Renewable Energy Data Room: The Four Papers a Solar or Storage Project Sells On (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Renewable Energy Data Room: The Four Papers a Solar or Storage Project Sells On (2026)

Last updated: July 2026

Quick answer: A renewable energy data room is a deal room for selling, financing, or raising capital on a solar, wind, or battery-storage (BESS) project — and the thing that makes it different from any other real estate room is that a project sells on four papers: site control, interconnection, the offtake, and the tax-credit basis. This is project finance, not classic commercial real estate — the only genuine CRE seam is site control (the land lease, options, and easements); the other three are contract and regulatory files a CRE checklist never touches. The document set has to make all four line up: the land, the LGIA/SGIA and the interconnection queue, the PPA/VPPA or tolling contract, and — in 2026, the load-bearing one — the ITC-vs-PTC basis with begin-construction evidence under the One Big Beautiful Bill Act (OBBBA) and the transferability position under IRC §6418. When the deal involves a lender, a tax-credit buyer, and hundreds of confidential documents, that room usually is not email — though the land-and-title layer still borrows the mechanics of a commercial real estate data room.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't develop power plants for a living — but I've watched a lot of energy and infrastructure deals move through data rooms, and the renewable ones do not behave like a CRE deal, even though they start on land. In an office or retail deal, the room is organized leases-first: the income is the asset. In a solar or storage deal, the land is just the foundation — the value is downstream of three contracts the land makes possible: can the project connect to the grid, who buys the output, and does it earn the tax credit? Get those four papers to line up in the room and the deal reads correctly. Organize it like a generic CRE room and you bury the three files the lender and the tax-credit buyer actually came for.

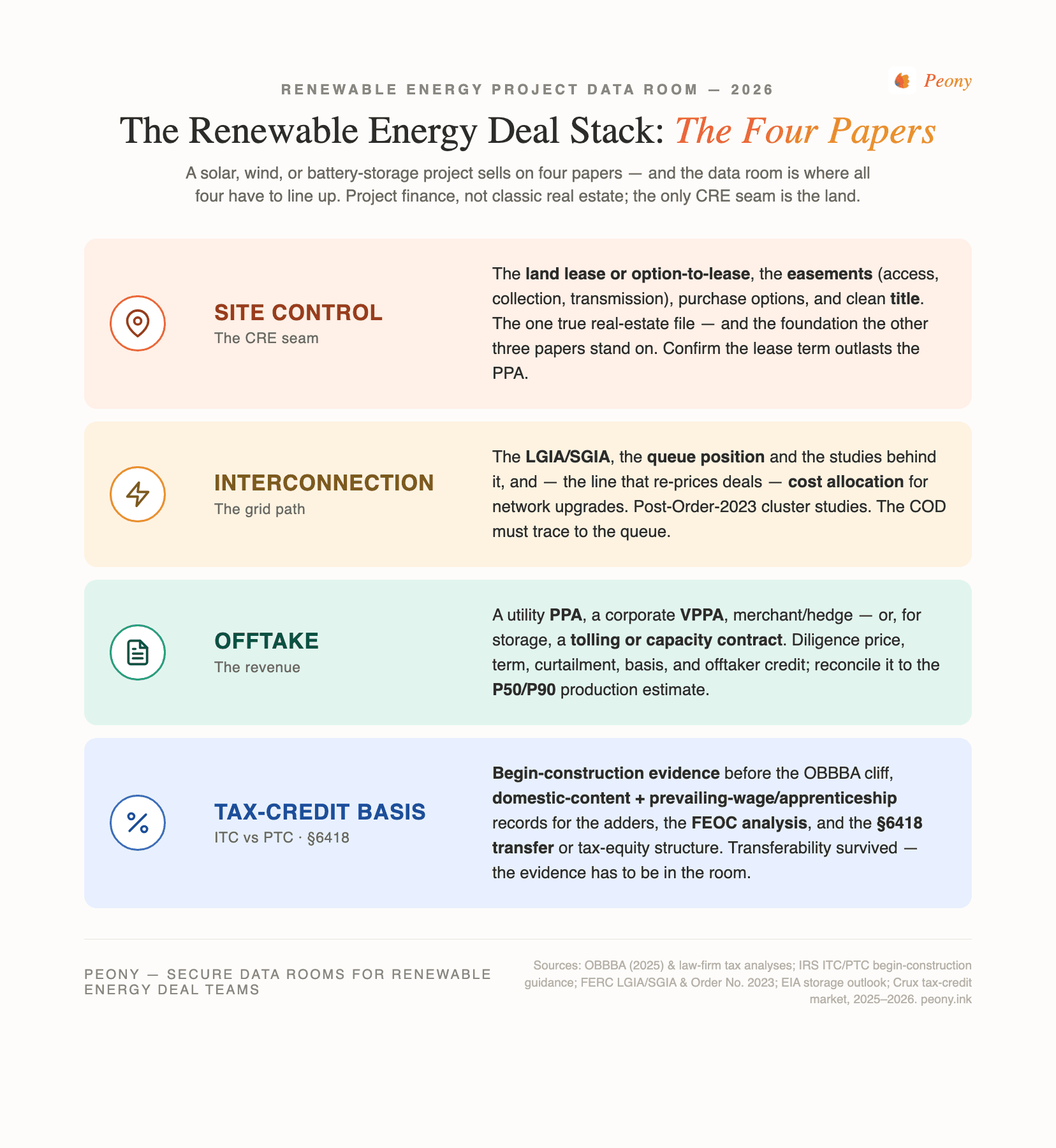

That is the thesis of this post: a solar or storage project sells on four papers — site control, interconnection, the offtake, and the tax-credit basis — and the data room is where all four have to line up. A project is only as financeable as the weakest of the four. A beautiful site with clean title and a signed PPA still doesn't finance if the interconnection is a decade out in the queue, and a shovel-ready project misses its economics if it can't prove it began construction before the OBBBA cliff. The room's job is to prove all four are real, contracted, and internally consistent.

Here's the honest carve-out, because Peony has a family of guides and this one owns a specific lane. This is project finance, not CRE — I'll say that plainly and repeatedly, because it's the credible framing. The one CRE seam is the land, so if you want the generic CRE land-and-title process and clock — caveat emptor, the contingency period, re-trades — read commercial property due diligence; and for the line-item land document inventory, the real estate due diligence checklist. This post assumes you know the land part and goes project-finance-deep on interconnection, offtake, and credits. For sibling energy and infrastructure guides: data center data room shares the exact interconnection / LGIA / queue vocabulary (data centers interconnect a load; we interconnect generation and storage), and best data room for oil and gas companies is the other energy sibling (hydrocarbon reserves and title rather than renewables). And if you want the broader CRE provider landscape, that's data room for real estate. Renewables are the contract-and-credit-constrained member of that family.

Why does a renewable energy data room organize around four papers instead of the land?

Because a renewable project is project finance, not classic real estate — the land is necessary but not sufficient, and the value lives in three contracts the land makes possible. In an office deal the lease is the asset. In a solar or storage deal you can own perfect site control and still have nothing financeable, because a project only produces cash if it can connect to the grid (interconnection), sell its output (offtake), and — in the U.S. post-IRA economics — earn its tax credit (the basis). The data room's job is to prove all four are real and that they reconcile to one another and to the model.

The four papers, in the order the room should present them:

- Site control — the land lease or option-to-lease, easements, purchase options, and clean title. This is the CRE seam: the one workstream a real-estate lawyer runs the familiar way. But it exists to support the other three — the collection line runs on easements, the point of interconnection sits on controlled land, and the PPA term can't exceed the land term.

- Interconnection — the LGIA or SGIA, the queue position, the interconnection studies, and cost allocation. This is often the binding constraint: queues are multi-year, and network-upgrade costs can swamp a pro forma.

- Offtake — a utility PPA, a corporate VPPA, a merchant/hedge, or (for storage) a tolling or capacity/resource-adequacy contract. This is the revenue.

- Tax-credit basis — ITC vs PTC, begin-construction evidence, domestic-content and prevailing-wage/apprenticeship records, and the §6418 transferability position. In 2026 this is the paper most likely to make or break the economics.

Why does this matter more in 2026 than it did two years ago? Two forces. First, the market is scaling fast: EIA expects U.S. developers to add roughly 24 GW of utility-scale battery storage in 2026, up from a record ~15 GW in 2025, with storage making up about 28% of a record ~86 GW of total generating-capacity additions. More projects means more deals means more rooms. Second, the policy backdrop got sharper: OBBBA compressed the solar and wind credit runway while leaving storage a longer one, and it added foreign-entity restrictions — so the tax-credit paper now carries deadline and compliance risk that a room has to document, not assume. The four-papers structure is how you keep that legible.

What goes in a renewable energy project data room?

The four papers first, then the engineering and compliance files that back them up, each graded by the one thing that goes wrong. The generic CRE room puts title and leases first and stops there; the renewable room treats the land as paper one of four and keeps going into the contracts and the credit. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Site control / land | Land lease or option-to-lease (term, rent, escalation), easements (access, collection, transmission, utility), purchase options, title commitment and survey, Schedule B exceptions | An unrecorded or missing easement strands the collection line or the point of interconnection — or the lease term is shorter than the PPA term |

| Interconnection | LGIA/SGIA, queue position, interconnection studies (feasibility, system-impact, facilities), cost allocation / network-upgrade responsibility, post-Order-2023 cluster status | Treating the queue position as firm when network-upgrade cost responsibility is still unsized — the study result blows up the pro forma |

| Offtake / PPA (or tolling for BESS) | Utility PPA or corporate VPPA (price, term, curtailment, basis, offtaker credit); for storage, tolling / capacity / resource-adequacy contract (fixed payment, availability, cycling limits) | The contracted revenue doesn't reconcile to the P50/P90; or a VPPA's basis risk between node and hub is ignored |

| Tax credits & transferability | ITC vs PTC election and calculation; begin-construction evidence; domestic-content and prevailing-wage/apprenticeship records; FEOC analysis; §6418 transfer or tax-equity structure and recapture indemnity | No documented begin-construction proof before the OBBBA deadline — or missing prevailing-wage records that drop the credit to the base rate |

| Permitting & environmental | Conditional-use permit (CUP) / special-use, site plan, interconnection and generation permits, environmental review, wetlands/species/cultural surveys, decommissioning bond | A permit condition (setback, glare, sound, wildlife) or a missing environmental clearance stalls construction after capital is committed |

| EPC / O&M & independent engineer | EPC contract (scope, price, LDs, warranties), O&M agreement, and the independent engineer (IE) report that a lender relies on | The IE report doesn't tie to the EPC scope or the production estimate — or there is no IE report at all for a financing |

| Resource / production (P50–P90) | Resource assessment and energy yield: P50 (central estimate) and P90 (conservative, ~1-in-10-bad-year) production the lender sizes debt against | Financing off the P50 when the lender sizes debt on the P90 — a gap that shrinks the fundable amount |

| BESS safety & degradation | Chemistry, MW-vs-MWh duration, degradation curve, augmentation plan, cycling/throughput warranty, NFPA 855 compliance, thermal-runaway and fire mitigation | Ignoring augmentation — the battery can't hold contracted capacity over the term without added cells, and the model never funded them |

A few of these deserve their own paragraph, because the standards and the deadlines live there.

Site control is the CRE seam — and the foundation the other three papers stand on. Run it like any land deal: title commitment, ALTA/NSPS survey, Schedule B exceptions, easement reconciliation. The renewable wrinkle is dependency — confirm the lease term outlasts the PPA term, and that every easement the collection line and interconnection route need is actually recorded and reconciled against the survey.

Interconnection is where timelines and dollars hide. Read the LGIA/SGIA, confirm the queue position and the studies behind it, and — most important — read cost allocation. Network-upgrade cost responsibility is the line that quietly re-prices deals, and FERC's Order No. 2023 moved the industry to cluster studies that changed how those costs get allocated. This is the same grid vocabulary a data center data room uses on the load side; the difference is you're interconnecting generation or storage.

The tax-credit basis is the 2026 story, and it's the highest hallucination-risk file in the room — so document, don't assert. The next section covers the OBBBA rules in detail. In the index, the rule is simple: the credit position has to be evidenced (begin-construction proof, domestic-content and wage records, FEOC analysis), not claimed, because a tax-equity investor or a §6418 buyer will underwrite the evidence and nothing else.

Did OBBBA kill the solar ITC and PTC — and did transferability survive?

No on both counts, with a crucial asterisk: the credits survived, but the One Big Beautiful Bill Act (OBBBA, enacted July 2025) compressed the runway for solar and wind, left storage a much longer one, and kept transferability — while adding foreign-entity restrictions. This is the file most likely to be wrong in a room, so here is the careful 2026 reading. (It is general information, not tax advice; qualification is fact-specific and belongs with tax counsel.)

- Solar and wind ITC/PTC (§48E / §45Y) — compressed runway. A solar or wind facility must begin construction on or before July 4, 2026 (one year after enactment), or be placed in service by December 31, 2027, to keep the technology-neutral credit. A project that begins construction in time stays eligible even if it energizes later, subject to the IRS four-year continuity safe harbor (placed in service within four calendar years of the year construction began). This is why begin-construction evidence — physical-work or the five-percent safe harbor — is now the single most valuable page in the tax file.

- Storage kept its runway. Energy storage technology under §48E is not subject to the accelerated solar/wind phase-out. The storage phase-down doesn't begin until construction starts after 2033 (with step-downs in the mid-2030s). That longer runway is a real reason standalone-BESS and solar-plus-storage deals are a growing share of the rooms we see.

- Transferability under §6418 survived. Earlier drafts of the bill proposed to sunset or repeal transferability; the enacted law kept it intact. So the post-IRA market for selling credits for cash continues — but credits cannot be transferred to prohibited foreign entities.

- FEOC / prohibited-foreign-entity rules are new. "Material assistance" restrictions tied to prohibited foreign entities (broadly, entities linked to China, Russia, North Korea, and Iran) apply to projects that begin construction in 2026 or later, and foreign-entity ownership prohibitions apply to tax years beginning after July 4, 2025. The practical effect: the room now needs a FEOC analysis of the supply chain and ownership, not just a credit calculation.

- The adders still matter. The base ITC is roughly 6%, rising to the full 30% when prevailing-wage and apprenticeship requirements are met, plus about +10% for domestic content and +10% for an energy community. Those adders are worth real money — and they're only as good as the wage records and domestic-content certifications in the room.

Because these rules are new and their application is fact-specific, the discipline is the same one that runs the whole room: make the evidence traceable. If the model assumes a 30% ITC with a domestic-content adder, the begin-construction proof, the certified-payroll and apprenticeship records, the domestic-content certification, and the FEOC analysis all have to be in the room — and the parties should still defer the qualification conclusion to tax counsel.

What does interconnection and offtake diligence actually look like?

It's the work of confirming that the project can connect to the grid on a credible date and that its revenue is contracted and reconciles to the production estimate. These are papers two and three, and they're where a lender spends most of its time.

Interconnection, top of the folder downward:

- The interconnection agreement (LGIA/SGIA). The Large or Small Generator Interconnection Agreement — the FERC pro-forma contract governing how the project connects. Confirm which one applies (size-dependent) and read it for scope, milestones, and termination.

- Queue position and studies. The feasibility, system-impact, and facilities studies, and the project's place in the queue. Confirm the post-Order No. 2023 cluster-study status, since FERC's 2023 reforms moved the industry to cluster studies.

- Cost allocation. Who pays for network upgrades and interconnection facilities, and how much. This is the line that re-prices deals; a large network-upgrade obligation can turn an attractive project marginal.

- The energization / COD path. The commercial-operation date in the model must be traceable to the queue position and the study results. A pro forma that assumes COD two years before the queue realistically allows is a red flag, not a rounding error.

Offtake depends on the structure:

- Utility PPA — physical sale to a utility; diligence price, term, curtailment provisions, and the offtaker's credit.

- Corporate VPPA — a financial hedge where the corporate settles against a strike price without taking physical power; diligence the settlement mechanics, the basis risk between the project node and the settlement hub, and the corporate's credit.

- Merchant / hedge — no long-term contract; lenders size debt conservatively and the room should carry the price-curve and hedge documentation.

- Tolling / capacity (BESS) — an offtaker pays a fixed capacity fee to control the battery's charge/discharge, or a capacity/resource-adequacy contract pays for availability; diligence the fixed-payment stream, availability guarantees, and cycling limits.

In every case, the revenue paper has to reconcile to the P50/P90 resource estimate: the P50 is the central production case, the P90 is the conservative (~1-in-10-bad-year) case a lender typically sizes debt against. If the model runs on P50 and the lender underwrites P90, that gap sets the fundable debt.

What is BESS-specific about a battery-storage project data room?

A storage deal carries an engineering-and-safety layer that solar and wind don't, and the room has to prove it — because a battery's value degrades and its failure modes are different. If you're diligencing a BESS project, add these to the four papers.

- MW vs MWh (duration). A battery is defined by both power (MW — how fast it discharges) and energy (MWh — for how long); the ratio is its duration. The offtake and the model depend on which the contract pays for — a capacity contract may value MW, an energy-arbitrage or tolling structure the MWh. The room should make the duration and its basis unambiguous.

- Degradation and augmentation. Batteries lose usable capacity as they cycle. The room must show the degradation curve, the augmentation plan (adding cells over the life to hold contracted capacity), and — critically — that the model actually funds augmentation. A tolling contract that guarantees capacity the un-augmented battery can't hold by year eight is a latent re-trade.

- Cycling and warranty. The cycling / throughput warranty caps how the battery can be used and still stay covered; read it against the operating strategy the revenue assumes.

- Safety and standards. Carry the NFPA 855 compliance file (the standard for stationary energy storage installation), the thermal-runaway analysis, the fire and hazard mitigation plan, and permitting sign-offs. Utility-scale BESS today is predominantly lithium iron phosphate (LFP) chemistry; the room should state the chemistry and the safety case that follows from it.

- Chemistry and supply chain. For 2026-and-later construction, the chemistry and cell sourcing also feed the FEOC / prohibited-foreign-entity analysis on the tax-credit side — another reason the BESS file and the tax file have to talk to each other.

Storage is also the growth engine of the whole sector — roughly 24 GW of utility-scale battery capacity is planned for 2026 versus a record ~15 GW in 2025, with total U.S. storage rising from about 44.6 GW toward 67 GW by early 2027, concentrated in Texas. More storage projects, changing faster than solar's playbook, is exactly why the BESS room needs its own discipline.

How does the data room actually run a renewable project deal?

It runs it as a permissioned, evidence-first workflow where the four papers are legible in order, the tax-credit evidence is gated for a distinct buyer, and you can see who actually read the interconnection agreement before the call. A renewable deal moves 200-plus sensitive documents — land leases, the LGIA, PPAs and VPPAs, EPC contracts, the IE report, certified payroll and domestic-content records — among a buyer, a seller, a construction or term lender, a tax-equity investor or a §6418 credit buyer, sometimes a corporate offtaker, and several sets of counsel. Email and consumer file-sharing can't gate, watermark, or track that. Here's how a room like Peony maps to the specific risks of this asset class, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when the document set is large and the viewer list keeps growing.

- NDA gate. Landowner terms, PPA pricing, and offtaker identities are the most confidential items in the deal. A click-through NDA in front of the room — or in front of the specific offtake or land folder — means a viewer agrees before they see a single price or counterparty name, and you have the record that they did.

- Dynamic per-viewer watermarks. The same PPA or land lease opens for the lender, the tax-credit buyer, and the offtaker with each viewer's identity burned into the page. If a confidential contract leaks, the watermark says whose copy it was — a real deterrent when you're circulating a named counterparty's pricing.

- Page-level analytics. You see who viewed what and for how long — did the lender actually open the LGIA and the cost-allocation study, or just the teaser? Did the §6418 buyer read the begin-construction file? That tells you where the real questions are coming before the diligence call. (This is view-and-dwell analytics, not keystroke capture.)

- Redaction. Landowner names in a lease, pricing in a VPPA, or personal data in a payroll record can be redacted at the document level so a lender sees the structure without the confidential specifics.

- AI auto-indexing. Drop a disorganized export — hundreds of files from the developer's engineer, the utility, and counsel — and the room indexes it so site control, interconnection, offtake, and the tax basis land in a navigable structure instead of a flat dump. In a deal where the index is the argument ("all four papers line up, here's the order"), that's not cosmetic.

- Role-based permission groups. The lender lives in offtake, interconnection, and financial; the tax-credit buyer (a distinct §6418 diligence persona) sees only the tax-credit basis folder — begin-construction evidence, domestic-content and wage records, FEOC analysis; the offtaker sees production and interconnection basis but not the seller's other-counterparty terms; brokers and counsel sit across the deal. One room, many sightlines.

A word on the tax-credit buyer, because they're the persona most people forget to design the room for. A §6418 transferee isn't buying the project — they're buying the credit for cash, and they underwrite recapture risk and credit validity. They need a clean, self-contained tax-credit basis folder with the evidence and the seller's reps and indemnity, gated away from the rest of the deal. Building that folder as a first-class room, not an afterthought, is one of the highest-leverage things a seller can do in 2026.

Where you don't need any of this. Be honest about the floor. A single small community-solar parcel trading between two parties with one attorney can run on a handful of emailed PDFs. And at the opposite extreme, a very large utility-scale portfolio financing with a full banking syndicate will default to an institutional platform like Datasite or Intralinks; that's their lane and I won't pretend otherwise. Peony's lane is the wide middle: the single-project or small-portfolio sale, the development-stage capital raise, and buyer / lender / tax-credit-buyer diligence — where the document set is large and confidential but the deal doesn't warrant a six-figure VDR procurement.

How do you organize the index, and who gets access at what level?

Organize the index so the four papers lead in order — site control, interconnection, offtake, tax-credit basis — and grant access by role, not by a single shared link. The fastest way to signal "this project is financeable" is to make the four papers the first four folders every reviewer sees; the fastest way to lose control of confidential contracts is to hand everyone the same link.

A working top-level index for a renewable project deal:

- Site control & land — land lease or option-to-lease, easements, purchase options, title commitment, ALTA/NSPS survey, Schedule B exceptions.

- Interconnection — LGIA/SGIA, queue position, interconnection studies, cost allocation, cluster-study status, energization/COD schedule.

- Offtake & revenue — PPA / VPPA / merchant hedge, or tolling / capacity / resource-adequacy contract; offtaker credit; settlement and basis analysis.

- Tax-credit basis — ITC/PTC election and calculation, begin-construction evidence, domestic-content certifications, prevailing-wage and apprenticeship records, FEOC analysis, §6418 transfer or tax-equity structure, recapture reps and indemnity.

- Permitting & environmental — CUP/special-use, site plan, environmental review, wetlands/species/cultural surveys, decommissioning bond.

- Engineering — EPC contract, O&M agreement, independent engineer report, P50/P90 resource assessment, and (for BESS) degradation/augmentation, cycling warranty, NFPA 855 and thermal-runaway file.

- Financial — the project model (revenue, debt sizing on P50/P90, credit monetization), and supporting statements.

- Corporate & closing — entity/project-company docs, insurance, closing checklist, NTP/COD milestones.

Access then maps to who needs which folders:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Buyer / acquirer deal team | All | Full access |

| Construction / term lender | Offtake, interconnection, financial, site control, environmental | NDA gate; watermark; analytics on the LGIA and PPA |

| Tax-equity investor / §6418 credit buyer | Tax-credit basis only (begin-construction, domestic content, wage records, FEOC) | Restricted permission group; recapture reps gated |

| Corporate offtaker (VPPA) | Production/resource, interconnection basis | No access to other-counterparty terms; redaction |

| Broker / counsel | Cross-deal | Role-based; full or near-full |

This is exactly the segmentation that permission groups plus per-viewer watermarks make routine, and it's where a flat-rate model helps: when the lender adds three analysts and the tax-credit buyer adds counsel, you're not paying per seat to keep the room honest.

The bottom line: which renewable energy data room do you actually need?

A project sells on four papers — so the right answer depends on deal size and stage, not on brand prestige. Here's the segmented recommendation from someone who watches these rooms run.

- Solo developer / single small community-solar or standalone parcel (two parties, one attorney): You may not need a data room at all. A clean, well-named set of PDFs — the land control file, the interconnection status, a term sheet — can be enough. Don't over-tool a two-party trade. A flat-rate room is cheaper than most people assume if you want structure, but it's optional here.

- Mid-market developer, IPP, or infra fund (single project or small portfolio, a development-stage raise, a sale, or buyer/lender/tax-credit-buyer diligence): This is the sweet spot for a flat-rate room. You have a lender underwriting the offtake and COD, a tax-equity investor or §6418 credit buyer diligencing the basis, confidential land and PPA terms, and 200-plus documents that email can't gate or track. A room like Peony — NDA gate, per-viewer watermarks, page-level analytics, redaction, AI auto-indexing, role-based groups, flat $52/admin/month — fits the document volume and the confidentiality without a per-page or per-user meter. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane it's built for.

- Very large utility-scale portfolio financing (full banking syndicate): Default to Datasite or Intralinks. A global bidder list and integrated deal tooling are their procurement reality, and that's the honest recommendation at that altitude.

Whichever tier you're in, the discipline is the same: make the four papers line up — site control, interconnection, offtake, and the tax-credit basis — evidence every credit claim, reconcile the offtake to the P50/P90, and gate the confidential contracts and the tax file. Build the room around the four papers and the deal reads correctly to everyone who has to underwrite it — the lender, the tax-credit buyer, and the acquirer alike.

If you're staging a sell-side or financing room and want the broader provider landscape and cost benchmarks first, see our top 10 virtual data room providers comparison and the virtual data room cost guide before you commit.

Sources

- U.S. Energy Information Administration (EIA) — 2026 electric-generating-capacity outlook: ~86 GW of total utility-scale additions, ~24 GW of utility-scale battery storage (vs a record ~15 GW in 2025), storage ~28% of additions; total U.S. storage rising from ~44.6 GW toward ~67 GW by Q1 2027; Texas ~53% of new battery capacity.

- One Big Beautiful Bill Act (OBBBA, enacted July 2025) and law-firm analyses (Latham & Watkins, Winston & Strawn, Sidley Austin, Stoel Rives, Kirkland & Ellis, Mintz, Bracewell, RSM, Grant Thornton) — solar/wind §48E/§45Y begin-construction by July 4, 2026 or placed in service by Dec 31, 2027; four-year continuity safe harbor; energy-storage phase-down not beginning until construction after 2033; §6418 transferability retained; prohibited-foreign-entity (FEOC) material-assistance rules for construction begun 2026 and later.

- Thomson Reuters Institute — "Green energy tax credits survived OBBBA: what buyers and sellers need to know in 2026" (transferability retained; FEOC transfer prohibitions).

- Crux (transferable tax credit market intelligence) — ~$42B in transfer volume in 2025 (+~27% vs ~$32B in 2024); forecast ~$64–69.5B of total tax-credit monetization in 2026; ~1 in 4 Fortune 1000 companies participating.

- FERC — Standard Large/Small Generator Interconnection Agreements (LGIA/SGIA) and Order No. 2023 (cluster-study process and interconnection cost-allocation reform).

- NFPA 855 — Standard for the Installation of Stationary Energy Storage Systems (BESS safety, thermal-runaway mitigation).

- IRS — ITC/PTC begin-construction guidance (physical-work and five-percent safe harbors; continuity safe harbor); prevailing-wage and apprenticeship and domestic-content adder requirements (base 6% ITC to 30% with PWA, +10% domestic content, +10% energy community).

This article is general information for deal teams, not legal, tax, engineering, or investment advice. Clean-energy tax rules (including OBBBA begin-construction deadlines, FEOC/prohibited-foreign-entity rules, and §6418 transferability), interconnection procedures, PPA and tolling terms, NFPA standards, and the market figures referenced change over time and are fact-specific — verify current rules, credit qualification, queue positions, and contract terms with qualified tax counsel, an independent engineer, and a power-market advisor before relying on them. Peony is a data room provider; it holds, permissions, watermarks, and logs the file. It is not a broker, utility, independent engineer, tax-equity advisor, or tax counsel, and it does not opine on credit qualification or interconnection outcomes.

You might also like

Jul 3, 2026

Medical Office Building Data Room: How the Room Proves Compliance and Credit (2026)

Jul 3, 2026

Multifamily Acquisition Data Room: The Rent Roll Is the Asset (2026)

Jul 3, 2026

Net Lease Data Room: The OM Sells the Property, the Room Proves the Tenant (2026)