Note Sale Data Room: Proving the Chain of Title Before the Bid Date (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Note Sale Data Room: Proving the Chain of Title Before the Bid Date (2026)

Last updated: July 2026

Quick answer: A note sale data room is a deal room for selling, buying, or financing a loan secured by commercial real estate — and the thing that makes it different from any other CRE room is that it is organized around enforceability and transferability of the loan, not square feet. Because in a note sale you're buying the debt, not the dirt, the document set leads with the collateral file — the original note, the allonge and endorsement chain, the recorded mortgage/deed of trust, the assignment chain, the title policy, UCC filings, and the guaranty — and the loan tape reconciled to those documents, because that is what proves the buyer can actually collect and, if it comes to it, foreclose. The market backdrop in 2026 is a wall of maturing CRE debt (the MBA counts roughly $875B due in 2026 and $652B in 2027, out of about $5.0T outstanding) and elevated distress (Trepp's overall CMBS delinquency rate sat near 7.35% in June 2026, with office around 11.57%), so banks and servicers are selling paper rather than working it out — and the buyer's whole job is to prove the chain of title before the bid date. When that trade involves multiple bidders under NDA, a collateral file per asset, and confidential borrower financials, the room that runs it is usually a commercial real estate data room — not email.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't buy distressed notes for a living — but I've watched a lot of CRE deals move through data rooms, and note sales do not behave like property sales. In a property deal, the room is organized around the building: leases, survey, environmental, condition. In a note sale, the building is downstream of a more basic question — do you actually own an enforceable, transferable loan, and can you prove it? The value and the risk live in the collateral file and the loan tape, not in the square footage. Reorganize the room around the paper and the trade reads correctly. Leave it organized like a property sale and you bury the one file the buyer's counsel actually came for.

That is the thesis of this post: in a note sale you're buying the debt, not the dirt — so the room has to prove the chain of title to the note before the bid date. A clean collateral file with an unbroken endorsement and assignment chain is worth more, and closes faster, than a note on a beautiful building whose chain of title has a break in it. The asset here is enforceability; the property is only the backstop.

Here's the carve-out, because Peony has a family of CRE guides and this one owns a specific lane. If you want the generic CRE property process and clock — caveat emptor, the contingency period, re-trades — read commercial property due diligence; that post is about buying the property, this one is about buying the paper. If you want the line-item property document inventory, that's the real estate due diligence checklist — a note buyer uses it only to value the collateral backstop, not to trade the loan. If you want provider and archetype selection for real estate broadly, that's data room for real estate. And if you're raising a fund to buy this paper rather than trading a single loan, see real estate fund data room. None of those cover the debt axis — the collateral file, the loan tape, the chain of title — which is the entire subject of this guide.

Why does a note sale data room prove the loan instead of the building?

Because you are buying the debt, and everything about that trade's value and risk flows from whether the loan is enforceable and transferable. When a lender sells a note, it is not conveying the real estate — it is transferring the right to be repaid and, if the borrower defaults, the right to foreclose on the collateral. That right lives in a stack of paper: the note, the endorsements, the recorded assignments, the mortgage, the title policy. If that stack is clean, the buyer owns something enforceable. If there is a break in it, the buyer may own a lawsuit.

The market in 2026 is why this is a live question at scale. A wall of CRE debt is maturing into a higher-rate world: the Mortgage Bankers Association counts roughly $957B of commercial and multifamily mortgages that matured in 2025, about $875B scheduled for 2026 — around 17% of the $5.0T outstanding — and another $652B in 2027. Loans written at 3-4% cannot always refinance at today's rates, and when the math doesn't work, the loan either goes non-performing or the bank sells it at a discount. Distress is showing up in the data: Trepp's overall CMBS delinquency rate was near 7.35% in June 2026, with office around 11.57% (down from a record ~12.34% in January 2026). Banks are under reserve pressure — the FDIC's Q4 2025 profile put industry reserve coverage near 171% and community banks nearer 154% — which pushes more of them to sell paper rather than work it out. The result is that non-performing note supply is the highest it's been in roughly a decade, and disciplined buyers are acquiring quality paper at real discounts to unpaid principal balance (deal-specific — commonly cited in a wide 20-60% off UPB range for commercial paper, never a promised price).

When paper trades that actively, the diligence question is no longer "is the building sound?" It is "can I enforce and transfer this loan, and is the chain of title clean?" So the room's job is not to prove the property. It is to prove the paper — the collateral file, the loan tape, and an unbroken chain of title, before the bid date. That is the spine the index has to be built on.

What goes in a note sale data room?

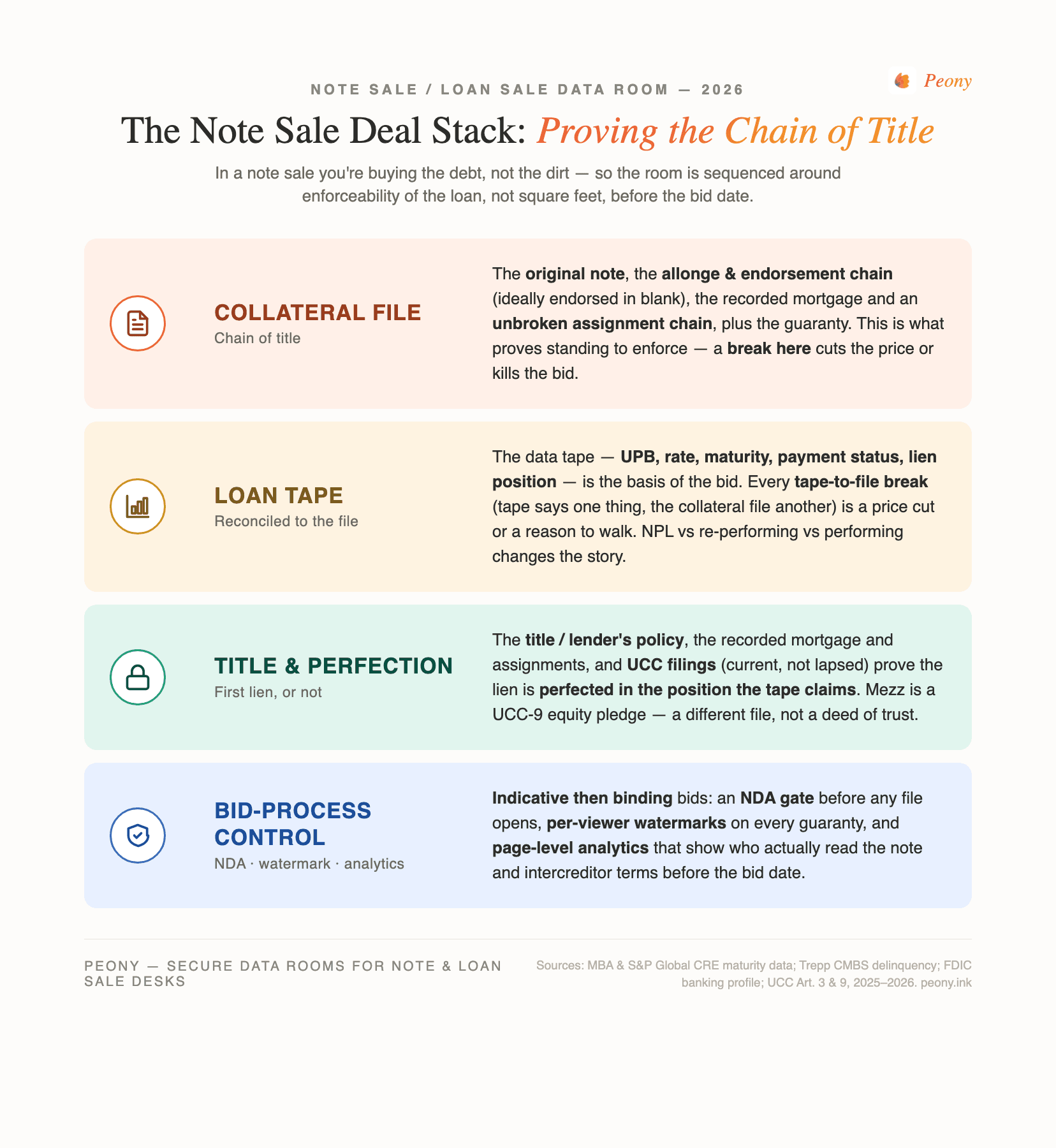

The workstreams of a debt trade, sequenced so the collateral file leads and graded by the one thing that goes wrong in each. The generic CRE room puts property reports first; the note-sale room puts the loan first, because enforceability is the gating risk a buyer's counsel is actually underwriting. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Collateral file / chain of title | Original note; allonge + endorsement chain (ideally endorsed in blank); recorded mortgage/deed of trust; unbroken assignment chain; guaranty | A break in the chain — a missing assignment, an endorsement that doesn't run to the seller, or a lost original with no proper affidavit — surfaces after the bid |

| Loan tape accuracy | UPB, rate, origination/maturity dates, payment status, escrow, lien position — each field reconciled to the underlying documents | Tape-to-file breaks: the tape says one thing (UPB, maturity, lien position) and the collateral file or servicing history says another |

| Title & lien perfection | Title/lender's policy, endorsements, recording of the mortgage and every assignment, UCC financing statements (and continuations) for personal-property or mezzanine collateral | The lien isn't perfected or the recording/UCC lapsed — the buyer thinks it's buying a first lien and it's junior or unperfected |

| Borrower & guaranty | Borrower entity docs and financials; the guaranty (recourse vs non-recourse, carve-outs); default and demand correspondence | The guaranty is unsigned, expired, or a "bad-boy" carve-out only — treated as full recourse when it isn't |

| Servicing & payment history | Payment/transaction history, escrow analysis, modification and forbearance documents, servicing notes, the servicing-transfer file | Payment history doesn't reconcile to the tape; a modification isn't documented; servicing transfer (RESPA notices) is botched |

| Property / collateral value | Appraisal or broker price opinion (BPO), rent roll and leases, environmental where relevant — as the backstop to the debt, not the asset being sold | Underwriting the property like a purchase instead of a recovery — over-relying on a stale appraisal for the foreclosure/liquidation value |

| Intercreditor / mezz | Intercreditor or co-lender agreement, A/B note terms, mezzanine pledge and UCC filings, participation agreement — control, cure, standstill, and waterfall | The seniority/control terms aren't legible; the buyer learns after bidding that another lender controls the workout or holds cure/buy-out rights |

A few of these deserve their own paragraph because the enforceability, and the liability, live there.

The collateral file is the workstream with the least flexibility. You can update an appraisal in weeks; you cannot retroactively create a recorded assignment that was never made. Standing to foreclose depends on the buyer holding the note with a complete endorsement chain (an endorsement in blank makes the note bearer paper) and an unbroken chain of recorded assignments of the mortgage. So the room must make the chain of title traceable at a glance: the original note on top, the allonges and endorsements with it, then every assignment in order, then the recorded mortgage and the title policy. Buyer's counsel reads these in sequence, and if the sequence is scrambled or a link is missing, the price moves or the deal stalls.

The loan tape is where value and reality can quietly diverge. The tape is the seller's summary; the collateral file and servicing history are the ground truth. Every line where they disagree — a UPB that doesn't tie, a maturity that predates a modification, a "first lien" that the title policy shows as second — is either a price adjustment or a reason to walk. Put the tape and the documents that support each field in the same room so the reconciliation can actually happen before the bid.

MERS and the assignment chain have a specific trap. Where a loan was tracked in MERS, transfers may not have been recorded in the county land records, so the chain a buyer needs to see is partly in MERS and partly in the recorder's office. Reconcile them, and where a recorded assignment is missing, get a corrective or confirmatory assignment into the room before closing — not after.

What is a collateral file, and how do you review the chain of title?

The collateral file is the set of documents that proves who owns the loan and that it can be enforced, and the chain-of-title review is the work of tracing that ownership from origination to the seller — and then to the buyer — without a gap. Get this right and the rest of the trade is ordinary; get it wrong and nothing else matters, because a note you cannot enforce is worth its liquidation value at best.

Run the review in this order, top of the collateral folder downward:

- Original promissory note. The threshold document. Confirm it is the original (wet-ink where required), read the terms against the loan tape, and check the endorsements. Possession of the original note with a proper endorsement is what establishes the right to enforce.

- Allonge and endorsement chain. An allonge is a paper firmly affixed to the note that carries an endorsement when there's no room left on the note itself; endorsements are not recorded in public records, so they only exist in the file. Trace the endorsements from the original lender to the seller — ideally ending in an endorsement in blank, which makes the note bearer paper and simplifies transfer. A chain that stops short of the seller is a break.

- Recorded mortgage / deed of trust and the assignment chain. Unlike endorsements, assignments of the mortgage are recorded. Confirm the mortgage was recorded and that there is an unbroken chain of recorded assignments to the seller. Where MERS was the nominee, reconcile the MERS transfers against the recorded chain.

- Title / lender's policy and lien position. Read the policy and the current title to confirm the mortgage is a perfected lien in the position the tape claims (first, second) and that no intervening liens or releases undercut it.

- UCC filings and guaranty. For any personal-property or equity collateral (especially a mezzanine loan), confirm the UCC financing statements are filed and current (continuations not lapsed). Read the guaranty for recourse scope and carve-outs.

The non-negotiable rule: every enforcement assumption in the bid has to be traceable to a document in the room. If the buyer is pricing a clean first lien with full recourse, the room has to contain the endorsed note, the unbroken assignment chain, the first-lien title policy, and the signed guaranty to back it. Where a link is missing, the honest move is to surface it early — cure it with a corrective assignment or a lost-note affidavit, or price it — not to let it emerge during binding diligence. Peony holds, permissions, watermarks, and logs that collateral file; it does not perform the collateral-file review or opine on perfection or enforceability — that is the buyer's counsel's job, and this post is not legal advice.

What is the difference between an NPL, a re-performing, and a performing note sale?

They are three different risk stories, and the room has to tell each one differently. Conflating them is a classic error: a buyer who underwrites a performing note like a distressed one overpays for diligence, and a seller who markets an NPL like clean paper loses credibility the moment the file is opened.

| Sale type | What the buyer is underwriting | What the room must lead with |

|---|---|---|

| Non-performing (NPL) | The collateral, the enforceability of the note, and a workout/foreclosure path | Collateral file + chain of title + current property value (BPO/appraisal) + demand file |

| Re-/sub-performing (RPL/SPL) | The durability of resumed or modified payments | Modification documents + a clean, reconciled payment history + collateral file |

| Performing whole loan | Yield, borrower credit, and clean transferability | Loan tape + borrower financials + collateral file (transfer-ready, endorsed) |

For an NPL, the property value is the recovery backstop, so the appraisal or BPO and the foreclosure timeline (judicial vs non-judicial state) carry real weight — but the enforceability of the note still comes first, because a buyer that can't foreclose can't reach the collateral. For an RPL/SPL, the whole thesis is that the payments will stick, so the modification agreement and an unbroken, reconciled payment history are the star exhibits. For a performing whole-loan sale, the trade is closest to a bond: clean paper, good credit, a transfer-ready collateral file.

One market reality binds all three: most CRE note sales are "as-is, where-is" with limited reps and warranties. The seller is not standing behind the loan the way a borrower stands behind a representation in an M&A deal — the buyer takes what the file shows. That pushes even more weight onto what the room can prove, which is exactly why the collateral file and the reconciled loan tape sit at the top of the index. Label which of the three you are selling in the first folder, so no bidder underwrites the wrong story.

What is a loan tape, and how do you reconcile it to the collateral file?

A loan tape (or data tape) is the spreadsheet that summarizes the loan or the pool — and reconciling it means proving, line by line, that what the tape asserts is what the documents show. The tape is the buyer's first read and the basis of the indicative bid; the collateral file and servicing history are the ground truth that the binding bid depends on. The gap between them is the deal.

A CRE loan tape typically carries, per asset:

- Balances and terms — UPB, note rate, origination and maturity dates, amortization, any modification.

- Status — current/delinquent, days past due, default status, bankruptcy or foreclosure flags.

- Collateral — property type, location, appraised or BPO value, and loan-to-value.

- Lien and structure — lien position, whether it's a whole loan, an A/B piece, or a participation, and any escrow or reserves.

Reconciling it is the discipline that separates a real diligence room from a data dump:

- Does the UPB on the tape tie to the note and to the servicing/payment history?

- Does the maturity date match the note and any modification agreement?

- Does the stated lien position match the title policy and the recorded assignment chain?

- Does the payment status match the transaction history and the demand/default correspondence?

Every unreconciled line is either a price adjustment or a reason to walk — so the room should place the tape and the documents that support each field within reach of each other, ideally with the collateral file and servicing history indexed to match the tape's asset IDs. Our real estate due diligence checklist covers the property-side documents a buyer uses to sanity-check the collateral value; here, the point is that the tape has to survive contact with the file.

How does an intercreditor, A/B note, or mezzanine sale change the room?

It adds a seniority and control layer that often matters more to value than the property does — so the room has to make that layer as legible as the note itself. When you buy a piece of a structured loan, you are buying a position in a capital stack governed by an agreement between the lenders, and the terms of that agreement decide what your position is actually worth in a workout.

- A/B note and senior/junior structures. The loan is split into a senior A-piece and a subordinate B-piece, governed by a co-lender or intercreditor agreement. Read who controls the workout, who has the right to cure, buy-out and purchase options, standstill provisions, and the payment waterfall. A B-note with no control rights in a distressed deal is a very different asset from one with a buy-out right.

- Mezzanine loans. A mezz loan is typically not secured by a mortgage on the real estate — it is secured by a pledge of the equity interests in the property-owning entity, enforced under UCC Article 9 (a UCC foreclosure/sale, not a real-estate foreclosure). So the collateral file looks different: the pledge agreement, the UCC financing statements and their continuations, and the intercreditor agreement with the senior mortgage lender — not a recorded deed of trust. Confirm the UCC filings are perfected and current, because a lapsed continuation can quietly subordinate the position.

- Participations. A participation sale transfers an economic interest in a loan without transferring the note itself; the lead lender keeps the note and the relationship. The governing document is the participation agreement — read voting rights, the lead's servicing obligations, and what happens on default.

Because these control terms are commercially sensitive and drive price, they belong behind an NDA gate with per-viewer watermarks, and — since a bidder who misreads the intercreditor agreement will misprice the bid — page-level analytics that show whether the bidder actually opened it are genuinely useful.

How does the data room actually run a note sale?

It runs it as a permissioned, evidence-first bid process where the collateral file is legible, the confidential borrower and guaranty documents are gated and watermarked, and you can see which bidders actually read the note before they bid. A note sale — even a small-pool one — moves the loan tape, a collateral file per asset, borrower financials, guaranties, servicing histories, and intercreditor documents among a seller, multiple competing bidders, buyer's counsel, and sometimes a note-on-note lender. Email and consumer file-sharing cannot gate, watermark, or track that. Here's how a room like Peony maps to the specific risks of a debt trade, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when you're onboarding a dozen competing bidders and each one adds analysts and counsel.

- NDA gate. A note sale opens with an NDA — borrower financials, guaranties, and workout correspondence are confidential, and often the borrower doesn't know the loan is being sold. A click-through NDA in front of the room means a bidder agrees before they see a single document, and you have the record that they did.

- Dynamic per-viewer watermarks. The same guaranty or borrower financial opens for two competing bidders with each viewer's identity burned into the page. If a confidential borrower document leaks, the watermark says whose copy it was — a real deterrent when you're circulating a named borrower's financials to a competitive field.

- Page-level analytics. You see who viewed what and for how long — did the serious bidder actually open the intercreditor agreement, the endorsement chain, and the guaranty, or just the tape? That tells you where the real bids are coming from before the bid date. (This is view-and-dwell analytics, not keystroke capture.)

- Redaction. Borrower personal data, account numbers in a payment history, or pricing in a participation agreement can be redacted at the document level so a bidder sees the structure without the confidential specifics — useful at the indicative stage before a shortlist is set.

- AI auto-indexing. Drop a disorganized servicing export — hundreds of files from the seller's servicer and counsel — and the room indexes it so the collateral file, the tape support, and the servicing history land in a navigable structure instead of a flat dump. In a note sale, where the index is the argument ("the chain of title is clean, here it is in order"), that's not cosmetic.

- Role-based permission groups. Indicative-stage bidders see the tape and a summary file; shortlisted bidders see the full collateral file and borrower financials; buyer's counsel lives in the chain-of-title folder; the note-on-note lender sees the collateral file and the loan sale agreement; losing bidders are cut off when the shortlist is set. One room, many sightlines, one bid date.

For a 5,900+-customer flat-rate room, the structural fit is the bilateral note sale, the small pool, and the buyer's own diligence room — where the document set is confidential and per-asset but the trade doesn't warrant a percent-of-proceeds platform.

Do you even need a VDR — and where do RCM, DebtX, Mission Capital, and Newmark win?

Be honest about both ends of the range, because a note sale data room is the right tool for the middle, not for everything.

At the very small end, a data room can be overkill. A single note sold to one known buyer with one attorney — where the collateral file is a dozen PDFs and there's no competitive process — can run on a secure email thread or a shared folder. Don't over-tool a one-note, one-buyer trade.

At the advised, bulk-or-pooled end, the loan-sale platforms win — and I won't pretend otherwise. When a bank or servicer is disposing of a large pool and wants maximum price through maximum exposure, the value is the buyer network and the valuation, and the room comes bundled with it:

- RCM (Real Capital Markets) — the CRE marketplace, with roughly $2.4T of lifetime transactions across 72,000+ assignments; over half of US commercial assets sold above $10M are brought to market on it. The marketplace is the product.

- DebtX — a full-service loan-sale advisor for secondary-market whole loans (CRE, C&I, SFR, consumer), running valuation and the sale process end to end.

- Mission Capital (a Marcus & Millichap company) — loan-sale advisory across CRE, residential, and specialty debt, with the M&M distribution behind it.

- Newmark Loan Sale Advisory — performing and non-performing note sales run by real-estate finance professionals inside a full-service capital-markets shop.

These advisors typically work on a success fee in the low single-digit percent of proceeds (often around 1-3%) — which is money well spent when you're marketing a pool to hundreds of buyers and need their network and valuation.

Peony's honest lane is the middle: the bilateral or small-pool note sale, and the buyer's own diligence room. If you already know your buyers, or you're a fund building the room to run your own collateral review, you don't need a marketplace — you need a secure, permissioned, watermarked room that runs the bid process. There, a flat $52/admin/month undercuts a percent-of-proceeds platform by a wide margin, and you keep the buyer relationship. Peony is not a loan-sale advisor or a marketplace, and it does not opine on enforceability — it holds, permissions, watermarks, and logs the file and runs the room. Credit the platforms where they win; use the flat-rate room where it fits.

How do you organize the index, and who gets access at what level?

Organize the index so the collateral file is folder one and grant access by role and bid stage, not by a single shared link — because the fastest way to signal "this paper is clean" is to make the chain of title the first thing every bidder's counsel sees, and the fastest way to lose control of a borrower's financials is to hand every bidder the same link.

A working top-level index for a note sale:

- Collateral file / chain of title — original note, allonges and endorsements, recorded mortgage/deed of trust, the full assignment chain, guaranty, and (if applicable) the lost-note affidavit and corrective assignments.

- Loan tape & summary — the data tape, a sale-type label (NPL / RPL / performing), and a bid-process letter with the bid date.

- Title & lien — title/lender's policy, updated title or O&E search, UCC financing statements and continuations.

- Borrower & guaranty — borrower entity docs, financials, rent roll (where held), guaranty, and default/demand correspondence.

- Servicing & payment history — transaction/payment history, escrow analysis, modification/forbearance documents, servicing notes, the servicing-transfer file.

- Property / collateral value — appraisal or BPO, leases, environmental where relevant — as the recovery backstop.

- Structure — intercreditor/co-lender agreement, A/B note terms, mezzanine pledge and UCC, participation agreement.

- Transaction — loan sale agreement, assignment and endorsement forms, closing checklist.

Access then maps to who needs which folders, and at which stage:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Seller / loan-sale advisor | All | Full access |

| Indicative-stage bidder | Loan tape + summary collateral file | NDA gate; watermark; no borrower PII yet |

| Shortlisted (binding) bidder | Full collateral file, borrower financials, servicing, structure | NDA; per-viewer watermark; analytics on note |

| Buyer's counsel | Collateral file / chain of title, title, structure | Role-based; tracing the chain |

| Note-on-note lender | Collateral file, loan sale agreement, tape | Restricted permission group |

This is exactly the segmentation that permission groups plus per-viewer watermarks make routine, and it's where a flat-rate model helps: when a competitive field grows from three bidders to ten and each adds counsel and analysts, you're not paying per seat to keep the room honest — and you can cut losing bidders off the instant the shortlist is set.

The bottom line: which note sale data room do you actually need?

You're buying the debt, not the dirt — so the right answer depends on whether you're running a competitive process, how many bidders and how much confidential paper are involved, and whether you need a marketplace. Here's the segmented recommendation from someone who watches these rooms run.

- Single note, one known buyer, one attorney (no competitive process): You may not need a data room at all. A clean, well-named collateral file — endorsed note, assignments, mortgage, title policy, guaranty — sent over a secure channel to one counterparty can be enough. Don't over-tool a one-note trade.

- Bilateral or small-pool note sale, or a buyer's own diligence room: This is the sweet spot for a flat-rate room. You have a competitive bid or a small pool, a collateral file per asset, confidential borrower financials, and 100-plus documents that email can't gate, watermark, or track. A room like Peony — NDA gate, per-viewer watermarks, page-level analytics, redaction, AI auto-indexing, role-based groups, flat $52/admin/month — fits the document volume and the confidentiality without a per-page, per-user, or percent-of-proceeds meter. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane it's built for.

- Advised bulk or pooled disposition marketed to hundreds of buyers: Default to a loan-sale platform — RCM, DebtX, Mission Capital (Marcus & Millichap), or Newmark. The buyer network and the valuation are the product, the room comes bundled, and the ~1-3% success fee is worth it at that scale. That's the honest recommendation for a large pool.

Whichever tier you're in, the discipline is the same: prove the collateral file, reconcile the loan tape to the documents, trace the chain of title before the bid date, and gate the confidential borrower and structure data. Build the room around the paper — not the property — and the trade reads correctly to everyone who has to underwrite it.

If you're staging a sell-side or financing room and want the broader provider landscape and cost benchmarks first, see our top 10 virtual data room providers comparison and the virtual data room cost guide before you commit.

Sources

- Mortgage Bankers Association (MBA) — commercial/multifamily mortgage maturities: ~$957B matured in 2025, ~$875B scheduled for 2026 (~17% of the ~$5.0T outstanding), ~$652B in 2027.

- S&P Global Market Intelligence — CRE mortgage maturity estimates ($998B in 2025, ~$1.148T in 2026, ~$1.257T in 2027) as a higher-end methodology alternative to the MBA survey figures.

- Trepp — CMBS delinquency data, June 2026: overall rate ~7.35% (down 20 bps on a lodging cure); office ~11.57% (off a record ~12.34% in January 2026); retail ~6.91%; multifamily ~7.23%; lodging ~5.22%; industrial ~1.20%.

- FDIC — Q4 2025 Quarterly Banking Profile / Risk Review: industry reserve-coverage ratio ~171%, community banks ~154% at year-end 2025 — reserve pressure driving loan-sale supply.

- Uniform Commercial Code (UCC) Articles 3 & 9; MERS — negotiable-instrument enforcement (endorsement, holder status, endorsement in blank), security-interest perfection and UCC-9 mezzanine foreclosure, and MERS-vs-recorded assignment reconciliation. (General legal framework — not legal advice.)

- RCM (Real Capital Markets / LightBox), DebtX, Mission Capital (Marcus & Millichap), Newmark Loan Sale Advisory — advised bulk/pooled loan-sale marketplaces and advisory: RCM ~$2.4T lifetime volume across 72,000+ assignments, >50% of US commercial assets sold above $10M; DebtX full-service whole-loan advisory; Newmark performing and non-performing note sales.

- Market context (2026): non-performing note supply reported at roughly a decade high, with commercial paper trading at deal-specific discounts to UPB (commonly cited in a ~20-60%-off range — never a promised price).

This article is general information for deal teams, not legal, tax, or investment advice. Enforceability of a note, standing to foreclose, lien perfection, UCC rules, state foreclosure procedure, market maturity and delinquency figures, and the specific platforms referenced all change over time and vary by jurisdiction — verify current figures and confirm chain of title, perfection, and enforceability with qualified counsel before relying on them. Peony is a data room provider, not a broker, loan-sale advisor, servicer, or law firm; it holds, permissions, watermarks, and logs the file but does not perform the collateral-file review or opine on enforceability.

You might also like

Jul 3, 2026

Multifamily Acquisition Data Room: The Rent Roll Is the Asset (2026)

Jul 1, 2026

Cell Tower Data Room: How a Tower Portfolio Sale Closes (2026)

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)