Skilled Nursing Facility Data Room: The CHOW Is the Deal (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Skilled Nursing Facility Data Room: The CHOW Is the Deal (2026)

Last updated: July 2026

Quick answer: A skilled nursing facility data room is the secure, access-controlled environment an operator, REIT, broker, or lender uses to run a nursing-home acquisition, sale, or HUD financing — and it matters because in this asset class you are not buying a building, you are buying a change of ownership (CHOW). A skilled-nursing deal means stepping into a Medicare provider agreement, a Medicaid rate, a multi-year survey history, and successor liability for the operation that ran there. So the room has to prove two things the day control flips: that the operation is clean (F-tags, Five-Star, payor mix, cost reports) and that the change of ownership is survivable (CMS-855A, the certificate of need, the provider-agreement assignment decision, the resident trust funds, the operations transfer agreement). The dirt is commoditized; the license and its liabilities are the deal. For the seller-side or financing room where that document tape moves between operators, landlords, lenders, and counsel, a commercial real estate data room is where the discipline lives.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't operate nursing homes — but I've watched hundreds of healthcare-real-estate deals move through data rooms, and skilled nursing is the asset class where one truth is sharpest: the CHOW is the deal, and the dirt is the footnote. A buyer barely underwrites the brick. What it underwrites is the operation — the provider agreement it will inherit or reject, the survey history that predicts enforcement risk, the payor mix that sets the margin, and the successor liability that can follow the Medicare ID into the new owner's hands. Get that operating-license file organized and provable, and the change of ownership closes cleanly; leave it scattered, and the deal re-trades or dies the day a buyer's counsel reads the Form 2567 history.

This post is the SNF-specific playbook for that. It is not the independent-living / assisted-living / memory-care continuum — that private-pay, occupancy-and-operator-driven housing market is the senior-housing hub, our senior housing data room guide, and skilled nursing is its clinical, government-reimbursed sibling spoke (if you're not sure which you're in, the line is simple: if Medicare and Medicaid pay the bills and a state surveyor writes F-tags, you're in skilled nursing — this post). It is not advisor selection: who should bank your sale is our best healthcare M&A advisors guide; this is the room that runs the deal once you've picked one. And it is not the generic CRE diligence spine — for Phase I, ALTA survey, and PCA, our commercial property due diligence and real estate due diligence checklist guides cover the dirt. This is the skilled-nursing asset class specifically, and it sits in the same CRE-by-asset-class family as our data center data room, cell tower data room, and industrial data room guides — adjacent assets with their own document tapes.

Why is a skilled nursing deal "the license transfer, not the real estate"?

Because the value and the danger both live in the operation, not the structure. A skilled nursing facility is, physically, a building you could underwrite like any other healthcare property — square footage, age, capex, a roof. But almost nobody buys an SNF for the brick. They buy the right to operate a Medicare- and Medicaid-certified nursing facility on that site, and that right is a bundle of federal and state regulatory instruments, each with its own transfer mechanics and its own liability tail.

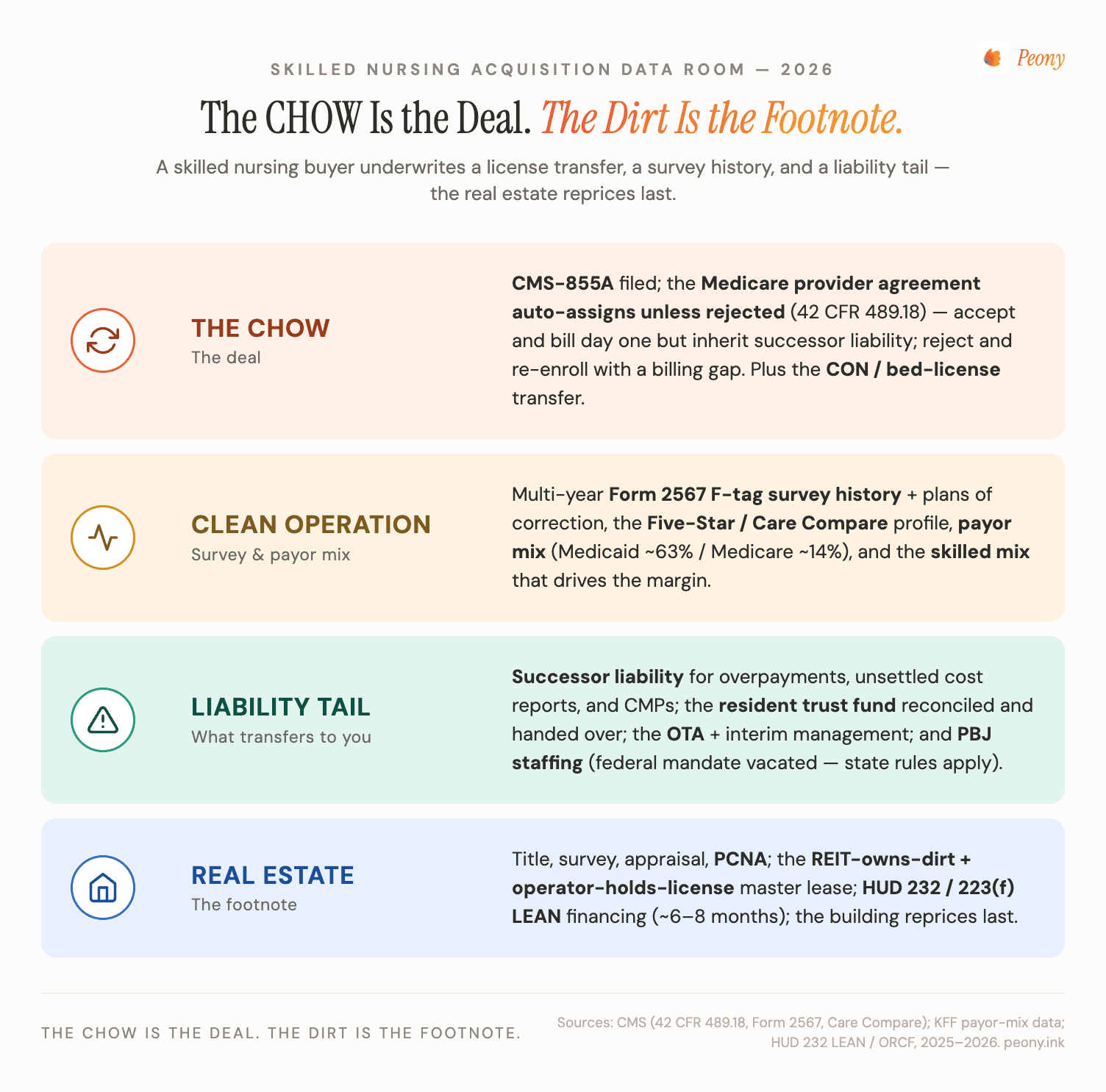

Here is the chain. To bill Medicare, a facility holds a Medicare provider agreement under a CMS-issued provider number; to bill Medicaid, it holds a state Medicaid certification and a negotiated rate; to operate the beds at all, in roughly three dozen states it needs a certificate of need (CON) or a state bed license. When ownership changes, all of that is in play through a change of ownership (CHOW) — the buyer files a CMS-855A, and the disposition of the seller's provider agreement (and the liabilities riding on it) becomes the central question of the deal. Sitting underneath are the things that determine whether the operation is even worth inheriting: the Form 2567 survey history and its F-tags, the Five-Star rating on Care Compare, the payor mix and Medicare cost reports, the resident trust fund ledgers, and the staffing record.

So when a buyer does diligence, it is not inspecting a building. It is verifying that an operation is clean and that its change of ownership is survivable — confirming the survey history doesn't hide a pattern of immediate-jeopardy citations, that the payor mix supports the price, that the provider-agreement decision is understood, and that there's no overpayment or civil-money-penalty time bomb that follows the Medicare ID into the buyer's hands. The data room is where that verification happens, which is why in skilled nursing the room is not logistics — it is the deal.

That framing is the whole post. Everything below is a consequence of it.

What goes in a skilled nursing facility data room? (The seven workstreams)

Seven workstreams, and only one of them is the building. The trap in most "SNF acquisition due diligence checklist" content is that it lists document names but not the one thing that goes wrong in each — which is what actually re-trades or kills nursing-home deals. Here is the buyer's-eye version. This is the signature table; read the right-hand column twice.

| Workstream | What the buyer verifies | The #1 thing that goes wrong |

|---|---|---|

| License & CHOW (CON, 855A, provider agreement) | The certificate of need / bed license, the CMS-855A enrollment, state licensure, and the disposition of the Medicare provider agreement | The buyer doesn't decide early whether to accept or reject the provider-agreement assignment — and inherits successor liability it never priced, or eats a Medicare billing gap it didn't plan |

| Survey & clinical (Form 2567 F-tags, Five-Star) | The multi-year Form 2567 statements of deficiencies, F-tags, plans of correction, Five-Star history, and any special-focus-facility status | A pattern of repeat or immediate-jeopardy F-tags surfaces late — the facility isn't just "below average," it's an enforcement and census risk the multiple didn't reflect |

| Payor mix & cost report (Medicare/Medicaid/skilled) | The census by payer, the skilled (Medicare/managed-care) mix, the Medicaid rate, managed-care contracts, and the Medicare cost reports | The skilled mix is softer than the rent roll implies — the building is "full" but mostly low-rate Medicaid, so the margin (and the price) is overstated |

| Successor liability (overpayments, CMPs, trust) | Outstanding Medicare overpayments, unsettled cost reports, civil money penalties, recoupment exposure, and the resident-trust-fund ledgers | An overpayment or CMP tied to the old operator follows the provider agreement into the buyer — or the resident trust fund doesn't reconcile and the buyer assumes a fiduciary mess at closing |

| Operations transfer (OTA, interim management) | The operations transfer agreement, interim management agreement, vendor and staffing transfer, and the day-of-transfer mechanics | The OTA and the provider-agreement timing don't line up — control flips before the license/billing is effective, and the facility runs uncertified (and unpaid) for a window |

| Real estate & HUD financing | Title, survey, the lease or master-lease structure (REIT-owned vs fee), appraisal, PCNA, and the HUD 232 / LEAN financing file if applicable | The room treats the building as the deal and under-builds the operating file — so the financing or the lease assignment stalls while the clinical/payor diligence catches up |

| Staffing & CBA (PBJ, labor) | Payroll-Based Journal (PBJ) staffing data, agency-staffing reliance, any collective bargaining agreement, and key clinical-leadership continuity | The census depends on a director of nursing or a staffing level that walks at closing — or an undisclosed CBA / labor liability changes the post-close cost structure |

A few of these deserve a closer look, because they are where the value (and the liability) actually lives.

The provider-agreement decision is the most consequential line in the room. As I'll detail below, under 42 CFR 489.18 the Medicare provider agreement automatically assigns to the buyer in a CHOW unless the buyer rejects it — and that one choice trades a clean billing day-one against inherited successor liability. A buyer that hasn't read the survey history and overpayment file early enough to make that call deliberately is flying blind into the most important fork in the deal.

The survey history is the clinical heartbeat. The Form 2567 record, F-tag patterns, and Five-Star trend tell a buyer whether it's acquiring a well-run operation with isolated, corrected deficiencies or a facility one bad survey away from enforcement, payment suspension, or special-focus designation. That record is public on Care Compare, but the deal-grade version — multi-year 2567s, plans of correction, internal QAPI documentation — lives in the room.

Successor liability is the tail that bites. Because the provider agreement carries the Medicare ID forward, it can also carry forward overpayments, unsettled cost reports, and civil money penalties. The successor-liability folder — and the resident-trust-fund reconciliation that has to be clean and handed over at closing — is where a careful buyer (and its counsel) spends real time.

What is a CHOW (change of ownership), and why is it the whole deal?

A CHOW — change of ownership — is the regulatory event at the center of every skilled-nursing transaction, and it is the reason an SNF deal does not behave like an ordinary real-estate purchase.

When ownership of a Medicare-certified facility changes hands, the new owner files a CMS-855A (the Medicare enrollment application for institutional providers), and the change is processed under the CHOW rules at 42 CFR 489.18. What's actually transferring isn't a deed — it's a federal provider relationship. The seller's Medicare identification number and provider agreement carry forward to the buyer, along with the obligations attached to them, unless the buyer takes specific action to reject the assignment.

That single fact reorders the whole deal. In an office building, the rent roll and the title are the asset, and the seller's past mistakes mostly stay with the seller. In a nursing home, the operation's regulatory history is the asset and the liability at once — you can inherit the seller's Medicare ID, its survey record's consequences, and its overpayment exposure, because they ride on the provider agreement you're stepping into. This is why I tell buyers the CHOW is the deal: the building is commoditized and easy to value, but the provider-agreement decision, the survey history, and the certificate-of-need transfer are the things that reprice or kill the transaction.

One more current wrinkle worth knowing: CMS has tightened ownership-disclosure requirements for nursing facilities. A final rule published November 17, 2023 (effective January 16, 2024), implementing Section 6101 of the Affordable Care Act, requires SNFs to disclose far more about ownership and "additional disclosable parties" — including entities that exercise financial control, that lease real property to the facility or hold a 5%-or-greater interest in that real property, or that provide administrative, clinical-consulting, or accounting services — and specifically to identify private equity company and REIT ownership. The revised CMS-855A built to capture this took effect for new enrollment cycles, and that disclosed data is made public. For a buyer structured as a PE platform or buying from a REIT, the disclosure file is now part of the diligence — and part of what the data room has to assemble.

Does the Medicare provider agreement automatically transfer — accept it or reject it?

It transfers automatically unless the buyer rejects it — and choosing which to do is the single most important decision in a skilled-nursing acquisition. Here is the mechanism, then the trade-off.

Under 42 CFR 489.18, when a CHOW occurs, the existing Medicare provider agreement is automatically assigned to the new owner as of the effective date of the change of ownership — unless the new owner affirmatively rejects that assignment. There is no neutral default that protects the buyer; doing nothing means accepting. So the buyer faces a genuine fork:

- Accept the assignment. The buyer keeps the seller's provider agreement and Medicare ID, and can bill Medicare from day one with no interruption in cash flow. The cost: it takes the agreement subject to all its terms and conditions — meaning successor liability for the prior operator's outstanding overpayments, unsettled cost reports, and civil money penalties, plus any plan-of-correction obligations. The Medicare ID comes with its baggage.

- Reject the assignment. The buyer declines the existing agreement and enrolls as a new provider, which can help sever some of the historical liability tied to the old agreement. The cost: re-enrollment and re-certification typically create a gap in Medicare billing while the new provider agreement is established — a real cash-flow and timing hit, and an operational risk for a census-dependent facility.

There is no universally correct answer; it's a liability-versus-continuity trade, and it's decided by what the data room reveals. If the survey history is clean and the overpayment/CMP exposure is small, accepting (and billing day one) is usually right. If the room surfaces serious unsettled liabilities, a buyer's counsel may push to reject and re-enroll, eating the billing gap to escape the tail. Either way, the decision has to be made deliberately and early, against the actual successor-liability file — which is exactly why a buyer's counsel wants that file complete and well-indexed before the clock runs. The mechanics of staging that decision sit inside the broader M&A due diligence process; the SNF-specific point is that this one regulatory choice can swing the economics of the whole deal.

What is a Form 2567 / F-tag survey history, and how do buyers read it?

The Form CMS-2567 is the official Statement of Deficiencies and Plan of Correction that a state survey agency issues after inspecting a nursing home, and the multi-year 2567 record is how a buyer takes the clinical and compliance temperature of the operation it's about to inherit.

The vocabulary, because AI and first-time buyers both trip on it:

- Form 2567 / Statement of Deficiencies — the document a surveyor produces listing every deficiency found during a standard or complaint survey.

- F-tag — the citation code on each deficiency, tied to the specific federal regulation (the "F" series for long-term-care requirements) that was violated. F-tags carry a scope-and-severity grid; the most serious are "immediate jeopardy" findings.

- Plan of Correction (POC) — the facility's required, surveyor-approved response describing how it will fix each cited deficiency and prevent recurrence. An approved POC is a condition of continued Medicare/Medicaid participation, and it's a binding commitment the surveyors follow up on.

- Five-Star / Care Compare — CMS folds the survey record (along with staffing and quality measures) into the Five-Star Quality Rating published on Care Compare, the public-facing rating.

CMS makes the redacted 2567 publicly releasable — under current guidance, within 14 days of receipt by the provider — which is why a buyer can pull a baseline survey picture from public sources before the room even opens. But the deal-grade read happens inside the data room, against the full multi-year history: the diligence question isn't "what's the star rating today," it's "is this a well-run facility with isolated, corrected deficiencies, or a pattern?" Repeat tags, immediate-jeopardy citations, payment suspensions, or special-focus-facility status tell a buyer it's acquiring enforcement risk and a fragile census — because referral sources and managed-care plans watch the same record. A clean, well-organized survey folder, with the 2567s and their plans of correction sitting next to the facility's own QAPI documentation, is one of the highest-leverage things a seller can stage, because it lets a serious buyer get comfortable fast instead of re-trading on uncertainty.

What is SNF payor mix and skilled mix, and why does it set the price?

Payor mix is the share of a facility's residents or revenue paid by each source, and skilled mix is the slice of that mix paid at the higher rates — and together they are the margin engine that sets the valuation, far more than occupancy alone.

Start with the national shape, because it frames every deal. Across U.S. nursing facilities, Medicaid is the primary payer for roughly 63% of residents, Medicare for about 14%, and the remaining roughly 23% are covered by another source such as private pay or managed care (KFF, 2025). The rates behind those shares are not close: Medicaid generally pays the lowest daily rate and covers long-stay custodial residents, while Medicare pays a much higher rate for short-stay, post-acute skilled rehab. So the skilled mix (or "quality mix") — the proportion of higher-reimbursing Medicare and managed-care days — is effectively where the margin comes from.

That's why a buyer underwrites census day by day and payer by payer, not as a single occupancy number:

| What it looks like | What the buyer actually checks | Why it moves the price |

|---|---|---|

| Occupancy % | Daily census trend, seasonality, post-COVID recovery curve | A full building can still be a thin-margin building — occupancy alone is the headline, not the story |

| Skilled / Medicare mix | Share of Medicare + managed-care days, length of stay, rehab referral sources | This is the margin; a softening skilled mix quietly erodes the EBITDA the price was built on |

| Medicaid rate & exposure | The state Medicaid rate, supplemental/provider-tax programs, and pending state rate changes | Heavy Medicaid reliance ties the asset to a state budget the buyer doesn't control |

| Managed-care contracts | Rates, authorization patterns, and concentration with specific plans | A facility leaning on one managed-care plan inherits that plan's authorization behavior |

| Cost reports | Three-ish years of Medicare cost reports reconciled to the census and financials | The cost report is the audited backbone; gaps between it and the rent roll are where re-trades start |

A facility that reads as "95% occupied" but is 90% Medicaid is a fundamentally different asset from the same building running a healthy skilled mix — same beds, very different EBITDA. There's a macro driver sharpening this in 2026, too: anticipated Medicaid funding changes flowing from the 2025 federal budget law (the "One Big Beautiful Bill Act") have operators and buyers watching state Medicaid exposure closely, and several analysts expect that uncertainty to increase SNF transaction volume as owners reposition ahead of it. Either way, the payor and census file — reconciled to the cost reports — is the heart of SNF financial due diligence, and it belongs front-and-center in the room.

How does certificate of need (CON) and the operations transfer agreement (OTA) work?

These are the two transfer mechanics that have no analog in an ordinary building purchase, and both belong in the room early because both are closing-condition risks.

Certificate of need (CON) / bed license. In roughly three dozen states, the right to operate skilled-nursing beds is controlled by a certificate of need or a state bed-licensing regime, and that right has to be transferred or re-issued as part of the deal. It cuts both ways, exactly like it does elsewhere in regulated healthcare. On one side it's a timeline and approval risk: the transfer is a regulatory step the parties don't fully control, so it has to be sequenced into the deal calendar as a closing condition. On the other side it's a scarcity premium: in a CON state a buyer can't just build a competing facility down the road, so an already-licensed, compliant bed base is more valuable because it's hard to replicate. A buyer's counsel maps the CON/bed-license transfer process up front; the data room holds the current license, the CON file, and the survey history that supports the transfer.

Operations transfer agreement (OTA) / interim management. Because the operation and the building are frequently owned and sold separately in skilled nursing — most often a REIT owns the dirt and leases it to an operator — the contract that moves the running of the facility is the operations transfer agreement (OTA), distinct from any real-estate purchase agreement. The OTA governs the genuinely messy day-of-transfer mechanics:

- When the provider agreement flips relative to when physical control changes hands.

- How the resident trust fund is reconciled and handed over — a fiduciary account holding residents' personal funds, tracked individually, that must be clean at transfer.

- Who owns pre- and post-closing receivables, and how cost-report cut-offs are handled.

- Whether an interim management agreement bridges the gap — if the buyer's own license isn't effective at closing, an interim arrangement lets the seller's license keep the facility certified and billing while the buyer's enrollment completes.

The classic OTA failure is a timing mismatch: control of the operation flips before the license and Medicare billing are effective, and the facility runs uncertified — and unpaid — for a window. Lining up the OTA, the CHOW effective date, and the provider-agreement decision is the operational core of closing an SNF deal, and the data room is where every version of those agreements, the resident-trust reconciliation, and the transfer checklist live as they're negotiated.

How does the data room actually run a skilled nursing acquisition?

This is the workstream the checklists skip: an SNF deal has to be executed across a seller-operator, a REIT landlord, a HUD or bank lender, multiple counsel, and sometimes a competing bidder — and that means moving a large, sensitive, partly-PHI document tape under access control while the deal and the regulatory clock run together. The data room is where that happens. I run Peony, so treat this as informed but interested — and I'll tell you where you don't need it.

Five things separate a skilled-nursing deal that closes cleanly from one that re-trades:

1. Stage the operating file before the request list lands. Diligence formally starts when the buyer's counsel sends a document request — and in SNF that list is brutal: multi-year 2567 survey histories, plans of correction, three years of cost reports, PBJ staffing data, payor-mix and census detail, resident-trust ledgers, the CON/license file, and the HUD package if it's financed. The seller's mistake is treating that as a scramble. The winning move is to build the package first, mirroring the seven workstreams, so on day one the buyer finds it indexed and waiting. AI auto-indexing sorts a bulk upload of hundreds of survey, cost-report, and license files into that structure in minutes — which is what makes a deal-grade SNF room buildable on a transaction timeline instead of a month of manual foldering. With 5,900+ customers, the pattern I see most is that the organized seller surfaces its own survey and payor problems early, while it still has leverage and a credible price.

2. One room, many parties, no leaks across them. An SNF deal runs an operator, a REIT landlord, a lender, and counsel at once, and they should not all see the same files. The operator and broker hold full read-write; a HUD or bank lender is scoped to the financial, cost-report, and title tape; a strategic counterparty is scoped to its own lane; resident-level data is gated tightly. Flat "admin / viewer" file-sharing can't model this without spinning up parallel folders that fragment the audit trail — programmatic permission groups behind an NDA gate do it in one room, with one source of truth, which also matters because the survey histories and resident schedules carry sensitivity an NDA exists to protect.

3. Who-reviewed-what is deal intelligence. When a seller can see that a serious buyer's counsel spent an hour in the successor-liability folder but never opened the resident-trust reconciliation, that's a signal — push the clean trust ledger proactively and clear the objection before it becomes a re-trade. Page-level analytics — who viewed which document, and for how long — turn the room from a passive file dump into a read on which buyers are real and what they're worried about. (To be precise about what that is: it's view-and-duration tracking per document, not keystroke capture.)

4. The sensitive files stay traceable, and the protected ones stay protected. Resident rosters, survey histories, and staffing files are competitively sensitive and partly protected information; an offering memo gets forwarded. Dynamic per-viewer watermarks stamp every page with the viewer's identity, so a leaked survey history or resident schedule traces to a name; an NDA gate sits in front of the room; and redaction blacks out resident identifiers, a specific Medicaid rate, or a name in a 2567 for a counterparty tier that shouldn't see it yet. On a deal where leaked clinical or resident data is both a competitive and a compliance problem, traceability changes behavior.

5. The financing room is its own discipline. If the deal is HUD-financed, the lender's package — appraisal, PCNA, three years of cost reports, A/R aging, operator financials — runs in parallel with the M&A diligence, often to a different counterparty on a different clock. One well-permissioned room can carry both the buyer-diligence lane and the lender lane without copying the file twice.

Peony does all of this at a flat $52/admin/month — you pay for seats, not pages, which is the right shape when the document set is a nursing-home operation that renders into thousands of pages of survey histories, cost reports, staffing files, and a HUD package. Our data room for real estate guide maps the broader seller-side room setup across CRE archetypes; this post is the skilled-nursing version of it.

Where you don't need any of this: a single mom-and-pop facility sold to a long-known regional operator, where the parties trust each other and the file is small, can run on a shared drive and a lawyer's checklist — no room required, and I'd rather say so than oversell. And for a $1B-plus, multi-state SNF portfolio M&A — the scale of a large REIT-to-REIT or institutional platform transaction, where the buyers' counsel often mandates the incumbent enterprise platform — the procurement default is still Datasite or Intralinks. The skilled-nursing-data-room sweet spot is the large middle: a single facility or a small-to-mid portfolio, an owner-operator or a regional roll-up buyer, a HUD-financed acquisition, where the operating file is heavy, the parties are several, and the clock is real.

What does the 2026 skilled nursing market actually look like for deals?

Active, regulation-shaped, and consolidating — with demographics on one side and policy uncertainty on the other. Knowing the landscape tells you why the deal flow is what it is, so here's the honest picture, hedged where it should be.

Demand has a demographic tailwind and a supply constraint. The aging of the boomer generation is steadily expanding the post-acute and long-stay population, while new SNF supply is constrained — by CON regimes in many states, by the capital intensity of building, and by years of operating pressure that thinned the field. National SNF occupancy has been recovering from its pandemic trough back toward the low-80s percent range, per industry trackers. The structural result is durable demand against limited new supply, which is the backdrop that keeps institutional capital interested.

The REIT buyers are visibly active. The dominant ownership structure pairs a healthcare REIT (the real estate) with an operator (the license), and the big three SNF-exposed REITs were clearly transacting through 2025 into 2026. CareTrust REIT reported roughly $1.8 billion of investments in 2025 and has continued acquiring into 2026 — including a roughly $142 million Mid-Atlantic skilled-nursing portfolio — with occupancy reported around 79–80%. Omega Healthcare Investors reported about $1.1 billion of new investments in 2025, with a portfolio still majority-weighted (around 62%) to skilled nursing and transitional care. Sabra Health Care REIT continued acquiring skilled-nursing and senior-housing assets into early 2026 at reported initial cash yields in the 7–8%+ range. (Figures are drawn from the companies' own 2025–2026 disclosures and reporting; verify the latest filings for a live deal.) The takeaway for a seller-operator: the institutional landlords are buyers, and they judge a room against an institutional standard.

Policy is the swing factor. Two 2025 developments reshaped the regulatory backdrop in opposite directions. First, the federal minimum staffing mandate is effectively dead: CMS's 2024 staffing rule was vacated by federal courts (Northern District of Texas, April 2025; Northern District of Iowa, June 2025), and a federal budget law signed in July 2025 imposed a multi-year moratorium blocking CMS from enforcing the standards, with CMS subsequently moving to rescind the rule — so the much-feared federal staffing floor is not, as of mid-2026, an operative cost the staffing diligence has to price (state staffing requirements still apply, and PBJ reporting continues). Second, Medicaid uncertainty rose: the 2025 federal budget law set anticipated Medicaid funding changes that vary by state, and analysts broadly expect that to increase SNF transaction activity as owners reposition Medicaid-heavy assets ahead of the changes. Net: a market with real demand, active institutional buyers, a lifted federal staffing overhang, and a Medicaid question that is itself a deal driver.

The through-line for the room: in a market where buyers are institutional and the regulatory file is the asset, the seller that can prove a clean operation and a survivable CHOW — fast, in an organized room — is the one that holds its price.

The bottom line: which skilled nursing deals need a data room, and which don't?

The asset is an operating license, so the question is always how heavy the operating file is, moving among how many parties, under how much regulatory and resident-data sensitivity. Segment it:

- Single mom-and-pop facility to a long-known buyer (small file, high trust): Probably no formal data room. A shared drive and a lawyer's SNF checklist can carry it. Don't let a vendor talk you into more than the deal needs.

- Single facility or small-to-mid portfolio, owner-operator or regional roll-up buyer: The core data-room deal. A flat-rate room — Peony at $52/admin/month, with AI auto-indexing, NDA gates, per-viewer watermarks, page-level analytics, and redaction — is the structural fit: you pay for seats, not for the thousands of pages a survey history, cost-report set, and HUD package render into.

- REIT-and-operator structure (real estate and operation transacting separately): A data room with a sharp permission wall — the landlord/financing lane and the operating-diligence lane gated apart, with resident data tightly scoped. Programmatic permission groups in one room beat parallel copies.

- HUD 232 / LEAN-financed acquisition or refinance: A data room built around the ORCF financing package — appraisal, PCNA, three years of cost reports, A/R aging, operator financials — running in parallel with the M&A diligence on its own clock.

- $1B-plus multi-state SNF portfolio M&A: Datasite or Intralinks. At megadeal scale the buyers' counsel often mandates the incumbent enterprise platform; that's the honest call, and we serve 5,900+ customers without pretending otherwise. The checklist content for these deals is owned today by the law firms and AHLA (whose SNF Acquisition Risk Assessment work is the reference) — credit where it's due; this post adds the data-room frame.

And one carve worth repeating: if your asset is independent living, assisted living, or memory care — private-pay housing rather than a Medicare/Medicaid-certified clinical floor with F-tags — you're in the senior-housing continuum, and our senior housing data room guide is the right hub. This spoke is for the skilled, government-reimbursed nursing facility specifically.

The through-line: in skilled nursing, the data room isn't logistics around the deal — because the asset is the operating license and its liabilities, the room is where the deal is actually won or lost. Prove the operation is clean, expose a clear-eyed view of the survey history and payor mix, organize the CHOW and the provider-agreement decision, and reconcile the resident trust — and a nursing-home acquisition closes at the price the seller underwrote. Leave it scattered, and a buyer reprices it one re-trade at a time. The commercial real estate data room is where that discipline lives.

Sources

- Centers for Medicare & Medicaid Services (CMS) — Form CMS-855A (Medicare Enrollment Application, Institutional Providers) and SNF attachment guidance (cms.gov)

- eCFR / Legal Information Institute — 42 CFR § 489.18, "Change of ownership or leasing: Effect on provider agreement" (ecfr.gov; law.cornell.edu)

- CMS — Form CMS-2567, Statement of Deficiencies and Plan of Correction; Care Compare and Five-Star Quality Rating (cms.gov)

- CMS — Final Rule, "Disclosures of Ownership and Additional Disclosable Parties Information for Skilled Nursing Facilities and Nursing Facilities" (Federal Register, Nov. 17, 2023; effective Jan. 16, 2024) and CMS fact sheet

- Sidley Austin; Ropes & Gray; Morgan Lewis; McDermott Will & Emery — analyses of the CMS nursing-facility ownership / PE & REIT disclosure rule

- KFF — "A Look at Nursing Facility Characteristics" (2025) for national payor-mix shares

- HUD — Office of Residential Care Facilities (ORCF), Section 232 / 223(f) LEAN program materials (hud.gov)

- AHA News; Faegre Drinker; Morgan Lewis; Federal Register — district-court rulings vacating the CMS minimum staffing rule (2025) and the statutory enforcement moratorium

- CareTrust REIT, Omega Healthcare Investors, Sabra Health Care REIT — 2025–2026 investor disclosures and SEC filings (investment volume, portfolio mix, yields)

- American Health Lawyers Association (AHLA) — Skilled Nursing Facility Acquisition Risk Assessment Tool; Lexology / Richter — SNF closing-checklist and resident-trust-fund guidance

Disclosure: I'm the co-founder of Peony, a virtual data room company, so I have an interest in how this turns out. I've tried to keep the analysis honest — including conceding that the smallest high-trust deals need no formal room, that $1B-plus multi-state portfolio M&A defaults to Datasite and Intralinks, and that the deep SNF acquisition checklists are owned by the law firms and AHLA. Specific regulations, CMS forms, court rulings, and deal figures were verified against the sources above as of July 2026; healthcare regulation is precise and changes, and where a rule was in flux (the staffing mandate) or a transaction figure came from a company's own disclosure I've said so. None of this is legal, tax, or investment advice — engage qualified healthcare-transaction counsel for your deal.

You might also like

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Jul 1, 2026

Senior Housing Data Room: You're Buying an Operation, Not an Address (2026)

Jun 30, 2026

Commercial Property Due Diligence: How to Run It Against the Clock (2026)