Multifamily Acquisition Data Room: The Rent Roll Is the Asset (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Multifamily Acquisition Data Room: The Rent Roll Is the Asset (2026)

Last updated: July 2026

Quick answer: A multifamily acquisition data room is the deal room for buying a single apartment asset (or a small 2-9 asset group) — and what makes it different from any other commercial real estate room is that the rent roll IS the asset. The income is almost entirely in-place leases, so the room's whole job is to let a buyer reconcile the rent roll to the actual signed leases — the lease audit — while proving out the T-12/T-3, loss-to-lease, other income/RUBS, physical condition, and agency debt. The catch that defines the asset class: the most important diligence document is also the one stuffed with resident personal data — names, SSNs, DOB, income on leases and applications — so it's a reconciliation-under-redaction problem. Redact the PII, gate the lease files, watermark per viewer, and permission by role, and the buyer verifies the income without a resident's identity ever leaving the room. When the deal has an agency lender, an LP, and hundreds of confidential leases, that room is usually a commercial real estate data room — not email.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't operate apartments for a living — but I've watched a lot of multifamily deals move through data rooms, and they don't behave like an office or industrial trade. In most CRE deals the room is organized title-and-leases-first, and the leases are a manageable handful. In an apartment deal the leases are the income — dozens or hundreds of them — and the single act that decides the deal is whether the rent roll reconciles to those signed leases. Get the room built around that and the deal reads correctly. Build it like a generic CRE room and you bury the reconciliation and, worse, you leak resident data.

That's the thesis of this post: the rent roll is the asset, so the room's job is to let a buyer reconcile the rent roll to the leases without leaking a single resident's PII. This is the tension unique to multifamily — the most important document to share is also the most dangerous to share, because leases and applications carry names, Social Security numbers, dates of birth, and income documentation. The room has to make reconciliation easy and disclosure safe at the same time. Call it reconciliation-under-redaction.

Here's the carve-out, because Peony has a family of real estate guides and this one owns a specific lane. If you're running a 10-plus asset institutional portfolio sale — 80-200GB, 8-15 bidders, blanket estoppels, a portfolio rollup — that's Archetype #2 in data room for real estate, a heavier and different beast; this post is the single-asset or small (2-9 asset) acquisition most buyers actually run. If you're raising LP equity to buy the deal — the PPM, the waterfall, 506(b)/506(c), your track record — that's the capital raise in real estate syndication data room; this is the property transaction and diligence room, not the raise. And if you want the generic CRE process and clock or the line-item document inventory, read commercial property due diligence and the real estate due diligence checklist; this post assumes those and goes multifamily-deep on the rent roll and the leases.

Why does a multifamily acquisition data room revolve around the rent roll instead of the building?

Because in an apartment deal the income is the asset, and the income is the rent roll — a live list of every unit, its resident, the in-place rent, the lease term, concessions, and deposits. A buyer isn't primarily valuing brick and drywall; they're valuing a stream of contractual rents, and every one of those rents is a line on the rent roll that must trace to a signed lease. Reconcile the rent roll to the leases and you've validated the income; fail to, and you're buying a spreadsheet the seller typed.

The market context in 2026 makes the discipline matter more, not less. U.S. apartment investment volume rebounded to roughly $165.5 billion in 2025 — up about 9.4% year over year, the second consecutive year of expansion (MSCI Real Capital Analytics). Sentiment entering 2026 is the least pessimistic on record in the NMHC survey, bid-ask spreads have narrowed, and buyers and sellers are transacting again. All-class cap rates sit near 5.6%, having widened about 9 basis points in 2025, with CBRE expecting them roughly flat through the first half of 2026 before compressing. Meanwhile the construction wave that flooded the Sun Belt is receding into a delivery cliff, which is why sellers of stabilized assets are moving now. More deals, thinner margins for error — which means the rent-roll-to-lease reconciliation is the difference between an underwritable price and a re-trade.

So the room's job is not to prove the building is pretty. It is to prove the rent roll is real — that the in-place rents, terms, concessions, and other income are exactly what the seller says — and to prove it without exposing the residents whose data fills the leases. That is the spine the index has to be built on.

What goes in a multifamily acquisition data room?

The same workstreams as any CRE deal, but re-sequenced so the rent roll and lease audit lead, and graded by the one thing that goes wrong in each. The generic CRE room puts title first; the multifamily room puts the rent roll and its reconciliation first, because that's the gating risk a buyer and an agency lender are actually underwriting. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Rent roll & lease audit | Every rent-roll line tied to a signed lease — in-place rent, term, concessions, deposits, addenda, renewals; occupancy status | The rent roll shows market rent while residents are mid-concession, or renewals/premiums that were never papered — so claimed in-place income isn't real |

| T-12 / T-3 financials & other income | Trailing-12 and trailing-3-annualized statements; the walk from gross potential rent to effective income; RUBS, parking, pet/application/late fees in other income | Overstated or non-recurring other income (a RUBS program that isn't fully implemented) inflates NOI; the T-3 hides a softening the T-12 masks, or vice versa |

| Resident PII & redaction | SSNs, DOB, and income docs on leases and applications are redacted before any outside party sees them; Fair Housing sensitivity | Sharing unredacted leases with a buyer, lender, or vendor — a resident-data leak and a Fair Housing exposure, with no record of who saw what |

| Physical condition / capex / PCA | Unit-walk findings vs the renovated/classic mix on the rent roll; deferred maintenance; the Property Condition Assessment and capital plan | Deferred maintenance the financials don't show, or a rent roll that claims a renovated premium the unit walk contradicts |

| Agency debt & loan assumption | Fannie DUS / Freddie Optigo term sheet, DSCR/LTV underwriting, rate-cap escrow, bad-boy carve-out guaranty; for assumptions, the lender's application, approval, and fees | Starting the loan-assumption process late — the agency's clock, not the buyer's, controls the timeline, and a missing assumption package blows the closing date |

| Title, survey & environmental | Title commitment (Schedule B exceptions), ALTA/NSPS survey, easements; Phase I ESA to ASTM E1527-21 (Phase II only if a REC appears) | Closing on a stale Phase I forfeits the CERCLA innocent-landowner defense; a survey easement isn't reconciled against the title commitment |

| Market rent & loss-to-lease | In-place rent (verified from leases, net of concessions) vs market rent (evidenced by comps); the loss-to-lease gap that is the value-add thesis | Loss-to-lease built on an aggressive market-rent assumption or overstated in-place rent — the upside evaporates in diligence |

A few of these deserve their own paragraph, because the value and the liability live there.

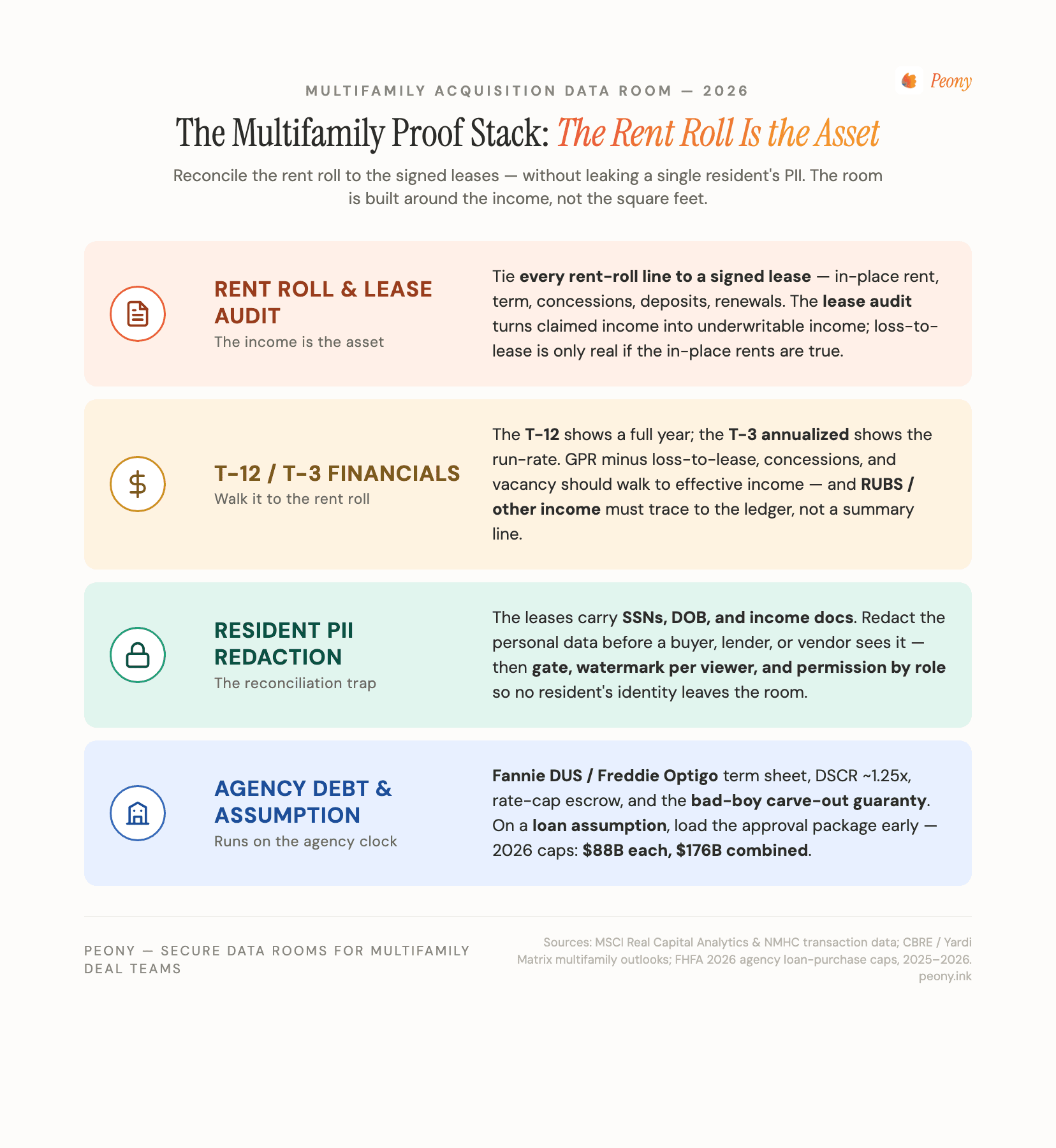

The rent roll and lease audit are the workstream everything else reconciles to. A rent roll is a claim; a lease is the contract that either backs it or doesn't. The room has to keep the two side by side so the diligence team can walk unit by unit — and it has to do that with the resident data redacted, which is the next workstream.

Resident PII is the constraint that makes multifamily different. No other CRE asset class puts personal data — SSNs, dates of birth, income documentation — in its single most important diligence document. The lease and application folder cannot be shared the way you'd share a NNN lease abstract. It has to be redacted at the document level, gated, and watermarked before a lender, an LP, or a third-party vendor sees it. We'll come back to how the room does this.

The environmental and title work has a standard spine. The Phase I ESA runs to ASTM E1527-21 (the only edition the EPA recognizes for All Appropriate Inquiries since February 13, 2024), and the PCA commonly runs to ASTM E2018. Our environmental due diligence guide covers the Phase I/II mechanics; here, just make sure the reports and photo logs are actually in the room and reconciled to the unit walk.

What is a lease audit, and how do you reconcile a rent roll to the leases?

A lease audit — also called a lease file audit — is the process of tying every line on the rent roll back to a signed lease, and it's the single act that turns claimed income into underwritable income. The buyer, or a third-party diligence vendor, pulls a sample (often 100% on a smaller asset, a statistically meaningful sample on a larger one) and checks each unit against its executed lease and ledger.

For each sampled unit, the reconciliation confirms:

- In-place rent — does the rent-roll figure match the lease and the current ledger, or is the unit mid-concession while the roll shows gross market rent?

- Lease dates — start, end, and whether an expired lease has gone month-to-month (often with a premium that may or may not be papered).

- Concessions — free rent, reduced rent, or move-in credits that reduce the effective rent below the stated rent.

- Deposits and fees — security deposits, pet deposits, and any one-time fees, tied to the ledger.

- Addenda and renewals — pet addenda, parking, storage, and renewals that change the economics but live outside the base lease.

The reason this is the heart of the deal: the rent roll and the leases disagree more often than sellers expect. A unit shown at $1,500 is actually collecting $1,300 net of a two-month concession. A "renewed" resident never signed the renewal. A month-to-month premium sits in the ledger but not the lease. Each discrepancy moves the in-place rent, and the in-place rent drives the price. The lease audit is how the buyer replaces the seller's asserted income with a verified number — and it's why the room has to keep the rent roll and the lease files navigable together, one click apart, with the resident PII already redacted.

How do you share a rent roll and lease files without leaking resident PII?

You redact the personal data before anyone outside the deal sees it, then gate, watermark, and permission what remains — that's the whole discipline, and it's the one thing generic CRE advice never addresses for apartments. The tension is structural: the buyer must reconcile rents, terms, and concessions across the lease files, but a buyer, a lender, or a third-party inspector has no business seeing a resident's Social Security number, date of birth, or pay stubs. Both things are true at once, so the room has to serve reconciliation and protect privacy in the same motion.

The workflow that resolves it:

- Redact at the document level. Strip SSNs, DOB, and income documentation off the leases and applications so the reviewer sees the lease structure — rent, term, concessions, addenda — without the identifying specifics. A rent roll can keep unit numbers and rents while masking full resident names where they aren't needed for the reconciliation.

- Gate the lease and application folder. Put an NDA in front of the room, or in front of the specific lease/application folder, so a viewer agrees to confidentiality before they open a single lease — and you have the record that they did.

- Watermark per viewer. Burn each viewer's identity into every page, so a leaked lease names whose copy it was — a real deterrent when you're circulating documents that contain residents' personal data.

- Permission by role. The agency lender sees the leases and the debt file; an LP sees a curated, more heavily redacted subset; the PCA engineer sees the physical file only; the appraiser sees the rent roll and comps. One room, many sightlines.

Handled this way, the lease audit still happens — the buyer reconciles every line — but no resident's identity leaves the room. One honesty note: Peony provides the redaction, the gate, the watermark, and the access controls; it is not a compliance service, and Fair Housing and privacy obligations remain the owner's and their counsel's. The room is the tool that makes safe disclosure practical; it doesn't absolve the disclosure.

What is loss-to-lease, and why does it decide the underwriting?

Loss-to-lease is the gap between the market rent a unit could achieve and the in-place rent the current resident actually pays — and it decides the underwriting because it is the value-add thesis, expressed in one number. If market rent is $1,500 and the in-place average is $1,350, the roughly $150 per unit of loss-to-lease is the upside a buyer expects to capture as leases roll to market on renewal and turnover. Multiply it across the units and the hold, and you have the core of the return.

Which is exactly why the rent-roll-to-lease reconciliation matters so much: loss-to-lease is only real if both sides of the gap are honest.

- In-place rent must be verified — from the signed leases and ledgers, net of concessions. A seller who presents the rent roll at gross market rent while residents are mid-concession understates the loss-to-lease the buyer inherits, or overstates current income; either way the number is fiction until the lease audit trues it up.

- Market rent must be evidenced — by real comps and a credible lease-up assumption, not an optimistic round number. An aggressive market-rent assumption inflates the loss-to-lease and, with it, the entire pro forma.

A couple of adjacent metrics ride alongside it. Economic occupancy (rent actually collected as a share of gross potential) can sit well below physical occupancy (units physically leased) when concessions, bad debt, and loss-to-lease are heavy — so a property that's "95% occupied" may be collecting far less than 95% of potential rent. The room should make all of this legible: the verified in-place rents from the leases, the market rents from comps, and the walk between physical and economic occupancy. Do that and the loss-to-lease survives diligence; leave it asserted and the buyer re-underwrites it to their own conservative number, and the deal stops penciling.

How is a T-12 different from a T-3, and what are the other-income and RUBS traps?

A T-12 is the trailing-twelve-month operating statement; a T-3 is the trailing three months, usually annualized (multiplied by four) to show the most recent run-rate. Buyers read both because they tell different stories, and the room should carry both plus the general ledger that supports them.

- The T-12 captures a full year — seasonality, turnover cycles, and one-time items all wash through it. It's the stable base.

- The T-3 annualized reveals the current trajectory. A T-3 running well above the T-12 can mean genuine momentum (rents climbing, occupancy recovering) — or a burst of non-recurring income that won't repeat. A T-3 below the T-12 can signal a softening the annual number still masks. The buyer underwrites to whichever they can defend.

The reconciliation to the rent roll closes the loop: gross potential rent, minus loss-to-lease, concessions, and vacancy, should walk to the T-12's effective rental income. If it doesn't, something in the rent roll or the statements is off, and that gap is a diligence item.

The soft spot is other income. Below rental income sits a line built from RUBS (ratio utility billing system) recoveries, application and admin fees, pet rent and fees, parking, storage, and late fees. It's easy to overstate here — to book a RUBS program that isn't fully implemented across the property, or to treat one-time fee spikes as recurring. Because other income flows straight to NOI and NOI drives value at the cap rate, an inflated other-income line quietly inflates the price. The fix is documentary: put the general ledger and the RUBS documentation in the room so the buyer can trace other income to its source rather than accepting a summary line. This income-verification discipline is the same one behind our real estate due diligence checklist — here it just runs unit-by-unit and fee-by-fee.

How do you diligence agency debt and a loan assumption?

Most stabilized multifamily is financed with agency debt — Fannie Mae's DUS program or Freddie Mac's Optigo program — so the debt file is a first-class workstream, and it gets materially heavier when the buyer is assuming the seller's existing loan rather than placing new financing.

For new agency debt, the room carries:

- The term sheet and the agency's underwriting requirements — the lender re-underwrites the rent roll and T-12 themselves, so those documents serve the debt as much as the equity.

- DSCR and LTV — debt-service coverage typically underwritten around 1.25x and LTV around 65-75%, though both move with rate and asset.

- Rate-cap escrow — on floating-rate agency debt, the required interest-rate cap and its escrow.

- The bad-boy carve-out guaranty — agency loans are largely non-recourse, but the sponsor signs a guaranty that springs to recourse on "bad-boy" acts (fraud, misapplication of funds, unauthorized transfer). It's in the file because the buyer's principals are signing it.

For a loan assumption, add the existing loan documents, the lender's assumption application and approval, the transfer/assumption fee, and the release of the original guarantor. The critical point: the assumption runs on the agency's clock, not the buyer's. Approval can take weeks to months, so the assumption package belongs in the room early — treating it as a closing-week item is how deals miss their date.

The macro backdrop is favorable in 2026. The FHFA set each Enterprise's multifamily loan-purchase cap at $88 billion — $176 billion combined — roughly 20% above 2025 and the highest since the caps began in 2015, with at least 50% required to be mission-driven affordable housing. Early-2026 production reflects it: Fannie's Q1 multifamily volume hit $17.1 billion (up about 45% year over year) and Freddie's reached about $14 billion (up about 40%). Agency liquidity is deep right now, which makes the debt file — and a clean assumption package — worth getting right. One honesty note: Peony organizes and secures the debt file; it does not underwrite, originate, or approve the loan. That's the lender's job.

How does the data room actually run a multifamily acquisition?

It runs it as a permissioned, redaction-first workflow where the rent roll and leases are navigable together, the resident PII is stripped before anyone outside the deal sees it, and you can see who actually opened the loan-assumption package before the call. A single-asset multifamily deal moves the rent roll, dozens-to-hundreds of leases and applications, the T-12/T-3 and general ledger, the PCA and Phase I, the survey, and the agency-debt file among a buyer, a seller, an agency lender, sometimes an LP or JV partner, and several third-party vendors. Email and consumer file-sharing cannot redact, gate, watermark, or track that. Here's how a room like Peony maps to the specific risks of this asset class, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when the lease count is high and the vendor list keeps growing.

- Redaction. This leads for multifamily, because the leases and applications carry resident SSNs, DOB, and income docs. Redact those at the document level so a lender, LP, or vendor reconciles the lease structure without ever seeing a resident's identity. It's the single feature that makes the rent-roll-to-lease reconciliation safe to run.

- Role-based permission groups. The agency lender lives in the rent roll, financials, leases, and debt-assumption folder; the LP sees a curated, more heavily redacted subset; the PCA engineer sees the physical file only; the appraiser sees the rent roll and comps. One room, many sightlines — so each party sees exactly its scope and nothing more.

- NDA gate. Because the lease files contain personal data, a click-through NDA in front of the room (or the specific lease folder) means a viewer agrees to confidentiality before they open a single lease — and you have the record that they did.

- Dynamic per-viewer watermarks. The same lease file opens for the lender and the LP with each viewer's identity burned into the page. If a lease leaks, the watermark says whose copy it was — a real deterrent when the documents contain residents' personal data.

- Page-level analytics. You see who viewed what and for how long — did the lender actually open the loan-assumption package and the T-12, or just the teaser? That tells you where the real questions are coming from before the diligence call. (This is view-and-dwell analytics, not keystroke capture.)

- AI auto-indexing. Drop a disorganized export — a property-management dump of leases, ledgers, and reports — and the room organizes it so the rent roll, leases, financials, and debt file land in a navigable structure instead of a flat pile of PDFs.

For a 5,900+-customer flat-rate room, the structural fit is the single-asset or small-portfolio acquisition, the value-add buy, the JV or preferred-equity confirmatory diligence, and the sell-side room that stages the trade — where the document set is large and privacy-sensitive but the deal doesn't warrant a six-figure VDR procurement.

Where you don't need any of this. Be honest about the floor. A duplex or a small owner-managed building trading all-cash between two parties with one attorney can run on a handful of emailed PDFs — a data room is overkill. And at the opposite extreme, a 10-plus asset institutional portfolio with a full broker process and 8-15 bidders is the heavier lane described in data room for real estate; the largest of those often default to Datasite or Intralinks, and that's their procurement reality. The room earns its place in the wide middle: any single-asset or small-portfolio deal with an agency lender, resident-PII-laden leases, a capital partner, and a document set too large and too sensitive for email — which is most apartment acquisitions that aren't a two-party small-building trade.

How do you organize the index, and who gets access at what level?

Organize the index so the rent roll and lease audit are folder one and grant access by role, not by a single shared link — because the fastest way to move the deal is to make the reconciliation the first thing every reviewer can do, and the fastest way to cause a resident-data problem is to hand everyone the same unredacted link.

A working top-level index for a single-asset multifamily deal:

- Rent roll & leases — current rent roll, the full lease files (redacted), applications, renewals, addenda, deposit ledger, delinquency report.

- Financials — T-12 and T-3 operating statements, general ledger, other-income and RUBS detail, budget, real-estate-tax and insurance bills.

- Market & rents — rent comps, sales comps, market survey, the loss-to-lease and market-rent analysis.

- Physical condition — unit-walk findings and photo log, PCA/capital plan, deferred-maintenance list, service contracts, warranties.

- Environmental & title — Phase I ESA (and II if any), ALTA/NSPS survey, title commitment and Schedule B exceptions, zoning.

- Estoppels — blanket residential estoppel/rep schedule; any commercial-unit or ground-lease estoppels if mixed-use.

- Debt — agency term sheet (DUS/Optigo), loan documents and assumption package, rate-cap escrow, bad-boy carve-out guaranty, payoff or assumption approval.

- Corporate & closing — entity docs, PSA, title/escrow, insurance, closing checklist.

Access then maps to who needs which folders:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Buyer / acquirer deal team | All (redacted) | Full access |

| Agency lender / debt counsel | Rent roll, financials, leases, physical, debt & assumption | NDA gate; watermark; analytics on the assumption file |

| LP / preferred-equity / JV partner | Curated subset — model, rent roll summary, market, reports | Restricted group; deeper PII redaction |

| Third-party vendors (PCA / Phase I / appraiser / lease-audit) | Their scope only | Scoped permission group; redaction |

| Investment-sales broker / counsel | Cross-deal | Role-based; full or near-full |

This is exactly the segmentation that permission groups plus per-viewer watermarks and document-level redaction make routine — and it's where a flat-rate model helps: when the lender adds analysts and the LP adds counsel, you're not paying per seat to keep the room honest and the residents protected.

The bottom line: which multifamily acquisition data room do you actually need?

The rent roll is the asset — so the right answer depends on deal size and how much confidential lease data is moving, not on brand prestige. Here's the segmented recommendation from someone who watches these rooms run.

- Duplex or small owner-managed building (two parties, one attorney, all-cash): You may not need a data room at all. A clean, well-named set of redacted PDFs — rent roll, a few leases, the T-12, title — emailed to one counterparty can be enough. Don't over-tool a two-party small-building trade.

- Single-asset or small-portfolio (2-9 asset) acquisition — value-add buyer, operator, or the sell-side broker staging it: This is the sweet spot for a flat-rate room. You have an agency lender underwriting or a loan to assume, dozens-to-hundreds of resident-PII-laden leases to reconcile against the rent roll, a PCA and Phase I, and often an LP or JV partner doing confirmatory diligence. A room like Peony — redaction, role-based groups, NDA gate, per-viewer watermarks, page-level analytics, AI auto-indexing, flat $52/admin/month — fits the document volume and the privacy problem without a per-page or per-user meter. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane it's built for.

- 10+ asset institutional portfolio sale (full broker process, 8-15 bidders, 80-200GB): This is the heavier lane in data room for real estate Archetype #2, and the largest of these often default to Datasite or Intralinks. That's the honest recommendation at that altitude.

Whichever tier you're in, the discipline is the same: make the rent roll reconcile to the leases, redact the resident PII before it ever leaves the room, walk the T-12/T-3 and other income to the rent roll, get the agency-assumption package in early, and permission every viewer by role. Build the room around the rent roll and the deal reads correctly to everyone who has to underwrite it — without a single resident's data walking out the door.

If you're staging a sell-side or refinancing room and want the broader provider landscape and cost benchmarks first, see our top 10 virtual data room providers comparison and the virtual data room cost guide before you commit.

Sources

- MSCI Real Capital Analytics — U.S. apartment investment volume ~$165.5B in 2025, +9.4% YoY, second consecutive year of expansion; above the ~$155.0B 15-year average.

- NMHC — January 2026 Quarterly Survey of Apartment Market Conditions (record-low pessimism; sentiment improving) and NMHC 50 (majority of respondents expecting more 2026 acquisitions).

- CBRE — U.S. Real Estate Market Outlook 2026 and Q1 2026 Multifamily Figures (all-class cap rates ~5.6%; +9 bps in 2025; roughly flat H1 2026 then compressing).

- Yardi Matrix / RealPage — 2026 supply and completions outlook and rent-growth forecast (record Q1 2025 absorption ~138,000 units; deliveries receding from the peak; muted near-term rent growth).

- FHFA — 2026 Multifamily Loan Purchase Caps for Fannie Mae and Freddie Mac ($88B each / $176B combined; ~20% above 2025; highest since 2015; ≥50% mission-driven).

- Fannie Mae (DUS) / Freddie Mac (Optigo) — Q1 2026 multifamily production (Fannie ~$17.1B, +45% YoY; Freddie ~$14B, +40% YoY); Optigo Lease-Up loan product.

- EPA / ASTM — All Appropriate Inquiries; ASTM E1527-21 Phase I ESA (sole recognized edition since Feb 13, 2024); ASTM E2018 Property Condition Assessment.

This article is general information for deal teams, not legal, tax, environmental, or investment advice. Fair Housing and privacy obligations, agency underwriting rules, ASTM standards, market cap rates, and the figures referenced change over time — verify current numbers and requirements with qualified counsel, a licensed appraiser, an environmental/engineering consultant, and your agency lender before relying on them. Peony is a data room provider, not a broker, appraiser, lender, or property manager; it does not underwrite loans, certify Fair Housing or privacy compliance, or value real estate.

You might also like

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Jun 30, 2026

Commercial Property Due Diligence: How to Run It Against the Clock (2026)

Jul 3, 2026

Medical Office Building Data Room: How the Room Proves Compliance and Credit (2026)