Senior Housing Data Room: You're Buying an Operation, Not an Address (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Senior Housing Data Room: You're Buying an Operation, Not an Address (2026)

Last updated: July 2026

Quick answer: A senior housing data room is a deal room for buying, selling, recapitalizing, or financing an IL, assisted living, memory care, or CCRC community — and the thing that makes it different from any other commercial real estate room is that it is organized around the operations transfer, not the property. You're not buying real estate; you're assuming an operating business — a license, an operator relationship, a resident census, a payor mix, and a survey history. So the index leads with the license and the change-of-ownership (CHOW) file, then census and payor mix, then the operating structure (RIDEA/SHOP vs triple-net), then the resident agreements and survey history — because that's what decides whether the operation is clean and transferable the day control flips. Senior housing is the hottest healthcare-RE asset class in 2026: rolling four-quarter transaction volume hit roughly $24B by year-end 2025 (a decade high), cap rates compressed to about 6.2%, and 86% of investors plan to expand. The building is the easy part. When the deal involves a lender, resident PHI, and hundreds of confidential documents, that room is usually a commercial real estate data room — not email.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't operate senior housing communities for a living — but I've watched hundreds of CRE and healthcare-real-estate deals move through data rooms, and the senior-housing ones do not behave like the others. In an office or retail deal, the room is organized leases-first: the income is the asset, and the building is most of the story. In a senior-housing deal, the building is the least of it. You're buying a license, a provider/operator relationship, a resident census, and a regulatory track record — an operating business that happens to sit inside real estate. Reorganize the room around that and the whole deal reads correctly. Leave it organized like a generic CRE folder and you bury the one file the lender and the buyer actually came for: can this operation be transferred, cleanly, on day one?

That is the thesis of this post: you're buying an operation, not an address. A beautiful building with a clean Phase I and a fresh roof is worth far less than its pro forma if the assisted-living license can't transfer cleanly, the survey history hides an open deficiency, or the census is propped up by concessions. The asset class is priced on the operation; the data room has to prove the operation.

Here's the carve-out, because Peony has a family of CRE guides and this one owns a specific lane. If you want the generic CRE process and clock — caveat emptor, the contingency period, re-trades — read commercial property due diligence; this post assumes you know that and goes operations-transfer-deep. If you want the line-item document inventory for ordinary real estate, that's the real estate due diligence checklist. If you want provider and archetype selection for real estate broadly, that's data room for real estate. If you're choosing who runs the sale — the M&A advisor for the operating company — that's best healthcare M&A advisors, a different job from the property+operations data room. And one critical sibling: this hub is the housing-with-services continuum (IL/AL/MC/CCRC). For skilled nursing specifically — the clinical, government-reimbursed facility with cost reports, CMS certification, and F-tags — see skilled nursing facility data room. Same operations-transfer DNA, different payor and regulator.

Why does a senior housing data room underwrite the operation instead of the building?

Because in senior housing the building is the commodity and the operation is the asset, and everything about value flows from whether the operation is clean and transferable. You can re-roof a community in months; you cannot conjure a clean license, a stable census, and a deficiency-free survey history out of thin air. The supply of buildings can be built — slowly, given today's construction costs — but the supply of well-run, well-licensed, census-stable operations is exactly what scarce capital is bidding for.

The market context makes this concrete. Senior housing is the strongest healthcare-real-estate asset class heading into 2026. On a rolling four-quarter basis, transaction volume reached roughly $24 billion by year-end 2025 — a decade high, the strongest since the second quarter of 2015 — as improving fundamentals and institutional conviction drove deal velocity. Average cap rates compressed to about 6.2% in Q4 2025 (assisted-living non-core Class A higher, in the low-7% range; independent-living Class A core nearer 6%), and roughly 85% of investors expect flat or lower cap rates in 2026. Sentiment is one-directional: about 86% of surveyed investors plan to expand their senior-housing portfolios in 2026, and 44% name assisted living their single best opportunity.

The reason is demographic and supply-side, and it's unusually clean. The 80+ cohort — the primary driver of senior-living demand — is projected to grow by more than a quarter (around 28%) between 2025 and 2030, reaching roughly 18.8 million people. Meanwhile new construction has collapsed: starts are at decade lows, fewer than 6,000 units were delivered in 2025, and net absorption outpaced new supply by nearly five times. Estimates of the gap vary, but the consensus is a shortfall of several hundred thousand units by 2030 (figures range from roughly 560,000 to 806,000 needed, with only a fraction projected to be built). That collision — a demand wave hitting a supply drought — is pushing occupancy up (independent living crossed 91%, assisted living reached roughly 88%, with the industry projected above 90% by year-end 2026) and driving the acquisition and refinancing activity that fills these data rooms.

When the asset is an operation, the room's job changes. It is no longer to prove the building is sound. It is to prove the operation is clean, licensed, census-stable, and transferable on a credible date. That is the spine the index has to be built on.

What documents do you need to sell a senior living community?

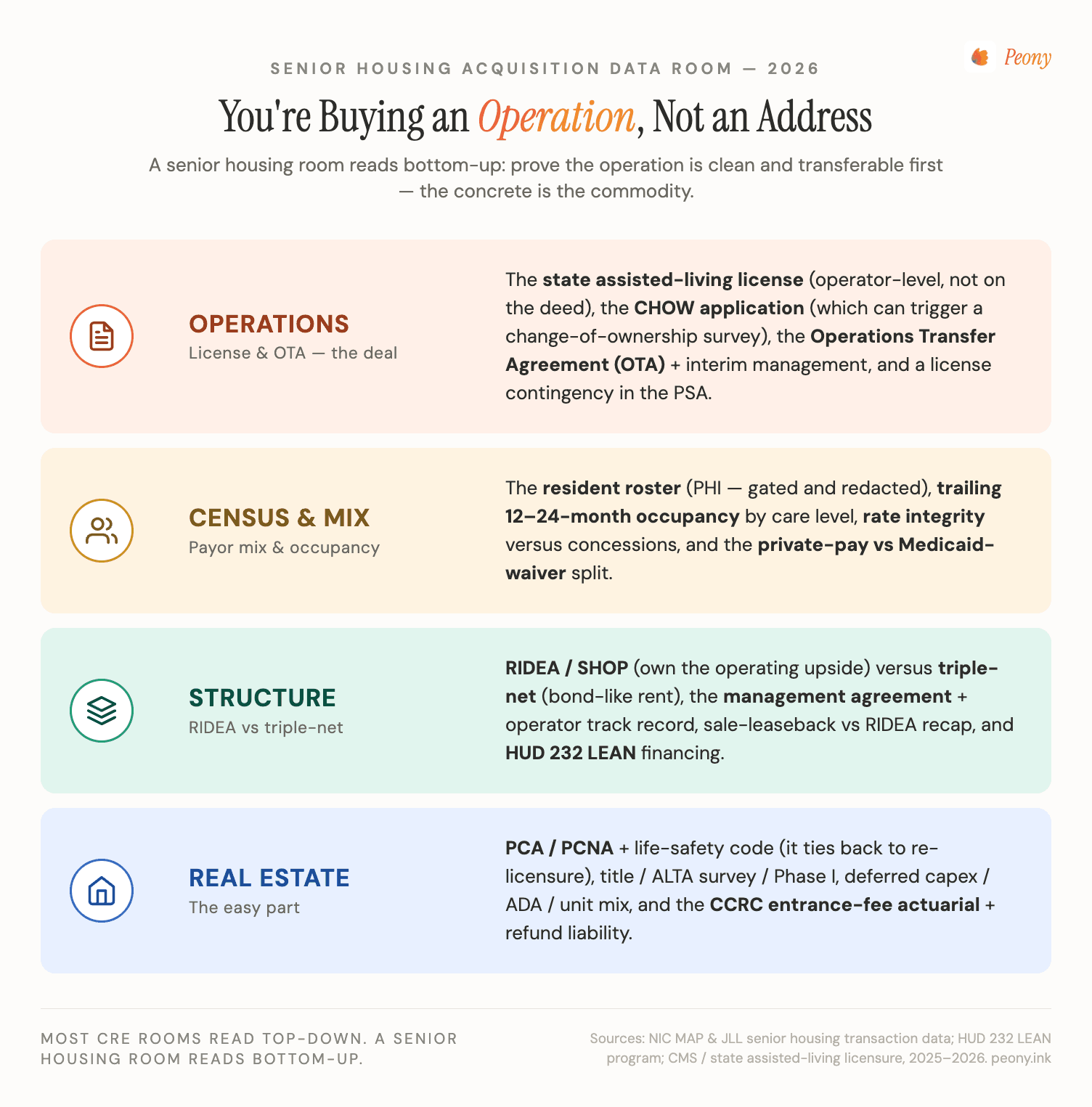

The same workstreams as any CRE deal, but re-sequenced so the operation leads and graded by the one thing that goes wrong in each. The generic CRE room puts title and leases first; the senior-housing room puts the operations transfer first, because that's the gating risk a lender or institutional buyer is actually underwriting. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Operations transfer (license, OTA, CHOW) | State assisted-living license; change-of-ownership (CHOW) application and status; operations transfer agreement (OTA); interim/bridge management agreement; license-contingency in the PSA | Assuming the license rides with the deed — when AL is licensed at the operator level, so the CHOW must be filed, may trigger a survey, and can run weeks to months |

| Census & payor mix | Resident roster; trailing 12-24mo occupancy and move-in/move-out trend; private-pay vs Medicaid-waiver split; rate integrity (concessions); memory-care census stability; lead/tour pipeline | Buying a stabilized-looking occupancy number that's actually propped by concessions or a few large at-risk residents — in-place NOI evaporates post-close |

| Operator & structure (RIDEA vs NNN, mgmt agmt) | Whether it's RIDEA/SHOP or triple-net; the management or operating agreement; operator track record and coverage; who actually holds the license | Underwriting a RIDEA/SHOP operating business as if it were a triple-net bond — or inheriting a management agreement whose terms or termination rights weren't read |

| Real estate & physical (PCA, life-safety) | Property-condition assessment / PCNA; life-safety code and fire-marshal compliance; deferred-maintenance and capex backlog; ADA and unit mix; title, survey, environmental | Treating the physical plant as the whole deal — or missing a life-safety / fire-code deficiency that the state ties to re-licensure |

| Regulatory & survey history (state AL) | Complete licensure file; survey and inspection reports; deficiencies/citations; plans of correction; complaint-survey history | A cherry-picked survey file that hides an open deficiency — which can stall the CHOW and re-license |

| Resident agreements & liability | Resident agreements and care contracts; rate schedules; CCRC entrance-fee contracts and refund-liability schedule; litigation and incident history; insurance | Unread resident-agreement terms (rate caps, refund obligations) or an undisclosed entrance-fee refund liability that transfers with the community |

| Financing (HUD 232 / agency) | HUD 232/223(f) eligibility (3-yr seasoning, ≤25% IL units, commercial-space cap); operating statements; PCNA; appraisal; operator experience; agency or bank debt and assumability | Assuming HUD timing is fast — LEAN processing typically runs 6-8 months, so a deal that hinges on agency financing has to start the file early |

A few of these deserve their own paragraph, because the standards and the liability live there.

The operations transfer is the workstream with the least flexibility. You can negotiate a price; you cannot will a license across the table. In most states, assisted living is licensed at the operator level, so the real-estate transfer does not automatically carry the right to operate. The new operator files a CHOW (change of ownership), the state reviews it, and the parties sign an OTA (operations transfer agreement) — frequently paired with an interim management agreement so resident care never lapses for a single day. The room must make this legible at the top: the license, the CHOW application and correspondence, the OTA, and the survey file the state will look at. Get this wrong and nothing else matters.

Census is where the income hides. A headline occupancy number is not a fact until you've seen the trailing trend, the attrition, and the rate integrity behind it. A community at "93% occupancy" held together by two months of concessions and three large private-pay residents who are one health event from moving out is not the same asset as one at 89% with a clean rate roll and a full tour pipeline. We'll come back to how the room makes this auditable.

The physical plant still matters — it's just not the headline. A property-condition assessment (PCA/PCNA) and a life-safety-code review belong in the room; senior housing carries fire-code, sprinkler, and ADA obligations that a state can tie directly to re-licensure. Our real estate due diligence checklist covers the standard physical and title workstreams; here, just make sure the life-safety file is actually present and current, because a fire-marshal deficiency can become a closing condition.

What is a CHOW, and how do you run the operations transfer?

A CHOW — change of ownership — is the regulatory process by which the community's operating license moves to (or is reissued to) the new operator, and the operations transfer is the choreography of doing that without dropping care to a single resident. This is the single most important section of a senior-housing deal, because the license, not the deed, is what lets you legally operate and bill on day one. Run it right and the rest is ordinary CRE; run it wrong and you own a building you can't operate.

Run it in this order, top of the index downward:

- State assisted-living license. Confirm who holds it, the license type and capacity (and any memory-care or dementia-care endorsement), the expiration, and whether it's in good standing. In most states this is an operator-level license, which is the whole reason a CHOW exists.

- Change-of-ownership (CHOW) application and status. The new operator files with the state licensing agency. Read the application, the agency correspondence, and the assumed timeline. Expect that the CHOW can run weeks to months and may trigger a change-of-ownership survey of the community.

- Operations transfer agreement (OTA). This is the contract among the current operator, the new operator, and (often) the owner that governs the orderly handoff — resident records, employees, vendor contracts, deposits, accounts, and the obligation to keep the license in good standing through transfer. Public OTAs (operators like The Pennant Group have filed them) show the shape: continuity of licensure is the spine.

- Interim / bridge management agreement. Because the CHOW often closes after the real-estate transfer, the parties frequently sign an interim management agreement so the seller's operator (or a transitional manager) runs the community under the existing license until the new license issues — care never lapses.

- License-contingency in the purchase agreement. The PSA should make the deal contingent on the license/CHOW path, and allocate who bears the risk and cost if a survey turns up a deficiency that has to be cured before re-licensure.

The non-negotiable rule: the closing structure has to match the licensing timeline. If the model assumes you're operating and billing on the deed-transfer date but the CHOW won't clear for 90 days, that gap is the deal. A lender will not fund — and a buyer should not close blind — on a "the license will transfer eventually" assumption. Make the license, the CHOW, the OTA, and the survey correspondence the first folder every reviewer opens.

What is the difference between a RIDEA (SHOP) and a triple-net senior housing deal?

It comes down to who carries the operating risk and the operating upside — and it changes what the room has to prove. The structure isn't a footnote; it's the difference between underwriting a rent check and underwriting an operating business.

| Triple-net (NNN) lease | RIDEA / SHOP | Direct owner-operator | |

|---|---|---|---|

| Who operates | A third-party operator leases from the REIT/owner | REIT participates in NOI via a TRS + a management agreement | The owner is the operator |

| Who carries the risk | Operator (REIT gets fixed rent + escalators) | REIT shares operating upside and downside | Owner-operator, fully |

| What the room leads with | The lease + the operator's rent-coverage ratio | The management agreement + census + payor mix + labor + track record | The full operating + real-estate file |

| It behaves like | A bond (credit + duration of the lease) | An operating business inside real estate | An operating business you own outright |

The trap is underwriting the wrong shape. A triple-net community is closer to a credit-tenant bond — you read the lease, the escalators, and whether the operator's coverage can service the rent. A RIDEA/SHOP community is an operating business: you read the management agreement, the census, the payor mix, the labor model, and the operator's track record, because you're directly exposed to occupancy and rate. Conflating them is expensive in both directions — modeling RIDEA upside off a triple-net's fixed rent understates the asset, and underwriting a RIDEA deal as if rent were guaranteed ignores the operating downside.

The reason this is front-of-mind in 2026 is that the largest owners are voting with their balance sheets. Through 2025, Welltower and Ventas both moved aggressively to convert triple-net communities into RIDEA/SHOP — Welltower reported roughly $14 billion of senior-housing acquisitions across 700-plus communities (part of about $23 billion of total transactions that year) and launched a new operator-alignment model with longtime partners, precisely to capture the operating upside the demand wave is creating. Omega Healthcare and LTC Properties have likewise leaned into RIDEA structures. When the institutional buyer's whole thesis is "own the operation, not just the rent," the seller's room has to make the operating numbers legible — or leave money on the table.

How do you diligence census, payor mix, and rate integrity?

You treat the census as the income statement it actually is, and you refuse to accept a headline occupancy number as a fact. Census and payor mix are where senior-housing deals are won and lost, because in a RIDEA/SHOP or owner-operator deal the occupancy and the rate are the NOI.

Here's what belongs in the room, and what each item is really testing:

- Resident roster and rent roll. The unit-by-unit roster — unit, care level (IL/AL/MC), move-in date, current rate, and contract type. This is protected health information, so it's gated and redacted (more below), but the buyer has to see the structure.

- Trailing occupancy and absorption trend. 12-24 months of occupancy, ideally split by care level. A flat headline can hide a memory-care wing softening while independent living fills.

- Move-in / move-out (attrition) data. Senior housing has natural, sometimes high, resident turnover; the question is whether move-ins are outpacing move-outs and what the replacement rate and lead pipeline look like.

- Rate integrity and concessions. How much of the in-place rate is real versus propped by move-in incentives, fee waivers, or below-market legacy rates? A community's "stabilized" NOI can be a concession mirage.

- Payor mix — private-pay vs Medicaid waiver. The housing-with-services continuum is private-pay-led, but some states layer Medicaid waiver dollars into assisted living. A private-pay community and a waiver-dependent one carry very different rate ceilings and reimbursement risk; the mix is a core value driver.

- Memory-care specifics. MC carries higher rates and higher acuity; its census stability, staffing ratios, and any state-mandated dementia-care requirements deserve their own read.

The #1 thing that goes wrong here is simple and recurring: buying a stabilized-looking occupancy number that's actually fragile — held up by concessions, by a handful of large private-pay residents near a health transition, or by a payor mix more waiver-dependent than the teaser implied. The room's job is to make the trend and the rate integrity auditable, not just the snapshot. And because the roster is full of PHI, it has to live behind an NDA gate with redaction and per-viewer watermarks — you cannot circulate a resident roster the way you'd circulate an office rent roll.

What survey, licensure, and resident-facing diligence belongs in the room?

The complete regulatory and resident-facing file — because the new operator inherits the regulatory posture and the resident obligations, and a buried deficiency or an unread refund liability becomes your problem the day control flips. This is the workstream most likely to be cherry-picked by a seller, which is exactly why a sophisticated buyer treats gaps as red flags.

On the regulatory side, the room should carry:

- The full state assisted-living licensure file — not a summary. License type, capacity, endorsements, standing, and history.

- Survey and inspection reports, including routine and complaint surveys, with all deficiencies and citations and the plans of correction. An open or recently-cured deficiency can directly affect the CHOW and re-licensure, so it has to be visible.

- Complaint and incident history and any enforcement actions, because the regulatory track record is part of what a lender and a buyer are pricing.

On the resident-facing side:

- Resident agreements and care contracts — the actual terms residents signed: rates, rate-increase caps, services included, and termination/refund provisions. These transfer with the community.

- CCRC entrance-fee contracts and the refund-liability schedule (for life-plan communities) — covered in its own section below, because the liability is long-dated.

- Litigation, incident, and insurance history — slip-and-falls, elopement events, wrongful-death claims, and the liability-insurance and any professional-liability coverage that responds to them.

The handling wrinkle that's unique to this asset class is PHI. Senior-housing records contain protected health information — names, conditions, care plans, incident details. A HIPAA-conscious room gates the resident and survey folders behind an NDA, redacts PHI where the buyer needs the structure but not the identities, burns a per-viewer watermark into every page so a leaked document is traceable to one viewer, and grants access by role so the lender, the buyer, and the incoming operator each see only their slice. This is table stakes for senior housing in a way it isn't for an industrial warehouse.

How does the data room actually run a senior housing transaction?

It runs it as a permissioned, operation-first workflow where the license and CHOW are legible at the top, the census and resident PHI are gated and redacted, and you can see who actually read the survey history before the call. A senior-housing deal moves 200-plus sensitive documents — the license, the OTA, the resident roster, survey deficiencies, management agreements, operating statements, entrance-fee contracts — among a buyer, a seller, a HUD or agency lender, a PE or REIT capital partner, an incoming operator, and several sets of counsel. Email and consumer file-sharing cannot gate, watermark, redact, or track that. Here's how a room like Peony maps to the specific risks of this asset class, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when the document set is large, the viewer list keeps growing, and the records are HIPAA-sensitive.

- NDA gate. The resident roster and survey deficiencies are the most confidential items in the deal. A click-through NDA in front of the room — or in front of the specific resident/survey folder — means a viewer agrees before they see a single resident's name or a single citation, and you have the record that they did.

- Dynamic per-viewer watermarks. The same resident roster opens for the lender, the buyer, and the incoming operator with each viewer's identity burned into the page. If a PHI-laden document leaks, the watermark says whose copy it was — a real deterrent when you're circulating protected health information.

- Page-level analytics. You see who viewed what and for how long — did the lender actually open the survey history and the census trend, or just the teaser financials? That tells you where the real questions are coming before the diligence call, and which party is genuinely engaged. (This is view-and-dwell analytics — who-viewed-what-and-how-long — not keystroke capture.)

- Redaction. Resident names and conditions in a roster, personal data in an incident report, or pricing in a third-party contract can be redacted at the document level so a lender or buyer sees the structure without the confidential specifics — the practical mechanism for staying HIPAA-conscious while still moving the deal.

- AI auto-indexing. Drop a disorganized export — hundreds of files from the operator, the licensing file, and counsel — and the room indexes it so the license, the CHOW, the census, and the survey history land in a navigable structure instead of a flat dump. In a deal where the index is the argument ("the operation is clean and transferable, here's the order"), that's not cosmetic.

- Role-based permission groups. The HUD lender lives in the operator, census, PCNA, and financial folders; the PE partner sees a curated subset; the incoming operator sees operating and census data but not the seller's other-portfolio information; brokers and counsel sit across the deal. One room, many sightlines.

For a 5,900+-customer flat-rate room, the structural fit is the mid-market-to-institutional single community, the small-to-mid portfolio roll-up, the RIDEA/SHOP recapitalization, the sale-leaseback, and the HUD 232 financing — where the document set is large, confidential, and PHI-laden, but the deal doesn't warrant a six-figure VDR procurement.

Where you don't need any of this. Be honest about the floor. A single small assisted-living building trading all-cash between two parties with one attorney can run on a handful of emailed PDFs — a data room is overkill, as long as the PHI is handled carefully. And at the opposite extreme, a $1B-plus REIT portfolio M&A take-private with a full banking syndicate will default to Datasite or Intralinks; that's their lane and I won't pretend otherwise. The data room earns its place in the wide middle: any deal with a lender, resident PHI, a survey file, a capital partner, and a document set too large and too sensitive for email — which is most senior-housing transactions that aren't either a two-party single-building sale or a mega-cap portfolio.

What goes in a HUD 232 financing data room, and how do you handle a CCRC?

These are the two financing-and-structure cases that trip people up, so they get their own section. A HUD 232 financing data room is built around what the lender and HUD's Office of Residential Care Facilities need to underwrite an FHA-insured loan; a CCRC room has to carry a long-dated entrance-fee liability that ordinary senior housing doesn't.

HUD 232 / 223(f). The Section 232 program insures mortgages on residential care facilities — assisted living, memory care, board-and-care — and via 232/223(f) it covers acquisition and refinance, not just new construction. The attraction is real: terms up to 35 years, fixed-rate and fully amortizing, non-recourse. The cost is timeline and eligibility. The room has to be lender-ready early because LEAN processing typically runs six to eight months. And the program has gating eligibility items the room must surface up front:

- The property is generally at least three years old for a 223(f) refinance/acquisition.

- Independent-living units are capped (broadly around 25% of the facility) — 232 is a care-facility program, not a market-rate-apartment program.

- Commercial space is limited (broadly not exceeding ~20% of area or income).

- Operator experience and the survey/licensure track record carry weight, alongside a project capital-needs assessment (PCNA), an appraisal, title, survey, environmental, and operating statements.

The trap is assuming agency timing is fast; a deal that hinges on a 232 has to start its file the day the LOI is signed. See our due diligence cost breakdown for the third-party report line items that feed the file, and our M&A due diligence process guide for sequencing the workstreams against the closing clock.

CCRC / life-plan communities are the hardest senior-housing asset to underwrite, because the entrance fee creates a liability, not just income. Residents pay a substantial entrance fee — commonly $100,000 to over $1 million, often around $400,000 — under a Type A (life-care, most comprehensive, care costs largely capped), Type B (modified, discounted care for a set period), or Type C (fee-for-service, lowest entrance fee, market-rate care) contract. Refund terms range from fully refundable to a declining-scale that amortizes toward zero. The diligence centers on:

- The entrance-fee actuarial study — many states require one every three to five years — testing whether the community is funding its future care obligations.

- The refund-liability schedule — how much of the entrance-fee cash on the balance sheet is actually owed back to residents or their estates.

- The contract-type mix (A/B/C) and the rate structure, because a Type-A-heavy community has carried a much larger future-care obligation than a Type-C one.

The trap is treating entrance-fee cash as free money when a chunk of it is a refundable liability. And because a CCRC spans the full continuum — IL, AL, memory care, and often skilled nursing under one roof — the room has to carry both the housing-with-services file described here and, for the SNF wing, the clinical file detailed in our skilled nursing facility data room guide.

How do you organize the index, and who gets access at what level?

Organize the index so the operations transfer is folder one and grant access by role, not by a single shared link — because the fastest way to signal "the operation is clean and transferable" is to make the license-and-CHOW file the first thing every reviewer sees, and the fastest way to mishandle resident PHI is to hand everyone the same link.

A working top-level index for a senior-housing deal:

- Operations transfer & licensure — state assisted-living license, CHOW application and correspondence, OTA, interim management agreement, survey and deficiency history, plans of correction.

- Census & payor mix — resident roster (gated/redacted), trailing occupancy by care level, move-in/move-out trend, rate roll and concessions, private-pay vs Medicaid-waiver split, lead/tour pipeline.

- Operator & structure — RIDEA/SHOP or triple-net designation, management or operating agreement, operator track record and coverage, organizational chart of who holds the license.

- Resident agreements & liability — resident agreements and care contracts, rate schedules, CCRC entrance-fee contracts and refund-liability schedule, litigation/incident history, insurance.

- Real estate & physical — PCA/PCNA, life-safety/fire-code compliance, deferred-maintenance and capex, ADA, unit mix, title, ALTA survey, environmental (Phase I).

- Financial — trailing and trended operating statements, rent/rate roll, budget, T-12 and T-3, and the model.

- Financing — HUD 232/223(f) or agency/bank debt, assumability, the PCNA and appraisal feeding the lender, and the financing-eligibility items.

- Corporate & closing — entity docs, vendor and employment contracts, any CBA, closing checklist.

Access then maps to who needs which folders:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Buyer / acquirer deal team | All | Full access |

| HUD / agency lender | Operator & structure, census, financial, real estate, financing | NDA gate; watermark; analytics on the survey + PCNA |

| PE / institutional / preferred-equity | Curated subset — model, census summary, structure, survey summary | Restricted permission group |

| Incoming operator (RIDEA/SHOP or mgmt) | Operating & census data, resident agreements | No access to seller's other-portfolio data; redaction |

| Investment-sales broker / counsel | Cross-deal | Role-based; full or near-full |

This is exactly the kind of segmentation that permission groups plus per-viewer watermarks and document-level redaction make routine, and it's where a flat-rate model helps: when the lender adds three analysts and the operator adds counsel, you're not paying per seat to keep a PHI-laden room honest. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane the room is built for.

The bottom line: which senior housing data room do you actually need?

You're buying an operation, not an address — so the right answer depends on deal size, structure, and how much regulated, resident-facing complexity is in play, not on brand prestige. Here's the segmented recommendation from someone who watches these rooms run.

- Single small community, all-cash, two parties, one attorney: You may not need a data room at all. A clean, well-named set of PDFs — license, recent survey, census, rate roll, title — emailed to one counterparty can be enough, as long as the resident PHI is handled carefully. Don't over-tool a two-party single-building trade. If you want structure without cost, a flat-rate room is still cheaper than most people assume, but it's optional here.

- Regional operator, developer, REIT, or PE buyer (single community or portfolio, a RIDEA/SHOP recap, a sale-leaseback, or a HUD 232 financing): This is the sweet spot for a flat-rate room. You have a lender underwriting the operation, resident PHI and survey deficiencies in play, a capital partner doing confirmatory diligence, and 200-plus documents that email can't gate, redact, or track. A room like Peony — NDA gate, per-viewer watermarks, page-level analytics, redaction, AI auto-indexing, role-based groups, flat $52/admin/month — fits the document volume and the confidentiality without a per-page or per-user meter.

- $1B+ REIT portfolio M&A / take-private: Default to Datasite or Intralinks. A full banking syndicate, a global bidder list, and integrated deal tooling are their procurement reality, and that's the honest recommendation at that altitude.

Whichever tier you're in, the discipline is the same: make the license and CHOW legible first, prove the census and rate integrity, read the operating structure for what it actually is, gate and redact the resident PHI, and surface the full survey history rather than the flattering slice. Build the room around the operation and the deal reads correctly to everyone who has to underwrite it. And if your asset sits at the clinical end of the spectrum, remember the sibling: skilled nursing is a different room — skilled nursing facility data room — and so are the other CRE asset classes, from data centers to industrial, each with its own operation-first index under the same commercial real estate hub.

Sources

- NIC / NIC MAP Vision — senior housing transaction volume (~$24B rolling four-quarter by YE2025, decade high); occupancy (independent living >91%, assisted living ~88%, industry projected >90% by YE2026); future-inventory-needed estimates (hundreds of thousands of units by 2030).

- JLL — 2026 Seniors Housing & Care Investor Survey and Trends — rolling four-quarter volume ~$24B through Q4 2025 (highest since Q2 2015 ~$26B); investor sentiment.

- CBRE — U.S. Senior Housing & Care Investor Survey (H2 2025) — cap rates compressed to ~6.2% (Q4 2025); segment Class A ranges (IL ~6.1% core / non-core higher; AL non-core ~7.2%); ~85% expecting flat/lower 2026 cap rates.

- Senior Housing News / McKnight's Senior Living — 86% of investors plan to expand in 2026; 44% name assisted living the top opportunity; rent-growth guidance.

- HUD — Office of Residential Care Facilities; Section 232 / 232(223)(f) "LEAN" program — eligible property types (AL, memory care, board-and-care); acquisition/refinance via 223(f); ~35-year term; ~6-8-month LEAN timeline; eligibility (3-year seasoning, ≤25% IL units, commercial-space cap).

- Welltower (Oct 27, 2025 release) / Ventas / Omega / LTC Properties — RIDEA/SHOP conversions; Welltower

$14B senior housing acquisitions across 700+ communities ($23B total 2025 transactions); operator-alignment model. - NIC / Argentum / NIC MAP demographic analyses — 80+ cohort growth ~28% 2025-2030 (to ~18.8M); construction starts at decade lows; absorption outpacing supply; the 2030 supply gap.

- Continuing-care / actuarial sources (American Academy of Actuaries; CCRC operators) — Type A/B/C contracts; entrance fees

$100K-$1M+ ($400K avg); refund structures; actuarial study every 3-5 years. - Arnall Golden Gregory; state licensing agencies; The Pennant Group OTA filing — CHOW process; operator-level assisted-living licensure; operations transfer agreement structure and continuity-of-license obligations.

This article is general information for deal teams, not legal, tax, healthcare-regulatory, or investment advice. Licensure and change-of-ownership rules, HUD program criteria, CCRC and entrance-fee regulation, cap rates, transaction volume, and the specific deals and figures referenced vary by state and change over time — verify current requirements, survey status, and contract terms with qualified healthcare-regulatory counsel, a HUD-approved lender, and a licensed appraiser or actuary before relying on them. Peony is a data room provider, not a broker, lender, operator, or healthcare-regulatory firm.

You might also like

Jul 1, 2026

Cell Tower Data Room: How a Tower Portfolio Sale Closes (2026)

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Jul 1, 2026

Industrial Data Room: The One That Survives the Buyer's Engineer (2026)