8 Best M&A Advisors in Kansas City for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: July 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led exits, family-business successions, PE recapitalizations, and strategic carve-outs — and Kansas City is the entry in our M&A advisor series where ownership structure, more than industry mix or bank density, decides what selling a company even means. Most "best Kansas City M&A advisors" pages fail a simple currency test: they still describe the flagship local firm by a name it gave up in January 2026, they mix the metro's two giant wealth managers into M&A lists, and they name firms that were absorbed or shut down years ago. At Peony we now serve more than 5,900 customers, and Kansas City sits squarely in the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark.

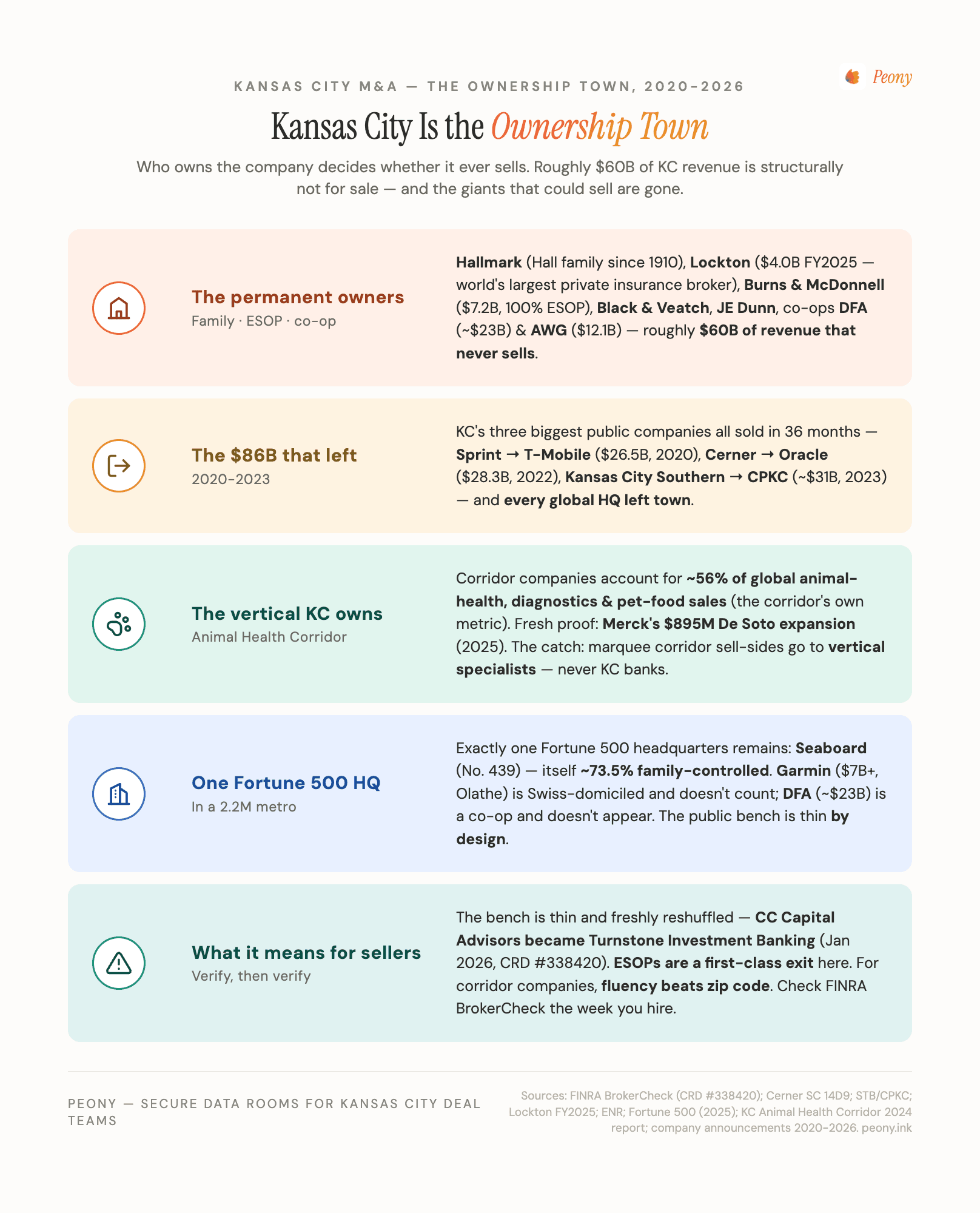

Here is the thesis I want you to internalize before you read another word: Kansas City is the Ownership Town. No other American metro's deal market is so completely shaped by who holds the equity. Roughly $60 billion of the metro's combined annual revenue sits in hands that structurally never sell — the Hall family's Hallmark (since 1910), the world's largest privately held insurance broker in Lockton ($4.0B in FY2025 revenue, its fifth straight year of double-digit organic growth), the 100%-employee-owned Burns & McDonnell ($7.2B) and Black & Veatch, family-and-employee-owned JE Dunn, and two of America's largest cooperatives in Dairy Farmers of America ($23B) and Associated Wholesale Grocers ($12.1B). Meanwhile, the three public giants that could sell all did — Sprint ($26.5B, 2020), Cerner ($28.3B, 2022), and Kansas City Southern ($31B, 2023) — roughly $86 billion in three years, and every global headquarters left town. What remains is a 2.2-million-person metro with exactly one Fortune 500 headquarters: Seaboard (No. 439), itself about 73.5% family-controlled.

That is not a sad story — it is a structural one, and it changes how you should sell a company here. It means the local sell-side bench is thin and must be verified, not assumed (the flagship just changed its name; more below). It means an ESOP is a first-class exit in this metro, not a consolation prize — the city's most admired employers are the proof. It means the one vertical where Kansas City genuinely owns the global table, the Animal Health Corridor, plays by vertical-specialist rules rather than local ones. And it means your buyer pool is national by necessity — the good news being that inbound capital (Panasonic's $4B gigafactory, Meta's $1B+ data center, Google's multi-billion-dollar campuses, CPKC's cross-border network) and homegrown consolidators (UMB's $2B Heartland acquisition, Creative Planning and Mariner rolling up wealth managers) are all writing checks in 2025-2026. This post is the working playbook I would hand to a Kansas City founder weighing a sale, a family-business owner weighing succession against an ESOP, or a corridor animal-health CEO fielding inbound interest. The frames come from cross-referencing FINRA BrokerCheck, SEC filings, and the verified 2020-2026 deal record against the region's structural specifics. I will be honest about the limits everywhere they exist.

Who are the best M&A advisors in Kansas City right now for $5M-$300M deals?

The Kansas City shortlist for 2026, sorted by tier and deal-size band — with the honesty banner up front: the genuinely-local registered bench is essentially one firm deep (and that firm has a new name as of January 2026), backed by credible non-registered boutiques, one national bank with a real local deal office, and the national and vertical-specialist banks that cover Kansas City from out of town.

| Firm | HQ / KC presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| Turnstone Investment Banking ★ (fka CC Capital Advisors) | Mission Woods, KS (lineage to 1994) | $5M-$100M+ EV | Industrials, construction & engineering services, consumer, agribusiness | Own FINRA broker-dealer (CRD #338420, approved June 2026) |

| Frontier Investment Banking | Leawood, KS (founded 1997) | $10M-$100M EV | Middle-market M&A, recaps, MBOs across manufacturing, services, logistics | M&A advisor (not a registered broker-dealer; M&A-broker model) |

| The DVS Group | Kansas City (founded 2004) | $2M-$50M EV | Buy-side, sell-side, and ESOP advisory for the lower middle market | M&A advisor (not a registered broker-dealer; M&A-broker model) |

| Piper Sandler (Leawood office) | Minneapolis HQ — genuine KC-metro IB office in Leawood | $100M+ EV | Healthcare investment banking plus a major public-finance practice | Established FINRA broker-dealer (CRD #665) |

| FORVIS Mazars Capital Advisors | Springfield, MO BD HQ — KC accounting office | $10M-$150M EV | Family- and entrepreneur-led M&A alongside the accounting relationship | Registered broker-dealer (CRD #43427) |

| Great Plains Capital Partners | Kansas City (Country Club Plaza) | $2M-$50M EV | Lower-middle-market generalist; names agriculture & animal health as a lane | M&A advisor (not a registered broker-dealer) |

| O'Keeffe & O'Malley | Kansas City (founded 1984) | $2M-$50M EV | Manufacturing, distribution, IT, and service businesses | M&A advisor (not a registered broker-dealer) |

| National middle-market banks | Chicago / Milwaukee / Minneapolis — no KC deal office | $75M+ EV | Harris Williams, William Blair, Lincoln, Baird, Houlihan Lokey cover KC remotely | Established FINRA broker-dealers |

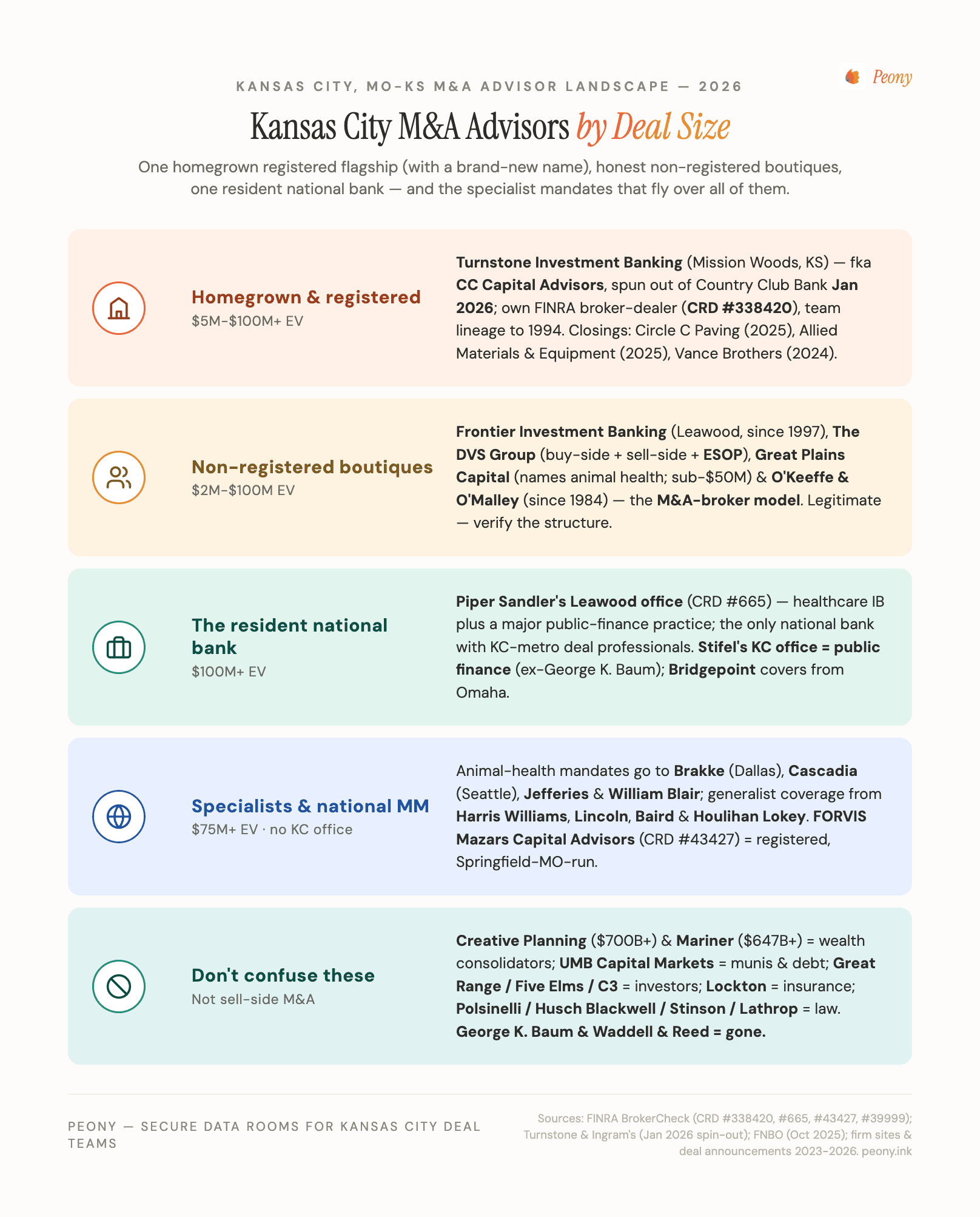

A few notes the table cannot carry. Turnstone Investment Banking is the homegrown flagship, and its story is the single most important current fact on this page: it is the firm formerly known as CC Capital Advisors, which spun out of Country Club Bank in January 2026 (after FNBO acquired the bank in October 2025) and received approval of its own FINRA broker-dealer registration — CRD #338420 — in June 2026. The team's lineage runs to Christenberry Collet & Company, founded 1994, and its published closings include Circle C Paving to Pavement Preservation Group (October 2025), Allied Materials & Equipment to Maple Hill Capital (March 2025), Vance Brothers to Pavement Preservation Group (November 2024), and Chance Rides to Permanent Equity (2023) — a genuinely local, genuinely registered, currently-active sell-side practice with a visible industrials and construction-services tilt. Frontier Investment Banking (Leawood, founded 1997) is the established non-registered alternative, claiming roughly $10B in lifetime transactions across manufacturing, services, and logistics. The DVS Group is the interesting one: born as a buy-side shop in 2004, it now runs sell-side and — uniquely for this metro — a dedicated ESOP practice, which in the Ownership Town is not a niche (more below).

Then the size-curve reality. Piper Sandler's Leawood office is the one national bank with a genuine KC-metro investment-banking presence — healthcare-tilted on the M&A side, plus one of the country's major public-finance practices — but it fishes at $100M+, so for most founder-owned deals it is the aspiration, not the first call. FORVIS Mazars Capital Advisors (CRD #43427, renamed from BKD in December 2024) is a real registered broker-dealer attached to the accounting firm — useful when the audit relationship is already there — but its broker-dealer is headquartered in Springfield, Missouri, and I could not confirm a dedicated KC-based deal team, so ask that question directly. Great Plains Capital Partners and O'Keeffe & O'Malley (the latter running since 1984) work the $2M-$50M band where much of the metro's actual deal count lives.

And the critical honesty point on the firms a Kansas City owner is most likely to already know: Creative Planning and Mariner are wealth managers, not M&A advisors — brilliant at rolling up RIAs, wrong number for selling your operating company; UMB's Capital Markets Division underwrites municipal bonds and manages debt, it does not run sell-sides; Lockton is an insurance broker; Great Range Capital, Five Elms, C3 Capital, Flyover, and KCRise are investors who might buy your company, not sell it; and Polsinelli, Husch Blackwell, Stinson, and Lathrop GPM are your lawyers, not your bankers. More on the sorting test below.

Why is Kansas City an "Ownership Town" — and what does that mean for selling my company?

Every city in this series has a structural signature. St. Louis is a Headquarters Town with a homegrown national bank; Cincinnati is a Brand Town whose consumer fluency lives out of town. Kansas City's signature is ownership itself: the metro's defining corporate fact is that its most important companies are built never to sell.

Walk the list, because the scale is startling:

- Hallmark — Hall family since 1910, roughly $3.5B in revenue, still private after 116 years.

- Lockton — the world's largest privately held insurance brokerage: $4.0B in FY2025 revenue, up 13%, essentially all organic, owned by the Lockton family and its producers. It is the company every private-capital firm in America would love to buy, and it will not return the call.

- Burns & McDonnell — $7.2B in 2024 revenue, 100% employee-owned through an ESOP since 1986, one of the largest employee-owned firms in the country.

- Black & Veatch — employee-owned, roughly $4.7B, currently planning a $1.34B new Overland Park headquarters campus.

- JE Dunn Construction — roughly $6.5B, family ownership plus an ESOP added in 2010.

- Dairy Farmers of America — a farmer-owned cooperative in Kansas City, KS with ~$23B in revenue. It would rank around #159 on the Fortune 500 by size; as a co-op, it does not appear at all.

- Associated Wholesale Grocers — a retailer-owned cooperative, $12.1B in 2024 sales across ~1,100 member companies.

That is roughly $60 billion of combined annual revenue that is structurally not for sale — held by families, employee trusts, and member-owners whose entire purpose is permanence. Add Seaboard (No. 439, the metro's only Fortune 500 company, ~73.5% controlled by the Bresky family) and Garmin (over $7B in revenue, operationally run from Olathe but legally domiciled in Switzerland, which is why it appears on no Fortune 500 list), and the pattern is total: Kansas City's corporate wealth lives in permanent hands.

What does this mean for you, a founder selling a $5M-$300M company? Three things. First, the local strategic-buyer bench is thinner than the metro's size suggests — the giants who might have been your acquirers either never sell or never buy companies like yours (a co-op buys milk plants, not your software firm), so a credible process needs national reach from day one. Second, the advisory bench matched the market and stayed small — one registered homegrown flagship, a handful of honest boutiques — which is why verification matters more here than in a bank-dense metro. Third, and most usefully: employee ownership is a first-class exit in this town, culturally normalized by its most admired employers, with real advisory infrastructure behind it. In most cities the ESOP conversation feels exotic; in Kansas City it is the hometown model.

What happened when Kansas City's public giants did sell? The $86 billion lesson

The inverse proof of the Ownership Town thesis is what happened to the companies that could sell. Between April 2020 and April 2023, Kansas City's three largest public companies all disappeared into out-of-town buyers:

- Sprint → T-Mobile ($26.5B all-stock, closed April 1, 2020). The Overland Park campus was sold and rebranded Aspiria; T-Mobile has said it will leave when its lease ends in 2029.

- Cerner → Oracle ($28.3B cash, closed June 8, 2022 — Cerner was advised by Goldman Sachs and Centerview Partners). Oracle has since closed Cerner's North Kansas City world headquarters, consolidated staff to a single south-KC campus, and is building Oracle's new global headquarters in Nashville.

- Kansas City Southern → Canadian Pacific (~$31B enterprise value; combined as CPKC April 14, 2023 — KCS was advised by BofA Securities and Morgan Stanley). CPKC's global headquarters is Calgary; Kansas City retains the designated U.S. headquarters.

Roughly $86 billion of headquarters value left in 36 months — and the pattern repeats at smaller scale: BATS Global Markets, the Lenexa-born stock exchange, sold to Cboe (~$3.2B, 2017; HQ to Chicago); Waddell & Reed sold to Macquarie ($1.7B, 2021; the brand is gone, the wealth arm flipped to LPL); Russell Stover sold to Lindt (2014, price undisclosed, press estimates ~$1.4B — though its HQ stayed); Boulevard Brewing sold to Duvel Moortgat (2013). Add Yellow Corp's 2023 collapse — the Overland Park trucker ceased operations that July, filed Chapter 11 in August, and its ~130 terminals were auctioned for ~$1.9B (XPO alone paid $870M) — and you have the full picture: the public side of Kansas City's economy has been a seller, and the marquee mandates all went to bulge-bracket banks, not the local bench. (The counter-example that stayed: AMC Entertainment remains headquartered in Leawood after Wanda's exit, and H&R Block is still a Kansas City public company.)

Two practical lessons for a founder. The marquee-deal advisor pattern — Goldman, Centerview, BofA, Morgan Stanley — tells you that when a Kansas City company is big enough, the advisory work flies over the local bench entirely; that is normal and not a knock on local firms, whose lane is the $5M-$150M founder economy. And the HQ-departure pattern tells you why the metro's civic energy now pours into inbound capital (Panasonic, the data centers, CPKC's US HQ) — which, as we will see, is where a current seller's tailwinds actually come from.

What just happened to CC Capital Advisors — and is Turnstone the same firm?

If you remember one current fact from this page, make it this one, because as of mid-2026 nearly every directory on the internet gets it wrong. CC Capital Advisors — the firm most Kansas City owners knew as the metro's flagship M&A shop and Country Club Bank's investment-banking arm — no longer exists under that name or that ownership. The sequence, verified against FINRA records and the firm's own announcements:

- 1994 — founded as Christenberry Collet & Company, an independent Kansas City M&A boutique.

- 2009 — joined Country Club Bank and operated for 15 years as CC Capital Advisors, the bank's M&A arm.

- October 2025 — FNBO (First National Bank of Omaha) acquired Country Club Bank; the bank's capital-markets unit began folding into FNBO's Northland Securities.

- January 8, 2026 — the M&A team departed and returned to full independence as Turnstone Investment Banking, based in Mission Woods, KS, led by managing director John Hense, with founder Terry Christenberry still on the roster.

- June 2026 — FINRA approved Turnstone's independent broker-dealer registration (operating as CC Capital Advisors LLC, CRD #338420, a Kansas registration).

So Turnstone is simultaneously the newest registered broker-dealer in this series and one of the oldest teams — a 30-year lineage under a five-month-old flag. Its published closings bridge the transition: Circle C Paving to Pavement Preservation Group (October 2025), Allied Materials & Equipment to Maple Hill Capital (March 2025), Vance Brothers (November 2024), Chance Rides to Permanent Equity (2023), with a visible strength in paving, construction materials, and industrial services.

The generalizable lesson is the reason this page exists: Kansas City's advisory bench reshuffled twice in twelve months, and any list written before January 2026 now points you to a bank arm that is being absorbed into an Omaha institution. Before you sign any engagement letter in this metro, pull the firm's current record on FINRA BrokerCheck — not because anyone did anything wrong here (this was an orderly, well-executed spin-out), but because currency is the whole game when the ground moves this fast.

Does Kansas City have a homegrown investment bank, or do I import one?

The honest answer: Kansas City has a genuine homegrown boutique bench but no homegrown institutional bank — and the institutional gap is structural, not cyclical. Unlike St. Louis (Stifel) or Minneapolis (Piper Sandler's HQ), Kansas City never grew a national investment bank, and the two institutions that might have become one both exited: George K. Baum & Company, the city's storied public-finance house (founded 1928), sold its core business to Stifel in 2019 — which is why Stifel's Kansas City office today is a public-finance office, not an M&A shop — and Waddell & Reed, the metro's asset-management flagship, sold to Macquarie in 2021 and vanished. (What remains under the Baum name, Baum Capital Partners, is a private-equity investor, not an advisor.)

So the homegrown bench you can actually hire is the one in the table: Turnstone (registered, CRD #338420), Frontier Investment Banking (Leawood, since 1997, non-registered), The DVS Group (buy-side, sell-side, and ESOP, non-registered), Great Plains Capital Partners and O'Keeffe & O'Malley at the smaller end — plus Piper Sandler's Leawood office, the one national bank that keeps genuine investment bankers in the metro (healthcare-tilted, alongside a major public-finance practice). One more nuance worth knowing because it confuses people: Bridgepoint Investment Banking, which markets actively in the region, is an Omaha firm with no Kansas City office — though in a small irony, the registered broker-dealer it transacts through, M&A Securities Group (CRD #39999), is based in Kansas City. The bankers are in Omaha; only the compliance entity is local.

For a larger or specialist process, you import: Harris Williams, William Blair, Lincoln International, Baird, and Houlihan Lokey all cover Kansas City from Chicago, Milwaukee, Minneapolis, and beyond, and the animal-health vertical has its own imported bench (next section). The practical rule mirrors the rest of this series: for a founder-owned deal up to roughly $100M, the genuinely-local firms give you senior attention that out-of-town banks reserve for bigger checks; above that, or in a specialist vertical, the imported bank earns its fee.

Who advises an animal-health, pet-care, or veterinary sale in the Animal Health Corridor?

Here is Kansas City's genuine claim to a global throne, and the sharpest sector lesson in this series. The KC Animal Health Corridor — the stretch from Manhattan, Kansas (home of K-State's vet school and the federal government's new $1.25B National Bio and Agro-Defense Facility) through the metro to Columbia, Missouri — hosts 300+ animal-health companies, supports 22,000+ direct jobs and about $10.5B of regional GDP, and by the corridor's own headline metric, companies with a corridor presence account for roughly 56% of global animal-health, diagnostics, and pet-food sales (a figure the corridor first published in 2014 and re-cited in its 2024 economic-impact report — treat it as the corridor's own broad metric, spanning pet food as well as pharmaceuticals). The anchors are blue-chip and current: Boehringer Ingelheim's St. Joseph site — in operation since 1917 and BI's largest US animal-health manufacturing plant, producing on the order of a billion vaccine doses a year, with a new R&D lab opened in 2024; Ceva Animal Health's North American HQ in Lenexa; Hill's Pet Nutrition's global HQ in Overland Park with plants in Topeka and Emporia; Mars Petcare and a Nestlé Purina technology center in the metro; and — the freshest proof — Merck Animal Health's $895M expansion in De Soto, announced May 2025. Every August, the corridor's Animal Health Summit runs an emerging-company forum whose presenting startups have collectively raised on the order of a billion dollars — it is the deal-flow event of the global vertical, held in Kansas City.

Now the honest part, and it is the part that matters if you own a company in this vertical: when corridor companies sell, Kansas City banks do not run the deals. The verified advisor credits on the vertical's marquee transactions: Bayer Animal Health's $7.6B sale to Elanco (2020) — Goldman Sachs for Elanco, BofA and Credit Suisse for Bayer. PetIQ's ~$1.5B take-private by Bansk (2024) — Jefferies. VIP Petcare's sale to Tractor Supply (May 2026) — William Blair for the seller, Centerview for Tractor Supply. Dechra's £4.5B sale to EQT — Investec. The vertical's specialist advisory bench sits everywhere except Kansas City: Brakke Consulting in Dallas (the animal-health industry's dedicated consultancy, still independent), Cascadia Capital's pet-and-animal-health practice in Seattle, the pet-sector coverage groups at Capstone and Corporate Finance Associates, and — for Missouri irony — R.L. Hulett's pet-industry M&A practice in St. Louis. The one Kansas City firm that names agriculture and animal health as a target sector, Great Plains Capital Partners, works sub-$50M deals.

So the playbook for a corridor founder: interview the vertical specialists first, wherever they sit, and make any local generalist prove — with named buyers — that it can reach the strategics (Merck, Zoetis, Elanco, BI, Mars, Nestlé Purina, Colgate's Hill's) and the sector sponsors who actually pay premium multiples in this vertical. Sector context for your timing conversations: pet-sector private-equity multiples compressed to a median of roughly 9.9x EV/EBITDA in 2025 from a 2024 peak near 16.8x, while strategics keep consolidating (Zoetis agreed to acquire Neogen's animal-genomics business for $160M in February 2026). One more corridor-specific discipline: your most likely buyers are each other's competitors, so run staged disclosure with dynamic watermarking from the first document — in a vertical this concentrated, your buyer list is your competitor list.

Is an ESOP a realistic exit for my Kansas City company?

In most metros this question is a footnote. In Kansas City it deserves its own section, because the city's crown-jewel employers are the national proof that employee ownership scales: Burns & McDonnell has been 100% employee-owned since 1986 and now runs at $7.2B in revenue; Black & Veatch is employee-owned at roughly $4.7B; JE Dunn added an ESOP to family ownership in 2010. When your employees' friends work at employee-owned firms — and the metro's engineering culture treats ownership as the crown jewels — selling to your own people reads as a first-class outcome, not a fallback.

The mechanics, honestly stated. An ESOP sells your stock to a trust for your employees at fair market value determined by an independent appraisal — not at the strategic premium a competitive auction can clear, and that gap is the core tradeoff. In exchange: sellers of C-corp stock can defer capital gains under Section 1042 by rolling proceeds into qualified replacement securities; a 100% ESOP-owned S-corp pays no federal income tax, which is why the structure compounds so well in professional-services and construction firms; you control timing and can sell in stages; and the company's identity, management, and workforce stay put — no small thing in a town that has watched three headquarters leave. The costs are real too: an independent trustee negotiates against you, the transaction stack (feasibility study, valuation, trustee counsel, plan design) runs into the hundreds of thousands, and the company carries an annual repurchase obligation to departing employee-owners forever after.

Who advises one: locally, The DVS Group runs a dedicated ESOP practice alongside its buy-side and sell-side work, and Optimum Transitions works the space; nationally, ESOP-specialist investment banks and trustee-side counsel matter as much as your own advisor. The decision framework I would use: if your priority ranking is legacy-workforce-taxes-timing, feasibility-test an ESOP before running a market process; if it is headline price, run the auction — and know that a good advisor can run the two in parallel as a real market check. Either way the diligence is identical in kind: the trustee's appraiser wants the same clean financial picture a strategic buyer would, staged through the same data room discipline.

Are Kansas City's companies actually buying right now — and does that help me sell?

Yes — but Kansas City's 2025-2026 buyer engine has an unusual shape: it is consolidators and inbound infrastructure, not a bench of Fortune 500 strategics. The verified record:

- UMB Financial closed its largest-ever acquisition in January 2025 — roughly $2.0B in stock for Denver's Heartland Financial — vaulting to ~$68B in assets. Kansas City's oldest bank is a buyer.

- The wealth consolidators. Two of America's most acquisitive wealth-management firms are headquartered in this metro: Creative Planning (Overland Park; $700B+ in assets under management and advisement; roughly 31 acquisitions including October 2025's $250B SageView deal) and Mariner (Leawood; $647B+; opened 2026 with a $1.8B dual acquisition and sold its $31B advisor network to LPL in April 2026). If you own an RIA or adjacent business, your most aggressive national buyers are local. For everyone else, they are proof of the metro's deal sophistication — on the buy side.

- Dairy Farmers of America bought Dean Foods' fluid-milk plants out of bankruptcy for $433M (2020) — the co-op as consolidator.

- The inbound wave. Panasonic's $4B De Soto gigafactory — one of the largest battery plants in North America — began mass production July 14, 2025 (with the honest caveat that its full four-line ramp has slipped past the original 2027 target amid softer EV demand). Meta's $1B+ Kansas City data center went live in August 2025; Google is building a second KC campus backed by up to $10B in Port KC bond authorization; local reporting counts dozens of data-center projects metro-wide. The new $1.5B KCI terminal (2023) and CPKC — the only single-line railway connecting Canada, the US, and Mexico, with its US headquarters in KC, $15.1B in 2025 revenue, and Americold's new $120M cold-storage hub at its KC intermodal terminal — round out the picture.

- The professional infrastructure. Kansas City-founded Polsinelli crossed $1B in revenue in 2025 (No. 55 in the Am Law 100); the KC Fed hosts Jackson Hole; Five Elms Capital closed its largest-ever fund ($1.1B Fund VI) for B2B software; Great Range Capital runs Midwest lower-middle-market buyouts from Leawood.

What it means for a seller: demand is genuine and rising for industrial, construction-services, logistics, food-and-ag, and services assets — the categories the inbound wave feeds — and sponsor capital (local and national) is active in exactly the $5M-$100M band this page covers. But because marquee local strategics are scarce (one Fortune 500 HQ, and it is a family-controlled agribusiness), your process must prove national reach rather than assume a hometown buyer. In practice that is the first screening question for any advisor on this page: show me the out-of-market buyers you brought to your last three closings. And when they bring them, page-level analytics will tell you which ones actually read past the teaser.

Which national banks cover Kansas City — and does any keep a real local office?

One does, and the rest fly in. The verified 2026 picture:

- Piper Sandler keeps a genuine multi-disciplinary office in Leawood — healthcare investment banking plus one of the country's major public-finance practices (CRD #665). It is the exception: a national bank with actual deal professionals resident in the metro, though its M&A lane starts around $100M.

- Stifel's Kansas City presence is the public-finance business it acquired from George K. Baum in 2019 — municipal bonds, not company sales. Its middle-market M&A covers KC from St. Louis and elsewhere.

- Harris Williams, William Blair, Lincoln International, Baird, Houlihan Lokey — no Kansas City deal office that I could verify; they cover the metro from Chicago, Milwaukee, Minneapolis, and the coasts, and they are the right call as deals scale past ~$75M-$150M or specialize (Blair's William Blair ran the sell-side of VIP Petcare, the corridor-adjacent deal of 2026).

- Bridgepoint Investment Banking covers KC from Omaha (its KC-based broker-dealer of record notwithstanding), and FORVIS Mazars Capital Advisors (CRD #43427) brings a registered, accounting-affiliated platform whose broker-dealer is run from Springfield, MO.

The takeaway is the same fluency-over-address rule that governs the whole series, with a KC-specific twist: because the local bench is one registered flagship plus boutiques, the "local vs national" decision arrives earlier on the size curve here than in Chicago or Dallas. A $150M industrial sale in this metro is almost certainly an imported-bank mandate; a $30M founder sale is almost certainly better served by Turnstone, Frontier, or DVS-tier senior attention. In between, run both kinds through the same test: named buyers, named closings, named senior staffing.

Don't mistake a wealth manager for a deal advisor — the Creative Planning and Mariner trap

Every metro has this trap; Kansas City has the largest version of it in the country, because the metro's two most famous financial brands are both wealth managers — and both are so good at acquiring that owners reasonably assume they must also sell. They do not, and the numbers make the confusion understandable: Creative Planning (Overland Park, founded by Peter Mallouk) reports over $700 billion in assets under management and advisement and has made roughly 31 acquisitions, including the $250B SageView deal; Mariner (Leawood, Marty Bicknell) reports $647B+ and opened 2026 with a $1.8B dual acquisition. These are two of the most acquisitive financial-services firms in America — as buyers of wealth managers.

The sorting logic: a wealth manager grows and protects your capital, especially post-liquidity; an investment bank or M&A advisor runs the competitive process that creates the liquidity. Three KC-specific notes. First, if you own an RIA, a retirement-plan practice, or an adjacent business, Creative Planning and Mariner flip categories — they may literally be your best buyers, which is exactly why they cannot be your advisor. Second, Mariner does market an investment-banking-and-valuation service line; it is delivered through affiliates (its captive broker-dealer, MSEC LLC, CRD #154327, plus partner networks) rather than as an independent investment bank — a legitimate structure, but ask precisely who runs your process, through which broker-dealer, and against what fee model. Third, the metro's other famous financial names sort the same way: UMB and Commerce are banks whose capital-markets desks do bonds and debt, not sell-sides; Lockton is the world's largest private insurance broker, not an advisor; and the private-capital names (Great Range, Five Elms, C3, Flyover, KCRise) are investors. The clean test never changes: ask any firm for its broker-dealer CRD (or an explicit statement that it operates as a non-registered M&A advisor), three named closings with buyers identified, and the senior person who will run your deal. On the document side, I run Peony, a data room company, and a telling early signal is whether the "advisor" pitching you insists on a real, permissioned data room — wealth managers email PDFs; deal people build rooms.

Does the Kansas-vs-Missouri state line matter for my sale?

Kansas City is the only two-state metro in this series — the state line runs through the middle of town, and the corporate map splits accordingly: Hallmark, Lockton, Burns & McDonnell, JE Dunn, and H&R Block on the Missouri side; Black & Veatch, Garmin (Olathe), Seaboard (Merriam), AMC (Leawood), and Dairy Farmers of America (Kansas City, Kansas) on the Kansas side. So does the line matter when you sell?

For your buyer list and your price: no. Buyers underwrite cash flow, market position, and management; no acquirer has ever paid a different multiple because the parking lot is in Johnson County rather than Jackson County. For the machinery of the deal: yes, in three specific ways. First, entity law — which state's statutes govern your corporation or LLC, your non-competes, and your required consents; your purchase agreement's reps and closing mechanics follow. Second, state taxes — Kansas and Missouri treat business income, pass-through elections, and capital events differently, and on a $25M-$100M sale the delta is real money; model it with your CPA at the start of the process, because some structures (asset vs stock, F-reorganizations, ESOP alternatives) shift the answer. Third, advisor registration — broker-dealer and M&A-broker rules run state by state; Turnstone's new registration (CRD #338420), for instance, is a Kansas registration. None of this is exotic — Polsinelli, Stinson, Lathrop GPM, and Husch Blackwell handle two-state closings in their sleep — but the sellers who get surprised are the ones who operated informally across the line for years (a Missouri entity, a Kansas warehouse, employees in both) and never papered it. Diligence will find it, so find it first: pull both states' filings, registrations, and tax accounts into the data room in week one, not after a buyer's counsel asks.

Who advises a Kansas City industrial, construction-services, or distribution sale?

This is the local bench's home turf, and the fit is almost suspiciously good: the metro's economy runs on engineering, construction, building products, and logistics (Burns & McDonnell, Black & Veatch, JE Dunn, CPKC, AWG), and the flagship local bank's published closings live in exactly that world — Turnstone's recent record is paving companies, construction materials, and industrial services (Circle C Paving, Vance Brothers, Allied Materials & Equipment). For a founder-owned industrial, construction-services, distribution, or logistics company in the $5M-$100M band, Turnstone is the natural first call, with Frontier Investment Banking (whose sector list spans manufacturing, logistics, and services) and The DVS Group as credible alternatives — and the ESOP option deserves a real look in this category, because construction and engineering services are precisely where the S-corp ESOP tax structure compounds best and where Kansas City's cultural proof lives. As deals scale past ~$100M, or when the buyer universe is national PE platforms rolling up your niche, the imported banks (Lincoln, Baird, Harris Williams, Houlihan Lokey) bring deeper sponsor coverage — at the cost of fly-in attention. Sector tailwind worth naming in your CIM: the inbound construction wave (Panasonic, the data-center buildout, Black & Veatch's own $1.34B campus) is exactly the demand engine a regional industrial-services buyer pool prices in. The screening question is unchanged: the last three closings in your sub-sector, with buyers named.

Who advises a Kansas City food, agribusiness, or consumer sale?

Kansas City's food-and-ag economy is enormous but co-op-heavy — DFA (~$23B) and AWG ($12.1B) are member-owned, Seaboard is family-controlled, and the metro's famous consumer names have already traded (Russell Stover to Lindt, 2014; Boulevard to Duvel, 2013). What that means for a founder: the strategics who buy Kansas City food businesses are mostly national and global (and the co-ops do buy — DFA took Dean Foods' plants for $433M — but they buy infrastructure, not brands), so a food, beverage, ag-services, or pet-food sale here is a national-process category from the first call. The corridor overlay is the differentiator: if your product touches animal health or pet food, you are in the one vertical where Kansas City is the global center — and the specialist rule from the corridor section applies (Brakke, Cascadia, the pet-coverage groups, William Blair on the vertical's 2026 marquee deal). For mainstream food and beverage below ~$100M, the local bench (Turnstone's agribusiness lane, Frontier, Great Plains — the latter explicitly naming agriculture) can run the process if it proves reach to the national strategic and sponsor set; above that, or for a branded consumer asset, the imported consumer-specialist banks earn the fee. One honest structural note: this is the series' repeat lesson that a city's economic identity and its advisory market are different things — Kansas City processes a staggering share of America's food, but the banks that sell food companies sit in Chicago and beyond.

How do I tell a real FINRA investment bank apart from a business broker in Kansas City?

Kansas City has three different kinds of firm that all describe themselves as "M&A advisors," and the state of the local market — one newly-registered flagship, many exempt boutiques, two giant wealth brands — makes the sorting test more load-bearing here than in any city since we started this series.

- Registered broker-dealers. Turnstone holds its own registration (CRD #338420, approved June 2026). Piper Sandler (CRD #665) and FORVIS Mazars Capital Advisors (CRD #43427) are registered. The national banks all are.

- Non-registered M&A advisors (the M&A-broker model). Frontier Investment Banking, The DVS Group, Great Plains Capital Partners, and O'Keeffe & O'Malley operate without their own broker-dealer registration — a legitimate, common model under the federal M&A-broker exemption (codified in 2023) for sales of privately held companies, subject to size and structure limits. Verify the model, and for a stock sale confirm how the securities piece is handled.

- Everyone else who sounds like an advisor. Wealth managers (Creative Planning, Mariner), bank capital-markets desks (UMB, Commerce — bonds and debt, not sell-sides), investors (Great Range, Five Elms, C3, Flyover, KCRise, Baum Capital Partners), insurance (Lockton), and law firms (Polsinelli, Husch Blackwell, Stinson, Lathrop GPM). None runs a competitive sale of your company.

Start at FINRA BrokerCheck, and remember the currency lesson this metro just taught: check the current record, because a directory from 2025 will tell you to call a bank arm that no longer exists. The clean test for any firm: its CRD (or an explicit non-registered statement), three named recent closings with buyers identified, and the senior person who will actually run your deal. If a firm cannot answer all three crisply, that is your answer.

Who handles sub-$5M Main-Street business sales in Kansas City?

Below roughly $5M of enterprise value you are in business-brokerage territory, and Kansas City has a deep main-street bench — O'Keeffe & O'Malley works down into this band, and the metro supports numerous brokers (Apex Business Advisors and franchise-network offices among them) handling restaurants, trades, small distribution, and owner-operator companies. It is a legitimate, different market: listing-driven, individual-buyer-weighted, lower absolute fees. Two Kansas City-specific notes. First, the crossover zone (~$3M-$8M) rewards a second opinion — a company with $1M+ of real EBITDA and professional financials can often graduate to a true competitive process at Turnstone/Frontier/DVS tier, where sponsor and strategic tension routinely outbids the individual-buyer market by more than the fee difference. Second, the ESOP question reaches surprisingly far down-market here — DVS works ESOPs in the lower middle market, and for a $4M-$8M services firm with a strong second layer of management, employee ownership can beat a thin individual-buyer pool. If your company is genuinely lower-middle-market, you have outgrown the main-street model; act like it.

Is now a good time to sell my Kansas City business?

The honest answer is that timing the macro matters less than your own readiness, but Kansas City's 2026 tailwinds are real and specific. Sponsor capital is active in the lower middle market (Five Elms just raised its largest fund; Great Range deploys locally; national platforms fly in for every quality industrial asset), the inbound-capital wave (Panasonic, Meta, Google, CPKC's network buildout) is feeding demand for construction-services, industrial, and logistics companies, and the metro's consolidators (UMB, the wealth giants) prove in-region checks clear. The counterweights: pet-and-animal-health multiples have come off their 2024 peak (median ~9.9x vs ~16.8x — still healthy, no longer euphoric), the EV-supply-chain ramp has visibly slowed (Panasonic's delayed full ramp is the honest marker), and financing costs still shape sponsor bids. Net: for a prepared seller in industrials, services, logistics, food-and-ag, or the corridor vertical, this is a genuinely good window; for a seller whose financials need a year of cleanup, the window matters less than the cleanup. The single biggest determinant of outcome is unchanged: a defensible quality-of-earnings picture, an advisor who can name your actual best buyers, and a clean data room before launch — the three things you control regardless of the cycle.

What's a reasonable success fee for a $25M Kansas City sell-side?

For a $25M Kansas City company, a blended success fee around 3-3.5% is squarely normal, typically a monthly retainer plus a success fee at close on a Double Lehman scale (10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, 2% above $5M — about $700K, or roughly 2.8%, on $25M, landing near 3-3.5% once minimums and uncredited retainer are added). Retainers run roughly $5,000-$25,000 per month at a boutique and are often credited against the success fee — but only if the engagement letter says so in writing. Watch three things more than the headline percentage: the base the fee applies to (total enterprise value including assumed debt and earnouts, or just cash at close), the tail period (banks ask for 18-24 months; negotiate toward 12), and any minimum-fee floor. Kansas City adds one comparison the rest of the country rarely runs: the ESOP alternative prices differently — a fixed professional-fee stack (feasibility, independent valuation, trustee counsel, plan design) that typically totals less than a success fee on the same company, in exchange for a fair-market-value price rather than an auction premium. Run both models on your actual numbers before anchoring on either. The fee delta between two good advisors is almost always dwarfed by the price delta a competitive process produces. I walk through the full fee math in the FAQ below.

Which virtual data room should a Kansas City seller actually use?

I run a data room company, so treat this as informed but interested — and I will be honest about where each tool fits. For a true $500M+ mega-deal with hundreds of bidders, Datasite and Intralinks are the incumbents, and your banker may simply require one. For the sub-$300M enterprise-value band that is the bulk of Kansas City deal flow — which is to say almost every deal in this article — you do not need an enterprise mega-platform, and you should not pay for one. Peony, iDeals, and FirmRoom all run clean, secure, modern sell-side processes at a fraction of the cost. What actually matters for a Kansas City lower-middle-market sale: per-buyer permissions so strategics, sponsors, and (in an ESOP) the trustee's advisors see different tiers, dynamic watermarking and screenshot protection so a leaked teaser is traceable — remember, in the corridor vertical your buyer list is your competitor list — page-level analytics so you can see which buyers are genuinely engaged, and pricing that does not punish you per page or per gigabyte. We serve more than 5,900 customers, many running exactly the kind of founder-owned and family-business sales this article is about. Whatever you choose, set the room up before you go to market — it is the cheapest lever you control.

Bottom line

Kansas City is the Ownership Town — the metro where who holds the equity decides everything. Roughly $60B of annual revenue sits in family, ESOP, and cooperative hands that never sell (Hallmark, Lockton, Burns & McDonnell, Black & Veatch, JE Dunn, DFA, AWG); the three public giants that could sell all did, for roughly $86B between 2020 and 2023, and every global HQ left; and the metro now has exactly one Fortune 500 headquarters, a family-controlled agribusiness. For a founder, the practical consequences: the genuinely-local bench is short and freshly reshuffled — anchored by Turnstone Investment Banking, the flagship formerly known as CC Capital Advisors, independent again since January 2026 with its own FINRA registration (CRD #338420) — backed by honest non-registered boutiques (Frontier, The DVS Group, Great Plains, O'Keeffe & O'Malley) and one national bank with a real local office (Piper Sandler, Leawood). An ESOP is a first-class exit here, culturally proven by the city's crown-jewel employers. In the Animal Health Corridor — the one vertical where KC owns the global table — sector fluency beats zip code, and the specialist bench sits out of town. Do not mistake the wealth giants (Creative Planning, Mariner) for deal advisors, verify every firm's current status on FINRA BrokerCheck (this metro just taught the internet why), and build a clean data room before you go to market. In the Ownership Town, the sellers who win are the ones who understand what kind of owner they want to become next.

Frequently asked questions about Kansas City M&A advisors

Should I hire a local Kansas City M&A boutique or a national investment bank to sell my company?

Hire a genuinely-local firm when your deal is in the ~$5M-$100M band and your best buyers are reachable strategics and middle-market sponsors; go national or vertical-specialist once the deal climbs toward $150M+ or your category is one where sector relationships decide the price. The KC wrinkles: the local bench just reshuffled (Turnstone, formerly CC Capital Advisors, now holds CRD #338420 — verify current status, not directory memory), and for Animal Health Corridor companies the buyers who pay the most are reached by vertical specialists (Brakke, Cascadia, Jefferies, William Blair) wherever they sit. Price comes from competitive tension, not a banker's zip code — and a clean, staged data room with page-level analytics is the cheapest lever you control either way.

I own a ~$25M Kansas City company — who are the best M&A advisors for a lower-middle-market sale?

The genuinely-local shortlist: Turnstone Investment Banking (Mission Woods, KS — the homegrown flagship, own FINRA registration CRD #338420, team lineage to 1994, published closings including Circle C Paving in October 2025 and Allied Materials & Equipment in March 2025), Frontier Investment Banking (Leawood, since 1997, non-registered), and The DVS Group (buy-side, sell-side, and ESOP, non-registered), with Great Plains Capital Partners and O'Keeffe & O'Malley at the smaller end and Piper Sandler's Leawood office fishing higher up the curve. Turnstone holds its own broker-dealer registration; Frontier, DVS, and Great Plains operate under the M&A-broker exemption — verify and structure accordingly. Ask every firm for its last three closings in your sub-sector with buyers named.

What happened to CC Capital Advisors — is Turnstone Investment Banking the same firm?

Same team, new name, new independence. Founded 1994 as Christenberry Collet & Company; joined Country Club Bank in 2009 and ran 15 years as CC Capital Advisors; FNBO acquired Country Club Bank in October 2025; the team spun out as Turnstone Investment Banking on January 8, 2026 (Mission Woods, KS, led by John Hense, founder Terry Christenberry still aboard); FINRA approved its independent registration — CRD #338420 — in June 2026. Any list still describing "CC Capital Advisors, Country Club Bank's M&A arm" is describing a firm that no longer exists in that form. Verify current status on FINRA BrokerCheck the week you hire, not the year the directory was written.

Who advises the sale of an animal-health, pet-care, or veterinary company in the Kansas City Animal Health Corridor?

Almost always a vertical specialist or national bank, not a KC generalist. The corridor is real — ~56% of global animal-health, diagnostics, and pet-food sales by its own metric, with Boehringer's largest US plant (St. Joseph), Ceva's North American HQ (Lenexa), Hill's (Overland Park), and Merck's $895M De Soto expansion — but the vertical's marquee sell-sides went to Goldman/BofA/Credit Suisse (Bayer-Elanco, $7.6B), Jefferies (PetIQ-Bansk, ~$1.5B), and William Blair opposite Centerview (VIP Petcare-Tractor Supply, 2026). The specialist bench — Brakke (Dallas), Cascadia (Seattle), the pet groups at Capstone and CFA — sits everywhere except KC; the one local claimant (Great Plains) works sub-$50M. Interview the specialists first, and run staged disclosure with dynamic watermarking — in this vertical, your buyer list is your competitor list.

Is my Creative Planning or Mariner advisor able to sell my business, or do I need an investment bank?

You need an investment bank or M&A advisor — your Creative Planning or Mariner advisor manages wealth. The confusion is understandable because both are famous and both acquire constantly: Creative Planning ($700B+ in assets under management and advisement, ~31 acquisitions including the $250B SageView deal) and Mariner ($647B+, a $1.8B dual acquisition to open 2026) are two of America's most acquisitive wealth consolidators — as buyers of RIAs. That skill does not transfer to running a competitive sell-side for your operating company. (Mariner markets an investment-banking-and-valuation line delivered through affiliates — ask exactly who runs your process and through which broker-dealer.) Sequence, don't substitute: the bank creates the liquidity; the wealth manager plans what happens to it.

Is an ESOP a realistic exit for my Kansas City company, and who advises one?

Yes — Kansas City is the best proof-of-concept city in America: Burns & McDonnell ($7.2B, 100% employee-owned since 1986), Black & Veatch, and JE Dunn are the metro's crown-jewel employers. An ESOP sells to an employee trust at fair market value set by independent appraisal — below a strategic-auction premium, in exchange for Section 1042 capital-gains deferral (C-corp), zero federal income tax for a 100% S-corp ESOP, staged timing, and a company that stays put. It is governance-heavy (independent trustee, annual repurchase obligation) and the professional-fee stack is real. Locally, The DVS Group runs a dedicated ESOP practice and Optimum Transitions works the space. If your priorities rank legacy-workforce-taxes-timing above headline price, feasibility-test an ESOP before — or alongside — a market process; the trustee's appraiser wants the same clean data room a buyer would.

Does it matter whether my company is on the Kansas or Missouri side of the metro when I sell?

Not for your buyer list or your multiple — buyers pay for cash flow, not zip codes. It matters for the machinery: which state's law governs your entity and non-competes, where filings and consents happen, and how each state taxes your gain (Kansas and Missouri differ; on a $25M-$100M sale the delta is real money — model it with your CPA at the start). Advisor registration also runs state by state — Turnstone's new registration (CRD #338420) is a Kansas registration. The sellers who get surprised are the ones who operated informally across the line for years; pull both states' filings, registrations, and tax accounts into the data room in week one.

Are Kansas City's big companies actually buyers right now, and does that help me sell?

Yes, but the engine is consolidators and inbound capital rather than Fortune 500 strategics: UMB closed its largest-ever deal (~$2.0B for Heartland Financial, January 2025); Creative Planning and Mariner are rolling up wealth managers nationally; DFA bought Dean Foods' plants ($433M); and the inbound wave is enormous — Panasonic's $4B gigafactory (mass production since July 2025, full ramp honestly delayed), Meta's $1B+ data center (live August 2025), Google's up-to-$10B second campus, CPKC's $15.1B network with Americold's $120M KC hub. Demand is genuine for industrial, logistics, food-and-ag, and services assets — but with one Fortune 500 HQ in the metro, your process still must prove national buyer reach. Page-level analytics will tell you which buyers actually engaged.

How does a sell-side M&A process work for a Kansas City company, and how long does it take from advisor hire to close?

Five overlapping stages, typically 6-9 months from engagement letter to close: 4-8 weeks of preparation (clean financials, quality-of-earnings, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA from a blind teaser; 3-5 weeks collecting indications of interest; 4-6 weeks of management meetings and the LOI stage; then 8-12 weeks of confirmatory diligence and definitive-agreement negotiation. In Kansas City the advisor must prove national reach (the local strategic bench is thin by design) while sponsor and inbound demand carries the industrial, logistics, and food-and-ag categories. An ESOP alternative runs 4-6 months of feasibility, valuation, and trustee negotiation. The biggest timeline risk is unprepared financials; a clean, staged data room built before launch is the most reliable way to compress the back half.

What do buyers diligence, and how do I set up a data room before going to market with my Kansas City company?

Buyers diligence durable, transferable cash flow — normalized EBITDA quality, customer concentration, margin trend, working capital, contract assignability — plus the sector layer: backlog, bonding, and labor for industrial and construction-services firms; FDA/USDA standing, certifications, and supply agreements for food, ag, and animal-health sellers; contracts and leases for distribution. Build the room around eight workstreams: financial, corporate/legal (both states' filings if you straddle the line), commercial, operations/technical, HR, IP and IT, tax (Kansas and Missouri), and insurance/compliance. The two documents that do the most work: a defensible quality-of-earnings file and the CIM. Protect yourself with staged disclosure — blind teaser, NDA-gated CIM, sensitive material held for the short list — enforced by per-buyer permissions, page-level analytics, and dynamic watermarking, with strategics, sponsors, and (in an ESOP) trustee advisors staged as separate visitor groups.

What does an M&A advisor cost to sell a $25M Kansas City company — is a 3 to 3.5% success fee normal, and how does Double Lehman plus a retainer work?

A 3-3.5% blended success fee is squarely normal for a $25M sale: Double Lehman (10/8/6/4% of the first four $1M increments, 2% above $5M) computes to about $700K (~2.8%) on $25M, landing near 3-3.5% with minimums and uncredited retainer. Retainers run $5,000-$25,000/month at a boutique, credited against the success fee only if the engagement letter says so. Watch the fee base (enterprise value vs cash at close), the tail (cap at 12 months vs the 18-24 asked), and any minimum floor. KC-specific comparison: an ESOP swaps the success-fee model for a fixed professional-fee stack that usually totals less — in exchange for fair market value rather than an auction premium; run both on your numbers. On the data-room line item, flat per-admin pricing keeps that cost predictable against a six-figure advisory fee.

Related resources

- The State of M&A Data Rooms — our 283-deal platform benchmark on how sell-side processes actually run.

- How to Build an M&A Data Room — the staged-disclosure playbook every Kansas City seller should run before going to market.

- How to Write a CIM — the confidential information memorandum your advisor builds after the teaser.

- Best Industrial M&A Advisors — the national sector view for Kansas City's manufacturing and construction-services sellers.

- Best M&A Advisors in St. Louis — the cross-state comparison: a Headquarters Town with a homegrown national bank (Stifel), the structural opposite of the Ownership Town.

- Best M&A Advisors in Cincinnati — the Brand Town, where consumer-sector fluency lives out of town — the same fluency-over-address rule KC's corridor teaches.

- Best M&A Advisors in Chicago — where William Blair, Lincoln International, and much of the national coverage of Kansas City deals is headquartered.

- Best M&A Advisors in Minneapolis — Piper Sandler's headquarters town; its Leawood office is KC's one resident national bank.

Footnotes and sources

- FINRA BrokerCheck (brokercheck.finra.org) — verified entity registrations and CRD numbers: CC Capital Advisors LLC d/b/a Turnstone Investment Banking (CRD #338420, approved June 2026, Kansas registration; sole owner Turnstone IB Holding Company LLC), Piper Sandler & Co. (CRD #665), FORVIS Mazars Capital Advisors, LLC (CRD #43427, renamed from BKD December 2024, Springfield, MO), M&A Securities Group, Inc. (CRD #39999, Kansas City, MO — Bridgepoint's broker-dealer of record), MSEC, LLC (CRD #154327, Overland Park — Mariner-owned). Frontier Investment Banking, The DVS Group, Great Plains Capital Partners, and O'Keeffe & O'Malley return no broker-dealer firm records (consistent with the federal M&A-broker exemption).

- Turnstone Investment Banking — firm announcement of the January 8, 2026 rebrand and independence from Country Club Bank; Ingram's coverage of the spin-out; published transaction list (Circle C Paving to Pavement Preservation Group, October 2025; Allied Materials & Equipment to Maple Hill Capital, March 2025; Vance Brothers, November 2024; Chance Rides to Permanent Equity, 2023). FNBO — completion of its acquisition of Country Club Bank (October 2025; capital-markets unit folding into Northland Securities).

- Ownership structures and revenue — Lockton FY2025 results ($4.0B revenue, +13%, announced 2025); Burns & McDonnell ($7.2B 2024 revenue; 100% ESOP since 1986; ENR Top 500); Black & Veatch (employee-owned; ~$4.7B; $1.34B Overland Park HQ plan per ENR); JE Dunn (family + ESOP since 2010; ~$6.5B per Forbes private-company data); Hallmark (Hall family since 1910;

$3.5B per Forbes); Dairy Farmers of America ($23B 2024, Dairy Foods Top 100 / NCB Co-op 100); Associated Wholesale Grocers ($12.1B 2024 consolidated sales); Seaboard Corporation (Fortune 500 No. 439 on the 2025 list; ~73.5% Bresky family ownership per proxy); Garmin (Olathe operational HQ; Schaffhausen, Switzerland legal domicile since 2010). - The 2020-2023 exits — Sprint/T-Mobile ($26.5B, closed April 1, 2020; Aspiria campus redevelopment); Cerner/Oracle ($28.3B, closed June 8, 2022; Goldman Sachs and Centerview Partners per the SC 14D9; North KC world headquarters closed; Oracle's Nashville HQ project); Kansas City Southern/Canadian Pacific (~$31B EV; STB approval March 15, 2023; CPKC combined April 14, 2023; BofA Securities and Morgan Stanley for KCS, BMO and Goldman Sachs for CP; Calgary global HQ, Kansas City US HQ); BATS Global Markets/Cboe (closed March 1, 2017); Waddell & Reed/Macquarie ($1.7B, closed April 2021; wealth unit to LPL ~$300M); Russell Stover/Lindt (2014, terms undisclosed, ~$1.4B press estimates); Boulevard/Duvel Moortgat (2013, undisclosed); Yellow Corp (operations ceased July 30, 2023; Chapter 11 August 6, 2023; ~$1.9B terminal auctions, XPO $870M).

- KC Animal Health Corridor — corridor economic-impact reporting (~56% of global animal-health, diagnostics, and pet-food sales — the corridor's own metric, first published 2014, re-cited in its 2024 report; 300+ companies; 22,000+ jobs;

$10.5B regional GDP); Boehringer Ingelheim St. Joseph (since 1917; largest US BI animal-health site; 2024 R&D lab); Ceva North American HQ (Lenexa); Hill's Pet Nutrition (Overland Park HQ; Topeka; $250M Emporia plant); Merck Animal Health De Soto ($895M expansion announced May 8, 2025); NBAF ($1.25B: $938M federal + $307M Kansas + $5M Manhattan; dedicated May 2023, science mission phasing in); Elanco Lenexa and Elwood sites (Bayer's former Shawnee plant sold to TriRx, 2021). - Animal-health deal record — Bayer Animal Health/Elanco ($7.6B, closed August 3, 2020; Goldman Sachs for Elanco; BofA Merrill Lynch and Credit Suisse for Bayer); Elanco Aqua/Merck (

$1.3B, closed July 2024); PetIQ/Bansk ($1.5B, closed October 2024; Jefferies — PetIQ is Idaho-based, cited for the vertical's advisor pattern); Dechra/EQT (£4.5B; Investec); VIP Petcare/Tractor Supply (closed May 2026; William Blair and Centerview); Zoetis/Neogen genomics ($160M, announced February 2026); Capstone Partners pet-sector data (median ~9.9x EV/EBITDA 2025 vs ~16.8x 2024). - Buyer engine 2025-2026 — UMB/Heartland Financial (~$2.0B all-stock, closed January 31, 2025); Creative Planning ($700B+ AUM/advisement as of December 31, 2025; ~31 acquisitions; $250B SageView deal October 2025); Mariner ($647B+ as of March 31, 2026; $31B advisor network sold to LPL April 2026); Panasonic Energy De Soto ($4B; mass production July 14, 2025; full ramp delayed); Meta Kansas City data center ($1B+, operational August 20, 2025); Google Kansas City campuses (up to $10B Port KC bond authorization, July 2025); CPKC (2025 revenue $15.1B, 59.9% operating ratio; Americold $120M KC hub, August 2025); Polsinelli ($1B+ 2025 revenue, Am Law No. 55); Five Elms Capital (Fund VI, $1.1B, October 2024); Great Range Capital (Fund III, $250M).

- US Census / BEA — Kansas City MO-KS metro population (

2.2 million); metro GDP ($186B nominal, 2023).

This article reflects my views as of July 2026 and is informational, not legal, tax, or investment advice. Firm registrations, names, and ownership change — this metro's flagship advisor changed all three in the past year — so verify current status on FINRA BrokerCheck before engaging any advisor. I am the co-founder of Peony, a data room company; where I mention Peony I have flagged the interest.