Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Last updated: July 2026

Quick answer: A data center data room is a deal room for buying, selling, financing, or JV-ing a data center — and the thing that makes it different from any other commercial real estate room is that it is organized around energization risk, not square feet. The document set leads with the power stack — the Will-Serve / power-availability letter, the interconnection agreement (LGIA/SGIA) and its cost-allocation, any PPA or behind-the-meter arrangement, and substation/transformer lead times — because in 2026 power is the binding constraint: U.S. interconnection queues hold roughly 2,600 GW with a ~5-year median wait (≈8 years for 2025 energizations in PJM/Virginia), and Northern Virginia vacancy sits near 0.3-0.5%. A powered shell or powered-land parcel with credibly secured power outranks a finished building with an uncertain energization date. The room underwrites the megawatts. When the deal involves a lender, a hyperscale tenant under NDA, and hundreds of confidential documents, that room is usually a commercial real estate data room — not email.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't build data centers for a living — but I've watched hundreds of CRE deals move through data rooms, and the data-center ones do not behave like the others. In an office or retail deal, the room is organized leases-first: the income is the asset. In a data-center deal, the income is downstream of a more basic question — can this thing be powered, on what timeline, and at what cost? Reorganize the room around that question and the whole deal reads correctly. Leave it organized like a generic CRE room and you bury the one file the lender and the tenant actually came for.

That is the thesis of this post: the data room underwrites the megawatts. A powered shell, or even raw powered land, with a signed interconnection agreement and a credible energization date is worth more than a beautiful finished building whose power is "in the queue." The asset class has been repriced around the grid, and the document set has to follow.

Here's the carve-out, because Peony has a family of CRE guides and this one owns a specific lane. If you want the generic CRE process and clock — caveat emptor, the 30-90 day contingency, re-trades — read commercial property due diligence; this post assumes you know that and goes power-deep. If you want the line-item document inventory for ordinary real estate, that's the real estate due diligence checklist. If you want provider and archetype selection for real estate broadly, that's data room for real estate. And if you're working a different infrastructure asset class, see the sibling guides launching alongside this one — cell tower data room (ground leases and tower cash flows) and industrial data room (logistics and warehouse). Data centers are the power-constrained member of that family.

Why does a data center data room underwrite the megawatts instead of the building?

Because in 2026 power is the scarce input, and everything about the asset's value flows from whether that power is secured. Data centers are the hottest CRE asset class on the back of AI and GPU demand, but the constraint has shifted from real estate to electricity. The supply of buildings can be built; the supply of deliverable power cannot keep pace.

The numbers tell the story. As of early 2026, U.S. interconnection queues held on the order of 2,600 GW of proposed generation and storage, and the timeline from interconnection application to commercial operation in PJM had stretched to roughly eight years for projects energizing in 2025 — up from under two years in 2008. The U.S. median wait is around five years. In Northern Virginia, the world's largest data center market, vacancy fell to roughly 0.3-0.5% — the lowest of any primary market — with available powered supply at about 21.5 MW at the end of 2025 and 96% of 2026 scheduled supply already committed. Dominion Energy's batching process has further extended power-delivery timelines.

When power is that scarce, the market reprices around it. Powered land — an entitled site with a committed utility load, typically 50-200MW — now commands a premium, because it collapses years of risk. Institutional capital has organized around the concept: investors pay up for shovel-ready, powered, and entitled sites precisely because they shorten time-to-energization. So the data room's job is no longer to prove the building is sound. It is to prove the megawatts are real, contracted, and arriving on a credible date. That is the spine the index has to be built on.

What goes in a data center acquisition data room?

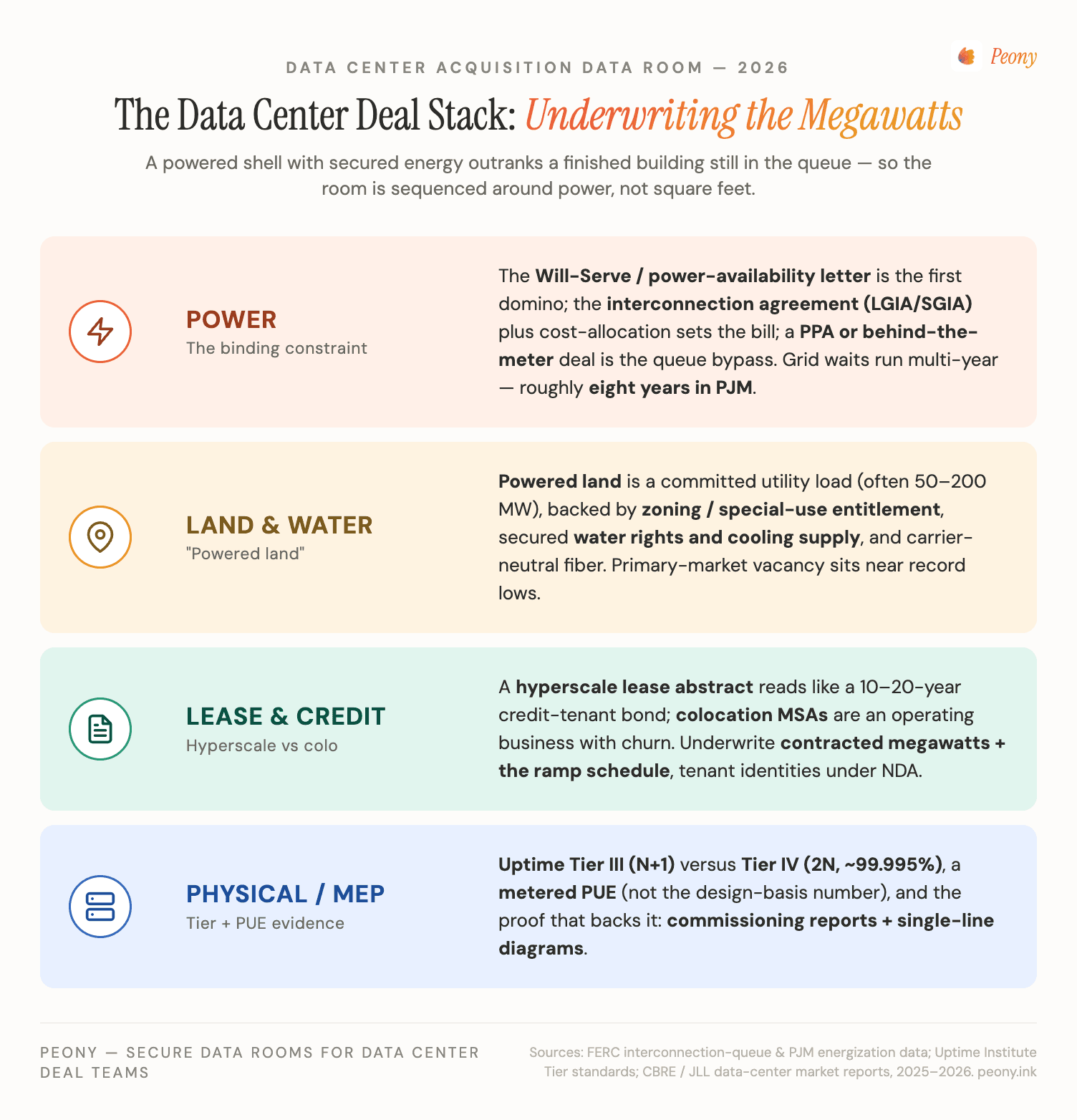

The same eight workstreams as any CRE deal, but re-sequenced so the power stack leads and graded by the one thing that goes wrong in each. The generic CRE room puts title and leases first; the data-center room puts energization first, because that's the gating risk a lender or hyperscale tenant is actually underwriting. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Power & energization | Will-Serve / power-availability letter; interconnection agreement (LGIA/SGIA) + cost-allocation/cost-responsibility; energization schedule; PPA / behind-the-meter terms; substation & transformer capacity and lead times | Treating a Will-Serve letter as firm, contracted power — when it's only an availability indication, and the binding timeline and cost live in an LGIA that may still be years out in the queue |

| Land, entitlement & water | Zoning / special-use permit, site plan, entitlement status, water rights and cooling-water availability, sound/setback compliance | The site is "powered" but not fully entitled — a special-use or water-allocation gap stalls the build long after the power is secured |

| Lease & tenant credit | Hyperscale lease abstract (term, rent, escalations, MW, options, termination) or colocation MSAs, rent roll, customer concentration, tenant financials | Underwriting a colocation rent roll as if it were a single credit-tenant bond — or accepting a hyperscale lease without reading the termination and power-ramp clauses |

| Physical / MEP | Cooling design (air vs liquid), redundancy (N+1 / 2N), Uptime Tier certification, single-line diagrams, commissioning (Cx) reports, capacity vs design load | Accepting an asserted "Tier III/IV" with no Uptime certification, no single-lines, and no commissioning evidence — a marketing claim treated as a diligence fact |

| Environmental (Phase I/II) | Phase I ESA to ASTM E1527-21; Phase II soil/groundwater sampling if a Recognized Environmental Condition appears; backup-generator fuel storage and air permits | Generator fuel tanks and emissions permits get overlooked; closing on a stale Phase I forfeits the CERCLA innocent-landowner defense |

| Title & survey | Title commitment (Schedule B exceptions), ALTA/NSPS survey, easements — especially utility, fiber, and transmission easements and rights-of-way | A transmission or fiber easement isn't reconciled against the survey, and the power or connectivity route turns out to be encumbered |

| Financial | Development: yield-on-cost, cost-to-complete, contingency. Stabilized: in-place lease NOI, escalations, WALT, expense recoveries | Modeling a powered-land deal on stabilized-asset assumptions — ignoring the cost and time to actually energize and fit out |

A few of these deserve their own paragraph because the standards and the liability live there.

Power is the workstream with the longest lead time and the least flexibility. You can re-roof a building in months; you cannot conjure an interconnection out of a five-to-eight-year queue. So the room must make the power story legible at a glance: the Will-Serve letter on top, the interconnection agreement and cost-allocation beneath it, the PPA or behind-the-meter arrangement, then the substation and transformer specs with their lead times. A lender reads these in order, and if the order is scrambled, the deal slows.

Physical/MEP is where claims masquerade as facts. Uptime Institute Tier ratings and PUE numbers get quoted in teasers, but a tier cannot be self-certified — it requires Uptime's review. The diligence version is the certificate, the single-line diagrams, and the commissioning reports, not the headline. We'll come back to this.

Environmental has a data-center wrinkle. Beyond the standard Phase I to ASTM E1527-21 (the only edition the EPA recognizes for All Appropriate Inquiries since February 13, 2024), data centers carry backup-generator fuel storage and air-emissions permits that ordinary office assets don't. Our environmental due diligence guide covers the Phase I/II mechanics; here, just make sure the generator and fuel-storage file is actually in the room.

What is the difference between powered land and a powered shell — and why does it change the diligence?

Powered land is an entitled site with committed utility power but no building; a powered shell is a built, energized building envelope with the data-hall fit-out left to do. The distinction is the single most important thing to establish about a data-center asset, because it tells you what you are actually buying and therefore what the room has to prove.

| Powered land | Powered shell | Turnkey / stabilized | |

|---|---|---|---|

| What exists | Entitled site + committed power load (often 50-200MW) | Building shell, roof, core utilities, energized | Fully built, fitted, often leased and operating |

| What you're buying | Secured megawatts + a development path | The shell + the power + a fit-out path | An income stream / credit tenant |

| Diligence weight | Interconnection timeline, entitlement, cost-to-complete | As-built shell + MEP design basis + what's included | In-place NOI, lease, tenant credit, as-built MEP |

| The room leads with | Will-Serve + LGIA + entitlement | Power stack + shell as-builts + MEP basis | Lease abstract + operating data + Tier/Cx |

The trap is selling — or underwriting — the wrong story. A powered-land deal modeled on stabilized-asset cash flows ignores the cost and time to energize and build, and a powered shell marketed as if the fit-out were included will re-trade the moment the buyer's engineer scopes the gap. The reason the distinction is worth real money in 2026 is scarcity: when a market like Northern Virginia has roughly 21.5 MW of available supply, a powered shell with a signed interconnection agreement is closer to a finished, leasable asset than a finished building whose power is still in the queue. Secured power is the asset; the concrete is the easy part. That is the literal meaning of "the room underwrites the megawatts."

What is a Will-Serve letter, and how do you run interconnection due diligence?

A Will-Serve letter is the utility's written statement that it can and intends to serve a stated load at a site — the first piece of evidence that the megawatts are real — and interconnection due diligence is the work of confirming that the rest of the power stack actually binds that promise on a credible timeline and cost. Get this section right and the rest of the deal is ordinary CRE; get it wrong and nothing else matters.

Run it in this order, top of the index downward:

- Will-Serve / power-availability / capacity-reservation letter. The threshold indication. Read it for the load it covers, the assumed timeline, the conditions, and — critically — what it does not promise. Regulated utilities operate under a "duty to serve," but that duty does not erase a multi-year queue. A Will-Serve letter is an availability indication, not a firm, contracted, on-schedule supply.

- Interconnection agreement — LGIA or SGIA. This is what actually binds it. The Large (or Small) Generator Interconnection Agreement is the FERC pro forma contract governing how the load connects. Confirm the queue position, the studies behind it (feasibility, system-impact, facilities), and the post-Order No. 2023 cluster-study status — FERC's 2023 reforms moved the industry to cluster studies and reformed how costs get allocated.

- Cost-allocation / cost-responsibility. Who pays for the network upgrades and interconnection facilities — and how much — is the line that quietly blows up pro formas. Network-upgrade cost responsibility can be enormous and is exactly what the interconnection studies size.

- PPA / behind-the-meter generation. If the deal relies on a power-purchase agreement or on-site generation, read the term, price, curtailment, and credit. Behind-the-meter is increasingly the way deals sidestep the queue entirely — the model behind Alphabet's roughly $4.75 billion acquisition of Intersect Power (announced late 2025), built around co-located "energy parks" that pair generation and storage with the data-center load.

- Substation & transformer capacity and lead times. Even with an agreement, the physical equipment has its own queue. Large-power transformers carry long manufacturing lead times; a deal can be "powered" on paper and still bottlenecked on a transformer delivery date. The room should show the equipment plan and its schedule.

The non-negotiable rule: the energization date in the model has to be traceable to documents in the room. If the pro forma assumes power in 2027 and the queue position implies 2030, that gap is the deal. A construction lender will not fund — and a hyperscale tenant will not commit — on a Will-Serve letter alone.

What is a hyperscale lease abstract, and how is colocation tenant credit different?

A hyperscale lease abstract is a one-page distillation of a long-term, single-tenant, triple-net lease — and the reason it matters is that a hyperscale data center is essentially a credit-tenant bond: its value is the credit and duration of one tenant's promise to pay. A colocation building is the opposite — an operating business with many customers — and conflating the two is one of the most expensive errors in the asset class.

For a hyperscale lease, the abstract has to capture:

- Term and renewals — typically 10-20 years, often with extension options; wholesale colocation and hyperscale leases commonly run a decade or more.

- Rent and escalations — base rent, the escalator (fixed or indexed), and any free-rent or ramp period tied to power delivery.

- The power commitment — the contracted megawatts and the ramp schedule, because the rent often steps with energized capacity.

- Options and termination — expansion rights, rights of first refusal, and any early-termination or contraction rights that puncture the "bond" thesis.

- Tenant credit — who actually signs (parent guarantee vs a thin subsidiary), since a 15-year lease is only as good as the entity behind it.

For colocation, you're underwriting a rent roll, not a bond: the MSAs (master service agreements), customer concentration, service-level commitments, churn and renewal probability, and the operating margin of the business. It behaves far more like multi-tenant office or industrial — closer to the income-verification work in our real estate due diligence checklist — than like a single-tenant net lease.

Two practical room notes. First, tenant identities are usually confidential — hyperscalers frequently lease under NDA and code names — so lease abstracts and customer schedules belong behind an NDA gate with per-viewer watermarks, not in an open folder. Second, abstract the two asset types in separate folders with separate templates; a reviewer who opens the lease file should immediately know whether they're reading a bond or a business.

What do Uptime Tier III, Tier IV, PUE, and redundancy actually tell a buyer?

They describe the facility's resilience and efficiency — but only the evidenced versions count. The single most common MEP-diligence error is accepting a marketing tier as a diligence fact. Here's the honest reading.

| Spec | What it means | What the room must contain to prove it |

|---|---|---|

| Tier III | Concurrently maintainable: N+1 redundancy and redundant distribution paths, so any component can be maintained without a shutdown | Uptime Institute certification (design and/or constructed-facility), single-line diagrams, commissioning reports |

| Tier IV | Fault-tolerant: 2N (fully duplicated) systems and simultaneously active paths; survives any single failure; targets ~99.995% uptime | Same — plus evidence both paths are genuinely independent end-to-end |

| PUE | Power usage effectiveness = total facility power ÷ IT power; lower is better | Metered, trailing operating PUE — not just a design number; the industry average is ~1.54 and has barely moved in six years |

| N+1 vs 2N | N+1 = full load plus one spare component; 2N = two full independent systems | Equipment schedules and the single-line showing where redundancy actually sits |

Two things to internalize. First, a facility cannot self-certify a tier — official Tier status requires Uptime Institute's review, so an asserted "Tier IV" with no certificate and no single-lines is a claim, not a fact; put the certification and the commissioning (Cx) reports in the room or discount the headline. Second, PUE is an operating number, not a brochure number. With the industry average stuck around 1.54 for years, a design-basis PUE of 1.2 means little without metered data proving the facility actually runs there. The room's job is to turn every one of these headline specs into a document a buyer's engineer can verify.

How does the data room actually run a data center acquisition?

It runs it as a permissioned, evidence-first workflow where the power stack is legible, sensitive tenant and customer data is gated and watermarked, and you can see who actually read the interconnection agreement before the call. A data-center deal moves 200-plus sensitive documents — PPAs, LGIAs, confidential hyperscale leases, customer MSAs, commissioning reports — among a buyer, a seller, a construction lender, an infrastructure-fund LP, sometimes a hyperscale tenant, and several sets of counsel. Email and consumer file-sharing cannot gate, watermark, or track that. Here's how a room like Peony maps to the specific risks of this asset class, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when the document set is large and the viewer list keeps growing.

- NDA gate. Tenant identities and PPA pricing are the most confidential items in the deal. A click-through NDA in front of the room — or in front of the specific tenant/customer folder — means a viewer agrees before they see a single megawatt of contracted load, and you have the record that they did.

- Dynamic per-viewer watermarks. The same hyperscale lease abstract opens for the lender, the LP, and the tenant with each viewer's identity burned into the page. If a confidential lease leaks, the watermark says whose copy it was — a real deterrent when you're circulating a named tenant's contract.

- Page-level analytics. You see who viewed what and for how long — did the construction lender actually open the LGIA and the cost-allocation, or just the teaser? That tells you where the real questions are coming before the diligence call, and which party is genuinely engaged. (This is view-and-dwell analytics, not keystroke capture.)

- Redaction. Customer names in a colocation rent roll, pricing in a PPA, or personal data in an estoppel can be redacted at the document level so a lender sees the structure without the confidential specifics.

- AI auto-indexing. Drop a disorganized export — hundreds of files from the seller's engineer, utility, and counsel — and the room indexes it so the power stack, leases, and MEP land in a navigable structure instead of a flat dump. In a deal where the index is the argument ("the megawatts are secured, here's the order"), that's not cosmetic.

- Role-based permission groups. The lender lives in the power and energization folder; the LP sees a curated subset; the hyperscale tenant sees the MEP basis and shell as-builts but not the seller's other-customer data; brokers and counsel sit across the deal. One room, many sightlines.

For a 5,900+-customer flat-rate room, the structural fit is the mid-market-to-institutional single-asset or single-campus deal, the JV, the preferred-equity raise, and the sale-leaseback — where the document set is large and confidential but the deal doesn't warrant a six-figure VDR procurement.

Where you don't need any of this. Be honest about the floor. A single powered-land parcel trading all-cash between two parties with one attorney can run on a handful of emailed PDFs — a data room is overkill. And at the opposite extreme, a $1B-plus hyperscale-portfolio take-private with a full banking syndicate will default to Datasite or Intralinks; that's their lane and I won't pretend otherwise. The data room earns its place in the wide middle: any deal with a lender, an NDA'd tenant, a capital partner, and a document set too large and too sensitive for email — which is most data-center transactions that aren't either a two-party land sale or a mega-cap portfolio.

How do you organize the index, and who gets access at what level?

Organize the index so the power stack is folder one and grant access by role, not by a single shared link — because the fastest way to signal "the megawatts are secured" is to make the energization file the first thing every reviewer sees, and the fastest way to lose control of confidential leases is to hand everyone the same link.

A working top-level index for a data-center deal:

- Power & energization — Will-Serve letter, LGIA/SGIA, interconnection studies, cost-allocation, PPA / behind-the-meter, substation & transformer plan and lead times, energization schedule.

- Land, entitlement & water — zoning/special-use, site plan, entitlement status, water rights and cooling-water supply.

- Lease & tenant credit — hyperscale lease + abstract, or colocation MSAs + rent roll, tenant financials, concentration.

- Physical / MEP — Uptime certification, single-lines, commissioning reports, cooling and redundancy design, capacity vs design load.

- Environmental — Phase I (and II if any), generator fuel storage, air permits.

- Title & survey — commitment, ALTA/NSPS survey, utility/fiber/transmission easements.

- Financial — development model (yield-on-cost, cost-to-complete) or stabilized model (NOI, WALT), and the supporting statements.

- Corporate & closing — entity docs, EPC/FID package (for development), insurance, closing checklist.

Access then maps to who needs which folders:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Buyer / acquirer deal team | All | Full access |

| Construction / project lender | Power & energization, title, environmental, financial | NDA gate; watermark; analytics on the LGIA |

| Infrastructure-fund LP / preferred-equity | Curated subset — model, leases, power summary | Restricted permission group |

| Hyperscale tenant (build-to-suit) | MEP basis, shell as-builts, power schedule | No access to other-customer data; redaction |

| Investment-sales broker / counsel | Cross-deal | Role-based; full or near-full |

This is exactly the kind of segmentation that permission groups plus per-viewer watermarks make routine, and it is where a flat-rate model helps: when the lender adds three analysts and the LP adds counsel, you're not paying per seat to keep the room honest.

The bottom line: which data center data room do you actually need?

The data room underwrites the megawatts — so the right answer depends on deal size and how secured the power is, not on brand prestige. Here's the segmented recommendation from someone who watches these rooms run.

- Solo sponsor / single powered-land parcel (two parties, one attorney, all-cash): You may not need a data room at all. A clean, well-named set of PDFs — Will-Serve letter, entitlement file, title, survey — emailed to one counterparty can be enough. Don't over-tool a two-party land trade. If you want structure without cost, a flat-rate room is still cheaper than most people assume, but it's optional here.

- Mid-market developer, colocation operator, or REIT (single facility or campus, a JV, a preferred-equity raise, or a sale-leaseback): This is the sweet spot for a flat-rate room. You have a lender underwriting the energization timeline, confidential tenant data, a capital partner doing confirmatory diligence, and 200-plus documents that email can't gate or track. A room like Peony — NDA gate, per-viewer watermarks, page-level analytics, redaction, AI auto-indexing, role-based groups, flat $52/admin/month — fits the document volume and the confidentiality without a per-page or per-user meter. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane it's built for.

- $1B+ hyperscale portfolio M&A / take-private: Default to Datasite or Intralinks. A full banking syndicate, a global bidder list, and integrated deal tooling are their procurement reality, and that's the honest recommendation at that altitude.

Whichever tier you're in, the discipline is the same: make the power stack legible, evidence every Tier and PUE claim, abstract hyperscale and colocation leases differently, and gate the confidential tenant data. Build the room around the megawatts and the deal reads correctly to everyone who has to underwrite it.

If you're staging a sell-side or refinancing room and want the broader provider landscape and cost benchmarks first, see our top 10 virtual data room providers comparison and the virtual data room cost guide before you commit.

Sources

- Uptime Institute — Tier Classification System (Tier III concurrently maintainable / N+1; Tier IV fault-tolerant / 2N, ~99.995% uptime; tiers cannot be self-certified); 2025 Global Data Center Survey (industry-average PUE ~1.54, stable for six years; 800+ operators surveyed).

- CBRE / JLL — North America Data Center Trends 2025-2026 (Northern Virginia record-low vacancy ~0.3-0.5%; ~21.5 MW available supply at end-2025; 96% of 2026 scheduled supply committed; powered/entitled land scarcity).

- FERC — Standard Large/Small Generator Interconnection Agreements (LGIA/SGIA) and Order No. 2023 (cluster-study process and cost-allocation reform).

- Lawrence Berkeley National Laboratory (LBNL) "Queued Up" / RMI — U.S. interconnection queue ~2,600 GW (early 2026); median wait ~5 years; ~8-year average to commercial operation in PJM for 2025 energizations.

- EPA / ASTM — All Appropriate Inquiries; ASTM E1527-21 Phase I ESA (sole recognized edition since Feb 13, 2024); E2018 Property Condition Assessment.

- Hines "Powered Land" report; Data Center Frontier; S&P Global — powered land vs powered shell; committed-load (50-200MW) definitions; "duty to serve"; behind-the-meter / on-site generation.

- Deal data: Digital Realty largest-ever single lease — 200MW, Charlotte, NC, for a hyperscaler (April 2026); Digital Realty agreement to acquire a Blackstone stake in three Northern Virginia data centers (288MW, ~$7.8B gross, June 29 2026); Digital Realty $3.25B U.S. Hyperscale Data Center Fund final close (March 2026); Alphabet's ~$4.75B acquisition of Intersect Power for co-located "energy parks" (announced December 2025).

This article is general information for deal teams, not legal, tax, engineering, or investment advice. Interconnection rules, utility tariffs, Uptime criteria, environmental standards, market vacancy, and the specific deals referenced change over time — verify current figures, queue positions, and contract terms with qualified counsel, a power/interconnection consultant, and a licensed MEP engineer before relying on them. Peony is a data room provider, not a broker, utility, or engineering firm.

You might also like

Jun 30, 2026

Commercial Property Due Diligence: How to Run It Against the Clock (2026)

Jul 1, 2026

Cell Tower Data Room: How a Tower Portfolio Sale Closes (2026)

Jul 1, 2026

Industrial Data Room: The One That Survives the Buyer's Engineer (2026)