Data Room for a Film or TV Catalog Sale (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: June 2026

I'm Sean Yu, co-founder of Peony, a data room platform used by 6,800+ teams across M&A, private equity, and media transactions. Before Peony I worked on sell-side and growth processes at Nomura, Backed VC, and Target Global. This guide is about a deal I find genuinely fascinating and that almost nobody writes about from the operator's seat: selling a film or TV catalog — a library of finished films and series and the rights underneath them.

Here's why it matters right now. The biggest media transaction in a generation is mid-flight: Paramount Skydance agreed to acquire all of Warner Bros. Discovery for $31.00 per share in cash — an ~$81 billion equity value, roughly $110 billion including assumed debt, a 147% premium to WBD's unaffected price — signed February 27, 2026, approved by WBD shareholders April 23, 2026, and cleared by the U.S. Department of Justice without conditions on June 12, 2026. As I write this it still awaits the EU — which is running two parallel reviews, a standard merger review and a foreign-subsidies probe into the Gulf sovereign-wealth money backing the deal — with the companies targeting a close in the third quarter of 2026. Buying WBD whole also shelved WBD's own previously announced plan to split into separate studios-and-streaming and cable companies. (The acquirer is Paramount Skydance, not Netflix — Netflix's competing bid, for WBD's studios and streaming only, was withdrawn February 26, 2026, one day before the Paramount agreement; the "Netflix buys WBD" framing that circulated is simply wrong.) At its core, a deal that size is a content-library, rights, and carriage diligence — and the same mechanics run all the way down to a $50 million indie catalog. This post is that mechanics, transaction-side. For the file-handling half — how to actually stream 4K screeners to buyers without handing over the masters — I wrote a separate companion, the secure video data room guide; this one is about the deal and the diligence.

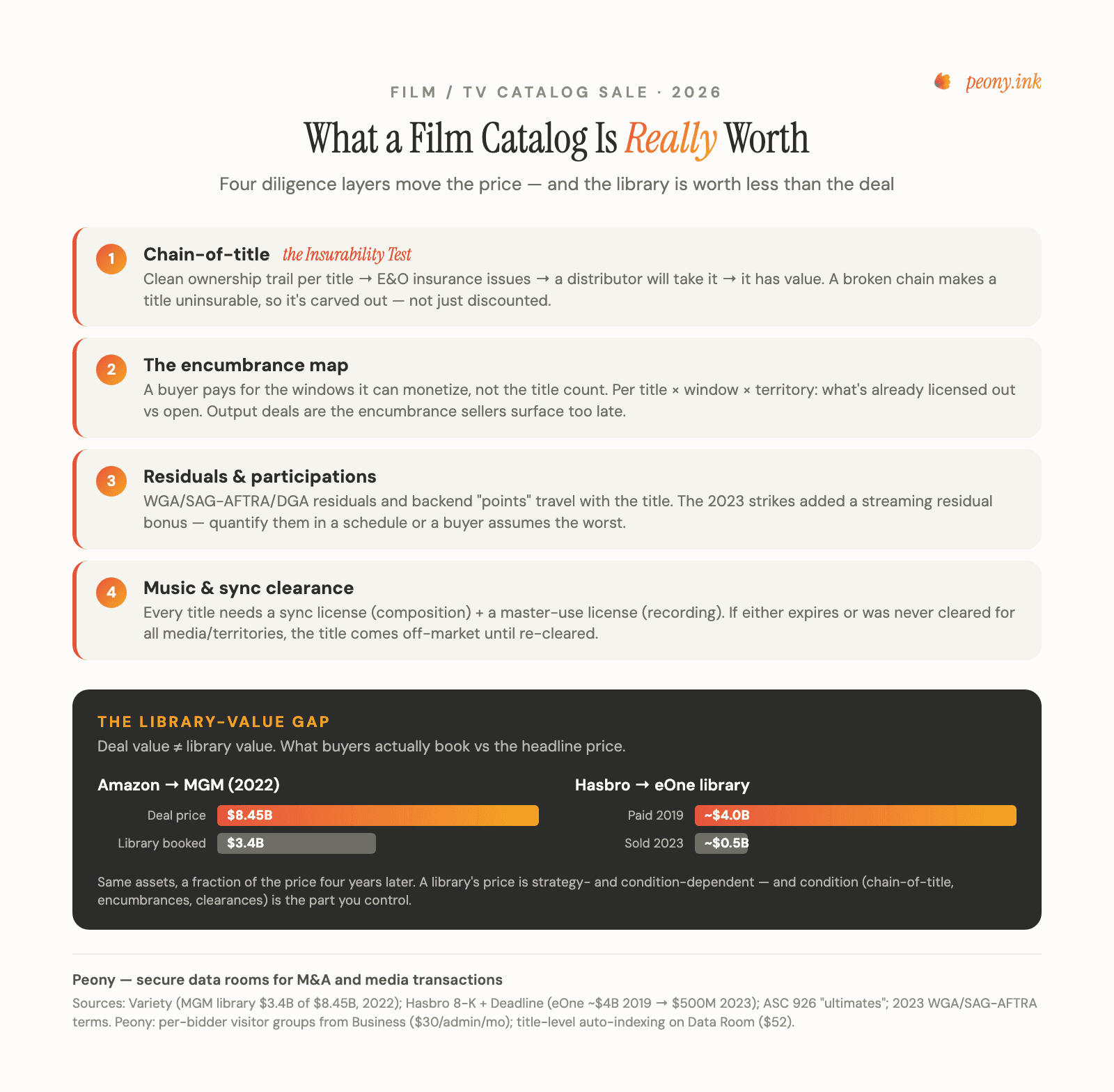

Quick answer: The market is real: Suits — a show that ended in 2019 — became Nielsen's most-streamed title of 2023 at 57.7 billion minutes viewed, beating the record set by The Office (Variety/Nielsen, Jan 2024), resetting how studios value back-catalogs; and the Paramount Skydance–WBD megadeal cleared the U.S. DOJ without conditions on June 12, 2026 at an ~$110B enterprise value (CBS News, Jun 2026). But know the Library-Value Gap before you go to market: Amazon paid $8.45B for MGM and booked the library at ~$3.4B (Variety, Nov 2022); Hasbro paid ~$4B for eOne in 2019 and sold the film/TV library for ~$500M in 2023 (Fortune, Aug 2023). A catalog sale is won or lost on three documents most sellers underprepare. First, chain-of-title per title — because a broken chain means no E&O insurance, and no E&O means no distribution, making a title unsellable, not just risky (the Insurability Test). Second, the encumbrance map — what windows and territories are already licensed out — because buyers pay for what they can monetize, not the title count. Third, residual and participation schedules — the 2023 strikes added a success-based streaming residual bonus (SAG-AFTRA's pool alone is estimated at ~$40M/yr; Variety, Nov 2023), so buyers now expect title-level schedules. Organize by title, then by rights. Wall each bidder into its own visitor group. On Peony, per-bidder isolation and NDA gates start on the Business plan ($30/admin/month); the title-structured Data Room plan ($52/admin/month) — with dynamic watermarks, auto-indexing, and granular per-file permissions — is the anchor for a real catalog process.

Why are film and TV libraries trading hands in 2026?

Because the industry flipped its strategy from hoarding content to monetizing it, and a back catalog turned out to be the most reliable cash machine in media. From roughly 2019 to 2022, every studio pulled its library back to feed its own streaming service. Then in mid-2023, NBCUniversal licensed Suits — a show that finished its run in 2019 — to Netflix, and it shattered streaming-viewership records. That single data point reset the industry's thinking: a well-cleared library is an "arms-dealer" asset you can license to rivals for cash, not a moat you have to defend. Sony and Universal, which lack a fully-owned U.S. general-entertainment streamer, leaned hardest into library licensing, and Wall Street came to treat the return of arms-dealer licensing as a structural positive rather than a sign of weakness.

Two forces turned that insight into a transaction wave. First, library cash flow is durable and re-licensable — a finished title keeps earning through SVOD and AVOD windows, linear syndication, FAST channels, airline and hospitality rights, international territory sales, format and remake rights, and now AI-training licensing. Second, private equity learned the playbook in music first. Blackstone took Hipgnosis Songs Fund private for about $1.6 billion in 2024 (and followed it with a ~$1.47 billion music asset-backed securitization), and Sony bought Queen's catalog for a reported ~$1.27 billion (£1 billion) the same year. Those deals proved that rights behave like a long-duration annuity with recurring cash flow — exactly the thesis now reaching film and TV catalogs, where royalty and IP funds bid alongside the strategics. When the buyer universe widens from "three studios" to "three studios plus every royalty fund," catalogs trade.

One thing you won't get from the market commentary (there's plenty of "why capital is coming to content" analysis): how one of these sales actually runs once you decide to do it. That's the rest of this post.

What is a film or TV catalog actually worth — and why doesn't it equal the deal price?

A catalog is worth the present value of what its titles will still earn — and that number is almost always lower than the headline deal price, which is the first thing a first-time seller gets wrong. Call it the Library-Value Gap. When Amazon acquired MGM for $8.45 billion in 2022, its own purchase accounting valued the content library at roughly $3.4 billion — the other ~$4.9 billion was goodwill, brand, and strategic optionality. The library you're selling and the price a strategic pays for owning it are two different numbers, and you should know both before you go to market.

How buyers actually get to the library number:

- Title-level "ultimates." Under the film-accounting standard (ASC 926), every title carries an ultimate — the estimate of total revenue it will earn across its full commercial life, generally up to about 10 years for a film. A catalog buyer is, in effect, buying the present value of every title's remaining ultimate. This is why a title-by-title revenue history and current ultimate projections belong in the room.

- Discounted cash flow on the library's recurring licensing and residual income, where the terminal value is a large share of the total and brutally sensitive to the discount rate and growth assumptions.

- Multiples, as a cross-check. A commonly cited rule of thumb is 5–10x annual net licensing revenue, and content businesses often trade around 4–12x EBITDA — useful guardrails, not gospel, and pure passive libraries lean on the licensing-revenue multiple more than EBITDA.

The deeper lesson is that a library's price is strategy- and condition-dependent, not fixed. Hasbro bought Entertainment One (eOne) for roughly $4 billion in 2019 and sold its film and TV library to Lionsgate for about $500 million in 2023 — a ~6,500-title library, same assets, a fraction of the price four years later. Part of that is the licensing cycle, which you don't control. But a large part is condition — chain-of-title, encumbrances, and clearances — which you do. The four layers below are what move a catalog from the low end of that range to the high end.

How do buyers prove you actually own what you're selling? The Insurability Test

They run chain-of-title, and the reason it's decisive is a causal chain I call the Insurability Test: clean chain-of-title → E&O insurance issues → a distributor will take the title → the title has value. Break the first link and the whole chain fails.

Chain-of-title is the unbroken, documented ownership trail for a single title — starting from the original source material (a novel, a screenplay, life-story rights) and running through every option, writer agreement, assignment, and transfer that moved the rights to you, plus the copyright registration and a copyright/UCC/lien search. Practitioners organize it into five buckets — underlying rights, screenplay, production, music, and distribution — and you should structure your data room the same way, per title.

Here's the part sellers underestimate. Errors-and-omissions (E&O) insurers require a complete chain-of-title review before they'll issue a policy, and any defect has to be cured first. Distributors and streamers won't take a title without E&O coverage. So a title with a gap in its chain isn't merely a risk a buyer discounts — it's a title that can't be insured, can't be distributed, and therefore can't be monetized. In diligence those titles get carved out of the deal entirely, and worse, a cluster of gaps makes the buyer suspicious of the whole catalog's record-keeping, which discounts even the clean titles.

The practical implication for your data room: don't wait for the buyer's lawyers to find the gaps. Run your own chain-of-title review first, title by title, cure what you can (re-execute missing assignments, register unregistered copyrights), and bring the copyright/lien search reports into the room. A catalog that walks in with clean, organized chain-of-title files diligences fast and holds its price; one that makes the buyer reconstruct ownership from scattered decades-old paper invites both delay and a discount.

Which rights can the buyer actually monetize? The Encumbrance Map

A buyer pays for the windows it can exploit, not for your title count — so the second decisive document is the Encumbrance Map: a per-title, per-window, per-territory schedule of what's already licensed out, to whom, and until when. Two libraries with identical titles can be worth wildly different amounts if one has its prime windows open and the other has them tied up.

Film and TV rights are sliced three ways at once — by window (theatrical → PVOD → home entertainment → Pay-1/SVOD → AVOD/FAST → linear), by territory (North America, Europe, Asia, and on down), and by language and term. Every cell in that grid is either available for the buyer to monetize or encumbered by an existing license. A title whose prime SVOD window and major territories are committed to a multi-year output deal generates no near-term cash for the buyer, no matter how good the film is.

The encumbrances buyers most often discover late — and resent — are output deals, where a studio has committed future or library titles to a distributor or streamer for a term. Surface those early and explicitly. The deliverable that separates a credible process from a discounted one is a clean availability matrix: for each title, which windows and territories are sold, to whom, for how long, and which are open. That schedule is, in a real sense, the actual product you're selling — the open windows — and presenting it crisply tells a buyer the library was run by professionals.

How do residuals, participations, and music clearances change the price?

They're the liabilities and time bombs that travel with each title, and a buyer underwrites every one of them as a deduction from your library's cash flow — so your job is to quantify and schedule them, not let the buyer guess.

- Residuals. Ongoing payments to talent and crew through WGA, SAG-AFTRA, and DGA for the reuse of content. They attach to the title and pass to the buyer, so the purchase agreement must state explicitly which residuals the buyer assumes — vague language is how an acquirer inherits liabilities it didn't price. The 2023 strikes added a success-based streaming residual bonus: a title viewed by the equivalent of 20% or more of a platform's domestic subscribers in its first 90 days triggers a +50% residual bonus for WGA writers and a 100%-of-residual bonus on the SAG-AFTRA side — of which the qualifying performers keep 75%, with 25% routed to a union-administered fund (SAG-AFTRA's pool is estimated at ~$40 million/year). It applies only to titles released on or after January 1, 2024, so it bears mainly on a catalog's newer titles — but it made residual exposure far more scrutinized and better documented across the board. Buyers now expect a title-level residual schedule and will assume the worst on anything you can't quantify.

- Profit participations ("backend"). Contracted shares of a title's profits owed to talent after costs are recouped — "points," where one point is roughly 1% of net profit. A first-dollar-gross participant on a hit franchise can materially cut an acquirer's economics, and backend is one of the most-litigated areas in Hollywood because "net" is defined by studio accounting. Bring title-level participation statements; their absence reads as hidden liability.

- Music and sync rights. Every piece of music needs two clearances — a sync license for the composition and a master-use license for the recording. These are often granted for limited media, territories, or terms, and if one expires or was never cleared for all media/territories, the title comes off-market in that window until re-cleared. Legacy catalog titles with fragmented, decades-old clearances are a classic landmine. A music-clearance matrix (scope, term, territory, expiry per title) belongs in the room.

The framing that protects your price: a quantified, scheduled liability gets priced into the deal at its real cost; an unquantified one gets a punitive, worst-case discount — or kills the title. Diligence rewards disclosure here.

What goes in the data room for a film/TV library sale? The Title-Level Room

Organize it by title first, then by rights within each title — never by document type. This is the Title-Level Room principle, and it's the opposite of how most general M&A rooms are built. A catalog buyer diligences one title at a time; a room sorted into generic "Contracts" and "Financials" folders forces them to reassemble each title across the structure, which is slow and signals a disorganized library — and a disorganized library gets a lower bid. Build a master title manifest as the index, then one folder per title. This also extends the generic folder tree from the M&A data room guide with the layers unique to film and TV.

| Per-title folder | What the buyer is really underwriting |

|---|---|

| 1. Chain-of-title documents | Most scrutinized. Underlying-rights/option/writer agreements, assignments, copyright registrations, and the copyright/UCC/lien search — does the title pass the Insurability Test? |

| 2. Existing license & encumbrance schedule | Co-most-scrutinized. What windows/territories are already sold — what can the buyer actually monetize? |

| 3. Distribution & output agreements | Current deals and any output commitments, with windows, territories, languages, terms |

| 4. Talent & crew agreements + residual schedules | Cast/director/producer deals and the per-title WGA/SAG-AFTRA/DGA residual liability that travels with the title |

| 5. Profit-participation / backend statements | Who has points, gross vs net, current statements — the net-cash-flow drag and litigation risk |

| 6. Music & sync licenses | Sync + master-use licenses with scope, term, territory, and expiry — the off-market risk |

| 7. E&O insurance | Policies, certificates, claims history — and confirmation each title is or can be insured |

| 8. Financials + title-level revenue & "ultimates" | Historical revenue by window/territory and current ultimate projections (ASC 926) |

| 9. Guild agreements | Applicable WGA/SAG-AFTRA/DGA/IATSE collective agreements and assumption obligations |

| 10. Tax credits / incentives | Production tax-credit certificates, soft money, co-production treaty documents |

| 11. Litigation / IP disputes | Pending or threatened infringement, participation, or rights disputes |

| 12. Masters & deliverables inventory | A reference list of masters and deliverables — the screeners and how to stream them live in the secure video data room setup, not here |

Two notes. The masters themselves don't go in the diligence room — buyers value rights and condition, not raw files, so a watermarked screener and an inventory are enough; the file-handling is the companion post's job. And buyers scrutinize these folders unequally: chain-of-title and the encumbrance schedule drive insurability and monetizable value, then residuals/participations and music clearances drive net cash flow. Put your preparation hours there. On Peony, auto-indexing on the Data Room plan classifies and structures thousands of title documents so you're not hand-building every folder, and granular per-file permissions let you release title-level detail in stages.

How do you run diligence for several studio and PE bidders at once?

One room, many walls — give each bidder its own visitor group, and never use a shared folder or spin up a separate room per bidder. This is the One Room, Many Walls pattern I wrote up for competitive auctions, and it applies cleanly to a catalog process. Each group gets isolated documents, its own NDA gate, its own tracked links, and its own audit trail, so no bidder can see that any other exists.

That invisibility matters more in entertainment than almost anywhere else, for a reason specific to this market: your rival bidders are often also your live licensing counterparties. The streamer diligencing your catalog this month is the same streamer you're negotiating a library license with next month, and the title-level economics they see in your room are competitive intelligence in both conversations. Walling each bidder off isn't just auction hygiene; it's protecting your licensing leverage.

Stage the disclosure as bidders get serious — the manifest and summary economics to the broad field, then title-level chain-of-title and encumbrance detail to the shortlist, then sensitive participation statements to the lead bidder and its clean team. Route every question through a moderated Smart Q&A workflow so nothing one bidder asks is visible to another and nothing publishes until you approve it. If you need physically separate Q&A channels per bidder inside one room, that's a Peony Enterprise capability; on every other tier the moderated workflow still prevents cross-bidder leakage because answers are never auto-broadcast.

How do you keep the sale confidential from talent, guilds, and the trades?

Treat confidentiality as valuation protection, because a catalog leak detonates on three fronts at once — the Three-Front Leak:

- Talent and guilds. Participation and residual terms are personal and sensitive; a leak about who holds points or what a title actually earns can damage relationships you depend on and complicate guild dynamics.

- Live licensing counterparties. As above, your title-level pricing is competitive intelligence to the streamers and distributors you're actively negotiating with — a leak weakens your hand at the table.

- The trades. Variety, Deadline, and The Hollywood Reporter exist to find exactly this story, and an "[Studio] explores library sale" headline moves the narrative before you're ready, spooking partners and signaling weakness.

The discipline is the same one that works on any leak-sensitive deal, sharpened for this market. Keep the working group tight — owner/CFO, counsel, banker — and code-name the project. Never email screeners or financials; an emailed file is an uncontrolled, unrevocable copy and the number-one leak vector. Share only through a room with NDA gates, per-bidder isolation, and dynamic per-viewer watermarks that stamp every page and every video frame with the viewer's email, IP, and timestamp, rendered server-side so they can't be cropped out — so a leaked screener or document identifies the exact bidder who leaked it. Add screenshot protection (Business) and Screenshield's deeper screen-capture blocking (Data Room), and watch page-level analytics for the tell — a "bidder" reading only your crown-jewel titles, or a login from a newsroom's network. The room can't make a leak impossible, but it makes every leak attributable, and an attributable leak mostly doesn't happen. I went deep on the analog-hole version of this — the phone-camera problem — in stopping phone photos of documents.

What's the best data room for a film or TV catalog sale?

Segmented honestly, because the right answer depends on who's running your process:

| Capability | Peony | Datasite | Intralinks | Firmex | Ansarada |

|---|---|---|---|---|---|

| Title-level auto-indexing | Yes (Data Room) | Partial | Partial | No | Yes |

| Per-bidder isolation (groups) | Yes (Business) | Yes | Yes | Yes | Yes |

| Dynamic per-viewer watermarks | Yes (Data Room) | Yes | Yes | Yes | Yes |

| Screen-capture blocking | Yes (Screenshield, Data Room) | Yes | Yes | Limited | Limited |

| Walled per-group Q&A threads | Enterprise | Yes | Yes | Yes | Yes |

| Pricing shape | Flat per admin | Metered per deal | Metered per deal | Per deal | Metered |

| Indicative cost, one process | $52–64/admin/mo | tens of thousands | tens of thousands | ~$5–10K/deal | $479+/mo entry |

How to read it. If a bulge-bracket bank runs a full sale of a major library, it will probably put you on Datasite or Intralinks, and that's a defensible default — they're built for banker-run processes with service teams attached, and the bank's staff already knows the tooling. Pay the metered cost knowingly. (As you compare "alternatives," know that Datasite acquired Firmex in 2021 and Ansarada in 2024 — three of the five logos here are one company.) If the owner's office or a boutique advisor runs the process — which describes most indie and mid-market catalog sales — the job is a title-structured room with per-bidder walls and watermark-everything at a flat, predictable price, and that's the lane Peony is built for: SOC 2 Type II certified, used by 6,800+ teams, live the same afternoon your advisor makes the first call. Where Peony honestly loses: if you need walled per-bidder Q&A threads on a standard tier (Firmex's coordinator workflow is genuinely strong, and on Peony that's an Enterprise feature), or a vendor-staffed team to run the room for you on a $500M+ banker-led process.

The advisors who actually run these deals are worth knowing too. On the 2026 Paramount Skydance–WBD deal, Moelis advised Netflix on its withdrawn bid; Centerview and RedBird led for Paramount — with BofA Securities, Citi, M. Klein & Company, and LionTree alongside, and Barclays advising Paramount's special committee; and Allen & Company, J.P. Morgan, and Evercore advised WBD. Those are the franchises that run media library and studio sales, and advisory-fee mechanics scale the way I broke down in M&A advisor fees.

| Your situation | Best choice | Why |

|---|---|---|

| Indie/mid-market catalog, owner- or boutique-run, 2–6 bidders | Peony (Data Room, $52) | Title-level auto-indexing + per-bidder walls + watermarks, flat price |

| Banker-run sale of a major library, full service team | Datasite / Intralinks | Built for bank-led mega-processes; your bank already runs them |

| Walled per-bidder Q&A threads required on a standard tier | Firmex | Its Q&A coordinator workflow is the strongest standard-tier version |

| Library recap / royalty-fund process with a multi-deal pipeline | Peony (Deal Team, $64) | Flat per-admin across unlimited rooms; one room per target |

| $100B+ regulated mega-merger with bespoke antitrust workstreams | Datasite / Intralinks | Enterprise compliance tooling and staffing fit the deal size |

How much should the data room cost for a catalog sale?

A few hundred dollars a month, not five figures — if you avoid metered pricing, because a catalog sale is the worst-case shape for a meter. The process runs long (often 6–12 months for a document- and rights-intensive library), the room is enormous (thousands of title-level documents), and parallel bidders multiply access — and per-page, per-user, and per-GB models price every one of those in. Firmex typically lands around $5,000–10,000 per deal; Datasite and Intralinks commonly reach the tens of thousands for a single process; Ansarada's metered entry starts around $479/month ($244 on a 12-month term). Flat-rate removes the variables: Peony's Data Room plan is $52/admin/month (billed annually) with unlimited rooms, storage, and bidders, and the M&A-grade Deal Team plan is $64/admin/month — so two admins on a six-month process spend roughly $600 total. (The full math on why metered billing punishes long, document-heavy processes is in flat-rate vs per-GB pricing.) Set against an advisory fee that runs into the millions on a real library sale, the room is rounding error — so optimize for predictability and a title-level structure, not for shaving the cheapest possible price.

Frequently asked questions

I run an indie studio — should I sell my film library outright, recapitalize it, or just license it in 2026?

Pick by what you need the cash for and how much control you'll give up. License it if you want recurring income and full ownership: the back-catalog licensing market revived hard after Suits proved a decade-old show could top streaming charts, so a well-cleared library can throw off cash without a sale. Recapitalize (sell a minority stake to a PE or royalty/IP fund) if you need a lump sum to fund new production but want to keep the library and the upside. Sell outright if you want maximum certainty now, you lack the capital to keep exploiting the library, or it's a generational exit. The data-room work is nearly identical for all three — a buyer or a lender diligences the same chain-of-title, encumbrances, and residual liabilities — so the prep you do to sell is the prep you do to recap or to prove the library to a licensee. For a 500-title catalog in the $75M–$150M value range, that prep typically runs three to six months of chain-of-title clean-up and encumbrance mapping regardless of exit path. On Peony, the Data Room plan ($52/admin/month) handles a sale, recap, or licensing process at a flat monthly rate — unlike Datasite or Firmex, whose per-deal metering makes a 12-month licensing arrangement just as expensive as a full sale process.

Who actually buys film and TV libraries — and does a streamer, a PE aggregator, or a royalty/IP fund pay the most?

Three buyer types, and the highest bid depends on who has a strategic use for your specific titles. Strategic buyers — major studios and streamers (Netflix, Amazon MGM, Sony, Paramount Skydance, Disney, NBCUniversal, Lionsgate) — pay the most when your library fills a programming gap or feeds their own platform, because they value it on platform engagement, not just standalone cash flow. Library aggregators and IP roll-ups (Lionsgate has played this role) pay for scale and re-licensing leverage. PE and royalty/IP funds (Blackstone, Apollo/Concord, KKR — proven in music, now reaching film/TV) value the library purely as a recurring-cash-flow asset and tend to pay a disciplined multiple of net licensing revenue, not a strategic premium. Run a process that includes at least one of each type: the strategic competes on fit, the financial buyer sets the cash-flow floor, and the tension between them is what gets you a real price. For a catalog in the $100M–$500M range, running a structured process with three or four pre-signed NDAs typically adds 15–30% to the final price versus a bilateral negotiation — the strategic's platform-value thesis and the PE fund's cash-flow DCF set the range together. Peony's visitor groups (Business, $30/admin/month) wall each bidder into an isolated view: a studio and a PE fund see the same title documents but can't see each other's access trail or NDA status.

I own a 300-title indie catalog and want to understand what a buyer will actually pay — how is a film or TV catalog valued?

On the present value of what every title will still earn — not on what the films cost to make. Three methods stack up. First, title-level 'ultimates': under the film-accounting standard (ASC 926), each title carries an 'ultimate' — the estimate of total revenue it will earn over its full commercial life (generally up to about 10 years for a film). A buyer is really buying the present value of every title's remaining ultimate. Second, a discounted cash flow on the library's recurring licensing and residual income, where the terminal value is large and very sensitive to the discount rate. Third, multiples as a sanity check — a commonly cited rule of thumb is 5–10x annual net licensing revenue, and content businesses often trade around 4–12x EBITDA. The headline you should internalize: deal value is not library value. When Amazon bought MGM for $8.45 billion, it booked the content library itself at about $3.4 billion — the rest was goodwill and optionality. For a 300-title catalog earning $5M/year in net licensing revenue, a 7x multiple produces a $35M indication before condition adjustments — chain-of-title gaps or encumbered prime windows cut that quickly. Peony's page-level analytics on the Data Room plan ($52/admin/month) show which titles buyers spend the most time reviewing — a forward signal of which ultimates are moving the DCF needle in their model, useful for steering the management presentation toward your strongest titles.

How do I prove chain-of-title across hundreds or thousands of titles before a buyer's diligence?

Build a title-by-title chain-of-title file, because a buyer's whole valuation rests on it. Chain-of-title is the unbroken documented ownership trail for each title — from the original source material (book, screenplay, life-story rights) through every writer agreement, assignment, and transfer, plus the copyright registration and a copyright/UCC/lien search. It matters because of a causal chain most first-time sellers underestimate: no clean chain-of-title means errors-and-omissions (E&O) insurers won't issue a policy, and without E&O a distributor or streamer won't take the title — so a title with a broken chain isn't just risky, it's effectively unsellable and gets excluded or steeply discounted. Practitioners organize chain-of-title into five buckets (underlying rights, screenplay, production, music, distribution); structure your data room the same way, per title, and fix gaps before a buyer finds them, because a gap discovered mid-diligence reads as risk across the whole catalog. For a 600-title library where half the underlying-rights files are in decades-old production binders, expect 15–25% of titles to surface some defect on a clean pre-process review — a three- to six-month prep window before the room opens. Peony's auto-indexing on the Data Room plan ($52/admin/month) structures thousands of title folders automatically; unlike Firmex or Google Drive, every time a buyer's lawyer opens a chain-of-title file you see it in the page-level log — a title they revisit three times is the one to pre-cure.

Buyers keep flagging residuals and music/sync gaps — how do I present those obligations without tanking the price?

Disclose them as quantified, scheduled liabilities, not as surprises. Residuals (ongoing WGA/SAG-AFTRA/DGA payments for reuse) travel with the title, and the 2023 strikes added a success-based streaming residual bonus for newer titles and made residual exposure far more scrutinized and better-documented — so buyers now expect a title-level residual schedule and will assume the worst on any title you can't quantify. Music is the other landmine: every title needs both a sync license (the composition) and a master-use license (the recording), and if either expired or was never cleared for all media and territories, the title comes off-market until re-cleared. The move is to bring a residual schedule and a music-clearance matrix (scope, term, territory, expiry per title) into the room on day one, and to make the purchase agreement explicit about which residuals the buyer assumes. A clean, quantified liability gets priced; an unquantified one gets a punitive discount or kills the title. For a 200-title catalog with productions from the 1990s and early 2000s, expect 20–35% of music licenses to need re-clearance for streaming in at least some territories — and pulling accurate residual schedules from guild records typically takes three to four months. Peony's title-structured Data Room plan ($52/admin/month) lets you load the music-clearance matrix and residual schedule as indexed documents inside each title's folder, so a buyer sees the liability number and the clearance status in one click rather than cross-referencing separate spreadsheets.

I'm about to open a data room for my 400-title catalog to three bidders — should I organize it by title, by rights, or by document type?

By title first, then by rights within each title — not by document type. A catalog buyer diligences title by title, so a room sorted into generic 'Contracts' and 'Financials' folders forces them to reassemble each title across folders and signals a disorganized library (which becomes a lower bid). Build a master title manifest as the index, then one folder per title containing its chain-of-title, talent/residual schedule, music licenses, distribution/output agreements, existing licenses (the encumbrance schedule), and title-level revenue/ultimates. Layer permissions on top so you can open the manifest and summary financials to everyone, then release title-level detail to serious bidders. On Peony, auto-indexing and granular per-file permissions on the Data Room plan ($52/admin/month) let you stand up a title-structured room without hand-building every folder, and visitor groups keep each bidder in its own walled view.

Three studios and a PE fund all want to diligence the catalog — how do I give per-bidder access without exposing the whole library?

One room, many walls — give each bidder its own visitor group, never a shared folder or a room per bidder. Each group gets isolated documents, its own NDA, its own tracked links, and its own audit trail, so no bidder can see that the others exist — which matters acutely in entertainment, where a rival studio is often also a live licensing counterparty. Stage disclosure by promoting a group as it gets serious: manifest and summary economics first, then title-level chain-of-title and encumbrance detail, then sensitive participation statements for the lead bidder. Route every question through a moderated Q&A workflow so nothing one bidder asks is visible to another. If you need fully walled, physically separate Q&A channels per bidder inside one room, that's available on Peony Enterprise; on any plan, the moderated workflow keeps questions from leaking because nothing publishes until you approve it.

My catalog has 200 titles but half the prime SVOD windows are locked up — which rights can a buyer actually monetize, and how do I show what's already licensed out?

Give them an encumbrance map: a per-title, per-window, per-territory schedule of what's already licensed, to whom, and until when. This is the single most important document after chain-of-title, because a buyer pays for the windows it can monetize, not for the title count. A library where the prime SVOD and major-territory windows are tied up in multi-year output deals is worth far less than the same titles with open windows, even though the catalog looks identical on paper. Map every title across the standard window cascade (theatrical, PVOD, home entertainment, Pay-1/SVOD, AVOD/FAST, linear) and across territory and language, marking each cell as available or encumbered with its expiry. Output deals — where you've committed future or library titles to a distributor for a term — are the encumbrances buyers most often miss until late, so surface them early. The clean version of this schedule is what separates a credible process from a discounted one. For a catalog where prime SVOD windows are committed through 2026–2027, expect buyers to price those titles at 40–60% of their open-window value. Load your encumbrance matrix as a pinned document inside each title's folder on Peony Data Room ($52/admin/month); page-level analytics then show which titles buyers cross-reference with the encumbrance schedule — revealing which output-deal constraints are weighing most on their model.

How do I keep the sale confidential so talent, guilds, and the trades don't find out?

Shrink the circle, share only through a walled room, and make every page traceable — because a catalog leak hits three fronts at once. It damages talent relationships (participation and residual terms are sensitive), it weakens your hand in live licensing negotiations (your title-level pricing is competitive intelligence to the same streamers who may be bidding), and the trades (Variety, Deadline, THR) will run the story the moment it leaks. Keep the working group tight — owner/CFO, counsel, the banker — and never email screeners or financials; an emailed file is an uncontrolled, unrevocable copy. Share through a data room with NDA gates, per-bidder isolation, dynamic per-viewer watermarks (every page and frame stamped with the viewer's email, IP, and timestamp), and download blocking, then watch page-level analytics for a bidder reading only your crown-jewel titles. The room's job here is deterrence and attribution: a leak you can trace to one bidder is a leak that mostly doesn't happen. For a sale where the lead bidder is also your largest current licensing counterparty, a single leaked title-level financial is a negotiating liability across two simultaneous relationships. On Peony Business ($30/admin/month), NDA gates and per-bidder isolation lock down the room; Data Room ($52/admin/month) adds dynamic watermarks that stamp every page server-side with the viewer's identity and timestamp plus Screenshield screen-capture blocking — something Google Drive and Dropbox offer no equivalent of at any price.

I'm running a quiet sale of a 300-title catalog through a boutique advisor — what's the best virtual data room for a film or TV catalog sale?

Match the room to who's running the process. If a bulge-bracket bank is running a full sale of a major library, it will likely default to Datasite or Intralinks — built for bank-led mega-deals with service teams attached, at a metered cost in the tens of thousands per process (worth knowing as you compare 'alternatives': Datasite also owns Firmex and Ansarada, so several names on the standard shortlist are one company). If the owner's office or a boutique advisor is running a quiet sale of an indie or mid-market catalog — most library deals — a flat-rate room with per-bidder walls and a title-level structure does the actual job: auto-indexing for thousands of title folders, granular per-file permissions, dynamic watermarks, Screenshield screen-capture blocking, NDA gates, page-level analytics, and moderated Q&A. That's Peony's lane: $52/admin/month on the Data Room plan, SOC 2 Type II certified, used by 6,800+ teams. The honest rule: take the bank's default for a banker-run mega-deal; take the flat-rate specialist when you're running it yourself and want predictable cost across a long, document-heavy process.

My advisory process will run 9–12 months with three parallel bidders and thousands of title documents — how much should the data room cost, and is flat-rate cheaper than Datasite or Intralinks?

A catalog sale is the worst-case shape for metered pricing: a long process (often 6–12 months), thousands of title-level documents, and several parallel bidders. Per-page and per-deal platforms price all three in — Firmex typically runs about $5,000–10,000 per deal, and Datasite or Intralinks commonly reach the tens of thousands for a single process. Flat-rate pricing removes the meter: Peony's Data Room plan is $52/admin/month (billed annually) with unlimited rooms, storage, and bidders, and the M&A-focused Deal Team plan is $64/admin/month (annual, minimum 4 admins) — so a six-month process with two admins runs a few hundred dollars total. Against an advisory fee that runs into the millions on a real library sale, the room is rounding error either way; what flat-rate buys you is the certainty that adding a fourth bidder or a fifth month never creates an invoice conversation mid-deal.

We found chain-of-title defects in about 15% of our titles during pre-process prep — will these actually kill the deal, or just discount it?

Both happen, and which one depends on whether the gap is curable. An expired or narrow rights window usually discounts: the buyer prices the title as if those windows don't exist until re-cleared, so a music license that lapsed in some territories just lowers that title's contribution. A broken chain-of-title is more dangerous, because it can make a title uninsurable — and an uninsurable title is effectively unsellable, so it gets carved out of the deal entirely rather than discounted. The pattern across recent deals is that a content library's price is strategy- and condition-dependent, not fixed: Hasbro paid roughly $4 billion for eOne in 2019 and sold its film/TV library for about $500 million in 2023. You don't control the licensing cycle, but you do control whether your rights documentation is clean — so the highest-return prep before a sale is curing chain-of-title and re-clearing lapsed music, title by title, before a buyer's lawyers find the gaps for you. For a 400-title catalog where 12% of titles carry a chain-of-title defect, expect those titles to be carved out entirely unless you cure them before the buyer's E&O insurability test. Peony's auto-indexing on the Data Room plan ($52/admin/month) flags which title folders are missing a chain-of-title file before any bidder opens the room — a pre-cure window that Firmex's and Datasite's generic folder structures don't surface automatically.

Related reading

- Secure video data room — the file-handling companion: how to stream 4K screeners to buyers without handing over the masters

- Data room for a sports team minority-stake sale — the other media/entertainment deal type, with league-approval and leak mechanics

- Best data room for multiple bidders — the One Room, Many Walls playbook for running parallel buyers

- Stop phone photos of documents — why per-viewer watermarks are the only control that survives a camera on a screener

- The M&A data room guide — the generic folder tree this post extends with film/TV-specific layers

- M&A advisor fees — how advisory fees scale on a process like a library sale

- How to prepare for due diligence — the readiness sprint before the room opens

- Flat-rate vs per-GB VDR pricing — why metered billing punishes long, document-heavy processes

- Data room for investors — multi-party access patterns for fundraising and recaps

Sell the library, not the story before you're ready. Open a title-structured data room on Peony or see how visitor groups wall off each bidder.

About the author: Sean Yu is the co-founder of Peony, the data room platform used by 6,800+ teams across M&A, due diligence, fundraising, and investment workflows. Before Peony, Sean spent his career on the deal side — M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries at Target Global — running and supporting sell-side, growth, and LP-fundraising processes across software, healthcare, and industrials in North America and Europe. He studied Biomedical Engineering at Imperial College London on a full scholarship and graduated with first-class standing before dropping out to build companies. Sean is also a co-founder of Gingercontrol, an AI-native trade-compliance platform that raised $2.1M. He advises a SaaS company at $20M ARR and Lucida Capital, a $35M AUM hedge fund and market maker. Contact: sean@peony.ink • LinkedIn.