Medical Office Building Data Room: How the Room Proves Compliance and Credit (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Medical Office Building Data Room: How the Room Proves Compliance and Credit (2026)

Last updated: July 2026

Quick answer: A medical office building (MOB) data room is a deal room for buying, selling, financing, or sale-leasing-back a medical office asset — and the thing that makes it different from any other office room is that it is organized around regulatory compliance and tenant credit, not square feet. An MOB trades on two things a regular office never does: whether the rent is Stark/FMV-compliant (a lease with a referral-source physician must be at fair market value, commercially reasonable, in writing, and at least a one-year term), and whether a creditworthy tenant — ideally an investment-grade health system — stands behind the lease. So the document set leads with the FMV rent opinion, the lease comps, the signed leases, and the tenant-credit / guaranty file, then the ground lease (if on-campus), the clinical build-out, and the usual title/survey/environmental. In 2026 the sector is repricing: average MOB cap rates fell to about 6.9% in Q1 (the first sub-7% reading since Q3 2024) as investment volume jumped roughly 78% year-over-year. When the deal involves a lender, healthcare counsel, and hundreds of confidential documents, that room is usually a commercial real estate data room — not email. Peony organizes and controls the evidence; it does not perform the appraisal or certify Stark/AKS compliance.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't practice healthcare law or appraise buildings for a living — but I've watched hundreds of CRE deals move through data rooms, and the medical-office ones do not behave like the others. In a plain office deal, the room is organized leases-first by square footage: the income is the asset, full stop. In an MOB deal, the income is downstream of two more basic questions — is the rent legally defensible, and is the tenant good for it? Reorganize the room around those two questions and the whole deal reads correctly. Leave it organized like a generic office room and you bury the two files the lender and counsel actually came for.

That is the thesis of this post: the room proves compliance and credit, not square feet. A medical office building's value and risk are regulatory and credit-driven in a way an ordinary office's are not. A building leased at an above-market rent with no supporting FMV opinion is a liability dressed up as income; a building leased to a three-physician practice is a different asset than the same building leased to an investment-grade health system, even at the same rent per foot. The document set has to make both of those things legible before it talks about parking ratios.

Here's the carve-out, because Peony has a family of CRE and healthcare guides and this one owns a specific lane. If you want the generic CRE process and clock — caveat emptor, the contingency period, re-trades — read commercial property due diligence; this post assumes you know that and goes Stark/FMV-and-credit-deep. If you want the line-item document inventory for ordinary real estate, that's the real estate due diligence checklist. If you want provider and archetype selection for real estate broadly, that's data room for real estate — it lists MOB only inside its single-asset Archetype #1, whereas this post goes MOB-deep. And crucially, distinguish this from the healthcare-operations siblings: a senior housing data room and a skilled nursing facility data room are operator/license transactions — you buy an operating business with an operating license, census, and payor risk on the P&L. An MOB is a real-estate lease-and-compliance deal — you buy the building and the leases, and the regulatory risk lives in the lease, not a license. Medical office is the regulatory-and-credit-constrained member of that family.

Why does a medical office data room prove compliance and credit instead of square feet?

Because for an MOB, the rent and the tenant are the two things that can quietly destroy value, and neither is visible in a floor plan. Ordinary office diligence asks whether the building is sound and whether the leases cover the debt. Medical office diligence asks two harder questions first: is the in-place rent legally defensible under the physician self-referral and anti-kickback rules, and is the tenant actually good for the rent over the lease term. Get those right and the rest is ordinary real estate; get either wrong and the income you underwrote may not be the income you own.

The sector's fundamentals in 2026 are strong, which raises the stakes on getting the paper right rather than lowering them. Medical-outpatient occupancy reached a record high near 92.7% at the end of 2025, average asking rents hit a record of roughly $25.40 per square foot, and rent growth held around 3.3% year-over-year. Capital has followed: average MOB cap rates compressed to about 6.9% in Q1 2026 — the first time below 7.0% since Q3 2024 — with a broad range of roughly 5.5% to 8.5% depending on asset quality, tenancy, and location, and investment volume rose about 78% year-over-year to $2.9 billion in the quarter (a trailing-four-quarter total near $13.9 billion). The average MOB sale price of about $310 per square foot ran roughly 55% above traditional office. Demographics and the shift of care to outpatient settings underpin all of it.

But that demand only translates into value if the income is bankable, and for an MOB "bankable" has a regulatory meaning. The rent under a lease with a referral-source physician is only durable if it is at fair market value and commercially reasonable — otherwise it is exposed to being reset or challenged. And the durability of the income depends on who signs: an investment-grade health-system guaranty prices very differently from an independent practice's covenant. So the data room's job is not to prove the building is pretty. It is to prove the rent is compliant and the credit is real. That is the spine the index has to be built on.

One boundary, stated early because it is the trust anchor of this whole post: a data room like Peony secures, permissions, watermarks, logs, and organizes the FMV evidence and the compliance file. It does not perform an FMV appraisal, and it does not certify Stark/AKS compliance. Those conclusions belong to a qualified healthcare-real-estate valuation firm and to healthcare regulatory counsel. The room makes their work reviewable; it does not replace it.

What goes in a medical office building acquisition data room?

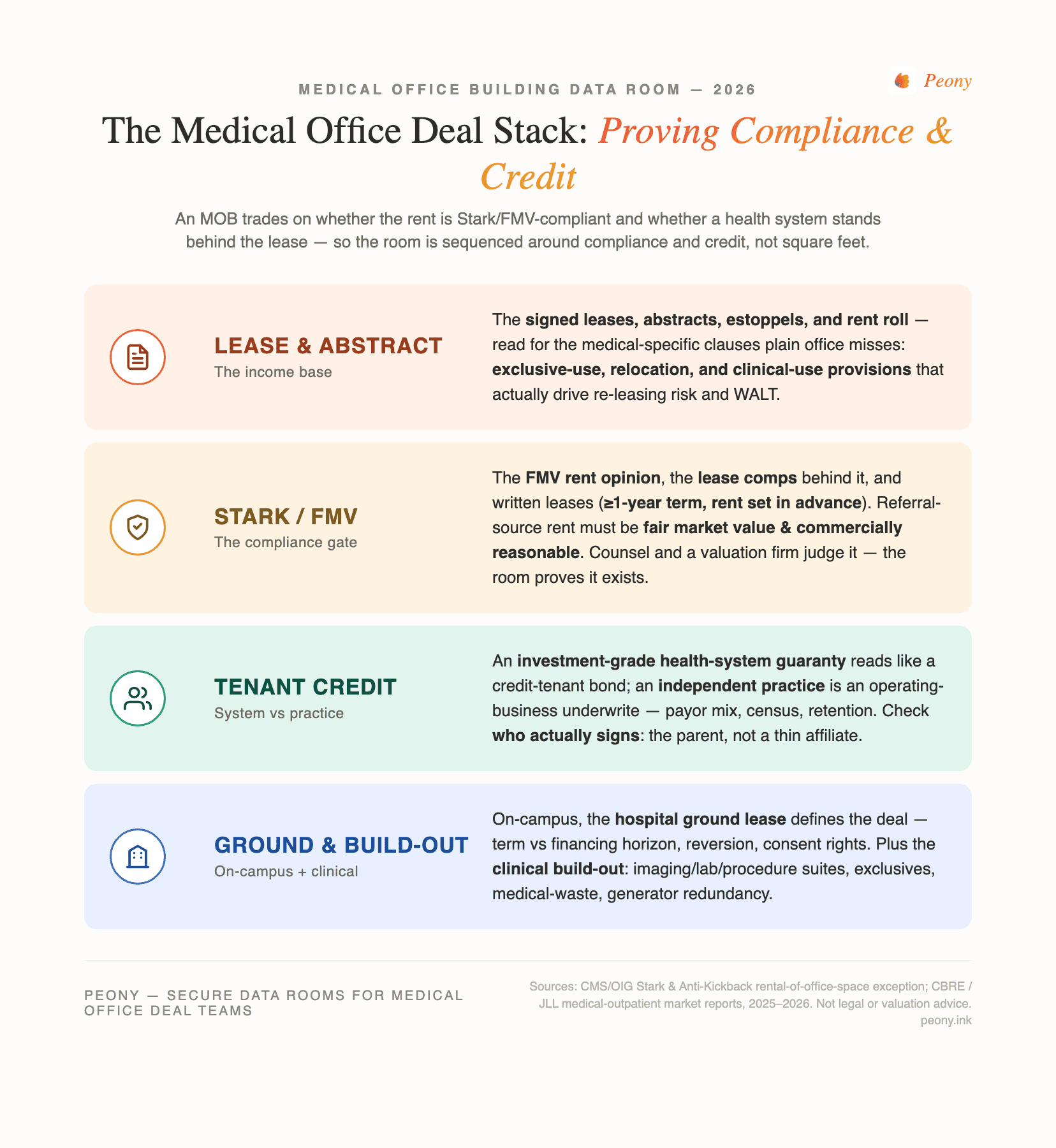

The same core workstreams as any CRE deal, but re-sequenced so the compliance and credit files lead and graded by the one thing that goes wrong in each. The generic office room puts leases and square footage first; the MOB room puts the FMV/Stark file and tenant credit first, because those are the gating risks a lender and counsel are actually underwriting. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Lease & abstract | Signed leases, lease abstracts (term, rent, escalations, options, exclusives), estoppels, SNDAs, rent roll | Abstracting a medical lease like plain office — missing the exclusive-use, relocation, and clinical-use provisions that actually drive re-leasing risk |

| Stark/AKS FMV documentation | FMV rent opinion / appraisal, the lease comps behind it, written and signed leases with ≥1-year terms, commercial-reasonableness memo, rent-set-in-advance evidence | Above-market rent with no current FMV opinion — the income isn't defensible, and a stale opinion triggers a re-trade or a compliance question |

| Tenant / health-system credit | Health-system guaranty vs individual-practice covenant, investment-grade rating or financials, payor mix, patient volume/census, physician retention | Pricing an independent-practice lease as if a health system stood behind it — the guaranty either doesn't exist or names a thin affiliate, not the parent system |

| Ground lease (on-campus) | Hospital ground-lease term vs building-lease term, reversion, consent/assignment and use restrictions, rent resets, remaining term vs financing horizon | The ground lease is shorter than the financing horizon (or the building leases), or the hospital's consent right blocks the sale/assignment |

| TI / clinical build-out & exclusivity | Imaging/lab/procedure-suite improvements, TI allowances and who funded them, exclusive-use clauses, medical-gas and shielding, generator/redundancy for clinical space | Treating specialized build-out as generic office TI — under-reserving for re-tenanting clinical space, or missing an exclusive that limits future leasing |

| Title, survey, environmental (medical waste) | Title commitment (Schedule B), ALTA/NSPS survey, easements, Phase I to ASTM E1527-21, plus medical-waste handling, generator-fuel storage, and ADA compliance | Medical-waste and generator-fuel items get overlooked; closing on a stale Phase I forfeits the CERCLA innocent-landowner defense |

| Rent roll / WALT | Consolidated rent roll, weighted-average lease term (WALT), rollover schedule, concentration by tenant/specialty, expense recoveries | Short WALT with concentrated rollover in specialty space that is expensive and slow to re-let — the income cliff isn't visible in the average |

A few of these deserve their own paragraph because the standards and the liability live there.

The FMV/Stark file is the workstream with the least room for improvisation. You can renegotiate an escalation; you cannot retroactively make an above-market rent defensible. So the room must make the compliance story legible at a glance: the FMV rent opinion on top, the lease comps and appraisal beneath it, the signed leases with their at-least-one-year terms, and the commercial-reasonableness memo. Counsel and the lender read these in order, and if the order is scrambled, the deal slows. We'll come back to exactly what Stark requires.

Tenant credit is where "medical office" stops being one thing. A building leased to an investment-grade health system is a near-net-lease bond; a building leased to independent practices is a small operating-business underwrite. The room should separate the two, store the guaranty next to the lease, and show the credit that stands behind each covenant.

Environmental has a medical-office wrinkle. Beyond the standard Phase I to ASTM E1527-21 (the edition the EPA recognizes for All Appropriate Inquiries), MOBs carry medical-waste handling, generator-fuel storage, and clinical-systems considerations that plain office assets don't. Our environmental due diligence guide covers the Phase I/II mechanics; here, just make sure the medical-waste and generator file is actually in the room.

What does Stark Law actually require for a medical office lease — and where does Peony stop?

Stark Law (the physician self-referral law) and the Anti-Kickback Statute (AKS) sit underneath every MOB whose tenants include referral-source physicians, and they are the reason an MOB's rent cannot be whatever two parties agree to. Here is the accurate, general framing — and then the hard boundary on what a data room does and does not do.

The mechanism is an exception. A lease between a designated-health-services entity (say, a hospital) and a physician who can refer to it has to fit within a rental exception to be safe. The rental-of-office-space exception generally requires that the arrangement:

- Be in writing and signed by the parties.

- Have a term of at least one year (short-term or month-to-month arrangements with referral sources are a classic trap).

- Cover space that is reasonably necessary for the tenant's legitimate business — no paying for space that isn't used.

- Set the rent in advance, at fair market value.

- Be commercially reasonable even if no referrals ever passed between the parties.

- Not take into account the volume or value of referrals or other business generated between the parties.

That last requirement is the whole game. It means the rent has to be independently supportable as FMV, arrived at without regard to the referral relationship — which is why the FMV rent opinion is the document the entire compliance file hangs on. AKS overlaps but is broader and intent-based: an arrangement can satisfy a Stark exception and still raise AKS exposure if it is structured to induce referrals. Both are the province of counsel.

Now the boundary, because this is the trust anchor of the post. Peony secures, permissions, watermarks, logs, and organizes all of this evidence — the FMV opinions, the appraisals, the lease comps, the signed leases, the commercial-reasonableness memos. It does not perform the FMV appraisal, and it does not certify that any lease or arrangement complies with Stark or AKS. Those determinations require a qualified healthcare-real-estate valuation firm (for the FMV opinion) and healthcare regulatory counsel (for the compliance conclusion). If a vendor tells you its software "ensures Stark compliance," be skeptical: a data room can prove the evidence exists, keep it current, and control who sees it — it cannot reach the legal conclusion. The room makes counsel's job faster and cleaner; it does not do counsel's job.

What is an FMV rent opinion, and how do you run the FMV file?

An FMV rent opinion is an independent, written valuation — normally from a qualified healthcare-real-estate appraiser — concluding that a lease's rent reflects the open-market value of the space, determined without regard to referrals between the parties. It is the piece of evidence that turns "the rent is $30 a foot" into "the rent is defensible at $30 a foot," and running the FMV file well is how the room proves the income is bankable.

Run it in this order, top of the index downward:

- The FMV rent opinion(s). The threshold document. Confirm it covers the relevant leases (not just the anchor), read the effective date, and check that it is current — a stale opinion is one of the most common re-trade triggers in the asset class.

- The lease comps and methodology behind it. An FMV conclusion is only as good as its comparables. The room should carry the comp set and the appraiser's methodology so a lender's own valuation team can retrace the logic.

- The signed leases and abstracts. Verify each referral-source lease is written, signed, and carries a term of at least one year, with the rent set in advance. The abstract should surface the escalators, options, exclusives, and any relocation or clinical-use clauses.

- The commercial-reasonableness memo. Evidence that the arrangement makes business sense on its own terms — that the space is reasonably necessary and the deal would be entered into even absent referrals.

- The full appraisal / valuation and any prior opinions. The complete valuation file, plus a history if the rent has been re-opined over time, so the trend is legible.

The non-negotiable rule: every dollar of in-place rent from a referral-source tenant should trace to a current FMV opinion in the room. If the pro forma leans on a rent the FMV file doesn't support, that gap is the deal — a lender won't fund confidently and counsel will flag it. And to say it once more: Peony holds, controls, and versions this file; the appraiser writes the opinion and counsel judges the compliance.

How is health-system credit different from independent-practice credit?

It is the difference between underwriting a bond and underwriting a business — and it is the second axis (alongside FMV) on which an MOB is priced. A building leased to, or guaranteed by, an investment-grade health system behaves like a net-lease credit-tenant asset: much of the value is the credit and duration of that system's promise, and buyers underwrite the guaranty and the system's rating the way they'd underwrite a corporate covenant. A building leased to an independent physician group is a small operating-business underwrite: you are betting on the practice's ability to pay across the lease term.

For a health-system-anchored lease, the file has to capture:

- Who actually signs or guarantees — the parent system versus a thin affiliate or a single hospital entity. A guaranty from a subsidiary is not a guaranty from the system.

- The system's credit — investment-grade rating or audited financials, because a long lease is only as good as the entity behind it.

- Term and options — remaining term, renewals, and any early-termination or contraction rights that puncture the "bond" thesis.

- On-campus dynamics — if the system is also the ground lessor, its consent, use, and reversion rights matter as much as the rent.

For an independent practice, you're underwriting a business, not a bond: the practice's financials, its payor mix (commercial versus Medicare/Medicaid exposure), patient volume and census, physician retention and succession, and the probability it renews rather than relocating. It behaves far more like multi-tenant office or a small operating tenant — closer to the income-verification work in our real estate due diligence checklist — than like a single-tenant net lease.

Two practical room notes. First, physician-level financials and payor data are confidential — they belong behind an NDA gate with per-viewer watermarks, not in an open folder, and often need redaction. Second, abstract the two tenant types in separate folders with separate templates; a reviewer who opens the tenant file should immediately know whether they're reading a health-system bond or a practice's business.

Why does the on-campus ground lease change the whole underwrite?

Because on an on-campus MOB, you often don't own the dirt — the hospital does, and it ground-leases the land to the building owner — so the ground lease, not the fee, defines what you actually have. An on-campus asset sits on a hospital's campus with the system or its affiliated physicians as anchor tenants; an off-campus asset stands independently in the community. That single fact reshapes the diligence.

For an on-campus deal, the room has to answer:

- Ground-lease term versus building-lease and financing horizons. If the ground lease has 22 years left and you're placing 15-year financing against 20-year building leases, the mismatch is the risk. A ground lease shorter than the leases it sits under is a red flag.

- Reversion and improvements. What happens to the building at ground-lease expiry — does it revert to the hospital? That governs residual value.

- Consent and assignment rights. Health systems commonly hold consent rights over a sale or assignment; a deal can be fully negotiated and still need the hospital's sign-off.

- Use restrictions and exclusivity. The system may restrict tenant mix or competing uses, which constrains re-leasing.

For an off-campus deal, the underwrite is more ordinary real estate, but it leans harder on independent-practice credit and re-leasing risk, since there's no captive hospital campus driving demand. The room should establish, in folder one, which kind of asset this is — because a reviewer who assumes fee-simple ownership on an on-campus ground-leased building is reading the wrong deal.

How does the data room actually run a medical office acquisition?

It runs it as a permissioned, evidence-first workflow where the FMV/compliance file leads, sensitive physician and payor data is gated and watermarked, and you can see who actually read the FMV opinion and the guaranty before the call. An MOB deal moves 150-plus sensitive documents — FMV opinions, signed leases, health-system guaranties, physician-practice financials, payor data, the ground lease, clinical build-out drawings — among a buyer, a seller, a lender, healthcare counsel, and a broker. Email and consumer file-sharing cannot gate, watermark, or track that. Here's how a room like Peony maps to the specific risks of this asset class, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when the document set is large and the viewer list keeps growing.

Lead with the two things this asset class turns on — the FMV evidence and the gated compliance file — and note the boundary as we go:

- AI auto-indexing. Drop a disorganized export — leases, appraisals, comps, financials from the seller, its appraiser, and counsel — and the room indexes it so the FMV/Stark file, tenant credit, and the ground lease land in a navigable structure instead of a flat dump. In a deal where the index is the argument ("the rent is compliant, here's the proof"), that's not cosmetic. (Peony organizes the evidence; it does not judge whether the evidence satisfies Stark.)

- NDA gate. Physician-practice financials, payor data, and health-system lease terms are the most confidential items in the deal. A click-through NDA in front of the room — or the specific compliance/financials folder — means a viewer agrees before they see a single lease, and you have the record that they did.

- Dynamic per-viewer watermarks. The same FMV opinion or health-system guaranty opens for the lender and for counsel with each viewer's identity burned into the page. If a confidential appraisal leaks, the watermark says whose copy it was.

- Page-level analytics. You see who viewed what and for how long — did the lender actually open the FMV opinion and the guaranty, or just the rent roll? That tells you where the real questions are before the diligence call. (This is view-and-dwell analytics, not keystroke capture.)

- Redaction. Physician names and compensation in a practice's financials, or personal data in an estoppel, can be redacted at the document level so a lender sees the structure without the confidential specifics.

- Role-based permission groups. The lender lives in the FMV/compliance, credit, and financial folders; counsel lives in the Stark/AKS lease folder; the broker sits across the deal; physician-level data stays in a restricted group. One room, many sightlines.

For a 5,900+-customer flat-rate room, the structural fit is the single-MOB or small-portfolio acquisition, the sale-leaseback, and the financing — where the document set is large and confidential but the deal doesn't warrant a six-figure VDR procurement.

Where you don't need any of this. Be honest about the floor. A single small MOB trading all-cash between two parties with one attorney can run on a handful of emailed PDFs — a data room is overkill. And at the opposite extreme, a multi-billion-dollar health-system portfolio monetization — the kind of entity-level disposition that runs a full broker/institutional process — will default to Datasite or Intralinks; that's their lane and I won't pretend otherwise. (The 2025-26 Welltower disposition of roughly 18 million square feet of outpatient medical to Remedy Medical Properties and Kayne Anderson for about $7.2 billion, in tranches, is exactly that altitude.) The data room earns its place in the wide middle: any single-asset or small-portfolio deal with a lender, healthcare counsel, confidential physician data, and a document set too large for email.

How do you organize the index, and who gets access at what level?

Organize the index so the FMV/compliance file and tenant credit are folders one and two, and grant access by role, not by a single shared link — because the fastest way to signal "the rent is compliant and the credit is real" is to make that evidence the first thing every reviewer sees, and the fastest way to lose control of confidential physician data is to hand everyone the same link.

A working top-level index for an MOB deal:

- Stark/AKS FMV documentation — FMV rent opinion(s), lease comps and methodology, signed leases (written, ≥1-year), commercial-reasonableness memo, full appraisal.

- Tenant / health-system credit — guaranty, system rating/financials, or independent-practice financials, payor mix, census, retention.

- Lease & abstract / rent roll — abstracts, estoppels, SNDAs, consolidated rent roll, WALT, rollover schedule.

- Ground lease (on-campus) — ground lease, term/reversion, consent and use restrictions, subordination.

- TI / clinical build-out — imaging/lab/procedure-suite improvements, TI history, exclusives, medical-gas/shielding, generator/redundancy.

- Title & survey — commitment, ALTA/NSPS survey, easements.

- Environmental — Phase I (and II if any), medical-waste handling, generator-fuel storage, ADA.

- Financial & closing — operating statements, model, entity docs, insurance, closing checklist.

Access then maps to who needs which folders:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Buyer / acquirer deal team | All | Full access |

| Lender | FMV/compliance, credit, rent roll, title, environmental | NDA gate; watermark; analytics on the FMV opinion |

| Healthcare regulatory counsel | Stark/AKS FMV, leases, ground lease | Role-based; full on the compliance file |

| Seller's broker | Cross-deal | Role-based; full or near-full |

| Physician-level financials / payor data | Restricted subset only | Restricted permission group; redaction |

This is exactly the kind of segmentation that permission groups plus per-viewer watermarks make routine, and it is where a flat-rate model helps: when the lender adds three analysts and counsel adds an associate, you're not paying per seat to keep the room honest.

The bottom line: which medical office data room do you actually need?

The room proves compliance and credit — so the right answer depends on deal size and how clean the FMV and tenant story is, not on brand prestige. Here's the segmented recommendation from someone who watches these rooms run.

- Owner selling a single small MOB (two parties, one attorney, all-cash, clean FMV): You may not need a data room at all. A well-named set of PDFs — the FMV opinion, the leases, title, survey, environmental — emailed to one counterparty can be enough. Don't over-tool a two-party trade. A flat-rate room is still cheaper than most assume if you want structure, but it's optional here.

- Physician group, developer, or specialist owner (single MOB or small portfolio, a sale-leaseback, or a financing): This is the sweet spot for a flat-rate room. You have a lender underwriting the FMV and credit, healthcare counsel reviewing Stark/AKS, confidential physician financials, and 150-plus documents that email can't gate or track. A room like Peony — AI auto-indexing, NDA gate, per-viewer watermarks, page-level analytics, redaction, role-based groups, flat $52/admin/month — fits the document volume and confidentiality without a per-page or per-user meter. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane it's built for.

- Multi-billion-dollar health-system portfolio monetization: Default to Datasite or Intralinks. A full broker/institutional process, an entity-level disposition, and integrated deal tooling are their procurement reality, and that's the honest recommendation at that altitude.

Whichever tier you're in, the discipline is the same: make the FMV/compliance file legible, evidence every referral-source rent with a current FMV opinion, separate health-system credit from independent-practice credit, and gate the confidential physician data. Build the room around compliance and credit and the deal reads correctly to everyone who has to underwrite it. And remember the boundary: the room proves the evidence exists and controls who sees it — the valuation firm and healthcare counsel reach the conclusions.

If you're staging a sell-side or refinancing room and want the broader provider landscape and cost benchmarks first, see our top 10 virtual data room providers comparison and the virtual data room cost guide before you commit.

Sources

- CBRE — Q1 2026 U.S. Medical Outpatient Buildings Figures (average MOB cap rate ~6.9%, first sub-7% since Q3 2024; investment volume +78% YoY to ~$2.9B, trailing-four-quarter ~$13.9B; record occupancy ~92.7% at end-2025; record asking rent ~$25.40/sf; average sale price ~$310/sf vs ~$200/sf traditional office).

- JLL / Cushman & Wakefield — 2026 Medical Outpatient Building perspective and capital-markets outlook (cap-rate range ~5.5-8.5%; rent growth ~3.3% YoY; outpatient demand and demographic tailwinds).

- CMS / OIG — Physician Self-Referral Law (Stark) rental-of-office-space exception and Anti-Kickback Statute framing: leases must be in writing and signed, at least a one-year term, cover reasonably necessary space, set rent in advance at fair market value, be commercially reasonable, and not vary with the volume or value of referrals.

- Healthcare-real-estate legal commentary (CBIZ; Breazeale, Sachse & Wilson; ArentFox Schiff) — FMV and commercial-reasonableness requirements for MOB leases with referral-source physicians; recent Stark FMV-exception clarifications.

- EPA / ASTM — All Appropriate Inquiries; ASTM E1527-21 Phase I Environmental Site Assessment.

- Deal data: Welltower's disposition of ~18M sf of outpatient medical (296 properties, 34 states, ~94% leased) to Remedy Medical Properties and Kayne Anderson Real Estate for ~$7.2B, announced October 2025 and closing in tranches through mid-2026 (first ~$2B tranche closed October 2025); Remedy/Kayne Anderson thereby became the largest U.S. outpatient-medical owner. Verify current figures before relying on them.

This article is general information for deal teams, not legal, tax, valuation, or investment advice. Stark Law and Anti-Kickback rules, FMV standards, environmental standards, cap rates, market data, and the specific deals referenced change over time — verify current requirements, valuations, and contract terms with healthcare regulatory counsel and a qualified healthcare-real-estate valuation firm before relying on them. Peony is a data room provider, not an appraiser, valuation firm, or law firm; it secures and organizes the FMV and compliance evidence but does not perform appraisals or certify Stark/AKS compliance.

You might also like

Jul 1, 2026

Skilled Nursing Facility Data Room: The CHOW Is the Deal (2026)

Jul 3, 2026

Multifamily Acquisition Data Room: The Rent Roll Is the Asset (2026)

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)