Net Lease Data Room: The OM Sells the Property, the Room Proves the Tenant (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Net Lease Data Room: The OM Sells the Property, the Room Proves the Tenant (2026)

Last updated: July 2026

Quick answer: A net-lease data room is a deal room for buying, selling, financing, or sale-leasing-back a single-tenant net-lease asset — and the thing that makes it different from any other commercial real estate room is that it is organized around the lease and the tenant's credit, not the square footage. A single-tenant net-lease (STNL) or sale-leaseback asset is a bond wearing a building: its value is one tenant's promise to pay for a fixed term, so the document set leads with the lease, the tenant-credit file, the estoppel certificate, and the SNDA the lender needs — because those decide whether the income is real and financeable. In 2026 STNL cap rates sit near 6.80% (essentially flat), tracking the 10-year Treasury with a lag, while sale-leaseback volume is rebounding (~$14.4B across 714 deals in 2025; the strongest Q1 since 2022). The offering memorandum sells the property; the room proves the tenant. When the deal involves a lender, a 1031 buyer on the clock, and confidential tenant financials, that room is usually a commercial real estate data room — not email.

I'm Sean Yu, co-founder of Peony, a data room company serving 5,900+ customers across M&A, fundraising, and real estate. I don't broker net-lease deals for a living — but I've watched hundreds of CRE transactions move through data rooms, and the single-tenant net-lease and sale-leaseback ones do not behave like the others. In a multi-tenant office or retail deal, the room is organized around the rent roll and the physical asset: many leases, many square feet, diversified income. In a net-lease deal there is essentially one lease and one tenant, and the whole valuation collapses onto two questions — is that tenant good for the rent for the full term, and does the lease actually say what the offering memorandum says it says? Reorganize the room around those two questions and the deal reads correctly. Leave it organized like a generic CRE room and you bury the lease, the guaranty, the estoppel, and the SNDA — the four files the buyer and the lender actually came for.

That is the thesis of this post: the offering memorandum sells the property; the data room proves the tenant. A single-tenant net-lease or sale-leaseback asset is a bond wearing a building — the coupon is the rent, the maturity is the lease term, and the credit is the tenant. So the room is built around lease + credit + estoppel + SNDA, and the concrete is almost an afterthought. Get the tenant proof right and a private 1031 buyer, a net-lease REIT, or a lender can all underwrite the same file in an afternoon.

Here's the carve-out, because Peony has a family of CRE guides and this one owns a specific lane. If you want the generic CRE process and clock — caveat emptor, the contingency period, re-trades — read commercial property due diligence; this post assumes you know that and goes tenant-and-lease-deep. If you want the line-item document inventory for ordinary real estate, that's the real estate due diligence checklist. If you want provider and archetype selection for real estate broadly, that's data room for real estate. And note the sibling asset-class guides: the data center data room and the industrial data room each touch sale-leaseback for their own asset class — but this post owns the generic net-lease, NNN, and sale-leaseback lane, and they link here for the mechanics.

Why does a net-lease data room prove the tenant instead of the building?

Because in a single-tenant net-lease deal the building is nearly incidental and the tenant is nearly everything. When one credit tenant occupies the whole property under a long-term net lease, the owner's income is not diversified across a rent roll — it is a single, fixed stream of payments from one company for a defined term. That is the literal definition of a bond: a coupon (the rent), a maturity (the lease expiration), and an issuer (the tenant). The real estate is the collateral, but the value is the credit.

The market prices it exactly that way. In Q1 2026, single-tenant net-lease cap rates sat around 6.80% on average (Boulder Group), but the dispersion around that average is the whole story: a premier long-term ground lease to an investment-grade tenant — a 15-year McDonald's, say — can trade in the 4.30–4.60% range, while a short-remaining-term deal with weaker or troubled credit pushes to 9% or higher. Same asset class, hundreds of basis points of spread — and the difference is almost entirely tenant credit and remaining lease term, not the quality of the drywall. Net-lease cap rates track the 10-year Treasury with a lag, which is why well-capitalized net-lease REITs underwrite to a spread over their cost of capital: W. P. Carey targets at least 150 basis points, and Realty Income deployed roughly $2.4 billion in Q4 2025 alone at about a 7% initial cash yield.

When value is that concentrated in one lease and one credit, the data room's job changes. It is no longer to prove the building is sound — a Phase I and a property-condition report handle that, the same as any asset. It is to prove the income is real, contracted, and financeable: the lease says what the OM claims, the tenant is good for the rent, the estoppel confirms it from the tenant's own hand, and the SNDA keeps the lease alive through a foreclosure so the lender will fund. That is the spine the index has to be built on.

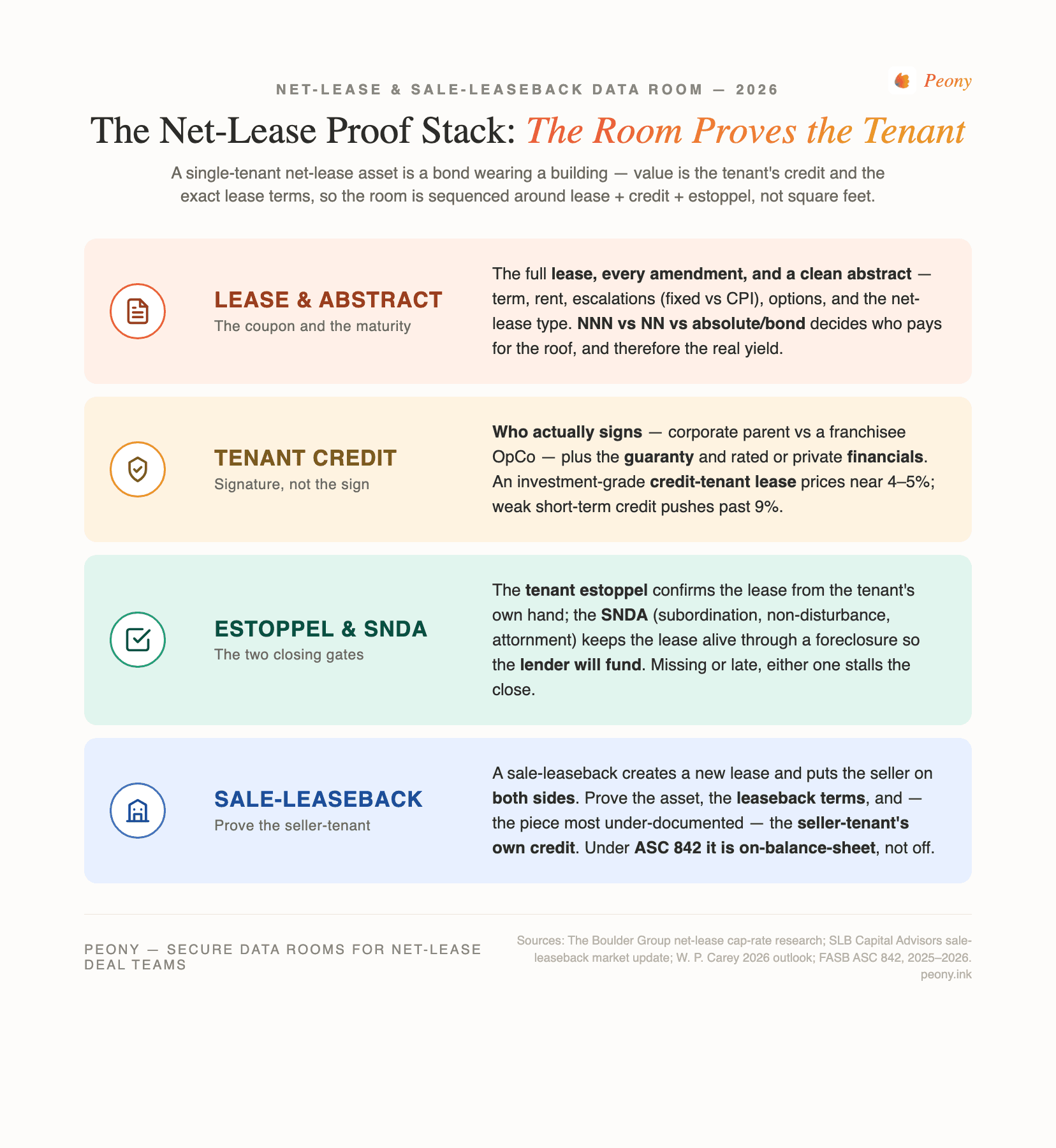

What goes in a net-lease or sale-leaseback data room?

The same core workstreams as any CRE deal, but re-sequenced so the lease and the tenant's credit lead, and graded by the one thing that goes wrong in each. The generic multi-tenant room puts the rent roll and physical asset first; the net-lease room puts the lease, the credit, and the two closing documents — estoppel and SNDA — first, because those are the gating risks a buyer and lender actually underwrite. Here's the buyer's-eye version — the signature table for this asset class.

| Workstream | What you verify | The #1 thing that goes wrong |

|---|---|---|

| Lease & abstract | Full lease, all amendments and side letters, and a clean abstract: primary term, rent, escalations (fixed vs CPI), options/renewals, ROFR/ROFO, go-dark & co-tenancy, net-lease type (NNN/NN/absolute) | The abstract disagrees with the lease — an unrecorded amendment, a concession, or a landlord obligation buried in an exhibit that the OM never mentioned |

| Tenant credit & guaranty | Who actually signs (corporate parent vs franchisee/OpCo), the guaranty, S&P/Moody's rating or private financials, single-tenant concentration | Buying the brand on the sign instead of the signature in the lease — a thin franchisee OpCo signs, and the household-name parent never guaranteed anything |

| Estoppel certificate | Current, signed tenant estoppel: dates, rent, next escalation, deposit, lease in full force, no default, no offsets or side agreements | The estoppel arrives late or surfaces a discrepancy (concession, offset, unpaid landlord obligation) that re-prices or kills the deal at the closing table |

| SNDA & lender | Subordination, non-disturbance and attornment agreement in a form the lender will accept; loan documents; debt assumption terms | A missing or non-conforming SNDA holds up the loan — the lender won't fund without non-disturbance, and the tenant won't sign without it either |

| Rent roll / escalations / WALT | The single lease's payment schedule, escalation timing and mechanics, remaining term and WALT (portfolio), percentage-rent or reimbursement true-ups | Modeling a flat rent when the escalator is CPI-linked or capped — or over-crediting a long term when a near-dated break/termination option shortens the real WALT |

| Title, survey & environmental | Title commitment (Schedule B exceptions), ALTA/NSPS survey, easements/access, Phase I ESA to ASTM E1527-21 (Phase II if a REC appears) | Closing on a stale Phase I and forfeiting the CERCLA innocent-landowner defense; an access or reciprocal-easement gap on a pad or outparcel |

| Sale-leaseback-specific: seller-tenant credit & leaseback terms | The newly created leaseback (term, rent, net structure, guaranty) and the seller-tenant's own corporate credit and financials; ASC 842 sale-vs-financing treatment | Documenting the asset but under-documenting the seller-tenant's credit — after closing, the buyer's entire yield is that same company's rent, and no one stress-tested it |

A few of these deserve their own paragraph, because the money and the liability live there.

The lease is the workstream with the least room for error. In a diversified rent roll, one bad lease is a rounding error; in a single-tenant deal it is the deal. So the room must present the full lease, every amendment and side letter, and a clean abstract — and the abstract has to reconcile to the lease line by line. The most expensive net-lease surprises live in exhibits and amendments: a free-rent concession, a landlord roof obligation slipped into an NNN, a co-tenancy or go-dark right that lets the tenant walk. Put the whole chain in the room, not just the base document.

Tenant credit is where the brand fools people. A nationally branded pharmacy or QSR can be operated by a franchisee whose operating company signs the lease — so the guaranty behind a 15-year "national tenant" deal may come from a thin OpCo, not the parent. The diligence version is the actual signing entity, the guaranty, and the tenant's financial statements, side by side with the lease. We'll come back to credit-tenant leases below.

Environmental follows the standard CRE playbook. A Phase I ESA to ASTM E1527-21 — the only edition the EPA recognizes for All Appropriate Inquiries since February 13, 2024 — with a Phase II if a Recognized Environmental Condition appears. Net-lease retail carries a wrinkle worth flagging: gas/convenience, auto, and dry-cleaner tenants raise contamination risk, so read the environmental file against the tenant's use. Our environmental due diligence guide covers the Phase I/II mechanics; here, just make sure the file matches the tenant's operations.

What is the difference between NNN, NN, absolute-net, and bond/true-net leases — and why does it change the diligence?

The four lease types differ in how much of the building's cost the tenant carries, and that allocation directly sets the real yield and therefore what the room has to prove. "Net lease" on an offering memorandum can mean any of them, so establishing which one you're actually buying is the first substantive question in the deal.

| NN (double-net) | NNN (triple-net) | Absolute / bond / true-net | |

|---|---|---|---|

| Tenant pays | Base rent + taxes + insurance | Base rent + taxes + insurance + maintenance | Everything — including roof, structure, casualty, condemnation |

| Landlord still owns | Roof, structure, and often more maintenance | Often roof, structure, parking-lot capital items | Nothing — a true "coupon-clipping" position |

| What the buyer underwrites | The landlord's residual capital exposure | The residual roof/structure/parking obligations | Essentially just the tenant's credit and the lease term |

| The room leads with | Lease + a capital-reserve view | Lease + landlord-obligation schedule + credit | Lease + guaranty + tenant financials |

The trap is treating an NNN as if it were absolute-net. A "triple-net" lease often still leaves the landlord holding the roof, structure, and parking lot — real, recurring capital costs. If the buyer models the deal as a clean coupon and ignores a roof at year seven, the effective yield is lower than the cap rate advertised. The room's job is to make the exact allocation legible: pull the maintenance, repair, casualty, and capital-responsibility clauses into the abstract so the buyer prices the obligations they're keeping. In an absolute-net or bond lease, the tenant genuinely carries everything, so the diligence narrows almost entirely to credit and term — which is why bond leases behave most like an actual bond and trade at the tightest cap rates when the tenant is investment-grade.

What is a tenant estoppel certificate, and why does it gate closing?

A tenant estoppel certificate is a signed statement from the tenant confirming the facts of the lease as of closing — and it gates the deal because it is the buyer's and lender's independent confirmation, straight from the tenant, that the lease being sold actually says and does what the seller claims. In a single-tenant net-lease deal, where the whole value is that one lease, no buyer and no lender will close without a current, clean, signed estoppel.

A conforming estoppel confirms, at minimum:

- The lease and amendments — that the attached lease (and the listed amendments) is the complete, in-force agreement, with no side letters.

- Dates and term — commencement, expiration, and any remaining options.

- Rent and escalations — current base rent, the date and amount of the next escalation, and any percentage-rent or reimbursement terms.

- Deposits and prepayments — security deposit held, and any prepaid rent.

- No default, no offsets — that neither party is in default and the tenant has no claims, offsets, or defenses against rent.

- Landlord obligations — that all landlord work, allowances, and concessions are complete and paid (or an itemized list of what isn't).

The reason it gates closing is that any discrepancy between the estoppel and the OM is the deal. If the estoppel reveals a rent concession the seller didn't disclose, an unrecorded amendment, an offset right, or an unfinished landlord obligation, the buyer re-prices or walks — and better to learn it from the estoppel than after closing. The practical failure mode is timing: estoppels take time to circulate and get signed, and a tenant with no incentive to hurry can stall a closing. So a well-run room puts the estoppel at the top, next to the lease it certifies, with a status tracker showing which estoppels are requested, outstanding, and returned. On a small multi-tenant strip, the same logic applies to the major tenants.

What is an SNDA, and why does the lender require it?

An SNDA — subordination, non-disturbance and attornment — is a three-party agreement among the tenant, the landlord/borrower, and the lender that settles what happens to the lease if the landlord defaults on its mortgage. It is the second document, alongside the estoppel, that a financeable net-lease deal must collect, and it exists because the lender and the tenant each need a promise the other has to make.

The three words are three promises:

- Subordination — the tenant agrees its lease is junior to the lender's mortgage, so the mortgage has priority.

- Non-disturbance — in exchange, the lender agrees that if it forecloses, it will not terminate the lease or disturb the tenant's possession, as long as the tenant isn't in default. This is the clause the tenant cares about.

- Attornment — the tenant agrees to recognize the foreclosing lender (or a subsequent buyer) as its new landlord and keep paying rent to them.

Why the lender requires it: in a single-tenant deal the loan is underwritten to that one lease's cash flow. Without subordination and attornment, the lender's position relative to the lease is uncertain; without offering non-disturbance, the tenant might refuse to subordinate at all. The SNDA resolves the standoff — the lease survives a foreclosure, the lender's priority is clear, and the income the loan depends on stays intact. A missing or non-conforming SNDA (wrong form, tenant won't sign, terms the lender rejects) can hold up the loan and therefore the closing, which is why it belongs in the room early, with the loan documents and the lease, behind the same NDA gate. Estoppel and SNDA are the two documents that most often decide whether a net-lease deal closes on time.

How do you run a sale-leaseback through a data room?

A sale-leaseback monetizes owned real estate: an owner-occupier — very often the CFO — sells the building the company operates from and simultaneously signs a long-term lease back, freeing the capital trapped in the real estate while keeping operational control. Running it through a data room means proving three things at once, and the third is the one sellers most often under-document.

The three proofs:

- The asset. Title, survey, environmental (Phase I to ASTM E1527-21), property condition, and zoning/use — the same real-estate file any buyer needs.

- The lease being created. Unlike an acquisition, there is no existing lease to abstract — the sale-leaseback creates the lease at closing. So the room carries the negotiated leaseback: term (often 10–25 years), rent (set to a market or agreed cap rate on the sale price), escalations, the net-lease structure (frequently absolute-net or NNN), and any guaranty. The buyer is underwriting a lease that doesn't exist yet, so the draft and its final form are central documents.

- The seller-tenant's own credit. This is the piece that separates a sale-leaseback from an ordinary acquisition. After closing, the buyer's entire yield is that same company paying rent under the new lease — so the seller-tenant's corporate financials, leverage, and business durability are the investment. A sale-leaseback buyer underwrites the seller as a credit at least as hard as it underwrites the building.

Because a sale-leaseback puts the seller on both sides — vendor today, tenant tomorrow — the room needs disciplined permissions. The buyer's lender and credit team see the seller-tenant financials; the buyer sees the asset file and the draft leaseback; the seller's most sensitive corporate financials are gated and redacted to only the parties who must see them. And be honest about the accounting: under ASC 842, a qualifying sale-leaseback is not off-balance-sheet — the leaseback is recognized as a right-of-use asset and a lease liability on the seller-tenant's books (more on that below). Sale-leasebacks are having a moment — roughly $14.4 billion across 714 transactions in 2025 (up 18% in dollar volume), with 168 deals in Q1 2026, the strongest first quarter since 2022 (SLB Capital Advisors), as stabilizing rates and returning M&A push corporates and PE sponsors to unlock real-estate value. A flat-rate room such as Peony fits that flow, especially when the sale-leaseback is the real-estate leg of a larger acquisition on a deadline.

Is a sale-leaseback off-balance-sheet under ASC 842?

No — and this is worth stating plainly because it's one of the most persistent myths in the category. Under the older ASC 840 standard, many operating leases stayed off the balance sheet, so sale-leasebacks were routinely pitched as off-balance-sheet financing. ASC 842 ended that. In a qualifying sale-leaseback, the seller-tenant derecognizes the sold asset — but the leaseback comes right back onto the balance sheet as a right-of-use (ROU) asset and a corresponding lease liability. The lease is visible, not hidden.

That doesn't make the sale-leaseback a worse deal — it makes the pitch honest. The real, durable benefits are intact:

- Capital unlock at full value. The seller monetizes the real estate at a cap-rate price — often 100% of value — which typically beats the loan-to-value a mortgage would advance against the same building.

- Operational control retained. The company keeps using the property under the lease it just signed.

- Gain recognition. A qualifying sale lets the seller recognize gain on the disposition (subject to the ASC 842 rules on excess proceeds and off-market terms).

One more honest wrinkle the room has to support: if the transaction fails the ASC 842 sale criteria — for instance, if the leaseback terms make it look like the seller never really gave up control — it is not treated as a sale at all. It becomes a financing transaction: the seller keeps the asset on its books and records the proceeds as a liability, like a loan. Whether a given deal qualifies as a sale turns on the specific terms, which is why the leaseback structure is a document the buyer's and seller's auditors both read carefully. Peony stores, permissions, and watermarks those documents; it does not provide accounting or tax advice — verify the treatment with your auditor.

How do you underwrite net-lease tenant credit, and what is a credit-tenant lease?

You underwrite who actually signs the lease and who stands behind it, because a single-tenant asset is a bond wearing a building and the coupon is only as good as the issuer. The strongest case is a credit-tenant lease (CTL): a long-term, typically absolute-net lease to an investment-grade tenant, where the value is essentially the tenant's rated credit and the lease duration — so much so that CTL financing is underwritten more like corporate debt than like a mortgage. An investment-grade tenant with an S&P/Moody's rating and a full corporate guaranty prices at the tightest cap rates in the asset class.

The middle and the risk live in unrated and franchisee credit. Here is the single most expensive net-lease error: buying the brand on the sign instead of the signature in the lease. A nationally branded pharmacy, restaurant, or dollar store can be operated by a franchisee, and the entity that signs the lease may be that franchisee's operating company — not the household-name parent. So a "15-year national tenant" deal can be backed by a guaranty from a thin OpCo with a fraction of the parent's balance sheet. The room resolves this by putting three things side by side:

- The signing entity — exactly who is on the signature block, and whether a parent or franchisor guaranty backs it.

- The guaranty — its scope, term, and any burn-off or cap.

- The financials — the rated entity's public financials, or the private tenant's statements, plus any single-tenant-concentration context (for a small portfolio, how much of the income rides on one credit).

Two practical notes. First, layer credit against remaining term and escalations: a strong tenant with two years left is a very different asset from the same tenant with fifteen, and CPI-linked or fixed escalations change the coupon's growth. Second, keep the tenant financials and guaranty behind an NDA gate with per-viewer watermarks — private tenant statements are exactly the kind of document a seller should never email around. And the honesty guardrail: Peony secures and permissions the credit file; it does not rate the tenant or opine on creditworthiness. That's the buyer's and their advisors' call.

How does the data room actually run a net-lease acquisition or sale-leaseback?

It runs it as a permissioned, evidence-first workflow where the lease and credit lead, the estoppel and SNDA are tracked to closing, confidential tenant financials are gated and watermarked, and you can see who actually read the lease before the call. A net-lease deal moves 100-plus sensitive documents — the lease and amendments, guaranties, tenant financials, estoppels, SNDAs, loan documents — among a buyer, a seller, a lender, a 1031 accommodator, and several sets of counsel. Email and consumer file-sharing cannot gate, watermark, or track that. Here's how a room like Peony maps to the specific risks of this asset class, at a flat $52/admin/month with no per-page or per-user surcharge — which matters when the viewer list keeps growing.

- NDA gate. Tenant financials, guaranties, and negotiated lease economics are the most confidential items in the deal. A click-through NDA in front of the room — or in front of the specific tenant-credit folder — means a viewer agrees before they see a single financial statement, and you have the record that they did.

- Dynamic per-viewer watermarks. The same lease, guaranty, or estoppel opens for the buyer, the lender, and counsel with each viewer's identity burned into the page. If a confidential tenant financial leaks, the watermark says whose copy it was — a real deterrent when you're circulating a named tenant's private statements.

- Page-level analytics. You see who viewed what and for how long — did the lender actually open the estoppel and the SNDA, or just the flyer? That tells you where the real questions are coming before the diligence call, and which party is genuinely engaged. (This is view-and-dwell analytics, not keystroke capture.)

- Redaction. Tenant personal data in an estoppel, pricing in a guaranty, or sensitive figures in the seller-tenant's financials can be redacted at the document level so a lender sees the structure without the confidential specifics.

- AI auto-indexing. Drop a disorganized export — the lease, a stack of amendments, the tenant's financials, title, survey — and the room indexes it so the lease-and-credit file, the estoppel/SNDA, and the property file land in a navigable structure instead of a flat dump. When the index is the argument ("here's the tenant, here's the lease, here's the proof"), that's not cosmetic.

- Role-based permission groups. The lender lives in the lease, estoppel, SNDA, and financial folders; the buyer sees the whole file; on a sale-leaseback the seller-tenant's corporate financials are gated to the buyer's credit team and lender; brokers and counsel sit across the deal. One room, many sightlines.

For a 5,900+-customer flat-rate room, the structural fit is the single-asset net-lease acquisition, the small net-lease portfolio, the sale-leaseback, and the buyer/lender diligence around them — where the document set is confidential but the deal doesn't warrant a six-figure VDR procurement.

Where you don't need any of this. Be honest about the floor. A single sub-$5M retail pad or QSR ground lease trading all-cash between two parties with one attorney can run on a handful of emailed PDFs — the lease, the estoppel, title, survey. A data room is overkill. And at the opposite extreme, a marketed institutional net-lease portfolio — a JLL, CBRE, or Newmark process — or a $1B-plus REIT M&A take-private will default to Datasite or Intralinks; that's their lane and I won't pretend otherwise. The data room earns its place in the wide middle: any deal with a lender, an NDA'd tenant credit file, a 1031 buyer on the clock, and a document set too sensitive for email.

How do you organize the index, and who gets access at what level?

Organize the index so the lease and tenant credit are folder one and grant access by role, not by a single shared link — because the fastest way to signal "this income is real and financeable" is to make the lease, the credit, the estoppel, and the SNDA the first thing every reviewer sees, and the fastest way to lose control of confidential tenant financials is to hand everyone the same link.

A working top-level index for a net-lease deal:

- Lease & abstract — full lease, all amendments and side letters, clean abstract, guaranty.

- Tenant credit — signing-entity chart, guaranty, S&P/Moody's rating or private financials, single-tenant concentration.

- Estoppel & SNDA — current signed estoppel (with a status tracker), SNDA in the lender's form, loan documents.

- Rent roll / cash flow — payment and escalation schedule, WALT, reimbursement/percentage-rent true-ups.

- Title & survey — commitment (Schedule B), ALTA/NSPS survey, easements and access.

- Environmental & condition — Phase I (and II if any), property-condition report, use-specific environmental items.

- Financial model — in-place NOI, escalations, and the underwriting model; cap-rate and spread assumptions.

- Sale-leaseback / corporate & closing — the draft leaseback, seller-tenant corporate financials, entity docs, ASC 842 memo, closing checklist.

Access then maps to who needs which folders:

| Persona | Primary folders | Gate / control |

|---|---|---|

| Buyer / acquirer deal team | All | Full access |

| Lender / CMBS or life-co originator | Lease, tenant credit, estoppel & SNDA, financial, title/enviro | NDA gate; watermark; analytics on estoppel/SNDA |

| 1031 buyer's accommodator / counsel | Closing file, estoppel & SNDA, title | Restricted permission group |

| Sale-leaseback: seller-tenant financials | Gated corporate-financials folder | Redaction; shared only with buyer credit + lender |

| Investment-sales broker / counsel | Cross-deal | Role-based; full or near-full |

This is exactly the kind of segmentation that permission groups plus per-viewer watermarks make routine, and it is where a flat-rate model helps: when the lender adds analysts and the buyer adds counsel, you're not paying per seat to keep the room honest — and the 1031 buyer on a 45/180-day clock never waits on access.

The bottom line: which net-lease data room do you actually need?

The room proves the tenant — so the right answer depends on deal size, the financing, and how confidential the tenant credit file is, not on brand prestige. Here's the segmented recommendation from someone who watches these rooms run.

- Solo investor / single small pad or QSR ground lease (two parties, one attorney, all-cash): You may not need a data room at all. A clean, well-named set of PDFs — lease, estoppel, title, survey — emailed to one counterparty can be enough. Don't over-tool a two-party pad trade. If you want structure without cost, a flat-rate room is still cheaper than most people assume, but it's optional here.

- Net-lease buyer, 1031 buyer, or CFO running a sale-leaseback (single asset, a small portfolio, or the sale-leaseback itself): This is the sweet spot for a flat-rate room. You have a lender underwriting to the lease and requiring an SNDA, confidential tenant financials and guaranties, a 1031 clock that can't tolerate a diligence stall, and 100-plus documents that email can't gate or track. A room like Peony — NDA gate, per-viewer watermarks, page-level analytics, redaction, AI auto-indexing, role-based groups, flat $52/admin/month — fits the confidentiality and the document volume without a per-page or per-user meter. With 5,900+ customers across M&A, fundraising, and real estate, this is the lane it's built for.

- Marketed institutional net-lease portfolio (JLL/CBRE/Newmark process) or $1B+ REIT M&A / take-private: Default to Datasite or Intralinks. A full banking syndicate, a global bidder list, and integrated deal tooling are their procurement reality, and that's the honest recommendation at that altitude.

Whichever tier you're in, the discipline is the same: lead with the lease, prove the tenant's credit, collect the estoppel and SNDA before they can stall the close, and gate the confidential financials. Build the room around the tenant and the deal reads correctly to everyone who has to underwrite it — because the offering memorandum sells the property, but the room proves the tenant.

If you're staging a sell-side or refinancing room and want the broader provider landscape and cost benchmarks first, see our top 10 virtual data room providers comparison and the virtual data room cost guide before you commit. For the fund-vehicle angle — a net-lease fund raising from LPs rather than a single-asset trade — see the real estate fund data room guide.

Sources

- The Boulder Group — Net Lease Research Report, Q1 2026 (single-tenant net-lease cap rates ~6.80%; retail ~6.55%, industrial ~7.15%, office ~7.90%; premier tenant range ~4.30–4.60% for 15-yr McDonald's ground leases to 9%+ for short-term weaker credit; supply and bid-ask spread data).

- SLB Capital Advisors — U.S. Sale-Leaseback Market Update (2025 volume ~$14.4B across 714 transactions, +18% dollar volume / +3% count; Q4 2025 ~$4.7B; Q1 2026 168 deals, strongest first quarter since 2022; cap-rate compression H2 2025 into early 2026).

- W. P. Carey — 2026 Net Lease Outlook (net-lease cap rates track the 10-year Treasury with a lag; target investment spread of at least 150 bps over cost of capital; sale-leaseback demand driven by M&A and private-equity acquisition leverage).

- Realty Income — January 2026 8-K (roughly $2.4B invested in Q4 2025 at ~7% initial weighted-average cash yield).

- NNN transaction volume — industry forecasts of ~$34–36B for full-year 2026 vs ~$32.1B estimated 2025.

- FASB / ASC 842 — sale-and-leaseback accounting (leaseback recognized as a right-of-use asset and lease liability on the balance sheet — not off-balance-sheet as under ASC 840; failed-sale transactions accounted for as financings).

- IRS — Section 1031 like-kind exchange timelines (45-day identification / 180-day exchange).

- EPA / ASTM — All Appropriate Inquiries; ASTM E1527-21 Phase I ESA (sole recognized edition since February 13, 2024).

This article is general information for deal teams, not legal, tax, accounting, or investment advice. Cap rates, sale-leaseback volumes, ASC 842 treatment, lease and estoppel/SNDA law, environmental standards, and 1031 rules change over time and vary by jurisdiction and facts — verify current figures and treatment with qualified counsel, your auditor, and a licensed appraiser or broker before relying on them. Peony is a data room provider, not a broker, appraiser, 1031 qualified intermediary, or law firm, and does not opine on tenant credit.

You might also like

Jul 3, 2026

Multifamily Acquisition Data Room: The Rent Roll Is the Asset (2026)

Jul 1, 2026

Data Center Data Room: How the Room Underwrites the Megawatts (2026)

Jun 30, 2026

Commercial Property Due Diligence: How to Run It Against the Clock (2026)