VC LP Reporting Guide (What Your LPs Actually Want) in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

VC LP Reporting Guide: What Your LPs Actually Want in 2026

Last updated: March 2026

We run Peony, a data room company, and I've watched hundreds of fund managers share LP reports through our platform. The pattern I see over and over: GPs spend weeks building a beautiful quarterly report, email it as a PDF attachment, and have no idea whether a single LP actually opened it. Meanwhile, the LPs who did read it have questions they send piecemeal over email, Slack, and phone calls for the next month.

LP reporting isn't just a compliance checkbox. It's the single most consistent touchpoint between a GP and their investors, and how you handle it shapes whether those LPs re-up for Fund II or quietly pass.

This guide covers the metrics, cadence, templates, technology, and common mistakes that separate institutional-quality LP reporting from "good enough."

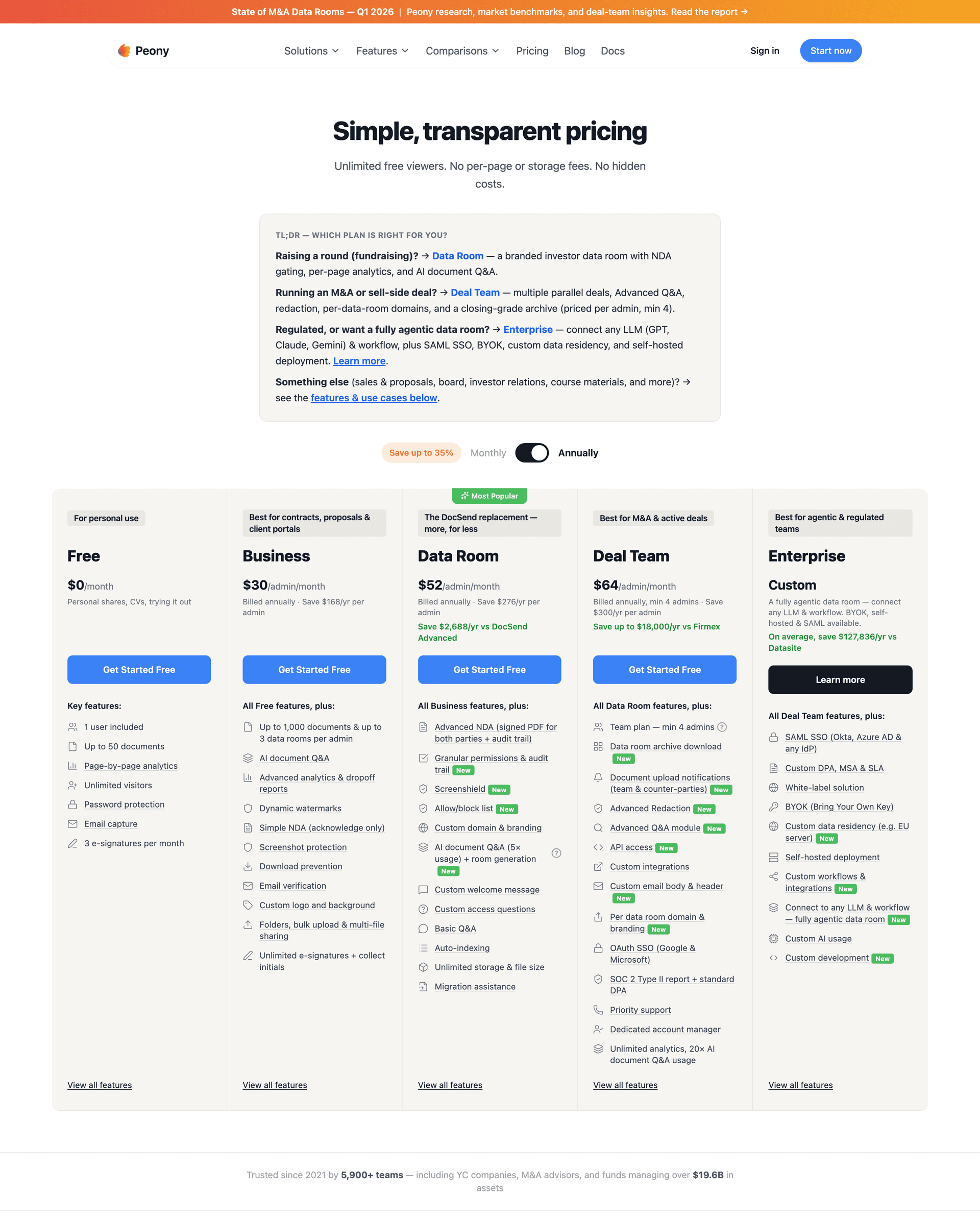

TL;DR: ILPA's Reporting Template v2.0 (2025) is now the benchmark standard for fee and expense disclosure. 92% of institutional LPs say reporting quality influences re-up decisions (Preqin 2024 Investor Survey). The SEC's private fund reporting rules were vacated by the Fifth Circuit in 2024, but LP expectations haven't budged. Report net IRR, TVPI, DPI, RVPI quarterly, hit your deadlines, and distribute through a secure portal rather than email. Peony (free tier available) provides page-level analytics showing exactly which report pages each LP reads, AI auto-indexing that organizes quarterly packs in under 3 minutes, and enterprise security (screenshot protection, NDA gates) on the Business plan ($30/admin/month), with dynamic watermarks on the Data Room plan ($52/admin/month).

By the Numbers: LP Reporting in 2026

- 92% — Ninety-two percent of institutional LPs say reporting quality directly influences their re-up decisions. (Preqin 2024 Global Alternatives Report)

- 45 / 75 days — The SEC's 2023 private fund adviser rules proposed quarterly statement deadlines of 45 days for liquid funds and 75 days for illiquid funds, though the Fifth Circuit vacated those provisions in June 2024. (SEC Release No. IA-6383)

- Q+60 days — The industry-standard LP reporting deadline is 60 days after quarter-end for interim reports, per ILPA best-practice guidance. (ILPA Principles 3.0)

- 4 core metrics — Every LP report must include net IRR, TVPI (Total Value to Paid-In), DPI (Distributed to Paid-In), and RVPI (Residual Value to Paid-In), calculated net of fees and carry. (ILPA Performance Template)

- v2.0 — The ILPA Reporting Template was updated to version 2.0 in 2025 and is now the de facto standard for fee and expense disclosure across the private equity industry. (ILPA Reporting Template)

- 20+ fund managers — A typical institutional LP is invested with more than 20 fund managers, making standardized reporting essential for cross-fund comparison. (Preqin 2024 Investor Survey)

- 73% — Seventy-three percent of LPs cite "lack of transparency" as their top frustration with GP reporting. (ILPA LP Survey)

- 3 minutes — Peony's AI auto-indexing organizes a full quarterly reporting pack for secure LP distribution in under three minutes, replacing hours of manual folder setup. (Peony Auto-Indexing)

What Is LP Reporting and Why It Matters in 2026

LP reporting is the structured, periodic disclosure a general partner (GP) makes to its limited partners (LPs) covering fund performance, portfolio updates, financials, fees, and risk. It's how your investors know whether you're doing what you said you'd do with their capital.

In 2026, three forces have raised the bar:

-

ILPA standardization. The Institutional Limited Partners Association updated its Reporting Template to v2.0 in 2025 and released a companion Performance Template. Together, these give LPs a granular, comparable format for fees, expenses, carry, and returns. Even if you don't adopt every field, your LPs are benchmarking you against managers who do.

-

Post-regulatory expectations. The SEC's 2023 private fund adviser rules would have required standardized quarterly statements within 45 or 75 days depending on fund liquidity. The Fifth Circuit vacated key provisions in June 2024, but most institutional LPs had already recalibrated their expectations. The legal mandate may be gone; the investor mandate is not.

-

Technology gap visibility. LPs investing across 20 or more managers can immediately tell who sends a polished portal link with tracked access and who sends an email attachment with "Q3 Report v3 FINAL.pdf." The contrast is sharper every year.

The good news: getting LP reporting right is more achievable than ever, especially for emerging managers. The templates are public, the technology is affordable, and the bar for "good" is well-defined.

The Core VC LP Reporting Pack

A complete quarterly LP reporting package in 2026 includes six components. I'll break each one down in the sections that follow.

| Component | Frequency | Key Deliverables |

|---|---|---|

| Summary letter / MD&A | Quarterly | Market context, portfolio narrative, risk commentary |

| Fund-level financials | Quarterly + annual audit | Balance sheet, income statement, cash flows |

| Performance metrics | Quarterly | Net IRR, TVPI, DPI, RVPI, benchmarks |

| Portfolio company schedule | Quarterly | Holdings detail, valuations, milestones |

| Fees, expenses, and carry | Quarterly (ILPA format) | Management fees, fund expenses, offsets, carry accrual |

| Capital account statements | Quarterly | Per-LP contributions, distributions, ending balance |

Optional additions depending on your strategy: ESG/impact reporting, co-investment summaries, and currency exposure analysis for global funds.

ILPA's Quarterly Reporting Standards outline a similar core structure: summary letter, balance sheet, schedule of investments, statement of operations, statement of cash flows, plus supplemental management reports and fee templates.

Performance Metrics: How LPs Actually Want to See Returns

This is the section LPs flip to first. Getting it right means showing a blend of metrics, always net of fees and carry, with enough context to be meaningful.

The four metrics every LP expects

-

Net IRR -- the time-weighted internal rate of return of the fund, calculated net of management fees, fund expenses, and carried interest. This is the headline number, but it's not enough on its own.

-

TVPI (Total Value to Paid-In) -- total value (realized distributions plus current NAV) divided by capital paid in. Shows the overall multiple of money.

-

DPI (Distributed to Paid-In) -- actual cash and stock distributions returned to LPs divided by capital paid in. This is the "cash-on-cash" metric LPs care about most in mature funds, and increasingly in younger ones too.

-

RVPI (Residual Value to Paid-In) -- remaining net asset value divided by capital paid in. The unrealized portion of TVPI. LPs mentally discount this, especially in early-stage VC where markups can evaporate.

Invest Europe's Investor Reporting Guidelines explicitly recommend reporting these four metrics at fund level on a net-of-fees, net-of-carry basis and clarifying how TVPI decomposes into DPI + RVPI.

Best practices for performance presentation

- Show metrics since inception and over trailing periods (1-year, 3-year where applicable).

- Include J-curve progression charts showing cumulative contributions, distributions, and NAV over time. LPs use these to compare your pacing against peer funds.

- Provide vintage-year and benchmark context where possible. Cambridge Associates, PitchBook, and Preqin all publish quarterly VC benchmark data. Even a simple quartile ranking gives LPs the comparative frame they need.

- Separate gross and net returns clearly. Mixing them is one of the fastest ways to erode LP trust.

- For funds with multiple closes, show performance from first close as the primary benchmark, with supplementary metrics from subsequent close dates if requested.

The goal is giving LPs a clear, honest picture of both realized and unrealized performance, and how it's evolving. Not a vanity IRR on a cherry-picked date.

Fund Financials, Cash Flows, and Capital Accounts

Your LPs need to reconcile what's happening in the fund with their own books. Fund administrators produce most of this, but as GP you're responsible for making sure it's consistent and readable, not just technically correct.

Fund-level financial statements

- Balance sheet -- assets (portfolio investments at fair value, cash), liabilities (accrued expenses, management fee payable), and partners' capital.

- Statement of operations -- investment income, realized and unrealized gains/losses, management fees, fund expenses, net income.

- Statement of cash flows -- capital calls, distributions, investment purchases and proceeds, operating expenses paid.

Capital account statements (per LP)

Every LP needs a statement showing:

- Opening capital balance

- Contributions called during the period

- Share of income/loss

- Management fees and expenses allocated

- Carried interest accrued

- Distributions received

- Ending capital balance

ILPA's capital call and distribution best practices emphasize that call and distribution notices should tie cleanly into cumulative cash-flow metrics and fund financials, so LPs aren't manually reconstructing history.

For funds with multiple share classes or side-letter economics, capital account statements need to reflect the specific fee rate, carry percentage, and any offsets applicable to each LP. I'll cover how to handle this in the share-class section below.

Portfolio Company Reporting: Signal Over Noise

This is the section LPs enjoy reading when it's done well, and skim past when it's a wall of undifferentiated bullet points.

What to include for each active company

ILPA's supplemental portfolio company reporting checklist suggests:

- Basics: company name, headquarters, sector, entry date, investment stage

- Your position: cost basis, ownership percentage, current fair value, valuation methodology

- Key developments: product milestones, revenue trajectory, team changes, commercial wins or losses

- Risk factors: regulatory exposure, customer concentration, burn rate relative to runway

- For exited positions: summary of outcome, realized multiple, timeline from entry to exit

How to structure the narrative

The mistake I see most often is treating every portfolio company equally in the report. LPs don't want two pages on a $50K follow-on that's 0.3% of the fund. They want depth on the positions that drive NAV and risk.

- Group by status: separate your portfolio into categories like core performers, stable positions, watch list, and exited. This immediately tells LPs where to focus.

- Tier the detail: give your top 10 to 15 holdings by NAV a full narrative write-up. Keep the rest tabular with key metrics only.

- Flag what changed: LPs are comparing this quarter to last quarter. Make it easy by noting significant valuation changes, new financing rounds, or strategic pivots explicitly.

- Address sector-specific risks: for AI companies, mention regulatory and compute cost exposure. For biotech, note clinical trial milestones. For fintech, cover regulatory changes. LPs investing across sectors appreciate when you demonstrate awareness of the risks specific to your portfolio.

Use Peony's AI document extraction to let LPs ask natural-language questions about individual portfolio companies across all your uploaded reports and get cited answers with exact page numbers, rather than digging through PDFs manually.

Fees, Expenses, and Carry: Embracing ILPA v2.0

Fees are where LP trust is won or lost. The ILPA Reporting Template v2.0 was updated specifically to bring more granularity and comparability to this section.

What the ILPA v2.0 template covers

- Management fees: base amount, fee rate, calculation basis (committed vs. invested capital), any step-downs

- Fund-level expenses: broken down by category (legal, audit, tax, administration, insurance, travel, other)

- Transaction and monitoring fees: amounts received, offset percentages, net impact to the fund

- Carried interest: accrued carry, distributed carry, clawback exposure if applicable

- Organizational expenses: capped amounts, actual spend, amortization if applicable

The template aligns fields with general ledger accounts, which is a meaningful improvement over v1.0. It means LPs can map your numbers directly into their portfolio monitoring systems rather than manually translating categories.

Why this matters for emerging managers

You might think fee transparency is mainly a concern for mega-funds. It's the opposite. Institutional LPs evaluating an emerging manager have less track record data to go on, so they scrutinize fees and alignment more carefully. Adopting ILPA-style fee reporting early signals that you take governance seriously.

You don't need to populate every field on day one. Start with management fees, fund expenses by category, and carry accrual. Add transaction fees and offsets as they become relevant.

ILPA Templates and Reporting Standards in 2026

The Institutional Limited Partners Association has published several interrelated reporting frameworks. Here's how they fit together.

ILPA Reporting Template v2.0 (2025)

The core fee and expense disclosure framework. Updated in 2025 to align with general ledger accounts and add more granular breakdowns of transaction fees, monitoring fees, and organizational expenses. Intended to supplement your quarterly narrative report, not replace it.

ILPA Performance Template

Standardizes how funds report net IRR, TVPI, DPI, RVPI, and related metrics. Provides a consistent format so LPs can compare performance across managers without reconciling different calculation methodologies.

ILPA Quarterly Reporting Standards

A broader framework covering the full quarterly pack: summary letter, financial statements, portfolio schedule, and supplemental data. Recommends quarterly reports within 60 days of quarter-end and audited annual statements within 120 days of fiscal year-end.

ILPA Principles 3.0

The overarching governance framework covering alignment of interests, governance, and transparency. The reporting templates are the practical implementation of the transparency principles.

How to adopt these without drowning

Start with the Reporting Template v2.0 for fees and the Performance Template for returns. These are the two areas where LPs most want standardization. Layer in the broader Quarterly Reporting Standards structure over time. Most fund administrators are already familiar with ILPA templates and can help you populate them.

Upload your completed ILPA templates alongside your narrative report to a Peony data room and use AI auto-indexing to organize everything into a clean quarterly folder structure. The entire setup takes under 5 minutes.

Quarterly Reporting Cadence and Best Practices

The standard cadence

| Report Type | Frequency | Target Deadline | Notes |

|---|---|---|---|

| Quarterly report (full pack) | Quarterly | 60 days after quarter-end | ILPA recommended timeline |

| Audited annual financials | Annual | 120 days after fiscal year-end | Includes Q4 narrative letter |

| Capital call / distribution notices | As needed | 10 business days before due date | ILPA best practice |

| Ad-hoc updates | As needed | Within 5 business days of event | Material events only |

| Annual meeting materials | Annual | 30 days before meeting | Agenda, presentation, logistics |

What triggers an ad-hoc update

Not every development warrants an out-of-cycle communication. Reserve ad-hoc updates for:

- Large exits or IPOs (especially if they materially change fund-level metrics)

- Significant markdowns (sub-50% write-downs on material positions)

- Key person departures or additions

- Fund-level events: extension votes, GP commitment changes, key person clause triggers

- Regulatory or legal events affecting the fund or material portfolio companies

Cadence best practices

-

Set an internal SLA and share it. Tell your LPs in the side letter or LPA what they can expect: "Quarterly reports within 60 days, audited financials within 120 days, ad-hoc updates within 5 business days of material events." Then hit those marks consistently.

-

Front-load the summary letter. Many LPs manage 20 or more fund relationships. Your summary letter may be the only page they read in full. Put the most important information -- headline performance, major portfolio events, material changes to fund strategy or team -- in the first two paragraphs.

-

Maintain consistent formatting across quarters. LPs compare your reports period-over-period. If you change your layout, metric definitions, or portfolio groupings every quarter, you force them to re-orient each time. Pick a format and stick with it.

-

Use the same format across funds. If you manage multiple vehicles (Fund I, Fund II, co-invest SPV, continuation vehicle), keep the reporting structure consistent. LPs invested across your vehicles shouldn't have to learn a new format for each one. For continuation vehicle-specific considerations, see our guide to structuring data rooms for continuation vehicles.

How to Distribute LP Reports Securely

The delivery mechanism matters as much as the content. I've seen GPs spend weeks on a report and then email it as an unprotected PDF to a distribution list. That's a security gap and a missed intelligence opportunity.

Why email attachments are inadequate

- No access control. Once the PDF is sent, anyone who receives or intercepts it can read, copy, and forward it.

- No engagement data. You have no idea whether LPs opened the report, which sections they read, or how long they spent on it.

- No version control. If you need to correct a number, you can't recall the original. You just send another email with "updated" in the subject line.

- No audit trail. If a portfolio company's sensitive information leaks, you can't trace how it happened.

The data room approach

A dedicated LP reporting data room solves all four problems:

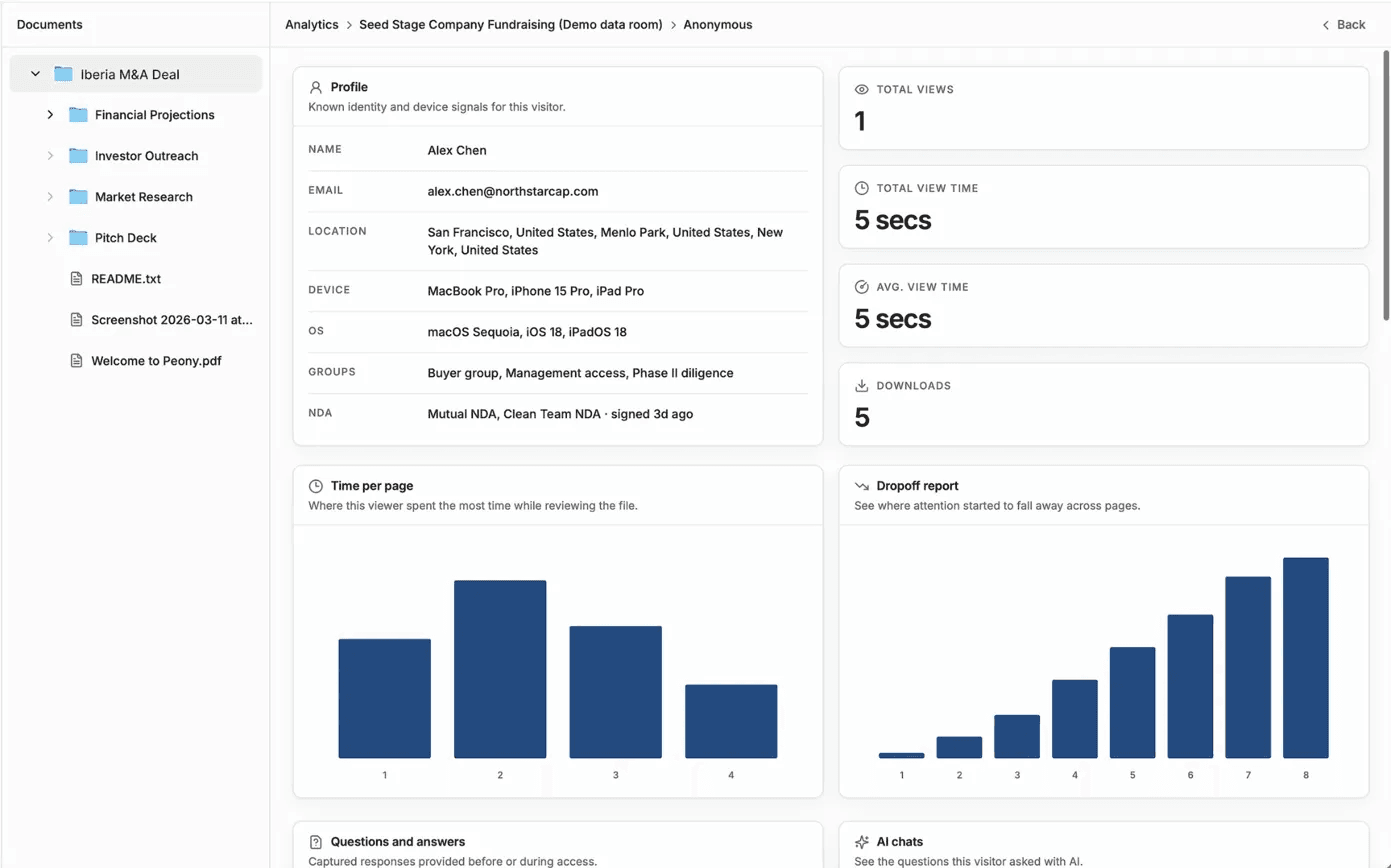

- Per-LP access controls. Each LP gets a unique, identity-verified link that shows them the shared fund content plus only their own capital account statement and class-specific schedules.

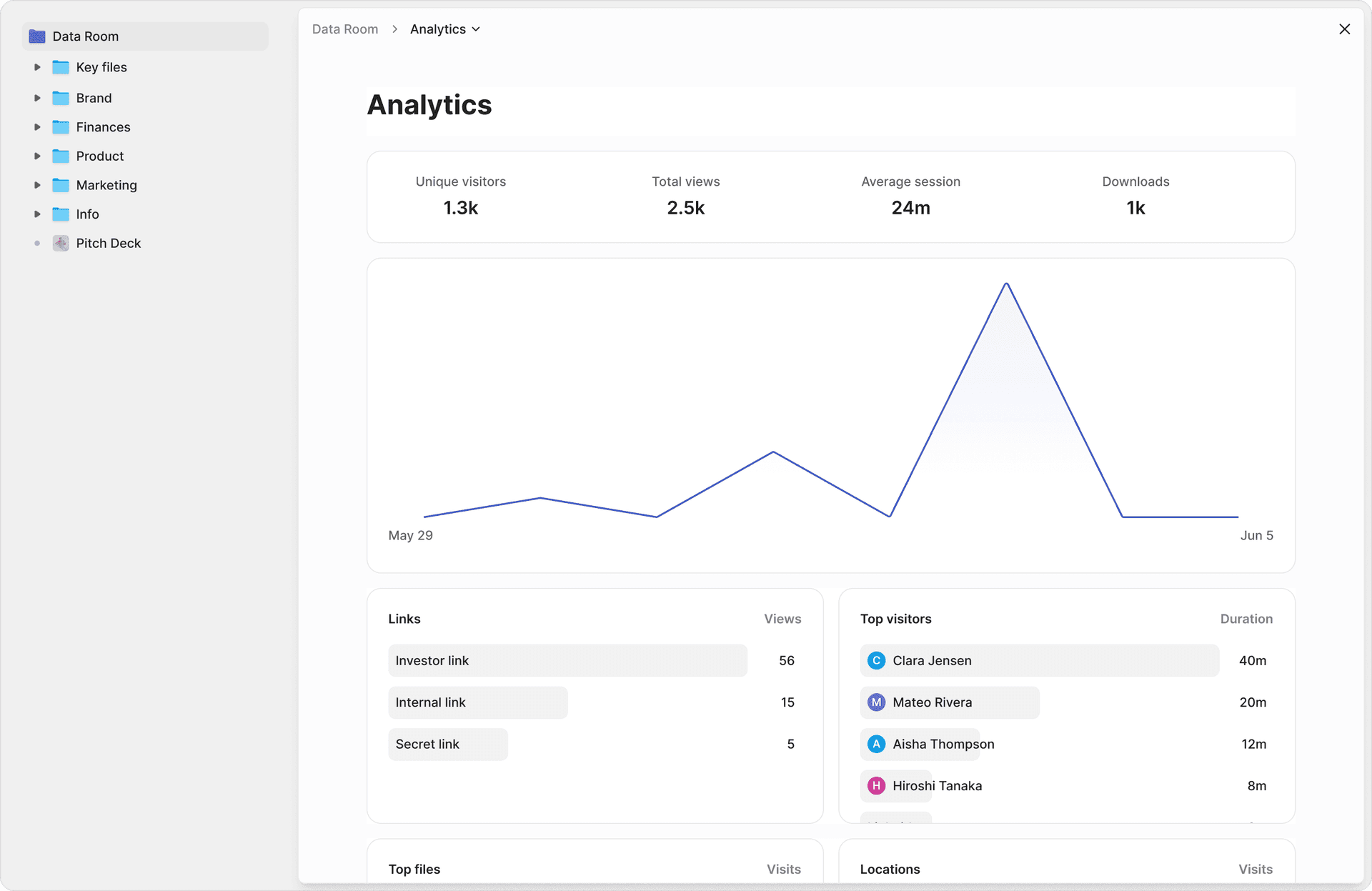

- Page-level engagement analytics. You can see exactly which pages each LP read and for how long. If your largest LP hasn't opened the Q3 report two weeks after distribution, you know to make a call.

- Version control. Update a document in the room and every LP sees the current version at the same link. No "v2 FINAL" email chains. Peony's link management lets you update documents while keeping the same shared URL.

- Security layers. Screenshot protection that blocks and logs capture attempts. Dynamic watermarks with each LP's identity baked into every rendered page. NDA gates before first access. Password protection and email verification for multi-factor access control.

- Audit trail. Complete log of every action, so if you ever face a leak, you have forensic data.

Q&A workflow for LP questions

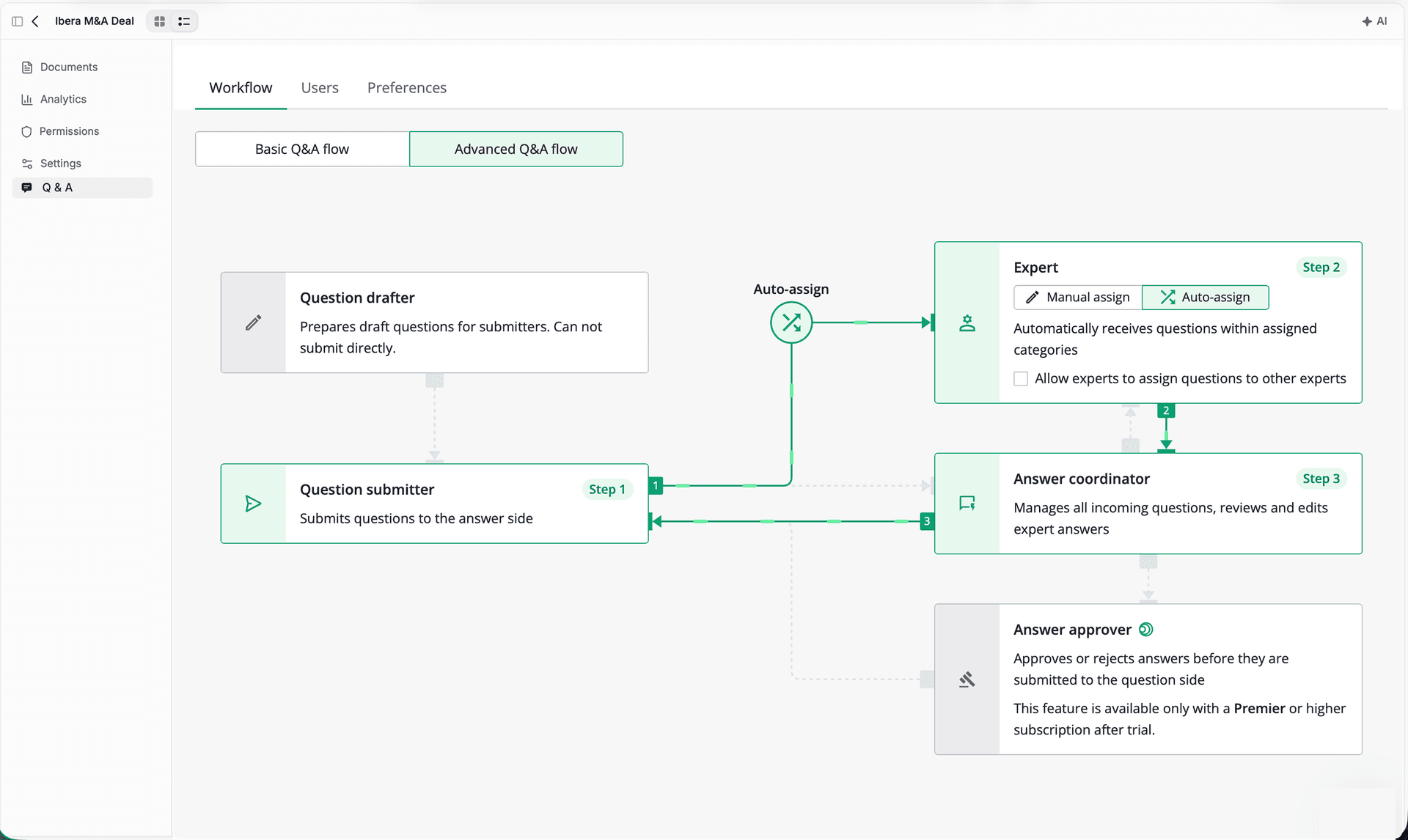

After LPs read the report, questions come in. The traditional approach -- scattered emails, Slack messages, phone calls -- is a nightmare to track and creates inconsistent responses.

Peony's Smart Q&A workflow centralizes this: LPs submit questions directly in the data room, AI drafts initial responses based on the documents in the room, your team reviews and approves, and the approved answer goes back to the LP. Every exchange has a full audit trail. This is especially valuable during annual meetings or when multiple LPs ask variations of the same question.

Side letter execution

Many LP relationships involve side letters covering fee discounts, co-investment rights, MFN clauses, or reporting requirements. Peony's built-in e-signatures with AI-powered field detection handle side letter execution without requiring a separate DocuSign or HelloSign subscription.

One honest caveat. If your fund's anchor LP mandates a specific legacy VDR provider by name in their side letter — which happens occasionally with sovereign wealth funds and the largest endowments — Peony's newer brand won't satisfy that requirement yet. For every other LP relationship, Peony delivers stronger analytics, faster setup, and better security at a fraction of legacy pricing.

Common LP Reporting Mistakes

I've reviewed hundreds of LP reports that come through our data rooms. These are the five mistakes I see most often, roughly in order of how much they damage LP relationships.

1. Reporting gross returns without clear labeling

Some GPs lead with gross IRR in the summary letter and bury the net figure in an appendix. LPs notice. ILPA and Invest Europe both recommend that headline performance metrics be presented net of all fees and carry. Show gross as a supplementary metric if you want, but net must be the primary number.

2. Missing or late delivery with no communication

Missing your reporting deadline happens. What destroys trust is going silent about it. If your report is going to be late, send a brief update to LPs before the deadline explaining why and providing a revised date. Most LPs are understanding about a two-week delay; none are understanding about silence.

3. Burying fee disclosures

Fees buried in footnotes or aggregated into a single line item signal that you'd rather LPs not look too closely. The ILPA v2.0 template exists specifically to make fee disclosure transparent and comparable. Adopting it (even partially) demonstrates good faith.

4. No engagement tracking

If you send a report and never know whether LPs read it, you can't identify disengaged LPs who might be headed for the exit. Peony's page-level analytics solve this by showing you exactly which pages each LP viewed and for how long. A LP who hasn't opened a report in two quarters is telling you something.

5. Inconsistent formatting across quarters

Every quarter your LP operations team or fund admin builds the report, they should start from the previous quarter's template. Changing layouts, metric definitions, or portfolio groupings without explanation forces LPs to waste time reorienting. Consistency compounds trust.

Bonus: forgetting LP-specific data

LPs with different economics (fee discounts, carry rates, co-investment allocations) need capital account statements that reflect their specific terms. Sending a LP the wrong capital account statement is a serious breach. Use per-LP access permissions in your data room to ensure each investor only sees their own data.

The Bottom Line

LP reporting is a relationship tool, not a compliance exercise. The GPs who treat it that way -- who report transparently, hit their deadlines, and make information easy to access -- are the ones whose LPs re-up without a second conversation.

Here's how I'd tier the approach:

If you're raising Fund I or II (under $50M): Start with a clean quarterly narrative, the four core performance metrics (net IRR, TVPI, DPI, RVPI), per-LP capital account statements, and a basic ILPA-style fee breakdown. Distribute through a Peony data room on the free tier — the same platform works for fundraising and ongoing reporting. You'll have page-level analytics, screenshot protection, and dynamic watermarks from day one.

If you're at Fund III+ ($50M to $250M): Add the full ILPA Reporting Template v2.0 for fees and expenses, a portfolio company schedule with tiered detail, vintage-year benchmarks, and a formal reporting SLA. Use Peony's Smart Q&A to centralize LP questions and AI document extraction to let LPs self-serve answers across your reporting archive.

If you're institutional scale ($250M+): Everything above, plus co-investment reporting, ESG/impact metrics if applicable, currency exposure analysis for global portfolios, and multi-level access gating with NDA, password, email verification, and 2FA layers. Consider built-in e-signatures for side letter management.

At every stage, the platform matters less than the discipline. But having a secure, intelligent reporting portal that tracks engagement, protects sensitive data, and centralizes LP communications makes that discipline dramatically easier to maintain.

Frequently Asked Questions

What metrics should a VC fund include in quarterly LP reports?

Every quarterly LP report should include net IRR, TVPI (Total Value to Paid-In), DPI (Distributed to Paid-In), and RVPI (Residual Value to Paid-In), all calculated net of fees and carry. Best practice also includes vintage-year benchmarks, contribution and distribution waterfall charts, and a J-curve progression chart. Peony's page-level analytics show you exactly which metrics pages each LP spends the most time on, so you can prioritize the data that matters most to your investor base.

How often should VC funds report to LPs?

The industry standard is quarterly written reports with full performance, portfolio, and financial data, plus annual audited financials. ILPA recommends quarterly reports within 60 days of quarter-end and audited annual statements within 120 days of fiscal year-end. Ad-hoc updates should go out for material events like large exits, significant markdowns, or key team changes. Peony data rooms let you set up a persistent LP portal where you upload each quarter's report and LPs get notified automatically, eliminating the email attachment cycle.

What is the ILPA Reporting Template v2.0?

The ILPA Reporting Template v2.0, updated in 2025, is a standardized Excel-based framework for disclosing management fees, fund expenses, transaction and monitoring fees, and carried interest calculations at a granular level. It aligns reporting fields with general ledger accounts, making it easier for LPs to reconcile data across managers. The companion ILPA Performance Template standardizes how funds report net IRR, TVPI, DPI, and RVPI. Peony's AI auto-indexing can organize your ILPA template files alongside narrative reports into a clean folder structure in under 3 minutes.

How do I share LP reports securely?

The most secure approach is a dedicated data room with per-LP access controls rather than email attachments or shared drives. Best practice includes NDA gates before first access, dynamic watermarks with each LP's identity baked into every rendered page, screenshot protection that blocks and logs capture attempts, and link-level permissions so each LP only sees their own capital account data. Peony's Free plan includes email verification, link expiry, and per-page analytics. The Business plan ($30/admin/month) adds NDA gates and screenshot protection, with dynamic watermarks on the Data Room plan ($52/admin/month), so even emerging managers can distribute LP reports at institutional grade.

What are the most common LP reporting mistakes fund managers make?

The five most common mistakes are: reporting gross returns without clearly labeling net-of-fee figures, sending static PDFs with no way to track whether LPs actually read the report, inconsistent formatting across quarters that forces LPs to relearn your layout, burying fee disclosures in footnotes instead of using ILPA-style breakdowns, and missing the reporting deadline without proactive communication. Peony's page-level analytics solve the second problem by showing you exactly which pages each LP read and for how long, so you know who is engaged and who needs a follow-up call.

Do I need separate LP reports for different share classes?

You need class-specific capital account statements and fee and carry schedules wherever economics differ, such as a founders class versus a standard LP class or fee-discount side letters. However, the fund-level performance section, portfolio company updates, and market commentary can be shared across all LPs. Peony supports this with multi-level access gating: you can set per-folder permissions so each LP sees the shared fund content plus only their own class-specific schedules, all within one data room rather than maintaining separate portals.

What happened to the SEC private fund adviser reporting rules?

The SEC adopted private fund adviser rules in August 2023 requiring standardized quarterly statements on fees and performance within 45 days for liquid funds and 75 days for illiquid funds. In June 2024, the Fifth Circuit Court of Appeals vacated key provisions, holding the SEC exceeded its statutory authority. The legal mandate is currently off the table, but the directional expectation from institutional LPs remains: they benchmarked your reporting against those standards and still expect ILPA-aligned transparency. Peony's Q&A workflow helps you manage LP compliance questions efficiently: LPs submit questions, AI drafts answers, your team reviews, and approved responses go out with a full audit trail.

What is the best data room for LP reporting?

The best LP reporting data room combines persistent document storage, per-LP access controls, engagement analytics, and a Q&A workflow in one platform. Peony is purpose-built for this: AI auto-indexing organizes quarterly reports in under 3 minutes, page-level analytics show which sections each LP actually reads, dynamic watermarks and screenshot protection prevent leaks, built-in e-signatures with AI field detection handle side letter execution, and the entire platform starts free with the Business plan at $30 per month and the Data Room plan at $52 per month for unlimited rooms.

Related Resources

- Venture Capital Data Room Checklist -- what documents belong in a VC fundraising data room

- Seed Funding Guide -- how to raise your seed round from first pitch to close

- Data Room for Investors -- how to set up a data room that investors actually want to open

- How to Share an Interactive LP Report With Your Limited Partners (Securely) -- the last-mile sharing mechanic: send the live quarterly report through a per-LP secure viewer instead of a flattened PDF

- How to Structure a Data Room for Continuation Vehicles -- LP reporting considerations for GP-led secondaries

- Startup Fundraising Strategy -- the complete playbook for startup fundraising

- Best Data Rooms for Startups -- comparing data room options for early-stage companies

- Venture Capital Software Solutions -- the full VC tech stack from deal flow to LP reporting

- Best Data Rooms for Private Equity -- data room comparison for PE fund operations

- Peony for Venture Capital -- how Peony supports the full VC workflow

- Peony Pricing -- free tier, Business at $30/month, Data Room at $52/month

You might also like

Jun 29, 2026

How to Share an Interactive LP Report With Your Limited Partners (Securely)

Jul 7, 2026

Narrative Data Room: What It Is, When It Works, and When It Backfires (2026)

Jun 29, 2026

How to Share an Interactive Financial Model With an Investor (Securely)