UK Data Centre Due Diligence: The Grid-First Guide for Developers and Investors (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

UK Data Centre Due Diligence: The Grid-First Guide for Developers and Investors (2026)

Last verified: July 2026

I'm Sean Yu, co-founder of Peony, a data room company. I spend my days looking at how deals are actually diligenced, and UK data centre development is the one sector where the received order of due diligence is completely inverted. In most real-estate deals you start at the site — location, planning, land. In UK data centre deals, the site is nearly the last thing anyone cares about.

The reason is simple and unforgiving: in UK data centre deals, diligence starts at the substation, not the site. Planning can be argued; land can be optioned; but a firm grid connection date can only be evidenced — and every serious investor now reads the connection file first. Power is the binding constraint, the queue is rationed, and no lender or equity partner will fund construction until a firm, dated connection is on the table. Everything else in the room is priced around that one fact.

This guide is written for two people on opposite sides of the same table. The first is a UK data centre developer raising capital — often a small team, sometimes a single principal with large ambitions, sitting on a site with a grid application and a plan to build. The second is the investor or family office underwriting that raise, whose advisers will interrogate the developer's room. Different jobs, one shared truth: the deal lives or dies on the connection file, and the room is where that gets proved.

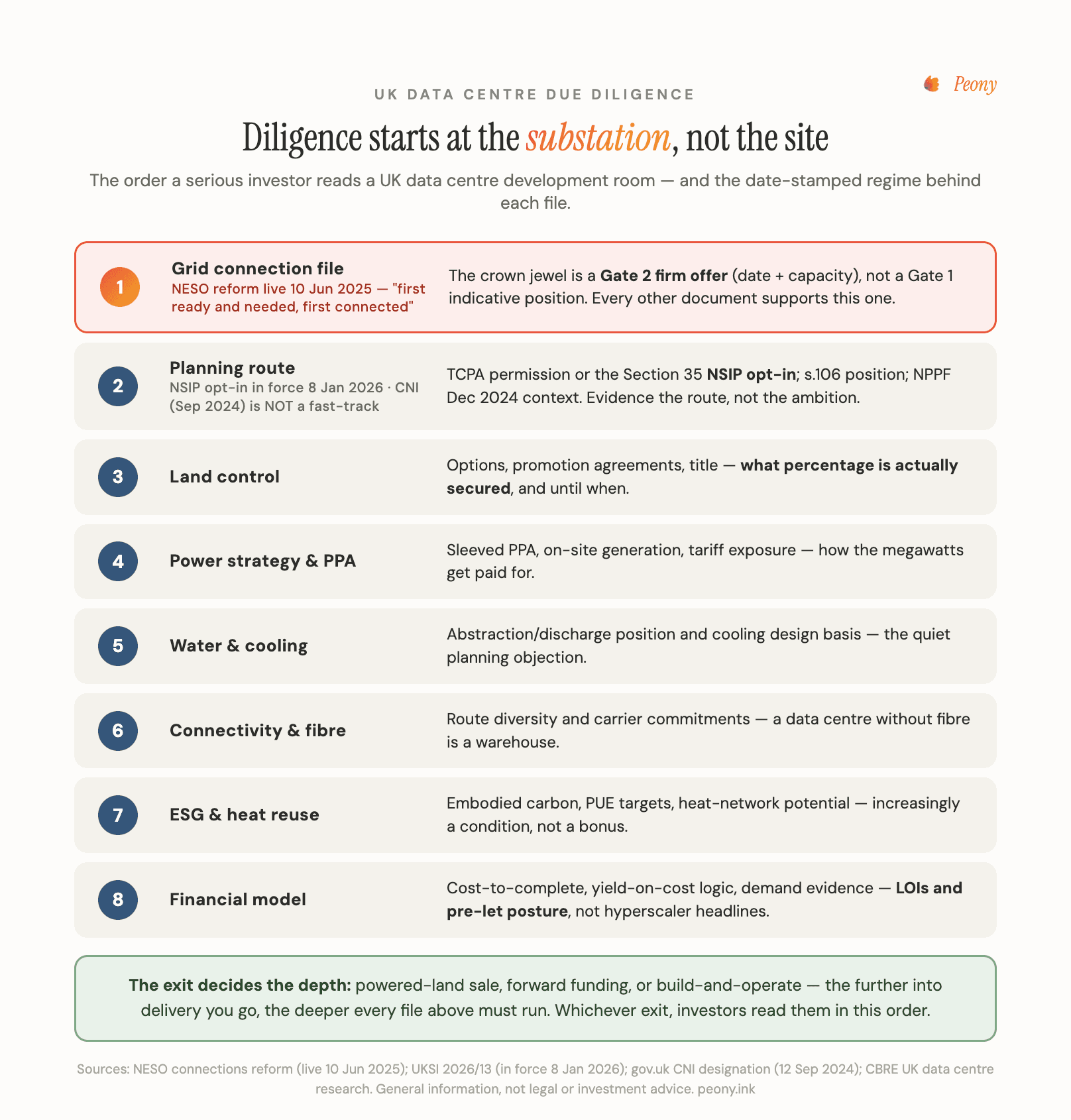

Quick answer: UK data centre due diligence runs in a strict order — grid connection status → planning route → land control → power strategy → water and cooling → connectivity → ESG → financial model — because power is the binding constraint and everything else is priced around it. The crown-jewel document is the grid connection offer, and the fact that matters most is its gate status: under the NESO connections reform live since 10 June 2025, a Gate 2 offer is firm (confirmed connection point, capacity, and date), while a Gate 1 offer is indicative only. The data room is the developer's evidence file for a JV or forward-funding raise — the ordered, current, access-controlled place where the connection offer, consents, land, and model are proved to a £100M+ counterparty. For the general project-finance version of this room, see the infrastructure projects data room guide; for the UK provider shortlist, best data room providers UK.

Where this post sits. This is the UK development-stage guide — grid offers, NSIP, powered land, and the investor raise. It is deliberately not the US acquisition room: if you're buying an operating or stabilised US asset (Will-Serve letters, Northern Virginia vacancy, powered shell versus powered land), read the data center data room guide. For the general project-finance room that applies across infrastructure, see the horizontal sibling, the infrastructure projects data room guide. This post is the data-centre-and-grid-specific version of that job.

Why does UK data centre diligence start with the grid connection?

Because power is the binding constraint, the queue that allocates it is rationed, and a lender or equity partner will not fund a pound of construction until a firm, dated connection is evidenced.

Start with the problem the market was drowning in. Under the old first-come, first-served connections model, the Great Britain queue grew roughly tenfold in five years to more than 700 GW of generation and storage awaiting grid access — around four times what Great Britain actually requires. A queue that size means the connection date, not the site, is the real asset. Anyone can apply; almost nobody can evidence a firm, near-dated connection. That scarcity is exactly why the connection offer is the crown-jewel document in a UK data centre room.

Then came the reform. NESO's connections overhaul — approved by Ofgem in April 2025, with first offers from 10 June 2025 — reordered the queue on a "first ready and needed, first connected" basis, replacing first-come-first-served. NESO now makes offers in twice-yearly application windows, and a project has to pass a two-part test to earn a firm place:

- "Ready" — readiness criteria: secured land rights meeting a minimum land-per-MW (an option agreement of roughly three years or more, ownership, or a long lease) and sufficiently progressed planning (an application submitted, or a DCO submitted for a DCO project).

- "Needed" — strategic alignment: capacity aligned to national energy targets and the Clean Power 2030 framework.

Gate 1 versus Gate 2 — what document evidences each?

This is the distinction the whole room turns on, so be precise about it.

A Gate 2 offer is a firm connection offer: a confirmed connection point, confirmed capacity in MW, and a confirmed connection date, granted because the project passed both "ready" and "needed." It is the financeable, room-critical document — the one a lender treats as threshold evidence that the megawatts are real. A Gate 1 offer is indicative: a connection point and a capacity reservation for a project that has not yet met the Gate 2 criteria, which must hit further milestones to progress.

What evidences each? For Gate 2, the offer letter itself, stating the gate, the capacity, the date, and the milestone or liability terms — plus, once accepted, the connection agreement. For Gate 1, the indicative offer and, crucially, your milestone plan showing the path to Gate 2. The reason a Gate 2 offer letter is the crown-jewel document is that it is the one piece of paper that converts "we have a site" into "this site can be powered, and here is when." An investor reads it first because it answers the only question that can kill the deal before any other work is worth doing.

Is a Gate 2 grid connection offer enough to raise JV equity for a UK data centre?

Honestly: a Gate 2 offer is necessary but not sufficient. It clears the single biggest kill question, and then the real underwriting begins.

Here is the nuance that matters. A Gate 2 offer de-risks the fatal objection — is the power firm, dated, and real? — and that is worth an enormous amount, because most sites never get past it. But no serious investor signs a term sheet on the connection offer alone. Having cleared power, they underwrite four more things, each of which can still re-price or sink the deal:

- Planning — is there a clear, evidenced consenting route (local or NSIP) with a status and a timeline, and where does the Section 106 position sit?

- Land control — is the site actually controlled by an option, a lease, or freehold title that is in the room, not merely asserted?

- Cost-to-complete — is there a real construction cost plan, ideally under a design-and-build contract with a guaranteed maximum price, so the model is anchored to a buildable number?

- Demand evidence — is there a hyperscale pre-let, an LOI, or at least a credible colocation lease-up plan, so the income the model assumes is more than a hope?

So what must a Gate 2-stage room contain? Lead with the Gate 2 offer letter and the connection agreement at the top of the index. Then evidence the other four so a reader cannot find the gap: the planning position, the executed land documents, a construction cost plan with a contractor covenant, and whatever demand evidence exists. A Gate 2 offer gets you a serious meeting and a real process; the rest of the room is what turns that process into a signature. The developers who struggle are the ones who think the connection offer is the deal. It is the ticket to the deal.

What changed in UK data centre planning — CNI, NPPF, and the NSIP opt-in?

Three separate things changed between 2024 and 2026, and the single most common mistake is to treat them as one fast-track. They are not. Let me take them honestly and in order, because an investor reading your planning file will know the difference.

CNI designation is not a planning fast-track — say so first. On 12 September 2024, the government designated UK data centres and data infrastructure as Critical National Infrastructure, the first new CNI designation in around nine years, placing digital infrastructure alongside energy and water. What that designation actually does is narrow and worth stating precisely: it creates a dedicated government team to monitor and anticipate threats, gives prioritised access to security agencies including the National Cyber Security Centre, and provides coordinated access to emergency services during an incident. What it does not do is confer any planning advantage. It is a security and resilience posture, not a route through the planning system — and if your room implies CNI status accelerates consenting, a competent adviser will mark it down. Present CNI honestly, as a durable signal of state-backed criticality, never as a consenting shortcut.

The NPPF changes (December 2024) are where planning policy actually moved. The revised National Planning Policy Framework, published December 2024, for the first time makes explicit reference to data centres: decision-makers must have particular regard to the economic need for data centres and digital infrastructure, and take account of their specific locational needs. The same revision defined "grey belt" in national policy for the first time — previously developed or underutilised green-belt land that does not strongly contribute to green-belt purposes — subject to the "golden rules." Two hedges the honest room respects: the precise extent to which local authorities must identify specific data centre sites is asserted by secondary summaries and should be framed as "particular regard to need and locational requirements," not a hard site-allocation mandate; and "grey belt" was framed largely around housing and employment land, so its application to a data centre is plausible but scheme-specific, not automatic.

The NSIP opt-in (in force 8 January 2026) is the real acceleration lever — with caveats. Since the Infrastructure Planning (Business or Commercial Projects) (Amendment) Regulations 2026 came into force on 8 January 2026, a data centre can opt in to the Nationally Significant Infrastructure Projects regime and seek a Development Consent Order decided by the Secretary of State, via a Section 35 direction under the Planning Act 2008, instead of going to the local planning authority. Three things a developer must get right in the room:

- It is opt-in, not mandatory — you request a direction, and the Secretary of State grants it only if the project is of national significance and meets the statutory criteria.

- The regulations set no MW or capacity threshold — "national significance" is deliberately left to be fleshed out in a National Policy Statement that was still pending in early 2026 (with consultation on a draft signalled for around February 2026). Until the NPS lands, treat the route as promising but carrying real uncertainty.

- DCO applications are ultimately determined against the relevant NPS, so the route's speed and criteria firm up only when that document exists.

What route should a developer evidence in the room, and how does an investor read a Section 106 position? Evidence a chosen, coherent route — local planning or NSIP — with a clear status and timeline; an undecided consenting strategy reads as a red flag, while a clearly evidenced one, either route, reads as competence. On Section 106, an investor does not treat a s.106 obligation as a problem in itself — it is a normal part of a large consent — but they read it for scale and certainty: what the obligations are, whether they are agreed or still in negotiation, and what they cost the model. A s.106 that is understood and priced is fine; a s.106 that is vague or open-ended is where the adviser starts asking hard questions. Write this part of your room carefully and from the primary position, not from half-remembered dates — the reforms above are precise, and getting the 8 January 2026 date or the opt-in nature wrong is the kind of error that quietly costs you credibility.

Should I sell powered land or forward fund the data centre development myself?

There are three exits, and choosing between them is really a choice about how much risk you carry and how much upside you keep — which in turn sets how deep your data room has to go.

Sell powered land. You sell the entitled, power-secured site and let a better-capitalised party build. It is the fastest, lowest-risk, lowest-return exit, and the room is the lightest of the three: a clean grid connection offer, the planning position, evidenced land control, and a clear title and connection story. The buyer is underwriting whether the megawatts and the consents are real, then building themselves — so your room proves entitlement and power, not construction. For the acquisition-side view of that same trade — powered land versus a powered shell, and how a buyer diligences each — see the data center data room guide, which covers the operating and stabilised-asset perspective in a US context.

Forward fund the development. You keep development control and upside, and a core buyer funds construction (or commits to buy on completion) against a pre-let. The room now has to add the full construction and cost-to-complete file — the design-and-build contract, the cost plan, the programme, the contractor covenant — plus real demand evidence, because the funder is underwriting a build, not just a site. This is the natural path when a strong pre-let already de-risks the asset.

Build and operate. You carry entitlement, power, construction, and lease-up risk all the way to a stabilised asset, and the room carries everything, including the operating model and the stabilised income assumptions. Deepest diligence, deepest risk, most upside.

The deciding variables are your balance sheet, your risk appetite, and how firm your demand is. A firm hyperscale pre-let makes forward funding or build-out far more financeable; without one, powered land is often the honest exit rather than a fallback. The point is to match the exit to what you can actually evidence — an investor can tell the difference between a developer who chose powered land deliberately and one who is calling a forced sale a strategy.

What's the typical development cost per MW for a UK hyperscale data centre?

There is no single honest number — and if a source hands you a precise figure without telling you what's inside it, be sceptical. The right answer is a hedged range plus a discipline for reading it.

Development cost is normally expressed per MW of IT load, and what's included swings the figure enormously. A meaningful £/MW number has to be clear about whether it includes land, the grid connection and any reinforcement works, the shell, the mechanical and electrical fit-out, the cooling design (air versus liquid materially changes the cost), and commissioning. Two quotes that look wildly different are often just measuring different scopes — one is shell-only, the other turnkey; one counts MW of IT load, the other MW of facility capacity.

With that caveat stated plainly: UK all-in figures are commonly cited in the region of £9-14m per MW of IT load, inclusive of shell, mechanical and electrical, fit-out, commissioning, and grid works. Treat that as a market-commentary composite, not a fixed benchmark. The disciplined move is to benchmark your own pro forma against a specialist cost index — Turner & Townsend's Data Centre Construction Cost Index is the standard reference, and London sits among the higher-cost European markets — and, above all, to confirm what any quoted number includes and excludes before it goes anywhere near your model. Why do quoted figures vary so widely? Because Tier and redundancy level, IT-load versus facility-capacity definitions, cooling technology, land and grid works, and shell-versus-turnkey scope each move the number by millions per MW. A £/MW figure without its inclusions is not a benchmark; it's a rumour. Model from your own inputs and state your assumptions.

What does the demand side look like?

Strong at the headline level and highly specific at the deal level — and an investor cares only about the second. Announcements are not your pre-let.

The macro picture is genuinely buoyant. The UK has drawn a run of large hyperscaler and sponsor commitments: AWS committed £8bn to UK data centres (announced 11 September 2024); Microsoft committed £2.5bn to UK AI datacentre infrastructure (its Nov-2023 commitment, with a GPU build-out toward 2026 — keep this distinct from the larger, separate Microsoft UK figure cited in later 2025 coverage); Google is investing £5bn in the UK over two years, opening its Waltham Cross data centre on 16 September 2025; and Blackstone committed £10bn to an AI campus at Blyth in Northumberland, on or near the former Britishvolt site (announced 25 September 2024). On the market side, CBRE put London 2024 take-up at 116 MW, forecast a record circa 183 MW for 2025, and projected London vacancy below roughly 8% at the end of 2025, trending, on CBRE's forecast, toward roughly 6% by the end of 2026 — a projection, not an outturn — with almost all new London space pre-let before delivery. (Take-up and vacancy definitions differ across brokers, so cite the house and the quarter and don't blend them.)

London data centre site vs regional UK site for investor appetite

The honest split: London and the western corridor carry the deepest tenant demand and the lowest vacancy — but power scarcity and planning friction. Regional sites, from Scotland's 400kV corridor to the North East, carry the power headroom and NSIP-scale potential — but thinner colocation demand. So investor appetite divides by strategy, not postcode prestige: an AI-training or hyperscale campus underwrite chases secured megawatts and goes where the grid is; latency-sensitive colocation underwrites London vacancy and pre-let comps. Your room should prove the matching thesis — a regional file leads with the grid offer and the anchor-tenant strategy, a London file leads with vacancy, comparables and pre-let evidence. A regional site pitched to a colocation-thesis investor (or the reverse) is a mismatch no document volume fixes.

Here is the honest part every developer needs to hear: those announcements are not your demand. A £10bn campus commitment by a named hyperscaler tells you the sector is hot; it tells an investor nothing about whether your site has a tenant. What investors actually read as demand evidence is document-level and specific to your scheme: a signed hyperscale pre-let (a long-dated, investment-grade lease that turns your development into a credit-tenant income stream), or failing that an LOI or heads of terms, or — for a multi-tenant play — a credible colocation lease-up plan with realistic absorption against that sub-8% London vacancy backdrop. A hyperscale pre-let and a spec colocation build are different risk animals: the pre-let is close to investment-grade income and raises capital easily; the speculative colo build carries lease-up risk and needs more equity and margin. Put the tenant evidence you actually have in the room, framed honestly for which model you're running — and never let a macro announcement stand in for a pre-let you don't have.

What goes in the UK data centre investor due diligence checklist?

Here is the development-room document set, grouped by the folder skeleton an institutional counterparty expects to navigate. This is a development raise — the story is entitlement, power, and pre-let, not in-place cashflow — so the room is ordered grid-first, exactly as the diligence runs.

- Grid and power file (the crown jewels) — the grid connection offer (Gate 2 firm versus Gate 1 indicative, with capacity in MW, connection date, and milestone or liability terms); the connection agreement once accepted; evidence of "ready plus needed" status; correspondence with the network operator; and cancellation or securities terms.

- Planning file — planning permission (local route) or DCO / Section 35 direction status (NSIP opt-in); the chosen route stated clearly; conditions discharge; the Section 106 position; EIA and environmental statement; and any grey-belt or green-belt analysis where relevant.

- Land file — option agreements, promotion agreements, conditional contracts, or long leasehold or freehold title; the title report; rights of access; power and fibre wayleaves and easements; and overage.

- Power strategy and PPA — the corporate PPA or sleeved/utility supply arrangement, any on-site generation or battery storage, backup provision, and the energisation programme. (For generation-heavy strategies, the renewable energy data room guide covers that side of the file.)

- Water and cooling — the water strategy and cooling design (air versus liquid or immersion), water discharge consents, and water-use efficiency; increasingly a consenting and community-sensitivity item in the UK.

- Connectivity and fibre — fibre routes and diversity, carrier and meet-me arrangements, latency to key hubs, and any dark-fibre or IRUs.

- Technical and EPC — the design-and-build contract (often with a guaranteed maximum price), the cost plan, the programme, contractor covenant, collateral warranties, professional-team appointments, insurances, and technical or QS reports.

- ESG and sustainability — embodied carbon, PUE targets, the renewable and PPA strategy, heat reuse and off-site heat recovery (a live UK theme — Google's Waltham Cross facility designed in off-site heat recovery), water stewardship, and BREEAM alignment.

- Financial model — yield-on-cost (development yield), stabilised NOI, exit cap rate, dev-cost per MW, lease-up assumptions, and return metrics (IRR, equity multiple) with sensitivities.

- Corporate / SPV — the SPV structure charts, cap table, board consents, shareholder or JV term sheets, and KYC on the principals.

The order is the point. A generic real-estate folder tree buries the grid file three folders deep; an institutional data centre room puts it first, because that is where the underwriting starts.

How a small developer looks institutional to £100M+ counterparties

The uncomfortable truth for a small developer is that the first work product a £100M fund sees is your room — and it is judged before you are. A newly incorporated developer with gigawatt ambitions on the 400kV network can look every bit as institutional as an established platform, or every bit as amateur, depending entirely on how the room is run.

Institutional-grade is discipline, not headcount. Five things separate a room that reads as professional from one that reads as a shared drive:

- Index discipline. The folder structure mirrors how an investor underwrites — grid first, then planning, land, power, demand, model — so a reader finds what they need in the order they think. A room organised by document type instead of by diligence logic makes the reader do your work.

- Version control. Documents live behind stable links, and replacing the file behind a link retires the old version without breaking the address — so nobody ever opens a superseded connection offer or a stale model. Stale versions circulating is one of the fastest ways to look amateur.

- A managed Q&A process. Questions come through a tracked workflow, not a scatter of emails, so answers are consistent, attributable, and don't contradict each other across bidders.

- Watermarked, staged disclosure. Sensitive commercial terms — grid capacity, PPA pricing, pre-let economics — release in tiers behind an NDA, each document dynamically watermarked to the viewer, so a leaked page points back to who leaked it.

- Page-level analytics to read intent. Page-level analytics show which counterparty opened which document, how long they spent, and what they re-visited — so you can tell who is genuinely progressing (heavy time in the model, the grid offer, the lease), who has gone cold, and when to push the term sheet.

That last point is worth dwelling on, because it is where a small developer gains a genuine edge. In a competitive raise you are running many counterparties through the same room in parallel. Reading their engagement — not guessing at it — lets a one-person or five-person team sequence follow-up, time the term-sheet push, and hold leverage like a much larger shop. The site gets you the meeting; the disciplined, current, controlled room is what makes a fund decide you are a developer, not a broker.

The family office on the other side of the table

Flip the table. On the buy-side sits a family office deploying principal capital into a data centre development, and its advisers will interrogate the developer's room with a specific set of questions — so it helps a developer to know how that reader thinks.

Family offices have become real players in digital infrastructure, but the numbers keep the appetite in proportion. The UBS Global Family Office Report 2025 surveyed 317 family offices with an average of roughly US$1.1bn in assets, and found infrastructure at only around 1% of the average strategic allocation — against 21% in private equity (direct plus funds), 30% equities, and 11% real estate. (Those allocation percentages are corroborated from UBS's published summary; confirm each against the report itself before quoting as exact.) The honest read is that infrastructure is a small but directional allocation — family offices invest heavily through direct deals, and data centre development JVs fit the appetite for tangible, long-dated, inflation-linked, cash-yielding real assets. They often co-invest alongside a specialist developer or GP rather than originate solo.

What will a family office's advisers ask of the developer's room? The same grid-first fundamentals, with a buy-side emphasis: power certainty (is the connection genuinely Gate 2?), anchor-tenant covenant (is the pre-let truly investment-grade?), cost certainty (is there a guaranteed-maximum-price design-and-build contract?), downside and exit (cap-rate and lease-up sensitivities), sponsor track record and alignment, and governance and reporting rights in the JV. They value read-side control — view-only access, watermarking, a clean audit of who saw what, and a structure their investment committee can consume — because discretion and confidentiality are non-negotiable for principal capital. For how Peony serves that buy-side reader specifically, see our family offices solution.

Where does the data room fit — and what should it cost?

The room is the developer's evidence file — the ordered, current, access-controlled place where the connection offer, consents, land, and model are proved to a counterparty. On cost, the model matters more than the sticker, and Peony is built for exactly this shape of deal.

Peony is priced per admin seat, with recipients free. The Business plan is $30 per admin per month and the Data Room plan — which adds dynamic watermarking and unlimited rooms — is $52 per admin per month on annual billing (roughly £25-45 at current exchange rates, though I'd take the USD figure as the real one). The decisive detail for a capital raise is that your recipients are free: you pay for your internal admin seats, and every investor, adviser, and counterparty you invite into the room accesses it at no cost. A per-user platform bills you for exactly the thing a competitive raise is made of — lots of external readers — which is the wrong incentive when you're running a dozen funds through the room at once. That per-admin, free-recipient model is why 5,900+ customers run controlled sharing on Peony without their bill scaling with their audience, and it's why the economics work for a lean development team.

A note for the UK reader specifically: the UK is Peony's second-largest market, with 140+ customers across the UK and Europe, so this is not a US tool bolted awkwardly onto a UK deal. What Peony gives a development raise is the controlled document layer the room needs: granular folder, file, and page permissions; dynamic watermarks; NDA gating before sensitive terms release; page-level analytics to read investor intent; AI Q&A against models you connect (with zero retention); built-in e-signatures; exportable audit logs; and screenshot protection (Business) or Screenshield (Data Room). It is SOC 2 Type II and has held 99.96% uptime since August 2025. For the UK provider shortlist and how Peony sits against the alternatives, see best data room providers UK; for the security evaluation a counterparty's own team will run, see the data room security questionnaire. And if you're running a data centre raise end to end, the data centres solution page is the product view of everything above.

I run Peony, a data room company, and I'd rather be straight about where it fits than oversell it. Peony is the controlled evidence layer for your raise — it gates, versions, watermarks, tracks, and logs, and its per-admin, free-recipient pricing is built for the shape of a capital raise with many counterparties. It doesn't secure your grid connection, draft your s.106, or underwrite your model — those are your job. But if the job you have is presenting a firm connection offer, clean consents, evidenced land, and a credible model to a £100M+ counterparty in a way that reads as institutional, that is precisely what the 5,900+ customers who use it rely on it to do.

If this guide describes the raise you are preparing, Peony for data centres and digital infrastructure is the product-side version of it — the staged disclosure, watermarking and Q&A mechanics above, applied to exactly this persona.

Frequently asked questions

We're a small UK developer with a Gate 2 offer — is a Gate 2 grid connection offer enough to raise JV equity for a UK data centre?

A Gate 2 offer is necessary but not sufficient. It de-risks the single biggest kill question — is the power real, firm, and dated? — because under the NESO connections reform that went live on 10 June 2025, a Gate 2 offer means your project passed both the 'ready' and 'needed' tests and holds a firm connection point with confirmed capacity and a connection date. That clears the fatal objection. But a JV partner still underwrites four more things: planning route and status, land control (option, lease, or freehold), cost-to-complete under a priced construction contract, and demand evidence (a hyperscale pre-let or credible colocation lease-up plan). So a Gate 2 offer gets you a serious meeting, not a signed term sheet. The honest framing for your room: lead with the Gate 2 offer letter as the crown-jewel document, then evidence the other four so the investor cannot find the gap. Gate 2 answers the question that kills most deals; the rest of the room answers the questions that price them.

Our grid offer is still Gate 1 — how do we get a Gate 2 grid connection offer under NESO queue reform?

A Gate 1 offer is indicative — a connection point and a capacity reservation for a project that hasn't yet met the firm criteria. To move to Gate 2, the reformed process (live since 10 June 2025, 'first ready and needed, first connected') requires you to pass two tests. 'Ready' means secured land rights meeting a minimum land-per-MW — an option agreement of roughly three years or more, ownership, or a long lease — plus sufficiently progressed planning, typically an application submitted (a DCO submitted for a DCO project). 'Needed' means your capacity aligns with national energy targets and the Clean Power 2030 framework. NESO makes offers in twice-yearly application windows, so timing your land and planning evidence to a window matters. In the room, a Gate 1 position isn't fatal — but you present it honestly, show the milestone plan to Gate 2, and don't let a reader mistake indicative for firm. Investors have learned the difference and will check the offer letter's gate status themselves.

We're weighing our raise — forward funding vs JV equity for a UK data centre development, which is better for a small developer?

It depends on how much of the build risk and upside you want to keep. In a JV equity structure, you contribute land control, entitlement, power, and development expertise; an institutional partner provides the majority of the equity, you run the build, and you share the promote or carry — you keep more upside and more risk. In forward funding, a core buyer funds construction (or commits to buy on completion), which de-risks you and hands you an exit, but you crystallise value earlier and keep less of it; this is common where a strong pre-let already de-risks the asset. For a first-time developer with a thin balance sheet, forward funding off the back of a hyperscale pre-let is often the cleaner path to getting built; a developer with a track record and appetite for risk keeps more through a JV. Both need the same room — grid, planning, land, model, demand — because the buyer or partner underwrites the same fundamentals either way. The structure changes who holds the risk, not what diligence asks.

As a first-time raiser, should we bring in an infrastructure fund or a family office as our data centre development capital partner?

They behave differently, and the difference matters for a first raise. Infrastructure funds are institutional, process-driven, and repeat players — they run a defined diligence programme, expect a fully populated room, and move at committee speed; they are the natural home for a large forward-funding or JV cheque. Family offices deploy principal capital, can move faster and with more discretion, and increasingly target digital infrastructure directly for its long-dated, inflation-linked income — but per the UBS Global Family Office Report 2025 (317 family offices surveyed), infrastructure is still only around 1% of the average strategic allocation, so their appetite is real but selective and often taken as a co-investment alongside a specialist developer rather than a solo origination. A pragmatic sequence for a first-timer: a family office or a specialist developer-GP can anchor early development equity when you have less to show, and an infrastructure fund comes in at forward-funding or JV stage once the grid and planning are evidenced. Either way, your room is the first work product they judge — see how a family office reads a developer's room in our family offices guide.

We hold consented powered land — should we sell powered land or forward fund the data centre development ourselves?

There are three exits, and they demand different diligence depth. Selling powered land is the fastest, lowest-risk, lowest-return exit — you sell the entitled, power-secured site and let a better-capitalised party build; the room is lighter (grid offer, planning, land control, a clean title and connection story) because the buyer builds. Forward funding sits in the middle — you keep development control and upside, a funder pays for construction against a pre-let, and the room must add the full construction and cost-to-complete file plus demand evidence. Build-and-operate is the deepest — you carry entitlement, power, construction, and lease-up risk to a stabilised asset, and the room carries everything including the operating model. The right choice turns on your balance sheet, your risk appetite, and how firm your demand is: a firm hyperscale pre-let makes forward funding or build-out far more financeable; without one, powered land is the honest exit. For the powered-land-versus-powered-shell view on the acquisition side of that trade, see our data center data room guide.

Our site is 200MW in England — should we pursue NSIP or local planning to keep investors comfortable?

As of early 2026 you have a genuine choice, which is new. Since the Infrastructure Planning (Business or Commercial Projects) (Amendment) Regulations 2026 came into force on 8 January 2026, a data centre can opt in to the Nationally Significant Infrastructure Projects regime and seek a Development Consent Order decided by the Secretary of State, via a Section 35 direction, instead of going to the local planning authority. Two honest caveats: the regulations set no MW threshold — 'national significance' is judged case by case and will be fleshed out in a National Policy Statement that was still pending in early 2026 — and the route is opt-in, not automatic, so you request a direction and the Secretary of State grants it only if the project qualifies. The trade-off investors weigh: local planning is familiar and can be quicker for a well-received scheme, while the NSIP route offers central determination that bypasses local refusal risk but carried real uncertainty until the NPS lands. What matters in the room is that you evidence a chosen, coherent route with a status and a timeline — not that you pick a particular one. An investor reads an undecided consenting strategy as a red flag; a clearly evidenced one, either route, as competence.

We're an 8-person developer — how do we make a small data centre developer look institutional to a £100M counterparty in the data room?

The room is the first work product a fund sees, and it is judged before you are. Institutional-grade is mostly discipline, not headcount: a clean index that mirrors how an investor underwrites (grid first, then planning, land, power, demand, model), current documents behind stable links so nobody opens a superseded version, a managed Q&A process rather than a scramble of emails, watermarked and staged disclosure so sensitive terms release in tiers, and page-level analytics so you can read which counterparty is genuinely progressing. A newly incorporated developer with big ambitions on a high-voltage network can look every bit as credible as an established platform if the room is ordered, current, and controlled — because what the fund is testing at this stage is whether you handle information like a professional. A shared-drive folder with duplicate PDFs and no access control signals the opposite, no matter how good the underlying site is. The site gets you the meeting; the room decides whether you look like a developer or a broker.

Investors said our data room isn't institutional grade — what's missing for a data centre deal?

Usually it's one of five gaps. First, the grid file is thin or buried — the connection offer should be at the very top, with its gate status (Gate 2 firm versus Gate 1 indicative), capacity in MW, connection date, and milestone terms legible at a glance. Second, the consenting route is ambiguous — no clear statement of local planning versus NSIP, no status, no Section 106 position. Third, land control is asserted not evidenced — the actual option, lease, or title isn't in the room. Fourth, there's no cost-to-complete backed by a real construction cost plan, so the model floats free of the build. Fifth, demand is a hope not a document — no LOI, no pre-let, no credible colocation lease-up plan. Beyond content, the mechanics matter: stale versions circulating, no watermarking on sensitive terms, no access control, and no Q&A discipline all read as amateur. The fix is rarely more documents — it's the right documents, in the right order, current, and controlled. Our data room security questionnaire guide is the checklist a counterparty's own team will run against your room.

We're modelling our raise — what's the typical development cost per MW for a UK hyperscale data centre, and what yield-on-cost do infrastructure funds target?

There is no single honest number, and any source that gives you a precise one without stating what's inside it should be treated with caution. Development cost is normally expressed per MW of IT load and varies materially by specification: what's included changes the figure enormously — land, grid connection and reinforcement works, the shell, mechanical and electrical fit-out, cooling (air versus liquid changes it), and commissioning. UK all-in figures are commonly cited in the region of £9-14m per MW of IT load, but that range is a market-commentary composite, not a fixed benchmark, and you should benchmark your own pro forma against a specialist cost index such as Turner & Townsend's and, critically, confirm what any quoted number includes and excludes before relying on it. On yield-on-cost, the mechanism matters more than a headline figure: development returns come from building to a yield-on-cost above the stabilised exit cap rate for a de-risked, pre-let asset — you create value by taking entitlement, power, and construction risk and crystallising it at a lower cap on exit. The specific spread varies by market, cost of capital, and tenant covenant, so model it from your own inputs rather than importing someone else's number.

Investors keep asking about grid connection before anything else — what do we show them?

Show them the connection offer, and make it the first thing they open. In a UK data centre raise, power is the binding constraint — not land, not the building — and no lender or equity partner funds construction until a firm, dated connection is evidenced. So the crown-jewel document is your grid connection offer, and the single most important fact in it is its gate status: a Gate 2 offer is firm, with a confirmed connection point, capacity, and date, meaning you passed the 'ready' and 'needed' tests under the reform that went live on 10 June 2025; a Gate 1 offer is indicative only. Put the offer letter at the top of the index, and around it place the connection agreement (once accepted), the capacity in MW, the connection date and milestone or liability terms, evidence of your 'ready plus needed' status, and your power strategy — the PPA or supply arrangement, any on-site generation or battery storage, and the energisation programme. That package answers the question they're really asking, which is not 'do you have land?' but 'can this site actually be powered, and when?'

Our energisation date has slipped to 2031 — will investors still fund the project?

A later energisation date isn't automatically a deal-breaker — what investors underwrite is certainty, not speed. A firm, evidenced 2031 date backed by a Gate 2 connection offer, a coherent construction programme, and a matching demand plan is more fundable than a hopeful 2029 date resting on a Gate 1 indication and no pre-let. The reason is that in a supply-constrained market, credibly secured future power is itself the scarce asset; a firm later date is a real, financeable position, while an optimistic earlier one that unravels in diligence destroys trust. What matters is that the date is evidenced end to end — the connection offer's stated date, the milestones to hold it, the build programme that lands on it, and demand that turns up when it does. Present the slippage honestly with the reasons and the mitigations rather than burying it; a bidder who finds a hidden timeline problem re-prices or walks, while one who sees a well-managed timeline gains confidence in the sponsor. The date is a fact to evidence, not a weakness to hide.

Related resources

- Infrastructure Projects Data Room — the general project-finance room this data centre guide builds on

- Data Center Data Room — the US acquisition-side view: powered land vs powered shell, Will-Serve letters

- Renewable Energy Data Room — the power-generation sibling: grid, PPA, and project consents

- Best Data Room Providers UK — the UK provider shortlist and how Peony compares

- Data Room Security Questionnaire — the security evaluation a counterparty's team runs against your room

- Data Centres solutions — the product view for a data centre capital raise

- Family Offices solutions — the buy-side reader on the other side of the table

- Page Analytics — read which investor is genuinely progressing

- NDA Gate — confidentiality acceptance and watermarked disclosure before sensitive terms release

You might also like

Jul 16, 2026

Best Data Room Providers UK (2026): An Honest Buyer's Guide

Jul 16, 2026

Data Room for Infrastructure Projects: The Project-Finance Raise Room (2026)

Jul 12, 2026

Virtual Deal Room: Deal Room vs Data Room + Best Software (2026)