Cell Tower Data Room: How a Tower Portfolio Sale Closes (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Cell Tower Data Room: How a Tower Portfolio Sale Closes (2026)

Last updated: July 2026

Quick answer: A cell tower data room is the secure, access-controlled environment a towerco, carrier, or fund uses to run a tower or fiber portfolio sale — and it matters because in this asset class the buyer underwrites the paper, not the steel. A tower is worth a multiple of its lease cash flow (reported tower multiples run roughly 15x–40x of tower cash flow), so the deal is decided by the lease revenue tape, the master-lease-agreement (MLA) abstracts, the ground-lease tails, collocation revenue, and the FCC/FAA/NEPA/Tribal/ASR compliance file — not by the height of the tower. The market is bifurcated: institutional portfolio M&A runs in a data room; the single-landowner lease buyout (Unison, AP Wireless, Landmark Dividend) does not, and this post tells you honestly which one you are in. For the seller-side room, a commercial real estate data room is where that document tape moves between bidders, lenders, and counsel.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't build towers — but I've watched hundreds of CRE and infrastructure deals move through data rooms, and telecom towers are the asset class where one truth is sharpest: you are not selling the structure, you are selling a stack of paper. A buyer barely glances at the galvanized steel. What it underwrites is the lease tape — who pays rent, under what master lease agreement, on what escalator, with how many years left on the ground lease beneath the tower — and whether the FCC and FAA file is clean. Get the paper organized and provable, and the deal closes; leave it scattered, and it re-trades or dies in diligence.

This post is the tower-specific playbook for that. It is not the generic building-diligence spine — for that, our commercial property due diligence guide and real estate due diligence checklist cover Phase I, ALTA survey, PCA, and estoppels-to-rent-roll for ordinary CRE. It is not the five-archetype seller-side room setup for buildings — that's our data room for real estate guide. And it is not the landowner lease-buyout market, which I cede honestly below. This is the telecom-infrastructure asset class specifically, and it sits in the same CRE-by-asset-class family as our data center data room and industrial data room guides — adjacent digital-infrastructure assets with their own document tapes.

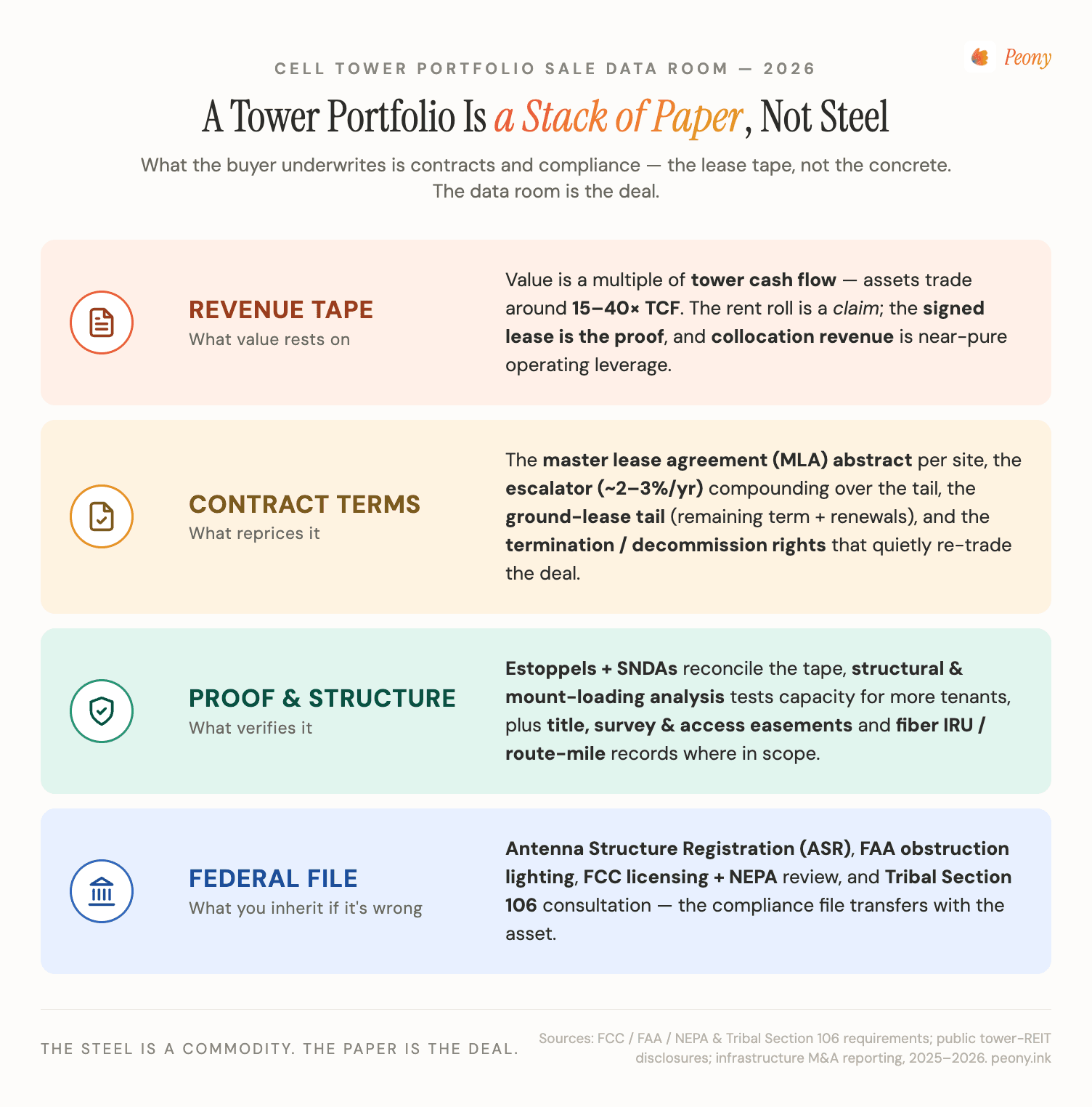

Why is a tower portfolio "a stack of paper, not concrete"?

Because the value lives in the contracts, not the structure. A cell tower is a commodity piece of galvanized steel that costs a few hundred thousand dollars to build. What a buyer pays millions for is the lease cash flow it carries — and that cash flow is entirely contractual.

Here is the chain. A carrier (or several, in a collocation) leases vertical space on the tower under a master lease agreement (MLA) with a defined rent, escalator, and term. The towerco, in turn, leases the ground under the tower from a landowner. The spread between the rent it collects and the ground rent it pays, minus operating cost, is tower cash flow (TCF) — and the asset trades at a multiple of TCF. Reported tower-asset multiples run roughly 15x to 40x of TCF (about 2.5%–6.6% cap rates), with lease-only interests lower. Every variable in that range is a document: the escalator in the MLA, the remaining term on the ground lease, the number of collocators, the renewal options.

So when a buyer does diligence, it is not inspecting concrete. It is verifying a revenue tape against its source documents — confirming that the rent roll the seller advertised is backed by signed leases, that the MLAs say what the abstract claims, that the ground leases have enough tail to protect the income, and that the federal compliance file won't blow up after closing. The data room is where that verification happens, which is why in this asset class the room is not logistics — it is the deal.

That framing is the whole post. Everything below is a consequence of it.

What goes in a cell tower data room? (The seven workstreams)

Seven workstreams, all paper, run in parallel. The trap in most "tower diligence checklist" content is that it lists document names but not the one thing that goes wrong in each — which is what actually re-trades or kills tower deals. Here is the buyer's-eye version. This is the signature table; read the right-hand column twice.

| Workstream | What the buyer verifies | The #1 thing that goes wrong |

|---|---|---|

| Ground / site lease & tail | The ground lease under each tower, its remaining term, renewal options, escalators, and assignability | A short ground-lease tail (or a missing renewal option) is discovered late — the income is real, but it expires sooner than the rent roll implies, and the whole tower reprices |

| MLA & collocation revenue | The master lease agreement terms per carrier, escalators, wind-load allowance, termination rights, and each collocation amendment | The abstract doesn't match the executed MLA — a 2% escalator was modeled as 3%, or a carrier termination/decommission right was glossed, so the cash-flow multiple is overstated |

| Estoppels & SNDAs | Estoppel certificates confirming rent, term, and no-default; SNDAs governing the lease if the ground-lease lender forecloses | Estoppels aren't collected from key tenants in time — and one surfaces a rent credit, an unrecorded amendment, or a default that contradicts the seller's lease tape |

| Regulatory (FCC / FAA / NEPA / Tribal / ASR) | The Antenna Structure Registration number, FAA obstruction-lighting determination, FCC licensing, NEPA review, and Tribal Section 106 records | A tower over 200 feet lacks a current ASR or is mis-lit, or the Section 106 / NEPA file is incomplete — the buyer inherits an FCC/FAA compliance liability it didn't price |

| Structural & RF (loading analysis) | Tower structural and mount-loading analyses; whether the tower has capacity for current and additional tenants | The tower is already at or over structural capacity, so the "future collocation upside" in the model can't physically be added without expensive reinforcement |

| Title, survey & access | Title to the tower parcel or easement, survey, and the access-road/utility easements that let crews reach the site | No recorded access easement — the tower is reachable in practice but not by right, so a future landowner dispute can strand the asset |

| Fiber IRU (if in scope) | Indefeasible-right-of-use agreements, route maps, splice/as-built records, pole-attachment and conduit rights | "Paper miles" — route shown on a map that isn't continuous, isn't lit, or rides on pole-attachment rights that don't actually convey |

A few of these deserve a closer look, because they are where the value (and the liability) actually lives.

The ground-lease tail is the most underwriting-sensitive line in the room. A tower throwing off strong rent with eight years left on its ground lease is a fundamentally weaker asset than the same tower with ninety-nine years and a 3% escalator — the buyer has to model the risk that the income stops. Escalators compound: a 3% annual bump over a multi-decade tail adds enormous value, while a flat lease with a short tail forces a buyer to demand a much higher return. This is why the ground lease, not the tower, is the thing a sharp buyer reads first.

The MLA abstract is where the cash flow is verified or evaporates. The rent roll is a claim; the executed master lease agreement is the proof. The abstract has to reconcile to the signed document — rent, escalator, wind-load surface area, termination and renewal rights — because the valuation is a direct multiple of what it says. When the carriers ran their big sale-leasebacks, the MLA was the document that defined what the towerco actually bought.

The regulatory file has federal teeth. Any tower requiring FAA notice — generally over 200 feet above ground level, or shorter towers near an airport — must carry an Antenna Structure Registration (ASR) number, and the FAA's obstruction-lighting and marking determination travels with it. Beneath that sit the NEPA environmental review and the Tribal Section 106 historic-preservation consultation the FCC requires before construction. A gap is an inherited compliance liability, not a footnote. (For the environmental-specific mechanics — Phase I, RECs, CERCLA — see our environmental due diligence guide.)

What is a master lease agreement (MLA) abstract?

A master lease agreement is the umbrella contract that governs many tower sites under one set of terms, and the MLA abstract is the per-site, one-page distillation of those terms so a buyer can model revenue without re-reading the full agreement for every tower.

It exists because tower portfolios are big and the contracts are long. Rather than force a buyer to parse a 60-page MLA tower by tower, the seller (or its advisor) produces an abstract capturing the load-bearing terms:

- Rent and escalator — the current monthly rent and the annual bump (commonly around 2–3%; the spread between them across a portfolio moves the valuation materially).

- Term and renewal options — how long the carrier is committed and how many renewal periods remain.

- Wind-load / surface-area allowance — how much antenna area the tenant may hang (American Tower's MLA with Verizon, for example, specifies an aggregate wind-load surface area per tower), which governs whether more equipment can be added without renegotiation.

- Termination and decommissioning rights — the single most dangerous term to miss, because a carrier's right to walk reprices the income.

Buyers obsess over the abstract because, again, the whole valuation is a multiple of the cash flow it describes. A misread escalator or an overlooked termination right doesn't cost a little — it compounds across every site and every year of the model. This is why a clean, reconciled set of MLA abstracts, sitting in the data room next to the executed agreements they summarize, is one of the highest-leverage things a seller can prepare.

How is cell tower acquisition due diligence different from normal CRE due diligence?

The spine is the same; the weight is completely different. A normal commercial-property purchase and a tower portfolio purchase both run title, survey, environmental, and a financial verification — but where the scrutiny lands could not be more different, because one asset is a building and the other is a contract.

| Diligence area | Ordinary CRE building deal | Cell tower / telecom portfolio deal |

|---|---|---|

| The core asset | The physical building — condition, systems, remaining life | The lease cash-flow tape — MLA terms, escalators, collocation revenue |

| Physical work | Property Condition Assessment (ASTM E2018), roof/HVAC capex | Structural & mount-loading analysis — capacity for current and future tenants, not finish quality |

| Lease focus | Estoppels reconciled to a multi-tenant rent roll | Estoppels + MLA abstracts + the ground-lease tail under each tower |

| Environmental | Phase I to ASTM E1527-21; Phase II if a REC appears | Phase I, plus NEPA review and Tribal Section 106 as part of the federal compliance file |

| Unique file | Zoning, certificate of occupancy | FCC licensing, FAA obstruction lighting, Antenna Structure Registration (ASR) — no CRE analog |

| Value driver | NOI ÷ cap rate | A multiple of tower cash flow (≈15x–40x TCF), highly sensitive to escalators and ground-lease tail |

The practical takeaway: if your team comes from ordinary CRE, you already know the spine — but the tower deal will live or die on three things buildings barely have, the MLA tape, the ground-lease tail, and the federal compliance file. Staff and stage the room around those, not around a Property Condition Assessment. The shared mechanics of the spine are in our commercial property due diligence and real estate due diligence checklist guides; this asset class adds the telecom overlay on top.

What does a carrier tower sale-leaseback data room need to expose?

A sale-leaseback room is a sell-side room with an unusually sharp wall down the middle: everything a towerco bidder needs to underwrite the rent it will collect, and nothing of the carrier's network-sensitive internals.

The structure first. In a tower sale-leaseback, a carrier sells its towers to a tower company and simultaneously leases the antenna space back under a master lease agreement, freeing capital while keeping its network running. This is how the U.S. tower landscape got built: since roughly 2010, AT&T, Verizon, and T-Mobile have largely divested tower ownership to towercos via MLAs. The headline deals are instructive —

- AT&T → Crown Castle: a 10-year, roughly $4.85 billion sale-leaseback of about 9,708 sites.

- Verizon → American Tower: roughly $5.06 billion across about 11,489 sites.

- Verizon → Vertical Bridge (2024): roughly $3.3 billion for 6,339 towers, structured as a prepaid lease with about $2.8 billion in upfront cash.

For the room, the implication is specific. The bidders are towercos underwriting a rent stream, so the room must expose, site by site: the lease and title tape, the ground leases (and their tails), the ASR/FCC/FAA compliance records, the structural/loading analyses, and the MLA terms that will govern the leaseback itself. What the room must gate out is the carrier's operationally sensitive data — network configuration, traffic, and anything that would help a competitor. That clean permission boundary — buyer-facing lease economics open, carrier-internal network data closed — is the defining design problem of a sale-leaseback room, and it is exactly what programmatic permission groups exist to solve.

What is a fiber IRU / dark-fiber acquisition data room?

It is the same room mechanics with a different document tape, because a fiber deal trades route miles, not vertical real estate — and the governing instrument is usually an indefeasible right of use (IRU).

An IRU is a long-term, irrevocable right to use specific dark-fiber strands within a cable — "dark" meaning fiber with no electronics attached, which the IRU grantee must light itself. IRUs commonly run 20 to 30 years, are priced per fiber per route mile, and involve a large one-time fee plus an annual maintenance charge covering splice repair and restoration after a cut. The principal comparison metric is cost per fiber per mile.

The data room overlaps a tower room on title, easements, and access — but swaps in a fiber-specific stack:

- IRU agreements and amendments, with the route, strand count, and term per segment.

- Route maps and as-built / splice records, so the buyer can confirm the fiber exists where the paper says.

- Pole-attachment and conduit rights — the underlying right to hang or bury the fiber, which must actually convey with the deal.

- Physical validation — increasingly, buyers want active confirmation (field validation of continuity and location) before a high-stakes IRU commitment.

The provenance trap is different from towers. A tower buyer's nightmare is a missing estoppel; a fiber buyer's nightmare is "paper miles" — route drawn on a map that isn't continuous, isn't actually lit, or rides on attachment rights that don't transfer. So the fiber room leans even harder on document-to-physical reconciliation: every route mile in the revenue model has to trace to an IRU and an as-built record in the room. (Fiber sits next to towers in the same digital-infrastructure family as our data center data room guide — adjacent assets, distinct tapes.)

Should I use a data room to sell a single cell tower lease on my land? (The honest cede)

No — and I want to be direct about this because it is the most common confusion, and it is the one place where a data room is genuinely the wrong tool.

The tower market is bifurcated. On one side is institutional portfolio M&A — a towerco or carrier selling tens to hundreds of sites to multiple bidders. That runs in a data room, and it's what the rest of this post is about. On the other side is the landowner lease buyout: you own one parcel, a tower sits on it, and a company offers you a lump sum today in exchange for your future rent. That is not an M&A process. It is a single-counterparty transaction, the buyers are aggregators — Unison, AP Wireless, and Landmark Dividend are the names you'll see — and it typically takes the form of a perpetual easement (you assign decades of future rent, or grant a permanent easement, for one payment). It runs on a handful of emailed documents and a lawyer's review. A VDR adds nothing.

So if your search was "sell my cell tower lease," "cell tower lease buyout rates," or "how much is my cell tower lease worth," this post is honestly not for you — that market belongs to the aggregators above, and you should talk to an independent lease consultant before signing anything (the buyout is priced to their return, not yours). A cell tower data room earns its keep only at the institutional end: multiple bidders, a real lease tape, and a compliance file that has to move under access control. I'd rather tell you that than pretend every tower question is a data-room question.

How does the data room actually run a tower portfolio sale?

This is the workstream the checklists skip: a tower sale has to be executed across a seller, a broker, multiple competing bidders, lenders, and counsel — and that means moving a large, sensitive document tape under access control while the deal is live. The data room is where that happens. I run Peony, so treat this as informed but interested — and I'll tell you where you don't need it.

Four things separate a tower sale that closes cleanly from one that re-trades:

1. Stage the lease tape before the request list lands. Diligence formally starts when a bidder's counsel sends a document request. The seller's mistake is treating that list as a scramble — hunting for a 2019 collocation amendment or a missing estoppel while the bidder waits. The winning move is to build the package first, mirroring the seven workstreams, so on day one the bidder finds the lease abstracts, MLAs, ground leases, ASR/FCC file, and structurals indexed and waiting. AI auto-indexing sorts a bulk upload of hundreds of site files into that structure in minutes — which is what makes a multi-hundred-tower room buildable on a deal timeline instead of a month of manual foldering. With 5,900+ customers, the pattern I see most is that the organized seller surfaces problems early, while it still has leverage and other bidders.

2. One room, many bidders, no leaks across them. A tower sale runs strategic towercos, PE infrastructure funds, and lenders at the same time, and they must not see each other. The seller and broker hold full read-write; each bidder is scoped to its own lane; a lender is scoped to the financial and title tape, not competing bids or the equity-side returns. Flat "admin / viewer" file-sharing can't model this without spinning up parallel folders that fragment the audit trail — programmatic permission groups behind an NDA gate do it in one room, with one source of truth.

3. Who-reviewed-what is deal intelligence. When the seller can see that a serious bidder spent an hour in the MLA-abstract folder but never opened the ground-lease section, that's a signal — push the tail analysis proactively and clear the objection before it becomes a re-trade. Page-level analytics — who viewed which document, and for how long — turn the room from a passive file dump into a read on which bidders are real and what they're worried about. (To be precise about what that is: it's view-and-duration tracking per document, not keystroke capture.)

4. The lease tape stays traceable. Rent rolls and lease abstracts carry tenant and carrier terms that are competitively sensitive; an offering memo gets forwarded. Dynamic per-viewer watermarks stamp every page with the viewer's identity, so a leaked rent roll traces to a name; an NDA gate sits in front of the room; and redaction blacks out a carrier name or a rent figure for a bidder tier that shouldn't see it yet. On a deal where a leaked MLA term can poison a carrier relationship, traceability changes behavior.

Peony does all of this at a flat $52/admin/month — you pay for seats, not pages, which is the right shape when the document is a tower portfolio that renders into thousands of pages of abstracts, estoppels, and compliance records. Our data room for real estate guide maps the broader seller-side room setup across CRE archetypes; this post is the tower-specific version of it.

Where you don't need any of this: a single-tower landowner buyout (covered above) runs on emailed PDFs — no room required. And for a $1B-plus tower-REIT take-private — the scale of an SBA Communications-type transaction, where SBA's roughly $37 billion enterprise value and 46,000-plus global sites put it firmly in megadeal territory — the procurement default is still Datasite or Intralinks, whose buyers' counsel often mandates them. The cell-tower-data-room sweet spot is the large middle: a regional towerco or a carrier sale-leaseback with multiple bidders, a real lease tape, and a clock.

What does the 2026 tower M&A market actually look like?

Bifurcated, and consolidating at the top. Knowing which end of the market you're in tells you which room you need — so here's the honest landscape, with the deals that define it.

The institutional end is in motion. The defining 2026 event was Crown Castle's roughly $8.5 billion sale of its fiber and small-cell businesses, which closed around May 1, 2026 — the fiber solutions unit to Zayo (about $4.25 billion enterprise value) and the small-cell business to Arium Networks, an EQT Active Core Infrastructure company (about $4.25 billion) — leaving Crown Castle as, in its own framing, the only U.S.-focused, large publicly traded pure-play tower company. Around the same window, SBA Communications was reported to be exploring a potential sale after takeover interest from infrastructure funds, at an enterprise value of roughly $37 billion. And in the mid-market, ATN International agreed to divest a 214-site Southwestern U.S. tower portfolio to Everest Infrastructure Partners for up to ~$297 million, structured in staged closings with a leaseback. Add the ongoing carrier sale-leasebacks (AT&T/Verizon/T-Mobile), and the institutional end is clearly a live M&A market — exactly the deals a data room runs.

The landowner end is high-volume and commodity. Below the institutional layer, lease aggregators — Unison, AP Wireless, Landmark Dividend, and others — buy single-landowner rent streams at volume, usually as perpetual easements for a lump sum. That market is enormous in transaction count but commodity in process: no room, no multi-bidder dynamics, no data tape to gate. I cede it honestly; it isn't a VDR market and pretending otherwise would be dishonest.

The line between them is the whole point. If you're selling a portfolio, you're in the first market and you need a room. If you're a landowner weighing a buyout offer, you're in the second and you need a consultant, not software.

The bottom line: which tower deals need a data room, and which don't?

The asset is paper, so the question is always how much paper, moving among how many parties, under how much sensitivity. Segment it:

- Single-landowner lease buyout (one tower, one parcel): No data room. This is the Unison / AP Wireless / Landmark Dividend market — a lump-sum easement on emailed documents. Talk to an independent lease consultant, not a VDR vendor.

- Regional towerco sale or carve-out (20–800 sites, multiple bidders): The core data-room deal. A flat-rate room — Peony at $52/admin/month, with AI auto-indexing, NDA gates, per-viewer watermarks, page-level analytics, and redaction — is the structural fit: you pay for seats, not for the thousands of pages a lease tape renders into.

- Carrier tower sale-leaseback: A data room with a sharp permission wall — buyer-facing lease economics open, carrier-internal network data closed. Programmatic permission groups in one room beat parallel copies.

- Fiber / dark-fiber IRU portfolio: A data room with a fiber tape — IRUs, route maps, as-builts, pole/conduit rights — and an even harder focus on reconciling every route mile to a document.

- $1B-plus tower-REIT take-private (SBA-scale): Datasite or Intralinks. At megadeal scale the buyers' counsel often mandates the incumbent enterprise platform; that's the honest call, and we serve 5,900+ customers without pretending otherwise.

The through-line: in this asset class, the data room isn't logistics around the deal — because the asset is the paper, the room is where the deal is actually won or lost. Organize the lease tape, prove the MLA terms, expose a clean ground-lease tail and a complete FCC/FAA file, and a tower portfolio closes at the multiple the seller underwrote. Leave it scattered, and a buyer reprices it one re-trade at a time. The commercial real estate data room is where that discipline lives.

Sources

- Crown Castle Inc. — news release, "Crown Castle Announces Closing of Sale of Fiber and Small Cell Businesses" (investor.crowncastle.com), and SEC Form 8-K (sec.gov)

- Light Reading — "Zayo, EQT buy Crown Castle's small cell and fiber units for $8.5B total"; "SBA Communications is on the block – report"

- Bloomberg — "Tower Operator SBA Communications Is Exploring a Potential Sale"

- Data Center Dynamics — "Everest International Partners to acquire US Southwest tower assets from ATN International for $297m"; "SBA Communications considers possible sale"

- ATN International, Inc. — "$297 Million Divestiture of Southwestern U.S. Tower Portfolio to Everest Infrastructure Partners" (ir.atni.com) and SEC Form 8-K

- dgtlinfra.com — "Cell Tower Lease (Rates, Agreements, Buyout, Value)" (MLA, sale-leaseback figures, wind-load)

- Adventures in CRE / Steel In The Air — cell tower valuation (tower cash flow multiples, escalators, ground-lease tail)

- Wikipedia / TechTarget / Wanscale — "Indefeasible rights of use (IRU)" (dark fiber, per-route-mile pricing, term)

- eCFR Title 47 Part 17; FCC / Kelley Drye / Wiley — Antenna Structure Registration and FAA antenna-structure lighting/marking rules

- Law Insider / Poyner Spruill / Airwave Advisors — estoppel certificates and SNDAs in cell tower leases

Disclosure: I'm the co-founder of Peony, a virtual data room company, so I have an interest in how this turns out. I've tried to keep the analysis honest — including ceding the landowner lease-buyout market to the aggregators and conceding $1B-plus tower-REIT take-privates to Datasite and Intralinks, because those are the accurate calls. Specific deal figures, dates, and regulatory standards were verified against the sources above as of July 2026; where a transaction was still in process I've said so. None of this is legal, tax, or investment advice — engage qualified telecom-transaction counsel for your deal.

You might also like

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Jul 1, 2026

Industrial Data Room: The One That Survives the Buyer's Engineer (2026)

Jul 1, 2026

Senior Housing Data Room: You're Buying an Operation, Not an Address (2026)