14 Best Software M&A Advisors for $5M–$100M ARR Deals (2026)

Co-founder and CEO at Peony. I built the data room platform with a background in document security, file systems, and AI. Founded Peony in 2021 in San Francisco.

14 Best Software M&A Advisors for $5M–$100M ARR Deals (2026)

Quick answer: For a $5M-$100M ARR B2B SaaS sale, the software-only specialist to know first is Software Equity Group (SEG) — it explicitly targets that exact ARR band and publishes the most-cited SaaS M&A research. For a founder-led, no-conflict process, Vista Point Advisors (FINRA CRD #157502) is exclusively sell-side and never represents buyers. Route by software type: communication software → Q Advisors; business-management / vertical SaaS → SEG and Union Square Advisors; cloud / enterprise software → Shea & Company and AGC Partners (with Tequity for the Salesforce/ServiceNow/SAP/Oracle partner ecosystem); fintech → FT Partners; cybersecurity → Momentum Cyber. Below ~$5M ARR, a curated marketplace (FE International, Empire Flippers, Quiet Light) usually beats a full boutique process. Above ~$100M-$250M EV, step up to a bank (Houlihan Lokey, William Blair, Baird, Harris Williams). Pick by software sub-vertical and deal size, not by logo.

This is the software-only cut. For the broad tech map — including IT services, hardware, and the city benches — see our technology & software M&A hub. This page is the software/SaaS-only slice of that hub: it goes deeper on software-only sell-side specialists and on sub-vertical routing (which specialist for communication software vs cloud vs vertical SaaS vs fintech vs security), and it names the honest marketplace tier below $5M ARR and the bank tier above ~$100M EV. No firm here is ranked against the other sectors; it is ranked against your software type and your ARR.

Last updated: July 2026

TL;DR: Software M&A splits by software sub-vertical and by deal size — the specialist map above is the whole game. What the map can't show is the traps: TripleTree is Capital One-owned (not independent), DBO Partners was absorbed by Piper Sandler in 2022, a marketplace listing is not a run auction, and a 6.3x average multiple is not the ~3.1x median most sellers should actually plan around. Verify registration on BrokerCheck before you sign — only two boutiques on this page carry a printed CRD, and that is deliberate.

Why I wrote this — and how it differs from our tech hub

I'm Deqian Jia, co-founder of Peony, a data room company used by 5,900+ customers. I spend most of my time on the part of our product that decides who — and now what — is allowed to read a confidential document, which means I sit on the document side of a lot of software sales: bootstrapped vertical-SaaS exits, founder-led application-software deals, cloud and enterprise-software carve-outs, fintech transactions, and security tuck-ins. Software is the sector where picking the wrong type of advisor costs the most, because so much of the value is metric-specific and sub-vertical-coded — a communication-software seller and a vertical-SaaS seller are shopping for genuinely different firms.

We already publish a broad technology & software M&A hub that maps the whole sector — SaaS, infrastructure and data/AI, cybersecurity, fintech, IT services, and the bulge-bracket ceiling, plus the city benches. This page is the software-only cut of that hub. It deliberately does not re-run the broad map. Instead it goes deeper on two things the hub only touches: the software-only sell-side specialists a $5M-$100M ARR founder actually shortlists (SEG, Vista Point, Corum, Founders), and the sub-vertical routing — which specialist to call for communication software, business-management/vertical SaaS, cloud/enterprise software, fintech, and security — plus the honest tiers on either side of the boutique band: the marketplaces below $5M ARR and the banks above ~$100M EV. If you sell IT services, MSP, or hardware, or you want the geo cut for a specific city, the tech hub is the better starting point.

One framing note before the roster. The buyer reality in software is that you will most likely sell to private equity: PE and VC-backed buyers were about 60% of SaaS M&A deals in 1Q26 (SEG). That should shape which advisor you hire — you want one whose Rolodex is full of the sponsors rolling up your category. And to be clear about scope: Peony is not an M&A advisor and does not place deals — the firms below do that. Peony is the data-room layer founders and bankers run the process on; I will flag where that fits, but the advisory firms are the subject here.

Who are the best software M&A advisors for a $5M–$100M ARR company?

For a $5M-$100M ARR B2B SaaS seller, the working core is a set of pure-play, sell-side software specialists — firms whose entire practice is selling software companies, who speak SaaS metrics natively, and who carry a current map of the PE platforms and strategics buying in your category. The six firms below are that core; the sub-vertical kings and the surrounding marketplace and bank tiers come after.

Software Equity Group (SEG) is the software-only specialist most lower-middle-market SaaS founders should know first, and it is the closest thing to an exact match for this reader. Based in San Diego and founded in 1992, SEG is a sell-side-only M&A bank for B2B software, SaaS, and AI companies, and it explicitly targets the $5M-$100M ARR band — so if you are an $8M or $30M ARR founder, you are inside its stated sweet spot, not below its floor. SEG is also the category's most-cited research voice: it publishes the SEG SaaS Index and widely-read quarterly and annual SaaS M&A reports, the proprietary dataset most other analysts triangulate against. For a founder who wants a senior, software-only team running a process built around SaaS metrics, SEG is best-in-class. (On registration: do not take a CRD from a listicle — verify SEG's current registration on BrokerCheck before engaging.)

Vista Point Advisors (San Francisco) is the archetype of the no-conflict, exclusively sell-side software boutique — and the answer to the founder's fear that a banker who also serves PE buyers will not fight hard enough on price. Vista Point is a founder-led software and internet boutique (founder Michael Lyon, 30-plus years in tech investment banking) that never represents buyers, so it has no buy-side relationship to protect and its advice on your sale is structurally unconflicted. It is one of the few boutiques whose registration you can cite with confidence: FINRA CRD #157502. For a founder- or family-owned SaaS company that wants a sell-side-only advocate, Vista Point is the reference name on the conflicts axis.

Corum Group (Bothell, Washington, in the Seattle area) is the veteran "sell your software company" firm — and, contrary to a persistent rumor, it is alive and active in 2026, with 290 lifetime deals as of June 2026 (276 M&A plus 14 fundings). Corum's distinctive model is education-led: it runs Merge Briefing seminars and "Selling Up, Selling Out" bootcamps and a monthly Tech M&A webcast, which double as a funnel and a founder-education resource. Its fee model is a monthly retainer plus a success fee, with no break-up fee. For a first-time software-founder seller who wants a firm that will also teach them the process, Corum is a natural fit. (Verify current registration on BrokerCheck before engaging.)

Founders Advisors (Birmingham, Alabama; established 2003) is the specialist for founder- and family-owned companies, including SaaS, and one of the few boutiques whose securities registration you can cite: securities are offered through Founders M&A Advisory LLC (BrokerCheck firm #269926, member FINRA/SIPC). The firm has advised on roughly 188 deals by its own count and carries a bench of about 57 professionals. For a founder-owned SaaS business — especially outside the coastal tech hubs — that wants a sell-side team fluent in the founder-liquidity conversation, Founders Advisors is a credible, verifiable choice.

Shea & Company (Boston, founded 2005) is a software-only investment bank for the middle market — but it is honestly a top-of-band option for this reader, not an entry point. Shea works a $25M-$500M enterprise-value band, which means a $5M-ARR seller (very roughly $15M-$25M EV) sits below its floor; you would fit Shea once you are at the larger end of this guide's ARR range. Shea cites $50B+ in completed transactions (attribute that to industry trackers) and closed 16 deals in 2025, including Raken's sale to Sverica (September 2025). Its government-software franchise is a standout — 30-plus deals and $12B+ over five years. For a scaled software company at the upper end of the lower-middle market, Shea's software-only focus and senior-led deal teams make it a reference name.

AGC Partners (Boston) is the high-volume, tech-only boutique with real software depth across a $25M-$1B band. AGC states it is the #1 most-active tech boutique by deal volume from 2009 through 2025 (attribute that claim — it is self-reported), and it closed 28 tech deals in 2025, split 14 PE-platform and 14 strategic — a near-perfect illustration of why a software seller needs a banker fluent in both buyer types. Named 2025-26 deals include Protecht's $280M growth investment from PSG, GetVisibility's sale to Forcepoint, and Booz Allen's acquisition of Defy Security; AGC also claims 145 security transactions. For a $25M-$1B software company that wants a well-connected, high-throughput process, AGC is a strong choice.

What's the software M&A specialist landscape in 2026? (the map)

The table below is the map for the whole software-specialist landscape this guide covers — the pure-play core, the sub-vertical kings, and the tiers on either side. Each firm is profiled in its section; this is the at-a-glance routing.

| Firm | HQ | Band | Registration status | The tell (who it's for) |

|---|---|---|---|---|

| Software Equity Group (SEG) | San Diego | $5M-$100M ARR | Verify on BrokerCheck | The exact-match sell-side-only SaaS bank + the SEG SaaS Index |

| Vista Point Advisors | San Francisco | Lower-middle SaaS | FINRA CRD #157502 | No-conflict, exclusively sell-side, founder-led |

| Corum Group | Bothell, WA | LMM software | Verify on BrokerCheck | Veteran "sell your software company" firm; education model; no break-up fee |

| Founders Advisors | Birmingham, AL | LMM incl. SaaS | Founders M&A Advisory #269926 | Founder/family-owned focus, verifiable registration |

| Shea & Company | Boston | $25M-$500M EV | Verify on BrokerCheck | Software-only, top-of-band; a $5M-ARR seller is below its floor |

| AGC Partners | Boston | $25M-$1B EV | Verify on BrokerCheck | High-volume tech-only; 14 PE / 14 strategic in 2025 |

| Union Square Advisors | San Francisco | ~$100M+ EV | Verify on BrokerCheck | Vertical-software specialist; does BOTH sell- and buy-side; independent |

| GP Bullhound | London + SF/NY | Global tech | Verify by jurisdiction | Global tech IB; internet/ecommerce/cloud/AI; $35B+ recent value |

| Drake Star Partners | Global (NY/EU) | Global TMT | Verify by jurisdiction | Broad TMT + gaming; Boutique TMT Bank of the Year (Feb 2025) |

| Tequity Advisors | Toronto | Sell-side | Likely CIRO (not FINRA) | The Salesforce/ServiceNow/SAP/Oracle partner-ecosystem niche |

| Q Advisors | Denver | Comms/digital-infra | Verify on BrokerCheck | THE communication-software answer; UCaaS/CPaaS/CCaaS |

| Bank Street Group | Stamford, CT | Digital infra | Verify on BrokerCheck | Digital-infrastructure-first — not a UCaaS-app specialist |

| FT Partners | San Francisco | Mid-cap-$5B+ | Verify on BrokerCheck | Fintech-only (its self-description); ex-Goldman founder |

| Momentum Cyber | San Francisco | Cyber, all sizes | Verify on BrokerCheck | Cybersecurity-only; independent (NOT acquired) |

A few notes the table cannot carry. SEG and Vista Point are the two names a $5M-$100M ARR founder should shortlist first — SEG for the exact ARR-band fit and research depth, Vista Point for the no-conflict, sell-side-only thesis. Shea is a top-of-band step-up, not an entry point. The sub-vertical kings matter enormously: if you sell communication software, fintech, or security, the specialist in that niche belongs on every pitch list regardless of the general-purpose boutiques. And the registration column is deliberately conservative — I print a CRD only for Vista Point and Founders, because those are the two I can verify; for everyone else, "verify on BrokerCheck" is the honest instruction, not a knock.

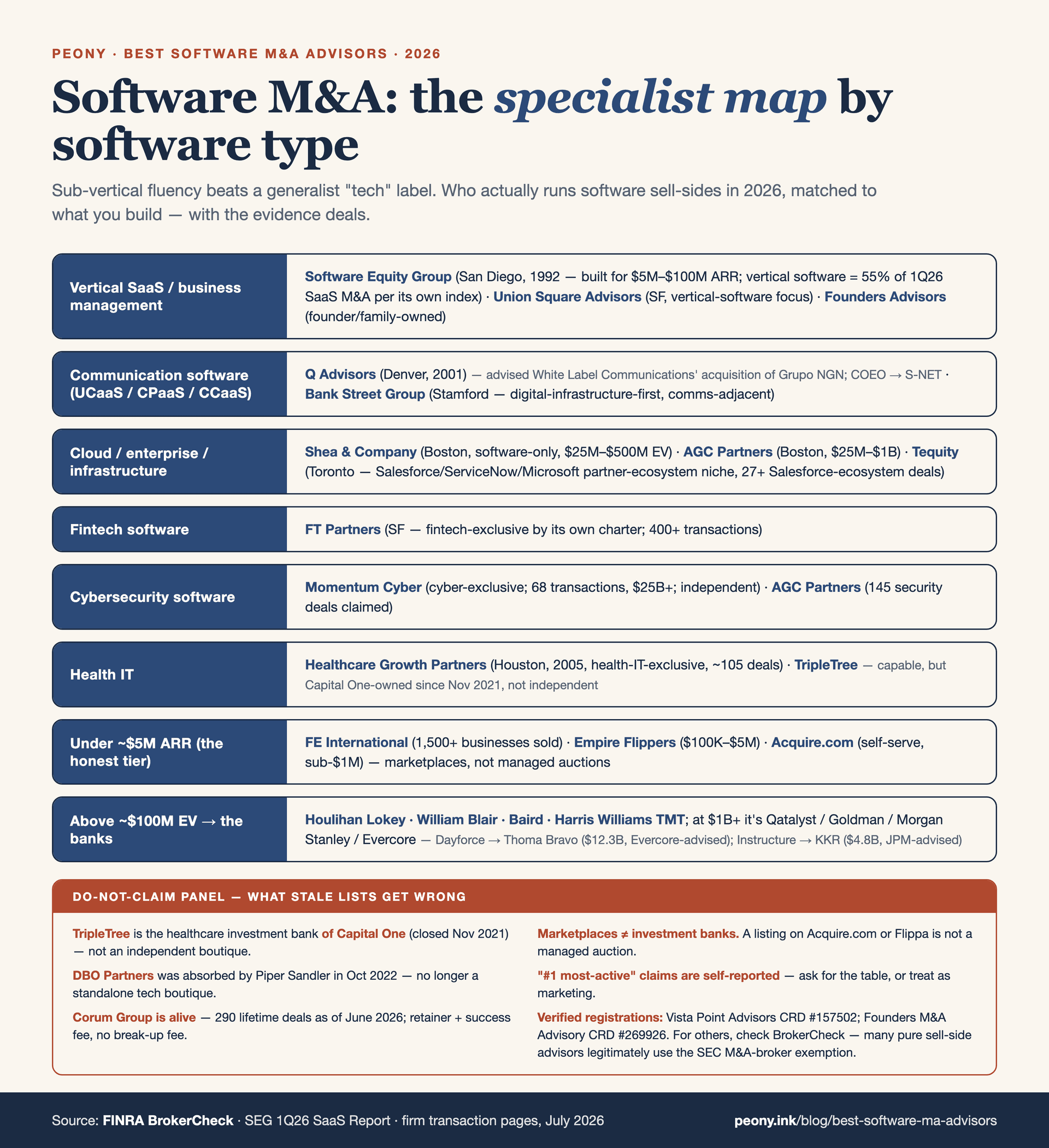

Which software M&A specialist fits my sub-vertical? (the routing table)

This is the heart of the software-only cut, and the part the broad tech hub does not do at this resolution. Match your software type to its specialist and to a piece of evidence — a named deal or a stated focus — that proves the fit.

| Software type | Specialist(s) | Evidence / the tell |

|---|---|---|

| Communication software (UCaaS/CPaaS/CCaaS) | Q Advisors (digital-infra boutique, since 2001) | White Label Communications' acquisition of Grupo NGN; COEO → S-NET |

| Digital infrastructure (comms/media/tech) | Bank Street Group | 185+ deals; Vero Networks $500M — infra-first, not UCaaS-app |

| Business-management / vertical SaaS | SEG; Union Square Advisors | Vertical software = 55% of 1Q26 SaaS M&A (SEG); Union Sq. Conservice → TPG (Dec 2025) |

| Founder/family-owned vertical SaaS | Founders Advisors | ~188 deals (firm-stated); securities via Founders M&A Advisory #269926 |

| Cloud software (enterprise/infrastructure) | Shea & Company; AGC Partners | Shea enterprise/infra core; AGC $25M-$1B band |

| Cloud-partner ecosystem (Salesforce/ServiceNow/SAP/Oracle) | Tequity Advisors | 27+ Salesforce-ecosystem deals; Toronto, sell-side-focused |

| Enterprise software (broad) | Shea, AGC, Union Square + the bank tier | Shea $25M-$500M EV; AGC $25M-$1B; Union Sq. $118B+ aggregate |

| Fintech / payments software | FT Partners | "The only IB focused exclusively on fintech" (its self-description); 400-500 transactions |

| Cybersecurity software | Momentum Cyber | 68 cyber transactions / $25B+; publishes the Cybersecurity Almanac; independent |

| Global / cross-border TMT | GP Bullhound; Drake Star | GP Bullhound $35B+ recent value; Drake Star TMT Bank of the Year (Feb 2025) |

Who is the best communication software M&A advisor?

For communication software — UCaaS, CPaaS, CCaaS, and the surrounding telecom-software stack — the specialist to call first is Q Advisors (Denver), a communications and digital-infrastructure boutique formed in 2001. Q Advisors lives in exactly this corner of the market, and its deal record shows it: it advised on White Label Communications' acquisition of Grupo NGN (a UCaaS/CPaaS/CCaaS transaction) and COEO on its sale to S-NET (UCaaS/CCaaS/SD-WAN). If your product is a communications application or platform, Q Advisors' relationships among the strategics and sponsors consolidating comms software are the point.

The infrastructure-adjacent option is Bank Street Group (Stamford, Connecticut; founded 2002), a digital-infrastructure bank (communications, media, and technology) with 185+ deals and transactions like Vero Networks ($500M). The honest nuance: Bank Street is digital-infrastructure-first, not a UCaaS-application specialist — it is the right call if your company sits closer to the network and infrastructure layer than the app layer, and I position it that way rather than overselling it as a pure communication-software shop. For a broad-TMT alternative that also covers communications alongside the rest of media and tech, Drake Star Partners is a credible global option.

Who is the best business management software / vertical SaaS M&A advisor?

For business-management software and vertical SaaS, the two names to know are SEG and Union Square Advisors — and the market context tells you why this category matters so much right now: vertical software was about 55% of 1Q26 SaaS M&A, up from 49% (SEG's own report). SEG works the exact $5M-$100M ARR band most vertical-SaaS founders occupy and markets your vertical's specific metrics. Union Square Advisors (San Francisco, founded 2007) is explicitly vertical-software-focused, with 170-plus transactions and $118B+ in aggregate value, deep coverage across sub-verticals (it covers 500+ govtech companies across 24 sub-verticals alone), and recent proof like Conservice's sale to TPG (December 2025). For a founder- or family-owned vertical-SaaS company specifically, Founders Advisors is the third name — its whole practice is oriented around founder-owned businesses. Union Square is the one firm in this trio that does both sell-side and buy-side, so if the no-conflict question matters to you, ask it directly (and see the conflicts section below).

Who is the best cloud software M&A advisor?

For cloud software — enterprise and infrastructure software delivered as a cloud platform — the specialists are Shea & Company (its enterprise and infrastructure-software coverage is a core franchise) and AGC Partners (which works the $25M-$1B band with deep enterprise-software relationships). The niche within the niche worth naming: if your company is built on top of a cloud platform's partner ecosystem — a Salesforce, ServiceNow, Microsoft, SAP, or Oracle ISV or SI — the specialist is Tequity Advisors (Toronto), a sell-side-focused boutique that owns the partner-ecosystem lane and has closed 27+ Salesforce-ecosystem deals. (Tequity is Canadian and therefore likely CIRO-regulated, not FINRA — so I do not print a US CRD for it; confirm its registration directly.) For a scaled cloud-software seller above this guide's band, the bank tier (Houlihan Lokey, William Blair) takes over.

Who are the best enterprise software M&A advisors?

For enterprise software broadly, the strongest specialists are Shea & Company (software-only, $25M-$500M EV), AGC Partners ($25M-$1B, high volume), and Union Square Advisors (vertical and enterprise software, $118B+ aggregate) — with the big-bank tier (Houlihan Lokey, William Blair, Baird) taking over above roughly $100M-$250M EV, and the elite desks (Qatalyst, Goldman, Morgan Stanley, Evercore) at $1B+. The routing inside "enterprise software" is mostly a size question: a $25M-$100M EV enterprise-software deal is boutique territory (Shea at the top of the band, AGC across it); a $250M+ deal wants a bank with financing and broader buyer reach. The marquee proof at the top frames the ceiling — Dayforce's sale to Thoma Bravo at roughly $12.3B (announced August 2025; Evercore was exclusive advisor to Dayforce) and Instructure's sale to KKR at $4.8B (J.P. Morgan lead advisor) — but those are bank-and-elite-boutique deals, not the boutique band this guide centers on.

What's the honest tier below $5M ARR — marketplaces and micro-SaaS?

Below about $5M ARR, the economics flip: a full boutique process, with its retainer and minimum fee, consumes too much of the proceeds, and the right venue is usually a curated marketplace or a self-serve platform rather than a managed auction. The important honesty here is that a marketplace listing is not a run auction — you are getting exposure and matchmaking, not a banker quietly creating competitive tension among a curated buyer list — so calibrate expectations accordingly.

The segmentation by deal size:

| Deal size | Best venue | What you're actually getting |

|---|---|---|

| Under $100K | Acquire.com; Flippa | Self-serve listing / marketplace ($5K-$100K on Flippa; sub-$1M self-serve on Acquire) |

| $100K-$1M | Empire Flippers; Acquire.com | Curated marketplace ($100K-$5M curated on Empire Flippers) |

| $250K-$5M | Empire Flippers; FE International; Quiet Light | Broker-marketplace with more hands-on process (~$250K-$5M) |

| $5M+ ARR | Managed boutique process | A real sell-side process (SEG, Vista Point, etc.) |

FE International (New York/Miami/London) is the most process-heavy of the marketplaces, focused on SaaS, ecommerce, and content businesses, with 1,500+ businesses sold and roughly $1B in aggregate transaction value. Empire Flippers runs a curated marketplace in the roughly $100K-$5M range; Quiet Light operates in the roughly $250K-$5M band; Acquire.com is self-serve and strongest sub-$1M; and Flippa covers the smallest tier, roughly $5K-$100K. All of these are brokers or marketplaces, not managed-process investment banks — which is exactly right for a micro-SaaS, and exactly wrong for a $20M ARR company that needs a competitive process. If you are near the $5M ARR line, the honest move is to get quotes from both a marketplace and a boutique and compare not just the fee but the process each will actually run.

When should I use a bank instead of a boutique (above ~$100M–$250M EV)?

Once a software deal climbs above roughly $100M-$250M in enterprise value, the calculus shifts toward a full-service or elite bank — for the financing access, the broader buyer reach, the public-company and stock-deal mechanics, and the senior-relationship coverage that a boutique cannot always match. The workhorses in that band are Houlihan Lokey, William Blair, Baird, Harris Williams (strong in TMT and govtech), Raymond James, and Piper Sandler. Two consolidation facts to keep straight so you do not shortlist a firm that no longer exists as an independent: Piper Sandler absorbed DBO Partners in October 2022 (so DBO is not a standalone option), and Piper also acquired G Squared Capital Partners, a DC-area government- and defense-tech boutique, on September 12, 2025.

At $1B+, the defaults become the elite boutiques and bulge brackets — Qatalyst, Goldman Sachs, Morgan Stanley, Evercore, and J.P. Morgan — for mega-buyer relationships and public-company mechanics. The marquee proof frames that ceiling: Dayforce → Thoma Bravo at ~$12.3B (announced August 2025; Evercore exclusive advisor to Dayforce) and Instructure → KKR at $4.8B (J.P. Morgan lead advisor to Instructure). The reason these are the wrong default for a $5M-$100M ARR seller is fit, not quality — your deal would be their smallest mandate of the quarter, staffed thin, while a software boutique with a live PE-platform Rolodex fights for it. The full ceiling, including the biggest tech deals, is in our tech M&A hub.

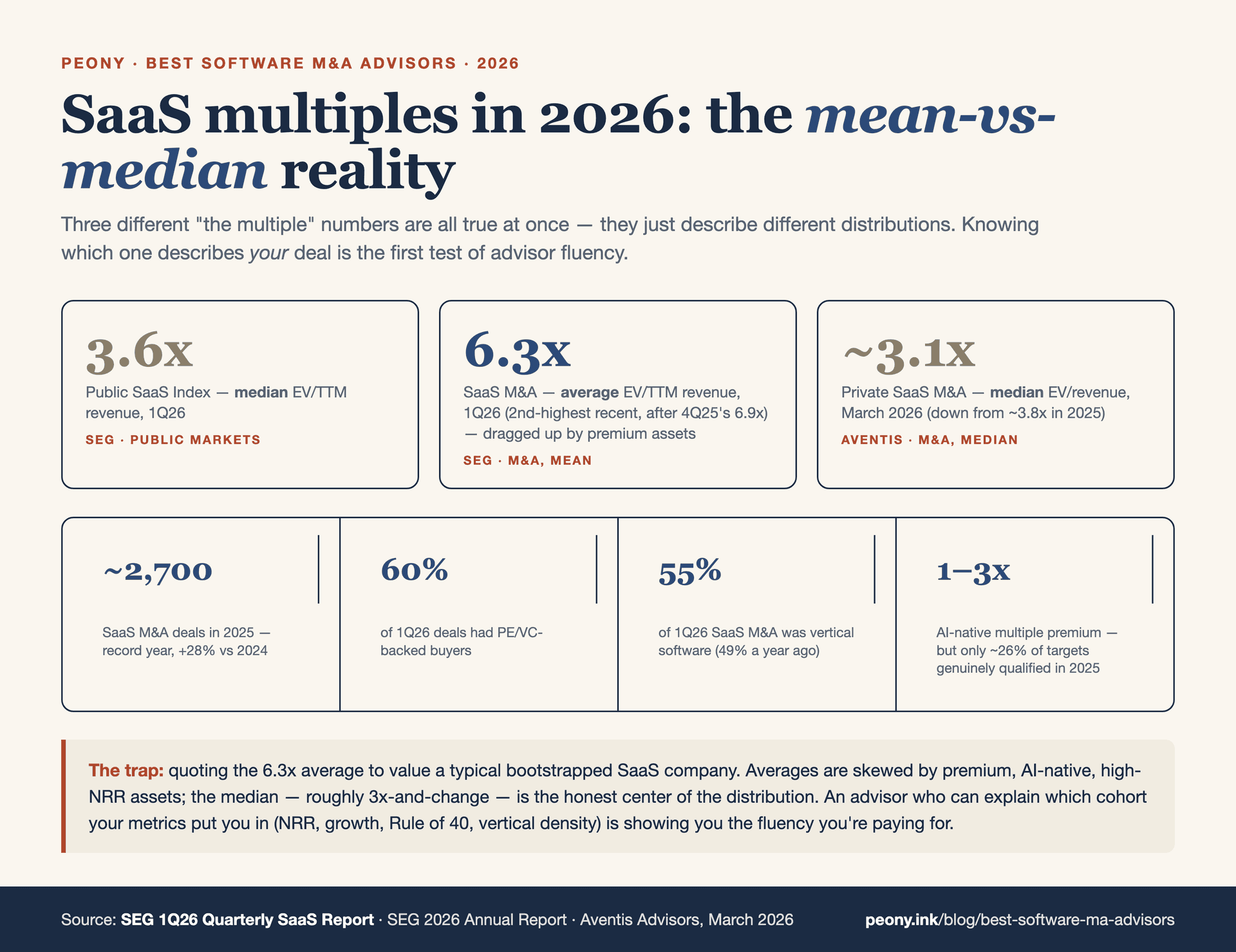

What software M&A multiples are realistic in 2026 — average vs median?

The single most important discipline in reading 2026 software multiples is to never conflate the average with the median, because premium assets skew the average sharply upward. Here are the anchors, labeled explicitly. On an average basis, SaaS M&A in 1Q26 cleared at about 6.3x EV/TTM revenue (SEG), the second-highest recent reading after 4Q25's 6.9x — and the gap between that and the public-market multiple reflects M&A buyers paying up for quality. On a median basis, private SaaS M&A ran closer to about 3.1x EV/revenue in March 2026 (Aventis Advisors), down from about 3.8x in 2025. For public SaaS as a reference point, SEG's public SaaS Index sat at a median EV/TTM revenue of 3.6x in 1Q26. So the honest planning range for a typical, steadily-growing private SaaS seller is anchored on the ~3.1x median, with the 6.3x average reserved for genuinely premium, high-growth assets.

Three more calibrations. First, deal volume is at record highs, which is good news for sellers: SEG counts about 2,700 SaaS deals in 2025 (a record, up ~28% vs 2024), and 659 SaaS M&A deals in 1Q26 with a trailing-twelve-month figure of 2,723 (+24% YoY). PE and VC-backed buyers were about 60% of 1Q26 deals (about 58% across FY2025), and vertical software was 55% of 1Q26 SaaS M&A — so a vertical-SaaS seller is selling into an actively consolidating buyer set. Second, the AI premium is real but narrow: AI-native SaaS can command a 1x-3x multiple premium (SEG Research), and 72% of 2025 deals referenced AI in the target's positioning — but only about 26% of evaluated targets qualified as genuinely AI-driven in 2025, so most sellers will not clear that bar honestly. Third, ignore the froth: the 15x-45x ARR figures you see are frothy private VC-round valuations, not M&A comparables — do not anchor your exit on them. For profitability context, the median EBITDA margin across the SEG SaaS Index was about 9.1% in FY2025.

How do I verify a software M&A advisor is legit and unconflicted?

Verification comes down to three checks, and doing them before you sign an engagement letter is the cheapest insurance you can buy. First, registration. Look the firm up on FINRA BrokerCheck or with your state securities regulator. Two firms in this guide have registrations you can confirm directly — Vista Point Advisors is FINRA CRD #157502, and Founders' securities are offered through Founders M&A Advisory LLC (BrokerCheck firm #269926) — and for every other firm you should look it up rather than trust a listicle. Crucially, "not on BrokerCheck" is not automatically a red flag: Congress codified an SEC M&A-broker exemption in 2023, and some legitimate pure sell-side advisors operate under it rather than as registered broker-dealers. The right move is to ask which basis a firm operates under and get the answer in writing.

Second, subsector and process fit. Ask each firm to name the five buyers it would call first for your specific product, how many software deals it has closed in your exact sub-vertical and ARR band in the last 18 months, and whether those went to strategics or to sponsors. A genuine specialist answers instantly; a generalist gives you categories. Watch for a "software practice" that is really IT-services or MSP work — ask to see the SaaS deal sheet specifically. And treat self-reported superlatives ("#1 most active," "the only firm that…") as claims to attribute, not facts — AGC's most-active claim and FT Partners' "only fintech-exclusive bank" description are both firm self-descriptions.

Third, conflicts. Ask whether the firm is exclusively sell-side or also represents buyers, whether it has done buy-side work for any of the specific PE platforms likely to bid on you, and how it walls off and discloses conflicts. Vista Point's never-represent-buyers model is the clean archetype; a both-sides firm like Union Square is not disqualified, but you should ask. The full intermediary-type decision — advisor vs broker vs bank, and the licensing line between them — is in our advisor vs broker vs investment bank hub, and the fee mechanics are in our M&A advisor fees hub.

What are the traps in a "best software M&A advisor" list?

Every directory-style list repeats the same avoidable errors. Here are the ones that matter, and the correct facts:

- TripleTree is not independent. It is the healthcare investment bank of Capital One (the acquisition closed November 2021). It has advised on 275+ deals since 1997 and does real health-IT work, but brand it correctly — it is Capital One-owned, not an independent boutique.

- DBO Partners is not a standalone firm. Piper Sandler absorbed DBO Partners in October 2022. Do not shortlist it as an independent option.

- Momentum Cyber is independent — and it is not DBO. Momentum Cyber (cybersecurity-exclusive, 68 cyber transactions / $25B+, publisher of the Cybersecurity Almanac) has not been acquired. Do not confuse it with DBO.

- Union Square Advisors is independent. It has not been acquired; it still operates as an independent, vertical-software-focused bank.

- Corum Group is alive and active. Despite periodic rumors, Corum reports 290 deals as of June 2026 — it is very much operating.

- Marketplaces are not banks. Acquire.com, Flippa, Empire Flippers, and Quiet Light are brokers or marketplaces, not managed-process investment banks. A listing is not a run auction.

- "#1 most active" is self-reported. Attribute superlatives to the firm claiming them, or drop them.

- A "software practice" may be IT-services work. Verify the SaaS deal sheet before you believe the label.

- Mean is not median. A 6.3x average multiple is not the ~3.1x median most sellers should plan around — conflating them sets false expectations.

- VC-round AI multiples are not M&A comps. Frothy 15x-45x ARR private-round numbers do not price an M&A exit.

- Registration nuance is real. Some legitimate pure sell-side advisors operate under the 2023 SEC M&A-broker exemption. Confirmed registered here: Vista Point (CRD #157502) and Founders M&A Advisory (#269926); for everyone else, check BrokerCheck or state records rather than asserting.

Where does Peony fit in a software sale?

Whichever advisor wins your mandate, the process runs out of a data room — and in software the room carries unusually sensitive material: customer-level ARR and churn data, source-code references, security attestations, and a full contract set. We built Peony, a data room company used by 5,900+ customers, to be the deal-infrastructure layer under whichever advisor you hire: per-bidder data rooms so strategics and sponsors see only what they should, per-page watermarks on every render to deter leaks, dynamic NDA gating before access, and page-level analytics that show your banker which buyers actually read the CIM and which scenarios they stressed. That last capability matters in a dual-track process — the engagement data is how you and your advisor tell a serious bidder from a tire-kicker. Our /solutions/ma page and pricing cover the deal-specific setup.

Two honest scoping notes. Peony is not an M&A advisor and does not place deals — the firms above do that; Peony is the layer that makes the diligence run cleanly once you have hired one. And on VDR selection specifically: Datasite and Intralinks are built for the $500M+ processes, while Peony, iDeals, and FirmRoom serve the sub-$500M band where nearly all $5M-$100M ARR software deals actually close — so for the deals this guide is about, the enterprise VDRs are usually over-tooled. For the software-specific room buildout, see our SaaS M&A data room guide and the m-and-a-data-room playbook; and because SaaS diligence increasingly turns on a live metrics model, our guide to sharing a financial model with an investor covers presenting your ARR and cohort model interactively without losing control of the file. Peony serves 5,900+ customers on exactly this document layer.

The bottom line

Software M&A is not one league table — for a $5M-$100M ARR seller it splits by software sub-vertical and by deal size. Start with SEG (the exact ARR-band fit and the SaaS-research standard) and Vista Point (the no-conflict, sell-side-only advocate). Route by type: communication software → Q Advisors; business-management / vertical SaaS → SEG and Union Square (Founders for founder-owned); cloud / enterprise software → Shea and AGC, with Tequity for the cloud-partner ecosystem; fintech → FT Partners; security → Momentum Cyber. Below ~$5M ARR, a curated marketplace usually beats a boutique; above ~$100M-$250M EV, step up to a bank (Houlihan Lokey, William Blair, Baird, Harris Williams). Plan your multiple around the ~3.1x median, not the 6.3x average. Verify registration (Vista Point CRD #157502; Founders M&A Advisory #269926; everyone else on BrokerCheck), screen hard for conflicts and real sub-vertical closings, and walk into diligence with a data room and metrics that already tie out — because preparation is the one input that pays you back on both timeline and price. For the broad tech map, IT-services and hardware benches, and the city cuts, see the parent technology & software M&A hub.

Related resources

- 13 Best Technology & Software M&A Advisors — the parent hub this page carves from: the broad tech map (SaaS, infrastructure & data/AI, cybersecurity, fintech, IT services, hardware) plus the bulge-bracket ceiling and the city benches

- Best Financial Services M&A Advisors — the fintech-software adjacency: where payments and financial-technology software overlaps the financial-services advisor bench

- 16 Best Healthcare M&A Advisors by Subsector — the health-IT adjacency: HCIT/healthtech SaaS sellers who need both software fluency and healthcare relationships

- M&A advisor vs broker vs investment bank — the decision that comes before this shortlist: which of the three intermediary types should sell your software company

- M&A advisor fees: what you actually pay — Modified-Lehman and Double-Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the base

- How to write a CIM — the confidential information memorandum a software banker builds around your ARR bridge and NRR cohorts

- SaaS M&A data room: 2026 guide — the software-specific data-room buildout, with the ARR bridge and NRR cohorts buyers expect

- M&A data room: setup and workstream mapping — the general sell-side data-room playbook

- Data-room analytics: how to spot serious buyers — reading buyer intent from engagement data during a targeted process

- Share a financial model with an investor — presenting your SaaS metrics model interactively without losing control of the file

- Best M&A Advisors in San Francisco — the Bay Area geo cut, where SEG, Vista Point, Union Square, FT Partners, and Momentum Cyber sit

- Best M&A Advisors in Austin — the geo cut for the growing Texas software-founder base

- Best M&A Advisors in Seattle — the geo cut where Corum Group is headquartered

Frequently asked questions

I run an $8M ARR vertical SaaS company — am I too small for SEG or Vista Point?

No — an $8M ARR vertical SaaS company sits squarely inside the sweet spot for both firms, and that is the single most useful fact for this reader. Software Equity Group (SEG) explicitly targets B2B software and SaaS companies in the $5M-$100M ARR range, which puts an $8M ARR business near the middle of its stated band, not below its floor. Vista Point Advisors (FINRA CRD #157502) is a founder-led, exclusively sell-side software and internet boutique built precisely for founder- and family-owned companies at lower-middle-market scale. Where you would genuinely be too small is for a software-only bank whose floor starts higher — Shea & Company works a $25M-$500M enterprise-value band, so an $8M ARR seller (very roughly $25M-$50M EV at a healthy multiple) is at or below Shea's floor, and I say that plainly so you do not waste a pitch. The honest filter is not the logo but the process: an $8M ARR founder wants a senior, sell-side-only team that markets your SaaS metrics and runs a tight process to the handful of PE platforms and strategics actually buying in your vertical. Ask each firm how many deals it closed in your ARR band and your sub-vertical in the last 18 months. We run Peony, a data room company used by 5,900+ customers, and across hundreds of software processes the firms that engage seriously are the ones that can answer that without hesitating.

Should I hire a software-specialist M&A bank or a generalist tech investment bank?

For a SaaS seller, a software specialist almost always beats a generalist tech bank, and the reason is mechanical, not snobbery. Software value is priced off your ARR base, your net revenue retention (NRR) and gross revenue retention (GRR), your growth-plus-margin profile (the Rule of 40), and the durability of your recurring revenue — not off a trailing EBITDA multiple. A generalist who runs a blunt EBITDA process under-credits exactly the things that earn a software premium: high NRR, low logo churn, expansion revenue, and a clean ARR bridge. Just as costly, a generalist rarely has direct lines to the specific PE platforms consolidating your category, and in software the buyer set is overwhelmingly private equity — PE and VC-backed buyers were about 60% of SaaS M&A deals in 1Q26 (SEG). A true software specialist — SEG, Vista Point, Corum, Shea, AGC, Union Square — lives in that buyer universe and speaks the metric language fluently. The honest exception: if your single most likely buyer is a strategic your CEO already knows well, a trusted generalist or a direct negotiation can sometimes win, because competition, not the banker's logo, moves price. But the default for a $5M-$100M ARR seller is a specialist. Note also that some pure sell-side software advisors operate legitimately under the SEC M&A-broker exemption Congress codified in 2023 rather than as registered broker-dealers — that is not a red flag by itself, but you should still verify registration (see the vetting section below). This is the software-only cut of our broader tech M&A hub, which covers the generalist-vs-specialist decision across all of technology.

Two PE firms and a strategic already reached out — do I still need an M&A advisor?

In almost every case, yes — and inbound interest is exactly the situation where an advisor pays for itself. Two PE platforms and a strategic feels like a competitive field, but until they are bidding against each other on a clock, it is three separate one-on-one negotiations, and a one-on-one negotiation is the one structure guaranteed to leave money on the table. The buyers who approached you do this for a living and run dozens of deals a year; most founders sell once. A sell-side software advisor turns inbound interest into a real process: it quietly adds the other platforms and strategics buying in your category, sets a bid deadline so the parties compete, and negotiates not just price but structure — rollover equity, earnouts, escrow, employment and non-compete terms, and the working-capital peg. The advisor also runs the confidential diligence so you can keep operating the company. The narrow case where going direct can work is a single trusted strategic offering a genuine premium plus a fairness check from a software-literate M&A attorney and a quality-of-earnings accountant — but even then, quiet competitive tension usually improves the terms. The intermediary-type decision sits upstream in our M&A advisor vs broker vs investment bank guide.

Should I run a full sell-side process or negotiate directly with the inbound buyers?

Run a process — but it does not have to be a wide, noisy auction to work. The core principle is that competition sets price, so the goal is to create credible competitive tension even when only inbound buyers approached you. There is a spectrum. A broad auction (dozens of parties) maximizes competition but raises confidentiality risk and takes longer. A targeted process (a curated shortlist of the 8-15 platforms and strategics genuinely active in your category, run behind a clickthrough NDA on a bid deadline) captures most of the price benefit with far less leakage — and for a $5M-$100M ARR software seller that is usually the right shape. A direct negotiation with a single inbound party is the weakest structure on price, and should only be chosen when a specific strategic is offering a premium you do not expect a process to beat and speed or confidentiality matters more than squeezing the last dollar. The practical move: hire an advisor who can run a tight, targeted process and show recent closings into both PE and strategic buyers, then let the inbound parties compete inside it rather than picking them off one at a time. To read which bidders are genuinely working your file, our data-room analytics guide covers the engagement signals that separate serious buyers from tire-kickers.

Do software M&A advisors actually understand SaaS metrics like NRR and the Rule of 40?

The genuine software specialists do — it is the core of what you are paying for — but plenty of firms wearing a 'tech' or 'software practice' label do not, so you have to test for it. A real software banker will separate recurring ARR from services and one-time revenue and defend a higher multiple on the durable, high-retention portion; will bridge your GAAP revenue, billings, and ARR (three different numbers) so a buyer's accountants cannot open a gap in the quality-of-earnings review; and will present net revenue retention as a trailing-12-month trend with the gross revenue retention underneath it and the cohort and customer-concentration detail — not a single point-in-time figure a buyer can discount. NRR is the SaaS equivalent of a reserve report: a high NRR driven by one or two accounts gets marked down for concentration risk, and a banker who does not surface that will lose ground. The screening test is simple: ask each advisor to walk through how they would bridge your GAAP revenue to ARR, how they would present your NRR cohorts to a skeptical buyer, and how the Rule of 40 (growth rate plus profit margin) shapes your positioning. Firms like SEG — which publishes the SEG SaaS Index and quarterly SaaS M&A research — do this in their sleep; a generalist reciting the acronyms without the mechanics is the tell. Broader software-metric context for all of technology is in our tech M&A hub.

Is it a conflict of interest if my sell-side advisor also does buy-side work for PE firms?

It can be, and it is worth understanding rather than assuming. The concern is straightforward: if the same firm that is selling your company also earns fees representing the private-equity buyers it is negotiating against — or hopes to win their next buy-side mandate — its incentive to push the last dollar out of those buyers on your behalf is at least in tension with its own relationships. This is why some software boutiques market themselves as exclusively sell-side. Vista Point Advisors is the clearest archetype: it never represents buyers, so it has no buy-side relationship to protect and its advice on your sale is structurally unconflicted. SEG and Corum are likewise sell-side-focused. The contrast is a firm like Union Square Advisors, which does both sell-side and buy-side work — that is not disqualifying (many excellent banks run both sides with information walls and full disclosure), but you should ask directly. The screening questions: Is your firm exclusively sell-side, or do you also represent buyers? Have you done buy-side work for any of the specific PE platforms likely to bid on me? How do you wall off and disclose conflicts? A credible advisor answers all three plainly; evasion is the red flag. Verify each firm's registration and disclosures too — Vista Point is FINRA CRD #157502 and Founders' securities entity is BrokerCheck firm #269926, and for any firm you can check BrokerCheck or state records.

How do I keep a sale confidential from my 55 employees and my customers?

Confidentiality is a process-design problem, and it is one of the most important ones for a founder-run company where 55 employees and enterprise customers could be spooked by a leak. Four levers do most of the work. First, a tight, targeted buyer list rather than a broad auction — the fewer parties who know, the lower the leak risk, which is one reason a curated process suits a founder-led SaaS company. Second, staged disclosure behind NDAs: a blind teaser (no company name) goes out first, the company identity and full data room open only to bidders who have signed a strong NDA, and the most sensitive material — customer-level ARR and churn, named contracts, source-code references, key-employee detail — is held to a short list only after indications of interest. Third, a strict internal need-to-know circle (usually just the founder, CFO, and maybe one or two others) with a cover story for unusual activity, and diligence calls scheduled off-hours. Fourth, and this is where the data room matters, per-bidder watermarking and controlled access so a leaked page is traceable to the party that leaked it, screenshot protection on the most sensitive files, and analytics that show exactly who opened what. We built Peony — used by 5,900+ customers — for precisely this: per-viewer watermarks on every render, visitor groups that show strategics and sponsors only what they should see, dynamic NDA gating before access, and page-level analytics. Your advisor manages the human side of confidentiality; the data room enforces the document side.

How long does it take to sell an $8M ARR SaaS company?

For a well-prepared $8M ARR SaaS company, plan on roughly four to nine months from engaging an advisor to close, with the biggest swing factors being how clean your metrics are and how much competitive tension the process generates. The arc runs: preparation and positioning (about four to six weeks) — assembling the ARR bridge, NRR and GRR cohorts, and the Rule-of-40 story, building a clean data room, and drafting the CIM; targeted buyer outreach behind a teaser and clickthrough NDA (two to four weeks); management presentations and first-round indications of interest (three to five weeks); selecting a lead party or short list and running confirmatory due diligence and exclusivity (four to eight weeks), where the quality-of-earnings review and deep SaaS-metric verification happen; and purchase-agreement negotiation and close. The two things that most often add time are a messy ARR and deferred-revenue picture that fails to reconcile in QoE, and a thin buyer list that produces too little competition. The cheapest lever you control on both timeline and price is walking into diligence with numbers that already tie out and a data room staged before launch. For the document buildout, see our SaaS M&A data room guide and the general M&A data room playbook.

How do I vet a software M&A advisor before signing an engagement letter?

Vet on three axes: registration, subsector fit, and conflicts. On registration, confirm the firm's status before you sign — Vista Point is FINRA CRD #157502 and Founders' securities entity is Founders M&A Advisory LLC (BrokerCheck firm #269926, member FINRA/SIPC); for any other firm, look it up on BrokerCheck or with your state securities regulator. Note that some legitimate pure sell-side advisors operate under the SEC M&A-broker exemption Congress codified in 2023 rather than as registered broker-dealers, so 'not on BrokerCheck' is not automatically disqualifying — but you should confirm which basis they operate under and get it in writing. On subsector fit, ask each firm to name the five buyers it would call first for your specific product, how many software deals it has closed in your exact sub-vertical and ARR band in the last 18 months, and whether those went to strategics or to sponsors — a genuine specialist answers without hesitating, and beware a 'software practice' whose deal sheet is really IT-services or MSP work. On conflicts, ask whether the firm is exclusively sell-side or also represents buyers, and how it walls off and discloses conflicts. On economics, get the fee structure, the minimum fee, the definition of transaction value (equity vs enterprise value, and how earnouts and rollover count), and the tail in writing. And treat self-reported superlatives — '#1 most active,' 'the only firm that…' — as claims to attribute, not facts. The intermediary-type framing is in our advisor vs broker vs investment bank hub.

What do software M&A advisors charge on a sub-$50M deal?

There is no software-specific fee study, so the honest answer uses lower-middle-market M&A norms and flags that software is priced like the rest of that market: a retainer or monthly work fee plus a success fee at close, with the success rate declining as deal size grows. Using the Axial M&A Fee Guide (2024-2025) benchmarks: at roughly $10M in enterprise value the success fee most commonly runs 4%-5.9%, with a minimum fee around $150K common; at about $25M it is roughly 3%-5%; and at about $50M it is roughly 2%-3.9%. Around 79% of engagements use a Modified-Lehman tiered structure or a flat percentage. Retainers commonly run about $50K up front or $3K-$15K per month, usually credited against the success fee if the engagement letter says so in writing, and success-fee-only arrangements have risen to about a third of engagements (up from 19% in 2024). Two things move the real number more than the headline rate: the minimum fee (on a small deal the floor, not the percentage, can set the bill — which is part of why a sub-$5M-ARR micro-SaaS is often better served by a marketplace than a full boutique process), and the definition of transaction value (a broad definition that sweeps in earnouts and rollover inflates the base on the same headline price). Negotiate the percentage, the minimum, the base definition, and the tail. Full mechanics, including worked Lehman and Double-Lehman math, are in our M&A advisor fees hub.

What ARR multiple can a bootstrapped $2M-EBITDA vertical SaaS company expect in 2026?

The honest 2026 answer requires separating two numbers that are constantly conflated — the average and the median — because they tell very different stories. On an average basis, SaaS M&A in 1Q26 cleared at about 6.3x EV/TTM revenue (SEG), the second-highest recent reading after 4Q25's 6.9x. But that average is skewed upward by a handful of premium, high-growth assets. On a median basis, private SaaS M&A ran closer to about 3.1x EV/revenue in March 2026 (Aventis Advisors), down from about 3.8x in 2025. For a bootstrapped, profitable ($2M EBITDA) vertical SaaS company growing at a steady rather than hyper rate, the median is the more realistic anchor — plan around roughly 3x-4x ARR and treat anything higher as upside you have to earn with growth, retention, and an AI story. Two levers move you within that range: the Rule of 40 (buyers in 2026 reward profitable growth, and a bootstrapped $2M-EBITDA business already screens well on the profit side), and net revenue retention (NRR above ~120% can lift the multiple materially). One caveat to ignore the froth: AI-native SaaS can command a 1x-3x multiple premium (SEG Research), but only about 26% of evaluated targets qualified as genuinely AI-driven in 2025, so most sellers will not clear that bar — and the 15x-45x ARR figures you see quoted are frothy private VC-round numbers, not M&A comparables. Vertical software specifically was about 55% of 1Q26 SaaS M&A (up from 49%), so a vertical SaaS company is selling into a buyer set that is actively consolidating your category.

Sources

- Software Equity Group (SEG) — quarterly and annual SaaS M&A reports and the SEG SaaS Index: softwareequity.com (1Q26 and FY2025 data: SaaS M&A average ~6.3x EV/TTM revenue, public SaaS Index median 3.6x, 659 deals 1Q26 / TTM 2,723, ~2,700 deals FY2025, PE/VC ~60% of 1Q26 buyers, vertical software 55% of 1Q26, ~9.1% median EBITDA margin, AI premium and 26%-qualify figures)

- Aventis Advisors — SaaS valuation multiples (private SaaS M&A median ~3.1x EV/revenue, March 2026): aventis-advisors.com

- Axial — M&A Fee Guide 2024-2025 (success-fee benchmarks, minimum fees, retainers, Modified-Lehman prevalence): axial.net

- Software Equity Group (SEG): softwareequity.com

- Vista Point Advisors (FINRA CRD #157502): vpadvisors.com

- Corum Group: corumgroup.com

- Founders Advisors (Founders M&A Advisory LLC, BrokerCheck #269926): foundersib.com

- Shea & Company: sheaco.com

- AGC Partners: agcpartners.com

- Union Square Advisors: unionsquareadvisors.com

- GP Bullhound: gpbullhound.com

- Drake Star Partners: drakestar.com

- Tequity Advisors: tequityadvisors.com

- Q Advisors: qllc.com

- Bank Street Group: bankstreet.com

- FT Partners (Financial Technology Partners): ftpartners.com

- Momentum Cyber: momentumcyber.com

- FINRA BrokerCheck (verify any advisor's registration): brokercheck.finra.org

- Named-deal releases: Dayforce → Thoma Bravo (~$12.3B, announced August 2025; Evercore advisor to Dayforce); Instructure → KKR ($4.8B; J.P. Morgan lead advisor); Protecht → PSG ($280M); Conservice → TPG (December 2025); Piper Sandler / DBO Partners (October 2022) and Piper Sandler / G Squared Capital Partners (September 12, 2025)

Disclosure: I am the co-founder of Peony, a data room company, so I have a commercial interest in the data-room layer discussed in the Peony section — the advisory firms above are independent and are not Peony partners or clients by virtue of appearing here. Firm facts, deals, and registrations were verified as of July 2026 and can change; confirm current registration on FINRA BrokerCheck or with your state securities regulator before engaging any advisor. Self-reported superlatives are attributed to the firms that make them. Nothing here is investment, legal, tax, or financial advice — retain your own M&A counsel and a quality-of-earnings accountant before acting.

About the author: Deqian Jia is the co-founder of Peony, the data room platform used by 5,900+ customers across M&A, fundraising, and private-deal workflows. He spends most of his time on the access-control and analytics layer that decides who — and now what — is allowed to read a confidential document. Contact: hello@peony.ink.