Data Room for a Sports Team Minority-Stake Sale (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

I'm Sean Yu, co-founder of Peony, a data room platform used by 6,800+ teams across M&A, private equity, and fundraising. Before Peony I worked on sell-side and growth processes at Nomura, Backed VC, and Target Global — and the sale process I'd least like to run over email is the one this guide covers: selling a minority stake in a professional sports team.

Here's why this post exists now. In February 2026, KKR agreed to acquire Arctos Partners — the largest institutional investor in pro sports, with roughly $15 billion under management and stakes in 30+ teams — in a deal initially valued at $1.4 billion. The NFL approved seven minority-stake transactions in the twelve months from December 2024, when its first private-equity deals cleared — Arctos, Ares, and Sixth Street all hold NFL stakes today. The NBA just raised the number of teams a single fund can hold from five to eight (effective December 3, 2025). Institutional capital buying into sports is no longer a trend story; it's a transaction pipeline. What nobody writes about is the unglamorous middle of every one of those deals: a franchise that has never produced institutional-grade diligence, opening its stadium lease, media contracts, and payroll to professional skeptics, in the single most leak-sensitive M&A environment that exists.

Quick answer: A sports team minority-stake sale runs through what I call the League-Approval Gate: unlike normal M&A, your buyer universe is pre-cleared by the league (caps, vetting, and an owners' vote — 24 of 32 in the NFL), so you run a quiet, parallel process with a handful of named buyers rather than a broad auction. The data room has three jobs: isolate each buyer in its own walled view (visitor groups with separate NDAs, documents, and audit trails), weight toward contracts (stadium lease, media rights, sponsorships — what scarcity-priced franchises are actually underwritten on), and make every page traceable (per-viewer watermarks, screenshot blocking, page-level analytics) because a leak hits fans, agents, and your stadium politics — not just price. On Peony, per-buyer isolation and NDA gates start on the Business plan ($30/admin/month); dynamic watermarks are on the Data Room plan ($52/admin/month), the anchor for a real stake-sale process, and fully walled per-buyer Q&A channels are on Enterprise.

Why is institutional money suddenly buying into sports teams?

Because the leagues opened the door, and the sellers need it open. MLB allowed fund investment in 2019, the NHL and a broadened NBA framework followed in 2021, and the NFL — the last and most reluctant — approved private equity up to 10% per team in August 2024. The first NFL deals cleared on December 11, 2024: Ares took 10% of the Miami Dolphins at an $8.1 billion valuation, and Arctos took 10% of the Buffalo Bills at $5.6 billion. Within a year the league had approved seven minority transactions, including Arctos' 8% of the Chargers (May 2025), the Bears' 2.3% estate sale at a then-record ~$8.9 billion (September 2025), the Giants' 10% to Julia Koch at $10.3 billion (October 2025), and Sixth Street's piece of an 8% Patriots sale at a $9 billion-plus valuation (closed November 11, 2025).

The demand side is structural. Franchise values have outrun every owner's balance sheet — Sportico's 2025 set puts the average NFL team at $7.13 billion, up 20% year over year, with the Cowboys at $12.8 billion [as of August 2025] — while the average controlling owner is in their seventies. Estate taxes, stadium capex, and legacy limited partners who've waited decades for liquidity all want the same thing: a way to convert a slice of paper wealth into cash without selling control. That's precisely the product the league rules created: passive, capped, non-voting institutional capital. And the supply side just institutionalized itself — KKR's February 2026 acquisition of Arctos puts a sports-stake specialist inside one of the world's largest alternative-asset managers, with stated ambitions to scale the platform far beyond its current size.

One thing the market commentary doesn't tell you (Datasite published a solid "institutionalization of sports" piece this month — entirely about why capital is coming, nothing about how a sale actually runs): every one of those transactions was, operationally, a diligence exercise run by a franchise that had probably never been through one. That's the part this guide covers.

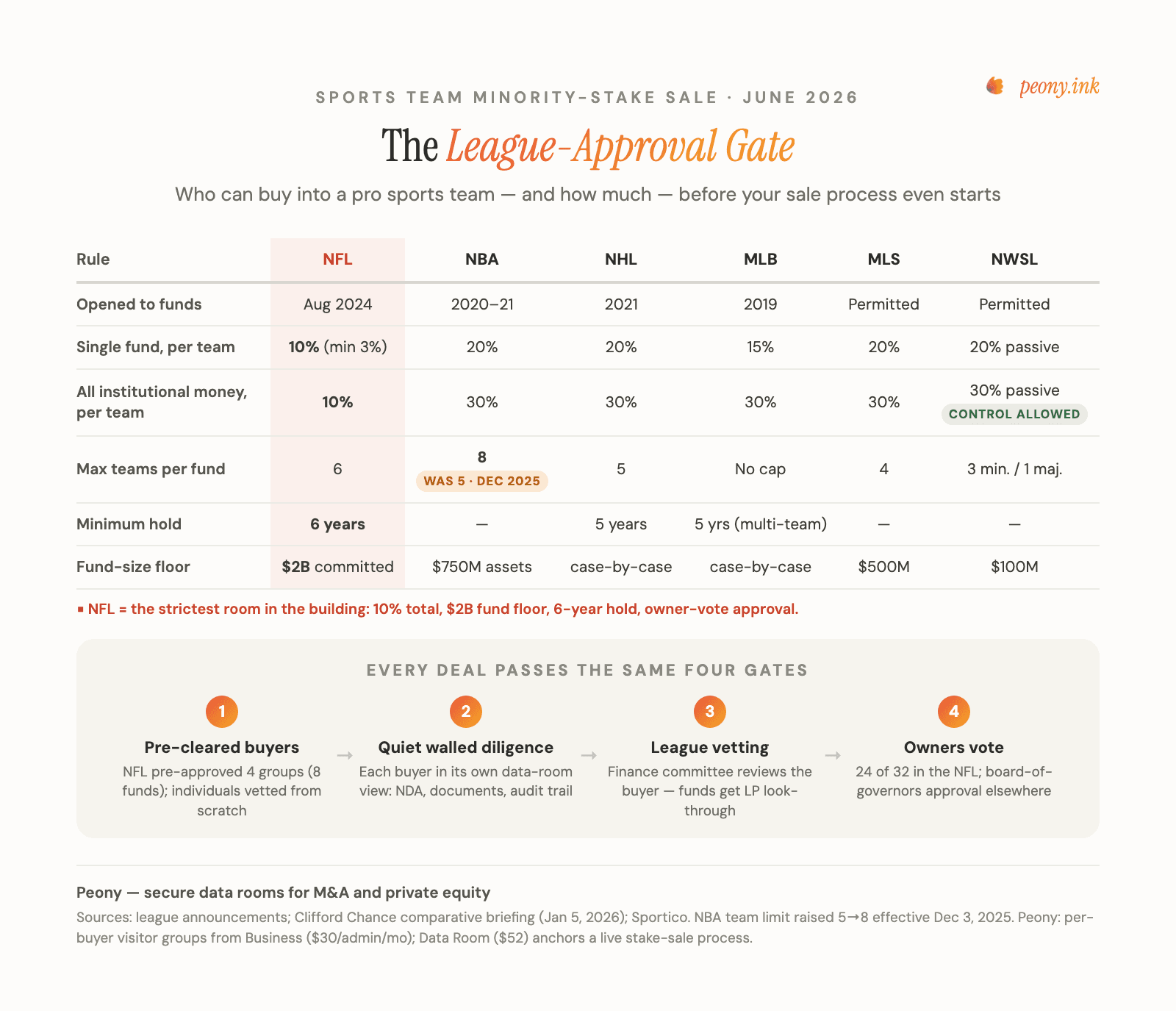

How much of my team can I sell — and to whom — under league rules?

Less than you'd think to funds, more than you'd think overall, and it varies sharply by league. This matrix is current as of June 2026 (the authoritative cross-league comparison is Clifford Chance's January 5, 2026 briefing, updated for the NBA's December 2025 rule change):

| Rule (June 2026) | NFL | NBA | NHL | MLB | MLS | NWSL |

|---|---|---|---|---|---|---|

| Opened to funds | Aug 2024 | 2020–21 | 2021 | 2019 | Permitted | Permitted |

| Single fund, per team | 10% (min 3%) | 20% | 20% | 15% | 20% | 20% passive |

| All institutional money, per team | 10% | 30% | 30% | 30% | 30% | 30% passive; control allowed |

| Max teams per fund | 6 | 8 (raised from 5, Dec 2025) | 5 | No cap (5-yr multi-team hold) | 4 | 3 minority / 1 majority |

| Minimum hold | 6 years | not disclosed | 5 years | 5 years (multi-team) | not disclosed | not disclosed |

| Fund-size floor | $2B committed | $750M assets | case-by-case | case-by-case | $500M committed | $100M committed |

| Can the fund control operations? | No | No | No | No | No | Yes, via majority |

Three things jump out of the table. The NFL is the strictest room in the building — 10% total institutional money per team, a $2 billion fund floor, a six-year hold, and (uniquely) a cap on any single person inside the fund holding more than 7.5% of it. MLB is the quiet outlier for funds — a single fund can hold stakes in an unlimited number of clubs. And the NWSL is the structural exception — the only league where a financial investor can take actual control, up to 100%.

The caps apply to funds, not to people. Individual and family-office buyers can take bigger pieces with full league vetting: the Bills sold roughly 20% in total across Arctos and individual buyers, the Eagles sold 8% to two family investment groups (no fund involved), and the Giants sold a full 10% to one family buyer. The binding constraint on the other side of the table: an NFL controlling owner must hold at least 30%, a team can have at most 25 owners — and the Green Bay Packers, being community-owned, can't do any of this.

One non-change worth stating plainly, because buyers will ask: the NFL did not raise its 10% cap in 2025 or at its March 2026 annual meeting. An expansion beyond 10% is reportedly under discussion among owners — it is not a rule.

Who is actually allowed to buy? The League-Approval Gate

Here's the structural feature that makes a sports stake sale unlike any other M&A process I've worked on, and it deserves a name: the League-Approval Gate. In a normal sell-side process, you cast wide, find buyers, then qualify them. In a sports sale, the qualification happened before your process began — the league decided who may buy before you decided to sell.

The NFL pre-approved exactly four buyer groups (eight funds) in August 2024: Arctos Partners, Ares Management, Sixth Street, and a consortium of Blackstone, Carlyle, CVC, Dynasty Equity, and Ludis — together committing roughly $12 billion of initial capital. As of June 2026 that list hasn't expanded (growth is anticipated in the legal commentary, but no new fund has been added), and every individual buyer outside it must clear league vetting from scratch: financial-standing review by the finance committee, character screening by a dedicated ownership committee, and the look-through right to examine a fund's own limited partners. Then comes the vote — three-quarters of owners, 24 of 32, for any NFL transfer. The league even reserves reported protections after closing: a call right to force a fund out to an approved buyer, and a reported requirement that funds share a slice of their eventual profits with the league.

The Gate inverts how you should build the data room, in three concrete ways:

- Your buyer list is named before the room opens. You're not configuring for anonymous inbound interest; you're building walls for two, three, maybe five specific counterparties you can list today. Build one visitor group per buyer on day one — pre-cleared funds in one lane, individually-vetted family offices in the other — and the room's permission architecture is your process map.

- There's a third reader in the room. Every diligence process has two audiences — you and the buyer. A franchise sale has three: the league office will review the buyer, the structure, and the financial fitness of the deal before the vote. You are effectively assembling two diligence packages — one that convinces the buyer, one that survives the league. Treat the room's audit trail as part of the approval file, not just insurance: a complete, timestamped record of who saw what is the cleanest answer to any question the finance committee asks about how the process was run.

- Buyer scarcity cuts both ways. With ten plausible buyers instead of a hundred, every leaked detail is attributable to a tiny circle — and every bidder knows the others by name even if they can't see them. Isolation isn't paranoia; it's how you keep two pre-approved funds from triangulating each other's position through your process.

What does the approval process look like, step by step?

Four gates, run quietly, over a few months. Recent deals sketch the rhythm: the Giants' sale was announced in late September 2025 and approved October 22, 2025; the first fund deals announced in fall 2024 cleared on December 11, 2024. Plan for weeks-to-months between handshake and vote, and a process like this:

- Structure with counsel (weeks 0–4). Confirm the stake fits the matrix above — cap room under the aggregate limit, controlling-owner minimum intact, buyer type eligible. Decide what you're actually selling: common LP units, preferred with a distribution policy, or a slice with tag-along rights attached. This is also where you set the minority-discount expectation: passive franchise stakes have typically traded at a 20–50% discount to pro-rata team value, because they carry no control and no liquidity.

- Run the quiet process (weeks 2–12). A sports-specialist advisor — Galatioto Sports Partners has run 135+ league transactions including the Bears' 2025 estate sale; Moelis ran the Giants' process; Inner Circle Sports was acquired by William Blair in 2026; Goldman, JPMorgan, PJT Park Hill, Evercore, and Guggenheim all run franchise mandates — approaches the short list. Diligence happens here, in parallel walled views. (Fee mechanics for processes like this follow the same logic I covered in M&A advisor fees.)

- League vetting (overlaps, then extends). The buyer files with the league; the finance committee reviews financial fitness; for funds, the league can look through to LPs. Nothing about your transaction is fully private from the league — design your disclosure accordingly.

- The vote and close. 24 of 32 in the NFL; board-of-governors approval elsewhere (the Celtics' control sale was approved by the NBA board August 13, 2025). Only after the vote do you stand down the process — and the data room's final job is the archive: a complete record of the process for the league file and for any partner who later questions how their stake was repriced.

What goes in the data room for a franchise minority-stake sale?

A franchise data room is contract-weighted, not financials-weighted — that's the second frame this post will insist on, the Contract-Weighted Room. A normal company sale is underwritten on cash flow, so diligence lives in the financial statements. A franchise is a scarcity asset priced on contracted revenue durability — Sportico's 2025 NFL set averages $7.13 billion per team against operating profits that would embarrass a mid-market SaaS company — so a buyer's reading time concentrates on the tenor and transferability of contracts, not the P&L. Run page analytics on a franchise process and you can watch it happen: the stadium lease and the media-rights folder get read five times as hard as the income statement.

Here's the twelve-category stack — it extends the generic folder tree from the M&A data room guide with the franchise-specific layers — and what the buyer is actually checking in each:

| # | Folder | What the buyer is really underwriting |

|---|---|---|

| 1 | League constitution & franchise agreement | Transfer consents, ownership caps, what an LP can and can't ever do |

| 2 | Team debt & league debt-limit compliance | Headroom vs the cap — the NFL allows $800M per team, plus $700M more for new buyers [as of May 2025] |

| 3 | CBA & salary-cap documents | Fixed labor economics; cap obligations that travel with the team |

| 4 | Stadium / arena: lease or ownership | The asset question — owned venue means ancillary revenue and development upside; leased means revenue-share, scheduling, and political constraints |

| 5 | Naming rights & PSL obligations | Contracted stadium revenue tenor; obligations to seat-license holders |

| 6 | Media agreements, national & local | The valuation backbone (and its reset dates — see below) |

| 7 | Sponsorship & corporate partnerships | Term, escalators, exclusivity carve-outs, change-of-ownership clauses |

| 8 | Ticketing agreements | Platform lock-ins, rev-share, season-ticket-holder commitments |

| 9 | Concessions, F&B, parking | Margin per attendee; operator contract terms |

| 10 | Mixed-use real estate & development SPVs | Where the next decade of value creation actually sits |

| 11 | Litigation, regulatory, stadium subsidies | Municipal obligations, clawbacks, pending disputes |

| 12 | Key-person & front-office contracts | GM/coach terms; what leadership costs to keep or change |

Two folders deserve special notes in 2026.

Folder 6 is where deals get interesting. The national backbone is genuinely strong — the NFL's ~$110 billion, 11-year media deals run through 2033, and the NBA's $76 billion, 11-year agreements began with the 2025-26 season — but it carries a reset date buyers will model: the NFL holds an opt-out after the 2029 season and is widely expected to use it. Local media is the opposite story. Diamond Sports' successor Main Street Sports Group collapsed this year — all nine of its MLB teams terminated their contracts on January 8, 2026 over missed payments, and the company is winding down with local rights reverting to teams and leagues. Which sets up the third frame: run the Stranded-Local-Revenue Check. Every MLB, NHL, and NBA seller should walk into diligence with a one-page answer classifying its local-media revenue as contracted (a solvent counterparty on a multi-year deal), league-carried (folded into a league direct-to-consumer platform), or stranded (reverted rights, monetization TBD). If you don't write that page, the buyer's analyst will — with a bigger discount attached.

For a minority deal specifically, the most-negotiated folder isn't on the asset side at all. It's the LP-protection set inside your governing agreement: distribution policy (does cash ever come out, or is everything reinvested), capital-call mechanics (can the controlling owner compel contributions, and what dilution follows a miss), transfer restrictions (rights of first refusal with 60–120-day notice periods are common, plus controlling-owner and league consent on any exit), drag-along/tag-along rights (tag-along is the minority holder's real liquidity protection — it lets you ride a future control sale at the control price), and information rights (what financials you're owed and when). Sophisticated funds read these before they read your sponsorship file; they're underwriting the partnership terms as much as the team.

If your franchise has never produced this material before, you're in good company — most haven't. Institutional buyers will ask for auditable statements rather than management summaries, contract abstracts with remaining term and escalators on every material agreement, and league-rule compliance laid out (debt versus cap, ownership table versus limits). Budget 60–90 days of preparation before the room opens; the general mechanics are in how to prepare for due diligence.

How do I run several approved buyers through diligence at once — without them seeing each other?

This is the One Room, Many Walls problem — I wrote the full operator's guide for competitive auctions, and a stake sale is its quiet, high-stakes cousin. The answer is one master room partitioned into walled buyer views, never a separate room per buyer (which triples your admin and guarantees disclosure drift), and never — this should go without saying but 2024-era deal stories say otherwise — email attachments.

The sports-specific version of the Staged-Disclosure Ladder looks like this:

| Rung | Stage | What the buyer's group can see |

|---|---|---|

| 0 | Soft sounding | Anonymized franchise profile via the advisor; no room access, NDA pending |

| 1 | First look | Franchise overview, summary financials, league-rule position, process letter |

| 2 | Confirmatory | Stadium lease, media & sponsorship contracts, detailed financials, governing agreement |

| 3 | Final buyer / clean team | Player payroll & CBA detail, draft purchase agreement, the league filing package |

| 4 | League approval | Process archive: per-buyer audit trails, NDA records, disclosure log for the file |

Mechanically, on Peony: one visitor group per buyer (per-group documents, NDA gates, personalized links, and audit trails are on the Business plan); granular per-file permissions, the Advanced NDA with countersigned PDF, auto-indexing, and Screenshield arrive with the Data Room plan ($52/admin/month) — the anchor tier for a live process. Promote a buyer by moving its group up a rung; cut one by revoking the group in a single action while its audit trail survives for the league file.

Q&A is where parallel diligence leaks if you let it. Run a moderated workflow — every question routes privately to your team, the platform drafts a cited answer from your documents, and nothing publishes until you approve it — so no fund ever sees another's questions or learns another exists. (Smart Q&A runs this on Peony; the full reasoning is in data room Q&A.) If you want physically separate Q&A channels per buyer group inside one room, that's available on Peony Enterprise; the moderated workflow keeps lower tiers leak-free because nothing is auto-broadcast, and a separate room per buyer remains the brute-force option on any plan.

One honest note: most stake sales involve two to five buyers, not fifteen. The walls matter more than the scale — with so few parties at the table, any cross-contamination is instantly attributable and instantly priced.

How do I keep the process from leaking to ESPN, player agents, or the locker room?

Treat confidentiality as valuation protection, not hygiene — that's the fourth frame, the Leak Premium. In normal M&A, a leak moves your price. In sports, a leak simultaneously hits three constituencies that aren't at the table: the fan base and season-ticket renewals ("are they selling?"), the locker room and every agent mid-negotiation (uncertainty is leverage you just handed away), and the city hall relationships your stadium economics depend on. The beat press exists to find exactly this story. That asymmetry — small buyer circle, enormous blast radius — is why I'd run a franchise process with tighter information discipline than a take-private.

The discipline, concretely:

- Shrink the circle. Controlling owner, CFO, counsel, advisor. Your GM and coaching staff usually have no need to know a passive LP sale is in motion — and an I-found-out-from-Twitter locker room is a real cost. Code-name the project; keep the room's name bland.

- No email, ever. Email is untracked, unrevocable, and the #1 leak vector in every process I've seen. If a buyer asks for "just the lease PDF as an attachment," the answer is a personalized room link.

- Make every page a signed confession. Dynamic watermarks stamp each page with the viewer's email, IP, and timestamp — server-side, on every render. A leaked page identifies its leaker. Even the analog hole — someone photographing a screen with their phone — captures the watermark; I wrote up that whole threat model in stopping phone photos of documents.

- Block what can be blocked. Download prevention on rungs 1–2, screenshot protection on the Business plan, Screenshield's deeper screen-capture blocking on the Data Room plan.

- Watch the analytics like a seismograph. Page-level analytics show who's reading what, from where, for how long. The tells: a sudden mass-print pattern, a login from an unexpected network, a buyer's "analyst" reading only the payroll file. You want the warning before the story runs, not after.

- Gate access on signed paper. NDA gates mean no document loads until that specific buyer accepts that specific NDA — logged, and on the Data Room plan, countersigned with a PDF in both parties' hands.

None of this makes a leak impossible; it makes every leak attributable and every reader accountable, which changes behavior at the only moment that matters — before the leak.

What's the best data room for a sports franchise stake sale?

Segmented honestly, because the answer depends on who's running your process:

| Capability | Peony | Datasite | Intralinks | Firmex | Ansarada |

|---|---|---|---|---|---|

| Per-buyer isolation (groups) | Yes (Business) | Yes | Yes | Yes | Yes |

| Per-viewer dynamic watermarks | Yes (Data Room) | Yes | Yes | Yes | Yes |

| Screen-capture blocking | Yes (Screenshield, Data Room) | Yes | Yes | Limited | Limited |

| Walled per-group Q&A threads | Enterprise | Yes | Yes | Yes | Yes |

| AI-drafted, cited Q&A answers | Yes (Business) | Yes | Partial | No | Partial |

| Pricing shape | Flat per admin | Metered per deal | Metered per deal | Per deal | Metered |

| Indicative cost, one process | $52–64/admin/mo | tens of thousands | tens of thousands | ~$5–10K/deal | $479+/mo entry |

How to read it. If a bulge-bracket bank runs your process, it will probably put you on Datasite or Intralinks, and that's a defensible default — they're built for bank-led processes with service teams attached, and the bank's deal staff already knows the tooling. Pay the metered cost knowingly. (Worth knowing as you compare "alternatives": Datasite acquired Firmex in 2021 and then Ansarada in August 2024 — three of the five logos on the standard shortlist are one company.) If the owner's office runs the process — and most minority-stake sales are exactly that: quiet, advisor-assisted, two to five buyers — the job description is per-buyer walls, watermark-everything, NDA gates, analytics, and moderated Q&A at a flat, predictable price. That's the lane Peony is built for: SOC 2 Type II certified, 6,800+ teams, and the room is live the same afternoon your advisor makes the first call. Where Peony honestly loses: if you need walled per-buyer Q&A threads on a standard tier (Firmex's coordinator workflow is genuinely strong, and on Peony that's an Enterprise capability) or a vendor-staffed service team to run the room for you.

| Your situation | Best choice | Why |

|---|---|---|

| Owner-run quiet sale, 2–5 pre-cleared buyers | Peony (Data Room, $52) | Per-buyer walls + watermarks + analytics, flat price, same-day setup |

| Bank-led marketing process, full service team | Datasite / Intralinks | Built for bank-led mega-processes; your bank already runs them |

| Walled per-buyer Q&A threads required on a standard tier | Firmex | Its Q&A coordinator workflow is the strongest standard-tier version |

| League-package archive + multi-deal pipeline (fund side) | Peony (Deal Team, $64) | Flat per-admin price across unlimited rooms; one room per target |

| Massive cross-border control sale with bespoke compliance | Datasite / Intralinks | Enterprise compliance tooling and staffing fit the deal size |

How much should the data room cost for a one-time stake sale?

A few hundred dollars a month, not five figures — if you avoid metered pricing. A stake sale is the worst-case shape for a meter: the process runs months (league vetting and the vote add weeks-to-months after signing), the room is contract-heavy (thousands of pages), and parallel buyers multiply access. Per-page, per-user, and per-deal models price all three in: Firmex typically lands around $5,000–10,000 per deal; Datasite and Intralinks commonly reach the tens of thousands for one process; Ansarada's metered entry starts at $479/month ($244 on a 12-month term). Flat-rate removes the variables — Peony's Data Room plan is $52/admin/month with unlimited buyers, storage, and rooms, and the M&A-grade Deal Team plan is $64/admin/month (annual, minimum 4 admins) — so two admins on the Data Room plan running a six-month process spend roughly $600 total. (The full math on why metered billing punishes long, document-heavy processes is in flat-rate vs per-GB pricing.) Against a process where the advisory fee alone runs seven figures, the room is rounding error either way; what you're buying with flat-rate is the certainty that adding a fourth buyer or a fifth month never creates an invoice conversation mid-deal.

Frequently asked questions

I'm selling 10% of my team to a fund — how does the league approval process actually work, step by step?

Four gates, in order. First, structure: your counsel confirms the stake fits league rules (cap, controlling-owner minimum, buyer eligibility). Second, the quiet process: a sports-specialist advisor runs diligence with one to four pre-cleared buyers in a walled data room. Third, league vetting: the league's finance committee reviews the buyer's financial standing — for a fund, the league can look through to its limited partners — and in the NFL a dedicated ownership committee screens the deal. Fourth, the owners vote: an NFL transfer needs 24 of 32 owners; other leagues use analogous board-of-governors approval. In recent deals the span from announcement to approval ran weeks to a few months — the Giants' 10% sale was announced in September 2025 and approved October 22, 2025, while the first NFL fund deals announced in fall 2024 were approved December 11, 2024.

How much of my team can I sell to private equity under league rules in 2026?

It depends on the league and the buyer type. To funds: the NFL caps institutional ownership at 10% of a team total (single fund 3–10%); MLB allows 15% per fund and 30% aggregate; the NBA, NHL, and MLS allow 20% per fund and 30% aggregate; the NWSL allows 20% passive — and is the only league that permits financial-investor control. To individuals and family offices, you can go further: the Bills sold roughly 20% across Arctos and individual buyers in 2024, and the Giants sold 10% to Julia Koch in 2025. The hard floor is control — an NFL controlling owner must keep at least 30% — and every transfer still needs league approval regardless of size.

Should I sell the stake to a league-approved fund like Arctos, Ares, or Sixth Street — or to a single ultra-high-net-worth buyer?

They are different processes, not just different names on the wire. The approved funds (in the NFL: Arctos, Ares, Sixth Street, and the Blackstone/Carlyle/CVC/Dynasty/Ludis consortium) are pre-vetted, structurally passive, and built to close — but they're capped (10% in the NFL) and hold for the long term (six-year minimum). An individual or family buyer can take a larger piece — the Giants sold 10% to one buyer at a $10.3 billion valuation; the Eagles sold 8% to two family groups — but goes through full league vetting from scratch. In practice many sellers run both lanes at once: two or three approved funds plus one or two family offices, each in its own walled view of the same data room, and let the structure compete as well as the price.

How do I give my legacy limited partners liquidity without giving up family control of the franchise?

Sell a passive minority slice, keep the control block intact. League rules are built for exactly this: institutional buyers are non-voting and non-operating by rule, so a 5–15% LP sale converts paper wealth into cash for legacy partners without touching governance — the NFL just requires the controlling owner to keep at least 30%. Expect pricing reality, though: minority franchise stakes typically trade at a 20–50% discount to pro-rata team value because they carry no control and no liquidity. The data room matters here because legacy-LP sales are the most leak-sensitive kind — you're effectively repricing every partner's stake in front of them — so each prospective buyer should diligence in an isolated, watermarked, fully logged view.

How do I keep the sale process from leaking to ESPN, player agents, or the locker room?

Shrink the circle, wall the room, and make every page traceable. Keep the working group to the controlling owner, CFO, counsel, and the advisor — your GM and coaching staff usually don't need to know a passive LP sale is happening. Never email diligence files; share only through a data room with NDA gates, per-buyer access walls, and dynamic watermarks that stamp every page with the viewer's identity, IP, and timestamp. Disable downloads for first-round access and watch page-level analytics for unusual behavior — mass printing or a login from a news organization's network is your early warning. A leak in sports doesn't just move price: it hits season-ticket holders, agents mid-negotiation, and your stadium politics all at once, which is why the room's job is deterrence and attribution, not just storage.

Can I watermark diligence documents so a leak traces back to the exact investor who leaked them?

Yes — that's what dynamic (per-viewer) watermarking does. Each page renders with the specific viewer's email, IP address, and access timestamp burned in, so a leaked page is a signed confession: it identifies who had it. Pair it with download prevention and screenshot protection, and anything that escapes — even a phone photo of a screen — carries the leaker's identity. On Peony, screenshot protection and download blocking are on the Business plan ($30/admin/month, billed annually); dynamic watermarks come with the Data Room plan ($52/admin/month), which also adds Screenshield to block screen capture and recording at a deeper level. No tool can physically stop a camera, but attribution turns a leak from anonymous to career-ending, which is the deterrent that actually works.

How do I control which approved bidders see the stadium lease, media-rights contracts, and player payroll?

Permission by folder tier and by buyer group, not document by document. Put each buyer in its own visitor group, then build the room in disclosure tiers: franchise overview and summary financials open to every active buyer; stadium lease, media and sponsorship contracts unlocked for serious second-round parties; player payroll, CBA detail, and the draft purchase agreement reserved for the final buyer and its clean team. Granular per-file permissions let you make exceptions inside a tier — for example, sharing the naming-rights agreement with the fund that asked while it stays hidden from the rest. Every view is logged per group, so you always know exactly which buyer has seen which contract, which matters when the league asks and when a losing bidder later claims it was treated unfairly.

Three league-approved funds want to diligence us at once — how do I run that without them seeing each other?

One room, many walls — not three rooms. Give each fund its own visitor group with isolated documents, its own NDA, its own tracked links, and its own audit trail; no group can see that the others exist. You maintain one master index and stage disclosure by promoting a group to the next tier as it advances, rather than rebuilding access in parallel rooms. Route questions through a moderated Q&A workflow so nothing any fund asks is ever visible to another — answers publish only when you approve them. If you want fully walled, physically separate Q&A channels per fund inside one room, that's available on Peony Enterprise; on any plan, a separate room per fund buys the same separation at the cost of triple admin.

What documents go in the data room for a sports franchise minority-stake sale?

Twelve categories, contract-heavy: (1) league constitution and franchise agreement, (2) team debt and league debt-limit compliance, (3) CBA and salary-cap documents, (4) the stadium or arena lease — or proof of ownership — plus practice facility and parking, (5) naming rights and PSL obligations, (6) national and local media agreements, including your RSN exposure, (7) sponsorship and corporate partnerships, (8) ticketing agreements, (9) concessions and F&B, (10) mixed-use real-estate and development entities, (11) litigation and regulatory matters including stadium-subsidy agreements, and (12) key-person and front-office contracts. For a minority deal, add the LP-protection set buyers actually negotiate: distribution policy, capital-call mechanics, transfer restrictions and rights of first refusal, drag-along/tag-along rights, and information rights.

This is our first institutional diligence — what will a PE fund actually ask a franchise to produce?

Things a family-run franchise often has never had to write down. Expect requests for auditable financial statements (not internal management summaries), contract abstracts showing the remaining term and escalators on every material media, sponsorship, and suite agreement, a clear answer on local-media exposure — contracted, league-carried, or stranded by the RSN collapse — your governing agreement with distribution and capital-call mechanics spelled out, league-rule compliance (debt versus the league cap, ownership table versus league limits), and stadium economics with the lease, subsidies, and development rights. The pattern: institutional buyers underwrite contract durability, not last season's EBITDA. Budget 60–90 days to assemble it before opening the room — gaps discovered mid-process read as risk and cost you more than the delay.

What's the best virtual data room for a confidential sports franchise sale?

Match the room to who's running the process. If a bulge-bracket bank is running a full marketing process, it will likely default to Datasite or Intralinks — built for bank-led mega-deals with service teams attached, at a metered cost in the tens of thousands per process (worth knowing: Datasite also owns Firmex and Ansarada, so several 'alternatives' on the standard shortlist are one company). If the owner's office is running a quiet two-to-four-buyer process — most minority-stake sales — a flat-rate room with per-buyer walls does the actual job: visitor-group isolation, dynamic watermarks, Screenshield screen-capture blocking, NDA gates, page-level analytics, and moderated Q&A. That's Peony's lane: $52/admin/month on the Data Room plan, SOC 2 Type II certified, used by 6,800+ teams. The honest rule: pick the bank's default for a bank-led auction; pick the flat-rate specialist when you're running it yourself and the buyer list fits on one hand.

How much does a data room cost for a one-time stake sale — and is flat-rate cheaper than Datasite or Intralinks for a franchise deal?

A franchise stake sale is the worst-case shape for metered pricing: months of access (league approval adds weeks-to-months after signing), thousands of pages of contracts, and several parallel buyers. Per-page or per-deal platforms price accordingly — Firmex typically runs about $5,000–10,000 per deal, and Datasite or Intralinks commonly reach the tens of thousands for a single process. Flat-rate pricing removes the meter: Peony's Data Room plan is $52/admin/month (billed annually) with unlimited buyers, storage, and rooms, and the M&A-focused Deal Team plan is $64/admin/month — so a six-month process with two admins runs a few hundred dollars, not five figures. Data-room cost is rounding error next to your advisory fees either way; predictability, not just price, is the point.

Related reading

- Data room for a film or TV catalog sale — the other media/entertainment deal type: library valuation, chain-of-title, and rights windowing

- Best data room for multiple bidders — the full One Room, Many Walls playbook this post applies to a pre-cleared buyer field

- Stop phone photos of documents — the analog hole, and why per-viewer watermarks are the only control that survives a camera

- Data room Q&A — the moderated workflow and the two layers of Q&A isolation

- 15 sports investors actively deploying in 2026 — the fund landscape, from sports-specialist VCs to ownership platforms

- Secure video data room — sharing footage and media assets with bidders, the media vertical's anchor

- M&A advisor fees — how advisory fees actually scale on processes like this

- How to prepare for due diligence — the 60–90-day readiness sprint before the room opens

- Flat-rate vs per-GB VDR pricing — why metered billing punishes long, contract-heavy processes

- The M&A data room guide — folder structure, staging, and Q&A for general transactions

- Data room for investors — multi-party access patterns beyond sports

Sell the stake without selling the story. Start free on Peony or see how visitor groups wall off each buyer.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 6,800+ teams across M&A, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.