10 Best M&A Advisors in Richmond for $5M–$500M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: July 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. Before Peony I ran M&A deals as a banker at Nomura and invested at Target Global and Backed VC, so I have sat on both sides of the table — and now, on the document side, I watch hundreds of deals a year move through our platform, from founder-led exits and family-business successions to PE recapitalizations and strategic carve-outs. Richmond is the entry in our M&A advisor series where the metro's defining fact is a historical inversion: it was once the Wall Street of the South, it sold every one of its investment banks, and it became a mid-market M&A capital instead. Most "best Richmond M&A advisors" pages fail two simple tests at once. They still present the town's famous flagship, Harris Williams, as if it would take a $25M seller's deal (it discontinued the arm that did, in 2011). And they file a wealth manager — Cary Street Partners — under "M&A advisors," when Cary Street sold a majority stake to a private-equity firm in 2025 and spends its energy buying RIAs. At Peony we now serve more than 5,900 customers, and Richmond sits squarely in the sub-$500M enterprise-value band that makes up the bulk of the deals we see in our state-of-the-market benchmark.

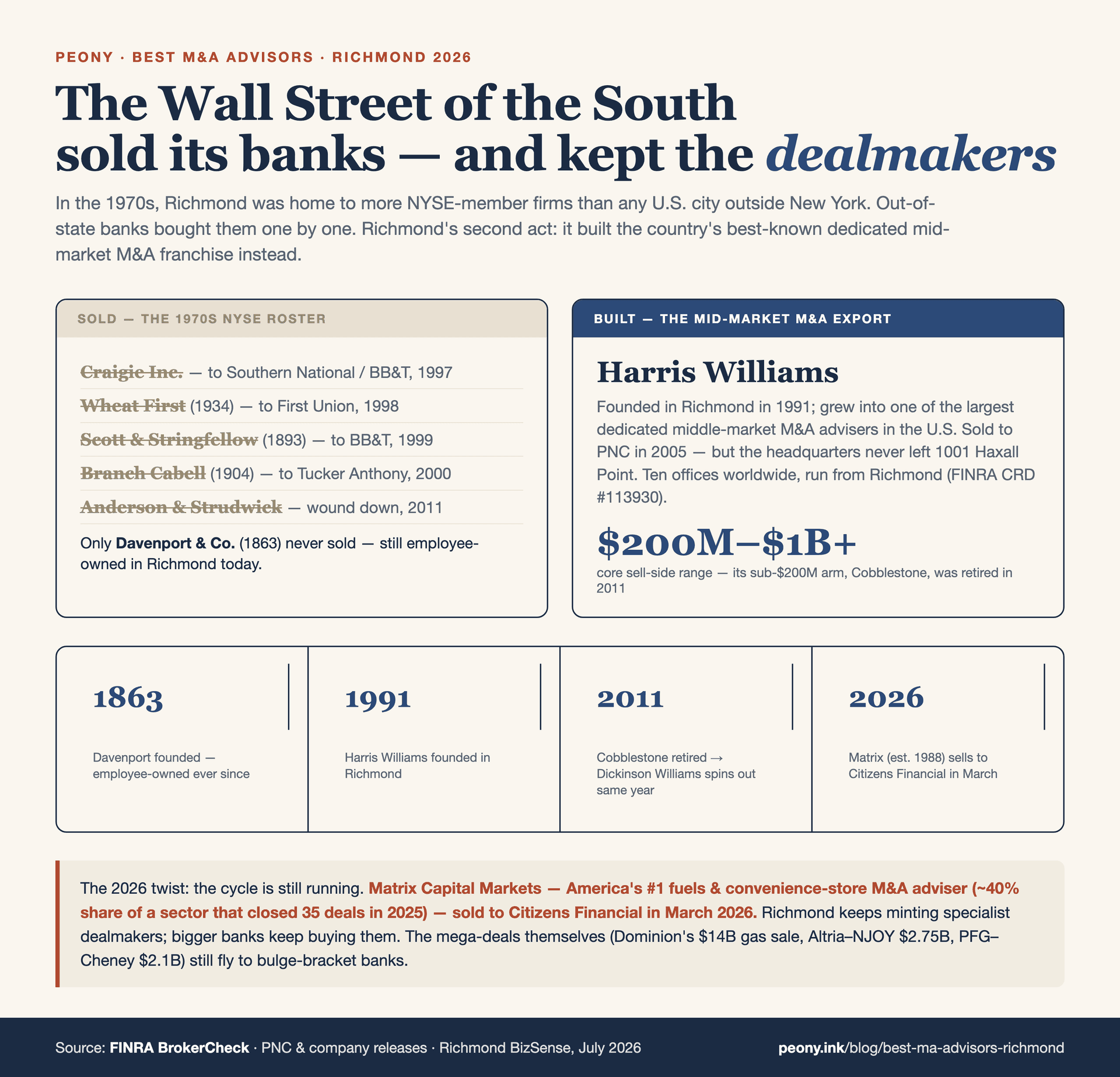

Here is the thesis I want you to internalize before you read another word: Richmond sold its Wall Street and built its M&A capital on the ashes. In the 1970s this city was headquarters to more NYSE-member firms than any US city outside New York. Then, one by one, they sold to out-of-state buyers — Craigie to Southern National (which became BB&T) in 1997, Wheat First to First Union in 1998, the venerable Scott & Stringfellow (founded 1893) to BB&T in 1999, Branch Cabell (1904) to Tucker Anthony in 2000 and on to RBC, Anderson & Strudwick to Sterne Agee in 2011. All but employee-owned Davenport & Company (founded 1863, still on East Cary Street) yielded to out-of-state partners. But Richmond's second act reorganized the whole advisor decision: Harris Williams, founded here in 1991, grew into one of the largest dedicated middle-market M&A advisers in the United States and kept its Richmond headquarters even after selling to PNC in 2005.

That single fact — a nationally significant M&A house headquartered at 1001 Haxall Point — is why this page reads differently from every other city in the series, and also why it comes with a catch. Unlike Baltimore, which invented American investment banking and then sold every homegrown heir and kept a thin bench, or Milwaukee, which sold its commercial bank but kept its homegrown investment bank (Robert W. Baird) available to local sellers, Richmond kept a flagship that mostly fishes above your size. So the practical payoff for the persona I wrote this for — a $25M-revenue owner weighing an unsolicited PE inquiry — is counterintuitive: the city's famous flagship won't take your deal, and the real bench for you is the registered pure-play boutiques and the exemption boutiques below it. This post is the working playbook I would hand to that owner. The frames come from cross-referencing FINRA BrokerCheck, the firms' own disclosures, Richmond BizSense reporting, and the verified 2025-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in Richmond right now for $5M-$500M deals?

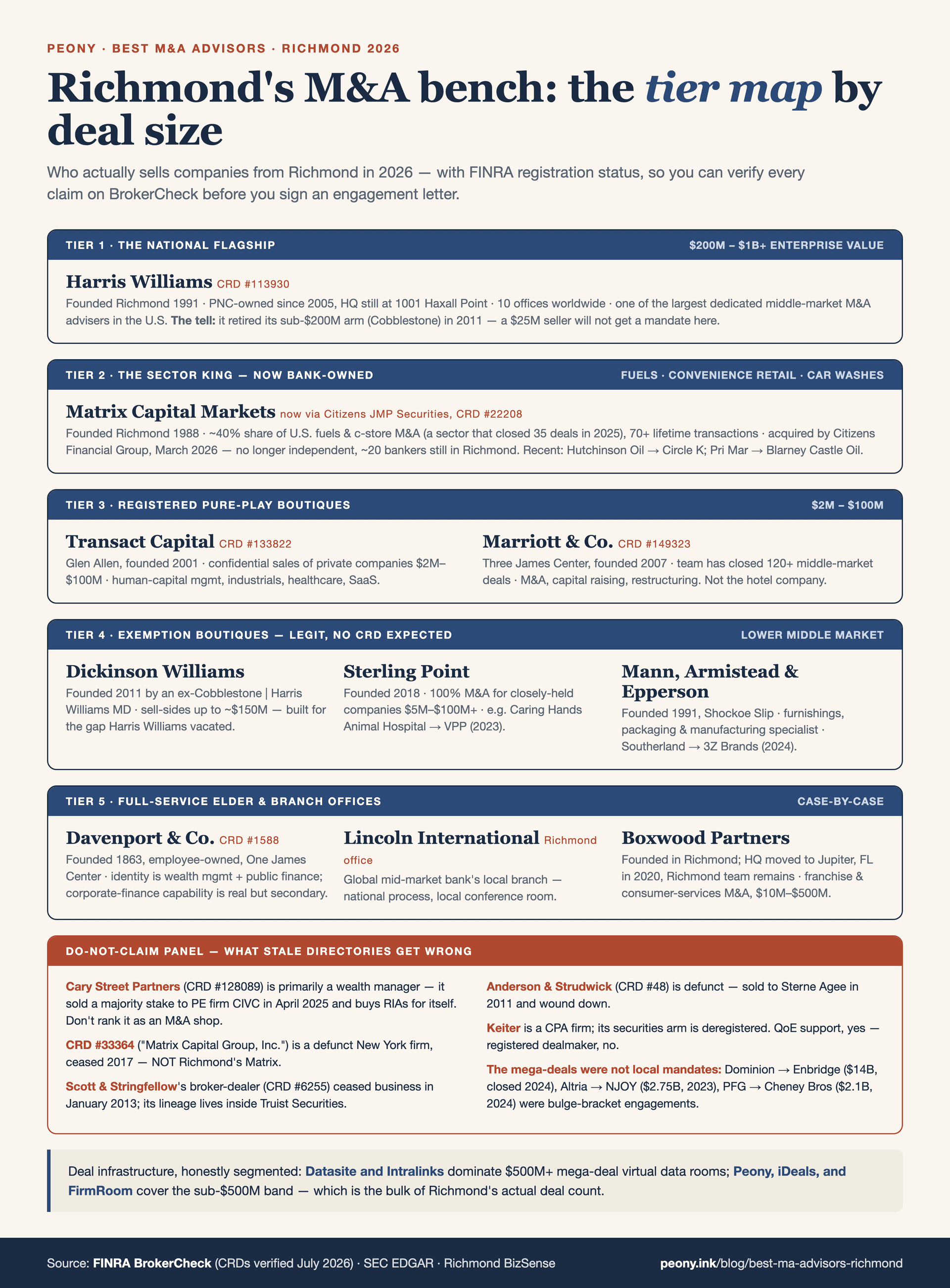

The best M&A advisor in Richmond depends on your deal's size and sector, and the honest segmented answer is the whole point of this page. For a $200M-plus company, Harris Williams (CRD #113930, 1001 Haxall Point) is the homegrown flagship and one of the largest dedicated middle-market M&A advisers in the US. For a fuels, convenience-store, or car-wash business, the specialist is Matrix Capital Markets Group — America's #1 advisor in that vertical, now operating inside Citizens JMP Securities (CRD #22208) after Citizens Financial Group acquired it in March 2026. For a $2M-$100M company — where a $25M-revenue seller sits — the registered pure-play boutiques Transact Capital Securities (CRD #133822, Glen Allen) and Marriott & Co. / Marriott Securities (CRD #149323) run true sell-side processes. And for lower-middle-market deals up to roughly $150M, the honest M&A-broker-exemption boutiques — Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson — are legitimate, focused options. The one name to be careful with: Cary Street Partners (CRD #128089) is primarily a wealth manager, not a sell-side M&A advisory, whatever a stale directory tells you.

Here is the 2026 shortlist, sorted by tier and deal-size band. The verification wrinkle in Richmond is different from most cities: the traps are not only dead firms (Scott & Stringfellow, Anderson & Strudwick) but a wealth manager wearing an M&A label, a flagship above your floor, and a specialist that changed owners in the last few months.

| Firm | HQ / Richmond presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| Harris Williams ★ | 1001 Haxall Point, Richmond (founded 1991, PNC-owned since 2005) | $200M-$1B+ EV | Large middle-market M&A on a national/global platform | Registered broker-dealer (CRD #113930) |

| Matrix Capital Markets Group (in Citizens JMP Securities) | Richmond (founded 1988; acquired by Citizens Financial Group, complete March 2026) | $25M-$300M+ EV, sector-specific | Fuels and convenience stores (~40% share), car washes, building products, healthcare | Registered broker-dealer — Citizens JMP Securities (CRD #22208) |

| Transact Capital Securities | Glen Allen (Richmond suburb), founded 2001 | $2M-$100M EV | Pure sell-side M&A; human capital, industrials, healthcare, SaaS/tech | Registered broker-dealer (CRD #133822) |

| Marriott & Co. / Marriott Securities | Three James Center, Richmond (founded 2007) | $5M-$100M EV | Middle-market M&A, capital raising, restructuring, valuations (team has closed 120+ deals) | Registered broker-dealer (CRD #149323) |

| Dickinson Williams & Co. | Richmond (founded 2011 by an ex-Cobblestone MD) | up to ~$150M EV | Lower-middle-market M&A | M&A advisor (non-registered; M&A-broker exemption) |

| Sterling Point Advisors | Richmond (founded 2018) | $5M-$100M+ EV | 100% M&A for closely-held LMM companies | M&A advisor (non-registered; M&A-broker exemption) |

| Mann, Armistead & Epperson | 119 Shockoe Slip, Richmond (founded 1991) | $5M-$100M EV | Furnishings/furniture, packaging, manufacturing, printing (~19 deals) | M&A advisor (non-registered; M&A-broker exemption) |

| Davenport & Company | One James Center, Richmond (founded 1863, employee-owned) | Regional generalist | Wealth + municipal/public finance, with a corporate-finance capability | Registered broker-dealer (CRD #1588) |

| Boxwood Partners | Founded in Richmond; HQ now Jupiter, FL (Nov 1, 2020); Richmond office remains | $10M-$500M EV | Franchise and consumer-services M&A | Registered/affiliated (see body) |

| Lincoln International (Richmond branch) | 200 S. 10th St, Richmond (branch of a global bank) | $100M-$500M+ EV | Global mid-market M&A — the national walk-in option | Established FINRA broker-dealer |

A few notes the table cannot carry. Harris Williams is the reason this page exists as its own entry: a genuinely homegrown firm — founded in Richmond in 1991 by Christopher Williams and Hiter Harris, headquartered at 1001 Haxall Point, roughly 700 employees across about ten offices — that grew into one of the largest dedicated middle-market M&A advisers in the United States and kept its Richmond center of gravity even after PNC acquired it in 2005. The nuance you must hold, covered in its own section below, is that Harris Williams fishes at $200M-$1B-plus and discontinued its sub-$200M Cobblestone arm in 2011, so for most readers of this page it is a landmark, not an option.

Matrix Capital Markets Group is the specialist that defines a whole vertical: America's #1 fuels and convenience-store M&A advisor, at roughly 40% market share. The critical currency point is that Matrix is no longer an independent Richmond boutique — Citizens Financial Group acquired it, reported complete March 9, 2026 by Richmond BizSense, and it now operates inside Citizens JMP Securities (CRD #22208). Transact Capital Securities (CRD #133822) and Marriott & Co. / Marriott Securities (CRD #149323) are the registered pure-play boutiques that run true sell-side processes at $2M-$100M. Then the honest non-registered tier — Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson — operates under the federal M&A-broker exemption, a legitimate and common model for private-company sales. Davenport & Company (CRD #1588) is the 160-year-old employee-owned elder statesman with a corporate-finance capability, but a regional generalist whose identity is wealth management and public finance, not a dedicated M&A shop.

And the critical honesty point on the name a Richmond owner is most likely to encounter in a bad directory: Cary Street Partners is primarily a wealth manager, not a sell-side M&A advisor. More on the sorting test below.

Why is Richmond "the Wall Street of the South that sold its banks"?

Every metro in this series has a structural signature. St. Louis is a Headquarters Town that grew and kept a national bank in Stifel. Milwaukee sold its commercial bank but kept its investment bank in Robert W. Baird. Baltimore invented American investment banking and then sold every homegrown heir. Richmond's signature is the most dramatic reversal in the series: it was the Wall Street of the South, it sold every one of its banks, and it rebuilt itself as a middle-market M&A capital.

The first act is almost forgotten now, but it was real. In the 1970s, Richmond was headquarters to more NYSE-member firms than any US city outside New York — a genuine regional financial capital, dense with brokerage houses and underwriters. Then, over roughly fifteen years spanning the great consolidation of American banking, every homegrown house sold to an out-of-state buyer. Craigie went to Southern National — which became BB&T — in 1997. Wheat First (Wheat, First Securities) went to First Union in 1998. Scott & Stringfellow, founded in 1893 and one of the oldest names in Southern finance, went to BB&T in 1999; its broker-dealer entity (CRD #6255) ceased business on January 2, 2013, and its lineage now lives inside Truist Securities. Branch Cabell, founded in 1904, went to Tucker Anthony in 2000 and then to RBC. Anderson & Strudwick (CRD #48) went to Sterne Agee in 2011 and was wound down around 2013. One firm did not sell: Davenport & Company, founded in 1863 and 100% employee-owned, is still headquartered in Richmond today — the lone survivor of the old order, and the reason its name still carries weight locally.

If the story ended there, Richmond would read exactly like Baltimore — a proud financial city whose institutions were absorbed by outsiders, leaving a thin bench. But the second act rewrote the ending. Harris Williams, founded in Richmond in 1991 — after the old houses had begun to sell — grew into one of the largest dedicated middle-market M&A advisers in the United States. And when PNC acquired it in 2005, Harris Williams did what none of the old houses' acquirers did: it kept its Richmond headquarters and center of gravity at 1001 Haxall Point. So Richmond lost its retail-brokerage Wall Street and gained something arguably more valuable for a modern founder — a nationally significant M&A advisory practice headquartered in town, plus a renewal cycle that kept spinning out new boutiques beneath it. The clearest example of that renewal: when Harris Williams discontinued its sub-$200M Cobblestone arm in 2011, a former Cobblestone managing director founded Dickinson Williams the same year to serve exactly the gap that closing left behind.

What does that mean for you, a founder selling a $5M-$500M company? Three things. First, the town's most famous name is probably not your advisor — Harris Williams fishes above your size, so "hire the flagship in your backyard" is not the move it would be in Milwaukee. Second, the real bench is deep and specialized precisely because of the renewal cycle — the registered boutiques (Transact Capital, Marriott & Co.) and the exemption boutiques (Dickinson Williams, Sterling Point, Mann Armistead & Epperson) exist to serve the lower-middle-market that the flagship vacated. Third, and this is the honest counter you must hold alongside the thesis: Richmond's marquee corporate deals still fly to bulge-bracket banks. Dominion Energy's roughly $14B gas-distribution divestiture to Enbridge, Altria's roughly $2.75B NJOY acquisition, Performance Food Group's roughly $2.1B Cheney Bros deal — none of those were local mandates. The "M&A capital" advantage is real, but it lives in the middle market, not at the top of the deal-size curve.

Is Harris Williams too big for my $25M-revenue company?

Yes — and there is a specific, verifiable reason, not just a size mismatch. Harris Williams (FINRA CRD #113930, headquartered at 1001 Haxall Point) is one of the largest dedicated middle-market M&A advisers in the United States, and its core mandates run roughly $200M to $1B-plus in enterprise value. For a $25M-revenue company with roughly $3.5M of EBITDA hoping for a $20M-$35M enterprise value, that is well below its floor. The firm describes itself as "one of the largest, independently owned, middle market M&A advisory firms in the United States" — I hedge that to "one of the largest dedicated middle-market M&A advisers," because the precise superlative is theirs to make, not mine.

Here is the part that stale directories miss. Harris Williams used to have an arm built for exactly your size: Cobblestone Advisors, launched in 1998 to handle $25M-$200M transactions. But Cobblestone was folded into the main firm and its brand discontinued on June 1, 2011. Since then, Harris Williams has largely not taken sub-$50M mandates — the small-deal capability left when Cobblestone's brand did. So any "best Richmond M&A advisors" page that implies you can hire Harris Williams to sell a $20M-$35M company is describing a capability the firm retired more than a decade ago.

The good news is that Richmond's renewal cycle built your bench out of that very closing. When Cobblestone shut down, a former Cobblestone managing director founded Dickinson Williams & Co. the same year (2011) to serve lower-middle-market deals up to about $150M — a firm that exists precisely because Harris Williams moved upmarket. So the practical takeaway is not "Richmond has no advisor for you"; it is "Richmond has a purpose-built lower-middle-market bench, and Harris Williams is a landmark rather than an option." Your real shortlist is the registered pure-plays (Transact Capital, Marriott & Co.) and the exemption boutiques (Dickinson Williams, Sterling Point, Mann Armistead & Epperson) — the firms that live in your size band and will give your deal senior attention. Admire the flagship; hire the boutique.

A note on Harris Williams's current deal flow, in the interest of honesty: I am not going to attribute specific 2025-26 client transactions to the firm, because I could not verify named recent mandates to the standard this series holds. What is fair to say is that Harris Williams runs on the order of a hundred-plus deals a year across its offices — a scale that itself tells you it is built for the mid-to-large middle market, not a $25M founder sale.

Should I hire a Richmond boutique or a national mid-market bank to sell my company?

For a $25M-revenue company, hire a Richmond boutique — and recognize that in this metro "go local" and "go national" only diverge above roughly $150M-$200M of enterprise value, because the local flagship is itself a national firm that will pass on your deal. This is the fork Richmond frames differently from any other city. In Milwaukee, "stay local" can mean hiring a top-12 global bank (Baird) headquartered downtown at almost any size. In Richmond, the equivalent flagship (Harris Williams) fishes at $200M-plus, so for a lower-middle-market seller the choice is not "local boutique vs. local flagship" but "local boutique vs. imported national bank" — and below roughly $150M the local boutique usually wins.

Reach for a Richmond boutique — Transact Capital (CRD #133822), Marriott & Co. (CRD #149323), Dickinson Williams, Sterling Point, or Mann, Armistead & Epperson — when your deal is in the ~$2M-$100M band and what you value most is senior attention. At a boutique, the person who pitched you runs your process, reads every buyer, and negotiates your LOI. Your buyer universe at this size is regional-to-national strategics and lower-middle-market private-equity firms, not a global auction — and a focused boutique with a real buyer list can manufacture just as much competitive tension in that market as a bigger bank would. For a founder-owned company where the sale is the financial event of a lifetime, that attention is worth real money.

Reach for a national mid-market bank — Harris Williams itself, or the Lincoln International team that keeps a Richmond branch office at 200 S. 10th St — when your deal scales past roughly $150M-$200M, spans a genuinely global buyer set, or sits in a vertical where a particular national platform owns the buyer relationships. Lincoln is the clean "national walk-in option" here: a global mid-market bank with an actual Richmond address, appropriate when your deal outgrows the local boutiques but you still want someone reachable in town.

The honest nuances that decide close calls: (1) the flagship's floor is real — do not waste a cycle pitching Harris Williams a $30M deal it retired the capability to run in 2011; (2) sector fluency can trump platform — if you sell convenience stores or car washes, Matrix (now inside Citizens JMP Securities) already knows your ten most likely buyers by name; and (3) the test is identical for local and national — named senior staffing, three named recent closings in your sub-sector, and the buyers on the other side. Run your best boutique and any national option through the same screen and let the answers decide. Price comes from competitive tension and preparation, not from the size of the logo on the engagement letter.

Did Matrix Capital Markets Group get acquired — and is it still an independent Richmond boutique?

No, it is no longer an independent Richmond boutique — and this is the most important currency correction on the page after the Cary Street one. Matrix Capital Markets Group was acquired by Citizens Financial Group, announced in February 2026 and reported complete on March 9, 2026 by Richmond BizSense. The Matrix team now operates inside Citizens JMP Securities (CRD #22208) — roughly three dozen staff, about twenty of them in Richmond. So any directory still presenting Matrix as a standalone independent firm is describing a structure that changed in early 2026.

What did not change is why Matrix matters: it is America's #1 fuels and convenience-store M&A advisor, and it is not close. Founded in Richmond in 1988, Matrix holds roughly 40% market share in that vertical — 21 of its 26 bankers work it — in a market that closed 35 deals in 2025 (up about 25% year over year, per Matrix's own sector review); the firm itself has completed 70-plus transactions. Its verticals extend to car washes, building products, healthcare, and industrials, but fuels-and-c-store is the franchise. Named deals that illustrate the lane: Hutchinson Oil to Circle K (about 20 stores), Pri Mar Petroleum to Blarney Castle Oil, and West Oil. If you own a fuels, convenience-store, or car-wash business anywhere in the country, this is the specialist — and now it comes with a national bank's balance sheet behind it.

There is one critical trap here that catches even careful researchers. The CRD number for Richmond's Matrix is not #33364. "Matrix Capital Group, Inc." (CRD #33364) is a completely different, defunct New York firm that ceased business in 2017. If you pull #33364 on BrokerCheck expecting Richmond's Matrix, you will get the wrong company. The registration you actually care about now is Citizens JMP Securities, CRD #22208, the entity the Matrix team operates under post-acquisition. This is the classic Richmond lesson in miniature: verify the current entity and its current owner, because the name you know may sit behind a different CRD than you expect.

For a Richmond seller who is not in fuels or convenience stores, the Matrix story is still instructive: it shows that even the city's specialist crown jewels get acquired by out-of-state financial institutions — the same pattern that took Craigie, Wheat First, and Scott & Stringfellow a generation ago, now playing out one more time in 2026.

What's the difference between a business broker and an M&A advisor for my Richmond company?

A business broker lists smaller, owner-operated businesses to a pool weighted toward individual buyers on a listing-and-commission model; an M&A advisor or investment bank runs a confidential, competitive, curated process for a middle-market company, marketing to strategic acquirers and private-equity firms and manufacturing tension among them. For a $25M-revenue company with roughly $3.5M of EBITDA, you are squarely in M&A-advisor territory, not business-brokerage territory — and getting this distinction right is the difference between a clean competitive exit and leaving money on the table.

The practical differences that matter for a Richmond seller:

- How your company is marketed. A broker often posts a semi-public or public listing that anyone can browse; an M&A advisor markets from a blind teaser under NDA and does not name your company until a buyer is vetted and committed. For a specialty-distribution or business-services owner terrified of competitors finding out, that difference alone is decisive.

- Who the buyer is. A broker's buyer is usually an individual, an owner-operator, or a small local acquirer; an M&A advisor's buyer is an institution — a strategic acquirer in your sector or a private-equity platform — that pays on multiples of EBITDA and can move on a $20M-$35M deal.

- How the fee works. A broker typically charges a flat commission on a listing; an M&A advisor charges a monthly retainer plus a success fee scaled to the deal (see the fee section below).

- What "the process" even means. A broker matches a willing buyer to a willing seller; an advisor engineers competition — running multiple credible buyers against each other to move price and terms.

In Richmond, the registered boutiques (Transact Capital, Marriott & Co.) and exemption boutiques (Dickinson Williams, Sterling Point, Mann Armistead & Epperson) run true M&A processes at your size — none of them is a business broker. Below roughly $2M-$3M of enterprise value you would legitimately be in brokerage territory, but a company with $3.5M of real EBITDA is not. For the full taxonomy — advisor vs. broker vs. investment bank — see our dedicated guide. The tell I use from the document side: deal people build a permissioned data room and stage disclosure; brokers email a listing sheet.

Are Richmond "M&A advisors" actually investment banks, or wealth managers in disguise?

Some are genuine sell-side M&A firms, and one prominent name is not — so the honest answer is "check each one, and start with the wealth-manager trap." The single most important firm to flag is Cary Street Partners (FINRA CRD #128089): it is primarily a wealth manager, not a sell-side M&A advisory. Cary Street carries nine business lines on BrokerCheck (mutual funds, variable annuities, municipal securities, and the like), it sold a majority stake to the private-equity firm CIVC Partners in April 2025, and it has been actively buying RIAs for itself (IFS Advisors, Pursuit Wealth). It does have a registered-but-secondary investment-banking capability, so it is not fair to say it does zero M&A — but its identity, revenue, and strategic direction are wealth management. Listing it as a Richmond M&A advisory, the way some directories do, would genuinely mislead a first-time seller. This is the #1 "wealth manager in disguise" example for this metro.

The genuine Richmond sell-side bench is a different set entirely:

- Registered broker-dealers running real M&A: Harris Williams (CRD #113930, but $200M-plus), Transact Capital Securities (CRD #133822), Marriott & Co. / Marriott Securities (CRD #149323), and Matrix's team inside Citizens JMP Securities (CRD #22208).

- Honest M&A-broker-exemption boutiques: Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson — no broker-dealer CRD, operating legitimately under the federal exemption.

- The nuanced case: Davenport & Company (CRD #1588). Davenport is a real, 160-year-old registered broker-dealer, and its own SEC filings state it is "regularly engaged in the valuation of businesses and securities in connection with mergers, acquisitions" — so it has a genuine corporate-finance capability. But its identity is wealth management (70-plus financial advisors in Richmond) plus municipal and public finance. Frame it accurately: the elder-statesman regional generalist with a corporate-finance function, not a dedicated M&A boutique. I would not point a $25M seller to Davenport for a competitive sale process before the pure-plays, but it is not a trap the way Cary Street is — it is a different animal, not a mislabel.

The clean test for any Richmond firm: pull the CRD on FINRA BrokerCheck, read the listed business lines (a wealth manager's nine-line profile looks nothing like a pure M&A boutique's), and ask for three named recent M&A closings with the buyers identified. A firm that sells companies for a living answers that in one breath; a firm that manages money will (honestly) describe something else. And the document-side tell holds: the firms that actually sell companies insist on a real, permissioned data room, because that is how a competitive process is run and protected.

How do I check whether a Richmond M&A advisor is a registered broker-dealer?

Go to FINRA BrokerCheck (brokercheck.finra.org) and search the firm's exact legal name — it returns the CRD number, registration status, business lines, office locations, and any disclosure events. This is free, authoritative, and the single most valuable ten minutes of diligence you will do before signing an engagement letter. For Richmond's bench, that means confirming Harris Williams (CRD #113930), Transact Capital Securities (CRD #133822), Marriott Securities (CRD #149323), Davenport & Company (CRD #1588), and — for the former Matrix — Citizens JMP Securities (CRD #22208).

Two Richmond-specific things to understand before you interpret what BrokerCheck shows you.

First, a firm returning no broker-dealer record is not automatically illegitimate. Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson operate under the federal M&A-broker exemption, which Congress codified in 2023. It lets qualified M&A brokers facilitate the sale of privately held companies without full broker-dealer registration, subject to size and structure limits. This is a normal, appropriate, and common model for pure sell-side advisory — most boutiques that only sell companies (rather than underwrite securities) fit it. So the absence of a CRD for these firms is expected, not a red flag. What you should do is confirm they operate under the exemption, and — if your deal is structured as a stock sale rather than an asset sale — ask specifically how the securities piece will be handled and through which entity.

Second, watch for name collisions and dead entities that stale directories still surface:

- "Matrix Capital Group, Inc." (CRD #33364) is a defunct New York firm that ceased business in 2017 — not Richmond's Matrix. Richmond's Matrix team is now under Citizens JMP Securities (CRD #22208).

- Scott & Stringfellow (broker-dealer CRD #6255) ceased business January 2, 2013; its lineage lives inside Truist Securities. It is not a live firm you can hire.

- Anderson & Strudwick (CRD #48) is defunct — sold to Sterne Agee in 2011, wound down around 2013. Stale directories still list it.

- Keiter's securities arm ("Keiter Capstone Securities" / CapGroup, CRD #47075) is deregistered. Keiter is an excellent Richmond CPA firm that provides quality-of-earnings and transaction-advisory support — not a registered dealmaker running your sale.

The generalizable discipline is the one this whole page keeps returning to: verify the current entity, its current owner, and its current registration before you sign anything, rather than trusting the reputation a name carried a decade ago. In a city where the banks sold themselves one after another — and where even the 2026 specialist crown jewel (Matrix) just changed hands — currency is the whole game.

How does the sell-side M&A process work step by step, and how long does it take?

A Richmond sell-side runs in five overlapping stages and typically takes 6-9 months from signing the engagement letter to close, longer if the financials need cleanup first. The rough timeline: 4-8 weeks of preparation (clean financials, a quality-of-earnings build, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA, starting from a blind teaser; 3-5 weeks to collect indications of interest and build a short list; 4-6 weeks of management meetings and the lead-bid/LOI stage; then 8-12 weeks of confirmatory due diligence and definitive-agreement negotiation to close.

Here is what actually happens in each phase, for a $25M-revenue Richmond company:

- Preparation (weeks 1-8). Your advisor normalizes the financials, builds or commissions a quality-of-earnings analysis, writes the CIM, and stands up a data room. This is the phase founders most often shortchange, and it is the one that most determines the outcome — buyers price uncertainty as risk, and unprepared financials invite a lower number and a longer diligence slog.

- Outreach (weeks 6-10). The advisor markets from a blind teaser to a curated list of strategic acquirers and private-equity firms under NDA, never naming your company until a buyer is vetted. This is where a good advisor's buyer relationships earn their fee.

- Indications of interest (weeks 9-14). Interested buyers submit preliminary, non-binding indications; the advisor builds a short list and creates competitive tension among them.

- Management meetings and LOIs (weeks 13-19). Short-listed buyers meet management, refine their views, and submit letters of intent; the advisor negotiates toward a lead bid with the best combination of price, terms, and certainty.

- Confirmatory diligence and close (weeks 18-30). The chosen buyer conducts deep due diligence — financial, legal, commercial, operational — while lawyers negotiate the definitive agreement. This is the phase where deals slow down or die, almost always over something diligence surfaces that preparation should have addressed.

The advisor's core job throughout is to manufacture competitive tension — which is exactly why taking a single unsolicited PE offer without a process tends to underperform. The single biggest timeline risk is unprepared financials. I run Peony, a data room company used by 5,900+ customers, and a clean, staged data room built before you go to market is the most reliable way to compress that back-half diligence phase — you cannot control the macro, but you can control whether a buyer's team spends three weeks or eight weeks confirming your numbers.

A private equity firm reached out unsolicited — do I still need an M&A advisor?

Yes — and counterintuitively, an unsolicited PE inquiry is the moment you most need one. A private-equity firm that contacts a founder directly is trying to buy the company without competition, which is entirely rational for them and potentially expensive for you. Without a competing bid, you have no leverage on price or terms, and a first-time seller rarely knows whether the offered multiple is generous or a lowball dressed up as a compliment ("we love what you've built and want to move fast, exclusively"). The flattery is real; so is the incentive to buy you cheap.

An M&A advisor's job is to convert that single inbound into a competitive process. The advisor runs a curated set of other credible strategics and sponsors against the party that called — under NDA, from a blind teaser, so your identity stays protected — and lets price be set by the market rather than by the one buyer at the table. That competitive tension typically moves the outcome by far more than the advisor's fee: on a lower-middle-market deal, the delta between a bilateral first offer and a competitively bid price is routinely a meaningful fraction of enterprise value, while the advisor's success fee is low-single-digit percent. The math favors the process.

An advisor also protects you on the things a first-time seller cannot see coming: the structure of the LOI, the earnout and rollover mechanics, the exclusivity and no-shop provisions (which, once signed, hand the buyer leverage to re-trade the price during diligence), and the confirmatory-diligence gauntlet itself. These are the mechanisms sophisticated buyers use routinely and founders encounter once. In Richmond, the boutiques on this page — Transact Capital, Marriott & Co., Dickinson Williams, Sterling Point — run exactly this play at your size.

One honest caveat: if the unsolicited offer is genuinely extraordinary, the buyer is uniquely strategic, and you have independent reason to trust the number, a full auction is not always mandatory. But even then, an advisor (or at minimum a strong deal attorney) should pressure-test the offer and the terms before you sign exclusivity. The default should be a process; the exception should be deliberate, not accidental. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects you — staged disclosure through a permissioned room — is identical whether one buyer called or ten did.

Is one unsolicited PE offer enough, or should I run a competitive process?

Run a process — one unsolicited offer is a starting point, not a fair price. Price on a private company is not a fixed number; it is whatever a motivated buyer will pay when they know another motivated buyer is in the room. The PE firm that reached out did so precisely because it hopes to transact bilaterally, without that pressure, and a first-time seller has no independent way to know whether its offer is at, above, or below what the market would clear. Running a process is how you find out — and how you move the number.

A tight, confidential process against a curated short list does three things at once:

- It tests the offer against real alternatives. You learn what the market actually thinks your company is worth, rather than accepting one buyer's self-interested estimate.

- It moves price and terms in your favor. Competitive tension is the single most powerful lever in M&A — buyers bid more, and concede more on terms, when they know they can lose the deal.

- It disciplines the original buyer. The firm that called now knows it cannot slow-walk diligence or re-trade the price after signing without risking the whole deal to a competitor.

The objection founders raise is confidentiality: "I don't want the whole world to know I'm for sale." That is a legitimate concern and a fully solvable one — a good advisor markets from a blind teaser under NDA and stages disclosure through a permissioned data room, so only serious, vetted buyers ever learn your identity, and even they see sensitive material only in the final wave. You are not choosing between "run a process" and "stay confidential"; a well-run process is confidential by construction.

Weigh the costs honestly. Running a process costs you a few months and a success fee; not running one often costs a materially lower price and weaker terms — a far larger number on a $20M-$35M deal. The only real exception is a genuinely exceptional bilateral offer you have independently pressure-tested, and even then you should get an advisor's read before signing exclusivity. I run Peony, a data room company used by 5,900+ customers, built for exactly this kind of staged, confidential release — the tooling that lets you run a real process without the leak you are afraid of.

How do I sell my Richmond business without employees or competitors finding out?

You keep it confidential with staged disclosure enforced by a permissioned data room: a blind teaser first, the named CIM only after a signed NDA, and the most sensitive material held back for a small short list of serious, later-stage bidders. This matters acutely for a Richmond specialty-distribution or business-services company, where the community is tight — your competitors, largest customers, and key employees may all know each other, sit on the same association boards, and trade gossip at the same industry events. A leak that you are "for sale" can spook a major customer, embolden a competitor to poach your best people, or unsettle the workforce, all before you have a signed deal. Confidentiality here is not paranoia; it is process discipline.

The structural defenses, which a good advisor runs as a matter of course:

- A blind teaser first. The initial one- or two-page document describes the business — sector, size, financial profile, investment highlights — without naming it, so a recipient (including a competitor who happens to receive it) cannot identify you from the teaser alone.

- The named CIM only after an NDA. The full confidential information memorandum, which names your company and discloses real detail, goes only to buyers who have signed a non-disclosure agreement — and your advisor curates that list to exclude the parties most likely to misuse it.

- Crown-jewel material held for the short list. Customer names, specific pricing, key contracts, and employee rosters are released only to a small set of serious, late-stage bidders — never in the first wave.

The tooling has to enforce all of that, which is where the document side I work on comes in. Dynamic watermarking stamps each viewer's identity across every page, so a leaked document is traceable to its source and buyers know it. An NDA gate blocks access to the CIM until the agreement is signed. And page-level analytics show exactly who opened what and when — so if a rumor starts, you have a record of who had access. In a market this interconnected, remember the rule: your buyer list is often also your competitor list. Treat every disclosure as if it might reach a rival, because in Richmond's business community it plausibly could. I run Peony, a data room company used by 5,900+ customers, precisely to make this staged, watermarked, permissioned release the default rather than a scramble.

Who advises the sale of a Richmond convenience-store, fuels, or car-wash business?

The specialist is Matrix Capital Markets Group, now operating inside Citizens JMP Securities (CRD #22208) after Citizens Financial Group acquired it in March 2026 — and in fuels and convenience stores, it is not a close call. Matrix is America's #1 advisor in that vertical, holding roughly 40% market share, with 21 of its 26 bankers dedicated to it, in a vertical that closed 35 deals in 2025 (up about 25% year over year). If you own a c-store chain, a fuels distributor, or a car-wash operator anywhere in the country — not just Richmond — this is the firm whose buyer list already has your ten most likely acquirers on it. Named deals that show the lane: Hutchinson Oil to Circle K (about 20 stores), Pri Mar Petroleum to Blarney Castle Oil, and West Oil.

This is the clearest example on the page of the fluency-over-address rule that governs the whole series. In a concentrated vertical like fuels-and-convenience, the specialist's buyer list beats any generalist's local relationship, because the specialist already knows — by name — the strategic consolidators and the sector-focused sponsors who will actually pay a premium multiple, and has probably sold to several of them before. A local generalist would have to go build that map from scratch, on your clock.

There is a live Richmond storyline that makes the vertical concrete. ARKO Corp / GPM Investments, headquartered in Richmond, is one of the largest convenience-store consolidators in the US — and 2025 was a pruning year for it, as it trimmed its footprint from about 1,389 to 1,118 company-operated stores while still making selective buys (Speedy Q's 21 stores in 2024, and an agreement in December 2025 to acquire Pride Convenience Holdings' 31 stores). So Richmond hosts both the country's #1 c-store M&A advisor (Matrix) and one of its largest c-store consolidators (ARKO) — the same deal universe, opposite sides of the table. I want to be precise: I am not claiming a specific Matrix-advised ARKO transaction; I am pointing out that the buyer engine and the specialist advisor for this vertical both live in Richmond, which tells you how deep the local sector expertise runs.

For a car-wash, building-products, or healthcare seller, Matrix's adjacent verticals apply the same way. The screening question is unchanged: ask for the last three closings in your exact sub-sector, with the buyers named. In this vertical, Matrix will have them.

Is Davenport & Company an M&A advisor, and what about the other Richmond wealth names?

Davenport & Company (FINRA CRD #1588) is a real, registered, 160-year-old firm with a genuine corporate-finance capability — but its identity is a regional generalist in wealth management and public finance, not a dedicated M&A boutique. So the honest answer is "yes, it can do corporate-finance work, but it is probably not the firm you hire to run a competitive sale of your $25M company before you have talked to the pure-plays." Davenport is worth its own section because it is the lone survivor of Richmond's old order and its name still carries real weight locally, which cuts both ways.

The case for taking it seriously: Davenport, founded in 1863 and 100% employee-owned (no single employee owns more than 10%), with roughly 400 associates across offices in Virginia, North Carolina, Maryland, and Georgia, states in its own SEC filings that it is "regularly engaged in the valuation of businesses and securities in connection with mergers, acquisitions..." — so it has a legitimate corporate-finance and valuation function, and it is a fully registered broker-dealer with real institutional depth. It is not a trap or a mislabel.

The case for calibrating expectations: Davenport's center of gravity is wealth management (70-plus financial advisors in Richmond alone) and municipal and public finance — underwriting bonds for localities and institutions. That is a different discipline from running a confidential competitive auction for a privately held operating company. I could not verify named private-company M&A sell-side mandates for Davenport to the standard this series holds, which is consistent with a firm whose corporate-finance work leans toward valuation, advisory, and public finance rather than founder-exit auctions. So I frame it as the elder-statesman regional generalist with a corporate-finance capability — a firm to respect, and possibly to consult, but not the first call for a competitive founder sale ahead of Transact Capital, Marriott & Co., or the exemption boutiques.

Now the sharper distinction. Davenport is a nuance; Cary Street Partners is a mislabel. Cary Street (CRD #128089) is primarily a wealth manager — nine business lines on BrokerCheck, majority stake sold to CIVC Partners in April 2025, actively acquiring RIAs (IFS Advisors, Pursuit Wealth) for its own book. Directories that file Cary Street under "Richmond M&A advisors" are simply wrong in a way they are not wrong about Davenport: Davenport at least has a real corporate-finance function, while Cary Street's M&A capability is genuinely secondary to a wealth-management identity. The clean test for both, and for any Richmond wealth name: read the BrokerCheck business lines, and ask for three named recent M&A closings with buyers identified. A dedicated M&A firm answers instantly; a wealth manager will (honestly) tell you that is not what they do.

Which Richmond "financial" names are not M&A advisors? A do-not-claim list

Every metro has firms whose names get miscataloged as M&A advisors; Richmond has a particularly rich set because it once had so many financial houses, and most of them are now dead, renamed, or absorbed. Here is the clearly-marked do-not-claim list — some legitimate firms doing other things, some genuinely defunct — but in each case the wrong number for selling your operating company.

- Cary Street Partners — primarily a wealth manager (CRD #128089), not a sell-side M&A advisory. Nine business lines on BrokerCheck; sold a majority stake to CIVC Partners in April 2025; buys RIAs for itself. It has a registered-but-secondary IB capability, but listing it as a Richmond M&A advisory misleads. (Full treatment above.)

- "Matrix Capital Group, Inc." (CRD #33364) — a defunct New York firm that ceased business in 2017. Not Richmond's Matrix. Richmond's Matrix team is now under Citizens JMP Securities (CRD #22208). Pulling #33364 expecting the fuels-and-c-store specialist gets you the wrong company.

- Scott & Stringfellow (broker-dealer CRD #6255) — one of the oldest names in Southern finance (founded 1893), but its broker-dealer ceased business January 2, 2013; its lineage lives inside Truist Securities. Not a live firm you can engage.

- Anderson & Strudwick (CRD #48) — defunct. Sold to Sterne Agee in 2011, wound down around 2013. Stale directories still list it as if it were active.

- Keiter — an excellent Richmond CPA firm, but its securities arm ("Keiter Capstone Securities" / CapGroup, CRD #47075) is deregistered. Keiter provides quality-of-earnings and transaction-advisory support — valuable in a deal — but it is not a registered dealmaker running your sale.

- Marriott & Co. is not Marriott International. Worth stating because the name collision is unavoidable: the Richmond M&A firm Marriott & Co. / Marriott Securities (CRD #149323, Three James Center, founded 2007, partner Justin Marriott) has nothing to do with Marriott International the hotel company. It is a legitimate registered middle-market advisor — this note is about the name, not a warning.

Two clarifications that belong here because stale lists get them backwards. Unregistered does not mean illegitimate: Dickinson Williams, Sterling Point, and Mann, Armistead & Epperson operate under the SEC M&A-broker exemption, which is normal and appropriate for pure sell-side advisory — explain it, do not red-flag it. And the marquee Richmond corporate deals were bulge-bracket engagements, never local mandates — do not let any directory attribute them to a hometown advisor. Dominion Energy's roughly $14B gas-distribution divestiture to Enbridge (closed across three tranches ending September 30, 2024), Altria's roughly $2.75B NJOY acquisition (closed June 2023), and Performance Food Group's roughly $2.1B Cheney Bros acquisition (closed October 2024) were all run by global banks, not by anyone on this page's local bench.

The point of the list is the sorting discipline, not disparagement. Before you take a firm's pitch as a sell-side advisor, confirm three things: that it is a registered broker-dealer (with a live CRD) or explicitly operates under the M&A-broker exemption; that it can name three recent closings with the buyers identified; and that a specific senior person will run your deal. Wealth managers, defunct houses, deregistered affiliates, and name-alikes fail that test fast.

Are Richmond's big companies actually buyers right now, and does that help me sell?

Yes — Greater Richmond hosts an unusually dense roster of large public acquirers for a metro its size, and their activity signals genuine strategic demand in the categories they touch, even though the marquee deals themselves fly to bulge-bracket banks. The region counts six Fortune 500 headquarters on the 2026 list, roughly $180.8B in combined revenue across its twelve Fortune-1000 companies — good for about 8th nationally: Performance Food Group (#80, roughly $59.9B revenue), CarMax (#162), Altria (#221), Markel Group (#270), Dominion Energy (#272), and Accendra Health (#407, the former Owens & Minor, renamed in December 2025). Below them sit Fortune 1000 names including Genworth, ARKO, Brink's, Everforth (the former ASGN, renamed April 2026), Universal, and NewMarket.

What this means for a seller, read honestly:

- Markel Group (Glen Allen) is a genuine serial acquirer through its Markel Ventures arm — recent buys include Valor Environmental (a 98% stake, June 2024) and Educational Partners International (68%, September 2024); on the insurance side, Markel also added the London marine specialist The MECO Group (June 2025). Markel Ventures actively buys quality private businesses to hold, which is exactly the kind of durable strategic demand a lower-middle-market seller wants in the ecosystem.

- ARKO Corp / GPM Investments (Richmond) is one of the largest US convenience-store consolidators — pruning in 2025 (about 1,389 to 1,118 stores) but still buying selectively (Speedy Q, 21 stores, 2024; agreed to acquire Pride Convenience's 31 stores, December 2025). Pair this with Matrix's c-store specialty and you have the vertical's advisor and one of its biggest buyers both headquartered in town.

- Performance Food Group is a live 2026 storyline: under activist pressure from Sachem Head, PFG entered an information-sharing arrangement with US Foods (September 16, 2025) to evaluate a potential merger; the two sides terminated that process on November 24, 2025, and PFG stayed standalone. The episode is still a reminder that even Richmond's largest names can be in play — and that scale-level M&A here is bulge-bracket territory.

Two honest caveats on the buyer engine. First, the big deals are not your comps — Dominion→Enbridge ($14B), Altria→NJOY ($2.75B), and PFG→Cheney Bros ($2.1B) were bulge-bracket engagements; do not let a stale list attribute them to a local advisor, and do not expect the local bench to run a deal at that scale. Second, some 2026 headlines are not completed M&A: Accendra Health's (Owens & Minor's) proposed $1.36B Rotech acquisition was terminated in 2025; LEGO's $1B-plus Chesterfield County factory topped out in October 2025 but does not open until 2027 (not an operating employer yet); and CoStar Group, though it is building a roughly $460M, ~1-million-square-foot research campus on the James River (completing around May 2026, ~3,500 employees), is headquartered in Arlington, not Richmond. For a seller, the takeaway is real strategic demand in food distribution, convenience retail, insurance-adjacent services, and specialty industrials — but a process that still needs national buyer reach, because the local strategics are a bonus, not a strategy. Once buyers are in the room, page-level analytics will tell you which ones actually engaged past the teaser.

Which national banks cover Richmond, and does any keep a real local office?

At least one keeps a genuine local presence, which separates Richmond from thinner-benched metros. The verified 2026 picture:

- Lincoln International keeps a Richmond branch office at 200 S. 10th St — a global mid-market investment bank with an actual local address. This is the clean "national walk-in option": when your deal scales past roughly $150M-$200M or into a vertical with a global buyer set, Lincoln gives you national reach with someone reachable in town. It is a branch, not a homegrown firm — but it is a real one.

- Harris Williams itself functions as the resident national option at the top of the local size range. Headquartered at 1001 Haxall Point, it competes on $200M-$1B-plus mandates as a national/global platform — so for a larger Richmond seller, the flagship in town is the national bank.

- Citizens now has a Richmond footprint through the Matrix acquisition — the Matrix team inside Citizens JMP Securities (CRD #22208) gives Citizens a resident, sector-specialist deal presence in the metro, concentrated in fuels, convenience stores, and adjacent verticals.

- The bulge-bracket and elite-boutique banks — Goldman Sachs, Morgan Stanley, and peers — cover Richmond from New York and show up only on the largest mandates (the Dominion- and PFG-scale deals). They keep no Richmond M&A office and are neither reachable nor appropriate for a founder-owned company.

The practical rule mirrors the rest of the series, with the Richmond twist that the "local flagship" is a national firm above your size. For a founder-owned deal up to roughly $150M, the boutiques on this page give you as much as an imported bank would, closer to home and with more senior attention per dollar. Past that, or in a specialist vertical where a particular national bank owns the buyer relationships, importing the specialist earns its fee. The test never changes: named buyers, named closings, named senior staffing — run the local and national options through the identical screen. For the Fifth District neighbor's bench, see our best M&A advisors in DC guide; for a Southeastern peer market, Nashville.

What does an M&A advisor cost to sell a $25M-$30M Richmond company?

For a $25M-$30M Richmond company, expect a monthly retainer plus a success fee at close, with a blended success fee in the low-single-digit percent. Independent middle-market data — the Axial/Firmex M&A Fee Guide 2024-25 (N=456) — puts blended success fees at roughly 4.8% at a $5M deal, about 3.4% at $20M, and around 2.0% by $100M, so a $25M-$30M sale sits in the low-3s percent on the success fee alone. Here is how the pieces work.

The formula. A declining-rate, Lehman-style structure is still the single most common, used in about 44% of engagements (versus roughly 26% flat-rate and 20% with an accelerator) — so do not believe anyone who tells you "nobody uses Lehman anymore." The modern default is Double Lehman (10-8-6-4-2%): 10% of the first $1M of consideration, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $4M. Run that on smaller checkpoints: a $10M deal computes to $400K (4.0%), a $20M deal to $600K (3.0%). The older Classic Lehman (5-4-3-2-1) is about half that — $200K on a $10M deal — and is now less common.

The retainer. Roughly five of six advisers charge one, typically $5,000-$10,000 per month (some charge a fixed $25K-$75K instead), and about 72% credit it against the success fee at closing (per a 2021-22 fee-guide survey) — but only if the engagement letter says so in writing, so negotiate the credit explicitly.

The minimum fee — the number that actually governs a small deal. Minimum fees appear in about 67% of engagement letters (2021-22 survey) and typically run $200K-$600K on $5M-$30M deals. On a deal at the smaller end of your range, it is often the floor, not the percentage, that sets the bill — a firm with a $400K minimum on your $25M deal is charging you a different effective rate than the Lehman math implies, so ask for the minimum first.

Three more terms deserve scrutiny:

- The tail period. Advisers often ask for 18-24 months, during which they collect if you sell to a buyer they introduced after the engagement ends. Negotiate toward 12 months, and require a named-buyer list within 10 days of termination — that list is your best defense against paying a tail on a buyer the advisor never actually sourced.

- Exclusivity. Typically 6-12 months — reasonable, but know the number.

- Expense caps. $25K-$50K is typical; cap out-of-pocket expenses so they cannot balloon.

Keep the whole cost conversation in proportion: the fee delta between two good Richmond advisors is almost always dwarfed by the price delta a competitive process produces. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — a predictable cost against an advisory fee that runs into six figures.

Which virtual data room should a Richmond seller actually use?

I run a data room company, so treat this as informed but interested — and I will be honest about where each tool fits. For a true $500M-plus mega-deal with hundreds of bidders and a bulge-bracket bank running the process, Datasite and Intralinks are the incumbents, and your banker may simply require one; their enterprise pricing typically starts around $50,000 or more per deal, which is rational at that scale and overkill below it. For the sub-$500M enterprise-value band that is the bulk of Richmond deal count — which is to say essentially every deal in this article, and certainly a $20M-$35M founder sale — you do not need an enterprise mega-platform and should not pay for one. Peony, iDeals, and FirmRoom all run clean, secure, modern sell-side processes at a fraction of that cost.

What actually matters for a Richmond lower-middle-market sale:

- Per-buyer permissions so strategics and financial buyers see different tiers of information, staged as separate access groups in one room — essential for the tiered disclosure a confidential process requires.

- Dynamic watermarking so a leaked teaser or CIM is traceable to the viewer who leaked it — critical when the likeliest bidders are the same companies you compete with every week.

- An NDA gate so nobody sees the named CIM until the agreement is signed.

- Page-level analytics so you can see which buyers genuinely engaged (and which never opened the CIM), which sharpens your advisor's follow-up and your read on real interest.

- Pricing that does not punish you per page or per gigabyte — a document-heavy diligence process should not inflate the bill.

We serve more than 5,900 customers, many running exactly the kind of founder-owned and family-business sales this article is about, and Richmond's lower-middle-market deals sit right in that band. For the full solution view, see our M&A data room solution. Whatever you choose, set the room up before you go to market — it is the cheapest lever you control, and the one that most reliably compresses the back half of the timeline.

Bottom line

Richmond was the Wall Street of the South, it sold every one of its investment banks to out-of-state buyers, and it rebuilt itself as a middle-market M&A capital instead. The old houses are gone — Craigie, Wheat First, Scott & Stringfellow, Branch Cabell, Anderson & Strudwick all yielded to outside partners, leaving only employee-owned Davenport & Company (CRD #1588) from the old order. But the second act built a real bench: Harris Williams (CRD #113930, 1001 Haxall Point) grew into one of the largest dedicated middle-market M&A advisers in the US and kept its Richmond HQ after selling to PNC in 2005, and in 2026 the specialist crown jewel Matrix Capital Markets Group (fuels and convenience stores, ~40% share) was acquired by Citizens Financial Group and now sits inside Citizens JMP Securities (CRD #22208).

For a founder, the practical consequence is counterintuitive: the city's famous flagship won't take your deal. Harris Williams fishes at $200M-plus and discontinued the sub-$200M arm that once served your size in 2011. Your real bench is the registered pure-play boutiques — Transact Capital Securities (CRD #133822) and Marriott & Co. / Marriott Securities (CRD #149323) — and the honest M&A-broker-exemption boutiques Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson, with Boxwood Partners (franchise/consumer) and a Lincoln International branch as the national options. The honest counters, held alongside the thesis: Richmond's marquee corporate deals (Dominion→Enbridge $14B, Altria→NJOY $2.75B, PFG→Cheney Bros $2.1B) were bulge-bracket engagements, never local mandates; and the metro's most dangerous mislabel — Cary Street Partners is a wealth manager, not a sell-side M&A advisory — is the one a stale directory is most likely to hand you. Verify every firm's current status on FINRA BrokerCheck, because in the city that sold its banks, even the 2026 specialist just changed hands. And whichever path you choose, build a clean, staged data room before you go to market. In the town that sold its Wall Street, the sellers who win are the ones who find the right boutique below the flagship — and still make it prove buyer reach, named closings, and senior attention before they sign.

Frequently asked questions about Richmond M&A advisors

I run a $25M-revenue company in Richmond — is Harris Williams too big for my deal?

Almost certainly yes, and there is a verified reason. Harris Williams (FINRA CRD #113930, headquartered at 1001 Haxall Point in Richmond, founded 1991, PNC-owned since 2005) is one of the largest dedicated middle-market M&A advisers in the United States, and its core mandates run roughly $200M to $1B-plus in enterprise value. Crucially, it used to run a sub-$200M arm called Cobblestone Advisors — but that arm was folded in and its brand discontinued on June 1, 2011, so Harris Williams largely does not take sub-$50M mandates today. For a $25M-revenue company with roughly $3.5M of EBITDA hoping for a $20M-$35M enterprise value, you are below its floor. The good news is that Richmond's renewal cycle built the bench for exactly you: when Harris Williams discontinued Cobblestone, a former Cobblestone managing director founded Dickinson Williams & Co. that same year (2011) to serve lower-middle-market deals up to about $150M. Your real shortlist is the registered pure-plays — Transact Capital Securities (CRD #133822, Glen Allen, $2M-$100M) and Marriott & Co. / Marriott Securities (CRD #149323) — plus the honest M&A-broker-exemption boutiques Dickinson Williams, Sterling Point Advisors ($5M-$100M+), and Mann, Armistead & Epperson. I run Peony, a data room company used by 5,900+ customers, and whichever you pick, a clean, staged room with page-level analytics is the cheapest lever you control before you even sign an engagement letter.

Should I hire a Richmond boutique or a national mid-market bank to sell my company?

For a $25M-revenue company, hire a Richmond boutique — and understand that the town's most famous name is a national bank that will pass on your deal. Richmond is unusual: its homegrown flagship, Harris Williams, grew into one of the largest dedicated middle-market M&A advisers in the US and kept its Richmond HQ even after selling to PNC in 2005, but it fishes at $200M-$1B-plus and discontinued its sub-$200M Cobblestone arm in 2011. So "go national" and "go local" collapse into the same fork most cities face only above roughly $150M-$200M of enterprise value. Below that — which is where a $20M-$35M deal sits — the registered pure-play boutiques (Transact Capital, CRD #133822; Marriott & Co., CRD #149323) and the exemption boutiques (Dickinson Williams, Sterling Point, Mann Armistead & Epperson) give you the senior banker who pitched you actually running the process, day to day, for a buyer universe that is regional-to-national rather than global. Reach for a national mid-market bank (Harris Williams itself, or the Lincoln International team with a Richmond branch office) only when your deal scales past roughly $150M-$200M or into a vertical with a genuinely global buyer set. The test never changes: named senior staffing, three named recent closings in your sub-sector, and the buyers on the other side. I run Peony, a data room company used by 5,900+ customers, and a clean data room is the lever you control before the banker is even chosen.

What's the difference between a business broker and an M&A advisor for a $25 million company?

A business broker lists smaller, owner-operated businesses (typically under ~$5M of enterprise value) to a pool weighted toward individual buyers, on a listing-and-commission model; an M&A advisor or investment bank runs a confidential, competitive, curated process for a middle-market company, marketing to strategic acquirers and private-equity firms and manufacturing tension among them. For a $25M-revenue company with roughly $3.5M of EBITDA, you are squarely in M&A-advisor territory, not business-brokerage territory — your best buyers are strategics and sponsors who will never see a broker's public listing, and reaching them confidentially is the entire job. The practical differences that matter: a broker often posts a semi-public listing, while an advisor markets from a blind teaser under NDA and never names your company early; a broker's buyer is usually an individual or a small operator, while an advisor's buyer is an institution that pays on multiples of EBITDA; and a broker's fee is a flat commission, while an advisor charges a retainer plus a success fee scaled to the deal. In Richmond, the registered boutiques (Transact Capital, Marriott & Co.) and exemption boutiques (Dickinson Williams, Sterling Point, Mann Armistead & Epperson) run true M&A processes at your size. For the full taxonomy, see our M&A advisor vs broker vs investment bank guide. I run Peony, a data room company; the tell is simple — deal people build a permissioned data room, brokers email a listing.

Are Richmond "M&A advisors" actually investment banks, or wealth managers in disguise?

Some are genuine sell-side M&A firms; the single most important one to flag is not — Cary Street Partners (FINRA CRD #128089) is primarily a wealth manager, not a sell-side M&A advisory, and listing it as one would mislead you. Cary Street carries nine business lines on BrokerCheck (mutual funds, annuities, municipal securities, and the like), sold a majority stake to the private-equity firm CIVC Partners in April 2025, and has been buying RIAs for itself (IFS Advisors, Pursuit Wealth). It has a registered-but-secondary investment-banking capability, but its identity is wealth management. The genuine Richmond sell-side bench is a different set: registered broker-dealers Harris Williams (CRD #113930, but $200M-plus), Transact Capital Securities (CRD #133822), and Marriott & Co. / Marriott Securities (CRD #149323); the honest M&A-broker-exemption boutiques Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson; and Matrix Capital Markets Group, now inside Citizens JMP Securities (CRD #22208). Davenport & Company (CRD #1588) is a real registered broker-dealer with a genuine corporate-finance capability, but its identity is wealth management plus municipal and public finance — a regional generalist, not a dedicated M&A boutique. The clean test: pull the CRD on FINRA BrokerCheck, read the listed business lines, and ask for three named recent M&A closings with buyers identified. I run Peony, a data room company used by 5,900+ customers; a firm that has never built a data room is not the one selling your company.

How do I check whether a Richmond M&A advisor is a registered broker-dealer?

Go to FINRA BrokerCheck (brokercheck.finra.org) and search the firm's exact legal name — it returns the CRD number, registration status, business lines, office locations, and any disclosures. For Richmond's bench that means confirming, for example, Harris Williams (CRD #113930), Transact Capital Securities (CRD #133822), Marriott Securities (CRD #149323), Davenport & Company (CRD #1588), and — for the former Matrix — Citizens JMP Securities (CRD #22208). Two Richmond-specific traps to watch. First, a firm returning no broker-dealer record is not automatically illegitimate: Dickinson Williams, Sterling Point Advisors, and Mann, Armistead & Epperson operate under the federal M&A-broker exemption that Congress codified in 2023, which lets qualified advisors facilitate the sale of privately held companies without full broker-dealer registration, subject to size and structure limits. That is a normal, appropriate model for pure sell-side advisory — confirm it rather than red-flag it, and for a stock deal ask how the securities piece is handled. Second, watch for name collisions and dead entities: "Matrix Capital Group, Inc." (CRD #33364) is a defunct New York firm, not Richmond's Matrix; Scott & Stringfellow (CRD #6255) and Anderson & Strudwick (CRD #48) are gone; and Keiter's securities arm (CRD #47075) is deregistered. I run Peony, a data room company; verifying the current entity, its current owner, and its current registration before you sign is the single cheapest piece of diligence you will ever do.

How long does it take to sell a $25 million company?

Plan on roughly 6-9 months from signing the engagement letter to close for a lower-middle-market sell-side, deal-dependent and longer if the financials need cleanup first. The rough shape: 4-8 weeks of preparation (clean financials, a quality-of-earnings build, the confidential information memorandum, and a data room); 2-4 weeks of buyer outreach under NDA, starting from a blind teaser that does not name your company; 3-5 weeks to collect indications of interest and build a short list; 4-6 weeks of management meetings and the lead-bid/LOI stage; then 8-12 weeks of confirmatory due diligence and definitive-agreement negotiation to close. For a $25M-revenue Richmond company, the advisor's core job throughout is to manufacture competitive tension across strategic buyers and private-equity platforms — which is exactly why a single unsolicited PE offer, taken without a process, tends to leave money on the table. The single biggest timeline risk is unprepared financials: sellers who walk in without a defensible quality-of-earnings picture add months and hand buyers leverage. I run Peony, a data room company used by 5,900+ customers, and a clean, staged data room built before you go to market is the most reliable way to compress the back half of the schedule — the confirmatory-diligence phase is where deals slow down or die, and preparation is the antidote.

A private equity firm reached out unsolicited — do I still need an M&A advisor?

Yes — in fact, an unsolicited private-equity inquiry is the moment you most need one, because it means a professional buyer has decided your company is worth pursuing before you have run any process to find out what it is worth. A PE firm that contacts a founder directly is trying to buy the company without competition, which is rational for them and expensive for you: without a competing bid, you have no leverage on price or terms, and a first-time seller rarely knows whether the offered multiple is generous or a lowball. An M&A advisor's job is to convert that single inbound into a competitive process — running a curated set of other credible strategics and sponsors against the party that called, under NDA and from a blind teaser, so price is set by the market rather than by the one buyer at the table. That competitive tension typically moves the outcome by far more than the advisor's fee. It also protects you on the things a first-time seller cannot see coming: the structure of the LOI, the earnout and rollover mechanics, the exclusivity and no-shop clauses, and the confirmatory-diligence gauntlet. In Richmond, the boutiques on this page (Transact Capital, Marriott & Co., Dickinson Williams, Sterling Point) run exactly this play at your size. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects you — staged disclosure through a permissioned room — is the same whether one buyer called or ten did.

Is one unsolicited PE offer enough, or should I run a competitive process?

Run a process — one unsolicited offer is a starting point, not a fair price. The whole reason competitive M&A processes exist is that price on a private company is not a fixed number; it is whatever a motivated buyer will pay when they know another motivated buyer is in the room. A single PE firm that reached out did so precisely because it hopes to transact bilaterally, without that pressure — and a first-time seller has no way to know whether its offer is at, above, or below what the market would clear. Running even a tight, confidential process against a curated short list of other strategics and sponsors does three things: it tests the offer against real alternatives, it moves price and terms in your favor through competitive tension, and it disciplines the original buyer, who now knows they cannot drag out diligence or re-trade the price without risking the deal. The objection founders raise is confidentiality — "I don't want the whole world to know I'm for sale." That is a real concern and a solvable one: a good advisor markets from a blind teaser under NDA and stages disclosure through a permissioned data room, so only serious, vetted buyers ever learn your identity. The cost of running a process is measured in months and a success fee; the cost of not running one is often measured in a materially lower price. I run Peony, a data room company used by 5,900+ customers, built for exactly this kind of staged, confidential release.

How do I sell my business without employees or competitors finding out?

You keep it confidential with staged disclosure enforced by a permissioned data room: a blind teaser first, the named confidential information memorandum only after a signed NDA, and the most sensitive material (customer names, pricing, employee rosters, key contracts) held back for a small short list of serious, later-stage bidders. This matters acutely for a Richmond specialty-distribution or business-services company, where your competitors, largest customers, and key employees may all know each other — a leak that you are "for sale" can spook a customer, embolden a competitor to poach staff, or unsettle the workforce before you have a signed deal. The structural defenses: the initial teaser describes the business (sector, size, financial profile) without naming it, so a recipient — including a competitor — cannot identify you from it; the full CIM goes only to NDA-signed buyers your advisor has curated to exclude the parties most likely to misuse it; and the crown-jewel material is released only in the final wave. The tooling has to enforce all of that: dynamic watermarking stamps each viewer's identity across every page so a leaked document is traceable to its source, an NDA gate blocks access until the agreement is signed, and page-level analytics show exactly who opened what and when. I run Peony, a data room company used by 5,900+ customers, precisely to make this staged, watermarked, permissioned release the default rather than a scramble — because your buyer list is often also your competitor list.

What are typical M&A advisor fees for a $25 million deal?

For a $25M deal, expect a monthly retainer plus a success fee at close, with a blended success fee landing in the low-single-digit percent. Independent middle-market data (the Axial/Firmex M&A Fee Guide 2024-25, N=456) puts blended success fees at roughly 4.8% at a $5M deal, about 3.4% at $20M, and around 2.0% by $100M — so a $25M sale sits near the low-3s to mid-3s percent on the success fee alone. The most common structure is still a declining-rate, Lehman-style formula: the classic Double Lehman (10-8-6-4-2%) charges 10% of the first $1M of consideration, 8% of the second, and so on, which on a $10M deal computes to $400K (4.0%) and on a $20M deal to $600K (3.0%); the older Classic Lehman (5-4-3-2-1) is roughly half that. Two numbers matter more than the headline percentage on a deal this size. First, the minimum fee: minimums appear in about two-thirds of engagement letters (per a 2021-22 fee-guide survey) and typically run $200K-$600K on $5M-$30M deals — so on a smaller deal it is the floor, not the percentage, that sets the bill. Second, the retainer: roughly five of six advisers charge one ($5,000-$10,000 per month, or a fixed $25K-$75K), and about 72% credit it against the success fee — but only if the engagement letter says so in writing. I run Peony, a data room company with flat per-admin pricing, a predictable line item against a six-figure advisory fee.

Do Richmond advisors still use the Lehman formula, and what retainer should I expect?

Yes — a declining-rate, Lehman-style formula is still the single most common fee structure, used in about 44% of engagements (versus roughly 26% flat-rate and 20% with an accelerator that raises the rate on higher tranches), so do not believe anyone who tells you "nobody uses Lehman anymore." The modern default is Double Lehman (10-8-6-4-2%): 10% of the first $1M of consideration, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $4M — which computes to $400K on a $10M deal (4.0%) and $600K on a $20M deal (3.0%). The older Classic Lehman (5-4-3-2-1) is about half those figures and is now less common. On the retainer: expect one from roughly five of six advisers, typically $5,000-$10,000 per month (some charge a fixed $25K-$75K instead), and about 72% of firms credit the retainer against the success fee at closing — negotiate that credit explicitly, in writing, because it is not automatic. Three more terms deserve scrutiny: the tail period (advisers often ask for 18-24 months, during which they collect if you sell to an introduced buyer — negotiate toward 12, and your best defense is requiring a named-buyer list within 10 days of termination); exclusivity (6-12 months); and any expense cap ($25K-$50K is typical). The fee delta between two good Richmond advisors is almost always dwarfed by the price delta a competitive process produces. I run Peony, a data room company used by 5,900+ customers.

Related resources

- The State of M&A Data Rooms — our platform benchmark on how sell-side processes actually run, across hundreds of deals in the sub-$500M band that covers most of Richmond.

- How to Build an M&A Data Room — the staged-disclosure playbook every Richmond seller should run before going to market.

- How to Write a CIM — the confidential information memorandum your advisor builds after the blind teaser.

- M&A Advisor vs Broker vs Investment Bank — the taxonomy every first-time seller should read before hiring anyone.

- Hard vs Soft Due Diligence — what buyers actually scrutinize in the confirmatory phase where deals slow down or die.

- Best M&A Advisors in Baltimore — the thematic twin: the town that sold everything and kept a thin bench, the closest peer to Richmond's "sold its banks" story.

- Best M&A Advisors in Milwaukee — the contrast: the city that kept its homegrown investment bank when it sold its commercial bank.