Oil & Gas Farm-Out Data Room: How to Structure It (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Last updated: May 2026

Quick answer: An oil and gas farm-out data room follows a 7-step workflow — pre-marketing teaser plus heads-of-terms, Phase I release (operator-tier full disclosure), indicative bid round, Phase II release (full pre-stack seismic plus EPC bid pack), final binding bid plus Farm-In Agreement negotiation, conditions precedent satisfaction, and closing with deed of assignment. Documents gate across the 4-tier farm-out access model — operator (T1, full), non-operating JV partner / IOC bidder (T2, JOA-controlled), state partner / NOC (T3, PSC carve-out), and project finance lender (T4, diligence-tier through IESC plus technical, legal, market advisors). Typical timeline: 16 to 28 weeks for international upstream; 9 to 14 months for FID-stage LNG farm-outs.

I run Peony, a data room platform. The workflow questions in this post come from a year of working with sell-side IR teams at offshore LNG developers, IOC bidder corp-dev evaluating PSC carve-outs, NOC and state-partner legal counsel reviewing the bilateral side-letter tier, ECA underwriting desks at JBIC/KEXIM/UKEF processing pre-FC diligence, and outside Farm-In Agreement counsel marking up AIEN 2019 templates. The question that recurs across every one of these seats: what's the actual workflow, and at which step do I gate which document to which counterparty without breaking JOA partition integrity?

The platform comparison anchor names the ten platforms; the 42-document checklist catalogs what goes in each folder; this post is the workflow playbook deep-dive. The 7-step farm-out workflow + 4-tier access model — operator (T1) / non-operating JV partner / IOC bidder (T2) / state partner / NOC (T3) / project finance lender (T4) — anchors the entire post.

TL;DR — the 7-step workflow plus 4-tier access model defines the playbook:

- Step 1 — pre-marketing teaser plus heads-of-terms (Weeks 0 to 2 to 3): non-confidential teaser to long-list, NDA-signed counterparties get CIM, pre-emption notices served in parallel.

- Step 2 — Phase I data room release (Weeks 2 to 3 through 6 to 8): full PSC, full JOA with COPAS, indicative reserves at 1P/2P/3P, post-stack seismic crops, file mass approximately 5 to 25 GB.

- Step 3 — indicative bid round plus Q&A (Weeks 6 to 8 through 10 to 12): non-binding offers, structured Q&A, short-list 3 to 6 bidders.

- Step 4 — Phase II data room release (Weeks 10 to 12 through 18 to 22): full pre-stack 3D SEG-Y (120 GB to 5.8 TB per wide-azimuth survey per SEG Wiki Open Data and SEG-Y Rev 2.0 specification, March 2017), full LAS, EPC bid pack at 80 to 150 GB, file mass 80 to 200+ GB.

- Step 5 — final binding bid plus FIA negotiation (Weeks 18 to 22 through 22 to 28): AIEN 2019 Model International Farmout Agreement marked up, JOA amendments negotiated.

- Step 6 — conditions precedent (60 to 180 days international, 30 to 90 days US domestic, 6 to 12 months LNG/project-finance): host-government consent, JOA pre-emption waivers, lender approval, antitrust, sanctions, decommissioning re-validation.

- Step 7 — closing (deed of assignment): working interest transfers, closing payments wire, post-closing data room transitions to lifecycle.

- 4-tier access model gates documents — bilateral state-partner side letters (T1 + T3 only), JOA + AFE archive (T1 + T2 only), pre-stack 3D SEG-Y (T1 + T2 Phase II only), ECA term sheets (T1 + T4 only).

- Real-deal anchors (2025-2026): Woodside-Stonepeak Louisiana LNG ($5.7B carry, closed June 25 2025 per Woodside ASX); Cenovus-BP Bay du Nord (announced June 2022, regulator-approved April 2023, FID anticipated 2027 per CBC News and Energy Mix); Mitsubishi-Aethon Haynesville ($5.2B equity, ~$7.5B EV with $2.33B debt assumption per Mitsubishi press release / World Oil / CNBC / Natural Gas Intel / ChemAnalyst, January 16 2026); offshore LNG developer running farm-out at FID stage to a major plus state partner plus project finance lender (public market context: Twinza Pasca A FEED entered February 2025, FID anticipated mid-2026, MRDC/Hevehe up to 50 percent interest at US$160 million / K620 million in stages per Business Advantage PNG 2025 / PNG Business News 2025 / OGJ 2025 / Argus Media 2025).

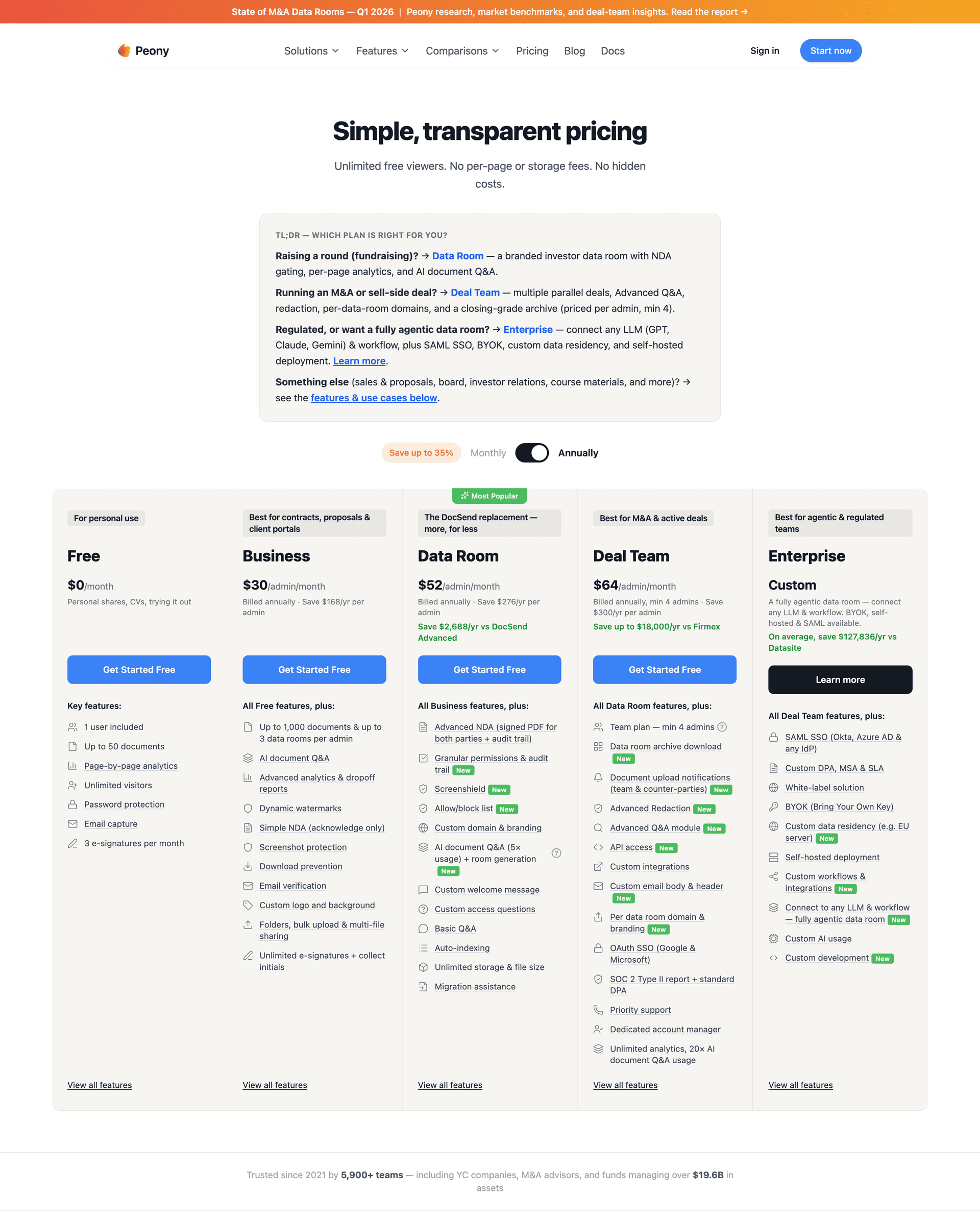

- Peony Data Room at $52/admin/month ships NDA gates, dynamic watermarks, screenshot protection, visitor groups, page-level analytics, and unlimited storage with no per-file cap — see the oil and gas data room platform comparison for the head-on cost analysis versus Datasite ($50,000 to $80,000 per deal at $0.40 to $1.00 per page per Capterra-aggregated buyer data, 2026), Intralinks (custom quote $10K to $200K+/yr), and Drooms NXG (European GDPR procurement-default).

The FID cliff — defined in the cluster anchor post as the document-mass plus counterparty-count surge between FEED and Final Investment Decision — is the diagnostic. The 7-step farm-out workflow plus 4-tier access model is the playbook that survives it.

What is an oil and gas farm-out data room?

An oil and gas farm-out data room is the structured document repository that supports the assignment of working interest in an upstream license, PSC, or operating agreement from one operator to a counterparty — typically a major, NOC, IOC, or PE/infrastructure fund — in exchange for cash, carry, or a combination of consideration structures. The defining feature that separates a farm-out data room from a generic M&A data room is the 4-tier farm-out access model — operator (T1), non-operating JV partner / IOC bidder (T2), state partner / NOC (T3), and project finance lender (T4) — which gates documents through programmatic permission groups expressing JOA partition rules, PSC confidentiality carve-outs, and Equator Principles 4 lender diligence scope.

The five categories of document that make farm-out data rooms structurally distinct from generic M&A data rooms and the 174-document due diligence checklist:

- Commercial agreements stack — full PSC text plus amendments, full JOA with COPAS accounting procedure, AFE archive with voting trail across multi-year work programs, FOB/DES LNG Sale and Purchase Agreements, pre-emption rights schedule, and bilateral state-partner side letters under the PSC. None of these exist in generic M&A checklists.

- Reserves disclosure tier — SPE-PRMS 2018 v1.03 audited reserves report at 1P/2P/3P (the v1.03 revision was published November 2022 with errata first appearing in v1.02 August 2022 per SPE.org), Canadian NI 51-101 Form 51-101F1 backup under CSA Staff Notice 51-327, SEC Form 10-K reserves disclosure with PV-10 reconciliation at 12-month average price (effective for Form 10-K years ending on or after December 31, 2009 per the SEC Modernization of Oil and Gas Reporting final rule).

- Geological and engineering raw data — pre-stack and post-stack 3D SEG-Y seismic cubes (120 GB to 5.8 TB per wide-azimuth towed-streamer survey per SEG Wiki Open Data and SEG-Y Rev 2.0 specification, March 2017), full LAS well-log archives, reservoir simulation models in Eclipse / CMG / Schlumberger Petrel, and EPC LSTK bid pack at 80 to 150 GB at FID stage.

- Regulatory filings tier — FERC §3 LNG export authorizations and §7(c) certificate filings under the Natural Gas Act for US, NOPSEMA WOMP / Environment Plan / Safety Case for Australia, OPRED PETS / OPEP / PON1 for UK, BSEE filings for US offshore, plus jurisdiction-equivalent regulators in Norway (Petroleum Safety Authority), Brazil (ANP), and Mexico (CNH).

- JOA mechanic ledger — historical AFE archive with voting trail showing operator-distribute → non-operator-review → approve / contest / 'go non-consent' under the JOA's accounting procedure (typically COPAS), plus the historical non-consent ledger and any sole-risk operations under AIEN 2012/2023 or AAPL Form 610-1989 Article VI.B.

Standard M&A checklists were built for corporate M&A — they do not cover the farm-out-specific workflow that runs through 7 named steps spanning roughly 16 to 28 weeks for typical international upstream and 9 to 14 months for FID-stage LNG. The next section breaks down the workflow step-by-step.

What are the 7 steps of an oil and gas farm-out workflow?

The 7-step oil and gas farm-out workflow runs from pre-marketing teaser through working-interest assignment in seven named steps spanning roughly 16 to 28 weeks for typical international upstream farm-out and 9 to 14 months for FID-stage LNG farm-out. Sell-side advisor or operator's corp-dev team owns the data room across all 7 steps; what changes step-to-step is document mass, counterparty count, and access tier. This is the proprietary workflow frame I use to diagnose farm-out data room composition.

The 7-step farm-out workflow at a glance

| Step | Phase | Timing | Document mass | Counterparty count | Access tier active |

|---|---|---|---|---|---|

| 1 | Pre-marketing teaser plus heads-of-terms | Weeks 0 to 2 to 3 | Under 2 GB | NDA-signed long-list (10+) | T1 plus public teaser |

| 2 | Phase I data room release | Weeks 2 to 3 through 6 to 8 | 5 to 25 GB | NDA-signed (5+) | T1 plus T2 Phase I |

| 3 | Indicative bid round plus Q&A | Weeks 6 to 8 through 10 to 12 | 5 to 25 GB | Bidders (5 to 10) plus Q&A | T1 plus T2 Phase I |

| 4 | Phase II data room release | Weeks 10 to 12 through 18 to 22 | 80 to 200+ GB | Short-list (3 to 6 bidders) | T1 plus T2 Phase II plus T3/T4 |

| 5 | Final binding bid plus Farm-In Agreement | Weeks 18 to 22 through 22 to 28 | 80 to 200+ GB | 1 to 2 preferred bidders | T1 plus T2 plus T3 plus T4 |

| 6 | Conditions precedent satisfaction | 60 to 180 days international; 30 to 90 days US domestic; 6 to 12 months LNG | Lifecycle growth | Confirmed buyer plus advisors | T1 plus T2 plus T3 plus T4 |

| 7 | Closing — deed of assignment | Trigger date plus 1 day | Closing memo set | Buyer plus regulators | Lifecycle data room |

Trigger to advance at each step is itemized in the H3 deep-dives below — the seismic-data NDA pattern bites hardest at the Step 3-to-Step 4 transition where the file mass jumps roughly 10× and the counterparty universe collapses to a short-list.

Step 1 — pre-marketing teaser plus heads-of-terms (Weeks 0 to 2 to 3)

In Step 1, the operator or sell-side advisor circulates a 4 to 10 page non-confidential teaser to a curated long-list of plausible counterparties. Interested parties sign a mutual confidentiality agreement (CA / NDA). Some farm-outs publish a heads-of-terms (HOTs) outline at this stage to set expectations on consideration structure (cash plus carry plus premium per AIEN 2019 Model International Farmout Agreement Article 3 — Consideration).

Documents added (Phase 1 release):

- Non-confidential teaser (PDF, public)

- Mutual NDA template (with carve-outs for existing seismic-data licensors)

- Process letter Phase I (timetable, bid format, governing-law election)

- Confidential Information Memorandum (CIM) — typically 50 to 120 pages, gated to NDA-signed parties

- Initial geological / commercial summary deck

File mass: under 2 GB.

Trigger to advance: sufficient NDA-signed counterparties (typically 5 or more) confirm interest. Note: existing JOA pre-emption rights are a separate gating event under most international JOAs (AIEN 2023 Model JOA Article 12, AAPL Form 610-1989 for US domestic) — operator must serve formal pre-emption notice; existing JV partners have a defined window (typically 30 days for AAPL 610; longer or shorter under negotiated international JOAs) to elect.

Step 2 — Phase I data room release (Weeks 2 to 3 through 6 to 8)

In Step 2, NDA-signed counterparties get access to the Phase I data room — full corporate, commercial, fiscal, and high-level technical documents sufficient to support an indicative non-binding offer (NBO). Proprietary 3D pre-stack seismic and detailed reservoir simulation models are typically NOT in Phase I — gated for short-listed bidders only at Phase II. This is the seismic-data NDA pattern: progressive disclosure across diligence stages.

Documents added:

- Full PSC text plus amendments

- Full JOA with COPAS accounting procedure

- Pre-emption rights schedule

- Indicative reserves report — SPE-PRMS classification at 1P/2P/3P (SPE-PRMS 2018 v1.03 published November 2022 per SPE.org)

- Production history (last 3 to 5 years), opex/capex actual vs budget

- AFE archive summary (typically 50 to 200 individual AFEs)

- Post-stack seismic crops plus well-log summary (LAS subsets)

- EIA / environmental permits (FERC §3 or §7(c) for US, NOPSEMA WOMP / Environment Plan / Safety Case for AU, OPRED PETS / OPEP / PON1 for UK, BSEE filings for US offshore)

- Tax and royalty status, fiscal-stability terms

- Insurance certificates, decommissioning security

File mass: approximately 5 to 25 GB.

Trigger to advance: indicative bid deadline (typically 4 to 6 weeks).

Step 3 — indicative bid round plus Q&A (Weeks 6 to 8 through 10 to 12)

In Step 3, counterparties submit non-binding indicative offers (NBOs). Sell-side advisor runs structured Q&A — written questions submitted via data room Q&A module, answers distributed to all bidders to maintain level playing field. Seller short-lists bidders for Phase II. Typical short-list: 3 to 6 bidders.

Documents added:

- Process Letter Phase II (binding-bid format, exclusivity rules, mark-up expectations on FIA draft)

- Q&A log (indexed by document and topic) — counterparty-anonymized

- Indicative-bid feedback memo

Trigger to advance: short-list confirmed; SPA / FIA draft (typically AIEN 2019 Model International Farmout Agreement as base) shared with short-listed bidders.

Step 4 — Phase II data room release (Weeks 10 to 12 through 18 to 22)

In Step 4, short-listed bidders get Phase II access — full technical archive needed for binding bid. This is where the FID cliff bites. Per SEG Wiki Open Data and SEG-Y Rev 2.0 specification (March 2017), pre-stack 3D seismic cubes routinely range 120 GB to 5.8 TB per wide-azimuth towed-streamer survey — file-mass threshold most legacy VDRs break at.

Documents added:

- Full pre-stack 3D SEG-Y seismic cubes (50 to 200 GB per survey; sometimes 1+ TB)

- Full LAS well-log archive (10 to 50 GB)

- Reservoir simulation model (Eclipse, CMG, or Schlumberger Petrel — 5 to 20 GB)

- Audited reserves report (full SPE-PRMS 2018 v1.03 backup) — DeGolyer & MacNaughton, Netherland Sewell, Ryder Scott, Sproule, GLJ Petroleum Consultants

- NI 51-101 Form 51-101F1 backup (Canadian dual-listed) under CSA Staff Notice 51-327

- SEC Form 10-K reserves disclosure with PV-10 reconciliation at 12-month average price

- Full PSC plus JOA plus AFE archive (all amendments, side letters carved out for state-partner only)

- EPC bid pack at FID (full P&ID set, isometrics, MTOs, EDS package, geotechnical data — 80 to 150 GB)

- FOB / DES LNG SPAs (drafts and executed)

- Project finance model plus sensitivity matrix plus tax model

- ECA financing term sheets (draft)

- Detailed environmental and social impact assessment (ESIA per Equator Principles 4 framework, July 2020)

- HSE statistics archive (TRIR, DART, LTI, plus IESC site-visit findings)

File mass: 80 to 200 GB at FID-stage; can hit 300+ GB for multi-asset packages.

Trigger to advance: binding bid deadline.

Step 5 — final binding bid plus Farm-In Agreement negotiation (Weeks 18 to 22 through 22 to 28)

In Step 5, bidders submit binding offers with marked-up FIA (typically AIEN 2019). Seller selects preferred bidder. Negotiation commences on definitive documents — FIA, JOA amendments, and (state-partner-involved transactions) tripartite or quadripartite shareholders' agreement.

Two AIEN-2019 consideration structures: (a) cash payments — past costs plus premium reflecting asset value; (b) carry — disproportionate future spending on seismic, exploration, or development.

Real archetypes (2022 to 2025 deal references):

- Cenovus → BP Bay du Nord 2022: C$600M cash plus C$600M maximum contingent oil-price-linked payment (expiring after two years), structured as a portfolio swap where BP transferred its 50 percent Sunrise oilsands interest to Cenovus and Cenovus transferred its 35 percent Bay du Nord interest to BP per BP and Cenovus press releases, June 13 2022 (announced June 2022, regulator-approved April 2023, FID anticipated 2027).

- Woodside → Stonepeak Louisiana LNG 2025: Stonepeak provides $5.7B carry — funding 75 percent of capex in 2025 and 2026 — for a 40 percent stake per Woodside ASX announcement and Stonepeak press release, June 25 2025; Woodside received approximately $1.9B closing payment reflecting Stonepeak's 75 percent share of capex incurred since the January 1 2025 effective date.

Documents added:

- Marked-up FIA (multiple versions during negotiation)

- Disclosure schedules (warranty exceptions, known liabilities)

- Marked-up JOA amendments (or back-to-back novation)

- Side letters (operator commitments, technical-service agreements, transition services)

Step 6 — conditions precedent (Weeks 22 to 28 onward; 60 to 180 days international, 30 to 90 days US domestic, 6 to 12 months LNG/project-finance)

In Step 6, the parties work through the conditions precedent stack between binding-bid signing and closing.

Typical CPs:

- Host-government / regulatory consent — for PSC-fiscal-regime deals, NOC must approve working-interest assignment. Usually longest-running CP.

- Existing JOA partner pre-emption-rights waiver or expiry — AAPL Form 610-1989 sets 30-day pre-emption window; international JOAs typically negotiated 30 to 60 days.

- Lender approval — change-of-control or asset-sale consent rights from project-finance lender or buyer's reserve-based lending. For LNG/project-finance under Equator Principles 4 (July 2020), Independent Environmental and Social Consultant (IESC) often re-validates buyer's ESG fitness as CP.

- Antitrust / competition clearance — US HSR, EU Merger Reg, equivalent national filings.

- Sanctions clearance — particularly post-2022; AIEN 2023 introduces a new economic-sanctions regime not in the 2012 version.

- Decommissioning security adequacy (UKCS / NCS / mature offshore) — buyer's decommissioning trust adequacy re-validated by regulator (NSTA UK, Petroleum Safety Authority Norway, BSEE US offshore).

Documents added:

- Government consent letter (state / NOC)

- JOA pre-emption waiver notices from existing partners

- Lender consent letters (operator-side and buyer-side)

- Antitrust / competition filings plus clearance letters

- Sanctions diligence sign-off

- Decommissioning security re-validation

Step 7 — closing plus completion (deed of assignment / working-interest transfer)

In Step 7, with all CPs satisfied or waived, parties execute the Deed of Assignment transferring working interest. US domestic: BLM (federal lands) plus state regulator plus title-records system. International: host-government petroleum ministry / regulator plus JOA partner registry. Cash plus closing payments wired; contingent-payment mechanics activate.

Documents added:

- Executed Deed of Assignment

- Closing memorandum (mutual sign-off on CP satisfaction)

- Wire confirmations and completion accounts

- Updated JOA partner registry

- Recorded title at relevant regulator(s)

- Tax filings (transfer taxes, stamp duties)

Post-closing data room state: transitions from transactional artifact to lifecycle data room — buyer retains read-only access, operator continues running JV data room for AFE / work-program / production reporting, lender disbursement tranches keep diligence access live across the 14-month FID-to-FC window for LNG.

Total workflow length: typical international upstream farm-out runs 16 to 28 weeks (4 to 7 months); FID-stage LNG farm-out runs 9 to 14 months end-to-end including CP tail. Compressed cycles (Woodside-Stonepeak's 11-week binding-bid-to-closing window) are exceptional — driven by pure-carry consideration structures and parallel Equator Principles 4 IESC review, not the typical pattern.

What is the 4-tier farm-out access model?

The 4-tier farm-out access model is the proprietary access frame I use to gate documents in farm-out data rooms — operator (T1), non-operating JV partner / IOC bidder (T2), state partner / NOC (T3), and project finance lender (T4). Most generic VDRs ship flat admin/collaborator/viewer hierarchies, which collapse on JOA partition rules. The 4-tier model is what makes a farm-out data room structurally distinct from a generic M&A data room. Midstream pipeline M&A uses a parallel 4-tier access model adapted for FERC counsel, throughput counterparties, and ROW landowners — see the midstream pipeline acquisition data room playbook for the 4-Tier Midstream M&A Access Model and how it differs from upstream farm-out gating.

Tier 1 — operator (full data, no gating)

Who: operator deal team, sell-side advisor, operator's external counsel, reserves auditor (DeGolyer & MacNaughton, Netherland Sewell, Ryder Scott, Sproule, GLJ Petroleum Consultants), financial advisor.

Sees: everything. Full pre-stack seismic, full LAS, full PSC plus JOA plus AFE archive, all bilateral side letters, all internal financial models, all Q&A, all bidder identities.

Why: operator owns the data, runs the process, bears disclosure liability.

Tier 2 — non-operating JV partner / farmee bidder (JOA-controlled scope)

Who: existing non-operating JV partners with pre-emption rights; confirmed Tier 1 IOC / major / NOC bidders post-short-list.

Sees: all Phase I plus Phase II data except bilateral state-partner side letters. Full PSC, full JOA with COPAS, pre-emption rights schedule, AFE archive (own AFE schedule visible in detail), production history, reserves audit, post-stack and pre-stack seismic, full LAS, EPC bid pack at FID, project finance model, FOB/DES LNG SPAs.

Does NOT see: bilateral side letters between operator and state-partner, competitor bidders' Q&A redlines, internal sell-side margin / fee discussions, runner-up bidder identities.

Why: the AIEN 2012/2023 Model JOA's operating-committee and operator-information articles together define what JV partners are entitled to see. State-partner side letters carry confidentiality carve-outs that override standard JOA disclosure. Per Ashurst's farm-out guidance, JOA partition integrity protects state-partner consent from being unwound.

Tier 3 — state partner / NOC (host-government carve-out access)

Who: host-government petroleum ministry, NOC representatives (Kumul Petroleum PNG, Petronas Malaysia, Sonangol Angola, NNPC Nigeria, KazMunayGas Kazakhstan), state-shareholder SPVs (Hevehe Petroleum Limited / MRDC vehicle in PNG per Business Advantage PNG 2025).

Sees: PSC compliance documentation, local-content reporting, environmental permits, abandonment / decommissioning provisions, state-partner side letters, fiscal-stability terms. Plus state-partner-only commercial side letters walled from T1 IOC bidder view.

Does NOT see: operator-only commercial side letters not relating to state-partner commitments, non-operating JV partner-only AFE detail, competitor bidder identities.

Tier 4 — project finance lender (diligence-tier access through advisors)

Who: commercial bank syndicate energy desk, ECAs (JBIC, KEXIM, US EXIM, UKEF, Bpifrance Assurance Export, Sinosure), multilaterals (IFC, ADB, EBRD), lender's external counsel (Hunton AK, Willkie Farr, White & Case, Latham & Watkins as most-named LNG project-finance counsel), lender's IESC per Equator Principles 4, lender's technical advisor, lender's market consultant.

Sees: cash-flow models, offtake contracts (FOB/DES LNG SPAs), EPC LSTK bid responses plus technical due diligence reports, debt-service projections, environmental and social impact assessments per Equator Principles, EIA and ESIA, completion guarantees, decommissioning security, ECA covenant documents, IESC site-visit reports.

Does NOT see: internal seller financial-margin / closing-bid mechanics, competitor bidder identities, JOA carry / non-consent provisions in detail (T4 only gets summary), state-partner bilateral side letters except those material to lender enforcement.

Access matrix — the load-bearing visualization

| Document type | T1 Operator | T2 Non-op JV / IOC bidder | T3 State partner / NOC | T4 Lender |

|---|---|---|---|---|

| Teaser plus CIM | Full | Full | Summary | Summary |

| Full PSC text | Full | Full | Full | Full |

| Bilateral state-partner side letters | Full | Walled | Full | Material-only |

| Full JOA with COPAS | Full | Full | Operator-relevant only | Summary |

| AFE archive | Full | Own plus voting trail | None | Summary |

| Pre-emption rights schedule | Full | Full | Full | Full |

| Pre-stack 3D SEG-Y | Full | Full (Phase II) | Summary | Technical advisor only |

| Full LAS archive | Full | Full (Phase II) | Summary | Technical advisor only |

| Reservoir simulation model | Full | Full (Phase II) | Summary | Technical advisor only |

| SPE-PRMS audited reserves | Full | Full (Phase II) | Full | Full |

| NI 51-101 / SEC 10-K backup | Full | Full | Full | Full |

| EPC LSTK bid pack | Full | Full (Phase II) | None | Technical advisor only |

| FOB / DES LNG SPAs | Full | Full (Phase II) | Full | Full |

| Project finance model | Full | Full (Phase II) | Summary | Full |

| ECA term sheets | Full | None | None | Full |

| ESIA / Equator Principles pack | Full | Full (Phase II) | Full | Full plus IESC site visit |

| Decommissioning security | Full | Full (Phase II) | Full | Full |

| Q&A log | Full | All bidders see same Qs | None | None |

| Bidder identities | Full | Anonymized to other bidders | Full | None |

The matrix is the citation-grade view of what each tier sees in a properly configured farm-out data room. Peony Data Room at $52/admin/month expresses every row of this matrix through programmatic visitor groups — without manual permission resets per counterparty and without per-page billing inflating the Phase II SEG-Y mass.

How do JOA carry and non-consent provisions gate in a farm-out data room?

JOA carry and non-consent provisions gate to T1 (operator) full mechanics, T2 (non-operating JV / farmee) for own carry plus partition-protected views of others, T3 (state partner) typically summary only at PSC-fiscal-regime level, and T4 (lender) full visibility where material to debt-service modeling. The two relevant model JOA forms are AAPL Form 610-1989 for US domestic onshore (de facto industry standard, Article VI.B governs non-consent) and AIEN 2023 Model International Joint Operating Agreement for international (the Association of International Petroleum Negotiators rebranded to the Association of International Energy Negotiators in 2022 — formally unveiled at the 2022 London Summit — with the 2023 Model JOA the first model contract published under the new AIEN name on February 16, 2023, rewriting decommissioning provisions, introducing a new economic-sanctions regime post-2022, enhancing anti-bribery, adding optional GHG emissions provisions, and transitioning the reference rate from LIBOR to SOFR per V&E and Bracewell guidance, 2024).

Carry provisions

Definition: farmee's commitment to fund disproportionate share of future expenditures (seismic, exploration, or development). Per AIEN 2019 — denominated in scope (e.g., "100 percent of seismic to $50M cap" or "75 percent of construction capex 2025 and 2026").

Carry archetypes from 2022 to 2025 deals:

- Cenovus → BP Bay du Nord (announced June 13 2022, regulator-approved April 2023 per CBC News and Energy Mix; FID anticipated 2027): C$600M cash plus C$600M maximum contingent oil-price-linked payment expiring after two years — structured as a portfolio swap (BP's 50 percent Sunrise oilsands ↔ Cenovus's 35 percent Bay du Nord) per BP and Cenovus press releases June 13 2022; hybrid cash-plus-swap rather than pure carry.

- Woodside → Stonepeak Louisiana LNG (announced April 7 2025, closed June 25 2025 per Woodside ASX and Stonepeak press release; closed 11 weeks after announcement): pure carry — Stonepeak provides $5.7B carry funding 75 percent of capex in 2025 and 2026 for a 40 percent stake; Woodside received approximately $1.9B closing payment reflecting Stonepeak's 75 percent share of capex incurred since January 1 2025 effective date.

Visibility: T1 full mechanics; T2 farmee full; other T2 partners get summary plus AFE notification triggers; T3 summary at PSC-fiscal-regime level; T4 full visibility material to debt-service modeling.

Non-consent provisions

Definition: what happens when one or more JOA partners decline to participate in a proposed operation. Under AAPL Form 610-1989 Article VI.B, a non-consenting party avoids cost contribution but forfeits production-revenue share until consenting parties recoup investment plus risk premium.

Penalty multipliers (industry-standard ranges, varying by basin and operation type per Energy Law Journal / Hunton AK / US LegalForms):

- Development wells: 200 to 400 percent

- Exploratory wells: at least 300 percent

- Offshore / deepwater: up to 1,000 percent

Visibility: T1 full mechanics plus historical non-consent ledger; T2 own non-consent history full plus others' summary; T3 typically none; T4 summary if affects loan-covenant calculations.

Sole risk operations

Where the JOC rejects a proposal but a minority partner proceeds at own risk. AIEN 2012/2023 plus AAPL 610: sole-risk parties bear 100 percent cost plus 100 percent upside until recoupment threshold.

The critical data-room test

A data room that exposes the historical non-consent election ledger to a Tier 1 IOC bidder pre-confirmation has misconfigured permissions and broken JOA partition integrity. This is the citable test for whether the seller has gated correctly. Peony Data Room at $52/admin/month uses programmatic permission groups expressing the 4-tier model precisely because flat hierarchies fail this test. For the 100GB+ pre-stack SEG-Y file-size mechanics that compound the gating problem on legacy VDRs with file-size caps, see the horizontal sibling Tested: 10 Data Rooms for Large Files (With NDA Gates).

How do pre-emption rights and conditions precedent affect farm-out timeline?

Pre-emption rights gate at Step 1 of the 7-step workflow as a parallel process — not at Step 3 or Step 5 where many sellers default — because most modern AIEN 2023 / AAPL 610-1989 JOAs require formal pre-emption notice to existing JV partners before circulating the teaser to a wider counterparty universe. Conditions precedent gate at Step 6 and typically run 60 to 180 days for international upstream, 30 to 90 days for US domestic, and 6 to 12 months for LNG / project finance deals.

Pre-emption rights in detail

Pre-emption rights are a common feature of farm-outs (Ashurst, "Navigating pre-emption rights in oil and gas transactions"). The window difference between AAPL Form 610-1989 (US domestic) and AIEN 2023 (international) drives the front-end of the workflow architecture:

- AAPL Form 610-1989: 30-day pre-emption window. JV partners have 30 calendar days from formal notice to elect whether to take their pro-rata share at the proposed price/terms. US domestic deals run a tight Week 0 to Week 4 pre-emption clock — fold the pre-emption notice into the same week as teaser distribution.

- AIEN 2023 international JOAs: typically negotiated 30 to 60 days, sometimes longer for state-partner involved transactions where consent layers stack. International deals (including Asian buyers for Canadian heavy-oil packages needing host-government consent) run a 60-day to 90-day pre-emption-plus-consent stack at the front of the workflow.

The pre-emption rights schedule populated for the data room must show every JV-partner notice obligation and the operator's contractual response window — gated to all counterparties (T1 through T4) because pre-emption rights are public-facing under the JOA's information article.

Conditions precedent in detail

The Step 6 CP stack typically spans six categories:

- Host-government / regulatory consent — usually longest-running CP. PSC-fiscal-regime deals require NOC approval of working-interest assignment.

- JOA partner pre-emption waiver or expiry — formal waivers from existing partners or expiry of the pre-emption window (the Step 1 clock running to ground).

- Lender approval — change-of-control or asset-sale consent rights from project-finance lender or buyer's reserve-based lending. For LNG under Equator Principles 4, the IESC re-validates buyer's ESG fitness.

- Antitrust / competition clearance — US HSR, EU Merger Reg, equivalent national filings.

- Sanctions clearance — post-2022 critical; AIEN 2023 introduces a new economic-sanctions regime not in the 2012 version. Sanctions diligence sign-off is required before closing on any farm-out where the buyer has counterparty exposure to sanctioned jurisdictions or persons.

- Decommissioning security re-validation — UKCS / NCS / mature offshore. Buyer's decommissioning trust adequacy re-validated by regulator (NSTA UK, Petroleum Safety Authority Norway, BSEE US offshore).

Real-deal CP timelines

- Cenovus → BP Bay du Nord: announced June 2022, regulator-approved April 2023 per CBC News and Energy Mix — the regulator-consent CP took roughly 10 months. FID is still pending mid-2026 with BW Offshore selected as preferred FPSO bidder late 2025 per CBC and Offshore Technology.

- Woodside → Stonepeak Louisiana LNG: announced April 7 2025, closed June 25 2025 per Woodside ASX — exceptional 11-week window driven by pure carry consideration (no large closing-payment wire that triggers the full antitrust / sanctions / lender-consent stack) and parallel Equator Principles 4 IESC review.

- Mitsubishi → Aethon Haynesville: announced January 16 2026, closing Q1 Japanese FY2026 (April to June 2026) per Mitsubishi press release / World Oil / CNBC / Natural Gas Intel / ChemAnalyst — the change-of-control / antitrust stack is the primary CP driver; Aethon Energy Management retains right to buy back up to 25 percent.

The data room implication: for a 9-to-14-month FID-stage LNG cycle, the data room transitions from transactional to lifecycle at the announcement-to-closing transition and the T4 lender-tier audit trail must preserve granularity across the full window. Peony Data Room at $52/admin/month handles both compressed-cycle and lifecycle-cycle workflows — flat per-admin pricing means the cost stays at $260 per month for 5 admins whether the room closes in 11 weeks or runs 14 months, while Datasite and Intralinks bill per-project or per-year subscription that scales with the CP tail.

What documents belong in each access tier?

Documents in a farm-out data room belong to one or more of the four access tiers — operator (T1, full data), non-operating JV partner / IOC bidder (T2, JOA-controlled scope), state partner / NOC (T3, PSC carve-out), and project finance lender (T4, diligence-tier through advisors). The complete document inventory by tier maps to the 42-document checklist across 12 canonical folders, with farm-out-specific gating rules layered on top.

Tier 1 — operator (full)

Every document. Phase I plus Phase II plus side letters plus competitor Q&A redlines plus bidder identities plus sell-side fee letters plus internal memos.

Tier 2 — non-operating JV partner / confirmed bidder

Phase I T2 access:

- Full PSC text plus amendments

- Full JOA with COPAS accounting procedure

- Pre-emption rights schedule (full)

- AFE archive: full visibility into own AFE plus JOA partition integrity for others

- Indicative reserves report (SPE-PRMS 1P/2P/3P)

- Production history (3 to 5 years)

- Post-stack seismic crops plus LAS subsets

- EIA / environmental permits (jurisdiction-specific)

- Tax and royalty status, fiscal-stability terms

- Insurance certificates, decommissioning security

Phase II T2 access (post short-list):

- Full pre-stack 3D SEG-Y seismic cubes (50 to 200 GB per survey)

- Full LAS well-log archive (10 to 50 GB)

- Reservoir simulation model (Eclipse / CMG / Schlumberger Petrel — 5 to 20 GB)

- SPE-PRMS audited reserves report (full backup)

- NI 51-101 Form 51-101F1 (Canadian dual-listed)

- SEC Form 10-K reserves disclosure with PV-10 reconciliation

- Full PSC plus JOA plus AFE archive

- EPC LSTK bid pack at FID (full P&ID set, isometrics, MTOs, EDS package — 80 to 150 GB)

- FOB / DES LNG SPAs

- Project finance model plus sensitivity matrix

- ECA financing term sheets

- ESIA per Equator Principles 4

- HSE statistics archive (TRIR, DART, LTI)

Walled from T2: bilateral state-partner side letters, competitor bidder identities, sell-side fee discussions, runner-up bidder identities.

Tier 3 — state partner / NOC

- Full PSC text plus amendments

- PSC compliance documentation (cost-recovery filings, profit-oil calculations, royalty payments)

- Local-content reporting

- Environmental permits (NOPSEMA / OPRED / BSEE / FERC equivalents)

- Abandonment / decommissioning provisions

- State-partner side letters (full — walled from T2)

- Fiscal-stability clauses plus review notices

- Historical regulatory filings (PETS / OPEP / PON1 / WOMP / Safety Case)

- High-level reserves audit (SPE-PRMS classification level)

Walled from T3: operator-only commercial side letters not relating to state-partner commitments, non-operating JV partner-only AFE detail, competitor bidder identities.

Tier 4 — project finance lender (through advisors)

- Cash-flow models (project finance model plus sensitivity matrix)

- Offtake contracts (FOB / DES LNG SPAs, condensate offtake LOIs)

- EPC LSTK bid responses plus technical due diligence reports (through technical advisor)

- Debt-service projections

- Environmental and social impact assessment per Equator Principles 4

- IESC site-visit reports

- ECA covenant documents

- Completion guarantees plus completion date schedule

- Decommissioning security (parental guarantees, letters of credit, decommissioning trust funds)

- Audit and litigation history (material claims only)

- Sanctions diligence sign-off (post-2022)

- Insurance certificates

Walled from T4: internal seller financial-margin / closing-bid mechanics, non-material litigation, JOA carry / non-consent detail (only summary), state-partner bilateral side letters except material to lender enforcement.

For the full 12-folder canonical doc-tree with sub-folder breakdown and file-size ranges per folder, see the oil and gas data room checklist.

How does a Phase I vs Phase II data room release differ in oil and gas farm-outs?

Phase I and Phase II data room releases differ along three axes: document mass (5 to 25 GB at Phase I vs 80 to 200+ GB at Phase II), counterparty count (NDA-signed long-list of 5+ at Phase I vs short-listed 3 to 6 at Phase II), and document type (corporate plus commercial plus high-level technical at Phase I vs full pre-stack seismic plus EPC bid pack plus reservoir simulation at Phase II). The transition between Phase I and Phase II is the seismic-data NDA pattern — progressive disclosure across diligence stages where teaser data sits in an open lobby, CA-gated material requires a confidentiality agreement, NDA-gated reserves data requires a full NDA, and bid-stage data is gated behind a counterparty-specific watermark.

Phase I release — operator-tier full disclosure

Phase I gates documents that support an indicative non-binding offer (NBO). The defining test is whether a counterparty can build a credible commercial valuation off the Phase I document set without seeing the full pre-stack seismic or the EPC bid pack at FID. Phase I documents include full PSC, full JOA, pre-emption rights schedule, indicative reserves at SPE-PRMS 1P/2P/3P, post-stack seismic crops, LAS subsets, AFE archive summary, environmental permits, tax and royalty status, and decommissioning security overview. File mass at Phase I runs approximately 5 to 25 GB.

Phase II release — technical deep-dive for binding bid

Phase II gates the full technical archive needed for a binding bid — full pre-stack 3D SEG-Y seismic cubes (120 GB to 5.8 TB per wide-azimuth survey per SEG Wiki Open Data and SEG-Y Rev 2.0 specification, March 2017), full LAS archives, reservoir simulation models, SPE-PRMS audited reserves backup, EPC LSTK bid pack at FID (80 to 150 GB), FOB / DES LNG SPAs, project finance model, and ESIA per Equator Principles 4. File mass at Phase II runs 80 to 200 GB at FID-stage and can hit 300+ GB for multi-asset packages or LNG-tier FID where the EPC bid pack alone is 80 to 150 GB.

The seismic-data NDA pattern across phases

| Phase | NDA tier | Reserves data | Seismic data | EPC pack |

|---|---|---|---|---|

| Lobby (pre-NDA) | None — public teaser only | Headline reserves estimate | Basin map only | None |

| CA-gated | Confidentiality agreement | Resource classification summary | Geological summary | None |

| NDA-gated Phase I (T2) | Full counterparty NDA | Indicative SPE-PRMS at 1P/2P/3P | Post-stack crops plus LAS subsets | None |

| NDA-gated Phase II (T2) | Counterparty-specific watermark | Full SPE-PRMS plus NI 51-101 / 10-K | Full pre-stack 3D SEG-Y plus full LAS archive | Full |

| Bid stage (T2) | Watermark plus screenshot block | Bid-stage subset | Bid-stage subset | Full |

Why screenshot protection matters specifically at Phase II: SPE-PRMS proved-developed-producing (PDP) decline curves and NI 51-101 Form 51-101F1 backup are some of the highest-value IP in upstream — leak-sensitive enough that an unwatermarked screenshot of a single PDP curve can shift bid prices in a contested farm-out. Generic file-share platforms (Box, Dropbox, Google Drive) do not ship dynamic watermarks tied to viewer identity or screenshot blocking, so they fail this test outright.

The Phase II file-size cap that breaks legacy VDRs: Datasite caps single files at 10 GB with zip files supported up to 50 GB per Datasite FAQ; Intralinks raised single-file cap to 25 GB across US, Germany, and Australia per Intralinks release notes 2025 — workable for individual reservoir reports but breaks on full pre-stack volumes; Firmex caps drag-and-drop at 10 GB per Firmex documentation. Peony Data Room at $52/admin/month has no per-file cap — pre-stack 3D seismic SEG-Y cubes load in single drag-and-drop operations.

For the file-size mechanics deep-dive on platforms that don't break on 100 GB+ pre-stack SEG-Y, see the horizontal sibling Tested: 10 Data Rooms for Large Files (With NDA Gates).

What does Peony do that legacy oil and gas VDRs don't on the 4-tier farm-out access model?

Peony Data Room at $52/admin/month does three things that legacy oil and gas VDRs do not on the 4-tier farm-out access model: (1) expresses each tier through programmatic visitor groups rather than manual permission resets per counterparty, (2) prices flat per-admin so the cost stays at $260 per month for 5 admins whether the room closes in 11 weeks or runs 14 months across the FID-to-FC window, and (3) ships unlimited storage with no per-file cap so 120 GB+ pre-stack SEG-Y cubes load without splitting through the Phase I-to-Phase II transition. Legacy VDRs (Datasite, Intralinks, Firmex, Drooms) ship the 4-tier security stack at enterprise tier but punish raw seismic and EPC-bid-pack data composition with per-page or per-project billing that turns the FID cliff into a per-deal cost cliff.

What ships on Peony Data Room that legacy oil and gas VDRs either skip, paywall, or charge per-deal for:

- Programmatic visitor groups that express the 4-tier farm-out access model — operator (T1) / non-operating JV partner / IOC bidder (T2, JOA-controlled) / state partner / NOC (T3, PSC carve-out) / project finance lender (T4, diligence-tier) — without manual permission resets per counterparty.

- No per-file cap — full pre-stack 3D SEG-Y cubes (120 GB to 5.8 TB), full LAS well-log archives, complete EPC drawing sets load in single drag-and-drop operations. Datasite caps at 10 GB single-file, Intralinks at 25 GB, Firmex at 10 GB drag-and-drop.

- NDA gates with integrated e-signatures — counterparty must sign before any documents are visible. Same legal enforceability as Datasite's enterprise contracts (ESIGN Act, eIDAS, PIPEDA). Custom NDA template upload supported — your fund counsel's standard, not a generic one.

- Dynamic watermarks — every page (including SPE-PRMS reserves curves and AFE schedules) stamped with viewer name, email, IP, and timestamp. Traceable to the leaker on any leaked SEG-Y or PSC fragment.

- Screenshot protection — blocks captures across desktop and mobile, logs blocked attempts. Required for bid-stage reserves data and EPC bid responses.

- Page-level analytics — exact page-by-page dwell time per viewer, exportable as audit trail. Lender counsel can verify which counterparty reviewed which version of the offtake LOI at which timestamp across the 14-month FID-to-FC window.

- AI document chat — query the entire data room in natural language ("show me every PDP curve in basin X") and get cited answers across LAS files, reservoir model exports, and reserves reports.

- AI auto-indexing — classifies geological reports, financial models, PSC text, and JOA / AFE schedules into deal-ready folders.

- AES-256 encryption at rest, TLS 1.3 in transit, SOC 2-ready, GDPR/CCPA/HIPAA compliant.

What's not on Peony Data Room: enterprise-tier custom-quoted contracts (because pricing is transparent at $52/admin/month); dedicated per-deal project managers (because median setup time is 4 minutes 19 seconds — no PM needed); FERC docket cross-reference workflow (FERC lookup is handled through the standard search rather than a dedicated integration — Datasite's FERC archive support is genuinely stronger for midstream pipeline acquisitions); and the Datasite-branded room expectation some Tier 1 IOC procurement teams default to.

Cost wedge on a representative FID-stage farm-out (5 admins, 14-month FID-to-FC window):

| Platform | 14-month total cost | Pricing model |

|---|---|---|

| Peony Data Room | $3,640 | 5 admins × $52/mo × 14 months flat |

| Datasite (per-page) | $50,000 to $80,000 | Custom-quoted; per-page billing $0.40 to $1.00 per page on Phase II SEG-Y mass |

| Intralinks (per-page or per-project) | $50,000 to $80,000+ | Enterprise tier; pre-built farm-out workflow templates |

| Firmex (per-project) | $5,000 to $15,000 + extension | Per 90-day project; CP-tail extensions billed separately |

| Drooms NXG | $30,000+ | European GDPR procurement-default; quote-based |

For the boutique upstream M&A advisor running 4 to 12 farm-outs per year, the mid-cap E&P running a divestiture, the offshore LNG developer running farm-out at FID stage, or the energy-focused PE / infrastructure fund running 5+ data-heavy oil and gas deals per year, Peony Data Room is the only platform that closes the cost gap to legacy enterprise VDRs without sacrificing the security primitives that gate confidential reserves data, EPC bid responses, JOA carry / non-consent provisions, and PSC bilateral state-partner side letters. For the head-on 12-criteria platform comparison covering single-file cap, NDA gate, dynamic watermark, screenshot block, FERC archive support, and 2026 starting price across Datasite, Intralinks, Drooms NXG, Firmex, and Peony Data Room, see the oil and gas data room platform guide.

FAQ

I'm an MD at a 9-person Houston upstream M&A boutique with a sell-side farm-out mandate at FID stage — what's the 7-step farm-out workflow and at which step do I gate Phase II seismic + EPC bid pack from indicative-bid Phase I bidders?

For your 9-person Houston upstream M&A boutique on a sell-side FID-stage farm-out, the 7-step workflow runs teaser plus heads-of-terms (Step 1, weeks 0 to 2 to 3), Phase I data room release (Step 2, weeks 2 to 3 through 6 to 8), indicative bid round plus Q&A (Step 3, weeks 6 to 8 through 10 to 12), Phase II data room release (Step 4, weeks 10 to 12 through 18 to 22), final binding bid plus Farm-In Agreement negotiation (Step 5, weeks 18 to 22 through 22 to 28), conditions precedent satisfaction (Step 6, 60 to 180 days for international, 6 to 12 months for LNG project finance), and closing with deed of assignment (Step 7). You gate the full pre-stack 3D SEG-Y cubes, full LAS archives, reservoir simulation models, and the EPC LSTK bid pack at 80 to 150 GB at the Step 3-to-Step 4 transition — that is the seismic-data NDA pattern. Indicative bidders see post-stack seismic crops plus LAS subsets plus the SPE-PRMS indicative reserves report at 1P/2P/3P; only short-listed bidders (typically 3 to 6 names after Phase I) get full Phase II access. Peony Data Room at $52 per admin per month expresses this through programmatic visitor groups with dynamic watermarks so each Phase II bidder sees their own watermarked SEG-Y but never the runner-up bidder's Q&A redlines or the bilateral state-partner side letters. Datasite and Intralinks support equivalent gating at enterprise tier ($50,000 to $80,000 per deal) but bill per page on the seismic-heavy mass. The Woodside-Stonepeak Louisiana LNG farm-out (announced April 7 2025, closed June 25 2025 per Woodside ASX and Stonepeak press release) ran exactly this 7-step pattern compressed to 11 weeks from binding bid to closing — driven by a $5.7B carry consideration structure and an Equator Principles 4 IESC site visit completed in parallel with regulatory consent.

I'm head of IR at a junior offshore E&P with one PSC at FID stage running farm-out to a major + state partner + project finance lender — how does the 4-tier access model express in a data room and what specifically gates from state-partner side letter to IOC bidder view?

For your junior offshore E&P running farm-out to a major plus state partner plus project finance lender, the 4-tier farm-out access model expresses in nested permission groups, not flat admin/collaborator/viewer hierarchies. Tier 1 is operator (your deal team, sell-side advisor, external counsel, reserves auditor, financial advisor) — full data including bilateral side letters, runner-up bidder identities, and sell-side fee letters. Tier 2 is non-operating JV partner / IOC bidder (the major bidder plus any existing JV partners exercising pre-emption rights under AIEN 2023 Model JOA Article 12 or AAPL Form 610-1989) — full PSC text, full JOA with COPAS accounting procedure, AFE archive with their own AFE schedule visible in detail, pre-emption rights schedule, post-stack seismic at Phase I and full pre-stack Phase II, EPC bid pack at FID. Tier 3 is state partner / NOC (host-government petroleum ministry, NOC representatives like Kumul Petroleum, Petronas, Sonangol, NNPC, KazMunayGas, or state-shareholder SPVs like Hevehe Petroleum Limited / MRDC vehicle in PNG per Business Advantage PNG 2025) — PSC compliance documentation, local-content reporting, environmental permits, abandonment provisions, and the bilateral state-partner side letters that are walled from T2. Tier 4 is project finance lender (ECAs JBIC/KEXIM/US EXIM/UKEF/Bpifrance Assurance Export/Sinosure, multilaterals IFC/ADB/EBRD, lender's external counsel including Hunton AK / Willkie Farr / White & Case / Latham & Watkins, lender's IESC under Equator Principles 4 July 2020) — cash-flow models, FOB/DES LNG SPAs, EPC LSTK bid responses, debt-service projections, ESIA, completion guarantees, ECA covenant documents. The specific gating test for state-partner side letters: bilateral side letters between operator and state-partner shareholder under the PSC are hard-walled from T2 (IOC bidder) view, full to T3, and material-only to T4. Per Ashurst's farm-out guidance, JOA partition integrity protects state-partner consent from being unwound. Peony Data Room at $52 per admin per month expresses this through programmatic visitor groups — see the oil and gas data room platform comparison for the head-on platform analysis.

I'm corp-dev at an IOC bid team running due diligence on a 25% PSC carve-out farm-in at Phase II — what JOA documents do I need access to, and how do I know the seller has properly walled state-partner bilateral side letters from my view?

For your IOC bid team running due diligence on a 25 percent PSC carve-out farm-in at Phase II, you need full Tier 2 access to the JOA stack — full JOA with COPAS accounting procedure (AIEN 2023 Model JOA for international or AAPL Form 610-1989 for US domestic), AFE archive with voting trail across multi-year work programs, pre-emption rights schedule (AIEN 2023 Article 12 or AAPL 610-1989 typically 30-day window), JOA carry mechanics where present, JOA non-consent ledger showing historical elections under AAPL Form 610-1989 Article VI.B (penalty multipliers run 200 to 400 percent for development wells, at least 300 percent for exploratory, up to 1,000 percent for offshore deepwater per Energy Law Journal / Hunton AK / US LegalForms — industry-standard ranges varying by basin and operation type), sole risk operation history if any minority partner has exercised sole risk, and the disclosure schedules accompanying the FIA. The defining test for whether bilateral state-partner side letters are properly walled from your bid-team view: in a properly configured T2 access tier, you see the full PSC text and the JOA partition for your own AFE schedule but you do NOT see the bilateral side letters between the operator and the state-partner shareholder. If the data room exposes those side letters to a Tier 1 IOC bidder pre-confirmation, the seller has misconfigured permissions and the JOA partition integrity is broken — that is the citable test for whether the seller has gated correctly. Peony Data Room at $52 per admin per month uses programmatic visitor groups expressing the 4-tier farm-out access model precisely because flat hierarchies fail this test — JOA partner #2 sees their AFE schedule and not the bilateral state-partner side letter without manual permission resets per counterparty. See the oil and gas data room checklist for the full 42-document gating matrix.

I'm a credit officer at a multilateral project-finance group reviewing an LNG FID disbursement package with a 14-month FID-to-FC window — what farm-out documents gate to lender (T4) tier and what scopes through the IESC under Equator Principles 4?

For your multilateral project-finance group reviewing an LNG FID disbursement package across a 14-month FID-to-FC window, T4 lender access scopes through five document categories. First, cash-flow models and project finance model with full sensitivity matrix and tax model — needed for debt-service coverage ratio and breakeven analysis. Second, offtake contracts including FOB/DES LNG Sale and Purchase Agreements (drafts and executed) plus condensate offtake LOIs — needed for revenue-side commitment underwriting. Third, EPC LSTK bid responses plus full technical due diligence reports — scoped through the lender's technical advisor, not lender directly. Fourth, ECA covenant documents, completion guarantees, and decommissioning security — direct to lender plus parallel review by lender's external counsel (typically Hunton AK / Willkie Farr / White & Case / Latham & Watkins per published LNG project-finance practice descriptions). Fifth, the Environmental and Social Impact Assessment under Equator Principles 4 (July 2020) plus Implementation Note (September 2020) plus Loan Documentation Guidance (December 2020). The IESC (Independent Environmental and Social Consultant) scope under Equator Principles 4: ESIA review, on-site verification of HSE statistics (TRIR, DART, LTI), human rights diligence per UN Guiding Principles, GHG emissions baseline, biodiversity impact, indigenous-peoples consultation per ILO 169 where applicable, and disbursement-condition re-validation across the 14-month FID-to-FC window. Documents walled from T4: internal seller financial-margin / closing-bid mechanics, runner-up bidder identities, JOA carry/non-consent provisions in detail (T4 only gets summary), state-partner bilateral side letters except those material to lender enforcement. The NextDecade Rio Grande LNG Train 5 FID is the reference scale — positive FID October 2025 with $6.7B financing closed and full notice to proceed issued to Bechtel (PGJ Online, 2025) — that scale of disbursement package routinely involves 12 to 25 financial-institution counterparties (commercial banks plus ECAs plus multilaterals plus DFIs). Peony Data Room at $52 per admin per month preserves audit-trail granularity across the 14-month window — for a 5-admin lender team that's $3,640 total versus $50,000 or more on Datasite or Intralinks at enterprise tier across the same window.

I'm a partner at a 5-person Calgary M&A advisory and existing JV partners have asked when I'll formally serve their pre-emption notice — when in the 7-step workflow does pre-emption gate, and how does AAPL Form 610-1989's 30-day window vs an international JOA's negotiated window affect the timeline?

For your 5-person Calgary M&A advisory serving formal pre-emption notice to existing JV partners, pre-emption gates as a parallel process at Step 1 (pre-marketing teaser plus heads-of-terms) of the 7-step workflow — not at Step 3 (indicative bid) or Step 5 (FIA negotiation) where many sellers default. Pre-emption rights are a common feature of farm-outs (Ashurst, "Navigating pre-emption rights in oil and gas transactions") and most modern AIEN/AAPL JOAs require the operator to serve formal pre-emption notice to existing JV partners before circulating the teaser to a wider counterparty universe — meaning the operator's response window starts the clock at Week 0 of the workflow, not at Week 6 to 8 when indicative bids land. The AAPL Form 610-1989 vs international AIEN window difference matters for timeline architecture. AAPL Form 610-1989 (US domestic onshore standard) sets a 30-day pre-emption window — JV partners have 30 calendar days from formal notice to elect whether to take their pro-rata share at the proposed price/terms. International JOAs under AIEN 2023 (the renamed form, formerly AIPN — the Association of International Petroleum Negotiators became the Association of International Energy Negotiators in 2022, with the 2023 Model JOA the first model published under the new name on February 16, 2023, per V&E and Bracewell guidance, 2024) typically have negotiated windows of 30 to 60 days, sometimes longer for state-partner involved transactions where consent layers stack. Three timeline implications for your Calgary heavy-oil advisory. First, US domestic deals run a tight Week 0 to Week 4 pre-emption clock — fold the pre-emption notice into the same week as teaser distribution. Second, international deals (including any Asian buyer for a Canadian heavy-oil package needing host-government consent) run a 60-day to 90-day pre-emption-plus-consent stack at the front of the workflow. Third, the historical AFE archive populated for the data room must show every pre-emption notice served on every prior AFE — that is the single most-asked completeness item from buyer's regulatory counsel. Peony Data Room at $52 per admin per month preserves the per-document NDA versioning and per-page audit trail needed to evidence pre-emption notice service across multi-year JOA windows — see the oil and gas data room checklist for the 42-document mapping.

I'm a principal at a 14-person energy-focused PE fund running 8 farm-in / divestiture buy-side mandates this year — how big is a typical farm-out data room in GB at indicative-bid Phase I vs binding-bid Phase II, and which platforms don't break on 100GB+ pre-stack SEG-Y?

For your 14-person energy-focused PE fund running 8 farm-in / divestiture buy-side mandates this year, a typical farm-out data room runs approximately 5 to 25 GB at indicative-bid Phase I and 80 to 200 GB at binding-bid Phase II — and can hit 300+ GB for multi-asset packages or LNG-tier FID where the EPC bid pack alone is 80 to 150 GB. Pre-stack 3D SEG-Y cubes routinely range 120 GB to 5.8 TB per wide-azimuth towed-streamer survey per SEG Wiki Open Data and the SEG-Y Rev 2.0 specification (March 2017) — most legacy VDRs cap individual files below 25 GB. The platforms that don't break on 100 GB+ pre-stack SEG-Y are Peony Data Room at $52 per admin per month (no per-file cap, unlimited storage), Intralinks VDRPro at enterprise tier (25 GB single-file cap raised from 15 GB across US, Germany, and Australia per Intralinks release notes, 2025 — workable for individual reservoir reports but breaks on full pre-stack volumes), and Datasite Diligence (10 GB single-file cap with zip files supported up to 50 GB per Datasite FAQ — also requires splitting on the largest seismic exports). Box Enterprise Advanced supports 500 GB single-file uploads (largest in market) but ships zero NDA gates, dynamic watermarks, or screenshot protection — fails the 4-tier farm-out test outright. Cost math at 5 admins for your 8-mandate year (280 to 480 GB total): Peony Data Room at $3,120/year flat versus Datasite at $0.40 to $1.00 per page (Capterra-aggregated buyer data, 2026) rendering 35 to 60 GB per deal as 30,000 to 60,000 pages = $96,000 to $480,000/year across 8 deals. The Mitsubishi-Aethon Haynesville farm-in benchmark — $5.2B equity (~$7.5B EV including $2.33B debt assumption per Mitsubishi press release / World Oil / CNBC / Natural Gas Intel / ChemAnalyst, January 16, 2026) — illustrates the upstream-divestiture data room scale: ~3,500+ wells, multi-county Haynesville plus Bossier shale archive, deep historical AFE archive going back to JOA inception. For the file-size mechanics deep-dive across mining, biotech, AEC, and oil-gas, see the horizontal sibling Tested: 10 Data Rooms for Large Files (With NDA Gates).

I'm IR at an E&P operator with a multi-year JOA where one non-operating partner has elected non-consent on three recent AFEs — when I run a farm-out, can the IOC bidder see that non-consent ledger, or is it a JOA partition I have to wall?

For your E&P operator with a multi-year JOA where one non-operating partner has elected non-consent on three recent AFEs, the IOC bidder evaluating the farm-out at T2 access tier can and should see your historical non-consent ledger — but only the non-consenting party's election history aggregated at the AFE-and-work-program level, not the bilateral side communications between operator and non-consenting partner. Under AAPL Form 610-1989 Article VI.B (US domestic) or AIEN 2023 Model JOA equivalent (international), non-consent is a JOA-defined election: the non-consenting party avoids cost contribution but forfeits production-revenue share until consenting parties recoup investment plus risk premium at the multiplier specified in the JOA (industry-standard ranges 200 to 400 percent for development wells, at least 300 percent for exploratory, up to 1,000 percent for offshore deepwater per Energy Law Journal / Hunton AK / US LegalForms — varying by basin and operation type). The IOC bidder needs to see the non-consent history because it directly affects what they're buying — if a non-operating partner has non-consented on three recent AFEs at 300 percent recoupment, the future cash-flow waterfall to the consenting partners (including the IOC's pro-rata share post-farm-in) is materially altered until the recoupment threshold is hit. Walling that ledger from the IOC bidder pre-bid would be a misconfigured permission set. What you do wall: bilateral side communications between operator and non-consenting partner discussing the rationale for the election, internal operator memos analyzing whether to pursue sole-risk operations under AIEN 2012/2023 Article 7 or AAPL 610 sole-risk equivalent, and the operator's own carry-forward modeling of recoupment timing. Those go in the operator-only T1 tier. Peony Data Room at $52 per admin per month uses programmatic visitor groups so the historical non-consent ledger is visible to T2 (IOC bidder) at AFE-and-work-program level while bilateral side communications stay walled to T1 — without manual permission resets per AFE.

I'm running a sell-side farm-out and the buyer's regulator-consent CP is dragging past 90 days — how do I keep the data room live during CP satisfaction without re-onboarding access tiers, and what platform handles per-deal lifecycle without per-page billing exploding?

For your sell-side farm-out where the buyer's regulator-consent conditions precedent is dragging past 90 days, you keep the data room live during CP satisfaction by transitioning the room from transactional artifact to lifecycle data room with the same 4-tier farm-out access model intact — operator (T1), non-operating JV partner (T2, now the confirmed buyer), state partner / NOC (T3, where applicable), and project finance lender (T4, where applicable). Documents added during the CP-satisfaction tail: government consent letter (state / NOC), JOA pre-emption waiver notices from existing partners, lender consent letters (operator-side and buyer-side, especially for change-of-control or asset-sale consent rights from project-finance lender or buyer's reserve-based lending), antitrust/competition filings and clearance letters (US HSR, EU Merger Reg, equivalent national filings), sanctions diligence sign-off (particularly post-2022 — AIEN 2023 introduces a new economic-sanctions regime not in the 2012 version), and decommissioning security re-validation by the regulator (NSTA UK, Petroleum Safety Authority Norway, BSEE US offshore). Conditions precedent typically run 60 to 180 days for international, 30 to 90 days for US domestic, and 6 to 12 months for LNG/project-finance deals where the lender's IESC re-validates the buyer's ESG fitness as a CP under Equator Principles 4. The platform that handles per-deal lifecycle without per-page billing exploding is Peony Data Room at $52 per admin per month — flat per-admin pricing means the cost stays at $260 per month for 5 admins whether the room runs 90 days or 14 months, the Q&A log is preserved indexed by document and topic, and the 4-tier access model carries forward without re-onboarding. Datasite and Intralinks both support lifecycle-room functionality at enterprise tier but bill per-project or per-year subscription that scales with the CP tail — for a 14-month FID-to-FC window with 5 admins on the lender side, that's $50,000+ on Datasite versus $3,640 on Peony. The Woodside-Stonepeak Louisiana LNG farm-out closed 11 weeks after announcement (April 7 to June 25 2025 per Woodside ASX) — exceptional speed driven by carry consideration structure and parallel Equator Principles 4 IESC review, not the typical 16-to-28-week pattern. Most international farm-outs run 9 to 14 months end-to-end including CP tail at FID-stage LNG.

I'm corp-dev at a major bidding on a UKCS asset farm-out — what OPRED + NSTA documents go in T2 view, what's gated to T3 (NSTA), and how does decommissioning security re-validation work as a CP?

For your major bidding on a UKCS asset farm-out, the OPRED-specific environmental and regulatory documents in T2 view are PETS (Petroleum Environmental Tracking System) submissions, OPEP (Oil Pollution Emergency Plan), and PON1 (release reports) — all administered by the Offshore Petroleum Regulator for Environment and Decommissioning (OPRED). NSTA (the North Sea Transition Authority, which took over from the Oil and Gas Authority and now handles UK upstream licensing and decommissioning since 2022) is a separate regulator from OPRED — NSTA decommissioning security documentation (parental guarantees, letters of credit, decommissioning trust funds, and Section 29 / Section 32 notice histories under the Petroleum Act 1998) sits in T2 view for non-operator JV partners but with NSTA-specific T3 carve-outs where the regulator itself reviews the buyer's decommissioning fitness. T2 access for OPRED PETS / OPEP / PON1: full disclosure with NDA plus dynamic watermark plus screenshot protection. T2 access for NSTA decommissioning security: full disclosure of operator's existing security plus the buyer-side proposed re-validation pack. T3 access (NSTA itself, sitting in the regulator carve-out tier where they exist as a JV partner — typically not in pure-private UKCS farm-outs unless specific licence terms apply): NSTA-relevant sections of the buyer's decommissioning fitness pack, full PETS/OPEP/PON1 history, and the operator's parental guarantee and trust-fund coverage. Decommissioning security re-validation works as a Step 6 condition precedent: NSTA reviews the buyer's parental guarantee adequacy (typically benchmarked against the buyer's investment-grade rating and the asset's Net Decommissioning Cost estimate), the buyer's letter-of-credit posting capacity, and the buyer's decommissioning trust fund contribution schedule. Re-validation typically runs 60 to 120 days for established mid-cap and major buyers; longer for first-time UKCS entrants where NSTA's diligence depth scales. The post-2022 sanctions regime under AIEN 2023 also folds in here — UKCS farm-outs to non-EU/UK buyers carry a sanctions clearance CP that runs in parallel. Peony Data Room at $52 per admin per month preserves the audit trail across the CP tail — see the oil and gas data room checklist for the UKCS-specific 42-document mapping.

I'm watching the Woodside Stonepeak Louisiana LNG farm-out close in 11 weeks at $5.7B carry — what does that 11-week CP-to-closing window tell me about FID-stage farm-out data rooms vs typical 16-28 week timelines?

The Woodside-Stonepeak Louisiana LNG farm-out closing 11 weeks after announcement (April 7 2025 to June 25 2025 per Woodside ASX and Stonepeak press release, June 25 2025) tells you three things about FID-stage farm-out data rooms versus typical 16-to-28-week international upstream patterns. First, the 11-week binding-bid-to-closing window is exceptional — driven by a pure carry consideration structure (Stonepeak provides $5.7B carry funding 75 percent of project capex in 2025 and 2026, Woodside received approximately $1.9B closing payment reflecting Stonepeak's 75 percent share of capex incurred since the January 1 2025 effective date) rather than the more common cash-plus-premium or cash-plus-contingent structures. Pure carry compresses the CP tail because there is no large closing-payment wire that triggers the full antitrust / sanctions / lender-consent stack — the buyer is essentially funding future capex, not buying past costs. Second, FID-stage LNG farm-outs typically run 9 to 14 months end-to-end including the CP tail, not 16 to 28 weeks like typical international upstream. The reason is the project finance lender side (T4) — Equator Principles 4 IESC site visits, ECA covenant negotiation, and multilateral DFI approvals run on independent timelines that don't compress easily. The Cenovus-BP Bay du Nord farm-out (announced June 2022, regulator-approved April 2023, FID still pending mid-2026) is the more typical pattern for non-LNG offshore — the regulator-consent CP took roughly 10 months and FID is still running. Third, the data room implication: for an 11-week compressed cycle, the seller must have the full 4-tier access model populated and battle-tested before announcement — there is no time to retrofit T3 (state partner) and T4 (lender) carve-outs in parallel with binding bid. For a 9-to-14-month FID-stage LNG cycle, the data room transitions from transactional to lifecycle at the announcement-to-closing transition and the T4 lender-tier audit trail must preserve granularity across the full window. Peony Data Room at $52 per admin per month handles both compressed-cycle and lifecycle-cycle workflows — flat per-admin pricing means the cost stays at $260 per month for 5 admins whether the room closes in 11 weeks or runs 14 months. The MRDC/Hevehe Pasca A archetype (up to a 50 percent interest in Pasca A, payable in stages totaling US$160 million / K620 million per Business Advantage PNG 2025 / PNG Business News 2025 / OGJ 2025 / Argus Media 2025) is the public-market reference for the offshore-LNG-developer-running-farm-out-at-FID-stage scenario where state-partner and major and project-finance lender all gate in parallel.

Bottom line

Oil and gas farm-out data rooms in 2026 are defined by the 7-step workflow plus 4-tier access model — the proprietary frame that runs from pre-marketing teaser through deed-of-assignment closing across operator (T1), non-operating JV partner / IOC bidder (T2), state partner / NOC (T3), and project finance lender (T4). Typical international upstream farm-outs run 16 to 28 weeks; FID-stage LNG farm-outs run 9 to 14 months end-to-end including the CP tail. Compressed cycles like Woodside-Stonepeak's 11-week window are exceptional — driven by pure-carry consideration structures and parallel Equator Principles 4 IESC review, not the typical pattern.

Use-case recommendations for the 7-step workflow plus 4-tier access model:

- For upstream international farm-outs at 80 to 200+ GB Phase II mass with 4-tier access (operator / non-operator / state partner / lender): populate the full 4-tier access matrix before Step 1 teaser distribution; serve formal pre-emption notice in parallel with teaser circulation; gate Phase II seismic plus EPC bid pack at Step 3-to-Step 4 transition; preserve audit trail across the CP tail through to lifecycle-data-room transition.

- For FID-stage LNG farm-outs with project finance lender T4 carve-out: front-load the ESIA per Equator Principles 4 plus IESC site visit plus ECA covenant documents at Step 4 Phase II; preserve T4 lender-tier audit trail granularity across the 14-month FID-to-FC window.

- For US domestic farm-outs under AAPL Form 610-1989: fold the 30-day pre-emption clock into Week 0 teaser distribution; populate the historical non-consent ledger at AFE-and-work-program level for T2 IOC bidder visibility while walling bilateral side communications to T1.

- For UKCS / North Sea farm-outs: front-load OPRED PETS / OPEP / PON1 plus NSTA decommissioning security in T2 view; treat decommissioning security re-validation as a 60-to-120-day Step 6 condition precedent.

- For midstream pipeline acquisitions adapting the 4-tier model: apply the parallel 4-Tier Midstream M&A Access Model (operator / FERC counsel / throughput counterparties / lender) front-loaded with the ROW Assignment Integrity Test and FERC Tier A-E document escalation — see the midstream pipeline acquisition data room playbook.

- For offshore LNG developers running farm-out at FID stage to a major plus state partner plus project finance lender: the public-market archetype (Twinza Pasca A — FEED entered February 2025, FID anticipated mid-2026, MRDC/Hevehe up to 50 percent interest at US$160 million / K620 million in stages per Business Advantage PNG 2025 / PNG Business News 2025 / OGJ 2025 / Argus Media 2025) demonstrates the full 4-tier complexity in one room.

For the head-on platform comparison covering single-file caps, NDA gates, dynamic watermarks, and per-page billing across Datasite, Intralinks, Drooms NXG, Firmex, and Peony Data Room at $52/admin/month, see the oil and gas data room platform guide. For the 42-document checklist organized across deal stage, document category, and counterparty access tier, see the oil and gas data room checklist. For the file-size mechanics deep-dive across mining, biotech, AEC, and oil-gas, see the horizontal sibling Tested: 10 Data Rooms for Large Files (With NDA Gates).

Peony Data Room at $52/admin/month sets up in under 5 minutes with NDA gates, dynamic watermarks, screenshot protection, programmatic visitor groups expressing the 4-tier farm-out access model — operator (T1), non-operating JV partner / IOC bidder (T2), state partner / NOC (T3), and project finance lender (T4) — page-level analytics, and unlimited storage with no per-file cap on full pre-stack SEG-Y cubes, EPC bid packs at FID, NI 51-101 reserves disclosure, or PSC text. Business at $30/admin/month covers core sharing with screenshot protection and simple NDA gating; Data Room is the tier that ships dynamic watermarks plus the granular per-file visitor-group permissions and unlimited storage the 4-tier access model requires for farm-out workflows. The conversion-handoff page for upstream, midstream, and LNG project teams is Energy Solutions. Free tier (2 GB, AES-256 encryption) is the entry point if you want to kick the tires before upgrading.

Related resources

- 10 Best Data Rooms for Oil and Gas Companies (2026 Guide) — the cluster anchor with 10-platform comparison, FID cliff diagnostic, and 4-tier farm-out access model.

- Oil and Gas Data Room Checklist (42 Documents, FEED to FID) — the 12-folder canonical structure with file-size ranges and NDA gating tier per document type.

- Tested: 10 Data Rooms for Large Files (With NDA Gates) — horizontal sibling on file-size mechanics across mining, biotech, AEC, and oil-gas.

- M&A Data Room Guide — general M&A data room workflow.

- Due Diligence Data Room Checklist (174 Documents) — the comprehensive M&A diligence baseline that this oil-gas farm-out workflow overlays.

- Energy Solutions — the conversion-handoff page for upstream, midstream, and LNG project teams.

- Peony Features Overview — NDA gates, dynamic watermarks, screenshot protection, auto-indexing, page-level analytics, visitor groups.

- Peony Pricing — Data Room tier at $52 per admin per month with no per-file cap and unlimited storage.

Cluster siblings (forthcoming May to June 2026):

- LNG Project Finance Data Room — FEED → FID document escalation, EPC bid pack, ECA financing pack.

- Upstream Oil and Gas Divestiture Data Room — 12-month divestiture timeline + reserve-report disclosure progressive-tiering.

- Midstream Pipeline Acquisition Data Room — ROW easement archive structuring + FERC docket cross-referencing.

- Oil and Gas Joint Venture Data Room — JV-partner DD as a recurring (not transactional) data room.