11 Best M&A Advisors in Indianapolis for $5M-$300M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

11 Best M&A Advisors in Indianapolis for $5M-$300M Deals (2026)

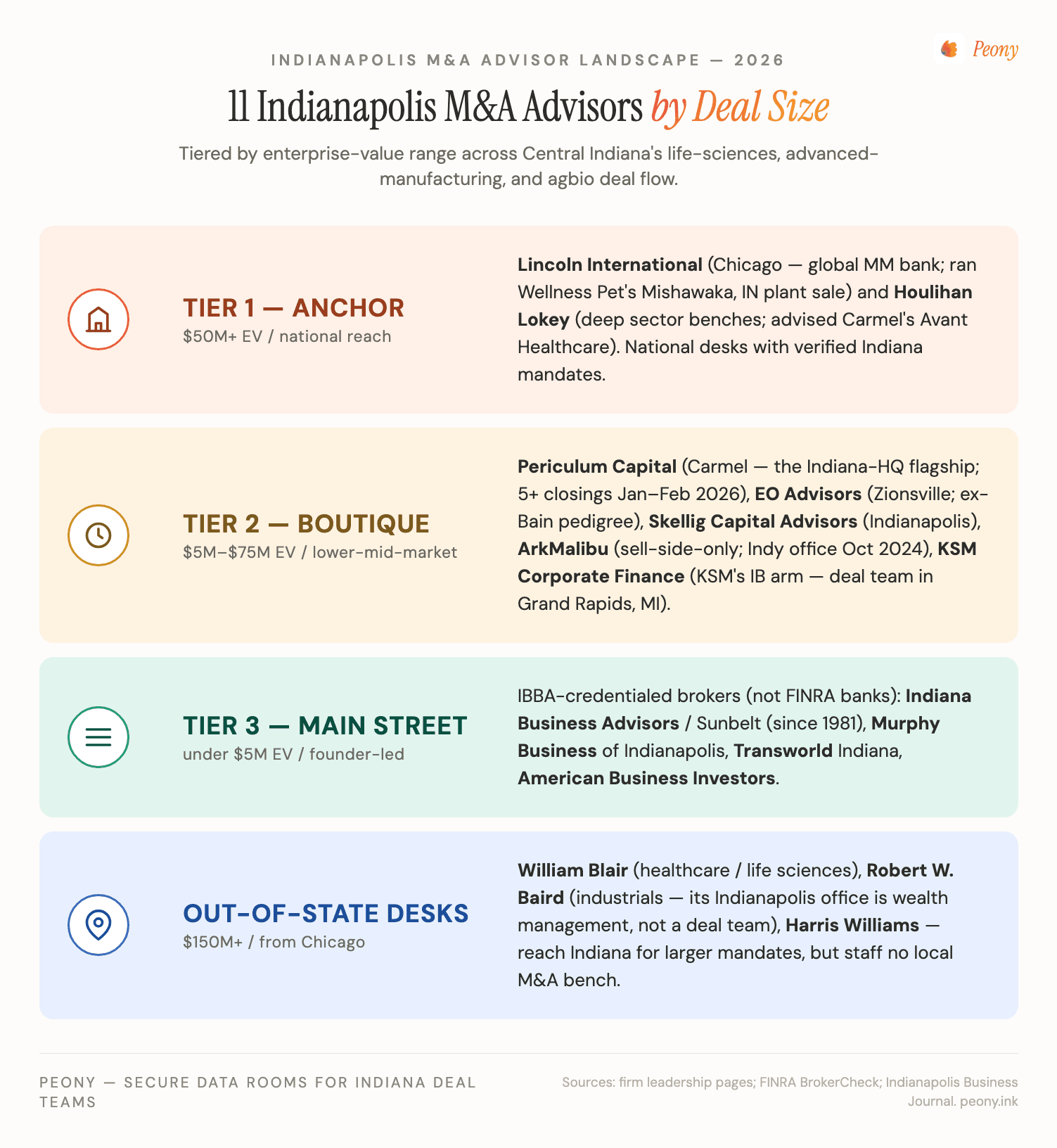

Quick answer: After sitting on the document side of enough Indiana sell-side processes, here is the 11-firm Indianapolis shortlist for 2026. What makes Indianapolis different from most secondary metros is that it has a real in-state middle-market investment bank — Periculum Capital in Carmel (FINRA CRD #43362), the clear flagship — instead of relying entirely on Chicago and New York desks reaching in. Backing it: boutiques EO Advisors (Zionsville / Indianapolis metro), Skellig Capital Advisors, ArkMalibu's new Indianapolis sell-side office, and KSM Corporate Finance (the Katz, Sapper & Miller IB arm). For $150M+ and specialized sectors, national banks with verified Indiana mandates reach in — Lincoln International and Houlihan Lokey. And below ~$5M, Main-Street brokers (Indiana Business Advisors / Sunbelt Indiana, Murphy Business, Transworld, American Business Investors) run the deal. The signature frame below — the Indianapolis Strategic-Acquirer Density Map — explains how an unusually dense pool of in-state buyers (Eli Lilly closed ~$6.1B of acquisitions in 2023 alone (BioSpace, Feb 2024); Allison Transmission closed its ~$2.7B Dana Off-Highway deal Jan 1-2, 2026 (PR Newswire, Jan 2026); Zimmer Biomet of Warsaw closed Paragon 28 for ~$1.1B in April 2025 (PR Newswire, Apr 2025)) decides which advisor wins which deal.

Last updated: June 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. I have sat on the document side of hundreds of deals — founder-led sales, PE recapitalizations, strategic carve-outs, and venture-stage exits — and Indianapolis keeps surprising people who assume a non-coastal metro is just a pass-through for Chicago bankers. It is not. At Peony we now serve more than 6,800 customers, and Central Indiana sits right in the heart of the sub-$300M enterprise-value band that makes up the bulk of our 283-deal platform benchmark. This is one city in our M&A advisor series, and structurally it is one of the more distinctive entries.

Most "best M&A advisors" lists are interchangeable directory pages. This one is not, because Indianapolis has two things almost no other secondary metro can claim at once. First, a genuine in-state middle-market investment bank — Periculum Capital, headquartered in Carmel — that runs real competitive sell-side processes rather than just custodying wealth. Most metros Indianapolis's size do not have that; they have wealth-management branches of national banks and a handful of Main-Street brokers, and every meaningful deal leaves town. Second, an in-state pool of large, acquisitive public strategics — Eli Lilly, Elevance Health, Cummins, Allison Transmission, Zimmer Biomet, Corteva, Steel Dynamics, Simon Property Group, Republic Airways — that closed or announced billions of dollars of M&A in 2023-2026. When an Indiana owner sells, several of the most logical strategic buyers are headquartered within an hour's drive, and that changes how you pick an advisor.

This post is the working playbook I would hand to a Central Indiana manufacturing owner weighing retirement, a Warsaw orthopedics supplier fielding inbound interest, a Carmel medtech or pharma-services founder, an agbio operator in the Corteva orbit, or a private-equity partner sourcing Indiana carve-outs. The five frames — Strategic-Acquirer Density, the Warsaw / Lilly Buyer Orbit, the Real-In-State-IB advantage, the Small-Market Confidentiality problem, and the Reshoring Exit-Timing Window — come from cross-referencing the verified 2023-2026 deal record against the region's structural specifics. I will also be honest about the limit: above roughly $150M, Indianapolis has a thin bench, and the largest processes co-advise with national firms. I will say so where it is true.

Who are the best M&A advisors in Indianapolis right now for $5M-$300M deals?

The Indianapolis-metro shortlist for 2026, sorted by deal-size band and tier:

| Firm | Founded / Indiana presence | HQ / Indianapolis-metro office | Sweet spot | Specialty |

|---|---|---|---|---|

| Lincoln International | 1996 (reaches Indiana from Chicago) | Chicago HQ | $150M-$1B+ EV | Cross-border industrials, consumer carve-outs |

| Houlihan Lokey | 1972 (sector-team-led, no Indy IB office) | Los Angeles HQ / national | $100M-$1B+ EV | Healthcare/pharma-commercialization, industrials, restructuring |

| Periculum Capital | 1998 (Carmel, IN — in-state flagship) | Carmel, IN | $5M-$150M EV | LMM/MM generalist — food & ag, consumer, distribution, healthcare, industrial |

| EO Advisors | 2021 | Zionsville / Indianapolis metro | $5M-$75M EV | LMM sell-side + capital formation |

| Skellig Capital Advisors | 2019 | Indianapolis | $25M-$1B+ EV (legacy pedigree) | Sell-side, recap, capital raise for Midwest companies |

| ArkMalibu (Indianapolis office) | 1990 HQ; Indy office Oct 3, 2024 | Cincinnati HQ / Indianapolis | $50M-$300M EV | Sell-side ONLY, upper-LMM |

| KSM Corporate Finance | IB arm launched Jan 2026 | Indianapolis-parented (team in Grand Rapids, MI) | $10M-$150M EV | MM sell-side, buy-side, capital advisory, ESOP |

| Indiana Business Advisors / Sunbelt Indiana | Since 1981 | Indianapolis | Under $5M EV | Main-Street + lower-LMM business brokerage |

| Murphy Business of Indianapolis | (local franchise) | Indianapolis | Under $5M EV | Small-business sale brokerage |

| Transworld Business Advisors Indiana | (Carmel) | Carmel, IN | Under $5M EV | Sub-$5M business sales |

| American Business Investors | (local) | Indianapolis | Under $5M EV | Sub-$5M business sales |

A few notes the table cannot carry. Periculum Capital is the headline — the single clearest middle-market investment bank headquartered in Indiana, and the reason an Indianapolis seller does not automatically have to ship the mandate to Chicago. Lincoln International and Houlihan Lokey are national banks that reach Indiana for larger and more specialized mandates, and both have a verified, named Indiana deal (more below). A critical honesty point on the "Indianapolis offices" of Baird, Stifel, and Raymond James: those are private wealth-management / brokerage branches, not corporate M&A deal teams — their Indiana sell-side work, when it happens, runs from Chicago and other institutional hubs. And the Tier 3 firms are business brokers, not FINRA-registered investment banks — the right call for genuinely Main-Street businesses under ~$5M, covered in the hire-by-size section below.

Is there an actual Indianapolis-headquartered investment bank, or do I have to hire a Chicago firm?

Yes — Indianapolis has a real in-state middle-market investment bank in Periculum Capital, which is exactly what most secondary metros lack, so you do not automatically have to hire a Chicago firm. This is the single most important structural fact about the Indianapolis market, and it is easy to miss because the city is also dotted with national-bank brand names that are actually wealth-management offices.

Periculum Capital Company / Periculum Capital Markets, LLC is headquartered in Carmel, IN, founded in 1998, and registered with FINRA (CRD #43362; Member FINRA/SIPC) — you can verify it on BrokerCheck. The firm reports more than 400 transactions and over $4B in transaction value across its history (a firm-reported figure, not independently audited), running principal-led sell-side processes across food & ag, consumer, distribution, healthcare, industrial, manufacturing, and energy. Its founders, Broecker and Shortle, sit on the firm's advisory board; the active managing directors lead the deals. What makes Periculum credible is not the brochure — it is the recent, named, in-band closings, which I detail in the deal-cadence section below.

The contrast that matters: when you see "Baird," "Stifel," or "Raymond James" with an Indianapolis address, that is almost always a private wealth-management branch, not a corporate M&A deal team. Those firms are real investment banks — but their sell-side mandates run from Chicago and institutional hubs, not from the local wealth office. Similarly, J.P. Morgan's Indianapolis presence is a commercial / midmarket relationship-banking team, and the J.P. Morgan MD most often associated with Indiana deals is New York-based, not a local sell-side banker. The practical implication: for a sub-$150M Indiana company, you have a genuine local choice in Periculum (plus the boutiques below) that you would not have in most metros this size — and you only need to reach for a Chicago or coastal firm when the deal is large, cross-border, or in a sector that needs a specialist desk. That selection logic carries through the rest of this guide, and the upstream version of the decision lives in our M&A advisor vs business broker vs investment bank guide.

Why does Indianapolis's strategic-acquirer density change your buyer pool?

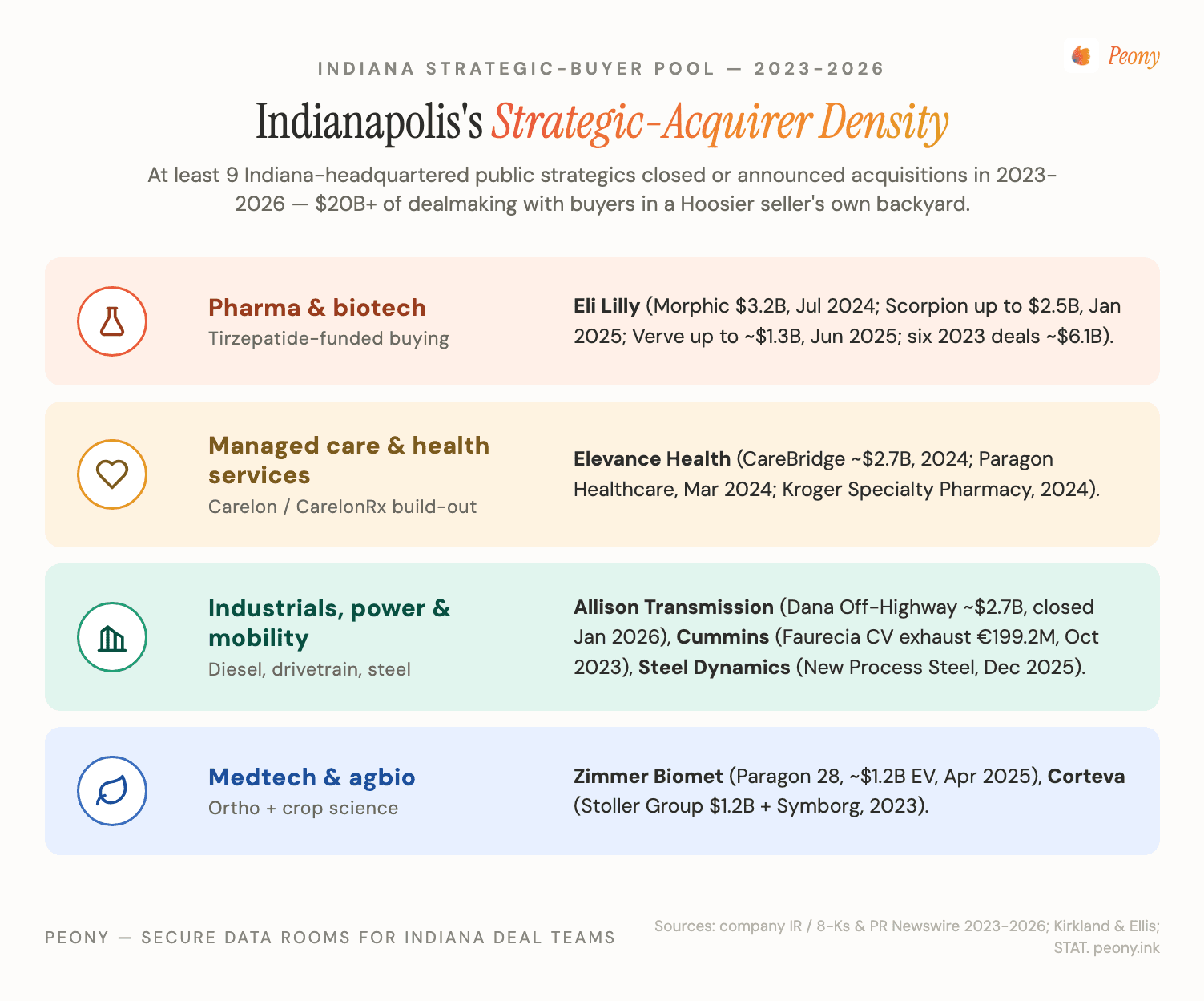

Indianapolis's signature M&A advantage is that an unusually dense set of large-cap strategic buyers is headquartered in-state for a non-coastal metro — so an Indiana sell-side process can run a serious strategic-buyer track without the seller ever leaving the region. At least nine Indiana-headquartered public companies closed or announced material M&A in 2023-2026. These companies are buyers, never advisors — but their deal flow is what gives the local advisory community (and a data room built for M&A processes) so much to work with.

The spine of the density map is Eli Lilly, whose tirzepatide-funded balance sheet turned it into one of the most active acquirers in pharma:

- 2023: six acquisitions worth about $6.1B (Mablink, POINT Biopharma, Versanis, Emergence, Sigilon, DICE) (BioSpace, Feb 2024). That includes POINT Biopharma (radioligand, ~$1.4B at $12.50/share, announced October 3, 2023), DICE Therapeutics (oral IL-17, ~$2.4B at $48/share, closed August 2023), and Versanis Bio (obesity/bimagrumab, up to ~$1.925B including milestones).

- Morphic Holding (oral α4β7 for IBD) — ~$3.2B at $57/share (a ~79% premium), announced July 8, 2024 (STAT, Jul 2024).

- Scorpion Therapeutics (PI3Kα) — up to $2.5B (~$1B upfront + up to $1.5B in milestones), announced January 13, 2025 (Lilly IR, Jan 2025).

- Verve Therapeutics (gene editing / PCSK9) — up to ~$1.3B (~$1B upfront / $10.50 per share + a $300M CVR, or $3.00 per share), announced June 17, 2025 (PR Newswire, Jun 2025).

Around that spine sit eight more in-state acquirers:

- Elevance Health (Indianapolis; managed care, led by President & CEO Gail K. Boudreaux) built out Carelon and CarelonRx with CareBridge (reported ~$2.7B, 2024), Paragon Healthcare (infusion; closed March 11, 2024 — Axios reported "over $1B," though terms were undisclosed), and Kroger Specialty Pharmacy (agreement March 2024, undisclosed).

- Allison Transmission (Indianapolis) closed its largest-ever deal, Dana's Off-Highway Drive & Motion Systems business for ~$2.7B, on January 1-2, 2026, creating a ~$5.5B-revenue industrial leader (PR Newswire, Jan 2026).

- Zimmer Biomet (Warsaw, IN) bought foot-and-ankle specialist Paragon 28 for ~$1.1B equity / ~$1.2B EV ($13/share + up to a $1 CVR), completed April 21, 2025 (PR Newswire, Apr 2025).

- Corteva Agriscience (Indianapolis global HQ) bought crop-biologicals maker Stoller Group for $1.2B (~12x EBITDA), closed early 2023 alongside Symborg (undisclosed). Corteva announced a planned split into "New Corteva" (crop protection) and a seed "SpinCo" on October 1, 2025.

- Cummins (Columbus, IN), Steel Dynamics (Fort Wayne — bought the remaining 55% of New Process Steel, completed December 1, 2025), Simon Property Group (Indianapolis REIT — one of several JV shareholders in the Catalyst Brands / JCPenney + SPARC venture launched January 8, 2025, not a sole buyer), and Republic Airways (Carmel — completed its all-stock merger with Mesa Air Group on November 25, 2025, now Nasdaq: RJET) round out the list.

For an advisor, this density is the whole game. The right Indiana banker does not just own a generic buyers list — they know which of these corporate-development teams is actively buying in your category this quarter and can get your CIM in front of the right VP. The screening test for any advisor pitching an Indiana seller: ask them to name, off the top of their head, the in-state strategics most likely to bid on your business and the last deal each closed. A genuinely Indiana-fluent advisor will not hesitate. One honest caveat, though: a dense in-state buyer pool is not a promise that your company is on Lilly's or Allison's shopping list — these are large-cap acquirers with specific theses, and a boutique's job is to find the buyer who actually wants your asset, not to dangle a logo.

How does the Warsaw orthopedics cluster and the Lilly buyer orbit reshape advisor selection for life-sciences sellers?

If your business touches orthopedics, medtech, pharma services, or the broader life-sciences ecosystem, hire a banker who can speak the regulatory and IP language and plug you into the right specialist-buyer network — a Main-Street generalist will leave multiple on the table here. Life sciences is Indiana's dominant cluster: the sector crossed $102B in total economic contribution for the first time, with about 70,000 people employed across 3,312 establishments at a ~$177,000 average wage, and Indiana ranks #1 in the nation for life-sciences/pharma exports (Inside INdiana Business, Mar 2026).

The center of gravity is Warsaw, IN — the "Orthopedic Capital of the World" — home to one-third of the world's orthopedic-device companies and two-thirds of the world's hip and knee manufacturers, with Zimmer Biomet headquartered there alongside DePuy/J&J and Medtronic spine operations (Becker's, Oct 2022). A Warsaw ortho supplier or a Carmel medical-communications firm is rarely a Main-Street process — the logical buyers are strategics and healthcare-focused PE platforms that a sector banker already knows. That is exactly the kind of deal national sector benches are built for: Houlihan Lokey advised Carmel-based Avant Healthcare on its sale to Real Chemistry (closed February 1, 2024), and Houlihan Lokey's pharma-commercialization desk and William Blair's healthcare/life-sciences practice (reaching Indiana from Chicago) are the strongest options for a regulated, IP-heavy, or larger medtech seller.

Where a strong Indianapolis generalist still fits: a smaller component supplier or services business in the $5M-$30M band, where a relationship-rich boutique like Periculum can run a tight process and pull the specialist buyers in by name. The advisor-fit test for a life-sciences seller: can the banker name the active orthopedic, spine, or pharma-services acquirers in your specific niche, and have they closed a comparable deal in the last 24 months? And because medtech diligence is QA- and IP-heavy, the data room work matters more here than in a plain industrial deal — dynamic per-viewer watermarking and screenshot protection are the controls that keep design files and regulatory submissions from walking out the door, and a structured diligence workflow keeps the buyer's questions from sprawling.

Who should advise an Indiana advanced-manufacturing or EV-supply-chain business?

For an Indiana advanced-manufacturing or EV-supply-chain business, favor a boutique with a real industrials bench and the capital-intensity fluency to handle supplier-network and facilities diligence — Periculum's industrial/manufacturing lane locally, or Baird's industrials desk reaching in from Chicago for larger mandates. Advanced manufacturing and logistics employ 840,000+ Indiana workers (about 25% of state jobs and 37% of output), and the sector drew a record $29B of investment in 2024 (CICP / Conexus, 2025).

The EV-battery build-out is the headline. StarPlus Energy (a Stellantis–Samsung SDI JV in Kokomo) finalized a $7.54B Department of Energy loan in December 2024 for two gigafactories (~67 GWh combined) (DOE LPO, 2024). But here is the honest both-sides signal: the GM–Samsung SDI battery plant in New Carlisle (~$3.5B, ~1,700 jobs) had its production timeline pushed to 2027 and its construction paused in late 2025 to align with softer EV demand (Detroit News, Oct 2025). The reshoring window is hot, but it is not uniform — and a manufacturing owner timing an exit should read the cycle, not just the press releases.

The advisor-selection implication: capital-intensive, supplier-network deals reward a banker who understands customer-concentration risk, capacity utilization, and the strategic-buyer logic of the in-state industrials (Allison Transmission, Cummins and its supplier base, Steel Dynamics). For a $5M-$75M supplier, that is a Periculum-style boutique; above ~$150M, you co-advise with a national industrials desk. And whatever the size, environmental diligence (Phase I/II site assessments, permits) is a recurring gate in a manufacturing footprint — the kind of workstream a clean sell-side data room gets ahead of, with a structured Q&A workflow to keep the buyer's diligence questions organized instead of scattered across email.

What's the difference between a business broker, a boutique bank, and a full investment bank in Indianapolis — and which do I need?

The difference is mostly deal size and licensing, and Indianapolis has a clean ladder across all three. A business broker handles Main-Street sales (typically under ~$5M, often the owner's whole net worth) and is usually credentialed through the IBBA or M&A Source rather than FINRA — in Indianapolis that is Indiana Business Advisors / Sunbelt Indiana, Murphy Business, Transworld, and American Business Investors. A boutique investment bank runs a competitive process for $5M-$75M businesses and, for a securities-based sale, generally must be or operate through a FINRA-registered broker-dealer — Periculum, EO Advisors, and Skellig are the local examples. A full investment bank (Lincoln International, Houlihan Lokey, William Blair, Baird reaching in) adds capital-markets capability, league-table credibility, and the bandwidth to run a $100M-$1B+ auction.

The licensing line is genuinely consequential, and Indiana has its own wrinkle. The federal M&A Broker exemption (Securities Exchange Act §15(b)(13), added by the Consolidated Appropriations Act, 2023, effective March 29, 2023) lets an unregistered intermediary handle a privately held company's stock sale only when the target had, in the prior fiscal year, under $25M EBITDA or under $250M in gross revenues (Jones Day, Jan 2023). But — and this is the part most sellers miss — the federal exemption does not preempt state law. Indiana responded with Administrative Order AO 25-001 (dated April 3, 2025), a conditional no-enforcement posture under which the Indiana Securities Division will not pursue an unregistered M&A broker-dealer if a set of conditions is met, including avoiding any of nine "Excluded Activities" (Indiana Securities Division). It is a conditional order, not a blanket statutory exemption — so verify your advisor's registration status rather than assuming the federal exemption cleared them in Indiana.

On credentials: a Main-Street broker should hold the IBBA's CBI (membership + education + three completed lead-seller transactions + exam) or the M&A Source's M&AMI; Indiana Business Advisors' Brian Knoderer holds the CM&AA plus Series 7 and 63. A securities-based middle-market sale should run through a FINRA broker-dealer you can verify on BrokerCheck. The full breakdown is in our selection hub.

Which Indianapolis advisor has actually closed deals recently?

Among the Indianapolis-metro firms, Periculum Capital has the clearest recent, verifiable, in-band track record — a wave of sell-side closings in January and February 2026 — while the verified national-bank Indiana mandates belong to Lincoln International and Houlihan Lokey. This is the question that separates a real advisor from a directory listing, and it is worth answering with names and dates.

Periculum Capital's January-February 2026 closings (all from the firm's own news releases via periculumcapital.com):

- Aerosmith Fastening Systems (a HKN International business) → Spotnails, exclusive financial advisor, February 24, 2026.

- Good Earth Lighting → Feit Electric Company, sell-side, February 10, 2026.

- Dealers Wholesale → Lacy Diversified Industries, exclusive financial advisor, January 22, 2026.

- BOC Oil → Cadence Petroleum Group, exclusive financial adviser, January 13, 2026.

- Cornerstone Autism Center → LEARN Behavioral, sell-side, January 5, 2026.

Further back, Periculum advised on the Hope Plumbing recap by Redwood Services (February 2025), Hoosier Penn Oil → Cadence Petroleum Group (October 2023), and Mi-Tech Tungsten Metals → Global Tungsten & Powders (November 2022). One correction worth flagging, because it circulates: Periculum advised the 2018 Pretzels, Inc. → Peak Rock sale, but the later Pretzels → Hershey transaction (December 2021) was advised by Evercore, not Periculum — so do not credit that one to a local firm.

The verified national-bank Indiana mandates:

- Lincoln International (Chicago) advised Wellness Pet Company on the sale of its Mishawaka, IN production plant to Belgium's United Petfood — United Petfood's first U.S. plant — announced June 6, 2024, terms undisclosed (Lincoln International).

- Houlihan Lokey was exclusive sell-side advisor to Avant Healthcare (Carmel, IN medical communications) on its sale to Real Chemistry, closed February 1, 2024, terms undisclosed (Houlihan Lokey).

For the newer entrants — ArkMalibu's Indianapolis office (opened October 3, 2024), KSM Corporate Finance (launched January 2026), Skellig (whose public transaction page reads as a template), and EO Advisors (no independently verifiable named 2024-2026 deal) — judge them on pedigree and team rather than a named local closing, because none has a publicly verified Indiana-attributable deal yet. That is not a knock; it is just the honest state of the record. ArkMalibu is a sell-side-only Cincinnati bank ($50M-$300M) whose Indianapolis office is led by Phil Daniels. KSM Corporate Finance is the IB arm of accounting firm Katz, Sapper & Miller — but note the mandatory caveat: its deal team operates from Grand Rapids, MI (it absorbed Charter Capital Partners' IB team), so it is Indianapolis-parented, not Indianapolis-operated.

Which firms should I NOT mistake for an M&A advisor in Indianapolis?

Several well-known Indiana firms get mistaken for sell-side M&A advisors but are not — they are funds, lenders, wealth managers, or strategic buyers, and hiring them for the wrong job (or listing them as advisors) is a common error. Getting this right is part of vetting the market honestly.

- Centerfield Capital Partners is a mezzanine-debt and equity fund (a financier), and Cardinal Equity Partners is a private-equity buyer — neither is a sell-side advisor.

- Goelzer Investment Management is a registered investment adviser / wealth manager, not a broker-dealer running deals.

- Cambridge Capital Management Corp. is an SBA 504 lender; Pearl Street Venture Funds and Springboard Capital are venture funds; Telamon is a tech/staffing company. None is an M&A advisor.

- The in-state strategic acquirers in the density map above — Eli Lilly, Elevance Health, Cummins, Allison Transmission, Zimmer Biomet, Corteva, Steel Dynamics, Simon Property Group, Republic Airways — are corporate buyers, not advisors or broker-dealers. They appear in this guide as the buyer pool, never as a firm you would hire to represent you.

Two more cautions for anyone scanning lists. Watch for out-of-state firms that get mislabeled as local — and for the Indianapolis "offices" of Baird, Stifel, and Raymond James, which are wealth-management branches rather than M&A deal teams. The reliable filter for any name on a "best Indianapolis M&A advisor" list: is it FINRA-registered (verify on BrokerCheck), does it run sell-side processes (not invest its own capital or manage wealth), and can it name a recent closing in your band? If the answer to all three is not yes, it does not belong on your shortlist.

Is now the reshoring exit-timing window for Indiana businesses?

For owners of Indiana businesses, the 2026 macro backdrop is about as favorable as it gets — record manufacturing investment, an unusually deep in-state strategic-buyer pool, and the Baby-Boomer succession wave are stacking demand at the same time, though the EV-battery slice is cooling. The reshoring and capex signals are concrete:

- Eli Lilly committed to more than double its U.S. manufacturing investment since 2020, exceeding $50 billion (announced February 26, 2025) (Lilly IR, Feb 2025). Its Lebanon, IN LEAP-district commitments have grown to roughly $13.5B since 2022, with a further $4.5B added in May 2026 for a genetic-medicine "Medicine Foundry" (operational ~2027) (WFYI, May 2026). (These are greenfield capex commitments, not M&A — but they signal the kind of corporate confidence that drives buy-side appetite.)

- StarPlus Energy finalized a $7.54B DOE loan for its two Kokomo gigafactories (December 2024) (DOE LPO, 2024).

- Conexus reports a record $29B of advanced-manufacturing investment in Indiana in 2024 (CICP, 2025).

- Allison Transmission closed its ~$2.7B Dana Off-Highway acquisition January 1-2, 2026, creating a ~$5.5B-revenue Indianapolis-HQ industrial leader (PR Newswire, Jan 2026).

- Roche announced an up-to-$550M Indianapolis diagnostics expansion (~650 new jobs by 2030) in May 2025 (MedTech Dive, May 2025).

The honest both-sides note: the GM–Samsung SDI plant in New Carlisle paused construction in late 2025 and slipped production to 2027 as EV demand softened — proof the window is hot but not uniform. On the seller side, the demographic wave is just as real: Baby Boomers hold a majority of U.S. private wealth and are projected to be largely out of the workforce by the mid-2030s, a durable owner-succession pipeline. And national deal volume is moving — the lower-middle-market ($10M-$100M EV) band was up sharply year-over-year entering 2026 (Capstone Partners, Q1 2026). The exit-timing read: Indiana industrial and life-sciences owners who have been waiting for "a better year" are arguably in one now, and the advisor conversation is worth starting 6-9 months before you want to be in market.

What's a reasonable success fee for a $25M Indiana sell-side, and how do fees vary?

Indiana M&A advisors price the way the broader U.S. lower-middle-market does: a monthly retainer or fixed work fee plus a success fee at close, with the success rate declining as deal size grows. For a $25M enterprise-value deal, expect a blended success fee in the 3-3.5% range.

The most common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M — which on a $25M deal computes to about $700K, roughly 2.8%. Add the slice of retainer that is not credited back plus any minimum-fee floor and the effective blended rate usually lands near 3-3.5%. That tracks national data: a $25M deal sits in the $10M-$30M band, where success fees run about 2-5% (Eton, 2026), so ~3-5% is the practical range to quote. For reference, the classic Lehman scale is 5-4-3-2-1 and the Main-Street default is the Double Lehman (10-8-6-4-2) — and on a small ~$2M deal the Double Lehman computes to $180,000 (9.0% blended), which is why brokers, not banks, handle that band.

The variation by advisor type in Indianapolis:

- Boutiques (Periculum, EO Advisors, Skellig) typically run Double Lehman or a negotiated flat rate at $25M-$75M, with a retainer in the $15,000-$30,000 per month range for the $10M-$30M band (Eton, 2026).

- The national banks (Lincoln International, Houlihan Lokey reaching in) carry higher retainer floors given their cost structures and reach for standard Lehman with capital-markets add-ons on larger deals.

- Main-Street brokers (Indiana Business Advisors, Murphy, Transworld, American Business Investors) on sub-$5M businesses often charge a flat percentage or a Double Lehman where the minimum fee dominates.

Across all of them, retainers (work fees) are frequently credited against the success fee at closing — but only if the engagement letter says so in writing, so negotiate the credit explicitly. A minimum-fee floor (commonly around $150,000) appears in most letters; on a $25M deal the percentage fee normally exceeds it, so the floor rarely binds at this size. What matters more than the headline percentage is the base it applies to (total enterprise value including assumed debt and earnouts, or just cash at close) and the tail period — banks ask for 18-24 months; cap it at 12. The full math, and the engagement-letter clauses that quietly inflate the bill, is in our M&A advisor fees hub.

What does the Indianapolis M&A deal cadence look like over the past 12 months?

A representative slate of verified 2023-2026 Indiana transactions — both the local-advisor sell-side closings and the big in-state strategic deals that define the buyer pool:

| Target (HQ) | Acquirer | Date | Approx value | Sector | Advisor (if known) |

|---|---|---|---|---|---|

| Aerosmith Fastening Systems | Spotnails | Feb 24, 2026 | undisclosed | Industrial fastening | Periculum Capital (sell-side) |

| Good Earth Lighting | Feit Electric Company | Feb 10, 2026 | undisclosed | Lighting / consumer | Periculum Capital (sell-side) |

| Dealers Wholesale | Lacy Diversified Industries | Jan 22, 2026 | undisclosed | Distribution | Periculum Capital (sell-side) |

| BOC Oil | Cadence Petroleum Group | Jan 13, 2026 | undisclosed | Fuel / lubricant distribution | Periculum Capital (sell-side) |

| Cornerstone Autism Center | LEARN Behavioral | Jan 5, 2026 | undisclosed | Healthcare services | Periculum Capital (sell-side) |

| Dana Off-Highway Drive & Motion | Allison Transmission (Indianapolis) | Jan 1-2, 2026 | ~$2.7B | Off-highway drivetrain | — |

| New Process Steel (remaining 55%) | Steel Dynamics (Fort Wayne) | Dec 1, 2025 | undisclosed | Steel / metals | — |

| Mesa Air Group | Republic Airways (Carmel) | Nov 25, 2025 | all-stock merger | Regional airlines | — |

| Verve Therapeutics | Eli Lilly (Indianapolis) | Jun 2025 (announced) | up to ~$1.3B | Gene editing / cardiometabolic | — |

| Paragon 28 | Zimmer Biomet (Warsaw) | Apr 21, 2025 | ~$1.1B equity | Orthopedics (foot & ankle) | — |

| Scorpion Therapeutics | Eli Lilly (Indianapolis) | Jan 2025 (announced) | up to $2.5B | Oncology | — |

| Wellness Pet (Mishawaka, IN plant) | United Petfood (Belgium) | Jun 6, 2024 (announced) | undisclosed | Pet food manufacturing | Lincoln International (sell-side) |

| Avant Healthcare (Carmel, IN) | Real Chemistry | Feb 1, 2024 (closed) | undisclosed | Medical communications | Houlihan Lokey (sell-side) |

| Morphic Holding | Eli Lilly (Indianapolis) | Jul 8, 2024 (announced) | ~$3.2B | Biopharma (IBD) | — |

The pattern worth internalizing: the local boutiques — Periculum above all — carry the verified sell-side mandates in the sub-$150M lower-middle-market range, while the eye-catching billion-dollar headlines are mostly in-state strategics buying. That is exactly why the Strategic-Acquirer Density frame matters so much for how you choose an advisor: the deal flow that feeds the Indianapolis advisory community is downstream of those large-cap buyers, and a well-connected local banker is your line into them.

Which Indianapolis advisor should I hire for a sub-$5M sell-side? What about a $25M-$150M one?

The right advisor scales with deal size, and Indianapolis has a clean ladder from Main-Street brokers up to the in-state investment bank and the national desks.

Under ~$5M (Main-Street): Use an IBBA- or M&A Source-credentialed business broker, not an investment bank — at this size a FINRA bank's minimum-fee floor (around $150,000) eats too much of the proceeds. In Indianapolis the options include Indiana Business Advisors / Sunbelt Indiana (the state's largest and most experienced brokerage, operating since 1981, led by Brian Knoderer, CM&AA), Murphy Business of Indianapolis (Tom Feick, owner/MD, IBBA member), Transworld Business Advisors Indiana (Carmel; Jess Lawhead, CBI), and American Business Investors (Thomas Poyser, CBI). These are business brokers, not FINRA-registered investment banks — the right fit for a genuinely Main-Street sale, where you should expect a flat percentage or a Double Lehman in which the minimum dominates.

$5M-$25M EV (lower middle market): This is the boutique sweet spot. Periculum Capital, EO Advisors, and Skellig Capital Advisors all run deals in this band with senior bankers personally on buyer calls. Periculum is the deepest generalist with the clearest recent track record; EO Advisors brings ex-Bain / HBS Baker Scholar pedigree; Skellig reaches up-market on legacy Indianapolis IB experience. Match by sector and by whether the firm can name buyers in your category.

$25M-$150M EV (core middle market): Here the boutiques compete with the newer specialist entrants and the national desks. Periculum remains the anchor in-state option; ArkMalibu's Indianapolis sell-side office ($50M-$300M) and KSM Corporate Finance (Indianapolis-parented, team in Grand Rapids) add capacity. The deciding factor is usually whether your best buyers are in-state strategics (favor a relationship-rich local boutique) or a broad national sponsor pool (start thinking about a national co-advisor).

$150M-$300M+ EV: This is where Indianapolis's bench gets thin, and the honest answer is that you will likely bring in a national bank — Lincoln International, Houlihan Lokey, William Blair, or Baird reaching in from Chicago and beyond — often co-advising with a local firm that holds the in-state relationships. Above ~$300M, expect the national banks to lead outright.

Honest comparison: which Indianapolis advisors fit which lane?

| Sub-vertical | $5M-$25M EV | $25M-$75M EV | $75M-$150M EV | $150M+ EV |

|---|---|---|---|---|

| Industrial / advanced manufacturing | Periculum + EO Advisors | Periculum + ArkMalibu + KSM | Periculum + ArkMalibu | Lincoln + Houlihan Lokey + Baird |

| Life sciences / medtech (Warsaw orbit) | Periculum (small suppliers) | Houlihan Lokey + William Blair | Houlihan Lokey | Houlihan Lokey + national HC banks |

| Agbio / food & ag | Periculum | Periculum + KSM | Periculum + national | National ag/food IBs |

| Distribution / logistics | Periculum + EO Advisors | Periculum + ArkMalibu | ArkMalibu + national | Lincoln + national |

| Business services / consumer | Periculum + EO Advisors + Skellig | Skellig + ArkMalibu | ArkMalibu + national | National generalists |

| Healthcare services | Periculum | Periculum + Houlihan Lokey | Houlihan Lokey | National healthcare IBs |

| Main-Street (under $5M) | Indiana Business Advisors / Murphy / Transworld / American Business Investors | — | — | — |

The honest limits to flag:

- Above ~$150M EV — Indianapolis has a genuinely thin local bench, and the largest processes co-advise with or hand off to national banks. This is the city's real structural weakness relative to a Chicago, and a seller in this band should plan for it rather than assume a local boutique can run a $250M auction solo.

- Above $500M EV — bulge-bracket and large-national capabilities matter, and Datasite or Intralinks become the dominant data-room choices given pre-existing relationships with QoE providers, law firms, and R&W underwriters. We built Peony for the sub-$500M band — at flat per-admin pricing — which is where the overwhelming majority of Indiana deals live.

- Cross-border buyer outreach (European or Asian strategics — the Wellness Pet → United Petfood deal is the local example) — pair a local boutique with a national or global platform for buyer-pool extension.

- Highly specialized sectors (orthopedics, gene therapy, defense-exposed) — route to a sector-specialist bank; a local generalist will underperform a desk that lives in the sub-sector.

For the deals that do fit — the $5M-$150M industrial, life-sciences, agbio, distribution, and business-services companies that make up the bulk of Indiana M&A — an Indianapolis-fluent advisor with a documented in-state relationship map is hard to beat, and a clean data room prepared before launch is the cheapest lever you control on both timeline and price.

Bottom line

Indianapolis is one of the few secondary metros that does not have to ship every meaningful deal to Chicago, because it has a real in-state middle-market investment bank — Periculum Capital in Carmel (FINRA CRD #43362) — at the center of its advisory landscape. That landscape is shaped by a rare asset for a non-coastal state: a dense cluster of acquisitive in-state strategics — Eli Lilly, Elevance Health, Cummins, Allison Transmission, Zimmer Biomet, Corteva, Steel Dynamics, Simon Property Group, Republic Airways — that closed or announced billions of dollars of acquisitions in 2023-2026, anchored by Lilly's tirzepatide-funded buying spree. That in-state buyer pool, plus the Warsaw orthopedics cluster and the broader life-sciences ecosystem, is what should drive advisor selection.

For a $5M-$75M lower-middle-market sale, start with Periculum, then EO Advisors and Skellig; for a $50M-$300M sell-side, add ArkMalibu's Indianapolis office and KSM Corporate Finance (Indianapolis-parented, team in Grand Rapids); for a specialized life-sciences or larger ($150M+) process, bring in Houlihan Lokey or Lincoln International (both with verified Indiana mandates) and William Blair or Baird from Chicago; and for a Main-Street deal under ~$5M, an IBBA-credentialed broker (Indiana Business Advisors / Sunbelt Indiana, Murphy, Transworld, American Business Investors) rather than a bank. The honest concession remains: above ~$150M, Indianapolis has a thin bench, and you should plan to co-advise.

The single most important advisor-selection question for an Indiana seller: which firm has the deepest documented relationship with the named in-state strategics and the PE platforms in your sub-sector, and can show recent closings in your band — like Periculum's January-February 2026 wave? In a state where so many logical buyers are headquartered down the road, that relationship map is the whole edge. We serve 6,800+ customers on the data-room side of exactly these deals, and the prep you do before you pick an advisor — clean financials, a staged data room, a tight buyer thesis — compounds everything the advisor does next. I run Peony, a data room company, and the Data Room tier gives you dynamic per-viewer watermarks, page-level analytics, and visitor groups at a flat $52 per admin per month — no per-page or per-GB fees, the predictable line item against a six-figure advisory fee.

Frequently asked questions about Indianapolis M&A advisors

I'm selling my $25M Indiana manufacturing company in 2026 — should I hire a local Indianapolis M&A boutique or a national investment bank?

For a $25M Indiana manufacturing deal, a local Indianapolis boutique is usually the right default — and you only reach for a national bank when your buyer pool is genuinely national or the deal climbs above roughly $150M. Price comes from competitive tension, not from the zip code on the banker's card, so the real question is where your best buyers sit. Indianapolis is one of the few secondary metros with an actual in-state middle-market investment bank — Periculum Capital in Carmel — plus boutiques like EO Advisors and Skellig that run lower-middle-market processes with senior bankers personally on buyer calls. A $25M manufacturing seller is squarely in their band, and a well-connected local banker can often reach the in-state strategics (Allison Transmission, Cummins suppliers, the broader industrial base) and the active PE platforms faster than an out-of-town team that treats your deal as its smallest mandate of the quarter. Where a national bank (Lincoln International, Houlihan Lokey, William Blair, Baird from Chicago) earns its fee is a cross-border buyer pool, a sector that needs a specialist desk, or a deal above ~$150M that needs capital-markets muscle. The honest concession: Indianapolis has a genuinely thin bench above ~$150M, so for a true large-cap process you will likely co-advise with a national firm. On the document side, the prep is the same either way — I run Peony, a data room company used by 6,800+ customers, and a clean, staged data room with page-level analytics is the cheapest lever you control before you even pick the banker.

As the owner of a $30M family-owned Indiana business, who are the best M&A advisors in Indianapolis for a lower-middle-market sale?

For a $30M family-owned Indiana sale, the shortlist starts with Periculum Capital (Carmel — the clearest in-state middle-market investment bank, FINRA CRD #43362), then EO Advisors (Zionsville / Indianapolis metro) and Skellig Capital Advisors (Indianapolis) for the lower-middle-market band, with ArkMalibu's Indianapolis sell-side office and KSM Corporate Finance as additional options. Above ~$150M you bring in national banks reaching Indiana from Chicago and New York — Lincoln International and Houlihan Lokey both have verified Indiana mandates. The screening test for any of them: ask the banker to name the last three deals they closed in your sub-sector and the buyers on the other side. Periculum can rattle off a January-February 2026 wave of closings (Aerosmith Fastening to Spotnails, Good Earth Lighting to Feit Electric, Dealers Wholesale to Lacy Diversified, BOC Oil to Cadence Petroleum, Cornerstone Autism Center to LEARN Behavioral) — that kind of recent, named, in-your-band track record is what separates a real fit from a directory listing. For a family-owned business specifically, also weigh how the firm handles confidentiality in a small market where word travels. We serve 6,800+ customers on the data-room side of exactly these deals, and the firms that read every page of a teaser — you can see it in page-level analytics — are usually the ones genuinely working your file.

Is it worth hiring an M&A advisor to sell my Indiana company, or should I use a business broker or just sell it myself?

It is worth hiring an advisor for almost any Indiana company above roughly $5M of enterprise value — and the choice between an investment bank, a business broker, and selling it yourself is mostly a function of deal size and licensing. Under ~$5M (Main-Street businesses, often the owner's whole net worth), the right call is an IBBA- or M&A Source-credentialed business broker — in Indianapolis that is Indiana Business Advisors / Sunbelt Indiana, Murphy Business, Transworld Business Advisors Indiana, or American Business Investors — because at that size a FINRA bank's minimum-fee floor would eat too much of the proceeds. From ~$5M to ~$75M you want a boutique investment bank (Periculum, EO Advisors, Skellig) running a competitive process; from ~$50M to $300M+ a full investment bank with capital-markets reach. Selling it yourself almost always leaves money on the table: the single biggest driver of price is competitive tension between multiple bidders, and bringing in even one credible competing buyer typically moves price by more than the entire advisory fee. Doing it yourself also exposes you to confidentiality leaks and diligence mistakes a first-time seller cannot anticipate. The one honest exception is a clearly above-market unsolicited offer from a buyer you trust — but even then, a one-page advisor sanity-check on valuation is cheap insurance. Whatever path you choose, prepare clean financials and a staged data room first; I run Peony, a data room company, and that prep compounds everything that comes next.

For a lower-middle-market Indiana sell-side, how does an Indianapolis boutique (like Periculum Capital) compare to a national bank like Houlihan Lokey?

For a lower-middle-market Indiana sell-side, an Indianapolis boutique like Periculum Capital gives you senior-banker attention and in-state relationships at a boutique fee, while a national bank like Houlihan Lokey gives you a deep sector desk and broader buyer reach that matter more as the deal gets larger or more specialized. Periculum is the clearest in-state middle-market investment bank (Carmel, FINRA CRD #43362, founded 1998), and its recent closings cluster in the sub-$150M lower-middle-market band where a managing director is personally on every buyer call — for a $20M-$75M generalist industrial, distribution, food-and-ag, or healthcare-services seller, that focus is hard to beat. Houlihan Lokey is the deep sector-bench bank: it advised Carmel-based Avant Healthcare on its sale to Real Chemistry (closed February 1, 2024), and its pharma-commercialization and industrials desks are exactly what a regulated, IP-heavy, or larger ($150M+) seller wants. The honest read: below ~$150M, a relationship-rich local boutique with a documented buyer map usually wins; above ~$150M, or in a specialized sub-sector with a national/cross-border buyer pool, the sector bench and capital-markets muscle of a Houlihan Lokey (or Lincoln International) earns its higher fee. Note Indianapolis's thin bench above ~$150M means the largest local processes often co-advise. We serve 6,800+ customers on the data-room side, and you can use visitor groups to run a strategics-vs-sponsors split as separate permissioned tiers in one room regardless of which advisor you pick.

I run a Warsaw, IN medtech company — do I want a sector-specialist healthcare banker or a generalist Indianapolis advisor?

For a Warsaw, IN orthopedics or medtech company, you almost always want a sector-specialist healthcare banker rather than a generalist Indianapolis advisor — the buyer network, regulatory diligence, and IP/QA scrutiny are specialized enough that a generalist leaves multiple on the table. Warsaw is the "Orthopedic Capital of the World," home to one-third of the world's orthopedic-device companies and two-thirds of the world's hip and knee manufacturers, with Zimmer Biomet headquartered there alongside DePuy/J&J and Medtronic spine operations. A medtech seller in that orbit is rarely a Main-Street process: the logical buyers are strategics and healthcare-focused PE platforms that a sector banker already knows. On the national side, Houlihan Lokey's pharma-commercialization and healthcare desks and William Blair's healthcare/life-sciences practice (reaching Indiana from Chicago) are built for exactly this — Houlihan Lokey's Carmel-based Avant Healthcare sale is the local proof point. Where a strong Indianapolis generalist still fits: a smaller component supplier or services business in the $5M-$30M band, where a relationship-rich boutique like Periculum can run a tight process and pull in the specialist buyers by name. The test for any banker pitching a Warsaw seller: can they name the active orthopedic and spine acquirers and the last comparable medtech deal they closed? On the document side, regulated medtech diligence is QA- and IP-heavy, so a data room with dynamic per-viewer watermarking and screenshot protection matters — I run Peony, a data room company, and those controls live on our Data Room tier.

How does a sell-side M&A process work for a lower-middle-market Indiana company, step by step, and what's the typical timeline to close?

A lower-middle-market Indiana sell-side runs in five overlapping stages and typically takes 6-9 months from signing the engagement letter to close, longer if the business needs cleanup first. The rough timeline: 4-8 weeks of preparation (clean financials, a quality-of-earnings file, the CIM, and a data room); 2-4 weeks of buyer outreach under NDA, starting from a blind teaser; 3-5 weeks to collect indications of interest and build a short list; 4-6 weeks of management meetings and the lead-bid/LOI stage; then 8-12 weeks of confirmatory due diligence and definitive-agreement negotiation to close. The advisor's job through all of it is to manufacture competitive tension — running a real auction across both strategic buyers (in Indiana that often means in-state acquirers and their supplier networks) and private-equity platforms, so no single bidder feels unchallenged. Manufacturing and medtech deals can run faster on the buy side when a strategic already knows the asset, but slower through environmental, regulatory, or QA diligence. The single biggest timeline risk is unprepared financials — sellers who walk in without clean, auditable numbers add months. A clean, staged data room prepared before launch is the most reliable way to compress the back half of the schedule; I run Peony, a data room company used by 6,800+ customers, and the sellers who set up the room before going to market consistently close faster than the ones who scramble after the first LOI.

What documents and data room do I need to prepare before selling my Indiana manufacturing business?

Before selling an Indiana manufacturing business, prepare a data room organized around the eight diligence workstreams a buyer will run: financial (3-5 years of statements plus a quality-of-earnings file), corporate/legal (cap table, org chart, bylaws, minutes), commercial (customer and supplier contracts, concentration analysis), operational (facilities, equipment, capacity, leases), HR (org chart, key-employee agreements, benefits), IP and IT (patents, trademarks, systems), tax (returns, nexus, credits), and environmental — which matters more in a manufacturing footprint, where Phase I/II site assessments and permits are common diligence items. The two documents that do the most work up front are a tight quality-of-earnings file and the CIM (confidential information memorandum) your advisor builds to market the business. The discipline that protects you is staged disclosure: a blind teaser first, the named CIM only after an NDA, and sensitive material (customer names, pricing, employee rosters, trade secrets) held back to later stages and released only to a short list. A data room with per-buyer permissions, page-level analytics, and dynamic watermarking is what makes that enforceable — each viewer sees only their tier, and every page they open carries their identity so a leak is traceable. I run Peony, a data room company used by 6,800+ customers, built for exactly this kind of tiered, watermarked release, and you can stage strategics, sponsors, and family offices as separate visitor groups in one room.

Can a small Indianapolis boutique actually get my deal in front of strategic buyers like Eli Lilly, Elevance, Cummins, or Corteva — and national PE?

Yes — and Indiana's strategic-acquirer density is actually a structural advantage rather than a limitation, because so many credible buyers are headquartered in-state. At least nine Indiana-headquartered public companies closed or announced material M&A in 2023-2026: Eli Lilly is the spine (six acquisitions worth about $6.1B in 2023, then Morphic for ~$3.2B in July 2024, Scorpion for up to $2.5B in January 2025, and Verve for up to ~$1.3B in June 2025), alongside Elevance Health (CareBridge, Paragon Healthcare), Cummins, Allison Transmission (Dana Off-Highway, ~$2.7B), Zimmer Biomet of Warsaw (Paragon 28, ~$1.1B), Corteva (Stoller, $1.2B), Steel Dynamics, Simon Property Group, and Republic Airways. A small boutique's job is not to know every buyer on earth — it is to know which of these corporate-development teams and which PE platforms are actually buying in your category this quarter, and to get your CIM in front of the right VP. The screening test: ask the advisor to produce a buyer list that mixes 8-15 named strategics with 15-30 named sponsors specific to your sub-sector. A genuinely Indiana-fluent boutique like Periculum can do that; a generalist who cannot name the in-state acquirers is the wrong fit. One honest caveat: these large-cap strategics are buyers, not a guarantee your specific company is on their list — and for a true cross-border or coastal-PE pool, a boutique should co-advise with a national firm. We serve 6,800+ customers on the data-room side, and visitor groups let you run the strategics-vs-sponsors split as separate permissioned tiers in one data room.

How do I keep the sale of my Indiana company confidential so employees and competitors don't find out?

Confidentiality is run through staged disclosure and tight access control — and in a small market like Indiana, where "everyone knows everyone," it is one of the main reasons to hire an intermediary rather than shop the business yourself. The standard playbook: the advisor markets a blind teaser first (industry, size, and financial highlights with no name); interested buyers sign an NDA before receiving the named CIM; and sensitive material (customer names, employee rosters, pricing, IP) is held back until later diligence stages and released only to a short list. A data room with per-buyer permissions and dynamic per-viewer watermarking is what makes this enforceable — each viewer sees only their tier, and every page they open carries their identity, so a leaked teaser is traceable back to the exact person who leaked it. That deterrence matters most in a state where a competitor, a customer, or a key employee might be one handshake away. Tell your advisor explicitly that no competitor on your do-not-contact list should ever receive even the blind teaser, and put that list in the engagement letter. I run Peony, a data room company used by 6,800+ customers, built for exactly this kind of tiered, watermarked release — dynamic per-viewer watermarks and screenshot protection are how you make a small-market sale leak-resistant, and page-level analytics tell you who actually opened what.

Before signing an engagement letter, how do I verify an Indianapolis M&A advisor's track record, and what red flags should I watch for?

Verify an Indianapolis advisor on three things — FINRA registration, named recent closings in your sub-sector, and a written staffing commitment — and treat the pitch itself as the least reliable signal. Start with the licensing line: a securities-based business sale should run through a FINRA-registered broker-dealer (check BrokerCheck — Periculum Capital is CRD #43362, for example), while Main-Street brokers like Indiana Business Advisors operate under business-brokerage credentials (IBBA's CBI, M&A Source) rather than FINRA, which is fine below ~$5M but not for a securities sale. Green flags: named recent deals in your category with the buyers identified, a senior banker who will commit in writing to staffing your calls personally, a realistic valuation backed by comparable transactions (not a flattering number to win the mandate), and a clear, capped fee structure. Red flags: a large upfront fee with a vague success structure; a valuation that sounds too good to be true; reluctance to name the senior banker who will actually run the deal; sending sensitive documents over email instead of a permissioned data room; and a tail period of 18-24 months they refuse to negotiate. For an Indiana seller specifically, test whether the advisor can speak fluently about the in-state strategic buyers and the relevant sub-sector multiples — a generalist who cannot name them is the wrong fit. I run Peony, a data room company, and a telling early signal is whether the advisor insists on a real data room with page-level analytics rather than emailing your financials around.

What does an M&A advisor charge to sell a $25M company in Indiana — is a 3-3.5% success fee normal, and how does the Double Lehman formula and retainer work?

For a $25M Indiana company, expect a monthly retainer plus a success fee at close, with a 3-3.5% blended success rate squarely in the normal range. The most common structure is a Double Lehman scale — 10% of the first $1M, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $5M — which on a $25M deal computes to about $700K, roughly 2.8%; add the slice of retainer that is not credited back plus any minimum-fee floor and the effective blended rate usually lands near 3-3.5%. That tracks national middle-market data: a $25M deal sits in the $10M-$30M band where success fees run about 2-5%, so quote ~3-5% as the practical range. Retainers (work fees) in this band run roughly $15,000-$30,000 per month, and they are frequently credited against the success fee at closing — but only if the engagement letter says so in writing, so negotiate the credit explicitly. A minimum-fee floor (commonly around $150,000) appears in most letters, but on a $25M deal the percentage fee normally exceeds it, so the floor rarely binds at this size. What matters more than the headline percentage is the base it applies to (total enterprise value including assumed debt and earnouts, or just cash at close) and the tail period — banks ask for 18-24 months; cap it at 12. The fee delta between two good advisors is almost always dwarfed by the price delta a competitive, well-run auction produces. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — a predictable cost against an advisory fee that runs into six figures.

Related resources

- M&A advisor vs business broker vs investment bank — the decision that comes before this Indianapolis shortlist: which of the three intermediary types should sell your company, by deal size, goal, and the licensing line that separates them

- M&A advisor fees: what you actually pay — the fee hub for this series: Lehman vs Double Lehman math, retainer credits, minimum-fee floors, and the engagement-letter clauses that inflate the bill

- M&A Due Diligence: 6-Phase Playbook + 8 Workstreams — what your buyer is actually doing once you sign the LOI

- M&A Data Room: Setup and Workstream Mapping — the data room setup playbook for sell-side prep

- Best Data Room for a Small M&A Deal (sub-$30M sale) — right-sized VDR selection and setup for a sub-$30M sale, the band where most Indiana founder exits land

- Sell-Side Due Diligence: The 90-Day Prep Pyramid — sell-side prep including vendor DD, which matters more in a manufacturing or medtech footprint

- State of M&A Data Rooms: 2026 Benchmark — the 283-deal Peony platform benchmark

- How to Write a CIM (Confidential Information Memorandum) — the authoring playbook for the offering document your advisor will build for the sale

- Best M&A Advisors in Chicago — the Midwest's largest M&A hub and the most common out-of-state desk reaching Indiana

- Best M&A Advisors in Detroit — the closest Midwest industrial comparator (automotive and manufacturing)

- Best M&A Advisors in Cleveland — the canonical Rust Belt strategic-acquirer-density comparator

- Best M&A Advisors in Columbus — the neighboring central-Ohio metro with the inverse setup: capital pouring in (Intel, data centers) but no homegrown national bank, where the homegrown boutiques transact through third-party broker-dealers

- Best M&A Advisors in Cincinnati — southern Ohio's consumer-brand "Brand Town" (P&G, Kroger), with a genuine homegrown registered bench (RKCA, Fifth Third Capital Markets)

- Best M&A Advisors in St. Louis — the closest Midwest comparator: another strategic-acquirer-dense metro anchored by a genuine in-state investment bank (Stifel, the St. Louis "Headquarters Town" analog to Indianapolis)

- Best M&A Advisors in Minneapolis — Upper-Midwest medtech, industrial, and AgTech comparator

- Best M&A Advisors in Nashville — Southeast healthcare-services comparator

- Best M&A Advisors in Dallas — Sun Belt growth-market comparator

- Best M&A Advisors in Kansas City — home of the Animal Health Corridor that Indiana-headquartered Elanco anchors from Greenfield; the "Ownership Town" where ESOPs are a first-class exit and the flagship advisor just renamed (Turnstone)

Footnotes and sources

- Periculum Capital — firm overview and January-February 2026 sell-side closings (Aerosmith Fastening, Good Earth Lighting, Dealers Wholesale, BOC Oil, Cornerstone Autism Center); firm-reported 400+ transactions / $4B+ value

- FINRA BrokerCheck — Periculum Capital Markets, CRD #43362 — FINRA/SIPC registration status

- EO Advisors — firm overview and leadership (Zionsville / Indianapolis metro; securities via M&A Securities Group)

- Skellig Capital Advisors — firm overview and leadership (Indianapolis; securities via Kittle Capital Markets)

- ArkMalibu — sell-side-only firm overview (Cincinnati HQ; Indianapolis office opened October 3, 2024)

- KSM Corporate Finance launch announcement — Katz, Sapper & Miller IB arm launched January 2026 via Charter Capital Partners' IB team (deal team operates from Grand Rapids, MI)

- Lincoln International — firm overview; Wellness Pet Company / Mishawaka, IN plant to United Petfood (announced June 6, 2024)

- Houlihan Lokey — firm overview; Avant Healthcare (Carmel, IN) sale to Real Chemistry (closed February 1, 2024)

- Eli Lilly Q4 2023 results — six 2023 acquisitions (~$6.1B) (BioSpace, February 2024)

- Eli Lilly to acquire Morphic Holding (~$3.2B) (STAT, July 2024)

- Eli Lilly to acquire Scorpion Therapeutics (up to $2.5B) (Lilly IR, January 2025)

- Eli Lilly to acquire Verve Therapeutics (up to ~$1.3B) (PR Newswire, June 2025)

- Eli Lilly plans to more than double U.S. manufacturing investment ($50B+) (Lilly IR, February 2025)

- Lilly $4.5B LEAP-district genetic-medicine Foundry (WFYI, May 2026)

- Allison Transmission completes ~$2.7B Dana Off-Highway acquisition (PR Newswire, January 2026)

- Zimmer Biomet completes ~$1.1B acquisition of Paragon 28 (PR Newswire, April 2025)

- BioCrossroads — Indiana life-sciences sector surpasses $100B (Inside INdiana Business, March 2026)

- Warsaw, IN orthopedics cluster (Becker's, October 2022) — one-third of orthopedic-device companies, two-thirds of hip/knee manufacturers

- Conexus / CICP — record $29B advanced-manufacturing investment in 2024 (CICP, 2025)

- DOE finalizes $7.54B loan to StarPlus Energy (DOE Loan Programs Office, December 2024)

- GM–Samsung SDI New Carlisle battery plant — construction paused (Detroit News, October 2025)

- Roche Indianapolis diagnostics expansion (up to $550M) (MedTech Dive, May 2025)

- Eton — M&A advisory fees by deal size (success-fee bands, retainer ranges; $10M-$30M = 2-5%)

- Firmex — M&A Fee Guide 2025 (success-fee curve corroboration)

- Jones Day — federal M&A Broker exemption, §15(b)(13) (Securities Exchange Act §15(b)(13); does not preempt state law)

- Indiana Securities Division (Secretary of State) — Indiana Uniform Securities Act; Administrative Order AO 25-001 (April 3, 2025) conditional no-enforcement order

- Capstone Partners — Q1 2026 Capital Markets Update (national lower-middle-market deal-volume trend)