LNG Project Finance Data Room: FEED→FID Escalation + ECA Debt Pack (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Last updated: May 2026

Quick answer: An LNG project finance data room scales through a six-phase FEED→FID document escalation curve — ~1-2 GB concept select, ~5 GB FEED entry, ~10-25 GB mid-FEED, ~25-50 GB FEED completion, 80-200 GB pre-FID lender diligence, 200-300+ GB post-FID. FID-stage content stratifies across EPC bid responses (LSTK 60-150 GB / convertible 50-70 GB / reimbursable 30-50 GB), offtake SPAs under AIEN 2025 Model SPA FOB, the 6-ECA disbursement-condition document set (JBIC, KEXIM, US EXIM, UKEF, Bpifrance, Sinosure), and ESIA per Equator Principles 4. This is the FID cliff at LNG scale.

I run Peony, a data room platform. The escalation-curve frame in this post is calibrated against a year of fielding diligence questions from LNG sponsor IR running pre-FID lender roadshows, project finance bank desk MDs underwriting LSTK EPC packages, AIEN 2025 Model SPA offtake counterparties negotiating FOB allocation, IESC technical advisors preparing pre-FC reports under Equator Principles 4, and ECA underwriters at JBIC, KEXIM, US EXIM, UKEF, Bpifrance, and Sinosure clearing covenant packages. The question that surfaces in every seat at the FEED-to-FID transition: how big does the data room actually get from FEED to FID, and which phase produces the biggest single doc-mass jump that legacy VDRs can't absorb?

The platform comparison anchor names the ten platforms and frames the FID cliff; the 42-document checklist catalogs what goes in each folder; the farm-out workflow playbook sequences the 7-step workflow plus 4-tier access model; this post is the LNG project-finance deep dive anchored on the FEED→FID document escalation curve.

TL;DR — an LNG project finance data room scales through 6 phases from ~1-2 GB at concept select to 200-300+ GB at financial close, with the steepest jump at FEED-completion-to-pre-FID when EPC bids + ECA term sheets + offtake SPAs land:

- Phase 1 — Pre-FEED / Concept Select (~1-2 GB): BOD, alternative selection, ESIA scoping, preliminary regulatory pathway analysis (FERC §3 / NOPSEMA / OPRED).

- Phase 2 — FEED entry (~5 GB): full FEED scope of work, regulatory pathway lodged, SPE-PRMS 2P reserves, early offtake LOIs / MOUs, state-partner equity-vehicle term sheets.

- Phase 3 — Mid-FEED (~10-25 GB): EPC pre-bid technical package, supplier shortlist (gas turbines, main cryogenic heat exchangers, refrigerant compressors), preliminary HAZID and HAZOP, ESIA draft baselines.

- Phase 4 — FEED completion (~25-50 GB): final FEED design package, EPC bid invitations / ITT to 3-5 prequalified consortia, final ESIA per Equator Principles 4 (effective October 1, 2020), Independent Technical Advisor report.

- Phase 5 — Pre-FID / FID lender diligence pack (~80-200+ GB; greenfield LNG can hit 300 GB): full EPC LSTK bid responses (60-150 GB per consortium), executed offtake SPAs under AIEN 2025 Model LNG SPA FOB, ECA financing pack across JBIC / KEXIM / US EXIM / UKEF / Bpifrance Assurance Export / Sinosure plus multilaterals IFC / ADB / EBRD, IESC pre-financial-close report under EP4.

- Phase 6 — Post-FID / Financial close plus construction (200-300+ GB): executed loan documentation, disbursement documentation, ITA monthly progress certificates, IESC quarterly E&S monitoring, change-order documentation, EP ongoing monitoring reports.

- EPC bid pack mass by structure: LSTK 60-150 GB per consortium, convertible / target-cost 50-70 GB, reimbursable 30-50 GB upfront and heaviest ongoing change-order documentation.

- Offtake structure split (EIA 2025): 75% FOB, 12% DES, 13% FOB/DES flex; over 90% of LNG volumes sold in 2025 under FOB SPAs; approximately 95% of 2025 volumes were 20-year SPAs; 56% Henry Hub indexed.

- Real-deal anchors (2025-2026): NextDecade Rio Grande Train 5 — $6.7B FID + financial close October 16, 2025 (Bechtel LSTK, 4.5 MTPA SPA with JERA/EQT/ConocoPhillips, substantial completion H1 2031); Woodside Louisiana LNG — FID late April 2025 ($17.5B for 16.5 MTPA three-train foundational, Bechtel revised LSTK December 2024, Stonepeak farm-down closed June 25, 2025); Venture Global CP2 Phase 1 — $15.1B FID + financial close July 28, 2025 (largest standalone project financing ever; 28-bank pool; 14.4 MTPA; first LNG 2027); Eni Coral North FLNG — FID October 2, 2025 (3.6 MTPA FLNG, JV Eni 50% + CNPC 20% + ENH 10% + KOGAS 10% + ADNOC's XRG 10%, Technip Energies EPC, first LNG 2028); TotalEnergies Mozambique LNG — force majeure lifted November 7, 2025; updated $20.5B budget per Q3 2025 earnings call October 30, 2025; US EXIM $4.7B re-approval March 13, 2025; UKEF $1.15B withdrawn December 2025.

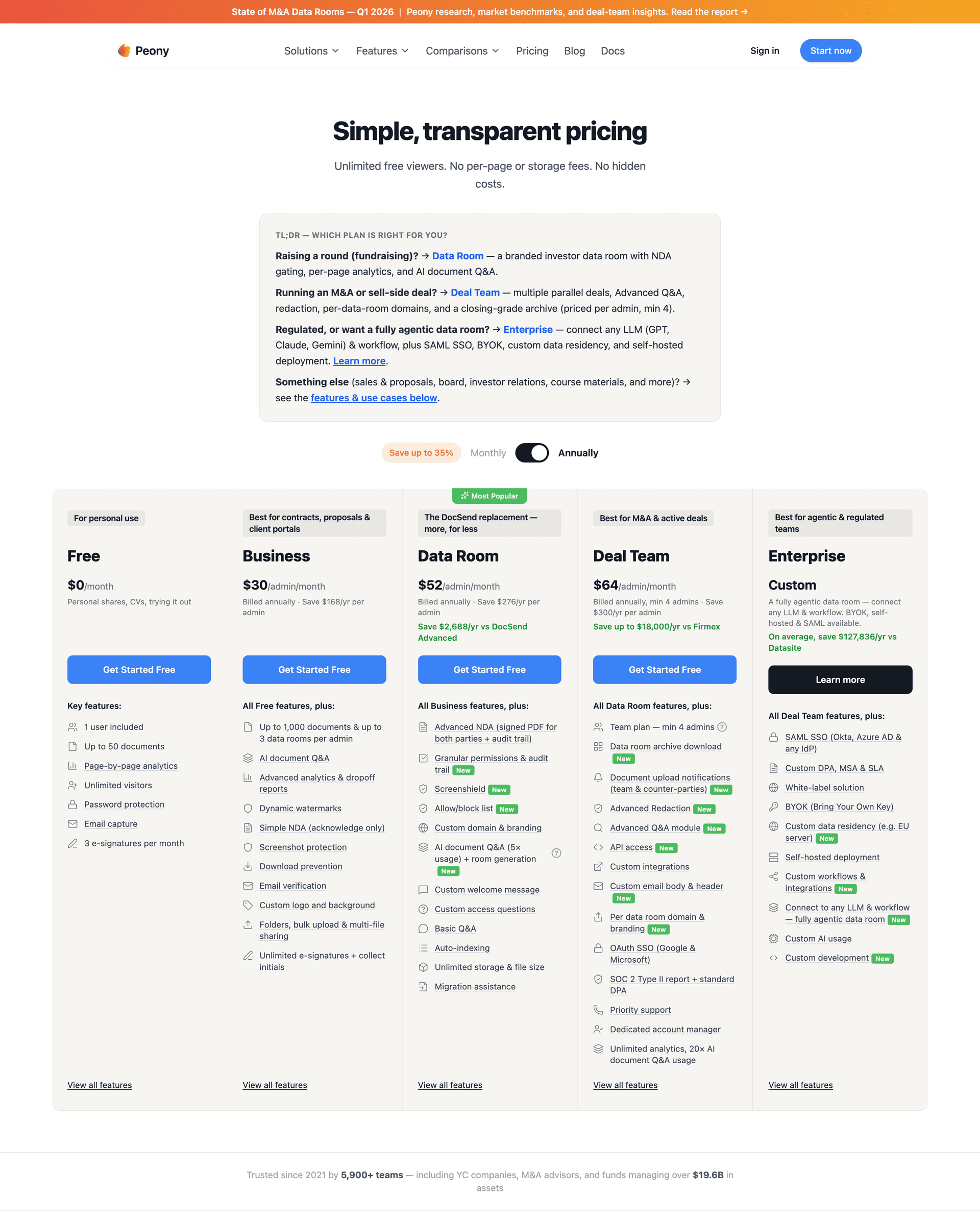

- Peony Data Room at $52/admin/month ships NDA gates, dynamic watermarks, screenshot protection, visitor groups, page-level analytics, and unlimited storage with no per-file cap — the structurally cheaper alternative to Datasite per-page billing (which can run six-figure invoices on 200 GB FID-stage data rooms at $0.40 to $1.00 per page per Capterra-aggregated buyer data 2026), and to Intralinks at custom-quoted enterprise pricing.

The FID cliff — defined in the cluster anchor post as the document-mass plus counterparty-count surge between FEED and Final Investment Decision — is the diagnostic. The FEED→FID document escalation curve is the proprietary frame for LNG project-finance specifically; this is the FID cliff at LNG scale, where doc mass jumps an order of magnitude from FEED completion (~25-50 GB) to pre-FID lender diligence (80-200+ GB) and counterparty count surges from 3-5 to 12-25 active diligence parties. Below FEED-completion file mass (typically under 50 GB) and counterparty count (3-5 active diligence parties), most VDRs handle the workflow. Past the Phase 4-to-Phase 5 jump — 80-200 GB of EPC LSTK bid responses plus executed offtake SPAs plus the ECA financing pack plus the IESC's pre-financial-close report — generic VDRs collapse on file-size caps, flat permission models, or per-page billing that turns a 100 GB EPC bid pack into a six-figure invoice.

This guide breaks down the six-phase FEED→FID document escalation curve, the LSTK / convertible / reimbursable bid pack mass differential that drives EPC documentation depth, the 6-ECA disbursement-condition document set across the major export credit agencies, the FOB / DES / tolling offtake structures under the AIEN 2025 Model LNG SPA FOB, and how Peony Data Room at $52/admin/month handles the 100 GB+ FID-stage data mass at flat per-admin cost. The frame inherits the seismic-data NDA pattern from the farm-out workflow playbook — progressive disclosure across diligence stages, where reservoir simulation models and proprietary 3D seismic gate to short-listed lenders only at Phase 5, never Phase 1-4.

What is an LNG project finance data room?

An LNG project finance data room is the structured document repository that supports development of a liquefied-natural-gas project from concept select through Final Investment Decision (FID) and on through financial close (FC) and construction — typically a 30-to-36-month timeline from FEED entry, with the data room scaling from approximately 5 GB at FEED entry to 80-200 GB at FID lender diligence and 200-300 GB through post-FID construction. The defining feature that separates an LNG project finance data room from a generic upstream M&A or oil and gas farm-out data room is the multi-counterparty syndicate at FID: typically 12-25 active diligence counterparties spanning operator plus state partner plus EPC consortium bidders plus 8-15 lender-side institutions (commercial banks plus 3-6 ECAs plus multilaterals plus DFIs plus their external counsel and ITAs).

Five document categories make LNG project finance data rooms structurally distinct from generic upstream rooms:

-

EPC technical pack at FID stage — the full LSTK (or convertible / target-cost / reimbursable) bid response from each consortium, typically 60-150 GB per bidder including completed P&IDs, isometrics, MTOs, EDS package, schedule of values, payment milestone schedule, performance and parent-company guarantees, liquidated damages structure, and cost-and-schedule risk register.

-

Offtake SPA stack under AIEN 2025 Model LNG SPA FOB — executed long-term SPAs (typically 20-year take-or-pay with DCQ / ACQ / volume tolerance / make-up rights), bilateral charter agreements where DES applies, port and channel documentation, vessel suitability documentation. AIEN — formerly AIPN, the Association of International Petroleum Negotiators, which became the Association of International Energy Negotiators in 2022 — published the 2023 Model JOA as its first model under the new name; the 2025 Model LNG SPA FOB is the corresponding offtake-side standard.

-

ECA financing pack across 3-6 export credit agencies — JBIC (Japan), KEXIM (Korea), US EXIM, UKEF (UK), Bpifrance Assurance Export, and Sinosure (China). Each ECA brings a distinct disbursement-condition document set anchored to content sourcing, ESIA framework, sanctions diligence, and offtake / equity participation by the ECA's home-country buyers or contractors.

-

Multilateral and DFI participation pack — IFC, ADB, EBRD, AfDB. Multilateral participation brings a catalytic effect on commercial-bank participation that ECAs alone do not. The 10-MDB Global Co-financing Platform launched October 2024 (including IFC, ADB, EBRD, AIIB) is the institutional infrastructure that streamlines multilateral co-financing on greenfield LNG.

-

Equator Principles 4 ESIA and IESC monitoring stack — final ESIA aligned with EP4 (effective October 1, 2020), IESC pre-financial-close report, IESC quarterly construction monitoring (for EP category A projects), Action Plan tracking, climate risk and resilience documentation, GHG emissions baseline, and the project company's E&S management system documentation.

Standard upstream data rooms are built around the 4-tier farm-out access model — operator / non-operating JV partner / state partner / project finance lender. LNG project finance data rooms extend that model with EPC consortium bidders as a fifth de-facto tier and the lender pool stratifying further into commercial banks plus ECAs plus multilaterals plus DFIs plus external counsel plus ITA plus IESC plus market consultants. Peony Data Room at $52/admin/month expresses this stratification through programmatic visitor groups — every bidder, every lender, every consultant in the syndicate sees the access tier appropriate to their role without manual permission resets.

What is the FEED→FID document escalation curve in LNG?

The FEED→FID document escalation curve is the proprietary frame I use to diagnose LNG project finance data room composition: the six-phase progression from concept select through post-FID financial close where document mass scales from approximately 1-2 GB to 200-300+ GB across roughly 30-36 months. The curve extends the broader FID cliff frame from the cluster anchor post specifically to project-finance LNG. Doc mass accumulates non-linearly — the steepest jump is the FEED-completion to pre-FID transition where EPC bid responses land at 60-150 GB per consortium and the ECA / multilateral disbursement-condition pack layers in.

Each phase has a defined timeframe, document mass envelope, and dominant content category. Sponsors, lender lead arrangers, ECA credit officers, and EPC proposal directors all reference the curve to align expectations on what should be in the data room when.

Phase 1 — Pre-FEED / Concept Select (~1-2 GB)

Timeframe: 6-18 months. Document categories: concept-selection report (onshore liquefaction vs FLNG vs floating storage), basis-of-design (BOD), pre-FEED engineering (PFDs, preliminary heat and material balances, plot plan, equipment list preliminary), environmental and social scoping report, resource confirmation (appraisal-well data, reservoir-volume estimates pre-PRMS booking), preliminary regulatory pathway analysis (FERC §3 / NOPSEMA / OPRED / petroleum ministry), preliminary commercial framework, heads-of-terms for partner farm-down or state-partner equity vehicle.

This is the lightest data-room phase but the highest-leverage one for setting the 4-tier access architecture: T1 operator full / T2 IOC bidder / T3 state partner / T4 lender. Get the access model right at Phase 1 and the room scales cleanly through to Phase 5; defer the access model and Phase 5 forces a re-architecture under FID time pressure.

Phase 2 — FEED entry (~5 GB)

Timeframe: Month 0 to 12-18. Document categories: full FEED scope of work (Worley / KBR / Wood / Saipem / Technip Energies / JGC / McDermott / Bechtel-FEED), updated locked BOD, geophysics summary plus preliminary geotech, regulatory pathway lodged (FERC §3 application US / Environmental Plan / Safety Case AU NOPSEMA / PETS / OPEP UK OPRED), marketing analysis plus early offtake LOIs / MOUs, state-partner equity-vehicle term sheets, updated SPE-PRMS 2P/3P reserves report (per SPE-PRMS 2018 v1.03 published November 2022).

FEED entry is the gating event that triggers most of the lender pre-engagement — banks and ECAs typically join structured calls and start indicative term-sheet discussions on FEED entry once the regulatory pathway has been formally lodged. The offshore LNG developer archetype with FEED entered February 2025 (public-market context: Twinza Pasca A per Business Advantage PNG and PNG Business News, 2025; Pasca Gas Agreement signed December 19, 2024) is the working reference for an FID anticipated mid-2026 — about 16 months from FEED entry to FID under typical offshore-LNG-with-state-partner-co-equity timing.

Phase 3 — Mid-FEED (~10-25 GB)

Timeframe: Month 12 to 18-24. Document categories: EPC pre-bid technical package (preliminary P&IDs, equipment list revised, specs for major equipment packages, structural and civil basis), supplier shortlist (gas turbines, main cryogenic heat exchangers, refrigerant compressors, BOG compressors), updated regulatory submissions (regulator Q&A, public consultation logs), preliminary HAZID plus HAZOP studies, project schedule plus capex estimate (typically plus or minus 20% accuracy at mid-FEED), construction execution plan, marine logistics plan, ESIA draft baselines (air, water, noise, biodiversity, social).

Mid-FEED is where the lender's market consultant typically issues the first independent LNG demand outlook report and where the IESC's pre-FC ESDD scope-of-work is finalized.

Phase 4 — FEED completion (~25-50 GB)

Timeframe: Month 18 to 24-30. Document categories: final FEED design package (completed P&IDs, isometrics, MTOs, equipment data sheets, instrument data sheets, electrical single-line diagrams, control philosophy), EPC bid invitations / ITT packages (typically issued to 3-5 prequalified consortia), final ESIA per Equator Principles 4 (effective October 1, 2020 — framework governing project-finance ESDD for projects above $10M), final HAZOP / SIL studies, initial offtake SPA negotiation drafts (FOB or DES), initial multilateral / ECA term-sheet discussions, plus or minus 10% accuracy capex plus opex estimate, Independent Technical Advisor (ITA) report (lender-commissioned, reviews FEED engineering quality plus schedule plus capex accuracy).

FEED completion is the trigger for ITT issuance to the EPC bidder shortlist. The Twinza Pasca A archetype targets engineering completion plus ITT issuance to potential contractors and fabrication yards before mid-2026 FID per Business Advantage PNG, 2025 — that's the working reference for offshore LNG with FEED started February 2025.

Phase 5 — Pre-FID / FID lender diligence pack (~80-200+ GB; greenfield LNG can hit 300 GB)

Timeframe: Month 24 to 30-36 (FID). This is where the FID cliff bites. The Phase 4 to Phase 5 transition is the steepest doc-mass jump on the entire FEED→FID curve.

Category A — EPC bid responses (full LSTK technical pack, 60-150 GB per consortium): each contractor's full design package (Bechtel, Technip Energies, JGC, Saipem, McDermott, Samsung C&T, Hyundai E&C, KBR, Worley), module yard plans, fabrication schedules, schedule of values, payment milestone schedule, performance plus parent-company guarantees, liquidated damages structure (delay LDs, performance LDs), cost-and-schedule risk register.

Category B — Reservoir plus operational (~10-30 GB): final SPE-PRMS 2P certification with audited reserves, reservoir simulation model (Eclipse / Petrel RE / CMG — typically 5-20 GB), production-and-export profile, final geotechnical site investigations. The seismic-data NDA pattern from the farm-out workflow playbook controls disclosure here: proprietary 3D pre-stack seismic and detailed reservoir simulation models gate to short-listed Phase 5 lenders only — never visible at FEED entry or to the broad EPC bidder pool, even under signed master NDA.

Category C — Commercial / offtake (~5-15 GB): executed offtake SPAs (FOB or DES) — typically 20-year take-or-pay; per AIEN 2025 Model LNG Sale and Purchase Agreement FOB, agreements specify volumes, pricing index (Henry Hub for US, JKM for Asia spot, oil-linked Brent for Asia long-term), DCQ (daily contract quantity), ACQ (annual contract quantity), volume tolerance; bilateral charter agreements (LNG vessels for DES sellers); take-or-pay obligation schedule.

Category D — Project finance package (~10-30 GB): project finance model (PFM) plus sensitivity matrix plus tax model, term sheets plus draft loan documentation from each lender, ECA term sheets (JBIC, KEXIM, US EXIM, UKEF, Bpifrance, Sinosure), multilateral term sheets (IFC, ADB, EBRD, AfDB), common terms agreement (CTA), direct agreements with project counterparties (offtake direct, EPC direct), intercreditor agreements, completion guarantees plus completion-date schedule, lender's IESC report (Equator Principles 4 requires IESC for category A pre-FC; complex projects ESDD 6-12 months), lender's market consultant (LNG demand outlook), lender's insurance advisor, lender's tax advisor, sanctions diligence sign-off (post-2022 critical).

Category E — Regulatory / ESIA (~5-10 GB): final ESIA per Equator Principles 4, IESC's pre-FC site visit reports, all regulator approvals (FERC §3 export approval; DOE export authorization for non-FTA countries — US; equivalent regulator approvals for international jurisdictions). Note that LNG terminal economics depend on upstream feed-gas pipeline FERC §7(c) review for interstate gas pipelines under the Natural Gas Act — the parallel midstream asset class to LNG project finance — see the midstream pipeline acquisition data room playbook for the FERC Tier A-E document escalation framework that governs gas-pipeline tariff and certificate diligence as the corollary to LNG-tier offtake economics.

Phase 6 — Post-FID / Financial close plus construction (~200-300+ GB)

Timeframe: Month 30-36 (FID) onward through construction. Documents: executed loan documentation final form, disbursement documentation (each disbursement requires contractor invoices plus ITA monthly progress certificate plus IESC quarterly E&S monitoring plus project company officer's certificate), construction monitoring reports (monthly ITA), HSE statistics archive (TRIR, DART, LTI), change-order documentation, Equator Principles ongoing monitoring reports (semi-annual or annual), insurance certificates plus adequacy reviews.

NextDecade Rio Grande LNG Train 5 reached positive FID and financial close on October 16, 2025 with $6.7 billion in committed financing per NextDecade IR — full notice to proceed issued to Bechtel for Train 5 the same day. Train 5 is commercially supported by 4.5 MTPA of 20-year LNG SPAs with JERA, EQT Corporation, and ConocoPhillips, with substantial completion targeted H1 2031 — that's the working reference for the Phase 5-to-Phase 6 transition on a US Gulf Coast LSTK-anchored project.

Document escalation curve summary table

| Phase | Timeframe | Data room mass | Dominant new content |

|---|---|---|---|

| Pre-FEED / Concept Select | Month -18 to 0 | ~1-2 GB | BOD, alternative selection, ESIA scoping |

| FEED entry | Month 0 to 12-18 | ~5 GB | FEED scope of work, regulatory pathway lodged, 2P reserves |

| Mid-FEED | Month 12 to 18-24 | ~10-25 GB | EPC pre-bid pack, supplier shortlist, HAZID/HAZOP-1 |

| FEED completion | Month 18 to 24-30 | ~25-50 GB | Final FEED package, ITT to EPC bidders, ESIA per EP4 |

| Pre-FID / FID lender diligence | Month 24 to 30-36 | ~80-200+ GB | Full EPC LSTK bids, project-finance pack, ECA term sheets, executed offtake SPAs, IESC final report |

| Post-FID / Financial close + construction | Month 30+ | 200-300+ GB | Disbursement docs, ITA monthly progress, ongoing E&S monitoring |

The diagnostic test: if your LNG project is approaching FID, ask the VDR vendor (a) what's your single-file cap for a 100 GB EPC LSTK bid pack, (b) how many nested permission tiers can you express programmatically (operator / IOC bidder / state partner / EPC consortium / commercial bank / ECA / multilateral / external counsel / ITA / IESC / market consultant), and (c) does per-page or per-project pricing apply across a 14-month FID-to-FC window. Datasite at $0.40 to $1.00 per page (Capterra-aggregated buyer data, 2026) on a 200 GB FID-stage room runs into six-figure annualized invoices; Peony Data Room at $52/admin/month handles the same mass at $624 per admin per year. The structural cost wedge is the largest in the entire VDR market on data-heavy FID-stage workflows — see the large-file data room comparison for the file-mass mechanics.

What documents are in an LNG EPC bid pack and how do LSTK, convertible, and reimbursable change composition?

An LNG EPC bid pack is the full technical, commercial, and risk-allocation response a contractor submits in answer to a sponsor's ITT issued at FEED completion — and the data-room mass differs materially across LSTK (lump sum turnkey), convertible / target-cost, and reimbursable (cost-plus) structures because each shifts cost-overrun risk differently and therefore demands different upfront documentation depth. LSTK bids run heaviest on technical detail (the contractor must price every component upfront), convertible bids run heavier on financial-controls documentation (open-book cost reporting plus audit-rights protocols), and reimbursable bids run thinner upfront but heaviest in ongoing change-order documentation across construction.

LSTK — Lump Sum Turnkey

LSTK is a fixed-price agreement under which the contractor delivers the complete project for a set price and assumes most cost-overrun risk per A&O Shearman's published LNG project finance practice. The data-room mass is heaviest at bid — typically 60-150 GB per consortium — because the contractor has to lock detailed P&IDs, isometrics, MTOs, sub-contractor quotes, schedule of values, payment milestone schedule, performance plus parent-company guarantees, and liquidated damages structure. Post-FID change-order documentation is comparatively limited because the base scope is fixed.

Recent LSTK examples (2024-2026):

- Woodside Louisiana LNG (formerly Driftwood / Tellurian) — Bechtel revised LSTK signed December 2024; Woodside took FID on Louisiana LNG in late April 2025; total US$17.5B for the 16.5 MTPA three-train foundational phase per Woodside ASX disclosures and PGJ Online; first gas targeted 2029. Stonepeak farm-down: 40% interest sold to Stonepeak with $5.7B carry funding 75% of project capex 2025-2026 and Woodside receiving approximately $1.9B closing payment when the Stonepeak transaction closed June 25, 2025.

- NextDecade Rio Grande Train 5 — Bechtel LSTK; full notice to proceed October 16, 2025; Train 5 is 6 MTPA (NextDecade total nameplate 30 MTPA); included in the $6.7B financing close.

- Commonwealth LNG / Technip Energies — LSTK signed under May 2024 FID; approximately $4.8B for 9.3 MTPA per EPC Intel.

Convertible / target-cost EPC

Convertible / target-cost EPC is initially structured with cost-reimbursable mechanics (target price plus sharing formula) with a conversion mechanism to LSTK once design risk retires. This structure has become more common in 2024-2026 because contractors are reluctant to take full LSTK risk on first-of-kind LNG. Data-room mass typically 50-70 GB per consortium upfront, plus heavier financial-controls documentation (open-book cost reporting, audit-rights protocols, change-order procedures).

Recent example: Worley CP2 LNG Phase 2 — Venture Global's CP2 Phase 2 EPC contract is reimbursable target-cost; FID for Phase 2 reached March 13, 2026; CP2 development could hit approximately $28B total per company filings.

Reimbursable (cost-plus)

Reimbursable EPC pays the contractor for legitimate project costs incurred plus a profit fee. Data-room mass thinner upfront — typically 30-50 GB — because pricing is less detailed and design develops during execution. The heaviest documentation load shifts to ongoing change-order, audit, and cost-reporting through construction. Lender pushback: ECAs and project finance lenders historically prefer LSTK for bankability because it caps cost-overrun exposure to the sponsor and lender pool.

EPC type — bid-pack documentation comparison

| Document category | LSTK | Convertible / target-cost | Reimbursable |

|---|---|---|---|

| Detailed P&IDs at bid | Required | Required | Often deferred |

| Detailed MTOs at bid | Required | Required | Lower precision |

| Sub-contractor quotes | Locked | Open-book | Open-book |

| Schedule of values | Locked-in | Indicative | Indicative |

| Performance LDs | High | Capped (target-price band) | Lower / negotiated |

| Change-order doc | Limited (base scope fixed) | Heavy (open-book) | Heaviest (continuous) |

| Audit rights for lender | Limited (pricing locked) | Full | Full |

| Typical bid-pack mass | 60-150 GB | 50-70 GB | 30-50 GB upfront, heavy ongoing |

The LSTK / convertible / reimbursable bid pack mass differential — 60-150 GB versus 50-70 GB versus 30-50 GB upfront — is the procurement signal a sponsor uses to right-size data room capacity at FEED completion. The data room implication for an EPC proposal director: each consortium's bid response gates to its own visitor group so Bechtel never sees Technip Energies' schedule of values and Hyundai E&C never sees JGC's MTOs. Each lender's ITA gates to a separate audit-rights view across all consortium bid responses, with dynamic watermarks tagging every page. Datasite, Intralinks, and Peony Business all support this pattern at security parity; the structural cost wedge is in pricing — Peony Data Room at $52/admin/month versus Datasite per-page billing where a 100 GB EPC LSTK bid pack rendering at 30,000-100,000 pages plus per-page rates of $0.40 to $1.00 generates six-figure invoices on the bid-evaluation cycle alone.

The cost wedge sharpens further across the FID-to-FC window. For a 5-admin lender-side team running a 14-month FID-to-FC window with the full EPC bid pack plus ECA pack plus offtake SPA stack: Peony Data Room runs $3,640 total flat (5 admins × $52 × 14 months); Datasite enterprise typically lands $50,000-$80,000 per project at $0.40-$1.00 per page across the rendered mass. The 7-22x cost gap on data-heavy FID-stage workflows is structural, not promotional.

What's in an LNG ECA financing pack — JBIC, KEXIM, US EXIM, UKEF, Bpifrance, Sinosure?

An LNG ECA financing pack stratifies across the 6-ECA disbursement-condition document set — JBIC (Tokyo), KEXIM (Seoul), US EXIM (Washington), UKEF (London), Bpifrance Assurance Export (Paris), and Sinosure (Beijing) — plus multilaterals (IFC, ADB, EBRD, AfDB), each carrying a distinct disbursement-condition document set anchored to home-country content sourcing, ESIA framework alignment, sanctions diligence, and offtake or equity participation by the ECA's home-country buyers or contractors. Major LNG projects typically pull together 30+ lenders; ECAs anchor the syndicate. Each ECA's guarantee can be 'comprehensive' (covering all non-payment risk with a 10-15% residual uncovered portion) or limited to political-risk-only per ICLG project finance USA 2025-2026.

JBIC — Japan Bank for International Cooperation

JBIC is Japanese-offtake-driven lending. Disbursement-condition documents: Japanese-buyer offtake SPAs executed (JERA, Mitsubishi, Mitsui, Tokyo Gas), Japanese equity / participation evidence, Japan energy security policy compliance, ESIA per JBIC Environmental Guidelines (aligned with EP4 plus IFC PS), quarterly construction progress reports (ITA-certified), local-content / Japanese-content reporting. Recent Japanese-financial-institution participation: MUFG is supporting Papua LNG; JBIC, MUFG, Mizuho, and SMBC are recurring participants in greenfield LNG syndicates.

KEXIM — Korea Eximbank

KEXIM lends with a Korean EPC contractor support and Korean offtake (KOGAS) anchor. Disbursement-condition documents: Korean-content evidence (typically ≥30% Korean equipment / services for full coverage), KOGAS offtake (where applicable), ESIA per KEXIM E&S guidelines, performance bonds plus parent guarantees from Korean contractors (Hyundai E&C, Samsung C&T, Daewoo Shipbuilding / Hanwha Ocean), construction progress monitoring. Recent participation: KEXIM was an ECA participant in Mozambique LNG's 2020 financing alongside Bpifrance, K-Sure, SACE, and Sinosure.

US EXIM

US EXIM lends under US content requirements and 'Make More in America' priorities. Disbursement-condition documents: US content certifications (typically 51% US content for full guarantee), US-supplier sourcing evidence, ESIA per US EXIM ESDD Procedures (aligned with EP4), OFAC sanctions compliance, beneficial-owner disclosure (FinCEN), US labor / wage compliance, quarterly construction progress reports. Recent action: the US EXIM board approved a $4.7 billion loan to Mozambique LNG on March 13, 2025 (a re-approval of the originally 2020-issued loan), supporting an estimated 16,400 jobs across 68 companies in 14 states.

UKEF — UK Export Finance

UKEF lends under UK content requirements and UKEF eligibility includes minimum risk standards, anti-bribery and corruption diligence, and ESG diligence. Disbursement-condition documents: UK content evidence (typically 20% threshold for the UK Export Development Guarantee), ESIA per UKEF E&S Guidelines (aligned with EP4), Bribery Act compliance, climate-related disclosures (UKEF withdrew from coal-fired power 2017; tightening on oil and gas continues), local-content reporting. Recent action: UKEF agreed US$1.15B for Mozambique LNG in 2020 but the UK government withdrew that backing in December 2025 amid security and ethical concerns per GTR; TotalEnergies replaced lost UKEF and Atradius cover with other lenders.

Bpifrance Assurance Export

Bpifrance is French export support across LNG, defense, and transport flagship sectors. Disbursement-condition documents: French-content evidence (typically supports French equipment exports — Technip Energies modules, Air Liquide cryogenic equipment), ESIA per French AFD environmental guidelines plus EP4, climate alignment (post-Paris Agreement), anti-bribery (Sapin 2) compliance. Recent participation: ECA participant in Mozambique LNG financing 2020.

Sinosure — China Export and Credit Insurance Corporation

Sinosure is the Chinese state insurer for Belt-and-Road LNG, Chinese equipment / EPC contractor support, and Chinese offtake (CNPC, Sinopec). Disbursement-condition documents: Chinese-content evidence, Chinese offtake SPA evidence (CNPC participates in Coral North FLNG offtake — 20% upstream interest per Eni's October 2, 2025 FID disclosures), Belt-and-Road Initiative alignment, Sinosure E&S guidelines plus EP4 alignment, construction progress monitoring. Recent participation: Sinosure participated in Mozambique LNG's Chinese-led loans 2020.

Multilaterals — IFC, ADB, EBRD, AfDB

Multilaterals are critical for LNG in IDA-eligible / frontier markets. Lower absolute dollar amounts than ECAs but bring catalytic effect — multilateral participation signals E&S compliance to commercial banks and de-risks for other lenders. Disbursement-condition documents: comprehensive ESIA per IFC Performance Standards (the de-facto baseline that EP4 incorporates), IESC quarterly site visits, Indigenous Peoples Plan (PS 7), Resettlement Action Plan (PS 5), anti-corruption plus integrity due diligence, disclosure per IFC Access to Information Policy, climate risk and resilience documentation. Recent institutional infrastructure: 10 MDBs jointly launched the Global Co-financing Platform in October 2024 — including IFC, ADB, EBRD, AIIB — to streamline co-financing on greenfield LNG and other large-scale infrastructure.

ECA pack comparison summary

| ECA | Home-country anchor | Content threshold | ESIA framework | Recent LNG participation |

|---|---|---|---|---|

| JBIC | Japanese offtake (JERA, Mitsubishi, Mitsui) | Japanese-supplier evidence | JBIC Env Guidelines (aligned EP4 + IFC PS) | Papua LNG (MUFG anchoring) |

| KEXIM | Korean EPC + KOGAS offtake | ≥30% Korean equipment/services | KEXIM E&S guidelines | Mozambique LNG 2020 |

| US EXIM | US content | 51% US content for full guarantee | US EXIM ESDD (aligned EP4) | Mozambique LNG $4.7B re-approved March 13, 2025 |

| UKEF | UK content | ≥20% (UK Export Dev Guarantee) | UKEF E&S Guidelines (aligned EP4) | Withdrew from Mozambique LNG December 2025 |

| Bpifrance | French equipment exports | French-supplier evidence | AFD env guidelines + EP4 | Mozambique LNG 2020 |

| Sinosure | Chinese EPC + CNPC/Sinopec offtake | Chinese-content evidence | Sinosure E&S (aligned EP4) | Mozambique LNG 2020 + Coral North 2025 |

| IFC / ADB / EBRD / AfDB | Catalytic / IDA-eligible markets | n/a | IFC Performance Standards (EP4 baseline) | 10-MDB Global Co-financing Platform Oct 2024 |

The data room implication for an ECA credit officer: each ECA gates to its own visitor group so JBIC sees Japanese-supplier evidence and JERA offtake but never the Sinosure-specific Belt-and-Road documentation; US EXIM sees US content certifications and OFAC sanctions sign-off but never the bilateral state-partner side letters between operator and host-country NOC. Quarterly disbursement-condition compliance tracking through construction requires the data room to preserve contractor invoices plus ITA monthly progress certificate plus IESC quarterly E&S monitoring plus project company officer's certificate, all hash-verified, with a per-document version log. Peony Data Room at $52/admin/month preserves this audit trail per the oil and gas farm-out workflow playbook — for a 6-ECA syndicate plus multilaterals plus commercial banks running a 14-month FID-to-FC window with 5-8 admins on the lender-counsel side, that's a few thousand dollars total versus tens of thousands on enterprise per-project pricing.

How do Equator Principles 4 and the IESC shape LNG project finance documentation?

Equator Principles 4 (EP4, effective October 1, 2020) is the framework governing project-finance environmental and social due diligence for projects above $10M — and it shapes LNG project finance documentation through three specific mechanisms: (1) all designated-country projects are no longer 'deemed in compliance' solely by host country law (Equator Principles Financial Institutions require independent verification); (2) the IESC (Independent Environmental and Social Consultant) anchors that verification through pre-FC ESDD plus ongoing construction monitoring; and (3) IFC Performance Standards are the de-facto baseline that EP4 incorporates. The IESC's pre-FC ESDD typically runs 6-12 months for complex projects; for EP category A projects, the IESC is retained for quarterly construction monitoring through completion and annual post-completion monitoring.

The IESC's pre-FC site visit covers ESIA review and on-site verification, HSE statistics audit (TRIR, DART, LTI), human rights diligence per UN Guiding Principles, GHG emissions baseline, biodiversity impact assessment, indigenous peoples consultation per ILO 169 and IFC PS 7 where applicable, resettlement action plan per IFC PS 5, and disbursement-condition mapping. Documents that must be in the data room before the pre-FC report can issue: the full ESIA aligned with IFC Performance Standards plus host-country regulatory submissions, baseline E&S monitoring data, the Stakeholder Engagement Plan and grievance mechanism log, the Indigenous Peoples Plan and Resettlement Action Plan where applicable, the Action Plan tracking remaining gaps with timelines, climate risk and resilience documentation, and the project company's E&S management system documentation.

Lender expectation across the IESC scope-of-work: the IESC's pre-FC report sits in the data room indexed by chapter and signed by the consultant's senior partner; quarterly construction monitoring reports through completion sit in a parallel folder gated to the lender pool plus the project company's HSE manager. For Papua LNG (TotalEnergies operator), IESC is currently reviewing E&S aspects on behalf of the future lender pool per TotalEnergies disclosures — the typical 6-12 month ESDD cycle that gates Phase 5 completion. For Mozambique LNG, the IESC re-engagement after the November 2025 force-majeure lift is the live reference for IESC scoping under amended financing. Peony Data Room at $52/admin/month preserves the per-page audit trail across the IESC's pre-FC ESDD and quarterly site visits with dynamic watermarks tagging every page — see /solutions/energy for the LNG-specific use cases.

How do FOB, DES, and tolling LNG SPAs differ in data room composition?

FOB, DES, and tolling are the three offtake structures under which an LNG project's revenue side gates to lender bankability — and data room composition differs across all three because each shifts shipping risk, title transfer point, and ancillary documentation requirements differently. FOB is the dominant structure in 2025 by a wide margin: 75% of US LNG contractual volumes were FOB, 12% DES, 13% FOB / DES flex per EIA. Over 90% of LNG volumes sold in 2025 were under FOB SPAs; approximately 95% were 20-year SPAs; 56% are Henry Hub indexed.

FOB (Free On Board). Title and risk transfer to the buyer at the loading flange of the LNG carrier at the loading terminal; buyer arranges shipping. The AIEN 2025 Model LNG Sale and Purchase Agreement FOB is the new industry standard for medium- to long-term FOB on take-or-pay basis, replacing earlier AIPN models — addressing daily contract quantity (DCQ), annual contract quantity (ACQ), volume tolerance, take-or-pay shortfall mechanics, and make-up rights. Data room implications: lighter doc mass on the seller side (no shipping fleet documentation), with the LNG SPA(s), lifting schedule, loading terminal compatibility, port and channel documentation, and buyer's vessel suitability documentation (VSDA) in the lender pack.

DES (Delivered Ex Ship, sometimes DAP / DAT). Seller arranges shipping; title and risk transfer at the discharge terminal. Data room implications: heavier doc mass with the LNG SPA plus bareboat charter or time charter agreements (LNG carriers), LNG vessel insurance certificates, discharge terminal access agreements, slot agreements at receiving regas terminal, and shipping risk management documentation.

Tolling. Project company sells LNG FOB at price equal to (Henry Hub feed-gas cost) plus (fixed liquefaction fee) plus (margin) — used predominantly by US tolling-model projects per Timera Energy. Data room implications: heaviest doc mass with the liquefaction services agreement (LSA), feed-gas supply agreement (e.g., the Woodside-bp feed-gas supply for Louisiana LNG referenced in Riviera), tolling fee structure documentation, and capacity reservation agreements. Tolling-model US projects are the asset class where midstream gas-pipeline diligence overlaps directly with LNG offtake economics — the feed-gas supply chain runs through FERC-regulated interstate pipelines whose tariff and certificate diligence is the parallel midstream workstream — see the midstream pipeline acquisition data room playbook for the FERC Tier A-E document escalation framework on the upstream-pipeline side of LNG project finance.

Indexation patterns across LNG SPAs: Henry Hub-linked (dominant for US LNG, 56% of 2025 contracted volumes per EIA), JKM Japan-Korea Marker (Asia spot), Brent-linked / oil-linked (Asian long-term contracts), TTF-linked (European deliveries), and hybrid / formula structures with min/max collars.

| SPA Structure | Title transfer | Shipping risk | Doc mass implication | Insurance evidence required |

|---|---|---|---|---|

| FOB | Loading flange | Buyer | Lighter (no shipping fleet) | Buyer's P&I + H&M (vessel suitability) |

| DES (DAP / DAT) | Discharge | Seller | Heavier (charter agreements + cargo insurance) | Seller's cargo insurance + LNG carrier H&M |

| Tolling | At LSA delivery point | Off-taker | Heaviest (LSA + feed-gas + capacity reservation) | Tolling capacity + feed-gas supply documentation |

For a 20-year take-or-pay anchor offtake to underpin lender bankability, FOB under the AIEN 2025 model is the structure that best fits — NextDecade Rio Grande Train 5's 4.5 MTPA of 20-year SPAs with JERA, EQT Corporation, and ConocoPhillips is the recent benchmark for FOB take-or-pay underpinning a $6.7B FID. The data room implication is that the SPA pack gates to T4 (lender) tier plus buyer's external counsel, with each offtaker's executed SPA in its own visitor group so JERA never sees the EQT or ConocoPhillips redlines and vice versa.

How big is a typical LNG project finance data room at FID?

A typical LNG project finance data room at FID is 80-200 GB for greenfield LNG — sometimes 300+ GB for the largest greenfield projects with full ECA debt packages — across the five FID-stage content categories defined by the FEED→FID document escalation curve. The structural composition: EPC bid responses 60-150 GB per consortium (Category A, dominating Phase 5 doc mass), reservoir plus operational pack 10-30 GB (Category B), commercial / offtake pack 5-15 GB (Category C), project finance package 10-30 GB (Category D), and regulatory / ESIA pack 5-10 GB (Category E).

Where the envelope stretches to 200-300+ GB: EPC bid responses scale with consortium count (3-5 active bidders × 60-150 GB each compounds to 300-750 GB pre-shortlist; once bid evaluation collapses to a single awarded contractor at FID, the room re-baselines to the 80-200 GB working envelope). Post-FID through financial close and construction the room scales further as disbursement documentation, ITA monthly progress certificates, IESC quarterly E&S monitoring, change-order documentation, and EP ongoing monitoring reports accumulate.

The counterparty count at LNG-tier FID is what makes the data-room architecture distinct from upstream M&A: 12-25 active diligence counterparties typically — operator (T1), state partner / NOC (T3), 2-6 EPC consortium bidders (parallel until FID award), 8-15 lender-side institutions (commercial banks plus 3-6 ECAs plus multilaterals plus DFIs), each lender's external counsel (typically Hunton AK, Willkie Farr, White & Case, Latham & Watkins per published LNG project-finance practice descriptions), the lender's ITA, the IESC under EP4, lender's market consultant, insurance advisor, and tax advisor. The 50-150 named individuals working across 12-25 organizations is the working norm — and the data room must preserve per-page audit-trail granularity across all of them through a 14-month FID-to-FC window plus the multi-year construction phase.

Vertical-fit cases — onshore liquefaction vs FLNG vs floating storage:

- Onshore liquefaction (NextDecade Rio Grande, Venture Global CP2, Woodside Louisiana LNG, Commonwealth LNG): full P&ID set across multiple liquefaction trains plus storage tanks plus loading jetties; 80-200 GB EPC bid pack at FID; FERC §3 export approval plus DOE export authorization for non-FTA countries.

- FLNG (Eni Coral North, Coral Sul, Pluto Train 2 onshore-with-offshore-feed): integrated hull-plus-topsides bid pack with class-society documentation (ABS, DNV, Lloyd's Register), flag-state registration, IMO Type C cargo containment system specifications, modular fabrication at Korean or Chinese yards, marine logistics for hull tow-out plus topsides integration; typically 50-100 GB integrated technical pack at FID with 10-30 GB marine-logistics tracking layered in.

- Floating storage and regasification (FSRU): lighter than FLNG on the liquefaction side but additional vessel-fleet documentation; typically smaller absolute file mass.

The Pluto Train 2 (Scarborough Energy Project) reference — Woodside operator, Bechtel EPC, 5 MTPA capacity, 96% complete in Q1 2026 with all 51 modules (56,000 tonnes) shipped from Batam Indonesia by December 2024 and first LNG targeted Q4 2026 per Woodside ASX — is the working late-stage onshore comparator for module-fabrication tracking. The Bay du Nord oil project (Equinor 60% operator plus bp 40%, with BW Offshore as preferred FPSO contractor under FEED agreement signed September 2025 and FID anticipated 2027 per PGJ Online — current ownership reflects Cenovus's 35% transfer to bp in 2022) is the working FPSO-architecture parallel to FLNG from a data room composition perspective.

What does Peony do that legacy LNG data room platforms don't on FID-stage 100GB+ EPC bid packs?

Peony Data Room at $52/admin/month handles FID-stage LNG project finance data rooms — 80-200 GB at FID, 200-300+ GB through post-FID financial close and construction — at a cost structure that decouples from data volume and counterparty count, while preserving the security primitives that gate disbursement-condition documentation under Equator Principles 4 and ECA covenants. The structural cost wedge against Datasite per-page billing is 7-22x on data-heavy FID-stage workflows — a six-figure invoice on legacy enterprise VDRs becomes a few thousand dollars on flat per-admin pricing.

Five capabilities that matter for FID-stage LNG project finance:

- No per-file cap. A 100-150 GB EPC LSTK bid pack uploads in a single chunked transfer with the audit trail preserved. Datasite caps single files at 10GB with zip files supported up to 50GB; Intralinks caps single files at 25GB across US, Germany, and Australia per Intralinks release notes; Firmex caps drag-and-drop at 10GB. Box Enterprise Advanced supports 500GB single-file uploads but ships zero NDA gates, dynamic watermarks, or screenshot protection — fails the basic 4-tier farm-out test.

- NDA gates with integrated e-signatures. Each bidder, lender, ECA, multilateral, and counsel signs the data room's NDA inline before any documents are visible. Signature record exportable as PDF audit trail satisfying disbursement-condition documentation under Equator Principles or ECA covenants.

- Dynamic watermarks tagging every page with viewer name, email, IP, and timestamp — across full P&ID sets, MTOs, audited reserves reports, executed offtake SPAs, and ECA covenant documents.

- Screenshot protection on desktop and mobile — non-negotiable for reserves engineers reviewing SPE-PRMS 2P certifications and lender counsel evaluating PV-10 reconciliations.

- Programmatic visitor groups expressing the LNG-extended 4-tier farm-out access model (operator / IOC bidder / state partner / EPC consortium / commercial bank / ECA / multilateral / external counsel / ITA / IESC / market consultant) without manual permission resets across the 14-month FID-to-FC window and the multi-year construction phase. Page-level analytics preserve per-page dwell time, per-document NDA signature record, watermark version log, and screenshot block attempts.

Trade-offs to be honest about: Peony does not ship a dedicated FERC docket cross-reference workflow (FERC docket lookup runs through standard search); Datasite remains the de-facto procurement standard at certain multilateral project-finance groups where buyer-side procurement expects a Datasite-branded room; Intralinks ships pre-built farm-out workflow templates at enterprise tier with SS&C Technologies' pedigree on $35T+ in transactions processed. Where those defaults are hard requirements, the legacy choice still applies. Where the data room is selected by the lender-side admin team rather than dictated by sponsor-side procurement, Peony becomes structurally compelling across a 14-month FID-to-FC window — for a 5-admin lender team that's $3,640 total versus $50,000+ on enterprise per-project pricing.

For smaller admin teams, Peony Business at $30/admin/month ships the NDA gate and screenshot stack with document and data-room caps (up to 1,000 docs and 3 data rooms per admin) — a fit for sell-side advisor teams of 2-3 admins on a single mandate. For the full FID-stage lender-side syndicate with 4-8 admins on a 14-month window, Peony Data Room at $52/admin/month is the right tier, adding dynamic watermarks and unlimited data rooms.

Cluster anchors for further reading: the 10 best data rooms for oil and gas companies (2026); the 42-document oil and gas data room checklist; the 7-step farm-out workflow plus 4-tier access model; the large-file data room with NDA gates; and /solutions/energy.

Frequently asked questions

I'm head of IR at an offshore LNG sponsor entering FEED with a state partner and pre-engaging project finance lenders — how big does my data room get from FEED entry through FID, and which phase produces the biggest doc-mass jump?

For your offshore LNG sponsor entering FEED with a state-partner equity vehicle and pre-engaging project finance lenders, the data room scales through six discrete phases — concept select (~1-2 GB), FEED entry (~5 GB), mid-FEED (~10-25 GB), FEED completion (~25-50 GB), pre-FID lender diligence pack (~80-200 GB and sometimes 300+ GB for greenfield LNG with full ECA debt package), and post-FID financial close plus construction (200-300+ GB). The biggest doc-mass jump is the FEED-completion to pre-FID transition — that's where the EPC bid responses land at 60-150 GB per consortium, the executed offtake SPAs come in, the ECA term sheets stack across 3-6 export credit agencies, and the IESC's pre-financial-close report under Equator Principles 4 (effective October 1, 2020) closes the diligence pack. I call this the FEED→FID document escalation curve — it extends the broader FID cliff frame from the oil and gas data room cluster anchor specifically to project-finance LNG. The non-linearity matters for procurement: a Phase 1 to Phase 4 data room (under 50 GB) runs comfortably on most VDRs, but the Phase 5 jump to 80-200 GB is where Datasite per-page billing creates six-figure invoices on a workflow that flat per-admin pricing handles for $52 per admin per month. Peony Data Room at $52/admin/month ships unlimited storage with no per-file cap — 60-150 GB EPC LSTK bid pack uploads in a single chunked transfer, NDA-gated to the lender syndicate. Recent benchmarks anchoring this curve: NextDecade Rio Grande LNG Train 5 reached positive FID and financial close on October 16, 2025 with $6.7 billion committed financing per NextDecade IR ($3.59B term loan plus $0.50B private placement notes plus $1.29B NextDecade equity plus $1.29B Financial Investors equity from GIP/BlackRock plus GIC plus Mubadala); Venture Global CP2 Phase 1 closed $15.1B financing on July 28, 2025 — the largest standalone project financing ever — across a 28-bank lender pool per company filings.

I'm a desk MD at an LNG project finance bank reviewing a $15B greenfield FID — what documents must be in the lender diligence pack at FID, and how do I confirm IESC has signed off under Equator Principles 4 before I disburse?

For your desk MD role at an LNG project finance bank reviewing a $15B greenfield FID, the lender diligence pack at FID must contain five document categories scoping ~80-200 GB total. First, executed EPC contracts (LSTK preferred for bankability per A&O Shearman LNG project finance practice — typical bid-pack mass 60-150 GB per consortium for full P&ID set, isometrics, MTOs, EDS package, schedule of values, payment milestone schedule, performance and parent-company guarantees, liquidated damages structure). Second, executed offtake SPAs — under the AIEN 2025 Model LNG Sale and Purchase Agreement FOB (the new industry standard for medium- to long-term FOB take-or-pay, replacing earlier AIPN models), with 75% of US LNG contractual volumes in 2025 sold FOB, 12% DES, 13% FOB/DES flex per EIA. Third, the project finance package — project finance model plus sensitivity matrix plus tax model, ECA term sheets across the syndicate (JBIC, KEXIM, US EXIM, UKEF, Bpifrance Assurance Export, Sinosure where applicable), multilateral term sheets (IFC, ADB, EBRD), common terms agreement, intercreditor agreements, completion guarantees, and direct agreements with project counterparties. Fourth, the reservoir and operational pack — final SPE-PRMS 2P certification with audited reserves, reservoir simulation model, production-and-export profile. Fifth, the regulatory and ESIA pack — final ESIA per Equator Principles 4, all regulator approvals (FERC §3 export approval and DOE export authorization for non-FTA countries in the US, equivalent NOPSEMA / OPRED approvals internationally). Confirming IESC sign-off under EP4 before disbursement: the Independent Environmental and Social Consultant must have completed pre-financial-close ESDD (typically 6-12 months for complex projects), conducted at least one pre-FC site visit, issued the pre-FC report with Action Plan, and (for Equator Principles category A projects) be retained for quarterly construction monitoring through completion. Peony Data Room at $52/admin/month preserves audit-trail granularity across the FID-to-FC window — for a 5-admin lender team running 14 months that's $3,640 total versus $50,000+ on Datasite or Intralinks at enterprise tier per Capterra-aggregated buyer data 2026. The Mozambique LNG syndicate is the live reference for ECA renegotiation under amended financing — force majeure lifted November 7, 2025; US EXIM $4.7B re-approved March 13, 2025; UKEF $1.15B withdrew December 2025; updated $20.5B budget per TotalEnergies Q3 2025 earnings call October 30, 2025.

I'm a credit officer at a Japanese / Korean ECA reviewing an LNG project finance package — what documents prove eligible Japanese / Korean content for full guarantee coverage, and how do I track quarterly disbursement-condition compliance through construction?

For your credit officer role at JBIC (Tokyo) or KEXIM (Seoul) reviewing an LNG project finance package, eligible Japanese or Korean content for full guarantee coverage is proven through five document categories layered into the data room. First, executed offtake SPA evidence with Japanese buyers (JERA, Mitsubishi, Mitsui, Tokyo Gas) for JBIC, or KOGAS for KEXIM — JBIC's offtake-driven lending model anchors disbursement to Japanese-buyer SPAs aligned with Japan's energy security policy. Second, equipment and services sourcing certifications — KEXIM typically requires ≥30% Korean equipment / services for full coverage; JBIC ties content to Japanese-supplier evidence including contract value breakdowns and parent-company certifications. Third, construction progress monitoring under JBIC Environmental Guidelines (aligned with EP4 plus IFC Performance Standards) or KEXIM E&S guidelines, including ITA (Independent Technical Advisor) monthly progress certificates. Fourth, performance bonds and parent guarantees from Korean contractors (Hyundai E&C, Samsung C&T) for KEXIM, or equivalent Japanese-contractor evidence (JGC, Chiyoda) for JBIC. Fifth, ESIA documentation aligned with each ECA's E&S framework. Tracking quarterly disbursement-condition compliance through construction: each disbursement requires contractor invoices plus the ITA monthly progress certificate plus the IESC quarterly E&S monitoring report under EP4 plus the project company officer's certificate confirming no event of default. The data room must preserve all four artifacts indexed by disbursement date with hash verification. Peony Data Room at $52/admin/month ships page-level analytics so the lender team sees per-page dwell time on the disbursement file plus per-document NDA signature record plus watermark version log — exactly the audit trail JBIC and KEXIM credit committees expect at quarterly disbursement re-validation. The Mozambique LNG syndicate originally pulled in Bpifrance, KEXIM, K-Sure, SACE, and Sinosure on the 2020 financing per Defund TotalEnergies and trade press; that depth of ECA layering is the working reference for Japanese-Korean content tracking on greenfield LNG. See the oil and gas data room checklist for the underlying 42-document gating matrix that the FID-stage data room extends.

I'm a proposal director at an LNG EPC contractor preparing a $10B+ bid — how does the data room composition differ between an LSTK bid and a convertible / target-cost bid, and what audit-rights documentation does the lender require for reimbursable scopes?

For your proposal director role preparing a $10B+ EPC bid, the data room composition differs materially across LSTK, convertible / target-cost, and reimbursable structures. LSTK (lump sum turnkey) bid packs run 60-150 GB per consortium because the contractor must price every component upfront — locked sub-contractor quotes, locked schedule of values, detailed P&IDs and MTOs at bid, performance liquidated damages capped high, and limited post-FID change-order documentation because the base scope is fixed (per A&O Shearman's published LNG EPC practice). Bechtel's revised LSTK with Woodside on Louisiana LNG, signed December 2024 ahead of FID in late April 2025, is the recent reference at $17.5B for the 16.5 MTPA three-train foundational phase per Woodside ASX disclosures and PGJ Online; NextDecade's Rio Grande Train 5 issued full notice to proceed to Bechtel under LSTK on October 16, 2025; Commonwealth LNG / Technip Energies signed LSTK under the May 2024 FID at approximately $4.8B for 9.3 MTPA per EPC Intel. Convertible / target-cost bid packs run 50-70 GB upfront — initially structured with cost-reimbursable mechanics (target price plus sharing formula) with a conversion mechanism to LSTK once design risk retires. This structure has become more common in 2024-2026 because contractors are reluctant to take full LSTK risk on first-of-kind LNG; Worley's CP2 LNG Phase 2 contract under Venture Global is reimbursable target-cost per Venture Global IR, with FID for Phase 2 reached March 13, 2026. Convertible structures carry heavier financial-controls documentation — open-book cost reporting, audit-rights protocols, and change-order procedures that must be programmatically gated to the lender's technical advisor. Reimbursable (cost-plus) bid packs run thinner upfront at 30-50 GB but the heaviest change-order, audit, and cost-reporting documentation across construction. ECAs and project finance lenders historically prefer LSTK for bankability — reimbursable scopes carry lender pushback unless the audit-rights documentation gates cleanly to the lender's ITA. Peony Data Room at $52/admin/month handles all three structures through programmatic visitor groups with dynamic watermarks — the contractor's bid team sees their own LSTK technical pack while the lender's ITA sees the audit-rights view, never the runner-up bidder's pricing or change-order redlines. See the oil and gas data room platform comparison for the head-on platform analysis and the large-file data room with NDA gates deep-dive on file-mass mechanics for 100GB+ EPC bid packs.

I'm an E&S officer at IFC reviewing an LNG project finance package — what does the IESC site visit cover under Equator Principles 4, and what documents must be in the data room before the IESC's pre-financial-close report can be issued?

For your E&S officer role at IFC reviewing an LNG project finance package, the IESC (Independent Environmental and Social Consultant) site visit under Equator Principles 4 (effective October 1, 2020) covers ESIA review and on-site verification, HSE statistics audit (TRIR, DART, LTI), human rights diligence per UN Guiding Principles, GHG emissions baseline, biodiversity impact assessment, indigenous peoples consultation per ILO 169 and IFC Performance Standard 7 where applicable, resettlement action plan per IFC PS 5, and disbursement-condition mapping. EP4 is the framework where all designated-country projects are no longer 'deemed in compliance' solely by host country law — Equator Principles Financial Institutions require independent verification through the IESC. IFC's Performance Standards are the de-facto baseline that EP4 incorporates. Documents that must be in the data room before the IESC's pre-financial-close report can be issued: the full ESIA aligned with IFC Performance Standards plus host-country regulatory submissions, baseline environmental and social monitoring data (air, water, noise, biodiversity, social), the Stakeholder Engagement Plan and grievance mechanism log, the Indigenous Peoples Plan where applicable, the Resettlement Action Plan with compensation matrix where applicable, the Action Plan tracking remaining gaps with timelines, the climate risk and resilience documentation, and the project company's E&S management system documentation. The IESC's pre-FC ESDD typically runs 6-12 months for complex projects, with at least one pre-FC site visit and (for EP category A projects) quarterly construction monitoring through completion. The Papua LNG project under TotalEnergies (37.55% operator), ExxonMobil (37.04%), Santos (22.83%), and JX Nippon (2.58%) is the live reference where IESC is currently reviewing E&S aspects ahead of FID, with EPC candidates JGC and Hyundai E&C selected per TotalEnergies disclosures; multilateral participation (IFC, ADB) anchors the catalytic effect that signals E&S compliance to commercial banks. The 10-MDB Global Co-financing Platform launched October 2024 (including IFC, ADB, EBRD, AIIB) streamlines co-financing across multilaterals — that's the institutional infrastructure that frames quarterly IESC reporting at IDA-eligible LNG sites. Peony Data Room at $52/admin/month preserves the per-page audit trail across the IESC's pre-FC ESDD and quarterly site visits — see /solutions/energy for the LNG-specific use cases.

I'm corp-dev at an LNG sponsor finalizing offtake structure decisions for FID — how does the data room composition differ between FOB, DES, and tolling under the AIEN 2025 Model SPA, and which structure best fits a 20-year take-or-pay anchor offtake to underpin lender bankability?

For your corp-dev role at an LNG sponsor finalizing offtake structure decisions for FID, the data room composition differs across FOB, DES, and tolling in three load-bearing ways. FOB (Free On Board) is the dominant structure — 75% of US LNG contractual volumes in 2025 were FOB, 12% DES, 13% FOB/DES flex per EIA. The AIEN 2025 Model LNG Sale and Purchase Agreement FOB (published 2025 by AIEN, formerly AIPN — the Association of International Petroleum Negotiators became the Association of International Energy Negotiators in 2022) is the new industry standard for medium- to long-term FOB on take-or-pay basis, addressing daily contract quantity (DCQ), annual contract quantity (ACQ), volume tolerance, take-or-pay shortfall mechanics, and make-up rights. Title and risk transfer to buyer at the loading flange of the LNG carrier; buyer arranges shipping. Data room implications under FOB: lighter doc mass (no shipping fleet documentation seller-side), with buyer's vessel suitability documentation (VSDA), port and channel documentation, and loading terminal compatibility evidence in the lender pack. DES (Delivered Ex Ship, sometimes DAP / DAT) shifts shipping risk to seller — title and risk transfer at discharge terminal. Data room implications under DES: heavier doc mass with bareboat charter or time charter agreements for LNG carriers, LNG vessel insurance certificates, discharge terminal access agreements, slot agreements at receiving regas terminal, and shipping risk management documentation. Tolling (predominantly used by US tolling-model projects per Timera Energy) is the heaviest data-room load — project company sells LNG FOB at price equal to Henry Hub feed-gas cost plus fixed liquefaction fee plus margin. Tolling implications: liquefaction services agreement, feed-gas supply agreement (e.g., the Woodside-bp feed-gas supply for Louisiana LNG referenced in Riviera and Woodside ASX), tolling fee structure documentation, capacity reservation agreements. For a 20-year take-or-pay anchor offtake to underpin lender bankability, FOB under the AIEN 2025 model is the structure that best fits — over 90% of LNG volumes sold in 2025 were under FOB SPAs, approximately 95% of 2025 volumes were 20-year SPAs, and 56% of 2025 contracted volumes are Henry Hub indexed per EIA. NextDecade Rio Grande Train 5's commercially supporting 4.5 MTPA of 20-year SPAs with JERA, EQT Corporation, and ConocoPhillips is the recent benchmark for FOB take-or-pay underpinning a $6.7B FID. Peony Data Room at $52/admin/month ships unlimited storage with no per-file cap — full SPA stacks under FOB or DES load without splitting, with NDA gates per offtaker tier and dynamic watermarks tagging every redline.

I'm watching the NextDecade Rio Grande Train 5 close at $6.7B in October 2025 and Venture Global CP2 Phase 1 close at $15.1B in July 2025 — what does the documentation timing look like for a FID where commercial banks alone (no ECAs) anchor the syndicate?

The documentation timing on a FID where commercial banks alone anchor the syndicate (no ECAs) compresses three workstreams that ECA-led financings typically run sequentially. NextDecade Rio Grande LNG Train 5 reached positive FID and financial close on October 16, 2025 with $6.7 billion in committed financing per NextDecade IR — $3.59B term loan plus $0.50B private placement notes plus $1.29B NextDecade equity plus $1.29B Financial Investors equity from GIP/BlackRock, GIC, and Mubadala. Train 5 is 6 MTPA (NextDecade's total nameplate is 30 MTPA), commercially supported by 4.5 MTPA of 20-year LNG SPAs with JERA, EQT Corporation, and ConocoPhillips, with full notice to proceed issued to Bechtel under LSTK on the same day per PGJ Online and substantial completion targeted H1 2031. Venture Global's CP2 Phase 1 closed $15.1 billion project financing on July 28, 2025 — the largest standalone project financing ever — across a 28-bank lender pool that included Bank of America, Barclays, Goldman Sachs, J.P. Morgan, Mitsubishi UFJ, Mizuho, MUFG, SMBC, Santander, Standard Chartered, ING, Natixis, and Deutsche Bank, with over $34 billion in commitments collected per Latham & Watkins (Venture Global counsel) and Skadden (lender counsel). Lead arrangers were ING and Santander on the construction term loan and working capital facility, BofA and Scotiabank on the equity bridge loan. CP2 Phase 1 is 14.4 MTPA with first LNG targeted 2027. The documentation timing implication: with no ECA-content gating layer, the disbursement-condition documentation collapses from a 6-ECA matrix (each with its own content certification, sourcing evidence, and ESIA framework) down to a single common-terms-agreement disbursement matrix indexed to ITA monthly progress certificate plus IESC quarterly E&S monitoring under EP4 plus project company officer's certificate. Three workstreams that ECA-led syndicates run sequentially run in parallel here — the EPC LSTK technical pack (60-150 GB), the offtake SPA pack (executed FOB SPAs with 20-year take-or-pay), and the project finance model with sensitivity matrix all gate to the lender pool simultaneously through a single visitor-group hierarchy. Venture Global CP2 Phase 2 reached FID and financial close on March 13, 2026 with Worley awarded reimbursable target-cost EPC; the all-in CP2 capex could reach approximately $28B per company filings. Peony Data Room at $52/admin/month handles the parallel-workstream load through programmatic visitor groups — for a 28-bank pool with 5 admins on the lender-counsel side that's $3,120/year flat, versus six-figure invoices on Datasite per-page billing.

I'm an ECA credit officer in the Mozambique LNG syndicate watching the November 2025 force-majeure lift, US EXIM March 2025 re-approval of $4.7B, and UKEF / Atradius December 2025 withdrawal — how does the data room handle ECA renegotiation under an amended financing agreement?

For your ECA credit officer role in the Mozambique LNG syndicate, the data room handles ECA renegotiation under an amended financing agreement by partitioning the original 2020 financing pack from the post-force-majeure amendment pack — preserving both as parallel disclosures with version-controlled audit trail. The Mozambique LNG project (TotalEnergies operator) reached force majeure in 2021 after the security incident in Cabo Delgado; force majeure was formally lifted on November 7, 2025 per TotalEnergies disclosures. The original 2020 financing pulled $14.9-15.4B across approximately 30 lenders with ECAs Bpifrance, KEXIM, K-Sure, SACE, and Sinosure participating per Defund TotalEnergies and trade press. US EXIM's $4.7 billion loan was re-approved on March 13, 2025 — supporting an estimated 16,400 jobs across 68 companies in 14 states. UKEF's $1.15B (originally agreed in 2020) was formally withdrawn in December 2025 amid security and ethical concerns per GTR; TotalEnergies replaced lost UKEF and Atradius cover with other lenders. The updated $20.5B budget is per TotalEnergies' Q3 2025 earnings call on October 30, 2025; first LNG is targeted for 2029. Data room mechanics for ECA renegotiation: the original common terms agreement, original ECA term sheets, and original direct agreements stay in the room as the baseline pack for the approximately 90% of lenders that reaffirmed commitment. The amendment pack — re-validated ESIA per Equator Principles 4 (originally July 2020 framework still controlling), updated security risk assessment, IESC re-engagement scope, force-majeure-and-restart documentation, and the post-FM disbursement-condition matrix — sits in a parallel folder gated to the amended-financing parties. UKEF's withdrawal triggers a separate carve-out: the UKEF facility documentation is preserved for audit-trail integrity but flagged as superseded; replacement-lender documentation gates to the new participants only. US EXIM's re-approval triggers another carve-out: the March 13, 2025 board minutes, US content re-certifications, and OFAC sanctions diligence sign-off (post-2022 critical) gate to the US EXIM credit officer view. Peony Data Room at $52/admin/month preserves the per-document version log and per-page audit trail across the multi-year amendment cycle — for the 14-month window from US EXIM March 2025 re-approval through December 2025 UKEF withdrawal, that's $52/admin per month flat, versus per-project enterprise contracts that re-bill on the amendment cycle.

I'm a proposal director at a contractor bidding on a floating LNG (FLNG) project — what's different in the FLNG data room vs onshore liquefaction, and how does the Coral North FLNG Mozambique FID October 2025 archetype frame Technip Energies' Coral Sul-to-Coral Norte progression?

For your proposal director role bidding on a floating LNG (FLNG) project, the FLNG data room differs from onshore liquefaction in five concrete categories that compress the typical onshore liquefaction stack and add marine-vessel-specific documentation. First, the EPC technical pack centers on the FLNG vessel (hull, topsides, integrated mooring system) rather than onshore liquefaction trains — that means class-society documentation (ABS, DNV, Lloyd's Register), flag-state registration, and IMO Type C cargo containment system specifications layer in alongside conventional process P&IDs. Second, modular fabrication scheduling dominates the document mass — module yard plans (typically Korean or Chinese yards including Samsung Heavy Industries, DSME / Hanwha Ocean, Hyundai Heavy Industries), fabrication progression tracking, and marine logistics for hull tow-out plus topsides integration replace onshore civil and structural detail. Third, the marine logistics pack is heavier on FLNG — hull-fabrication-yard agreements, transportation insurance for tow-out, met-ocean data for the field mooring location, and pre-installation seabed surveys. Fourth, the regulatory pack for FLNG centers on host-country offshore safety regulators (Mozambique INP, Australian NOPSEMA, Brazilian ANP, Namibian Ministry of Mines and Energy) plus IMO marine compliance, rather than FERC §3 land-based authorizations. Fifth, the offtake structure under FLNG typically defaults to FOB at the discharge of the FLNG vessel rather than DES, with shipping handled by the buyer's fleet. Eni's Coral North FLNG Mozambique reached FID on October 2, 2025 in Maputo — 3.6 MTPA newly built FLNG with the JV structure Eni 50% (operator) plus CNPC 20% plus ENH 10% plus KOGAS 10% plus ADNOC's XRG 10%, EPC awarded to Technip Energies, first LNG targeted 2028. The Coral Sul-to-Coral Norte progression frames Technip Energies' FLNG track record: Coral Sul was the first FLNG in Area 4 (operating since 2022; EPC delivered by the TJS Consortium of TechnipFMC, JGC, and Samsung Heavy Industries with Technip Energies inheriting the program post the February 2021 spinoff from TechnipFMC), and Coral North extends that module-fabrication and marine-integration capability to a second 3.6 MTPA unit in the same field with Technip Energies as standalone EPC contractor. The data room implication for an FLNG bid pack is that the contractor must integrate hull-yard documentation with topsides-yard documentation across a single audit trail — typically 50-100 GB of integrated technical pack at FID, with module shipping logistics layering 10-30 GB of marine-logistics tracking. The Pluto Train 2 (Scarborough Energy Project) reference is the late-stage onshore comparator — Woodside operator, Bechtel EPC, 5 MTPA capacity, 96% complete in Q1 2026 with all 51 modules (56,000 tonnes) shipped from Batam Indonesia by December 2024 and first LNG targeted Q4 2026 per Woodside ASX. Peony Data Room at $52/admin/month handles FLNG and onshore liquefaction equally through unlimited storage with no per-file cap — the integrated hull-plus-topsides bid pack uploads in a single chunked transfer with NDA gating to the lender syndicate per the oil and gas data room cluster anchor.

I'm IR at a junior offshore LNG developer running a state-partner-co-equity FID with project finance lender syndication targeted mid-2026 — how does an offshore LNG farm-out FID data room express the 4-tier access model (operator / NOC partner / IOC bidder / lender) and what's the typical 80-200 GB FID-stage doc mass made of?

For your junior offshore LNG developer running a state-partner-co-equity FID with project finance lender syndication targeted mid-2026, the 4-tier farm-out access model expresses through programmatic permission groups that gate the typical 80-200 GB FID-stage doc mass across operator (T1), non-operating JV partner / IOC bidder (T2), state partner / NOC (T3), and project finance lender (T4) tiers. The 80-200 GB mass at FID breaks down approximately as follows: EPC bid responses 60-150 GB per consortium (Category A in the FEED→FID escalation curve) — full LSTK technical pack including P&IDs, isometrics, MTOs, EDS package, schedule of values, payment milestone schedule, performance and parent-company guarantees, liquidated damages structure, and cost-and-schedule risk register; reservoir and operational pack 10-30 GB (Category B) — final SPE-PRMS 2P certification with audited reserves, reservoir simulation model in Eclipse / Petrel RE / CMG (typically 5-20 GB), production-and-export profile, final geotechnical site investigations; commercial / offtake pack 5-15 GB (Category C) — executed offtake SPAs typically 20-year take-or-pay under AIEN 2025 Model LNG SPA FOB, bilateral charter agreements where DES applies, take-or-pay obligation schedule; project finance package 10-30 GB (Category D) — project finance model plus sensitivity matrix plus tax model, ECA term sheets, multilateral term sheets, common terms agreement, intercreditor agreements, completion guarantees, IESC pre-FC report under Equator Principles 4; regulatory and ESIA pack 5-10 GB (Category E) — final ESIA per EP4, all regulator approvals. Tier expression: T1 (operator full access) sees the bilateral state-partner side letters under the production-sharing or gas agreement; T2 (IOC bidder) sees the full JOA stack and EPC bid pack but bilateral side letters are walled; T3 (state partner / NOC including Kumul Petroleum, Petronas, Sonangol, NNPC, KazMunayGas, or vehicle-style state SPVs) sees host-government compliance documentation, local-content reporting, environmental permits, abandonment provisions, and the bilateral side letters; T4 (project finance lender across ECAs JBIC/KEXIM/US EXIM/UKEF/Bpifrance Assurance Export/Sinosure plus multilaterals IFC/ADB/EBRD plus the lender's external counsel) sees cash-flow models, FOB/DES LNG SPAs, EPC LSTK bid responses, debt-service projections, ESIA, completion guarantees, and ECA covenant documents. The recent public-market reference for offshore LNG developers running farm-out at FID stage with state-partner co-equity and project finance lender syndication — the offshore LNG developer archetype with FEED entered February 2025 and FID targeted mid-2026 (Twinza Pasca A, public-market context only per Business Advantage PNG, PNG Business News, OGJ, and Argus Media) — illustrates the deal architecture: Pasca Gas Agreement signed December 19, 2024; MRDC (state-owned PNG NOC vehicle) acquiring up to a 50 percent interest in Pasca A via Hevehe Petroleum Limited, payable in stages totaling US$160 million (K620 million); first production targeted 2029; FEED Engineering completion plus ITT issuance to potential contractors and fabrication yards expected before FID. Peony Data Room at $52/admin/month expresses the 4-tier access model through programmatic visitor groups with dynamic watermarks tagging every page including the bilateral state-partner side letters — see the oil and gas farm-out workflow playbook for the 7-step workflow that anchors how documents move across the 4 tiers, and the 42-document checklist for the underlying gating matrix.

Related resources

- 10 Best Data Rooms for Oil and Gas Companies (2026 Guide) — head-on platform comparison and the FID cliff frame

- Oil and Gas Data Room Checklist (2026): 42 Documents Across 12 Folders — the underlying document-mapping matrix

- Oil & Gas Farm-Out Data Room: 7-Step Workflow + 4-Tier Access (2026) — the workflow playbook and access-model deep dive