Real Estate Fund Data Room (The 3-Room Model) in 2026

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

Real Estate Fund Data Room: The 3-Room Model for 2026

Last updated: June 2026

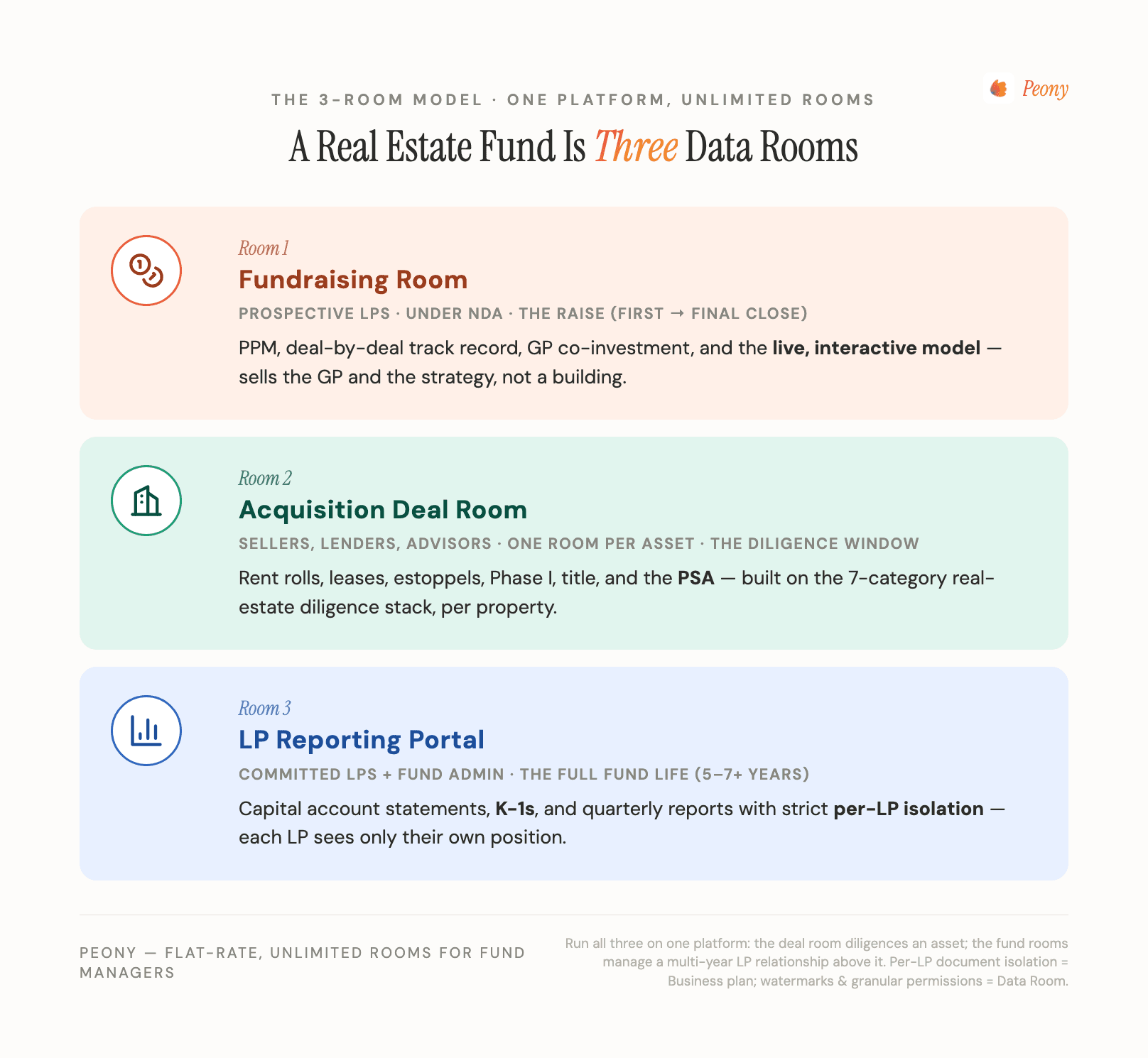

Quick answer: A real estate fund is not one data room — it's three, and treating them as one is the most common GP mistake. You need a fundraising room (PPM, track record, fund-level model, subscription docs — shown to prospective LPs under NDA), an acquisition deal room (opened per asset, holding rent rolls, leases, Phase I, and the PSA for that property), and a standing LP reporting portal (capital accounts, K-1s, quarterly reports, distribution notices — open to committed LPs for the fund's whole life). Run all three on one flat-rate platform — Peony Data Room at $52/admin/month, unlimited rooms — rather than paying per-deal VDR fees over and over across a 5-7 year fund.

I run Peony, a data room platform serving 6,800+ customers across M&A, fundraising, and real estate. Over the past 18 months I've set up rooms for first-time multifamily syndicators raising their debut $30-60M value-add fund, established sponsors running standing acquisition pipelines, and IR teams sending quarterly K-1s to hundreds of LPs. The pattern I keep seeing: GPs ask for "a data room for my real estate fund" as if it's one thing — and then jam fundraising decks, raw seller-side diligence, and LP tax documents into a single room with one permission scheme. It works until it doesn't: a prospective LP ends up seeing another investor's capital account, or a bidder on one property can see the fund's confidential model.

A real estate fund runs on three rooms, each with a different audience, lifespan, and document set. This guide breaks down all three — what goes in each, who sees what, how to share a live underwriting model without it dying in a PDF, and what the whole thing costs in 2026.

If you're running a single property transaction (buying or selling one asset), this isn't your post — see Data Room for Real Estate: 5 VDR Archetypes for the deal-level setups, and the Real Estate Due Diligence Checklist for the buyer-side document inventory. This post is the fund layer that sits above individual deals — the GP/LP relationship, not the building.

What is a real estate fund data room — and why do syndicators run three of them?

A real estate fund data room is the secure online environment a sponsor (GP) uses to raise capital from limited partners, diligence the properties the fund acquires, and report to investors over the fund's life. The reason it's three rooms and not one is that a fund serves three different audiences on three different clocks:

- Prospective LPs — during the raise, for weeks to months, looking at the fund and the GP, not at any single building.

- Sellers, lenders, and advisors — during each acquisition, for the diligence window of that specific asset.

- Committed LPs and the fund admin — for the entire 5-7 year (often longer) fund life, looking at their own positions and the fund's performance.

Collapsing those into one room forces a single permission model onto three incompatible jobs. The fix is structural: one platform, three purpose-built rooms.

| Room | Audience | Lifespan | Core documents |

|---|---|---|---|

| 1. Fundraising room | Prospective LPs (under NDA) | The raise (first close → final close) | PPM/OM, LPA/operating agreement, subscription docs, fund-level model, distribution waterfall, GP track record, team bios, GP co-invest, ILPA-style DDQ |

| 2. Acquisition deal room | Sellers, lenders, advisors, IC | Per-asset diligence window | Rent roll, leases, estoppels, Phase I, title, survey, PSA, operating statements, service contracts |

| 3. LP reporting portal | Committed LPs + fund admin | Full fund life (5-7+ years) | Capital account statements, K-1s, quarterly reports, distribution/capital-call notices, fund financials, audited statements |

The rest of this guide takes each room in turn.

How is a real estate fund data room different from a property deal room?

This is the distinction that trips up most first-time GPs, so it's worth being precise.

A property deal room (the kind covered in our 5 archetypes guide) is built around one asset and one transaction. It opens when you go to market, organizes around the standard 7-category real estate stack — title, financials, leases and rent roll, physical and environmental, market and zoning, insurance, regulatory — and closes after the sale. The audience is bidders.

A fund data room is built around a sponsor and a multi-year relationship. The fundraising room sells the GP and the strategy, not a building — the hero documents are the PPM, the track record, and the model, not a rent roll. The reporting portal stays open for years and is keyed to investors, not bidders. And the fund will spin up many property deal rooms underneath it over its life.

Put simply: the deal room diligences an asset; the fund room manages a relationship. A sponsor needs both, layered. The acquisition deal rooms are the per-deal instances; the fundraising room and reporting portal are the persistent fund-level layer above them.

Room 1 — What goes in the fundraising room when you're raising a fund from LPs?

The fundraising room exists to answer, in order, every question a sophisticated LP asks before wiring capital. Institutional diligence teams generally work down an ILPA-style due-diligence questionnaire, so the fastest-closing rooms mirror that structure:

- Fund terms. PPM / offering memorandum, limited partnership or operating agreement, subscription documents, side-letter templates. This is the legal spine of the offering.

- Strategy and the model. The fund-level underwriting model, target returns, and the distribution waterfall — preferred return (the "pref"), GP promote/carry, catch-up, and the leverage assumptions behind the projected IRR and equity multiple.

- Track record. Realized and unrealized performance, deal by deal — not just a topline IRR. Prior-fund returns, attribution, and honest treatment of any deals that underperformed. LPs trust a GP who shows the losers.

- Team and GP alignment. Principal bios, the GP co-investment commitment (how much of the GP's own capital is in the fund), and key-person provisions.

- Operations and compliance. Fund administrator, auditor, valuation policy, the completed ILPA DDQ, and Form ADV if the manager is registered.

Gate the whole room behind an NDA with integrated e-signature so a prospective LP signs before anything is visible, and use page-level analytics to see which sections each LP actually reads — the ones who spend twenty minutes in the track-record and model folders are your real prospects.

For the venture- and PE-fund version of this same exercise, our VC fund data room checklist walks the parallel structure. The fundraising discipline is identical; the documents differ — a real estate fund leads with property-level track record, NOI/cap-rate underwriting, and a real-asset waterfall rather than portfolio-company ownership.

Room 2 — How do you run the acquisition due diligence room for a fund's deals?

Once the fund is deploying capital, each property gets its own acquisition deal room — and this is exactly the territory our existing real-estate content already covers in depth, so I won't duplicate it here:

- What goes in each folder: the Real Estate Due Diligence Checklist maps all 7 categories and 80+ document types — title, rent roll, leases, estoppels, Phase I environmental, operating statements, service contracts, PSA.

- How to scope the room by deal type: the 5 VDR Archetypes guide routes CRE single-asset, multifamily portfolio, distressed, and development setups to the right folder tree and gating cadence.

- For a single apartment acquisition specifically: the multifamily acquisition data room covers reconciling the rent roll to leases without leaking resident PII — the per-asset room a value-add multifamily fund opens for each deal it closes.

The fund-specific point is how the deal rooms relate to the fund: run them as separate rooms from the fundraising room. A prospective LP has no business in the raw seller-side diligence of a specific asset, and the deal's seller has no business seeing your fund-level model or investor list. On a flat-rate platform with unlimited rooms there's no cost penalty for keeping them isolated — and the audit trail stays clean. Use a saved folder template so every new acquisition room starts from the same 7-category structure, and let AI auto-indexing classify the seller's bulk upload into the right folders rather than re-scaffolding by hand each time.

Room 3 — What does the post-close LP reporting portal contain?

This is the room most VDR guides ignore, because most VDRs are built for a transaction that ends — and a fund's reporting obligation doesn't. The LP reporting portal stays open for the fund's whole life and holds two layers of documents:

- Fund-level, shared with all LPs: the quarterly investor letter, portfolio NAV, fund financials, audited annual statements, capital-call and distribution notices.

- Investor-level, gated per LP: each limited partner's own capital account statement, K-1 tax documents, executed subscription agreement, and side letter.

The non-negotiable requirement here is per-LP isolation: every investor must see their own positions and only their own — never the other LPs' capital accounts, and never the full investor roster. A leaked LP list is a direct competitive gift to anyone raising against you, and confidentiality is a fiduciary expectation. With programmatic permission groups and per-investor folders, you configure this once with a saved permission template and reuse it every quarter, so the recurring K-1 and capital-account drop is a few minutes of work instead of a manual, error-prone re-share to each investor.

Because the portal is long-lived, the controls matter more than in a transient deal room: dynamic watermarks (viewer name + email + timestamp) on every tax document, screenshot protection, and a complete audit trail of who opened what and when — the record you want if a distribution dispute or an LP-side audit ever arises.

How do you share a live underwriting model or waterfall without it dying in a PDF?

This is where most data rooms quietly fail real estate funds. LPs want to interrogate your underwriting model and distribution waterfall — change a rent-growth assumption, see how the pref and promote split at different IRRs. Legacy VDRs convert every upload to a flat PDF, so the model arrives dead: no formulas, no interactivity. The GP ends up re-emailing the real .xlsx — which is precisely the uncontrolled leak the data room was supposed to prevent.

Peony renders your Excel model as a live, interactive spreadsheet right in the browser — the formulas compute, so an LP can change a rent-growth or exit-cap assumption and watch the returns move, essentially a Google-Sheets experience inside the room, with no download and no emailed file. For a fully bespoke model you can also publish it as an HTML artifact, which Peony renders live with the JavaScript executing (the same capability that runs interactive AI-generated artifacts in place). Both stay wrapped in the full control layer — dynamic watermarking, screenshot protection, per-viewer permissions, and instant revoke — which is exactly what the convert-to-PDF incumbents can't match. Three concrete wins:

- One version of the truth. There's exactly one current model in the room, so no LP can circulate a stale copy from their inbox.

- Show outputs, hide the secret sauce. Publish a version with the proprietary assumption tabs excluded — LPs see returns and sensitivities, not your full model logic.

- No leak round-trip. Because the live model works in the room, you never have to email the real file "just so they can play with it."

This is the clearest functional gap between Peony and the convert-to-PDF incumbents, and it maps directly onto the one document real estate LPs most want to touch.

How do you set permissions across GPs, LPs, lenders, and fund admin?

A fund's counterparties don't fit a flat admin / viewer hierarchy. Use permission groups keyed to role:

- GP / deal team — full access across all three rooms.

- Prospective LPs — fundraising room only, post-NDA, page-level analytics on.

- Committed LPs — fund-level reports shared to the group; personal capital account, K-1, and subscription docs gated to that investor alone.

- Lenders — in the relevant acquisition deal room only: debt docs, operating statements, reserves — not the fund model or investor list.

- Fund admin / auditor — reporting portal access to produce statements and K-1s, scoped to what they need.

The principle is least-privilege by audience, configured once per group and reused. For multi-bidder dynamics inside an acquisition room (keeping competing buyers walled off from each other), our multiple-bidders data room guide covers the isolation mechanics in depth.

What does a real estate fund data room cost in 2026?

For a fund, the pricing model matters more than the sticker price, because a fund runs many rooms over many years — and that's exactly where flat-rate beats per-deal:

- Peony Data Room — $52/admin/month, unlimited rooms, unlimited storage. One flat per-admin fee covers the fundraising room, every concurrent acquisition deal room, and the standing LP reporting portal — for the whole fund life. A GP with 4 admins (you + IR lead + fund admin + analyst) runs $2,496/year flat. Includes dynamic watermarks, screenshot protection, granular per-file permissions, NDA gating, and AI auto-indexing.

- Peony Business — $30/admin/month if your needs are lighter — a fundraising room plus reporting, without large per-asset deal rooms. Covers document sharing, NDA gates, and analytics; step up to Data Room when you need watermarks, screenshot protection, and granular per-file permissions for the LP portal.

- Legacy per-deal VDRs (Datasite, Intralinks) are priced for a single transaction window and bill $50,000-$80,000 per deal at enterprise tier. Fine for one bake-off; punishing across a fund's multiple acquisitions and 5-7 years of reporting, where the per-deal fee recurs with every asset and every year.

The structural point: a fund is the worst possible fit for per-deal pricing and the best possible fit for flat-rate. See the flat-rate data room breakdown for the full per-page-vs-flat math.

The bottom line: three rooms, one platform

A real estate fund isn't a data room — it's three:

- Fundraising room — sells the GP and the strategy to prospective LPs (PPM, track record, live model), NDA-gated.

- Acquisition deal rooms — diligence each asset, one room per property, built on the 7-category checklist and archetype guide.

- LP reporting portal — capital accounts, K-1s, and quarterly reports for the fund's life, with strict per-LP isolation.

Run them as separate rooms on one flat-rate platform, share your underwriting model live instead of as a dead PDF, and configure least-privilege permissions once per audience. That's the setup that reads as operational competence to an LP deciding whether to lock up capital with you for the better part of a decade — and the cheapest credibility a GP can buy.

See Peony for real estate → · Start a data room →

Related resources

- Self-Storage Data Rooms: Sell the Rate Trajectory — ECRI cohort curves, the in-place-vs-street gap, and staging the rate file amid the 2026 litigation wave

- Commercial Property Due Diligence: How to Run It Against the Clock — the per-asset acquisition diligence beneath the fund: the eight workstreams and the clock

- Data Room for Real Estate: 5 VDR Archetypes Mapped — the deal-level layer; how to scope each property transaction

- Real Estate Due Diligence Checklist (What Buyers Miss) — sibling post; the 7-category, 80+ document inventory for each acquisition room

- Note Sale Data Room — for a fund running a credit or distressed strategy: buying or selling the CRE loan/note itself (proving the chain of title to the note), rather than taking equity in the building

- Senior Housing Data Room: You're Buying an Operation — for healthcare-real-estate and RIDEA/operator structures: the operating-asset acquisition room (license, OTA, census), distinct from the blind-pool fund room

- Real Estate Syndication Data Room — the single-deal version: raising LP equity for one identified property (not a blind-pool fund)

- VC Fund Data Room Checklist (What LPs Actually Diligence) — the venture/PE-fund parallel to the fundraising room

- How to Share an Interactive LP Report With Your Limited Partners (Securely) — the reporting-portal last mile: sending a live capital-account or NAV report to each LP under a per-LP watermark instead of a flat PDF

- Private Placement Data Room — the securities-offering layer (PPM, Reg D 506(b)/506(c)) when the fund raise is run as a private placement

- Best Data Room for Multiple Bidders — bidder isolation inside an acquisition room

- Best Data Rooms for Private Equity — multi-deal pipeline workflow

- Peony for Real Estate

- Peony for Private Equity

- Peony Flat-Rate Data Room

- Peony Pricing

- Juniper Square Review (2026) — the fund-admin platform question for GPs: what it includes, what it costs, and when to add it.

You might also like

Aug 5, 2026

Juniper Square Review (2026): Pricing, Fit, and the Data-Room Question

Apr 10, 2026

I Tested 10 PE Data Rooms (What Deal Teams Actually Need) in 2026

Aug 7, 2026

Best M&A Data Rooms (I Built One, Then Tested 6 More) in 2026