Oil & Gas JV Due Diligence Data Room: AFE + AIEN 2023 JOA (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Last updated: May 2026

Quick answer: Oil and gas joint-venture diligence in 2026 turns on the 4-tier JV partner-disclosure ladder (operator equity → carry-tier → working-interest → ORRI/NPI), the 5-year AFE reconciliation diagnostic (under 15 percent variance equals PASS; 15 to 30 percent YELLOW; above 30 percent RED), and the AIEN 2023 Model JOA default-stress test (Articles 6, 7, 8). Recent benchmarks: NOG plus Infinity took 49 percent of Antero's $1.2 billion Utica package; Stonepeak paid Woodside $5.7 billion for a 40 percent Louisiana LNG interest; Sempra sold 45 percent of its infrastructure unit to KKR plus Canada Pension Plan Investment Board for $10 billion. Foreign-partner FOCI mapping under Trump's February 21, 2025 America First Investment Policy NSPM now flows through the developing Known Investor Program for allied investors and triggers automatic Section 721 review for foreign-adversary partners.

I run Peony, a data room platform. The JV-buyout frames in this post come from a year of fielding diligence questions from non-operated buyer corp-dev evaluating 30-to-45-percent JV interest acquisitions, PE infrastructure associates underwriting carry-tier and working-interest commitments, foreign LP counsel mapping FOCI exposure under Trump's February 2025 America First Investment Policy NSPM, Section 721 specialist outside counsel running UBO traces on Russia and PRC partner stacks, treasury and credit teams at regional banks syndicating term-loan-A on JV-bank-collateral structures, and AIEN-model legal counsel marking up Article 6/7/8 default-stress-test scenarios. The question that defines JV-specific diligence: how is JV partner-buyout diligence structurally different from upstream divestiture or farm-out, and what does the 4-tier partner-disclosure ladder demand that the other two cluster posts don't surface?

The platform comparison anchor names the ten platforms and frames the FID cliff; the 42-document checklist catalogs what goes in each folder; the farm-out workflow playbook sequences the 7-step workflow plus 4-tier farm-out access model; the LNG project finance deep dive maps the FEED-to-FID escalation curve; the upstream divestiture deep dive anchors the 12-month timeline plus 4-tier reserves disclosure progressive-tiering matrix; the midstream pipeline acquisition deep dive covers the ROW Assignment Integrity Test plus FERC Tier A-E framework. This post is the JV partner-buyout and JV-formation deep dive anchored on the 4-tier JV partner-disclosure ladder plus AFE reconciliation diagnostic plus AIEN 2023 Model JOA default-stress test plus foreign-partner FOCI mapping.

TL;DR — the 4-tier JV partner-disclosure ladder plus AFE reconciliation diagnostic plus AIEN 2023 Model JOA default-stress test plus foreign-partner FOCI mapping defines the playbook:

- The 4-tier JV partner-disclosure ladder: Tier 1 operator-equity (operating agreement, AFEs, joint operating committee minutes); Tier 2 carry-tier (capital-call history, default events, withering-interest triggers); Tier 3 working-interest counterparty (drilling commitments, redetermination ledger, JV-bank); Tier 4 ORRI/NPI/carried-interest (royalty owner schedules, NPI conversion triggers).

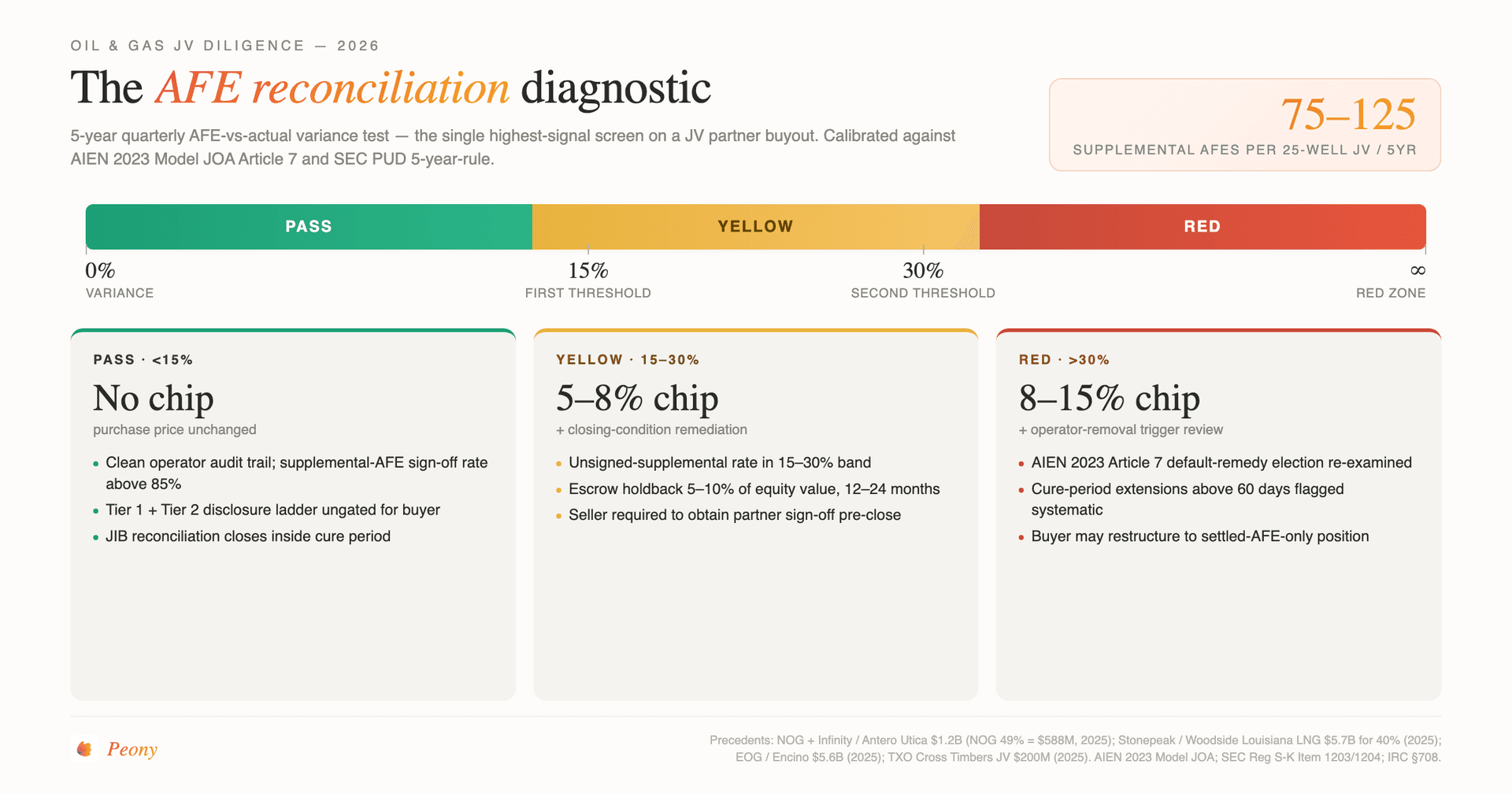

- The AFE reconciliation diagnostic: 5-year quarterly AFE-vs-actual variance test scored under 15 percent PASS, 15 to 30 percent YELLOW, above 30 percent RED. Reveals JV partner approval delays, cost-overrun-without-supplemental-AFE patterns, and operator-side opacity.

- The AIEN 2023 Model JOA default-stress test: 7-year lookback walk-through of Article 7 (Default), Article 8 (Withdrawal), Article 6 (Operating Committee voting). Withering interest is now optional rather than standard in the 2023 revision. AIEN 2019 Model Farm-In Agreement Article 3 covers Consideration (NOT Article 7).

- Foreign-partner FOCI mapping (Trump America First Investment Policy): Adversary-tier (China, Hong Kong, Macau, Cuba, Iran, North Korea, Russia, former Maduro Venezuela) triggers automatic Section 721 review; allied-investor tier flows through the developing Known Investor Program; UBO trace through 3-plus corporate layers required.

Why is JV due diligence different from upstream divestiture or farm-out?

JV due diligence is fundamentally different because it diligences the partner layer — the relationships, voting, and capital obligations between joint owners — rather than the asset itself. An upstream divestiture diligences the reserves, the operating cost stack, and the abandonment liability of an asset; a farm-out diligences the work program a farmee will earn into; a JV partner buyout or JV interest acquisition diligences the inter-partner machinery of an existing operating relationship. That distinction shapes everything about the data room structure, the document inventory, and the gating tiers.

The upstream divestiture deep dive anchored on the 12-month timeline plus 4-tier reserves disclosure progressive-tiering matrix plus PUD 5-year-rule plus seller's data room platform diagnostic test — and the upstream divestiture deep dive covers that ground. The farm-out playbook anchored on the 7-step farm-out workflow plus 4-tier farm-out access model. JV diligence is the third axis: it asks not "what is the asset worth?" or "what work will the farmee complete?" but instead "what is the partner's track record of paying cash calls, voting on operating committee, signing supplemental AFEs, and complying with default cure periods?"

The structural difference shows up in three places. First, document scope: where an upstream divestiture data room centers on reserves reports, the operating-cost stack, and the abandonment liability schedule, a JV diligence data room centers on the JOA archive (the joint operating agreement plus all amendments and side letters), the AFE history (every AFE issued plus every JIB reconciliation), the operating committee minutes archive, and the partner-financial-status archive. Second, gating tiers: where a farm-out data room uses the 4-tier farm-out access model (operator, non-operator, state partner, lender), a JV diligence data room uses the 4-tier JV partner-disclosure ladder (operator equity, carry-tier, working-interest counterparty, ORRI/NPI/carried-interest). Third, the regulatory overlay: where a midstream acquisition data room is dominated by FERC and PHMSA filings (covered in the midstream pipeline acquisition deep dive), a JV diligence data room is dominated by AIEN 2023 Model JOA default-stress testing plus the post-Trump-America-First-Investment-Policy FOCI mapping for any foreign partner.

The recent transactions illustrate the difference clearly. The Northern Oil and Gas plus Infinity Natural Resources joint acquisition of Antero Resources Ohio Utica assets for $1.2 billion announced 2025 (NOG holding 49 percent non-operated) is structurally a JV diligence — the diligence ran on the Antero operator-side AFE history, the partner-disclosure ladder for the working-interest tier, and the AIEN 2023 Model JOA default-stress test on the underlying joint operating agreement. The TXO Partners Cross Timbers JV $200 million asset divestiture is a JV-asset-divestiture diligence — the seller's IR ran exactly the AFE reconciliation diagnostic disclosed earlier. The EOG Resources $5.6 billion acquisition of Encino Acquisition Partners (a Carlyle-Riverstone JV in the Utica) was a 100-percent partnership-termination diligence under IRC Section 708 plus AIEN-Article-7 default-stress testing on every prior JV-partner default event.

What is the 4-tier JV partner-disclosure ladder?

The 4-tier JV partner-disclosure ladder is the proprietary diligence frame that maps every JV-relevant document to one of four disclosure tiers — operator equity (Tier 1), carry-tier (Tier 2), working-interest counterparty (Tier 3), or ORRI/NPI/carried-interest (Tier 4) — and gates each tier through a separate visitor-group access pattern in the data room. The ladder mirrors the 4-tier farm-out access model from the farm-out playbook and the 4-tier reserves disclosure ladder from the upstream divestiture deep dive — same architecture, JV-specific axis.

Tier 1 — Operator equity disclosures. This tier surfaces the documents that only the operator and the operator-equity-tier reviewers (typically the buyer's strategic-acquirer team plus operating-side outside counsel) need to see at the operator-relationship level. The Tier 1 archive includes the executed Joint Operating Agreement plus all amendments and side letters, every AFE the operator has issued in the lookback (initial AFEs plus supplemental AFEs), every JIB reconciliation report tying operator-billed actuals to AFE events, every operating committee meeting minutes packet (typically quarterly plus emergency meetings), every cash-call notice the operator has issued to all partners, every default notice issued under AIEN 2023 Model JOA Article 7, and every withdrawal request submitted under Article 8. The Tier 1 archive answers the question: "what has happened operationally inside this JV in the lookback window?"

Tier 2 — Carry-tier disclosures. This tier surfaces the documents specific to any partner whose interest is structured as a carry — that is, where the carrying partner pays a disproportionate share of capital costs in exchange for an enhanced interest position until a defined carry-out trigger. The Tier 2 archive includes the carry-tier capital-call history (showing every cash-call event tagged with whether the carrying partner is paying its full share or only the carry-tier share), every default event triggered against the carrying partner, every withering-interest trigger (relevant where the JOA elected withering interest as the default remedy — under the AIEN 2023 Model this is now optional rather than standard), and every reset-event in the carry mechanic (typically tied to a defined production milestone, capital-spend threshold, or calendar trigger). The Tier 2 archive answers the question: "is this carry partner converting on schedule, and what default risk does the carry mechanic expose?"

Tier 3 — Working-interest counterparty disclosures. This tier surfaces the documents specific to each non-operator working-interest partner — drilling commitments under the JOA's drilling-obligation provisions, redetermination ledger documenting any post-formation working-interest adjustment, JV-bank statement archive showing the working-interest partner's portion of inflows and outflows, and partner-by-partner credit-rating-history if the partner is publicly traded or otherwise rated. The Tier 3 archive answers the question: "is this working-interest counterparty financially capable of meeting its share of pending cash calls and complying with its drilling commitments?"

Tier 4 — ORRI/NPI/carried-interest disclosures. This tier surfaces the documents specific to overriding royalty interest, net profits interest, or carried-interest mechanics — typically the deepest-burdened tier and the one least visible to operating decisions. The Tier 4 archive includes the royalty owner schedules (every ORRI grant, every NPI grant, every carried-interest grant), the NPI conversion-trigger documentation (NPI typically converts to a working interest at a defined cumulative-revenue threshold), the carried-interest payback mechanism (typically the carrying partner recovers all its capital plus an interest premium before the carried partner becomes participating), and the royalty-burden calendar (every ORRI burden tied to specific wells with the burden percentage and the survival-period after assignment). The Tier 4 archive answers the question: "what royalty and burden tier is layered above the working-interest position, and what conversion or termination triggers are pending?"

The 4-tier JV partner-disclosure ladder maps directly onto Peony product surfaces. Tier 1 operator-equity uses Peony visitor groups to gate the operating-committee minutes and cash-call archive to operator-equity-tier reviewers only. Tier 2 carry-tier uses Peony page-level analytics to track which AFE-history pages the carrying partner's reconciliation team spent time on — that engagement signal tells the seller's IR team where the carry-out-trigger questions will land. Tier 3 working-interest uses Peony dynamic watermarks to embed reviewer name plus timestamp on every drilling-commitment page so any leak is traceable. Tier 4 ORRI/NPI uses Peony auto-indexing to recognize royalty-schedule structure across the typically hundreds of ORRI, NPI, and carried-interest documents without manual folder configuration.

How does the AFE reconciliation diagnostic work in 2026?

The AFE reconciliation diagnostic is the single highest-signal test for a JV partner buyer because AFE history is where every JV dispute originates — and the 2026 framework runs a 5-year quarterly AFE-vs-actual variance analysis scored against three thresholds (under 15 percent PASS, 15 to 30 percent YELLOW, above 30 percent RED) with three matching remediation responses (no chip, escrow holdback or operator-side closing condition, purchase-price chip plus operator-removal-trigger review). The 5-year scope tracks against US Securities and Exchange Commission PUD 5-year-rule alignment plus 7-year IRS partnership-record retention plus 1-year buyer pre-close model period — a structurally consistent calibration with the upstream divestiture 12-month timeline.

The diagnostic operates in three passes. Pass one inventories every AFE event in the 5-year lookback. The buyer's reconciliation team reads the AFE-issuance log, building a per-well AFE event series with the initial AFE date, the AFE amount, the AFE category (drilling, completion, workover, plug-and-abandon, facility, infrastructure), and the AFE-by-AFE supplemental history showing whether and when supplemental AFEs were issued for cost overruns. Pass two reconciles each AFE event against actuals by reading the JIB (joint-interest billing) archive — the operator's monthly billing to all partners showing actual costs incurred plus the operator's allocation methodology. The variance per AFE event is computed as (actual cost minus AFE amount) divided by AFE amount, expressed as a percentage. Pass three scores the 5-year aggregate against the three thresholds — under 15 percent variance equals PASS (no chip), 15 to 30 percent YELLOW (5 to 8 percent purchase-price chip plus operator-side remediation closing condition), above 30 percent RED (8 to 15 percent chip plus operator-removal-trigger review under AIEN 2023 Article 7).

Three patterns repeatedly surface in the diagnostic. First, the unsigned-supplemental pattern. Operators often skip the supplemental AFE process and bill cost overruns directly without re-approval — a 25-well JV in steady-state operation typically issues 75 to 125 supplemental-AFE events over a 5-year lookback, and the unsigned-supplemental rate is the single most common YELLOW finding. The buyer's reconciliation team scores under 15 percent unsigned-supplemental rate as PASS, 15 to 30 percent as YELLOW, above 30 percent as RED. Second, the cost-allocation methodology pattern. Operators allocate certain shared costs (rigs across multiple wells, completion crews, frac-water sourcing) by methodologies that may favor certain wells over others — the buyer's reconciliation team checks whether the allocation methodology produces consistent per-well costs over time or whether a step-change appeared at some point in the lookback window. Third, the cure-period-extension pattern. AIEN 2023 Model JOA Article 7 default-cure periods are typically 30 days for cash-call defaults, but operators frequently extend cure periods informally to maintain JV stability — the buyer's reconciliation team flags any informal cure extension above 60 days as a YELLOW finding because it signals operator willingness to accept partner-side credit deterioration.

The AFE reconciliation diagnostic ties into the broader 4-tier JV partner-disclosure ladder by surfacing Tier 1 (operator-issued AFEs) and Tier 2 (carry-tier capital-call history) evidence in parallel — the buyer's reconciliation team typically runs the AFE-issuance log against the JIB reconciliation log against the cash-call notice archive in three windowed views, looking for inconsistencies between AFE-driven cost predictions and actually-billed actuals.

Recent precedent at scale: the Northern Oil and Gas plus Infinity Natural Resources joint acquisition of Antero Resources Ohio Utica assets for $1.2 billion announced 2025 (NOG holding 49 percent non-operated for $588 million per Northern Oil & Gas IR press release, expected to close end of Q1 2026) ran the AFE reconciliation diagnostic across a multi-rig Antero-operated Utica position with detailed pass-by-pass output anchoring the partnership-equity diligence. The TXO Partners Cross Timbers JV asset sale for approximately $200 million in 2025 (TXO holding 50 percent interest, receiving $100 million net) ran the diagnostic on the seller-side as IR pre-curation before opening the data room to bidders.

Peony Data Room at $52/admin/month ships unlimited storage for the typical 12 to 20 GB of 8-year AFE archive across drilling, completion, workover, P&A, and facility AFEs, while Peony Business at $30/admin/month already includes page-level analytics tracking which AFE-event pages the buyer's reconciliation team spent time on — that engagement signal tells the seller's IR team where the chip will be requested before the buyer's first markup of the share-purchase agreement.

What does the JOA default-stress test cover under AIEN 2023?

The JOA default-stress test is the third proprietary diligence frame and the one most often handled by outside legal counsel rather than the corp-dev team — it walks the AIEN 2023 Model Joint Operating Agreement Articles 6 (Operating Committee), 7 (Default), and 8 (Withdrawal) across a 7-year lookback to surface every default event, every withdrawal request, every operating-committee voting record, and every cure-period mechanic invocation that bears on the buyer's post-close partner-relationship modeling. The 7-year buyer-side lookback tracks against US Securities and Exchange Commission PUD 5-year-rule alignment plus IRS 7-year partnership-record retention plus a 1-year buffer for the buyer's pre-close model period — a calibration buyer-side counsel chooses regardless of what the underlying JOA's executed lookback specifies.

The AIEN 2023 Model JOA Article 7 (Default) walk-through. Article 7 covers the default mechanism — what constitutes a default (typically failure to pay cash calls within the cure period), what the cure period is (typically 30 days for monetary defaults), and what remedies apply on uncured default. Modern model JOAs typically offer three default remedy options: withering interest (the defaulting partner's interest is progressively withered until extinction or until cure), forced sale at a discounted formula (the defaulting partner is forced to sell its interest to the non-defaulting partners at a defined discount to fair-market-value), or mandatory transfer (the defaulting partner's interest is automatically transferred to the non-defaulting partners pro-rata). Critically, withering interest as the default remedy is now OPTIONAL in the AIEN 2023 Model (it was one of the standard selection of remedies in earlier model JOAs) — so the buyer's outside counsel must verify which remedy the actual JOA selected. The Article 7 walk-through inventories every default notice issued in the 7-year lookback, every cure period extended or denied, and every default-remedy election (typically zero or a small number even in 7-year windows).

The AIEN 2023 Model JOA Article 8 (Withdrawal) walk-through. Article 8 covers the voluntary and forced withdrawal mechanism — when can a partner withdraw, what notice period applies, what fair-market-value buyout election the withdrawing partner has, and what cures the operating committee can apply. Modern model JOAs typically include explicit fair-market-value-buyout elections and notice-period mechanics in Article 8. The Article 8 walk-through inventories every withdrawal request submitted by any JV partner in the 7-year buyer-side lookback (typically zero or one in steady-state JVs), every withdrawal acceptance or denial by the operating committee, and every withdrawal-related buyout valuation if the buyout election was exercised.

The AIEN 2023 Model JOA Article 6 (Operating Committee) walk-through. Article 6 covers the operating committee — its composition, voting thresholds, tie-breaker mechanics, and operator-removal procedures. Operator-removal in modern model JOAs typically requires a majority of non-operator interests as the voting threshold (the precise threshold depends on the executed JOA). The Article 6 walk-through inventories every operating committee meeting minutes packet for the 7-year buyer-side lookback (typically 28 to 32 quarterly meetings plus 5 to 10 emergency meetings), every voting record showing per-partner vote on each agenda item, every tie-breaker mechanic invocation, and every operator-removal vote (typically zero).

The AIEN 2019 Model Form Farm-In Agreement (FIA) cross-reference. Where the JV operates under a JOA paired with a 2019 AIEN Model FIA (typical in farm-in-then-JV scenarios covered in the farm-out playbook), the AIEN 2019 FIA Article 3 covers Consideration (NOT Article 7 — Article 7 of the FIA is a different topic). This is a frequent citation error in older M&A workpapers and the buyer's outside counsel should explicitly verify any FIA-Article-7 reference in the seller-provided diligence summary against the actual AIEN 2019 FIA structure.

Pre-2022 AIPN-referenced JOA caveat. AIPN (Association of International Petroleum Negotiators) was renamed AIEN (Association of International Energy Negotiators) in 2022 — the rename was an organizational rebrand only, not a substantive model update. Any pre-2022 JOA referencing AIPN model agreements does NOT auto-update to the 2023 AIEN Model JOA — the parties must execute a formal amendment to incorporate the 2023 model. The buyer's outside counsel must identify the JOA's vintage explicitly and confirm whether amendments have brought it forward to AIEN 2023, or whether it operates under the pre-2022 model framework.

The Stonepeak acquisition of 40 percent of Louisiana LNG from Woodside for $5.7 billion in 2025 is the recent precedent at $5B-plus scale where the JOA default-stress test ran across a 7-year Louisiana LNG joint operating history. The Sempra Infrastructure Partners 45 percent interest sale to KKR plus Canada Pension Plan Investment Board for $10 billion in 2025 illustrates the same default-stress test mechanics on the infrastructure-platform tier.

Peony Data Room at $52/admin/month ships advanced NDA gates so the outside legal counsel tier digitally signs the seller's custom NDA template before any partner-financial-status backup is visible, plus dynamic watermarks embedding the firm-name plus reviewer-name plus timestamp on every operating-committee minutes page — exactly the audit trail buyer-side outside counsel and seller-side IR both expect during the 7-year-lookback diligence cycle.

How do you map foreign-partner FOCI risk after Trump's America First Investment Policy?

Foreign-partner FOCI mapping is the fourth proprietary diligence frame and the one most reshaped by Trump's February 21, 2025 America First Investment Policy NSPM — the framework divides foreign investors into three bands (foreign-adversary, allied-investor, unaligned) and the JV-diligence data room must produce ultimate beneficial ownership trace through 3-plus corporate layers for every non-US partner in the stack. The framework operates against the developing CFIUS Known Investor Program (KIP), which streamlines pre-clearance for allied-investor candidates through advance information collection by Treasury per the March 2026 Federal Register notice seeking public comment.

Band one — foreign-adversary tier. The America First Investment Policy NSPM identifies the foreign-adversary jurisdictions as the People's Republic of China (including Hong Kong and Macau), Cuba, Iran, North Korea, Russia, and the former Maduro regime of Venezuela. Investments from these jurisdictions trigger automatic Section 721 review with tightening enforcement — even minority investments below the standard 10-percent FIRRMA threshold trigger jurisdiction if any access-rights-based test is met (board representation, observer rights, information access, or veto rights). The OFAC sanctions screening overlay applies particularly hard against Russian partners post-February 2022 invasion of Ukraine, and the BIS export-control review applies to any oil-and-gas technology transfer (geological data, completion designs, well-stimulation specifications, proprietary completion technology). For a JV with any foreign-adversary partner, the recommended remediation pathway is forced-withdrawal under AIEN 2023 Model JOA Article 8.2 (sanctions-violation trigger) — typically the OFAC SDN listing of any UBO triggers automatic forced withdrawal under most well-drafted JOAs.

Band two — allied-investor tier. The allied jurisdictions include the United Kingdom, Canada, Japan, Australia, EU member states, and other formal US allies. The developing KIP (Known Investor Program) streamlines pre-clearance for these investors through advance information collection by CFIUS — investors who voluntarily submit comprehensive information in advance can flow through expedited review when actual transactions arise. Practical KIP-pre-clearance timing today runs 60 to 90 days for full information submission plus 30 to 45 days for refresh validation; the expected post-program-launch target is 30 to 45 days for full pre-clearance. The Sempra Infrastructure Partners 45 percent interest sale to KKR plus Canada Pension Plan Investment Board for $10 billion in 2025 is the recent allied-investor precedent at scale — CPP Investment Board as a Canadian sovereign-pension-equivalent flowed through expedited review under the KIP framework.

Band three — unaligned tier. Investors from jurisdictions outside both the foreign-adversary tier and the allied-partner tier flow through standard Section 721 review. The diligence load matches the standard FIRRMA framework: Part 800 covered-transaction analysis, Part 802 real-estate-transaction analysis (relevant for asset-level real-estate components), and the 30 to 45 day declaration window via short-form filing or 60 to 75 day full-filing window. NDAA FY2026 Section 8102 expanded the national-security-sensitive-sites list to include Department of Energy national laboratories, energy production facilities, and other critical infrastructure — so a US shale operator holding a deep gas storage facility on a national-laboratory-adjacent site could trigger Section 8102 expanded jurisdiction even from unaligned-tier investors.

The UBO trace requirement. Every non-US partner in the stack requires ultimate beneficial ownership trace through 3 or more corporate layers — fund-of-funds structures, holding-company chains, and offshore-vehicle layers all need to be unwound to natural-person UBOs. The data room exhibit must include corporate organization charts showing every layer plus beneficial-owner residence and citizenship documentation plus the LP register if any partner is a fund vehicle. The buyer's outside Section 721 specialist counsel (typically firms like Wilson Sonsini or Skadden) reviews the UBO trace against the OFAC SDN list, the BIS Entity List, and the broader sanctions screening matrix.

The asset-level US-business test under 31 CFR Part 800. CFIUS jurisdiction attaches when the target is a "US business" — defined as any business with substantial US activities in critical-technology, critical-infrastructure, or sensitive-personal-data. An LNG export terminal qualifies; a midstream transmission system qualifies (covered in the midstream pipeline acquisition deep dive); an upstream Permian operating partnership qualifies through critical-infrastructure exposure. The data room must include the asset-level US-business analysis showing why the target meets the Part 800 definition.

The recent precedent on JV-diligence FOCI mapping at scale: the Stonepeak acquisition of 40 percent of Louisiana LNG from Woodside for $5.7 billion in 2025 ran the FOCI mapping on the LNG-export-terminal asset — Stonepeak as a US-headquartered infrastructure fund avoided Section 721 entirely on the Louisiana LNG transaction, but the parallel Sempra Infrastructure Partners 45 percent sale to KKR plus CPP Investment Board for $10 billion illustrated the allied-investor track via the KIP framework. The Cactus acquisition of a 65 percent controlling interest in Baker Hughes's Surface Pressure Control business in 2025 (forming a JV with Baker Hughes retaining a minority interest) is the recent precedent for new-JV-formation diligence where Cactus as a US strategic acquirer paired with Baker Hughes as a UK-headquartered listed company — the FOCI mapping on Baker Hughes flowed through the allied-investor track without triggering Section 721.

Peony Data Room at $52/admin/month ships visitor groups so the CFIUS-counsel-tier reviewer sees the FOCI-mapping plus UBO-trace plus sanctions-screening subfolders without your fund's operational data being visible — see the LNG project finance deep dive for the parallel CFIUS-counsel-tier mechanics on LNG-export-terminal JVs.

What recent JV transactions illustrate the 4-tier ladder in action?

Eight recent JV-relevant transactions over the past 18 months illustrate the 4-tier JV partner-disclosure ladder, the AFE reconciliation diagnostic, the JOA default-stress test, and the FOCI mapping in real-world deal contexts — and together they form the recency-anchor for any 2026 JV diligence engagement.

Northern Oil and Gas plus Infinity Natural Resources / Antero Resources Ohio Utica — $1.2 billion announced 2025, expected to close end of Q1 2026. Northern Oil & Gas IR press release confirmed the joint acquisition of Antero Resources Ohio Utica assets with NOG's 49 percent non-operated interest representing $588 million of the combined $1.2 billion purchase price. Structurally a JV-formation diligence — Antero is the operator, NOG and Infinity are the joint non-operated buyers, and the data room ran the AFE reconciliation diagnostic plus the partner-disclosure ladder from Tier 1 (Antero operator-equity) through Tier 3 (NOG and Infinity working-interest counterparty positions).

EOG Resources / Encino Acquisition Partners — $5.6 billion announced 2025. EOG paid $5.6 billion for Encino, structurally a 100-percent-acquisition that retired the JV partnership tier — Encino was a Carlyle-Riverstone JV in the Utica formed 2017. The transaction triggered IRC Section 708 partnership-termination plus Section 754 election plus Section 743(b) basis adjustment workpapers in the data room, plus the AIEN-Article-7 default-stress test on every prior JV-partner default event. The operator-removal threshold under AIEN 2023 was relevant for the post-close operatorship transition.

Stonepeak / Woodside Louisiana LNG 40 percent — $5.7 billion in 2025. Stonepeak acquired a 40 percent JV interest in the Louisiana LNG project from Woodside. The data room ran the JOA default-stress test on the Louisiana LNG joint operating agreement, the FOCI mapping on Stonepeak's US-fund structure (no Section 721 triggered because Stonepeak is US-headquartered), and the project-finance-tier reserves diligence cross-referenced against the LNG project finance deep dive.

Sempra Infrastructure Partners 45 percent / KKR plus Canada Pension Plan Investment Board — $10 billion in 2025. Sempra sold 45 percent of its infrastructure unit to KKR plus CPP Investment Board for $10 billion. The diligence ran the FOCI mapping on the allied-investor track — KKR as a US-headquartered fund and CPP Investment Board as a Canadian sovereign-pension-equivalent — via the developing Known Investor Program framework. The 4-tier partner-disclosure ladder anchored the operator-equity-tier (Sempra retained operator), carry-tier (the new KKR plus CPPIB structure), and ORRI/NPI-tier (any embedded royalty positions in the underlying portfolio).

Cactus / Baker Hughes Surface Pressure Control 65 percent — undisclosed value, 2025. Cactus acquired a 65 percent controlling interest in Baker Hughes's Surface Pressure Control business, forming a new JV with Baker Hughes retaining a minority. Structurally a new-JV-formation diligence with Cactus as US strategic acquirer and Baker Hughes as UK-headquartered listed company — FOCI mapping flowed through the allied-investor track without triggering Section 721.

TXO Partners / Cross Timbers JV — $200 million asset sale in 2025. Cross Timbers Energy LLC, a JV in which TXO holds a 50 percent interest, signed purchase and sale agreements to sell oil and gas properties for approximately $200 million per Fort Worth Inc plus TXO IR. TXO expects to receive about $100 million in net proceeds. Structurally a JV-asset-divestiture diligence where TXO ran the AFE reconciliation diagnostic on the seller-side as IR pre-curation before opening the data room to bidders.

Western Midstream / Aris Water Solutions — $1.25 billion closed October 2025. Western Midstream completed its acquisition of Aris Water Solutions for $1.25 billion, creating a large integrated water midstream platform in the Delaware Basin. While structurally a corporate acquisition rather than a pure JV partner buyout, the integrated-water-midstream platform formation ran joint-operating mechanics across the prior Aris customer-counterparty network — the integration touched JOA-equivalent provisions covered in the midstream pipeline acquisition deep dive.

Mozambique LNG (Total plus partners) restart — 2024 to 2025. TotalEnergies' Mozambique LNG project restarted following a multi-year force-majeure period — the restart anchored on JV-partner re-confirmation across the partner stack including Mitsui, ENH, ONGC Videsh, Bharat PetroResources, PTTEP, and others. The data room exhibits cross-referenced the LNG project finance deep dive FEED-to-FID document escalation curve plus the 4-tier JV partner-disclosure ladder against multi-party JV restart diligence.

Quick Comparison Table

| Deal | Value | Date | Tier ladder anchor | FOCI band |

|---|---|---|---|---|

| NOG + Infinity / Antero Utica | $1.2B (NOG $588M, 49%) | Announced 2025; close Q1 2026 | Tier 1 operator (Antero) + Tier 3 WI (NOG, Infinity) | All US — no FOCI |

| EOG / Encino Acquisition Partners | $5.6B | Announced 2025 | 100% partnership-termination (Section 708) | All US — no FOCI |

| Stonepeak / Woodside Louisiana LNG | $5.7B (40%) | 2025 | Tier 1 operator + Tier 3 WI (Stonepeak) | US fund (Stonepeak) — no Section 721 |

| Sempra Infrastructure / KKR + CPPIB | $10B (45%) | 2025 | Tier 1 operator (Sempra) + Tier 2 carry-tier | Allied-investor (KKR US + CPP Canada) |

| Cactus / Baker Hughes SPC | undisclosed (65%) | 2025 | New-JV formation; Tier 1 operator (Cactus) | Allied-investor (Baker Hughes UK) |

| TXO / Cross Timbers JV asset sale | $200M ($100M net to TXO) | 2025 | 50/50 JV asset divestiture | All US — no FOCI |

| Western Midstream / Aris Water | $1.25B | Closed Oct 2025 | Corporate acquisition + JOA-equivalent integration | All US — no FOCI |

| Mozambique LNG restart | force-majeure unwind | 2024-2025 | Multi-party JV restart | Mixed (Total France-allied + others) |

Which M&A advisors lead JV transactions in 2026?

The M&A advisors leading JV transactions in 2026 cluster around three tiers — energy-specialty boutiques, bulge-bracket energy desks, and infrastructure-fund-side advisors — and the choice among them shapes the data room scope, the bid-process structure, and the typical fee math. The 2026 league rankings carry forward the post-shale-consolidation pattern from 2024-2025 where energy specialty boutiques dominated mid-market while bulge-brackets handled the mega-cap consolidation wave.

Tudor Pickering Holt & Co (TPH) — top energy-IB on JV and non-operated transactions. TPH is the Houston-anchored energy boutique that consistently leads non-operated and JV-tier diligence across upstream, midstream, and energy-transition transactions. TPH is now a Stifel subsidiary (the firm-aggregate Stifel email pattern is first.last@stifel.com for partners — a frequent diligence-process-touchpoint detail). Recent JV deal credits across the past 18 months include sell-side and buy-side roles on multiple Permian and Bakken non-operated transactions plus advisory on the LNG-tier JV diligence pattern reflected in Stonepeak / Woodside Louisiana LNG.

Petrie Partners — boutique founder-led upstream advisory. Petrie is the founder-led upstream-focused boutique with deep relationships across the Permian, Bakken, and Eagle Ford operator pool. Founder-tier email pattern is firstname@petriepartners.com (e.g., andy@petriepartners.com for Andy Slentz) — a small-founder-led-firm pattern that the oil and gas farm-out playbook references.

Jefferies energy team. Jefferies has rebuilt a strong energy practice covering both upstream and midstream JV transactions. The 2026 deal flow includes infrastructure-fund-tier advisory on multiple energy-transition transactions plus traditional upstream JV partner buyouts.

RBC Capital Markets energy desk. RBC anchors a strong Calgary-and-Houston dual-axis energy practice covering Canadian upstream and US Permian-Bakken-Eagle-Ford JV transactions. RBC was the lead financial advisor on the Sunoco-Parkland $9.1 billion transaction covered in the midstream pipeline acquisition deep dive.

Citi energy investment banking. Citi handles bulge-bracket-tier energy advisory for $5 billion-plus JV interest sales and partnership-termination transactions. The Citi advisory on the ONEOK-EnLink consolidation and on Western Midstream-Aris transactions references this scale.

Houlihan Lokey energy team. Houlihan Lokey hired Andy Hull from RBC Capital Markets in May 2025 to lead the midstream M&A practice, materially strengthening Houlihan's coverage of midstream JV transactions plus restructuring-adjacent energy advisory. The Houlihan energy team handles bulge-bracket-tier mandates with strong restructuring crossover.

Evercore energy practice. Evercore handles large E&P JV transactions and partnership-termination advisory. The Kinder Morgan-Outrigger Energy II transaction at $640 million in 2025 was an Evercore lead-advised mandate (paired with Citi) per the midstream pipeline acquisition deep dive.

Bulge-bracket overlay (Goldman Sachs, Morgan Stanley, JPMorgan, Barclays, BofA). For JV transactions above $5 billion, the bulge-bracket banks frequently run the lead financial advisor role. The Sempra Infrastructure Partners $10 billion transaction had bulge-bracket-tier representation; the Stonepeak / Woodside Louisiana LNG $5.7 billion transaction had bulge-bracket bid-side coverage.

The decision rule for choosing among advisors typically breaks on three factors: (1) JV size — under $1 billion specialty boutiques dominate; $1 billion to $5 billion mixed; above $5 billion bulge-brackets lead; (2) JV tier exposure — pure-upstream transactions favor TPH and Petrie; midstream-anchored transactions favor Houlihan plus the bulge-brackets; LNG and infrastructure transactions favor Citi plus the bulge-brackets; (3) FOCI complexity — foreign-adversary-partner exits favor restructuring-adjacent practices (Houlihan, Evercore restructuring); allied-investor-track diligence favors firms with deep CFIUS counsel relationships (Citi, bulge-brackets).

The Houston regional advisory pool overlaps materially with the Houston M&A advisor mapping including the energy-specialty firms in the bank-owned-boutique tier — a useful cross-reference for sell-side teams scoping advisor selection.

How should a Peony data room be structured for a JV deal?

Peony data rooms are structured for JV deals around the 4-tier JV partner-disclosure ladder — operator equity, carry-tier, working-interest counterparty, ORRI/NPI/carried-interest — with each tier expressed as a programmatic visitor group that gates the appropriate sub-folder set without requiring manual permission resets. The platform-tier choice is typically Peony Data Room at $52/admin/month for any JV transaction above $200 million in equity value, scaling with admin count rather than per-deal pricing — a structural difference from Datasite's per-page billing that materially shifts the cost wedge on JV transactions where the data room runs across multi-year diligence cycles.

Tier 1 operator-equity visitor group. This visitor group sees the full Tier 1 archive — executed JOA, all amendments, all AFE-issuance log, all JIB reconciliation log, all operating committee minutes, all cash-call notices, all default notices under AIEN 2023 Article 7, and all withdrawal requests under Article 8. Peony visitor groups gate this access to the buyer's strategic-acquirer team plus operating-side outside counsel only. Page-level analytics tracks which AFE-history pages and operating-committee-minutes packets the buyer's reconciliation team spent time on — a continuous engagement signal that tells the seller's IR team where the chip-leverage points are forming.

Tier 2 carry-tier visitor group. This visitor group sees the carry-tier-specific archive — capital-call history filtered for the carrying partner, default events triggered against the carrying partner, withering-interest triggers (where applicable under the JOA's Article 7 election), and reset-event documentation (carry-out-trigger evidence). Peony visitor groups isolate this tier from operator-equity-tier reviewers so the carry-tier evidence does not contaminate broader operating-relationship modeling. Auto-indexing recognizes carry-tier capital-call series across the multi-year archive without manual folder configuration.

Tier 3 working-interest counterparty visitor group. This visitor group sees the working-interest-specific archive — drilling commitments under the JOA's drilling-obligation provisions, redetermination ledger documenting any post-formation working-interest adjustment, JV-bank statement archive showing the working-interest partner's portion of inflows and outflows, and partner-by-partner credit-rating history. Peony dynamic watermarks embed reviewer name plus timestamp on every drilling-commitment page so any leak is traceable to the specific bidder.

Tier 4 ORRI/NPI/carried-interest visitor group. This visitor group sees the deepest-burdened-tier archive — every ORRI grant document, every NPI grant document, every carried-interest grant document, the NPI-conversion-trigger documentation, the carried-interest-payback-mechanism documentation, and the royalty-burden calendar. Peony auto-indexing recognizes royalty-schedule structure across hundreds of ORRI, NPI, and carried-interest documents without manual folder configuration.

FOCI-counsel-tier overlay. For JVs with any foreign partner, a fifth visitor-group tier surfaces the FOCI-mapping evidence — UBO trace through 3-plus corporate layers, beneficial-owner residence-and-citizenship documentation, prior-CFIUS-filing history, country-of-domicile risk profile under the foreign-adversary tier matrix, and governance-and-control map showing the foreign partner's voting rights plus board representation plus information access. This tier is gated to the buyer's outside Section 721 specialist counsel only — typically firms like Wilson Sonsini or Skadden — without the operating-tier reviewers seeing the UBO trace.

Pricing wedge math at JV scale. Peony Data Room at $52/admin/month flat scales linearly with admin count — for a typical JV-diligence team of 8 admins (buyer corp-dev plus buyer outside counsel plus seller IR plus seller outside counsel) running a 12-month diligence cycle, the total cost is $4,992 ($52 × 8 admins × 12 months). Datasite's per-page billing on a 200 to 400 GB JV data room (typical for $1 billion-plus JV transactions) frequently exceeds $50,000 to $150,000 per deal at enterprise tier per Capterra plus Vendr plus G2 buyer data 2026 — a 10× to 30× cost gap on data-heavy diligence cycles. The Seller's JV Data Room Platform Diagnostic Test scores the platform across capability questions: can the platform handle 200-plus GB total upload (Peony unlimited; Datasite enterprise yes; Box no); can NDA gate logic enforce per-tier access including FOCI-counsel tier (Peony yes; Datasite enterprise yes; Box no); does pricing scale flat or per-page (Peony flat $52/admin; Datasite per-page); can analytics surface 5-second-page-view filtering (Peony yes; Datasite yes); can visitor groups support per-counterparty subfolder permissioning so partner-financial-status data does not leak across tiers (Peony yes; Datasite yes via permission groups). A platform scoring below 6/8 on this test is unsuitable for a JV M&A data room above $1 billion.

For sell-side JV partners running auctions, the Peony Business plan at $30/admin/month handles smaller transactions (under $50 million equity value) with a tighter feature set; for full-scope JV partner buyouts at scale, Peony Data Room at $52/admin/month is the right tier — and the oil and gas data room cluster anchor covers the full platform comparison against Datasite, Intralinks, Firmex, and the rest of the VDR market.

Bottom Line

Oil and gas joint venture due diligence in 2026 is a structurally different exercise from upstream divestiture diligence or farm-out diligence — it diligences the partner layer rather than the asset layer — and the four proprietary frames (the 4-tier JV partner-disclosure ladder, the AFE reconciliation diagnostic, the AIEN 2023 Model JOA default-stress test, and the foreign-partner FOCI mapping under Trump's America First Investment Policy) define the playbook from initial NDA through closing.

For the buyer, the playbook starts with Tier 1 operator-equity disclosures and works downward through the ladder, with the AFE reconciliation diagnostic as the single highest-signal test for partner-side opacity and the JOA default-stress test as the legal-counsel-tier validation across Articles 6, 7, and 8. For the seller, the playbook starts with pre-curation of the 4-tier ladder and the AFE-history archive before opening the data room — the worst-case outcome is a YELLOW or RED finding the seller could have remediated pre-close.

For foreign-partner JVs, the FOCI mapping under the February 21, 2025 America First Investment Policy NSPM divides foreign partners into three bands (foreign-adversary, allied-investor, unaligned) and the data room must produce ultimate beneficial ownership trace through 3-plus corporate layers for every non-US partner. The developing CFIUS Known Investor Program offers expedited pre-clearance for allied-investor candidates; foreign-adversary partners trigger automatic Section 721 review with tightening enforcement.

The recent precedent set covers $1 billion to $10 billion-plus JV transactions across upstream (NOG plus Infinity / Antero $1.2B; EOG / Encino $5.6B), LNG (Stonepeak / Woodside Louisiana LNG $5.7B), infrastructure (Sempra Infrastructure / KKR plus CPPIB $10B), oilfield-services JV-formation (Cactus / Baker Hughes Surface Pressure Control 65 percent), upstream-asset JV-divestiture (TXO / Cross Timbers $200M), water-midstream platform integration (Western Midstream / Aris $1.25B), and LNG project restart (Mozambique LNG). Each anchors at least one of the four proprietary frames in real-world deal context.

Peony Data Room at $52/admin/month handles the 200 to 400 GB JV-diligence archive across the 4-tier partner-disclosure ladder with unlimited storage, visitor groups gating each tier separately, page-level analytics tracking buyer-side engagement on AFE-history and operating-committee-minutes pages, dynamic watermarks embedding reviewer identity on every drilling-commitment page, and auto-indexing recognizing JOA-amendment series and royalty-schedule structure across the multi-year archive — at flat pricing rather than per-page billing that scales with diligence-cycle duration.

This concludes the seven-post oil and gas data room cluster. Together the cluster covers the platform comparison anchor, the 42-document checklist, the farm-out workflow playbook, the LNG project finance escalation curve, the upstream divestiture timeline, the midstream pipeline acquisition framework, and now the JV due diligence ladder — a complete playbook for upstream-through-midstream oil and gas data room structuring in 2026.

Related Resources

- Oil & gas data room cluster anchor — platform comparison + FID cliff frame

- Oil & gas data room checklist — 42-document folder mapping

- Oil & gas farm-out data room — 7-step farm-out workflow + 4-tier farm-out access model

- LNG project finance data room — FEED-to-FID document escalation curve

- Upstream oil & gas divestiture data room — 12-month timeline + 4-tier reserves disclosure progressive-tiering matrix

- Midstream pipeline acquisition data room — ROW Assignment Integrity Test + FERC Tier A-E framework

- Best M&A advisors in Houston — Houston-tier advisor mapping for energy transactions

- Large file data room with NDA gates — large-file horizontal

- Peony solutions for energy — energy-vertical solutions overview