Industrial Data Room: The One That Survives the Buyer's Engineer (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Industrial Data Room: The One That Survives the Buyer's Engineer (2026)

Last updated: July 2026

Quick answer: An industrial data room is the virtual data room for selling or recapitalizing a warehouse, distribution center, or industrial outdoor storage (IOS) site — and the thing that separates it from a generic CRE room is that it has to be built around the building's physical truth, because that's what the buyer's engineer re-trades you on. Clear height, column spacing, ESFR sprinkler and NFPA 13 commodity classification, slab capacity and floor flatness (FF/FL), dock doors and truck-court depth, heavy power, and — for IOS — the zoning verification letter and grandfathered-use proof. A folder tree built for an office tower hides exactly those documents. The 2026 market is hot (big-box >500k SF leasing reportedly up ~32% YoY, reshoring lifting warehouse demand, IOS institutionalizing on the back of Brookfield's $1.2B Peakstone deal), which means more disciplined buyers and sharper re-trades. The deal is won on how fast and cleanly the spec proof moves between the parties — which is why serious sellers run it inside a commercial real estate data room.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't underwrite buildings for a living — but I've watched hundreds of CRE deals move through data rooms, and industrial is the asset class where a generic room fails most visibly. The reason is simple: an office deal is won on the rent roll and the cap rate, but an industrial deal is won or lost on the building's physical truth. The marketing flyer says "36-foot clear, ESFR, 185-foot truck court." The buyer's engineer shows up to verify it — and the gap between the brochure and the as-built reality is where the re-trade lives. A data room organized like every other CRE room buries the exact documents that settle those fights.

So this post is the asset-specific version: how to build the room around the seven specs the engineer re-trades. A quick map of the neighborhood so you land in the right place. If you want the generic CRE process and clock — caveat emptor, the 30–90 day window, the re-trade mechanics that apply to every asset type — that's our commercial property due diligence guide, and this post goes spec-deep where that one goes process-deep. If you want the line-by-line document inventory, pair this with the real estate due diligence checklist. And if you're selling an industrial company (an operating business, not a building), you want the best industrial M&A advisors instead — different intent entirely. This post is about the data room for industrial property.

What is an industrial data room — and why can't a generic CRE room do the job?

An industrial data room is the secure, access-controlled room where the seller of a warehouse, distribution center, light-manufacturing building, or IOS site assembles the diligence package for buyers, their lenders, and a stack of third-party consultants. The function is the same as any CRE data room — stage the proof, control access, track engagement. What's different is the content and the structure, and the difference is not cosmetic.

A generic CRE data room is built like an office or multifamily deal: title, leases, financials, then a catch-all "property" folder for everything physical. That works when the building is a commodity box where the rent roll is the asset. It fails on industrial, because in industrial the building is the asset — its dimensions, its fire protection, its floor, its power, and its yard determine what a tenant will pay and therefore what the property is worth. Bury those in a generic "property" folder and the buyer's engineer can't find them, so the engineer assumes the worst and re-trades.

Here's the mental model that makes the whole post click: every industrial diligence finding is a gap between two numbers — the marketed spec and the verified spec. The flyer says 36-foot clear; the engineer measures 34. The OM says ESFR; the fire-protection report shows a system rated for a lower commodity class than the buyer intends to store. The rent roll shows full occupancy; the estoppel surfaces three months of unrecorded free rent. The room's entire job is to close those gaps before the buyer opens them — because a gap the seller surfaces is a footnote, and a gap the buyer discovers is a price cut.

That's the thesis: the data room that survives the buyer's engineer is organized around the specs the engineer will re-trade, with the proof document sitting exactly where the consultant goes looking for it.

Why is industrial real estate so hot in 2026 — and why does that make the room matter more?

Three demand engines are running at once, and all three put more disciplined, better-advised capital across the table from sellers — which is exactly when a sloppy room costs you.

1. Reshoring and nearshoring. Supply-chain reshoring is pulling manufacturing and inventory back onshore, and the warehouse demand follows it. Hines has reportedly projected roughly a 35% increase in US warehouse demand over five years driven by reshoring. New domestic production needs new domestic distribution, and that shows up as build-to-suit and big-box absorption.

2. E-commerce and last-mile. CBRE has reported that last-mile delivery will represent more than 20% of total industrial leasing by 2026. The scarce, valuable end of this is the sub-50,000 SF infill building close to population — the box that gets a package to a doorstep same-day. These are hard to build (no land in the infill ring) and therefore command a premium, which makes their spec proof — and their zoning — worth getting right.

3. The big-box rebound and IOS institutionalization. Large-format leasing came back hard: deals for warehouses larger than 500,000 SF reportedly jumped about 32% year over year (Cushman & Wakefield), with third-party logistics providers and manufacturers driving most of the activity. Meanwhile industrial outdoor storage (IOS) crossed into institutional territory — Brookfield's roughly $1.2 billion all-cash acquisition of Peakstone Realty Trust (a portfolio of about 60 IOS properties plus traditional industrial, completed May 2026) signaled that a once-overlooked, fragmented niche is now a target for the largest buyers. Sale-leaseback, too, is again a mainstream institutional strategy for owner-operators monetizing the boxes they occupy.

The through-line: hot market, but smarter buyers. A REIT acquisitions team, a logistics fund, and a 1031 buyer racing a 45-day clock all show up with a PCA consultant and a fire-protection engineer. They are not going to take the flyer's word for the clear height. The hotter the market, the more the deal turns on whether your room lets them verify the spec fast — or forces them to assume the worst.

What does a buyer's engineer actually re-trade? (The signature spec table)

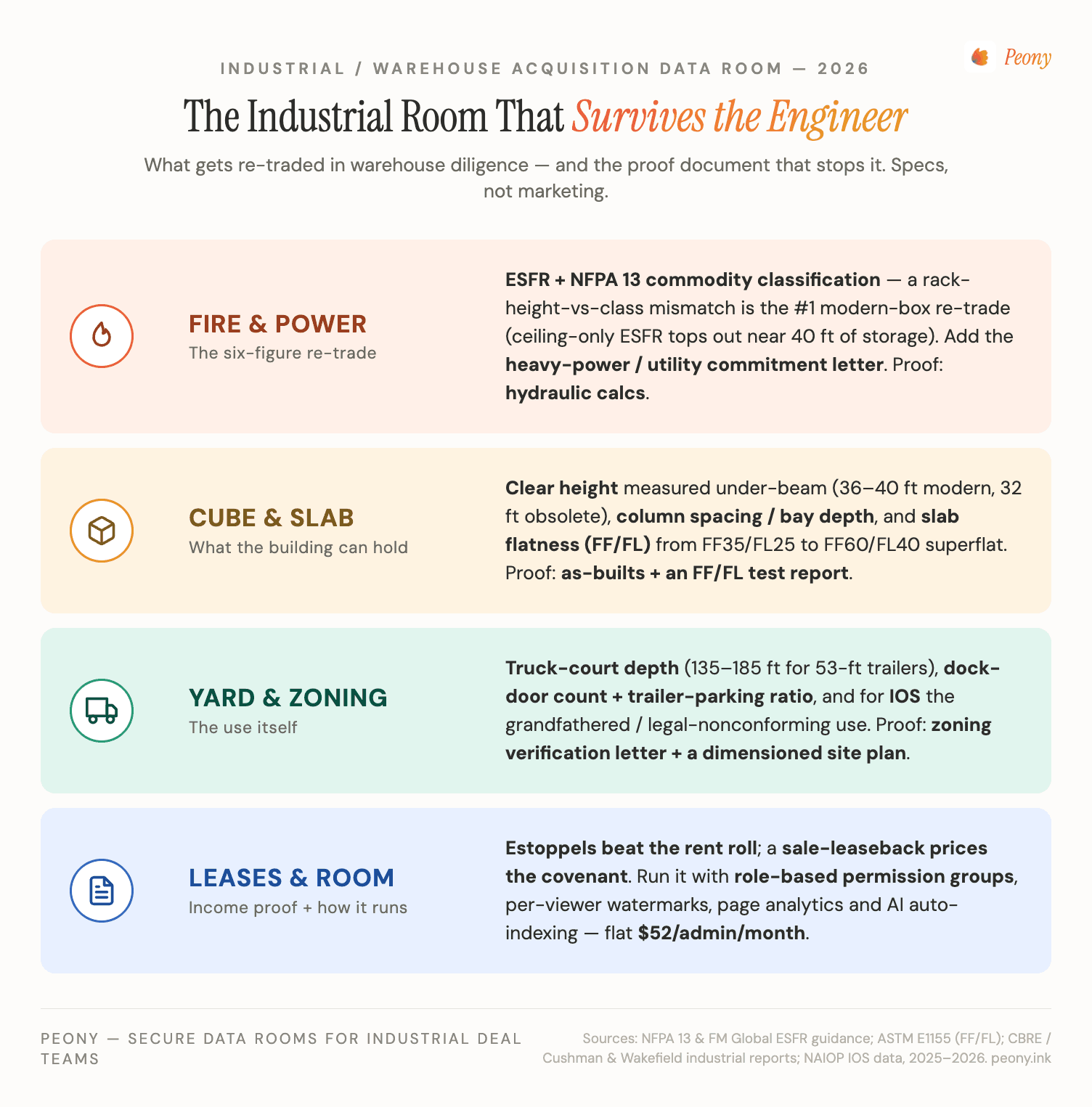

Here is the heart of it. For each industrial workstream, this is the spec the buyer's consultant verifies, the document that proves it, and the #1 thing the engineer re-trades when the proof is missing or the verified number doesn't match the marketed one. Build your room folder-for-folder against this table and you've built the room that survives diligence.

| Workstream | The spec the buyer verifies | The document that proves it | The #1 thing the engineer re-trades |

|---|---|---|---|

| Clearance & cube | Clear height (under-beam, not to deck), column spacing / bay depth, building dimensions | As-built architectural & structural drawings; a measured clear-height certification | The marketed clear height is to the deck, not the under-beam working height — so the usable cube is smaller; or 32' clear is functionally obsolete for big-box |

| Loading & yard | Dock-high door count, drive-in ratio, truck-court depth, trailer-parking ratio, cross-dock vs front-load | Site plan with dimensioned truck court; door schedule; striping/parking plan | The truck court is too shallow for modern 53' trailers to maneuver (135'–185' is the standard band), or the trailer-parking ratio won't serve a real 3PL operation |

| Fire & power | ESFR / in-rack sprinkler design, NFPA 13 commodity classification, electrical service & available power | Fire-protection drawings + hydraulic calcs; the commodity-classification basis; utility letter / panel schedule | The ESFR system or commodity class won't support the rack height and commodity the buyer's tenant intends to store — a six-or-seven-figure retrofit, the classic re-trade |

| Slab & structure | Floor flatness/levelness (FF/FL), slab thickness and capacity (psf), structural load capacity | Slab specification & FF/FL test report; structural drawings; geotechnical report | The slab is FF35/FL25 (fine for random forklift traffic) but the buyer needs FF45/FL35 for wire-guided or air-pallet racking — or the psf won't carry the intended load |

| Zoning & IOS | Permitted use, certificate of occupancy, legal-nonconforming / grandfathered status, parking/coverage | Zoning verification letter; CO; conditional-use permit; site plan; (for IOS) paving/stabilization detail | For IOS especially: the outdoor-storage use is grandfathered and can't be re-established if interrupted — and there's no zoning verification letter to prove it |

| Leases | Estoppel reconciled to rent roll, BTS lease abstract, SNDA, TI obligations, options | Signed estoppel certificates; the lease + abstract; SNDAs | An estoppel surfaces an unrecorded free-rent period, expansion option, early-termination right, or unfunded TI the rent roll never showed |

| Environmental | Phase I (Recognized Environmental Conditions), Phase II if triggered, yard-surface contamination | Phase I ESA to ASTM E1527-21; Phase II sampling report; PCA | A REC surfaces late (former industrial use, floor drains, USTs, or — for IOS — a contaminated yard surface) and triggers a Phase II that wasn't priced into the deal |

A few of these deserve a closer look, because they're where the most money moves.

Fire and power is the modern bulk-box's number-one re-trade. A buyer planning high-piled storage doesn't care that the building "has sprinklers" — it cares that the system is an ESFR (early suppression, fast response) design rated for the commodity classification of what its tenant will store, at the rack height it intends. NFPA 13 ties storage height, commodity class, and sprinkler design together; ESFR ceiling-only systems generally top out around 40 feet of storage with ceilings under about 45 feet, beyond which you're into specialized high-K or in-rack designs. If the marketed "ESFR" turns out to be a lower-class design, or the available electrical service can't power a tenant's automation and racking, the retrofit number is large — and it comes straight off your price. Stage the hydraulic calcs and the commodity-classification basis, not just the line item "ESFR: yes."

The slab is quietly decisive. Modern industrial tenants run forklifts, wire-guided very-narrow-aisle racking, and increasingly automated systems, all of which live or die on the floor. FF/FL numbers (FF = flatness measured at 1-foot intervals, FL = levelness at 10-foot intervals; higher is better) tell the buyer what the floor can do: FF35/FL25 is the common warehouse spec for random forklift traffic, FF45/FL35 is "very flat" for wire-guided or air-pallet work, and FF60/FL40 is super-flat for defined-path automation. A buyer whose tenant needs FF45 and finds an FF35 floor is looking at remediation — or a different tenant. Slab capacity in psf is the other half: it caps the rack load and the equipment. Put the slab spec and the FF/FL test report in the room; don't make the engineer assume.

IOS is all about the entitlement, and it's the flagship niche. Industrial outdoor storage — truck terminals, container yards, trailer parking, equipment laydown — is a different animal because the value isn't in a building; it's in the right to use the land that way. The sector is still roughly half locally and mom-and-pop owned, and a large share of sites are legal-nonconforming or grandfathered uses that municipalities increasingly won't permit by right (truck traffic, lower tax base, community resistance). That makes the zoning verification letter and proof of grandfathered status the single most important document in the room — because a buyer's deepest fear is that the use can't be replicated or won't survive an interruption. (Honest note: IOS keyword volume is genuinely thin, so most providers ignore this asset class — which is exactly why a purpose-built room earns the niche. EIOS — electrified IOS, for EV and refrigerated-trailer power — is the emerging sub-niche to watch.)

How do you build a warehouse acquisition data room? (The checklist, structured)

A warehouse acquisition due diligence checklist is everywhere online, and most of them are flat document dumps that list the rent roll next to the roof warranty as if they carried equal weight. The version that wins organizes the room around the seven workstreams above, so a buyer's analyst, lender, and consultants each walk straight to their lane. Here's the structure I'd stand up:

- 00 — Teaser / process. The OM, the process letter, the NDA. Gated; this is what back-up bidders see before they clear the gate.

- 01 — Clearance & cube. As-built architectural and structural drawings, the clear-height certification (under-beam), column-spacing and bay-depth plan.

- 02 — Loading & yard. Dimensioned site plan, dock-door schedule, drive-in ratio, truck-court depth, trailer-parking count and ratio, cross-dock vs front-load designation.

- 03 — Fire & power. Fire-protection drawings, ESFR/in-rack design and hydraulic calculations, the commodity-classification basis, the utility letter and panel/transformer schedule (available power is a leasing differentiator now).

- 04 — Slab & structure. Slab specification, FF/FL test report, geotechnical report, structural load capacity (psf).

- 05 — Zoning & entitlement. Zoning verification letter, certificate of occupancy, conditional-use permits, parking/coverage compliance, legal-nonconforming documentation (front-and-center for IOS).

- 06 — Leases & income. Rent roll, every lease, lease abstracts, signed estoppels reconciled to the rent roll, SNDAs, BTS abstract, TI and option schedules.

- 07 — Financial. Trailing-12 operating statement, CAM reconciliations, expense recoveries, normalized NOI, tax bills (watch the post-sale reassessment).

- 08 — Environmental & condition. Phase I ESA to ASTM E1527-21, any Phase II, the Property Condition Assessment, roof and major-systems warranties.

- 09 — Title & survey. Title commitment with Schedule B exceptions, ALTA/NSPS survey, easements and access.

The discipline that actually moves the price isn't the folder names — it's staging the package before the buyer's request list lands. Diligence formally starts when the buyer's counsel sends a request list; the losing move is treating that list as a scavenger hunt. The winning move is having all ten folders indexed and waiting on day one, so the buyer finds the proof instead of asking for it. That single habit is the most reliable re-trade preventer there is, because problems surface while you still have leverage and other bidders. For the exhaustive line-by-line inventory inside each folder, layer in our real estate due diligence checklist; for how the costs of all those third-party reports stack up, see the due diligence cost breakdown.

How do you structure an industrial sale-leaseback data room?

For a sale-leaseback — where an owner-operator (a manufacturer, a 3PL, a distributor) sells the building it occupies and signs a long-term lease back — the room inverts. The buyer isn't really buying a building; it's buying your covenant, a bond-like income stream backed by your corporate credit. So the room has to lead with the income and the credit, then support it with the building.

The sale-leaseback stack, in priority order:

- The lease abstract, first. Term, base rent, escalations, renewal options, the NNN structure, and any purchase option or right of first refusal. This is the instrument the buyer cap-rates. Make it the first thing in the room, with the full executed lease right behind it.

- Your credit, second. Audited or reviewed financial statements, the parent guarantee if there is one, and any credit rating. A sale-leaseback prices on the strength of the tenant standing behind the rent — investment-grade credit compresses the cap rate; a thin balance sheet widens it. Buyers and their lenders will underwrite this hard, so a complete, clean credit package is what gets you the price.

- The building, third — but still spec-complete. The same clearance/loading/fire/slab/zoning proof as any industrial room, because if your credit ever falters, the building is the buyer's residual. A buyer paying a tight cap rate on your covenant still wants to know the box is releasable to someone else — so the spec table above still applies.

The classic mistake is treating a sale-leaseback like a vacant-building sale and burying the lease in a generic folder. The income is the deal; structure the room so an acquisitions analyst can underwrite the credit and the residual in a single sitting. A flat-rate data room for real estate maps this single-tenant, credit-led framing directly.

Estoppel vs rent roll: which does an industrial buyer actually trust?

The estoppel, always — and understanding why is the difference between a clean close and a late re-trade. The rent roll is the seller's claim about the income. The estoppel certificate is the tenant's signed confirmation of it: the actual rent, term, security deposit, options, and — the part that bites — whether the landlord currently owes the tenant anything or is in default. The rent roll is marketing; the estoppel is evidence.

On industrial deals the gap between the two is a common re-trade because the income is concentrated. A single-tenant or build-to-suit asset's entire value rides on one lease, so one surprise in the estoppel moves the price by a lot:

- an unrecorded free-rent period the rent roll didn't reflect,

- an expansion or contraction option that changes the building's future,

- an early-termination or co-tenancy right that shortens the effective term,

- an unfunded tenant-improvement obligation the seller still owes,

- a rent that's actually in dispute or being abated.

The SNDA (subordination, non-disturbance, attornment) is the estoppel's companion: it governs what happens to the lease if the lender forecloses, and lenders will want it from major tenants. For a developer selling a build-to-suit, the lease abstract and the estoppel together are the asset — the building was designed for that tenant, so the durability of that lease is what a buyer is really pricing.

The discipline: collect estoppels from major tenants before your contingency deadline, reconcile every line against the rent roll inside the room, and surface any delta yourself. The buyer's counsel will find it regardless — finding it first is how you stay in control of the number.

How does the data room actually run an industrial acquisition?

This is the workstream the spec sheets skip: the diligence has to be executed across the seller, the buyer, a lender or debt fund, and a stack of third-party consultants — and on a real industrial deal that means moving 150-plus documents (drawings, surveys, reports, lease files) under access control against a contingency clock. The data room is where that happens. I run Peony, so treat this section as informed but interested — and I'll tell you plainly where you don't need any of it.

Five things separate a deal that closes cleanly from one that re-trades:

1. AI auto-indexing makes the spec-organized room survivable on a clock. Industrial diligence is document-heavy and the files arrive as a mess — a dump of drawings, PDFs, reports, and lease scans. AI auto-indexing sorts a bulk upload into the standard folder tree in minutes instead of the days it takes to hand-file. That matters most for the 1031 buyer racing a 45-day identification clock, where a week lost to filing is a week off a non-extendable deadline.

2. Role-based permission groups model the whole bidder hierarchy in one room. A portfolio process has parties who must not see the same things — the lead bidder gets the full set, back-ups get a teaser tier, the lender is scoped to financial/title/environmental/appraisal but not the equity returns, and each consultant sees only its lane. Programmatic permission groups do this in a single room instead of the cloned-folder sprawl that fragments your audit trail, with an NDA gate sitting in front of the room before anyone sees a document.

3. Page-level analytics tell you what the buyer is actually worried about. When you can see that a serious bidder spent forty minutes in the fire-and-power folder but never opened the leases, that's intelligence: push the commodity-classification basis and clear the objection before it becomes a re-trade. Page-level analytics turn the room from a passive file dump into a read on who's real and which spec they're circling — who viewed what and for how long, not keystroke surveillance.

4. Watermarks and redaction keep the confidential stuff traceable. Rent rolls carry tenant PII; offering memoranda get forwarded; a leaked tenant rate can blow up a relationship. Dynamic per-viewer watermarks stamp every page with the viewer's identity, and redaction blacks out tenant names or lease rates for parties who shouldn't see them yet — a back-up bidder, a consultant who only needs the building specs. On an industrial portfolio where competing 3PLs may be bidding, traceability changes behavior.

5. One flat price, regardless of how thorough you are. Peony is a flat $52/admin/month — no per-page, no per-GB metering. That's the right model precisely because industrial diligence is document-heavy: a usage-priced room punishes you for uploading every drawing and report, which is exactly what you should be doing. We serve 5,900+ customers, and our data room for real estate guide maps the setup across CRE single-asset, portfolio, REIT, distressed, and development archetypes.

Where you don't need any of this: a small, all-cash, single-tenant warehouse with one buyer and one attorney can absolutely run on a few emailed PDFs — no NDA to enforce, no competing bidders, no lender, no problem. And at the other end, a $1B-plus logistics portfolio or an institutional take-private defaults to Datasite or Intralinks, whose buyers' counsel often mandates them; that's their lane and they're excellent at it. The industrial-data-room sweet spot is everything in between: a last-mile infill box, a sale-leaseback, an IOS site, a regional warehouse portfolio — a deal with a lender, multiple bidders, real spec documents, and a clock.

How do you handle an industrial portfolio sale or a logistics JV?

A portfolio sale or a logistics JV scales every problem above, and adds two of its own: comparability and party complexity. A buyer underwriting twelve warehouses across five markets needs to compare them on the same axes — so the room should carry a portfolio-level spec roll-up (a single matrix of clear height, ESFR class, slab, truck court, and zoning status across every asset) sitting above the asset-by-asset folders. Make the buyer's analyst able to sort the portfolio by spec, and you've made the whole package legible.

On party complexity, a JV or a marketed portfolio process can have a lead bidder, several back-ups, a lender or a syndicate, a JV partner doing its own diligence, and a dozen consultants — all needing different, often overlapping, slices. This is precisely where flat "admin/viewer" file-sharing collapses and where role-based permission groups, per-viewer watermarks, and an audit trail earn their place. For the distressed end of the spectrum — a lender-driven sale, a receivership, a note sale on an over-levered logistics asset — the access-control and chain-of-custody requirements get even sharper; our data room for distressed asset sale guide covers that workflow.

One honest scoping note: at true institutional portfolio scale ($1B+), this is again Datasite/Intralinks territory by procurement default. The mid-market portfolio — a regional operator selling eight to fifteen boxes, or a developer recapitalizing a logistics JV — is where a flat-rate, spec-organized room is the structural fit.

How does an industrial data room compare to a data center or cell-tower room?

They're cousins — all three are "specialized real estate where the physical infrastructure is the asset" — but the spec that re-trades is completely different in each, which is the whole reason asset-class-specific rooms exist.

| Asset class | What the buyer's engineer re-trades on | The room leads with |

|---|---|---|

| Industrial / warehouse | Clear height, ESFR/commodity class, slab FF/FL & capacity, truck court, power, IOS zoning grandfathering | As-built specs + the lease/estoppel |

| Data center | Power (MW & utility commitment), cooling, PUE, redundancy (N+1/2N), connectivity, the power-purchase and interconnect agreements | The power capacity and the utility/interconnect contract |

| Cell tower | Ground-lease term, the master lease agreement (MLA), structural loading capacity, tenant/co-location revenue, zoning | The ground lease and the tower's structural capacity |

The mistake is using one template for all three. A data center deal is won on the power and cooling stack — the data room leads with the megawatt capacity and the interconnect agreement, and our data center data room guide goes deep on PUE, redundancy, and the utility commitment. A cell-tower deal is won on the ground lease and structural loading — the room leads with the lease term and the master lease agreement, covered in our cell tower data room guide. An industrial deal is won on the box and the covenant. Same principle — organize the room around the spec the engineer re-trades — three completely different spec sheets.

The bottom line: which industrial data room setup fits your deal?

The thesis holds across every variant: build the room around the specs the buyer's engineer will re-trade, and surface the gaps before the buyer opens them. A gap the seller surfaces is a footnote; a gap the buyer discovers is a price cut. Here's the segmented recommendation:

- Single last-mile or infill warehouse, one buyer, all cash, no NDA: you may not need a formal room at all — emailed PDFs can carry it. The moment a second bidder, a lender, or an NDA-gated rent roll appears, move to a room.

- Owner-operator doing a sale-leaseback: lead the room with the lease abstract and your corporate credit, back it with spec-complete building proof. The income is the asset. A flat-rate room is the structural fit.

- Developer selling a build-to-suit or spec building: the lease abstract and estoppel are the deal; the as-built drawings are the proof the building will perform. Stage both before the request list lands.

- IOS / truck terminal / trailer yard: the zoning verification letter and grandfathered-use proof are the single most important documents — put them front and center. This is the niche most providers ignore, which is why a purpose-built room wins it.

- Mid-market warehouse or logistics portfolio with a lender and multiple bidders: role-based permission groups, per-viewer watermarks, page-level analytics, and a portfolio spec roll-up — a flat $52/admin/month room organized around the seven-workstream tree.

- $1B-plus institutional logistics portfolio or take-private: Datasite or Intralinks remain the procurement default, and often the buyer's counsel mandates them. No shame in it — that's their lane.

For everything from a $3M infill box to a mid-market portfolio, a flat-rate, spec-organized commercial real estate data room is the fit — and across our 5,900+ customers, the pattern is consistent: the deals that close cleanly are the ones where the proof was waiting in the right folder before anyone asked for it. If you're still choosing a provider, our top 10 virtual data room providers comparison and virtual data room cost guide lay out the options and the pricing models side by side.

Sources

- CBRE — U.S. Real Estate Market Outlook 2026: Industrial and Q1 2026 U.S. Industrial & Logistics Figures (last-mile ≈20%+ of leasing; big-box dynamics; flight to quality)

- Cushman & Wakefield — big-box (>500,000 SF) leasing reportedly +32% year over year (via Supply Chain 24/7 / Commercial Property Executive)

- Hines — reported projection of ~35% increase in U.S. warehouse demand over five years (reshoring)

- Brookfield Asset Management / Peakstone Realty Trust — SEC Form 8-K and press coverage (CoStar, Bisnow, The Real Deal) on the ~$1.2B all-cash IOS-heavy acquisition, completed May 2026

- Fident Capital; Urban Land (ULI); Northmarq; CBRE — industrial outdoor storage institutionalization, fragmented ownership, and zoning/grandfathering

- NFPA 13 (Standard for the Installation of Sprinkler Systems) — ESFR and commodity-classification framework; QRFS, TERPconsulting, Risk Logic (ESFR storage-height limits)

- IFTI, Archtoolbox, Concrete Network, Wright Construction — floor flatness/levelness (FF/FL) classifications for warehouse slabs

- ASTM E1527-21 (Phase I ESA) and ASTM E2018 (Property Condition Assessment) standards

Disclosure: I co-founded Peony, a flat-rate virtual data room. I've written this to be genuinely useful whether or not you ever use our product — the spec-retrade framework applies to any industrial deal in any data room. Specific market figures, deals, and standards are sourced above and accurate to the best of my knowledge as of July 2026; verify any number that's load-bearing for your transaction, because a wrong specific is worse than a general truth. This is not legal, tax, environmental-engineering, or investment advice — engage qualified professionals for your deal.

You might also like

Jul 1, 2026

Cell Tower Data Room: How a Tower Portfolio Sale Closes (2026)

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Jul 1, 2026

Senior Housing Data Room: You're Buying an Operation, Not an Address (2026)