Private Placement Data Room: The Reg D Evidence Layer (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Private Placement Data Room: The Reg D Evidence Layer

Last updated: July 2026

Quick answer: A private placement data room is the secure, permissioned room an issuer or sponsor uses to run a Regulation D securities offering — and its real job is not presentation, it's proof. A PPM discloses; the data room proves. Because a Reg D raise runs on antifraud liability (Rule 10b-5), what you actually need is a provable, per-investor record of exactly what each investor saw and when — plus, for a Rule 506(c) raise, a verification-evidence trail. The room lives across three phases: (1) investor diligence (the PPM and exhibits, shown under NDA), (2) 506(c) accredited-verification intake (gate, collect, and log the evidence — the room does not verify accreditation itself), and (3) ongoing investor reporting after the close. Run it on a flat-rate platform — Peony at $30/admin/month (Business) for NDA gating, e-signatures, and the audit trail, or $52/admin/month (Data Room) when you need watermarks and per-file permissions — rather than paying per-deal VDR fees on every raise.

I run Peony, a data room platform serving 6,800+ customers across M&A, fundraising, and private securities offerings. Over the past two years I've set up rooms for operating companies selling their own stock under Regulation D, sponsors syndicating deal-specific SPVs, and placement agents marketing offerings to a qualified investor list. The mistake I see most often is treating the private placement data room as a nicer way to send a PDF. It isn't. In a Reg D raise, the room is the evidentiary spine of the offering — the thing that, if a dispute or an SEC exam ever arrives, lets you prove what you disclosed, to whom, and when, instead of relying on your memory and a folder of sent emails.

This guide is the hub for that workflow: what a private placement data room is, the three phases of a Reg D raise where it lives, the 506(b) versus 506(c) distinction that makes access scoping load-bearing, and how issuers, sponsors, and placement agents should build it. It links down to three companion guides — the PPM document itself, the 506(b) vs 506(c) deep dive, and the step-by-step room setup — so this page stays the map, and the spokes go deep.

If you're raising into a blind-pool fund vehicle, this is adjacent but not your post — a fund raise is technically a private placement, but the fund posts own that workflow: see the real estate fund data room and VC fund data room checklist. If you're an independent sponsor doing deal-by-deal Reg D raises, see the independent sponsor guide. This hub owns the operating-company and sponsor securities-offering case — a company selling its own securities under Reg D.

What is a private placement data room?

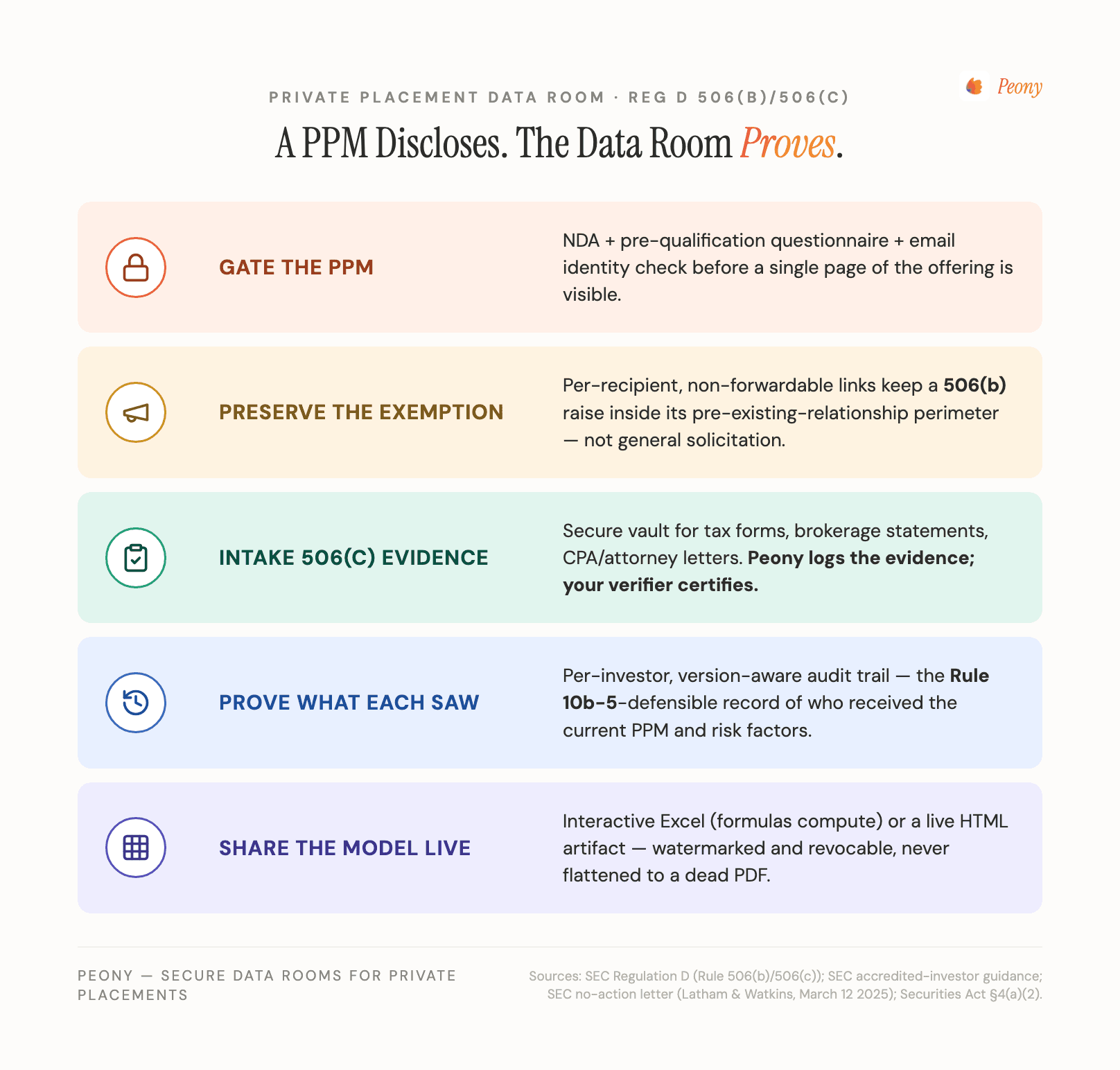

A private placement data room is the secure online environment an issuer (or a sponsor, or their placement agent) uses to conduct a private securities offering — typically under Regulation D — without registering the offering with the SEC. Inside it sit the private placement memorandum (PPM) and its exhibits, the subscription agreement and investor questionnaire, the financial model and supporting documents, and the access controls that decide who sees what.

But the definition that matters is functional. Unlike a generic file share, a private placement data room exists to do three things a Reg D offering legally needs:

- Gate access so the right investors — and only the right investors — see the offering, under an NDA, before any sensitive document is visible.

- Capture evidence — for a 506(c) raise, the accredited-verification documentation; for every raise, the executed subscription documents and written representations.

- Produce a record — a per-investor, per-version, timestamped audit trail of exactly what each investor received and when.

That third function is the one that turns a data room from a convenience into the evidence layer of your offering. We'll come back to why, but first: where in the raise does the room actually live?

A PPM discloses; the data room proves: why securities law makes the room load-bearing

Here is the non-commodity point that most "best data room" lists miss. A private securities offering doesn't escape liability just because it's exempt from registration. Reg D exempts you from registering the offering — it does not exempt you from the antifraud provisions of the securities laws, most importantly Rule 10b-5, which makes it unlawful to make a material misstatement or omit a material fact in connection with the sale of a security.

That single fact reshapes what your data room is for. Your PPM is the disclosure — it's where you state the risks, the use of proceeds, the conflicts, the capital structure, and the terms. But disclosure you can't prove you made is, for litigation purposes, close to no disclosure at all. If an investor later claims you omitted a material risk, your defense is a record: that this specific investor received this specific version of the PPM, with those risk factors, on this date, and signed a subscription agreement that referenced them.

An emailed PDF can't produce that record. You can't show which version landed in which inbox, whether the investor opened the updated risk factors, or that the document they signed against was the current one. A private placement data room can — and that's the whole game:

- The PPM discloses. It's the document that satisfies the disclosure side of your obligation.

- The data room proves. It's the controlled delivery that produces a per-investor, per-version, timestamped record of what was disclosed, gated behind a signed NDA, with the subscription e-signatures attached.

So the issuer's real need isn't a prettier brochure. It's a defensible evidentiary record — and for a 506(c) raise, a verification-evidence trail on top of it. That's the lens this entire post is built around, and it's why an operating-company Reg D raise needs more discipline than a casual investor file share.

Where does the private placement data room live? The 3 phases of a Reg D raise

The room isn't a single moment — it spans the offering's life across three phases, each with a different job:

| Phase | What the room does | Core artifacts |

|---|---|---|

| 1. Investor diligence | Delivers the PPM and exhibits under NDA to prospective investors; logs who saw which version, when | PPM, risk factors, financial model, cap structure, material contracts, NDA |

| 2. 506(c) verification intake | Gates access until verification evidence is collected and logged; captures subscription e-signatures (506(c) only) | Verification documentation, pre-qual questionnaire, written representations, subscription docs |

| 3. Ongoing investor reporting | Standing room after the close for distributions, notices, and tax documents to committed investors | Distribution/capital-call notices, K-1s, audited financials, investor updates |

Phase 1 — investor diligence. Prospective investors review the PPM and its exhibits. The room's job is to gate that behind an NDA, show the current version, and log every view. This is where the antifraud record gets built, one investor at a time.

Phase 2 — 506(c) accredited-verification intake. If you're raising under 506(c) (general solicitation permitted, all investors must be accredited), the room becomes the front door for verification: it holds access closed until the investor's accreditation evidence is collected, then opens the PPM. A 506(b) raise skips the verification gate but tightens access scoping instead (more on that below).

Phase 3 — ongoing investor reporting. The phase most transaction-only VDRs ignore. After the close, the issuer still owes investors distribution notices, K-1s, and updates for as long as they hold the security. A standing room — one you're not paying a per-deal fee to keep open — carries that load, with the same audit trail intact.

This three-phase span is exactly why flat-rate, unlimited-room pricing fits a private placement and per-deal pricing doesn't: the room outlives the transaction window.

What is the difference between Rule 506(b) and 506(c) for your data room?

The exemption you file under is a data-room decision, because 506(b) and 506(c) impose opposite constraints on access:

- Rule 506(b) — No general solicitation. You can only offer to investors with whom you (or your placement agent) have a pre-existing, substantive relationship. You may include up to 35 non-accredited but sophisticated investors alongside accredited ones, and you don't have to take affirmative verification steps for accredited investors (you can rely on their representations). According to the SEC, 506(b) is by far the larger channel — issuers raised roughly $259 billion through 506(b) over the SEC's stated 12-month window (July 2022–June 2023), about 16x the amount raised under 506(c), despite 506(c) allowing advertising.

- Rule 506(c) — General solicitation permitted. You can advertise the offering publicly, but every investor must be accredited, and you must take "reasonable steps to verify" their accredited status. Issuers raised roughly $16 billion under 506(c) over that same SEC window.

For the room, the practical translation is:

- Under 506(b), the room must stay invitation-only — scoped access is part of keeping the exemption intact.

- Under 506(c), the room must gate and capture verification evidence before the PPM is visible.

Either way, an accredited investor under the SEC's definition is, broadly, someone with income over $200,000 (or $300,000 jointly) for the prior two years, or net worth over $1 million excluding their primary residence — or who holds a Series 7, 65, or 82 license. And in either case, you file a Form D on the SEC's EDGAR system within 15 days of the first sale. We unpack the full mechanics in the Reg D data room: 506(b) vs 506(c) spoke; below is the trap that catches issuers most.

The 506(b) general-solicitation trap: why access scoping is exemption-load-bearing

This is the single most expensive mistake an issuer can make with a data room, so it gets its own section.

Under 506(b) you cannot generally solicit. The catch: a poorly scoped data room can itself look like general solicitation. A link anyone can open, a URL forwarded freely, a room indexed by a search engine, a "request access" page reachable by the public — any of these can undercut the argument that you only offered to investors with a pre-existing relationship. And losing the 506(b) exemption isn't a paperwork problem; it can convert your exempt offering into an unregistered public offering, with the liability that carries.

So under 506(b), access scoping is exemption-load-bearing, not a convenience. The controls that keep you safe:

- Personalized, per-investor links — never one shared URL pasted into emails or a deck.

- Email authentication — every viewer is identified before they see anything.

- NDA gating — the PPM stays invisible until the investor signs.

- Link expiry and one-click revocation — a forwarded link doesn't become an open door.

- A per-investor audit trail — the record that demonstrates access stayed scoped to your pre-existing relationships.

On Peony, all of these are available from the Business plan ($30/admin/month). The mental shift is the important part: in a 506(b) raise, your access-control settings are part of your securities compliance posture, not just your file hygiene.

How does a 506(c) data room collect accredited-verification evidence?

If you switch to 506(c) to advertise the raise, the room's job flips from scoping access to collecting verification evidence — and here precision matters, because it's easy to overclaim what a data room does.

A data room does not verify accreditation. Peony doesn't, and neither does any VDR. The actual accreditation determination is made by third-party verification services, or by a written confirmation from the investor's CPA, attorney, or registered broker-dealer. What the data room does is run the workflow around that determination and capture the evidence:

- Gate the PPM behind a signed NDA plus a pre-qualification questionnaire and email identity verification, so nothing sensitive is visible until the investor clears the front door.

- Collect and store each investor's verification documentation and their written representations.

- Capture subscription e-signatures on the subscription agreement in-flow.

- Log a per-investor audit trail showing the verification step preceded access.

The SEC's standard for 506(c) is "reasonable steps to verify," and a March 12 2025 SEC no-action letter (Latham & Watkins) added a path based on a high minimum investment amount plus written investor representations — a lower-friction route than collecting tax returns or net-worth statements, where the size of the check itself helps establish accreditation. Whichever path you use, the room is where the evidence of those steps lives.

Say it precisely on your own materials too: Peony collects, gates, and logs the verification evidence; it does not certify accreditation. Overclaiming here is itself a compliance risk.

Who needs a private placement data room: issuers, sponsors, and placement agents?

Four roles run or depend on this room, each for a slightly different reason:

- The issuer — an operating company selling its own stock, units, or notes under Reg D. Its binding constraint is antifraud liability and keeping the exemption intact; the room is its defensible record.

- The sponsor / syndicator — pooling investor capital into a deal-specific entity or SPV. It needs the offering room kept separate from any underlying asset deal room, and it lives the 506(b)-vs-506(c) decision on every raise.

- The placement agent / broker-dealer — marketing the offering to a qualified investor list on the issuer's behalf. It needs per-investor access scoping and an audit trail that doubles as suitability and recordkeeping evidence across many investors.

- Securities counsel — drafting the PPM and the Reg D filing strategy. For counsel, the room is litigation and exam insurance: it must prove what each investor received, when, and that the verification or scoping steps actually happened.

All four want the same underlying thing: a room that produces a record they can stand behind.

Can a solo sponsor run this alone? A 72-year-old broker's go-live

Yes — and I want to ground that in a real customer, because "evidence layer" can sound like something that needs a back office. It doesn't — Peony's 6,800+ customers include plenty of one-person shops.

Robert Castro is the owner-broker of Arris Properties, a one-man investment-sales brokerage in La Quinta, California, specializing in land and land development for rental housing in the Inland Empire. Decades in the business, no assistant, no tech team, no fund administrator. When he syndicated his own deal, he had the PPM and the rest of his Reg D documents prepared — and the piece he needed was exactly what this post calls the evidence layer. He set the room up himself and went live the next day. In his words:

"I'm going to set it up tomorrow and go live. I think I can figure it out. I'm 72 but I've been using technology for years. I prepared the PPM and the other Reg D docs I need to solicit. I read your instruction about sending emails to prospect investors so they can login using their email, so I have verification that they had access to the disclosures I need to have them review."

Read that last clause again, because it's the entire thesis of this post stated by a practitioner: email login as verification that each investor had access to the disclosures they're required to review. What Robert configured, concretely, is the four-layer record this post is about — each prospect authenticates with their own email (identity), signs the NDA before anything opens (sequence), every view of the PPM and exhibits is logged per version with timestamps (content), and the subscription documents are e-signed in the same room (commitment).

The generalizable point for every solo sponsor and small shop: the compliance-grade version of this workflow is not the enterprise version. You don't need staff to run it — you need the gate configured once and a per-investor link for each prospect. The fund-administration layer (NAV, distribution processing, K-1s at scale) is a genuinely different job you can add later if you end up operating a fund; it is not the price of admission for proving disclosure on a deal-by-deal Reg D raise.

How is a private placement data room different from a fund or investor data room?

Because the categories rhyme, it's worth being precise about what this room is not, so you link to the right guide instead of duplicating effort.

- Generic investor data room. A founder-facing room built around the cap table and the six standard fundraising folders, so a VC can reach a yes/no. The lens is engagement and presentation. That's the data room for investors post, and Peony's fundraising solution covers the engagement-tracking side.

- Fund data room. Built around a blind-pool vehicle, an LPA, an ILPA-style DDQ, and the GP-LP relationship. The hero documents are fund terms and track record. See the real estate fund and VC fund versions. A fund raise is a private placement, but those posts own the fund-vehicle workflow.

- Independent sponsor room. Deal-by-deal Reg D raises from capital partners under a ticking exclusivity clock. The independent sponsor guide owns that lane.

A private placement data room is built around a securities offering by an operating company or sponsor entity — and its lens is exemption compliance and antifraud evidence. The hero documents are the PPM, the subscription agreement, and the per-investor disclosure-and-verification record, not a DDQ or a cap table. If your raise is into a fund, follow the fund posts; if you're selling your company's own securities under Reg D, you're in the right place.

How do you share the model and PPM exhibits live without losing control?

Private placements increasingly hinge on a financial model — the use-of-proceeds build, the return scenarios, the cap structure waterfall. Investors want to interrogate it, and that's exactly where most data rooms quietly fail an issuer: legacy VDRs flatten every upload to a dead PDF, so the model arrives lifeless. The issuer ends up emailing the real .xlsx "just so they can play with it" — which is precisely the uncontrolled disclosure the room was supposed to prevent.

Peony handles this differently, and it's the clearest functional advantage for a private placement:

- Excel renders as a live, interactive spreadsheet in the browser — the formulas compute, so an investor can change an assumption and watch the returns move, a Google-Sheets experience inside the room, with no download and no emailed file.

- HTML exhibits render live with the JavaScript executing — if you've built a bespoke model or interactive PPM exhibit as an

.html/.htmartifact, Peony runs it in place (the same capability that runs interactive AI-generated artifacts live).

Both stay wrapped in the full control layer — dynamic watermarks (viewer name, email, timestamp), screenshot protection, per-viewer permissions, instant revoke, and the audit trail — on the Data Room plan ($52/admin/month). Two concrete wins for an offering:

- One version of the truth. There's exactly one current model and PPM in the room, so no investor signs against a stale exhibit — which is also part of your antifraud record.

- Show outputs, hide the sensitive tabs. Publish a version with proprietary assumption sheets excluded; investors see scenarios, not your full internal logic.

This is the difference between a room that supports your raise and a convert-to-PDF tool that forces you back into your inbox.

What does a private placement data room cost in 2026?

For an issuer, the pricing model matters more than the sticker price, because a private placement issuer often runs a sequence of raises and then needs a standing room for ongoing investor reporting:

- Peony Business — $30/admin/month. The core private-placement workflow: NDA gating, subscription-agreement e-signatures, personalized links, email authentication, link expiry and revocation, detailed analytics, and the per-investor audit trail. The right tier when the room's sensitivity is moderate.

- Peony Data Room — $52/admin/month (Most Popular). Adds dynamic watermarks, screenshot protection (Screenshield for mobile capture), granular per-file permissions, AI auto-indexing, and unlimited rooms — the tier most issuers and sponsors choose when the room holds sensitive financials or they run multiple offerings a year.

- Legacy per-deal VDRs (Datasite, Intralinks) are priced for a single transaction window and routinely run five figures per deal. Workable for a one-off mega-deal; disproportionate for a Reg D raise, and punishing if you do more than one.

The structural point: a private placement is a poor fit for per-deal pricing and a great fit for flat-rate, because the room spans diligence, verification intake, and years of reporting. See the flat-rate data room breakdown for the full math, and the setup guide for the build steps.

The bottom line: the room is your evidence, not your brochure

A private placement data room isn't a nicer way to send a PDF. In a Reg D offering it's the evidence layer: the thing that proves what each investor saw, when, and what they signed — across investor diligence, 506(c) verification intake, and years of ongoing reporting.

Get three things right and the room does its job: scope access so a 506(b) link never reads as general solicitation; collect and log the 506(c) verification evidence without ever claiming the room verifies accreditation itself; and keep one provable version of the PPM and model in the room behind watermarks and a per-investor audit trail. That's what turns disclosure into a defensible record — because the PPM discloses, and the data room proves.

See Peony for fundraising → · Start a data room →

Related resources

- Private Placement Memorandum: What Goes In a PPM — the disclosure document itself, section by section

- Reg D Data Room: 506(b) vs 506(c) — the exemption-choice deep dive and verification mechanics

- How to Set Up a Private Placement Data Room — the step-by-step build and document checklist

- Data Room for Investors — the generic founder-facing investor room

- Real Estate Fund Data Room (The 3-Room Model) — the fund-vehicle version, if you're raising into a fund

- VC Fund Data Room Checklist — the venture/PE-fund parallel

- Independent Sponsor Guide — deal-by-deal Reg D raises from capital partners

- SPV Data Room for Syndicate Leads — the single-deal co-investment version: circulating someone else's company to your own backers

- Real Estate Syndication Data Room — the single-asset real-estate raise (PPM + waterfall + sponsor track record)

- Peony Flat-Rate Data Room

- Peony for Fundraising

- Peony Pricing

- Juniper Square Review (2026) — evaluating the investor-platform layer above the Reg D evidence layer this hub covers.