How to Share an Interactive LP Report With Your Limited Partners (Securely)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

I'm Sean Yu, co-founder of Peony, and I've watched a lot of fund managers do beautiful work on a quarterly report and then mail it to their LPs as a PDF — which is a bit like building a working dashboard and then photographing it.

This post is about the last mile: how you actually send an interactive LP report to your limited partners. Not what goes in it, not how often — just the mechanics of getting a live, controlled report into the right hands. I run Peony, a data room company, so I'll be candid about where we fit and where simpler tools are the better call.

The one-line version: Your LPs deserve the live report, not a PDF of it. Share the live HTML through a secure viewer that binds each view to a named LP, gates on the LPA, shows you who opened it, and revokes after the window — instead of emailing a flattened PDF or dropping it on an uncontrolled link.

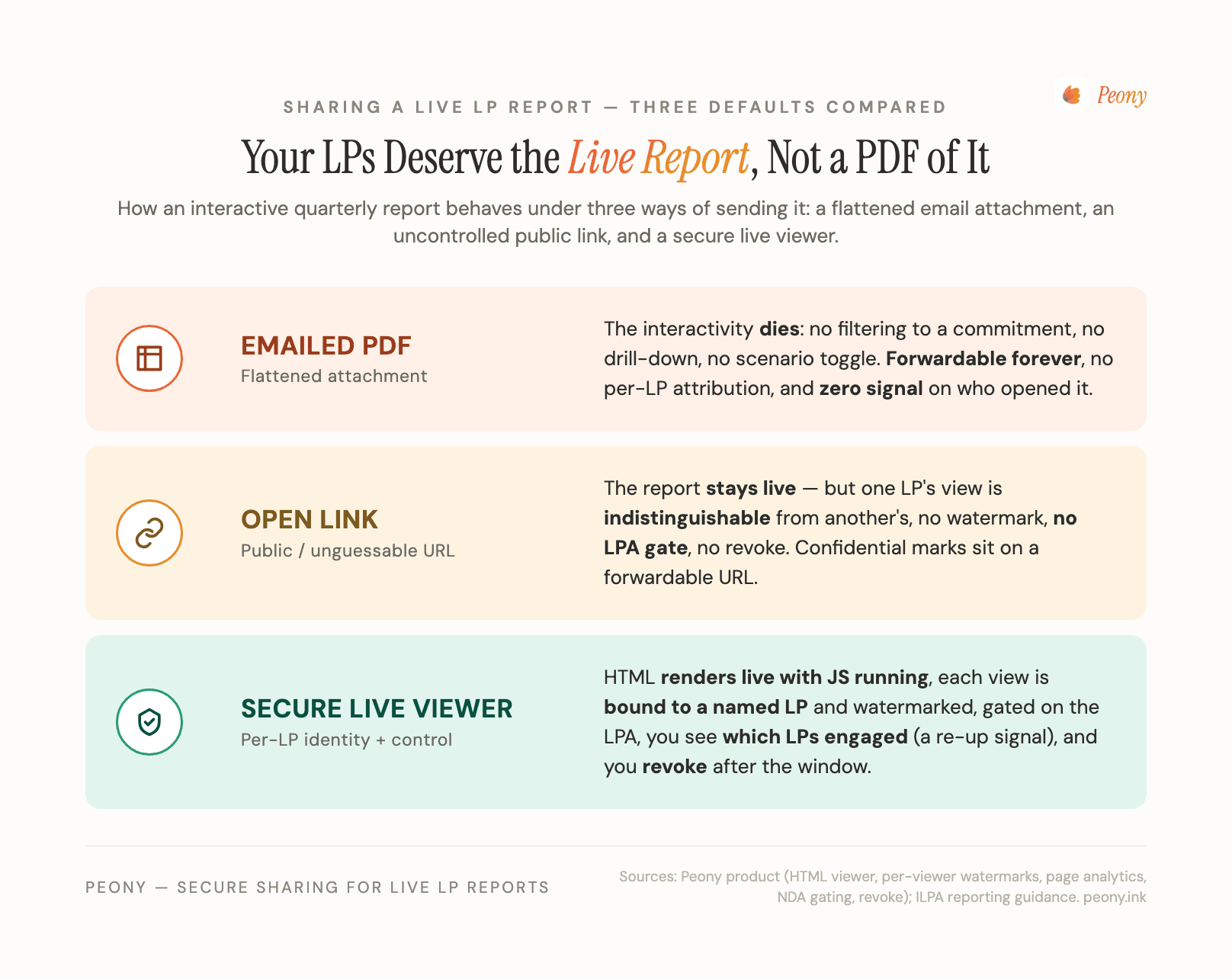

Why does emailing a PDF of your LP report quietly waste the report?

Because the moment you flatten an interactive report to a PDF, it stops being a tool and becomes a picture of a tool. GPs increasingly build their quarterly report as something live: fund-level marks with by-vintage and by-company drill-downs, a markdown the LP can expand, scenario views the LP can flex. Print that to PDF and the LP can no longer filter to their own commitment, drill into a single company's markdown, or model what the fund looks like under a different exit assumption. They get a static snapshot of a moment in your thinking instead of an instrument they can interrogate.

There's a second, quieter cost. A PDF attachment is forwardable forever, carries no attribution, and gives you no signal at all about who opened it. You sent eighty LPs a confidential set of marks and you have no idea which fifteen actually read it — which is exactly the information your IR team needs before a re-up conversation. The report did its job for you and then went dark.

So the flat PDF loses on both axes at once: the LP loses the interactivity, and you lose the engagement signal. That's the problem worth solving.

Why is dropping the report on an uncontrolled link the opposite mistake?

Because it preserves the interactivity but throws away every control that confidential fund marks require. The instinct after the PDF problem is reasonable — put the live HTML report on a link so it stays interactive. Tools like ShareDuo (shareduo.com) and Stacktree (stacktr.ee) do this well: real public or unguessable-link sharing, fast, free or cheap, no login, password and expiry, and Stacktree even supports MCP publish and update-in-place. For a non-confidential live page, that is genuinely a fine answer, and I'd point you straight at them.

The trouble is that an LP report is rarely non-confidential. Your LPA and side letters almost certainly bind the marks. And a public link, by design, cannot tell one LP apart from another. One LP's view is identical to the next LP's view: no per-LP watermark, no gate that records consent to the confidentiality terms, no way to see which LP engaged, and no way to revoke one recipient without breaking the link for everyone. Worse, a forwardable URL means your confidential marks can sit in a stranger's inbox indefinitely. You traded the PDF's deadness for a leak surface.

So neither default works for confidential marks. You want the link's liveness and the per-LP control the link can't give you.

What does sharing the report through a secure live viewer actually look like?

It means the LP opens a link that renders your live HTML report with its JavaScript running, but every view is bound to a named investor and wrapped in fund-grade controls. Concretely, the right setup does five things at once:

- It keeps the report live. The viewer renders

.htmland.htmnatively with JS executing, so the filters, drill-downs, and scenario toggles all work for the LP. This is the part most data rooms get wrong — they reject the HTML upload or convert it to PDF, and the interactive report dies on the way in. Peony renders it live; the AI-built report actually runs for the LP. You can see the behavior on the HTML viewer page. - It binds the view to a named LP. Each limited partner gets their own attributed link, and a dynamic watermark carries their name, email, and a timestamp across the rendered report. A forwarded screenshot now points back to whoever leaked it.

- It gates on the LPA. Before the LP reaches the report, an NDA or confidentiality acknowledgement presents the side-letter terms and logs the acceptance, so consent is part of the audit trail rather than a separate email.

- It shows you who engaged. Page-level analytics attribute every open to the named LP — which pages, how long. That's your re-up signal.

- It revokes after the window. When the reporting window closes, you revoke the link and the forwarded URL stops working.

That combination — live plus per-LP identity plus control — is the whole point. It's the only one of the three defaults that serves both the LP and you.

How does a per-LP watermark and identity binding protect confidential marks?

It converts an anonymous, forwardable artifact into an attributed one, which changes the behavior of everyone who touches it. A dynamic watermark stamps each LP's name, email, and a timestamp directly onto the rendered report, so a photographed or re-shared view carries its own source. On confidential fund marks that deterrent matters more than people expect: the LP who knows their name is on every page treats the file differently from one who received an anonymous PDF.

Identity binding goes a step further than watermarking. Because each LP opens their own attributed link rather than a shared URL, you can scope what each one sees — share the fund-level marks and portfolio commentary with everyone while restricting each LP's capital-account drill-down to their own link, using personalised links and granular per-file permissions. Layer in screenshot protection and the casual capture path gets harder too.

To be straight about the limits: no system makes a document literally un-forwardable, and a determined leaker can always photograph a screen with a second phone. What a per-LP watermark plus instant revoke buys you is attribution and an off-switch — the leaked copy is traceable, and the live link can be killed. That's a meaningfully better posture than "forwardable forever, no name on it," which is what both the PDF and the open link give you.

Why is "which LPs opened the report" a re-up signal worth instrumenting?

Because engagement on the quarterly report is one of the few honest leading indicators you get between closes. When each LP opens their own attributed link, page analytics tell you who opened the report, which sections they spent time on, and how long. The LP who reads the whole report twice the week before your next fund opens is usually the LP leaning in; the LP who never opened last quarter's report is a follow-up call your IR team should make now, not after the re-up window has passed.

This is the single biggest thing a PDF attachment can't do. You can request a read receipt and most clients will ignore it; you certainly can't tell which page an LP lingered on. With per-LP attribution, your IR lead works from a real list instead of a hunch. For the fund-specific version of this workflow, the investor relations and venture capital solution pages walk through how funds set it up.

A fair caveat: opens are a signal, not a verdict. An LP who skims on a phone in an airport isn't necessarily cold, and a careful LP might read once, thoroughly, and never return. Treat the analytics as one input into the re-up conversation, not a scoreboard.

How do I share an AI-built (Claude or GPT) interactive report and keep it live?

You share it through a viewer that renders the HTML natively, and ideally you push it there without ever flattening it. More GPs are building the quarterly report as an interactive artifact in Claude or GPT — a live performance page with charts, filters, and scenario sliders that recompute. The failure mode is that most data rooms reject the .html upload or convert it to an encrypted PDF, and the JavaScript dies, so the artifact you built becomes a screenshot.

Peony renders that file with its JS executing, so the LP gets the working app. And because our MCP server is publicly available now and bidirectional, you can build the report in Claude, install the Peony MCP, and push the artifact straight into a watermarked, gated, revocable room without leaving the chat — then read room contents back the same way. The detailed walkthrough lives in how to securely share Claude artifacts.

One honest boundary: Peony is the secure sharing layer, not a fund-admin or accounting system. We don't calculate your IRR or run your waterfall — you build the report (in Claude, in Excel, in your fund-admin tool) and we make sharing it live and controlled. If you want your own models under zero-retention, the Enterprise tier lets you connect your own GPT, Claude, and Gemini with permission-scoped, auditable access, but the marks come from you.

What interactivity do LPs actually lose when the report becomes a PDF?

They lose the three things that make a modern LP report a tool instead of a document: filtering, drill-down, and scenario modeling. It's worth naming them concretely, because "interactive" is a vague word and the loss is specific.

First, filtering to a commitment. In a live report, an LP with a $2M commitment can filter the fund-level view down to their pro-rata share, their fees, and their carry exposure. Flatten it and they're left doing arithmetic against a fund-wide number. Second, drilling into a company markdown. When a position gets written down, a sophisticated LP wants to expand that line and read the rationale, the comparable, and the revised exit case. A PDF gives them a footnote, if that. Third, scenario views. The best reports let an LP move an exit-multiple slider or toggle a downside case and watch TVPI and DPI recompute — which is exactly the conversation you want them having before a re-up. None of that survives the print-to-PDF step.

This is why "send it as a PDF" isn't a neutral formatting choice — it's a downgrade of the report's function. You did the work to make the report answer questions interactively; flattening it forces every LP who has a question to email you instead. Rendering the live HTML keeps the report doing its job. If you've built the report as an AI artifact, sharing Claude artifacts securely covers keeping that interactivity intact end to end.

Where do dedicated LP portals fit, and when should I not use a data room?

Use a dedicated LP portal when you need persistent fund administration; use a secure live viewer when you need to share one report this quarter. Dedicated portals like Carta, Juniper Square, and AngelList-style platforms are full fund-admin systems — they hold capital accounts, run distributions, file K-1s, and persist every statement quarter over quarter. If that's the job, a data room is the wrong tool and I'd tell you so.

The act this post is about is narrower and more frequent: you've already produced an interactive report and you need to get it to named LPs as a live, controlled artifact, today. That's a sharing problem, not a fund-admin problem, and it's where a secure viewer is faster and cheaper than standing up (or wrestling with) a portal. The two coexist cleanly — many funds run a portal for the system of record and reach for a secure data room when they want to share a single live report with attribution and an engagement signal. For how the room itself should be organized when you do go that route, the VC fund data room checklist and the real estate fund data room guide cover structure.

How does NDA and LPA gating fit into sharing the report?

Gating means the LP has to pass a confidentiality checkpoint before the report renders, and that checkpoint becomes part of your record. Most LPAs and side letters impose confidentiality on fund-level marks, individual company valuations, and capital-account detail. When you email a PDF, that obligation lives only in a document the LP signed months ago and may never re-read; nothing at the moment of access reminds them or captures fresh consent. A gate closes that loop.

In practice, an NDA gate presents the relevant confidentiality terms — or a short acknowledgement that the report is confidential under the existing LPA — before the LP reaches the live report, and it timestamps the acceptance against the named LP. If a leak is ever disputed, you have a clean record that this specific LP acknowledged confidentiality at this specific time, rather than a tangle of email threads. That's a materially stronger position than "the original LPA covers it, somewhere."

There's a sequencing nuance worth getting right. The gate should sit before the first render, not after, so an LP can't glimpse the marks and then decline. And the gate should be tied to the same attributed link as the watermark and analytics, so consent, identity, and engagement all hang together on one record. Done this way, gating isn't friction — it's the part of the workflow that makes the rest of it defensible.

Where Peony loses honestly: a gate captures consent to confidentiality, but it does not verify an LP's accreditation, KYC status, or eligibility — that's your fund administrator's and counsel's job, not the sharing layer's. We log who accepted what and when; we don't adjudicate whether they should have been on the list in the first place.

A practical send checklist for one live LP report

Here's the sequence I'd run for a quarterly send, assuming the report is already built:

- Confirm the report is live HTML, not a flat export. If you built it in Claude or GPT, keep it as

.html/.htmso the filters and scenario toggles survive the send. - Decide confidentiality. If the LPA or side letters bind the marks (they usually do), you need per-LP control — skip the public-link tools and use a secure viewer. If it's genuinely non-confidential, a ShareDuo or Stacktree public link is a fine, fast choice.

- Issue a per-LP attributed link, with a dynamic watermark carrying each LP's name and email.

- Gate on the LPA. Put the confidentiality acknowledgement before first view and let it log consent.

- Scope what each LP sees. Fund-level marks for everyone; each LP's capital-account drill-down restricted to their own link.

- Watch engagement. After the send, check page analytics to see which LPs opened the report — that's your re-up follow-up list.

- Revoke when the window closes. Kill the links so a forwarded URL goes dead.

That's the difference between treating the report as a one-way broadcast and treating it as a live, accountable conversation with your investors.

The bottom line

Across more than 5,900+ customers, the funds that get LP communication right have stopped thinking of the report as an attachment and started thinking of it as a live artifact they hand over under control. The flat PDF wastes the interactivity and tells you nothing; the open link keeps the report live but leaks across LPs and can't be revoked. The secure live viewer is the only one of the three that keeps the report working, binds each view to a named LP, gates on the LPA, shows you who engaged, and lets you revoke after the window.

We built Peony as that sharing layer — and we're trusted by 5,900+ customers to render live HTML reports with the controls confidential fund marks demand. If you've already done the hard work of building a genuinely interactive LP report, don't photograph it on the way out the door. Your LPs deserve the live report, not a PDF of it.

Related resources

- How to Share an Interactive Board Report With Your Directors (Securely) — the governance sibling: the same live-render-plus-per-viewer-control pattern, but a founder or CFO sending a live board report to named directors

- How to Share an Interactive Financial Model With an Investor (Securely) — the fundraising version: sending a live model to a VC under per-viewer control

- How to Send a Live Dashboard to a Client Securely — the consultant-to-client version of the same live-vs-flattened problem

- How to Share an Interactive ROI Calculator With a Prospect (Securely) — the B2B-sales version: keeping a live business-case calculator interactive without leaking your pricing logic

- VC LP Reporting Guide — what actually goes in the quarterly report and how often

- VC Fund Data Room Checklist — how the fund room itself should be organized

Sources & notes

- ILPA reporting guidance on quarterly LP statement content and cadence (net IRR, TVPI, DPI, RVPI), referenced for context on what the report contains; the sharing mechanic in this post is separate.

- Peony product capabilities referenced: native HTML/HTM rendering with JavaScript executing, per-viewer dynamic watermarks (Data Room plan), screenshot protection (Business plan) and Screenshield mobile (Data Room plan), NDA/confidentiality gating, granular per-file and per-link permissions, page-level analytics, instant revoke, and a publicly available MCP server.

- Pricing referenced as of June 2026: Free $0; Business $30/admin/month; Data Room $52/admin/month; Deal Team; Enterprise custom. See pricing for current figures.

- Public-link tools ShareDuo (shareduo.com) and Stacktree (stacktr.ee) and LP portals (Carta, Juniper Square, AngelList-style) are named for fair comparison; capabilities described from their public positioning.

Disclaimer: This article is for general informational purposes only and is not legal, tax, or investment advice; confirm your fund's confidentiality obligations against your LPA and side letters with qualified counsel.

You might also like

Mar 25, 2026

VC LP Reporting Guide (What Your LPs Actually Want) in 2026

Jun 29, 2026

How to Share an Interactive Financial Model With an Investor (Securely)

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)