeze — onboard a wide field of bidders in days on a court or forbearance clock, without losing control of who sees what, and while producing a defensible record. The playbook: pre-build the index and permission by visitor group (qualified bidders, stalking horse, secured lenders, creditors' committee) so onboarding the 20th bidder is one step; gate the sensitive IP being sold to qualified bidders under view-only, watermarked terms; model stalking-horse asymmetry as disclosed permission tiers in one room rather than a privileged separate room; and keep everything in the room so the audit trail is complete, attributable, and exportable for the sale hearing. For a cash-constrained estate, flat-rate pricing beats per-page or per-GB — an unknown bidder count and document size are exactly what metered billing punishes. On Peony, per-group isolation and NDA gating start on the Business plan ($30/admin/month); the Data Room plan ($52/admin/month) adds Screenshield, granular per-file permissions, and unlimited rooms.

What is a distressed asset sale data room?

A distressed asset sale data room is the secure, permissioned environment used to market and run diligence on a company or its assets in a distressed process — most commonly a sale under §363 of the U.S. Bankruptcy Code (a court-supervised sale, typically by auction), but also a Chapter 11 plan sale, an out-of-court workout with a secured lender, or an Assignment for the Benefit of Creditors (ABC). It's the same core tool as any M&A data room, used under a particular set of pressures: a compressed timeline, a wider and sometimes less-vetted bidder field, multiple constituencies with information rights, and the knowledge that the conduct of the sale can be examined and objected to before a judge approves it.

That last point is what makes a distressed room different from a healthy one. In a normal sale, your audit trail is good housekeeping. In a distressed sale, it's potential evidence: when the court is asked to approve the winning bid, the record of how the assets were marketed and how bidders were given access supports the finding that the sale was fair and the price was the best available. The room isn't just where diligence happens — it's where the defensibility of the whole process is built or lost.

How do I run a distressed sale on a compressed timeline without losing control?

Resolve the Speed-vs-Control Squeeze with group-based access — it's the one mechanism that lets you go fast and stay in control at once. A §363 process can run on a timeline of weeks, and you may need to take a bidder field from zero to twenty in a matter of days. Provisioning each login by hand, deciding folder by folder what each new bidder sees, is how you either move too slowly or make a mistake that hands someone access they shouldn't have. The fix is to do the thinking once, at the group level:

- Pre-build the index from a diligence checklist before the first bidder arrives, so you're never reacting under clock pressure.

- Create visitor groups by role — qualified bidders, the stalking horse, secured lenders, the creditors' committee — and attach folder- and file-level permissions to the group, not to individuals.

- Gate entry with an NDA each party accepts on the way in, logged automatically to its group's record.

- Onboard into the group. Adding the 18th qualified bidder becomes a one-step action: drop them in, and they inherit exactly the right view, with their NDA acceptance already on the record.

Now the room scales to a crowd without a corresponding spike in your workload or your error rate. You're permissioning roles, not people — which is the only way to onboard a wide field fast while keeping a clean, explainable access map you can show the court.

How do I handle the stalking horse without creating a fairness problem?

Model stalking-horse asymmetry as disclosed permission tiers inside one room — not as a privileged separate room. The stalking horse is the initial bidder that agrees to a baseline offer, sets the floor for the auction, and typically negotiates court-approved bid protections (such as a break-up fee or expense reimbursement) for taking that risk. It often gets earlier, and sometimes deeper, diligence access because it's doing the work to anchor the process. That asymmetry is Stalking-Horse Asymmetry, and it's legitimate — provided it's disclosed and the qualified bidders who follow get fair access to the same core diligence.

The way to keep it defensible is to make it explicit and logged. Put the stalking horse in its own visitor group with early access to the full diligence set. When the bid procedures are approved and the auction opens, create a qualified-bidder group and grant it access to the same core material. Everyone is in one room; each group's access is a documented permission set; and you can show, precisely, what the stalking horse saw and when versus the field. Running this as tiers in a single room — rather than giving the stalking horse a separate, privileged room you can't easily compare against the others — is itself part of what makes the asymmetry survivable if the creditors' committee questions it.

How do I manage creditor and committee information rights?

Give each constituency its own group, scoped to its role. A distressed process has stakeholders a clean sale doesn't: the unsecured creditors' committee, secured lenders and their advisors, and sometimes other parties in interest, each with legitimate information needs that are not the same as a bidder's. The committee generally needs broad visibility into financials, the marketing process, the proposed transaction, and claims and collateral — but it's not bidding, so it doesn't need a competing bidder's marked-up purchase agreement. Secured lenders need the collateral and financial picture. Bidders need the diligence set.

A visitor group per stakeholder type makes this clean and, importantly, explainable: the committee sees its scoped set, lenders see theirs, bidders see the diligence set, and no group sees another's documents or members. That role-based scoping serves two ends at once — it gives each constituency the access it's entitled to, and it lets you demonstrate to the court that access was appropriate to each party's role rather than ad hoc. The precise scope of committee access is a matter for counsel and the facts of the case; the room's job is to make per-group scoping trivial to set up and trivial to prove.

How do I protect the IP being sold during the auction?

Tier disclosure even when the IP is the asset — the crown jewels go to qualified bidders only, view-only and watermarked. It's tempting to think that because the assets (including IP) are what's being sold, you should just open everything. Don't. The risk that a competitor enters the bidder field to harvest source code, trade secrets, or customer data without seriously intending to buy is, if anything, higher in a distressed sale, where the field is wider and the timeline leaves less room to vet everyone.

So gate it: broad diligence — financials, contracts, asset schedules, the marketing materials — available to all qualified bidders; the most sensitive technical and customer detail held back for bidders that have cleared qualification or advanced to a later round, and reviewed view-only with downloads off, per-viewer dynamic watermarks on every page, and screen-capture blocking engaged. The watermark matters because it makes any leaked page traceable to the specific bidder who saw it. You're still selling the IP — but you're controlling the sequence and the terms under which a prospective buyer examines it, which is exactly the control a fire-sale timeline tends to erode if you don't build it into the room up front.

How do I build a defensible audit trail?

Keep everything in the room and export the per-user, per-group log. The defensibility of a distressed sale rests on being able to answer one question precisely: what could each party access, and when? A capable room timestamps every view, download, NDA acceptance, and Q&A exchange, each attributed to a named user, with document and folder access scoped per visitor group. Exported, that's a complete, attributable record supporting the declaration that the assets were broadly and fairly marketed and that qualified bidders had equal access to the same diligence.

Two disciplines make the record airtight. First, keep all diligence in the room — every answer to a bidder question goes through the room's Q&A, not a side-channel email that never hits the log, because a record with holes invites exactly the argument you're trying to prevent. Second, write your access rules into the bid procedures so the documented process matches the actual process. This is the Estate-Defensibility principle: in a distressed sale, the audit trail isn't housekeeping, it's part of the evidentiary basis for the sale order. Whether a particular log is admissible and sufficient is for your counsel and the court to determine — your job is to ensure the record is complete, attributable, and exportable, which a real room delivers and a shared drive cannot.

What should a distressed sale data room cost?

Far less than a legacy VDR, and on a flat plan you control rather than a per-deal meter. For a cash-constrained estate, the economics matter, and the legacy enterprise VDRs are the wrong shape: Datasite and Intralinks commonly run into the tens of thousands for a single process and bill on usage — pages, gigabytes, users — which is punishing when the document set is large and the bidder count is unknown.

| Platform | Pricing shape | Indicative cost for one distressed process |

|---|---|---|

| Peony — Data Room | Flat, per admin, unlimited storage + rooms | $52/admin/month, flat |

| Peony — Deal Team (built for M&A) | Flat, per admin (min 4 admins) | $64/admin/month (annual) |

| Firmex | Per deal / per room | ~$5,000–10,000 per deal |

| Datasite | Per deal, usage-metered | tens of thousands per process |

| Intralinks | Per deal, usage-metered | tens of thousands per process |

The case for flat-rate here is the unknown bidder count. You often don't know whether five or thirty bidders will show up, how large the records will grow, or how long a contested auction will run — and every one of those unknowns is a variable that per-page, per-GB, and per-user models bill against. Flat per-admin pricing fixes the cost regardless, so the estate can budget a known number and the process can scale without re-opening the line item. If you genuinely need short-term flexibility, a monthly plan exists; for most processes the annual flat plan is both cheaper and simpler. Whether the room is treated as an administrative expense is a question for counsel — but the spend itself is modest against the stakes of the sale.

Putting it together

A distressed asset sale asks the room to do the hardest version of the job: onboard a wide field fast, keep tight control of who sees what, protect the IP you're selling, and produce a record that survives scrutiny — all on a clock you don't control. The mechanics that deliver it are consistent: pre-build the index, permission by group, gate the crown jewels to qualified bidders, model stalking-horse asymmetry as disclosed tiers in one room, scope each constituency's access to its role, and keep everything in the room so the audit trail is complete. Get those right and the room does what a distressed process most needs — it lets you move at the speed of the deadline without sacrificing the control and the record the sale order depends on.

For the cross-track view — strategic versus distressed, and how to tell which one you're in — start with the restructuring data room hub. And remember the division of labor: counsel argues the case; the room gives counsel the facts.

Frequently asked questions

Our 363 sale closes in weeks — should I stand up a real VDR or just use Dropbox to save the estate money?

Use a real, permissioned data room — the money you'd save on Dropbox is trivial against the risk of a sale objection. A distressed sale is the one process where the conduct of the marketing and diligence can be challenged in open court: a losing bidder or the creditors' committee can argue the process wasn't fair or wasn't adequately marketed. A shared drive gives you no per-bidder walls, no clean revocation, and — critically — no attributable, exportable log of who could access what and when. A purpose-built room gives you all three, plus fast bidder onboarding. The cost of a flat-rate room is a rounding error in a §363 budget; the cost of a process objection that delays or unwinds your sale is not. This is process infrastructure, not a place to economize. (Always confirm the approach with your counsel — they own the legal standard.)

How do I set up a distressed-sale data room on a compressed timeline and onboard 20 bidders fast without losing control?

Pre-build the index, permission by group, and use NDA-gated self-onboarding so bidders provision themselves. The squeeze in a distressed sale is that you have to move fast and keep control at the same time — and group-based access is what lets you do both. Build the folder index once from a diligence checklist; create visitor groups (qualified bidders, the stalking horse, secured lenders, the creditors' committee); attach folder- and file-level permissions to each group, not to individuals; and gate entry behind an NDA each bidder accepts on the way in, logged automatically. Now adding the 18th bidder is a one-step action — drop them into the qualified-bidder group and they inherit the right view instantly, with their NDA acceptance on the record. You onboard a crowd in hours instead of provisioning each login by hand, and you never lose track of who can see what.

How do I produce a defensible audit trail of who accessed what for the sale hearing?

Keep everything in the room and export the per-user log. A capable data room timestamps every document view, download, NDA acceptance, and Q&A exchange, each attributed to a named user, with document and folder access scoped per visitor group. Exported, that's a complete record of exactly what each bidder could access and when — which is what supports a declaration that the assets were broadly and fairly marketed and that every qualified bidder had equal access to the same diligence. The two disciplines that make it airtight: keep all diligence in the room (no side-channel email answers that never hit the log), and write your access rules into the bid procedures so the record matches the stated process. Whether a given log is admissible and sufficient is a question for your counsel and the court — your job is to make sure the record is complete, attributable, and exportable, which a real room does and a shared drive does not.

What if a losing bidder claims it didn't get equal access — can the data room log prove otherwise?

A complete, per-bidder audit trail is your strongest factual answer to exactly that claim. When a losing bidder alleges it was disadvantaged, the question becomes evidentiary: what could each bidder access, and when? If every bidder sat in a visitor group with the same permission set and the room logged each group's views, downloads, and NDA acceptances, you can show — bidder by bidder — that access was equal and that material answers were published to all qualified bidders. That converts an emotional allegation into a documented comparison. The failure mode is running the process over scattered emails and shared links, where you can't reconstruct who saw what; then the allegation is hard to rebut. Keep the process in one room with group-level isolation and a full log, and equal-access disputes are answered with a record, not an argument. (Your counsel decides how to present it.)

How do I give the stalking horse early access, then open the room to qualified bidders, in one room?

Model it as permission tiers inside a single room, not as separate rooms. The stalking horse typically gets earlier and sometimes deeper diligence access — it's doing the work to set the floor and has negotiated bid protections — and that asymmetry is legitimate as long as it's disclosed and the eventual qualified bidders get fair access to the same material. Operationally: put the stalking horse in its own group with early access to the full diligence set; when the bid procedures are approved and you open the auction, create a qualified-bidder group and grant it access to the same core material. Everyone is in one room, each group's access is explicit and logged, and you can show the court precisely what the stalking horse saw versus the field. Managing this as tiers in one room — rather than a privileged separate room — is also what keeps the asymmetry defensible.

Should the creditors' committee get the same access as bidders, or a separate restricted view?

Give the committee its own group with a view scoped to its information rights — usually broad on financial and process information, but not necessarily identical to a bidder's. The unsecured creditors' committee and secured lenders have legitimate information needs, but they're not bidders, so their view should be defined for their role: financials, the marketing process, the proposed transaction, claims and collateral — rather than, say, a competing bidder's markup of the purchase agreement. A visitor group per stakeholder type makes this clean: the committee sees its set, secured lenders see theirs, bidders see the diligence set, and no group sees another's documents or members. This also keeps the record tidy for the court — you can show that each constituency got the access appropriate to its role. The exact scope of committee access is a matter for counsel and the case; the room just needs to make per-group scoping easy.

How do I gate the sensitive IP and source code being sold until a bidder is qualified?

Keep the crown jewels on a higher disclosure tier, released only to qualified bidders under view-only, watermarked terms. Even in a distressed sale where the assets — including IP — are what's being sold, you don't expose source code, key trade secrets, or sensitive customer data to every party that signs an NDA on day one. Tier it: broad diligence (financials, contracts, asset schedules) for all qualified bidders; the most sensitive technical and customer detail gated to bidders that have cleared qualification or reached a later round, and ideally reviewed view-only with downloads off, per-viewer dynamic watermarks, and screen-capture blocking. The risk is the same as in any sale — a competitor posing as a bidder to harvest IP — but in distress the bidder field is often wider and the timeline tighter, so the gating has to be built into the room's permissions from the start, not improvised mid-auction.

How do I revoke a losing bidder's access after the auction — and keep the record?

Revoke at the group level in one action, and retain the audit trail. Once the auction closes and the winning bid is selected, the other bidders' access should end cleanly — and because access is attached to a visitor group rather than to scattered individual links, disabling the group cuts off every user from that bidder at once, with no stray live link. Crucially, you keep the group's historical audit trail after revocation: in a process that may face a sale objection or later scrutiny, being able to show what each losing bidder accessed, and that its access was terminated at the right point, is part of a defensible record. The pattern to avoid is the shared-drive or open-link approach where access can't be reliably withdrawn and the historical record is incomplete.

How much does a data room cost for a 363 sale, and is there a month-to-month option for a cash-constrained estate?

Expect to pay far less than a legacy VDR, and prefer a flat plan you control over a per-deal metered contract. The enterprise VDRs (Datasite, Intralinks) commonly run into the tens of thousands for a single process and bill on usage — pages, gigabytes, users — which is painful for a cash-constrained estate with a large document set and many bidders. A flat-rate room removes the metering: Peony's Data Room plan is $52/admin/month, and month-to-month billing is available if you need short-term flexibility for a brief process, with unlimited storage and rooms and no per-page or per-bidder fees. For an estate, the appeal is predictability — the bill doesn't grow as you add the 20th bidder or upload another gigabyte of records. Whether a data room is treated as an administrative expense of the estate is a question for counsel, but the cost itself is modest relative to the process.

Is per-page or flat-rate pricing better for a distressed sale with an unknown bidder count?

Flat-rate, decisively — an unknown bidder count is the exact scenario per-unit pricing punishes. In a distressed sale you often don't know up front whether you'll have 5 bidders or 30, how large the document set will grow, or how long the process will run if the auction is contested. Every one of those unknowns is a variable that per-page, per-GB, and per-user models bill against, so your cost is unpredictable precisely when the estate can least afford a surprise. Flat per-admin pricing fixes the cost regardless of how many bidders show up or how big the room gets — you can put a known number in the budget and the sale process can scale without re-opening the line item. For a process whose shape is uncertain by nature, removing the metering is worth more than shaving a few dollars off a base rate.

Will a cheap data room hold up if the UCC objects that the process favored the stalking horse?

What holds up isn't the price of the room — it's whether the room produced a complete, attributable record and enforced the access rules you told the court you'd follow. A creditors' committee objecting that the process favored the stalking horse is making a fairness argument, and your answer is evidentiary: show that qualified bidders sat in a group with equal access to the same diligence set, that the stalking horse's earlier or deeper access was disclosed and consistent with its role, and that the log proves who accessed what and when. A capable but affordable room can do all of that; an expensive one with sloppy process discipline can't. So the question to ask of any room isn't 'is it cheap or premium' but 'does it give me per-group isolation, NDA gating, and a full exportable audit trail' — and then run a disciplined process inside it. Counsel argues the objection; the room gives counsel the facts.

Related reading

- Medical equipment sale data room — the dossier-driven disposition of high-value imaging equipment: PHI sanitization, buyer qualification, and the service-history file that sets price

- Data room for restructuring (hub) — strategic vs distressed, and which track you're on

- Data room for strategic alternatives — the going-concern track for exploring a sale or recap

- Best data room for multiple bidders — one room, many walls: isolating competing bidders

- Investment banking data room: the sell-side playbook — staged bidder access and process mechanics

- Data room Q&A: the moderated workflow — keeping the diligence record complete and on-the-record

- Flat-rate vs per-GB VDR pricing — why metered billing punishes a large, many-bidder process

- How to prepare for due diligence — room setup and turnaround under deadline

Run your distressed sale in a room built for speed, control, and a record that holds up. See the restructuring data room solution, start free on Peony, or see how visitor groups work.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 6,800+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.

You might also like

Jun 11, 2026

Data Room for Restructuring: Which Track Are You On? (2026)

Jul 22, 2026

Imaging Center M&A Data Room: Selling a Radiology Group in the Roll-Up Wave (2026)

Jul 16, 2026

Best Data Room Providers UK (2026): An Honest Buyer's Guide