9 Best M&A Advisors in Las Vegas for $5M–$500M Deals (2026)

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: July 2026

Why I wrote this

I'm Sean Yu, co-founder of Peony, a data room company. Before Peony I ran M&A deals as a banker at Nomura and invested at Target Global and Backed VC, so I have sat on both sides of the table — and now, on the document side, I watch hundreds of deals a year move through our platform, from founder-led exits and family-business successions to PE recapitalizations and strategic carve-outs. Las Vegas is the entry in our M&A advisor series where the metro's defining fact is not its industry mix or its deal volume but a regulator that sits inside every gaming deal: in Las Vegas, every deal closes twice — once at signing, and once at the regulator. Most "best Las Vegas M&A advisors" pages miss this entirely. They list generic local business brokers as if a slot-route or casino sale worked like selling a dry cleaner. They repeat the persistent error that Macquarie bought Union Gaming (it was CBRE). And they never mention the one fact that governs every gaming transaction in this state: you cannot close before the Nevada Gaming Commission approves the buyer, and that approval can take up to a year. At Peony we now serve more than 5,900 customers, and Las Vegas sits squarely in the sub-$500M enterprise-value band that makes up the bulk of the deals we see in our state-of-the-market benchmark.

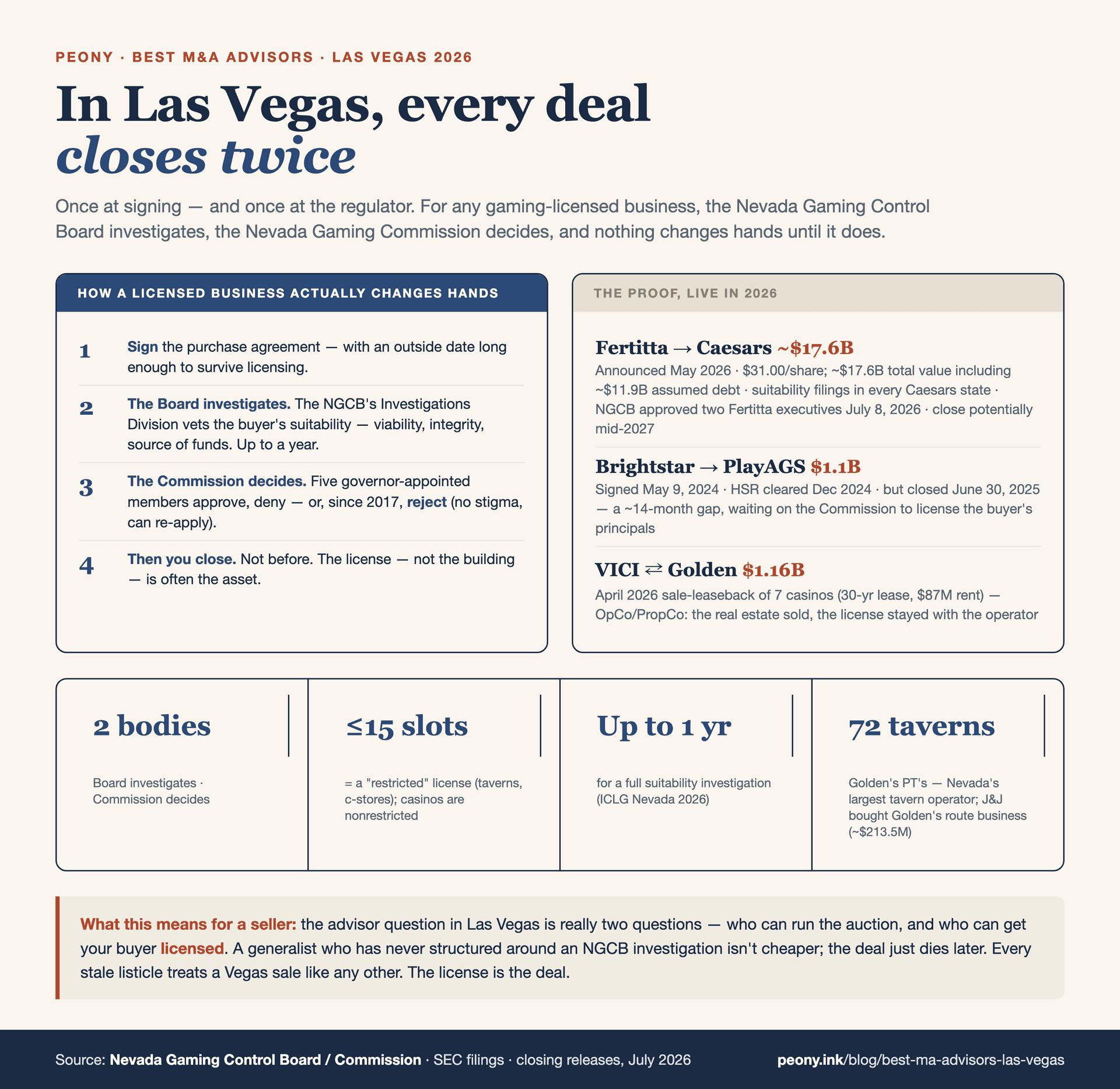

Here is the thesis I want you to internalize before you read another word: for any gaming-licensed business, the Nevada Gaming Control Board investigates and the Nevada Gaming Commission decides, and neither the money nor the license changes hands until the Commission votes yes. In an ordinary business sale, the deal is done when the lawyers sign and the wire clears. In Nevada gaming, signing is only the first close; the second — and the one that actually transfers the license — happens at a Commission hearing that may be a year away. That single fact reorganizes the entire advisor decision, the entire timeline, and the entire risk structure of your deal. The live 2026 proof is threading the system right now: Tilman Fertitta's roughly $17.6B acquisition of Caesars Entertainment (including about $11.9B of assumed debt) is working through suitability hearings in every Caesars state, and the Nevada Gaming Control Board reviewed two Fertitta executives on July 8, 2026 — with a potential close not until mid-2027.

This post is the working playbook I would hand to a Nevada gaming operator weighing a sale — the owner of a slot route and a group of taverns, a casino operator, or a gaming-technology supplier — fielding inbound interest from consolidators and wondering whether any advisor can value the business, whether the deal will survive licensing, and how to keep the whole thing quiet in an industry where everyone talks. The frames come from cross-referencing the Nevada gaming statutes and regulations, FINRA BrokerCheck, the firms' own disclosures, the ICLG Gambling 2026 Nevada chapter, and the verified 2024-2026 deal record against the state's regulatory specifics. I will be honest about the limits everywhere they exist — including the uncomfortable one that the best gaming-M&A banks are mostly not in Las Vegas at all.

Who are the best M&A advisors in Las Vegas right now for $5M-$500M deals?

The best M&A advisor in Las Vegas depends first on one question no other city in this series has to ask: does your business hold a gaming license? If it does, you want a gaming-specialist investment bank and a gaming attorney, and you should accept that the deepest specialists are mostly headquartered elsewhere. If it does not — a restaurant without gaming, a services company, a construction or hospitality-services business riding the capex boom — you are in the thin local generalist and permitted-business-broker tier, or you import a lower-middle-market boutique. And below roughly $2M of enterprise value, you are in true business-brokerage territory, where Nevada's Business Broker Permit under NRS 645.863 governs who can even list your business.

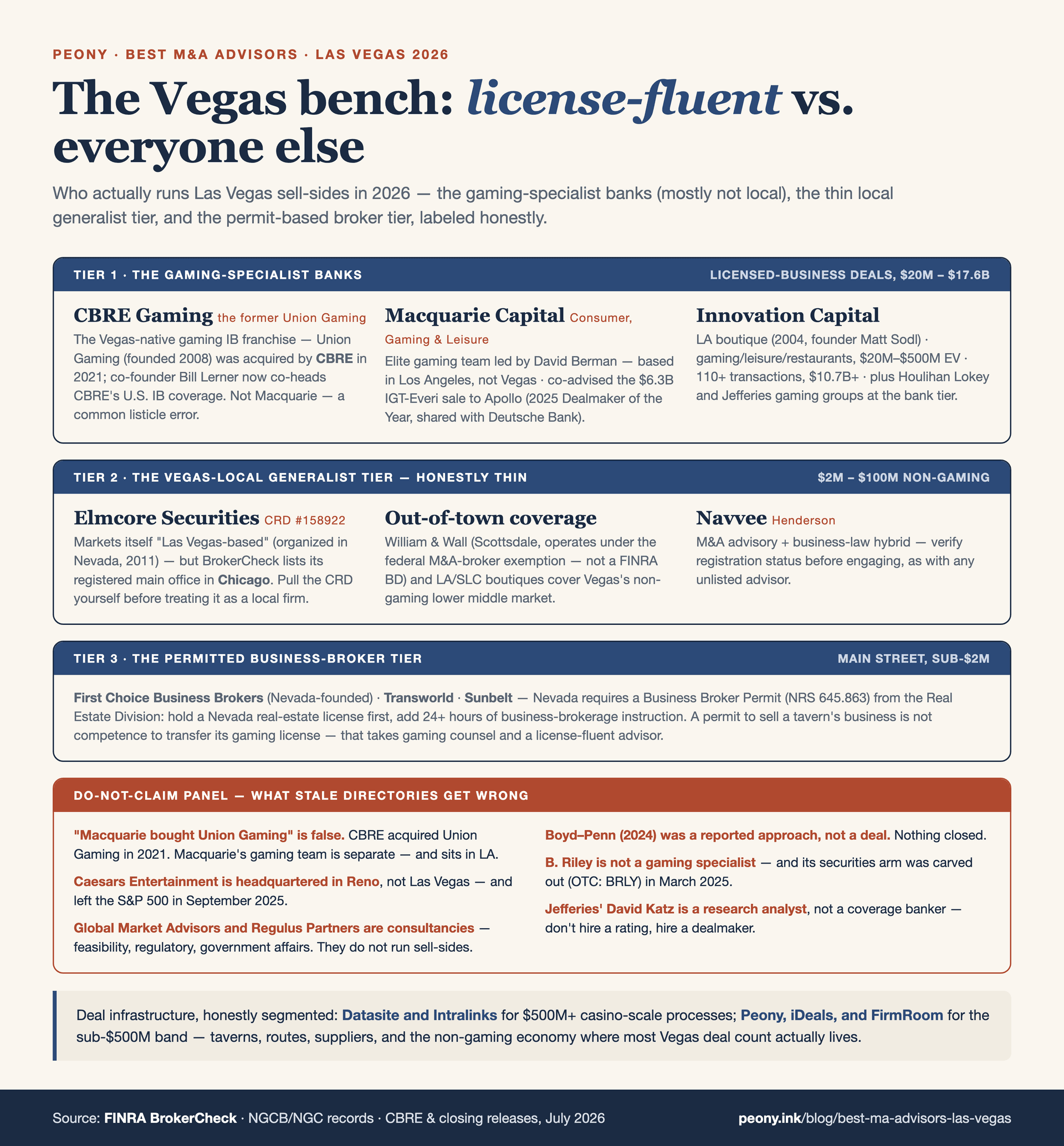

Here is the 2026 shortlist, sorted by tier and by whether the deal is gaming-licensed. The verification wrinkle in Las Vegas is unlike any other city: the traps are not dead firms so much as miscategorized ones — consultancies dressed up as banks (Global Market Advisors, Regulus Partners), a research analyst mistaken for a dealmaker (Jefferies' David Katz), a "Las Vegas-based" broker-dealer whose registered main office is actually Chicago (Elmcore, CRD #158922), and a persistent factual error about who bought Union Gaming (CBRE, not Macquarie).

| Firm | HQ / Las Vegas presence | Sweet spot | Specialty | FINRA broker-dealer status |

|---|---|---|---|---|

| CBRE Gaming (the former Union Gaming) ★ | Las Vegas (Union Gaming founded 2008; acquired by CBRE Group in 2021) | Gaming, mid-large | The Vegas-native gaming IB franchise; gaming M&A + gaming real estate (co-head Bill Lerner) | Part of CBRE's regulated broker-dealer platform (verify entity) |

| Macquarie Capital (Consumer, Gaming & Leisure) | Los Angeles (not Vegas); global platform | Gaming, large | Elite gaming IB (David Berman); co-advised the ~$6.3B IGT/Apollo deal | Established FINRA broker-dealer (Macquarie Capital (USA)) |

| Innovation Capital | El Segundo / Los Angeles (not Vegas), founded 2004 | $20M-$500M EV | Mid-market gaming, leisure, and restaurant M&A (110+ deals, $10.7B+; founder Matt Sodl) | Registered broker-dealer (verify entity on BrokerCheck) |

| Houlihan Lokey (Gaming) | National platform; no dedicated Vegas gaming-M&A HQ | Gaming, mid-large | National gaming coverage (Joel Simkins); runs gaming sell-sides | Established FINRA broker-dealer |

| Jefferies (Gaming, Lodging & Leisure) | National platform; no dedicated Vegas gaming-M&A HQ | Gaming, large | National gaming/lodging/leisure IB (David Katz is a research analyst, NOT a banker) | Established FINRA broker-dealer |

| Oakvale Capital / Partis Solutions | London (Oakvale) / iGaming-focused | Gaming (iGaming) | iGaming and online-gaming M&A tilt (Oakvale ~22 deals) | See body — non-US / boutique advisory |

| Elmcore Securities LLC | Markets as "Las Vegas-based" — but registered main office is Chicago | under $200M revenue | Mid-market IB for the non-gaming economy — pull CRD #158922 yourself | Registered broker-dealer (CRD #158922, main office Chicago) |

| William & Wall | Scottsdale, AZ (not Vegas), founded 2021; explicitly advises Nevada | under $300M rev / over $3M EBITDA | Out-of-town lower-middle-market coverage of the non-gaming economy | M&A advisor (federal M&A-broker exemption, NOT a FINRA BD) |

| Nevada permitted business brokers | Las Vegas (First Choice, Transworld, Sunbelt, M&A Business Advisors) | up to ~$10M EV | Main Street / small-business sales; NRS 645.863 Business Broker Permit tier | State Business Broker Permit (not FINRA broker-dealers) |

A few notes the table cannot carry. CBRE Gaming is the closest thing Las Vegas has to a homegrown gaming-M&A franchise, and its story contains the single most common error on stale lists. It began as Union Gaming, founded in Las Vegas in 2008 with a Hong Kong office, the specialist gaming boutique of its era. In 2021 it was acquired by CBRE Group — not Macquarie, whatever a dozen out-of-date directories tell you — and co-founder Bill Lerner now co-heads CBRE's gaming investment-banking coverage, with the team merged into CBRE's Las Vegas gaming real-estate group under Michael Parks. If a "best Las Vegas gaming advisors" page says Macquarie bought Union Gaming, it has a fact wrong that a five-minute check would have caught — and that tells you something about the rest of its facts.

Macquarie Capital runs one of the elite gaming investment-banking practices in the world under David Berman, but — and this is the metro's recurring theme — it is based primarily in Los Angeles, not Las Vegas; it co-advised the roughly $6.3B IGT/Apollo transaction. Innovation Capital (Los Angeles, founded 2004 by Matt Sodl) is the mid-market gaming, leisure, and restaurant specialist for the $20M-$500M band. Houlihan Lokey (Joel Simkins) and Jefferies are the national banks that run large gaming sell-sides. And the honest correction that saves you an embarrassing call: Global Market Advisors and Regulus Partners are consultancies, not investment banks — feasibility, regulatory, and research work, not sell-side M&A. More on the sorting test below.

Why does "every deal close twice" in Las Vegas?

Because Nevada is the one place in this series where a government regulator sits inside every gaming transaction, with the power to stop it — and the deal is not legally done until that regulator approves the buyer. The phrase "every deal closes twice" is not a metaphor; it is a description of the mechanics. There is the commercial close (the purchase agreement is signed, the price is set, the terms are locked) and there is the regulatory close (the Nevada Gaming Commission votes to license or find suitable the new owner, and only then does the gaming license — the thing that makes the business worth buying — actually transfer). Between those two closes can sit a year.

Here is the structure that produces it. Nevada regulates gaming through two tiers. The Nevada Gaming Control Board (NGCB) is the investigative and enforcement arm: a full-time body whose Investigations Division conducts the background, financial, and source-of-funds investigations of everyone who wants to hold or control a gaming license — buyers, principals, key employees, and anyone acquiring control through a change of ownership. In a disciplinary matter, the Board is the prosecutor. The Nevada Gaming Commission (NGC) is the decision-maker: five part-time members appointed by the Governor to four-year terms who take the Board's investigation and recommendation and cast the final vote to approve, deny, reject, or condition the license. The clean way to hold it: the Board investigates and recommends; the Commission decides.

For a seller, that two-tier structure has three consequences you must plan around. First, timing: a full suitability investigation can take up to one year, per licensing-practice guides including the ICLG Gambling 2026 Nevada chapter, because the depth of the Investigations Division's review — not the size of your business — sets the clock. Second, sequence: you sign, then the buyer files and is investigated, then the Board recommends, then the Commission votes, then you close. You cannot close before Commission approval; the license does not ride along with the signature. Third, buyer risk: because the regulator can find a buyer unsuitable, who you sell to is a suitability question, not just a price question — a buyer with a clean, known Nevada gaming record is a lower-risk counterparty than a first-time applicant, entirely apart from what they offer. Every part of this article — advisor selection, deal structure, timeline, confidentiality — flows from this one fact. In the sections that follow I will take the persona's most urgent questions in order: how the change of ownership actually closes, how long the Board takes, whether licensing delays can kill the deal, and how to structure around all of it.

How does a change of ownership actually close for a Nevada gaming licensee?

It closes in two acts, and the second act is the regulator — which is the whole reason I say every Las Vegas deal closes twice. In an ordinary business sale, closing is a single event: the parties sign, the buyer pays, and ownership (and any operating licenses) transfers that day. In Nevada gaming, the gaming license does not transfer on the signing date. Instead, the sequence runs like this: you negotiate and sign the definitive purchase agreement (this is the commercial close, and it sets price and terms); then the buyer — together with its principals, controlling owners, and key employees — files applications for licensure or a finding of suitability; the Board's Investigations Division runs a deep background, financial, and source-of-funds investigation; the Board holds a hearing and issues a recommendation; and finally, at a later hearing, the Commission votes to grant, deny, reject, or condition the license. Only after the Commission votes yes can the transaction actually close and the license effectively pass to the new owner.

The practical implications for how you run and paper the deal:

- The purchase agreement must condition closing on Commission approval. This is not boilerplate you can skip; it is the load-bearing clause. Closing is expressly contingent on the buyer obtaining the required Nevada gaming approvals, and the agreement needs an outside date (a drop-dead date) that gives the licensing process realistic room — often a year or more for an unlicensed buyer.

- Interim operations matter. Because months pass between signing and closing, the agreement typically addresses how the business is run in the interim, sometimes with management or interim-operating arrangements consistent with Nevada regulations, so the license stays in good standing while the application is pending.

- The buyer's identity is a gating item, not a detail. Since the Commission can reject the buyer, sellers and their advisors weigh a bidder's licensability alongside its price — a slightly lower bid from an already-licensed operator can be worth more than a higher bid from a first-time applicant with a longer, riskier suitability path.

The single load-bearing fact that stale advisor lists miss is this: the deal is not done when the lawyers sign; it is done when the Commission votes yes. A "best Las Vegas M&A advisors" page that describes selling a licensed gaming business as if it closed like any other sale is describing a transaction that does not exist in this state. Structure the deal for the two-close reality from the first draft.

How long does Nevada Gaming Control Board approval take when selling a gaming business?

Plan for months, and understand that a full suitability investigation can take up to one year — this is the timeline stale listicles never warn you about. The reason is the nature of the Board's work: the Investigations Division does not run a checklist; it conducts an intensive background, financial, and source-of-funds investigation of the buyer and everyone who will control or hold the license. The depth of that review sets the clock, and the clock is long. For a sense of scale on a sophisticated deal, the Fertitta Entertainment-Caesars approvals across all of Caesars' license states have been estimated at as long as 10 months — and that is an experienced buyer with elite gaming counsel, not a first-timer.

So for your own sale, do not assume a signed deal closes in the ordinary 60-to-90-day window. The realistic shape is two clocks stacked:

- The normal sell-side process runs about 6-9 months from engagement to signing (preparation, marketing under NDA, indications of interest, management meetings, LOI, and confirmatory diligence to a signed agreement).

- The gaming-licensing period then sits between signing and close, on top of that — potentially another several months to a year depending on the buyer.

Two levers genuinely shorten the licensing clock, and a gaming-fluent advisor will pull both from day one:

- Choose an already-licensed or low-risk buyer. A buyer who already holds Nevada gaming licenses, or who has a clean, well-documented gaming record across multiple jurisdictions, is a known quantity to the Board and typically clears faster than a first-time applicant whose sources of funds and background must be built from scratch. This is why who you sell to affects how fast you close, not just the price.

- File the moment the deal signs. The licensing clock does not start until the buyer's application is in. An advisor who has run gaming deals will have the buyer's suitability filing ready to go at signing rather than starting to assemble it weeks later — every week of delay in filing is a week added to close.

The mistake I see is treating licensing as a back-office formality discovered at the LOI stage. In Nevada gaming it is the gating path to close, and the advisor and gaming attorney should build the licensing calendar into the deal from the first conversation. I run Peony, a data room company used by 5,900+ customers, and a well-organized room keeps the buyer's licensing team and the Board's investigators moving on documents instead of waiting on them.

Will licensing delays kill my slot-route sale — and how do I structure around that risk?

Licensing delays rarely kill a well-structured deal, but they routinely kill a badly structured one — so the honest answer is that the risk is real, it is manageable, and managing it is precisely why you want a license-fluent advisor and a gaming attorney in the room before you sign anything. The failure mode is not usually that the Commission says no; it is that the deal was papered on an unrealistic timeline, the licensing calendar slipped past the outside date, and the parties had to renegotiate (or walk) from a position of weakness. The fix is structural, and it is well understood by people who do these deals for a living.

The structural moves that de-risk a gaming sale:

- Condition closing on Commission approval, with a realistic outside date. The agreement should make closing expressly contingent on the buyer obtaining Nevada Gaming Commission approval and set a drop-dead date that respects the up-to-a-year reality for an unlicensed buyer — not a 90-day date borrowed from an ordinary asset sale.

- Allocate suitability risk explicitly. Decide and document who bears the risk and cost if the buyer is found unsuitable or withdraws — reverse break-up considerations, expense allocation, and what happens to any deposit. A first-time seller who leaves this vague is exposed.

- Handle interim operations. Provide for how the route runs between signing and closing so the licenses stay in good standing and the location relationships are preserved while the application is pending.

- Pick a licensable buyer in the first place. The cheapest risk mitigation is choosing a buyer whose suitability is a low-risk question — an already-licensed consolidator over an unknown first-time applicant, all else equal.

The honest cautionary tale is the Brightstar-PlayAGS deal, and it cuts both ways. Brightstar Capital Partners agreed to acquire Las Vegas-headquartered gaming supplier PlayAGS for roughly $1.1B ($12.50 per share) on May 9, 2024. Antitrust cleared — HSR was satisfied by December 2024. But the deal could not close until the Nevada Gaming Commission licensed Brightstar's principals (including founder and CEO Andrew Weinberg) and AGS's CEO David Lopez, and that licensing drove the timeline: the deal actually closed June 30, 2025, a roughly 14-month sign-to-close gap largely attributable to licensing. Read it correctly and it is reassuring, not scary: the deal closed, because it was structured to survive the wait. That is the goal — not to eliminate the regulatory clock, which you cannot, but to build the deal so the clock cannot break it. I run Peony, a data room company used by 5,900+ customers, and keeping the licensing and diligence teams supplied from a clean, permissioned room is part of not letting the timeline slip.

What is the difference between a restricted and a nonrestricted Nevada gaming license, and why does it matter to my sale?

The distinction determines what you are actually selling, what the buyer must qualify for, and how the deal is structured — so get it right before you go to market. In Nevada, a restricted license authorizes no more than 15 slot machines and no other games, with the slots incidental to the primary business — this is the license behind taverns, bars, and convenience stores where gaming is a sideline to the food, drink, or retail operation. A nonrestricted license is the full-casino authorization (unlimited slots and table games, or a business whose primary purpose is gaming). The two carry very different regulatory weight, and the buyer of your business has to qualify for whichever license class the business holds.

For the distributed-gaming persona this article is written for, there is a crucial third wrinkle: a slot-route (distributed-gaming) operator license is itself a nonrestricted license, and it normally requires the operator to have three or more committed locations. So even though the individual taverns and stores on a route may each hold restricted licenses, the route operator sits on the nonrestricted side of the line — which means a buyer acquiring your route business is stepping into a nonrestricted licensing process, with the fuller suitability review that implies. That is not a detail; it shapes the buyer universe (only operators who can qualify nonrestricted can buy) and the timeline (nonrestricted suitability is the deeper review).

One thing I will not do is quote you a specific statewide count of licenses by class — that number is not something I can verify to this series' standard, and the authoritative source is the NGCB's monthly Board Informational Report, which is where you (or your advisor) should pull current figures rather than trusting a stat floating around a listicle. The practical takeaway for a seller: know exactly which license classes your business holds, understand that a route operator is nonrestricted, and make sure your advisor and gaming attorney scope the buyer's qualification path to match — because a buyer who can only qualify for a restricted license cannot buy a nonrestricted route.

What is the "reject versus deny" distinction, and why does it matter to a buyer's suitability?

It matters because the two outcomes carry very different consequences for a rejected applicant — and since your buyer's suitability is the gate to your close, understanding the difference helps you assess a bidder's licensing risk. Under a 2017 Nevada law, the Commission has three possible negative-or-positive outcomes when it acts on an application, not two. It can approve the applicant; it can deny the applicant, which carries real stigma — a denial must be disclosed in future applications and effectively bars the applicant for a period; or it can reject the applicant, a softer outcome that lets the applicant re-apply without carrying the denial stigma. The reject option, added in 2017, gives the Commission a way to turn down an application that is not ready without branding the applicant with a formal denial.

To illustrate the mechanism — and I present this as history, not news — when the 2017 law was new, the Commission used the reject outcome in the case of Brian Hinchley of Table Trac Inc., voting 3-1 to reject rather than deny. I flag the date deliberately: this is a 2017-era illustration of how the reject-versus-deny tool works, not a recent event, and I am citing it only to make the distinction concrete.

Why does this matter to you as a seller? Because it refines how you read a buyer's suitability risk. A buyer who has previously been denied anywhere carries a disclosure burden and a heavier path; a buyer who was merely rejected and re-applied is in a materially better position. And it underscores the broader point of this whole article: in Nevada, the buyer's regulatory history is part of your deal risk. A gaming-fluent advisor and a gaming attorney will diligence a bidder's licensing track record the way an ordinary advisor diligences a buyer's financing — because a buyer the Commission will not approve is a buyer who cannot close your deal, no matter how good the price looks on paper.

One more mechanism worth knowing if your buyer is public or fund-backed: under NGC Regulation 16.430, an institutional investor holding more than 10% but no more than 25% of a public licensee's voting securities can apply for a waiver of the individual suitability finding — but only if the position is genuinely passive, and crossing the 10% threshold starts a 30-day clock to apply once the Board gives written notice. You will never file under Reg 16.430 yourself; its relevance is that it explains why index funds can hold large stakes in the consolidator buying you without every portfolio manager being licensed — while a change of control, the thing your sale actually is, always goes through the full suitability machine. The regulation draws exactly the line this article keeps pointing at: passive money gets a waiver; ownership gets investigated.

What is the OpCo/PropCo structure, and does it affect how I sell a gaming business?

The OpCo/PropCo structure separates the real estate from the operating business, and understanding it matters even for a smaller seller because it shapes who your buyers are and what, exactly, is being bought. In the modern gaming industry, a casino is often split into two pieces: the PropCo — the physical real estate (the building and land), typically owned by a triple-net casino REIT such as VICI Properties or Gaming and Leisure Properties (GLPI) — and the OpCo — the operating business plus the gaming license, run by the operator who pays rent to the PropCo under a long-term triple-net lease. The single most important consequence for this article: the license stays with the operator (the OpCo), even when the real estate (the PropCo) is sold. The dirt can change hands without the license moving, and vice versa.

The fresh 2026 anchor makes it concrete. On April 30, 2026, VICI Properties closed a roughly $1.16B sale-leaseback of seven Golden Entertainment casinos — a 30-year triple-net master lease with about $87M in initial annual rent (a roughly 7.5% cap rate) — while the operating business went to a new entity controlled by Blake L. Sartini. Read the structure: VICI bought the real estate; the operations and the gaming license went to Sartini's operating entity. Two different transactions, two different buyer types, one property.

Why does this matter to a $5M-$500M seller who is not selling a Strip casino? Three reasons. First, it clarifies what you own — if you own the real estate under your gaming business, that is a separable asset with its own (REIT) buyer universe, distinct from the operating business with its (licensed operator) buyer universe. Second, it means the license follows the operator, so structuring a sale of the operations is a licensing transaction regardless of what happens to the dirt. Third, it widens your options: for some sellers, a sale-leaseback of the real estate to a REIT plus a separate sale of the operating business can unlock more total value than selling the whole thing to a single buyer. A gaming-fluent advisor will tell you whether splitting OpCo from PropCo makes sense for your situation — most smaller route and tavern operators will not, but you should understand the structure that dominates the sector you are selling into.

Should I hire a gaming-specialist investment bank or a local Las Vegas business broker?

For a gaming-licensed business of real size — a slot route, a tavern-gaming group, a casino, or a gaming supplier — hire a gaming-specialist investment bank, and accept the counterintuitive truth of this metro: most of the best ones are not physically in Las Vegas. This is the fork Las Vegas frames differently from every other city in the series. In Milwaukee, "stay local" can mean hiring a top-12 global bank downtown; in Las Vegas, "hire the best gaming banker" usually means hiring a firm in Los Angeles, or a national platform, because gaming M&A is a specialist vertical whose talent concentrated at CBRE Gaming (Vegas-native, but now inside a national real-estate firm), Macquarie (Los Angeles), Innovation Capital (Los Angeles), and the gaming groups at Houlihan Lokey and Jefferies.

A gaming specialist earns its fee two ways a local generalist broker simply cannot match:

- It knows the buyer universe by name. In distributed gaming the buyers are namable — J&J Ventures Gaming, Century Gaming, the tavern consolidators — and a specialist already knows which are acquiring, at what multiples, and how to make them compete. In casino and supplier deals the specialist knows the strategics, the REITs, and the gaming-focused sponsors. A generalist broker has to build that map from scratch, on your clock.

- It understands the licensing overlay. A gaming banker structures the deal for the two-close reality — the outside date that respects the licensing calendar, the buyer's licensability as a selection criterion, the filing-at-signing discipline. A general business broker who has never run a gaming deal will not see the regulatory clock coming.

Reach for a local Las Vegas business broker only for a small, non-gaming Main Street business — a restaurant without gaming, a services company, a retail operation — where the buyer pool is individuals and small operators rather than institutions. And even there, know the Nevada wrinkle: under NRS 645.863, brokering the sale of most businesses requires a Business Broker Permit (a real-estate license plus the permit), not just anyone with a business card. If your business holds a gaming license, the sector fluency and buyer relationships of a gaming specialist beat local convenience every time. I run Peony, a data room company used by 5,900+ customers, and whichever you pick, a clean data room is the cheapest lever you control before you even sign an engagement letter.

Which gaming-specialist banks actually cover Las Vegas deals — and where are they?

The honest map is that Las Vegas is covered by an excellent gaming-M&A bench that mostly sits somewhere else, with CBRE Gaming as the one genuinely Vegas-native franchise. Here is the verified 2026 picture, with the location truth stated plainly:

- CBRE Gaming (the former Union Gaming) — the Vegas-native gaming investment-banking franchise. Union Gaming was founded in Las Vegas in 2008 (with a Hong Kong office) and acquired by CBRE Group in 2021. Co-founder Bill Lerner now co-heads CBRE's gaming investment-banking coverage, and the team was merged with CBRE's Las Vegas gaming real-estate group under Michael Parks — so CBRE Gaming uniquely pairs gaming M&A with gaming real-estate expertise, which matters in an OpCo/PropCo world. The correction that saves you: many stale lists say Macquarie bought Union Gaming. That is false — it was CBRE.

- Macquarie Capital (Consumer, Gaming & Leisure) — one of the elite gaming IB practices globally, led by David Berman, based primarily in Los Angeles, not Las Vegas. Macquarie co-advised the roughly $6.3B IGT/Apollo transaction.

- Innovation Capital — a mid-market gaming, leisure, and restaurant boutique in the Los Angeles area, founded 2004 by Matt Sodl (ex-Merrill gaming/leisure). It targets $20M-$500M enterprise value, with 110+ transactions and $10.7B+ since inception; it advised on GLPI's $175M Tioga Downs real-estate acquisition (February 2024). In fairness, I could not verify a specific 2025-26 sell-side mandate for the firm, so I am not going to invent one.

- Houlihan Lokey (gaming coverage led by Joel Simkins) and Jefferies (Gaming, Lodging & Leisure) — the national banks that run large gaming sell-sides. One precise correction: at Jefferies, David Katz is a research analyst, not an investment banker — do not cite him as a dealmaker, a mistake I have seen more than once.

- Oakvale Capital (London, ~22 deals) and Partis Solutions — tilt toward iGaming and online gaming rather than land-based Nevada operations; classify them honestly if your business is online-facing rather than a Nevada route or casino.

The generalizable lesson is the fluency-over-address rule that governs this whole series, in its most extreme form. In gaming, the specialist's buyer list beats any local generalist's address so decisively that the specialist being in Los Angeles or on a national platform is a rounding error next to the value of its sector relationships. So the screening question for a gaming sale is not "are you in Las Vegas?" but "show me your last three gaming closings in my sub-sector — routes, taverns, casinos, or suppliers — with the buyers named, and tell me how you'll manage the licensing calendar." A firm that can answer both crisply is your advisor, wherever its office sits.

Who are the buyers for a Nevada slot route or tavern-gaming business right now?

The buyers are namable, and that is unusually good news for a seller — because a small, consolidating market means a route-fluent advisor can point to exactly who is acquiring. Nevada's distributed-gaming and tavern space is in active consolidation, and the natural acquirers for a route or tavern-gaming business are a short, identifiable list:

- J&J Ventures Gaming — the national distributed-gaming leader (roughly 29,000 machines across about 3,600 locations in Illinois, Montana, Nebraska, Nevada, and Pennsylvania). J&J entered Nevada by buying Golden Entertainment's third-party distributed-gaming route business (agreements March 2023; the Montana piece, about $109M, closed September 2023; the Nevada piece was roughly $213.5M net), and it later closed Leisure Gaming NV on January 9, 2025. J&J is a motivated, acquisitive buyer in exactly this space.

- Century Gaming — the second-largest Nevada route operator, another natural consolidator.

- Tavern consolidators, led by Golden Entertainment on the branded-tavern side. Golden is Nevada's largest tavern operator — 72 branded taverns as of June 30, 2025 (69 in the Las Vegas Valley) with 1,100+ onsite slots, under brands including PT's Gold, PT's Pub, PT's Ranch, Sierra Gold, and Lucky's. (Note the strategic split: Golden sold its third-party route business to J&J but kept and grows its branded-tavern estate — so it is a buyer of taverns, not routes.)

Why does naming the buyers matter so much for your sale? Because it turns the abstract "run a process" advice into something concrete. Your likely buyer set literally is J&J, Century, and the tavern consolidators — and a route-fluent advisor's job is to put the one or two who approached you up against the others (and against gaming-focused sponsors) under NDA, so price is set by competition rather than by whoever called first. It also underscores the confidentiality problem this article keeps returning to: this is a small world of a handful of acquirers who all know each other, so a leak travels fast. The pairing of "namable buyers" and "small industry" is exactly why you want staged, permissioned disclosure — the natural buyers are also the natural gossips. I run Peony, a data room company used by 5,900+ customers, built for exactly that staged, confidential release.

Two consolidators already approached me — can I sell directly without an advisor?

You can, but for a licensed gaming business it is usually the most expensive shortcut available — the two consolidators who called are professional, repeat buyers, and you are a first-time seller negotiating without leverage or a market check. The problem is structural, not about anyone's good faith. A consolidator that approaches you directly wants to transact bilaterally, without competition, because that is how they buy well. Facing one of them alone, you have no competing bid to reveal what your route or tavern group is actually worth, and no independent read on whether the multiple on the table is generous or a lowball wrapped in a compliment about your locations. That information asymmetry is what moves the price against you.

An advisor's core job is to convert those inbound calls into a competitive process — quietly running the two who approached against each other, and against other credible consolidators and sponsors (J&J Ventures Gaming, Century Gaming, the tavern consolidators, gaming-focused PE), under NDA and from a blind teaser, so price is set by the market. On a lower-middle-market gaming deal, that competitive tension typically moves the outcome by far more than the advisor's fee, and it disciplines the original buyer, who now knows they cannot slow-walk diligence or re-trade the price without risking the deal to a rival.

There is a second reason a gaming seller in particular should not go it alone: the licensing overlay. An advisor who has run gaming deals structures the transaction so the buyer's suitability review does not blow up the timeline — the realistic outside date, the buyer's licensability as a selection criterion, the filing-at-signing discipline. A first-time seller negotiating solo will not see the regulatory clock coming until it has already slipped. The honest caveat is the same as everywhere in this series: if the offers are genuinely extraordinary, the buyer is uniquely strategic, and you have independently pressure-tested the number, a full auction is not always mandatory — but at minimum get a license-fluent advisor or a strong gaming attorney to read the terms before you sign exclusivity. The default should be a process; the exception should be deliberate. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects you is identical whether one buyer called or five did.

How is a slot-route business valued — location contracts, participation splits, and all?

A slot-route (distributed-gaming) business is valued on the durability and transferability of its cash flow, which rests on the things unique to the model — and I am going to be honest with you about what can and cannot be said on multiples. The value drivers are: the location contracts (how many, how long the remaining terms, renewal and exclusivity provisions), the participation and revenue-split economics with each location, the machine count and mix, the space-lease-versus-participation structure of each deal, and — the point no ordinary valuation guide captures — whether the licenses and location relationships survive a change of ownership. A route's cash flow is only as durable as its contracts and only as transferable as its licenses.

Here is the honesty this deserves: there is no verified public multiple benchmark for route businesses. So the right answer to "what's my route worth?" is not a made-up "5-7x EBITDA" rule of thumb — it is a comparable-transaction analysis run by a license-fluent advisor who has actually seen where recent route and tavern-gaming deals cleared and can triangulate from real (often non-public) comps. Anyone who quotes you a crisp universal multiple without looking at your contracts is guessing, and you should treat the confidence as a warning sign.

The real valuation work looks like this:

- Normalize EBITDA. Adjust for owner compensation, one-time items, and the true economics of each location so the earnings base reflects transferable cash flow, not accounting artifacts.

- Assess contract and concentration risk. Weight the remaining terms, renewal odds, and exclusivity of the location contracts, and flag concentration — a route where a few locations drive most of the cash flow is riskier (and worth less) than a diversified one.

- Model the participation splits. The economics of who keeps what at each location drive margin; a buyer will rebuild this from the ground up in diligence.

- Triangulate against genuine comps. The advisor anchors value to actual recent transactions, not an internet multiple.

Notice that the valuation file and the diligence file are two sides of the same coin: a buyer will diligence contract assignability, license transferability, location concentration, and the machine base — exactly the drivers above. I run Peony, a data room company used by 5,900+ customers, and organizing location contracts, license records, and participation schedules into a clean, permissioned room is what lets an advisor build a defensible value story and lets a buyer confirm it without a fishing expedition.

What EBITDA multiple do Nevada route and tavern-gaming businesses sell for?

Honestly: there is no reliable published multiple for Nevada route and tavern-gaming businesses, and any advisor who quotes you a firm "5-7x" or "8x" without seeing your contracts is inventing precision that does not exist. I want to be blunt about this because the persona reading it likely walked in expecting a number, and the most valuable thing I can do is explain why the number they want is not real. Distributed-gaming and tavern-gaming M&A is a thin, private market: deals are negotiated between a handful of consolidators and operators, terms are rarely disclosed, and the value of any given route turns on location-contract quality, remaining terms, participation splits, machine count, and license transferability — all of which vary enormously from route to route. There is no clean public dataset of route EBITDA multiples to average, the way there is for, say, SaaS companies or restaurants.

So the credible answer to "what multiple will I get?" is a comparable-transaction analysis by a license-fluent advisor who has actually worked recent route and tavern deals and can triangulate from real (often non-public) comps — not a rule of thumb pulled from a generic small-business valuation guide. What is namable, and genuinely useful, is the buyer side: Nevada's distributed-gaming consolidation is real and active. Golden Entertainment sold its third-party distributed-gaming route business to J&J Ventures Gaming (the Montana piece, about $109M, closed September 2023; the Nevada piece roughly $213.5M net), Century Gaming is the second-largest Nevada route, and the tavern consolidators are acquiring branded taverns. There are motivated buyers with capital.

The way you convert "motivated buyers" into "a good multiple" is competitive tension — which is the advisor's job, not a formula. If you take one thing from this section, take this: do not anchor your expectations on an internet multiple, and treat any pitch that leads with a crisp universal multiple as a red flag about the advisor's rigor. The number that matters is the one a real process produces, and no one can promise it in advance. I run Peony, a data room company used by 5,900+ customers, on the document side of exactly these deals.

How do I keep my sale confidential in an industry where everyone in Nevada gaming talks?

You keep it confidential with staged disclosure enforced by a permissioned data room — a blind teaser first, the named confidential information memorandum only after a signed NDA, and the most sensitive material (location contracts, participation splits, license details, key-employee rosters) held back for a small short list of serious, vetted, later-stage bidders. This matters more in Nevada gaming than in almost any industry in this series, because it is a genuinely small world: the operators, the consolidators, the location partners, the regulators, and the gaming attorneys all know each other and see each other at the same conferences and Commission hearings. A leak that you are "for sale" can spook a location partner into not renewing, embolden a competitor to poach your locations or your best staff, or reach the regulator's orbit before you are ready — all before you have a signed deal.

The structural defenses, which a good advisor runs as a matter of course:

- A blind teaser first. The initial one- or two-page document describes the business — distributed gaming, location count, revenue and EBITDA profile — without naming it, so a recipient (including a competitor) cannot identify you from the teaser alone.

- The named CIM only after an NDA. The full confidential information memorandum, which names your company and discloses real detail, goes only to buyers who have signed a non-disclosure agreement — and your advisor curates that list to exclude the parties most likely to misuse it.

- Crown-jewel material held for the short list. Specific location contracts, participation economics, license particulars, and employee rosters are released only to a small set of serious, late-stage bidders — never in the first wave.

The tooling has to enforce all of that, which is where the document side I work on comes in. Dynamic watermarking stamps each viewer's identity across every page, so a leaked teaser or CIM is traceable to its source and buyers know it. An NDA gate blocks access to the CIM until the agreement is signed. And page-level analytics show exactly who opened what and when — so if a rumor starts, you have a record of who had access. In a market this interconnected, hold the rule: in Nevada gaming, your buyer list is also your competitor list, and everybody talks. I run Peony, a data room company used by 5,900+ customers, precisely to make this staged, watermarked, permissioned release the default rather than a scramble.

Do consolidators lowball owners who negotiate without an advisor?

Not always deliberately, but the structure of a no-advisor negotiation reliably produces a lower price — and the place it shows up most is not the opening offer. It is confirmatory diligence. The number a consolidator floats to get you into exclusivity is a marketing document; the real price is set weeks later, after their diligence team has catalogued every location contract nearing renewal, every participation split trending the wrong way, and every soft month of coin-in — each one presented, politely, as a reason to "revisit" the number. This is the re-trade, it is standard operating procedure for professional repeat buyers facing a first-time seller, and by the time it starts your alternatives have long since been told no. Facing that grind alone, most unrepresented owners concede in increments. The re-trade dynamic — not villainy — is what moves the price against you.

Competition is the only durable defense against the re-trade. An advisor keeps leverage alive through closing, not just at the letter-of-intent stage, by running the consolidator who called against other credible buyers (in distributed gaming: J&J Ventures Gaming, Century Gaming, the tavern consolidators, and gaming-focused private equity) — so the original bidder knows that grinding the price during the confirmatory phase risks losing the deal to a rival at the number they themselves offered. That protection is typically worth a multiple of what you will pay the banker, and most of it is earned precisely in the diligence phase, where represented sellers hold their number and unrepresented sellers watch it erode.

The objection I hear is confidentiality — "I don't want the market to know I'm shopping the business." It is a legitimate concern and a fully solvable one: a good advisor markets from a blind teaser under NDA, so only serious, vetted buyers ever learn your identity, and the process stays quiet even as it becomes competitive. You are not choosing between "run a process" and "stay confidential"; a well-run gaming process is confidential by construction. I run Peony, a data room company used by 5,900+ customers, built for exactly this kind of staged, confidential release — the tooling that lets you create competition without the leak you are afraid of.

What do M&A advisors charge to sell an $18M-revenue gaming business?

For an $18M-revenue gaming business — say roughly $4M of EBITDA — expect a monthly retainer plus a success fee at close, with a blended success fee in the low-single-digit percent. Independent middle-market data — the Axial/Firmex M&A Fee Guide 2024-25 — puts blended success fees at roughly 4.8% at a $5M deal, about 3.4% at $20M, and around 2.0% by $100M, so a deal in the $20M-$40M enterprise-value range (typical for that revenue and EBITDA) sits in the low-3s percent on the success fee alone. Here is how the pieces work.

The formula. A declining-rate, Lehman-style structure is still the single most common, used in about 44% of engagements. The modern default is Double Lehman (10-8-6-4-2%): 10% of the first $1M of consideration, 8% of the second, 6% of the third, 4% of the fourth, and 2% of everything above $4M. Run that on smaller checkpoints: a $10M deal computes to $400K (4.0%), a $20M deal to $600K (3.0%).

The minimum fee — the number that actually governs a smaller deal. Minimums appear in about two-thirds (roughly 67%) of engagement letters (per a 2021-22 fee-guide survey) and typically run $200K-$600K on $5M-$30M deals — so at the smaller end it is often the floor, not the percentage, that sets the bill. Ask for the minimum first.

The retainer. Roughly five of six advisers charge one, typically $5,000-$10,000 per month, and about 72% credit it against the success fee at closing (2021-22 survey) — but only if the engagement letter says so in writing, so negotiate the credit explicitly.

Two more terms deserve scrutiny, one of them gaming-specific:

- The tail period. Advisers often ask for 18-24 months, during which they collect if you sell to a buyer they introduced after the engagement ends. Negotiate toward 12 months, and require a named-buyer list at termination as your defense.

- The gaming timeline premium. Because the licensing period sits on top of the normal timeline — signing, then the suitability process, then close — a gaming deal can run longer than a comparable non-gaming deal, which means more retainer months. Budget for it, and clarify how the retainer works if the licensing calendar stretches the deal past a year.

Keep the whole cost conversation in proportion: the fee delta between two good gaming advisors is almost always dwarfed by the price delta a competitive process produces. On the data-room line item, I run Peony, a data room company with flat per-admin pricing (no per-page or per-GB fees) — a predictable cost against an advisory fee that runs into six figures, over a timeline that the gaming overlay can make unusually long.

Do I need a Nevada-licensed business broker, a gaming attorney, or an investment bank to sell?

For a gaming-licensed business of real size, you need at least two of the three working together: an investment bank (ideally a gaming specialist) to run the sale, and a gaming attorney to manage the licensing and suitability process. A Nevada-licensed business broker is the right lead only for a small, non-gaming Main Street business. Here is the clean division of labor, because getting the roles right is half the battle.

- The investment bank / M&A advisor runs the competitive process — builds the CIM, markets to strategic and financial buyers under NDA, manufactures competitive tension, and negotiates the deal. This is who gets you the price. For a gaming business, you want a gaming specialist (CBRE Gaming, Macquarie, Innovation Capital, Houlihan Lokey, Jefferies) whose buyer relationships and licensing fluency a generalist cannot match.

- The gaming attorney handles the regulatory spine — structuring the deal so closing is properly conditioned on Nevada Gaming Commission approval, preparing the buyer's suitability filings, and shepherding the application through the Board's Investigations Division and the Commission. This is who gets you closable. No banker substitutes for gaming counsel on the licensing path.

- The Nevada-licensed business broker is a different animal. Under NRS 645.863, brokering the sale of a business that does not derive most of its value from real property requires a state Business Broker Permit — you must first hold a Nevada real-estate license, then add the permit (which requires at least 24 hours of business-brokerage instruction, a $40 application, and expires with the underlying license). A plain real-estate licensee without the permit may only sell businesses where at least half the value is the real property itself. Brokers typically list smaller, owner-operated businesses to individual buyers — appropriate for a $500K restaurant, not a licensed route or casino.

So for the persona this article is written for — an owner selling a real gaming business — the honest answer is investment bank plus gaming attorney, not a business broker. The broker tier exists and is legitimate (and the NRS 645.863 permit is a genuine consumer protection worth knowing about), but it is built for Main Street deals, not licensed gaming operations. One nuance on the boutique bench: some out-of-town advisors, such as William & Wall (Scottsdale, AZ), operate — by their own disclosure — under the federal M&A-broker exemption (Exchange Act Section 15(b)(13), effective March 29, 2023), which exempts qualifying M&A brokers on private deals (target EBITDA under $25M / revenue under $250M) from SEC broker-dealer registration — antifraud rules still apply, and state registration is not preempted, so a Nevada nexus still matters. That is a legitimate model; just confirm which regime any advisor operates under. I run Peony, a data room company used by 5,900+ customers; whichever professionals you engage, the deal runs on a permissioned, staged data room — and the firm that has never built one is not the one selling your company.

Which "gaming advisor" names in Las Vegas are not actually M&A banks? A do-not-claim list

Las Vegas has a particularly rich set of names that get miscataloged as M&A advisors, because the gaming ecosystem is full of consultancies, research shops, and analysts who are genuinely expert — just not dealmakers. Here is the clearly-marked do-not-claim list: legitimate firms and people doing valuable work, but the wrong call for selling your operating company.

- Global Market Advisors — a Las Vegas gaming consultancy (feasibility studies, regulatory and licensing consulting, government affairs; a well-known voice is Brendan Bussmann), not an M&A investment bank. Superb for market studies and regulatory strategy; not who runs your sale.

- Regulus Partners — a research consultancy covering the global gaming sector, not a bank. Cite it for analysis, not for dealmaking.

- David Katz at Jefferies is a research analyst, not a banker. Jefferies genuinely runs gaming sell-sides through its Gaming, Lodging & Leisure investment-banking group — but do not name its sell-side research analyst as your dealmaker. This is a common and avoidable confusion.

- B. Riley — not a gaming specialist, and it was carved out (OTC: BRLY) in March 2025. Whatever general capabilities it retains, it is not the gaming-M&A specialist you want for a Nevada gaming sale.

And the single most important fact correction on this page, because it warps the geography of the whole market:

- Caesars Entertainment is headquartered in Reno, not Las Vegas (100 West Liberty Street), and it left the S&P 500 in September 2025 (it now sits in the S&P SmallCap 600). Caesars is the operator at the center of the marquee 2026 storyline, but it is not a Las Vegas-headquartered company, and a page that assumes it is has its map wrong.

Two clarifications that belong here because stale lists get them backwards. First, the persistent Union Gaming error: it was acquired by CBRE, not Macquarie — pull it up before you repeat it. Second, the best gaming banks being out of town is not a knock on them — CBRE Gaming (Vegas-native but inside a national firm), Macquarie (Los Angeles), and Innovation Capital (Los Angeles) are exactly who you want for a gaming sale; their office location is a rounding error next to their buyer relationships and licensing fluency. The point of the list is the sorting discipline: before you take a firm's pitch as a sell-side gaming advisor, confirm it actually runs gaming M&A (not consulting or research), that it can name three recent gaming closings with buyers identified, and that a specific senior banker will run your deal. Consultancies, research shops, and analysts fail that test fast.

Are Las Vegas's big companies actually buyers right now, and does the local economy help me sell?

Yes on both — Southern Nevada's economy is expanding and its gaming giants are active, though you have to read the corporate map carefully because the headline names sit in unexpected places. Start with the economy, because it feeds the non-gaming lower-middle-market directly. Clark County is roughly 2.42M people (2024, up about 2.1% year over year), driven by structural in-migration — about 53,200 California-to-Nevada moves in 2024 (Census state-to-state estimate), powered by no state income tax. In Q2 2026, Southern Nevada gaming revenue was up 7.4% and hotel occupancy ran 83.9%. And a historic capex wave is under construction: the Athletics' ballpark on the former Tropicana site (roughly $2B, 33,000 seats, about $400M spent, on schedule for ~April 2028), the Sphere ($2.3B), Allegiant Stadium ($1.9B), and F1 locked through 2037. That wave feeds a real lower-middle-market M&A pipeline in construction, the trades, food and beverage, and hospitality services — the non-gaming businesses that support the mega-projects.

Now the corporate map, with the 2025-list Fortune 500 ranks labeled by year (2026 ranks are unverified, so I omit them):

- MGM Resorts — #353 on the 2025 list — Las Vegas-based, a genuine gaming giant and, in its categories, an active strategic.

- Las Vegas Sands — #387 on the 2025 list — but read this one carefully: Sands sold the Venetian in 2022 and is now Asia-centric with no Strip presence, so despite the name it is not a Las Vegas operating buyer the way owners assume.

- Wynn Resorts — a Las Vegas-headquartered Fortune 500 member (I omit the exact rank as unverified). Note the live complication from the marquee storyline: Tilman Fertitta is also Wynn's largest shareholder, at more than 12%, even as his company pursues Caesars.

- Boyd Gaming and Golden Entertainment — both meaningful Nevada operators, but neither is a Fortune 500 company. Golden, as covered above, is the buyer engine on the branded-tavern side.

Two honest cautions. First, the marquee deals are not your comps and are not run by anyone on this page's local bench — they are bulge-bracket engagements (the Fertitta-Caesars ~$17.6B deal, the IGT/Apollo ~$6.3B deal, the Bally's/Standard General ~$4.6B deal). Second, Caesars is Reno-headquartered, not Las Vegas — the single most common corporate-geography error in this metro. For a seller, the takeaway is real: genuine strategic demand exists in gaming (from MGM, Wynn, Boyd, Golden, and the consolidators) and a genuinely booming lower-middle-market in the non-gaming support economy — but a licensed-gaming process still runs on the two-close, licensing-gated clock, and a non-gaming process still needs real buyer reach. Once buyers are in the room, page-level analytics will tell you which ones actually engaged past the teaser.

What is the live 2026 gaming M&A storyline, and what does it teach a smaller seller?

The live storyline is Tilman Fertitta's roughly $17.6B move on Caesars, and even though it is a mega-deal, it teaches a $5M-$500M seller everything about how Nevada gaming M&A actually works. Fertitta Entertainment agreed to acquire Caesars Entertainment for approximately $17.6B all-cash — including about $11.9B of assumed debt — at $31.00 per share, announced around May 28, 2026. Fertitta was already Caesars' largest shareholder at 12.1%. The deal has triggered suitability filings in every state where Caesars holds a license, the NGCB reviewed two Fertitta executives on July 8, 2026, a shareholder vote is expected later in 2026, and a potential close in mid-2027 — with approvals across all license states estimated at as long as 10 months. There is even a live conflict wrinkle: Fertitta is also Wynn Resorts' largest shareholder, at more than 12%, so his own suitability picture spans two major operators.

I want to be precise on two facts stale coverage gets wrong. The $17.6B figure includes the ~$11.9B of assumed debt — it is total enterprise value, not an equity check. And Caesars is headquartered in Reno, not Las Vegas (and left the S&P 500 in September 2025).

Three more 2024-2026 deals fill in the pattern, and each carries a structural lesson:

- Everi + IGT's Gaming & Digital business → Apollo (~$6.3B). A spin-then-combine structure: Everi holders received $14.25/share, the deal was announced February 29, 2024 (agreements July 26, 2024) and closed July 1, 2025, and the combined private company now operates as "IGT." Macquarie Capital and Deutsche Bank co-led the IGT side (2024 American Gambling Awards Dealmaker of the Year). Lesson: gaming deals use bespoke structures and take over a year sign-to-close.

- Bally's + Standard General (~$4.6B). A $18.25/share cash election with a rollover option — not a clean take-private: Bally's stayed public, combined with Queen Casino & Entertainment, and closed February 7, 2025, with Standard General (Soo Kim) at roughly 73.8%. Lesson: "acquisition" can mean many structures; read the mechanics.

- VICI's ~$1.16B sale-leaseback of seven Golden Entertainment casinos (closed April 30, 2026). The OpCo/PropCo split in action — real estate to the REIT, operations and license to Sartini's entity. Lesson: the license follows the operator.

What does all this teach a smaller seller? Three durable lessons. First, the regulator sits inside every deal — even the largest, most sophisticated buyers wait on suitability, so your deal will too; structure for it. Second, the sign-to-close gap is real and long — IGT/Apollo took over a year, Brightstar/PlayAGS took ~14 months, Fertitta/Caesars may take until mid-2027; a 90-day timeline is a fantasy for a licensed business. Third, structure is bespoke — spin-then-combine, cash-election-with-rollover, OpCo/PropCo split; a gaming-fluent advisor picks the structure that fits your situation, and a generalist will not know the menu. The mega-deals are not your comps, but they are your instruction manual.

Which virtual data room should a Las Vegas seller actually use?

I run a data room company, so treat this as informed but interested — and I will be honest about where each tool fits. For a true $500M-plus mega-deal with a bulge-bracket bank running the process, Datasite and Intralinks are the incumbents, and your banker may simply require one; their enterprise pricing typically starts around $50,000 or more per deal, which is rational at that scale and overkill below it. For the sub-$500M enterprise-value band that is the bulk of Las Vegas deal count — which is essentially every deal in this article, and certainly an $18M-revenue route or tavern sale — you do not need an enterprise mega-platform and should not pay for one. Peony, iDeals, and FirmRoom all run clean, secure, modern sell-side processes at a fraction of that cost.

What actually matters for a Las Vegas lower-middle-market gaming sale, where the buyer list is also the competitor list and the deal runs on a long, licensing-gated clock:

- Per-buyer permissions so consolidators and financial buyers see different tiers of information, staged as separate access groups in one room — essential for the tiered, confidential disclosure a small-industry gaming process requires.

- Dynamic watermarking so a leaked teaser, CIM, or location contract is traceable to the viewer who leaked it — critical when the likeliest bidders are the same operators you compete with and see at every gaming conference.

- An NDA gate so nobody sees the named CIM until the agreement is signed.

- Page-level analytics so you can see which buyers genuinely engaged (and which never opened the CIM), which sharpens your advisor's follow-up and your read on real interest — and which is doubly useful over a licensing timeline that can stretch a deal past a year.

- Pricing that does not punish you per page or per gigabyte — a document-heavy gaming diligence file (location contracts, license records, participation schedules) should not inflate the bill.

We serve more than 5,900 customers, many running exactly the kind of founder-owned and family-business sales this article is about, and Las Vegas's lower-middle-market gaming and non-gaming deals sit right in that band. For the full solution view, see our M&A data room solution. Whatever you choose, set the room up before you go to market — it is the cheapest lever you control, and over a licensing-gated timeline it is the one that most reliably keeps the regulatory and diligence clocks moving instead of stalling on missing documents.

Bottom line

In Las Vegas, every deal closes twice — once at signing, and once at the regulator. For any gaming-licensed business, the Nevada Gaming Control Board investigates and the Nevada Gaming Commission decides, you cannot close before Commission approval, and a full suitability investigation can take up to a year. That single fact — no other city in this series has it — reorganizes the entire advisor decision, timeline, and risk structure of your deal. The live 2026 proof is threading the system right now: Tilman Fertitta's ~$17.6B acquisition of Caesars (including ~$11.9B of assumed debt) is working through suitability hearings, with the NGCB having reviewed two Fertitta executives on July 8, 2026 and a potential close not until mid-2027; the earlier proof, Brightstar's ~$1.1B PlayAGS deal, cleared HSR in December 2024 but could not close until June 30, 2025 because it needed the Commission to license the buyer.

For an owner selling a real gaming business — a slot route, a tavern group, a casino, or a supplier — the practical bench is not what a stale local listicle suggests. The deepest gaming-M&A expertise sits at specialists who are mostly not in Las Vegas: CBRE Gaming (the Vegas-native former Union Gaming — acquired by CBRE, not Macquarie), Macquarie Capital (Los Angeles), Innovation Capital (Los Angeles), and the gaming groups at Houlihan Lokey and Jefferies — paired with a gaming attorney who manages the licensing spine. The thin Vegas-local generalist tier (Elmcore, CRD #158922, whose registered main office is actually Chicago; out-of-town boutiques like William & Wall) and the NRS 645.863 permitted business brokers serve the non-gaming and Main Street economy, not licensed gaming operations. The honest counters, held alongside the thesis: the marquee deals (Fertitta-Caesars ~$17.6B, IGT/Apollo ~$6.3B, Bally's/Standard General ~$4.6B) are bulge-bracket engagements, never local mandates; Global Market Advisors and Regulus Partners are consultancies, not banks; Caesars is headquartered in Reno, not Las Vegas. And on valuation, the honest answer beats a comforting one: there is no reliable public multiple for route and tavern-gaming businesses — anyone who quotes you a crisp "5-7x" without seeing your contracts is guessing, and the real number comes from a comparable-transaction analysis by a license-fluent advisor plus the competitive tension of a real process. Build a clean, staged data room before you go to market, choose a licensable buyer, file at signing, and structure for the two-close reality — in the one city where the regulator sits inside every deal, the sellers who win are the ones who plan for the second close from the first draft.

Frequently asked questions about Las Vegas M&A advisors

How does a change of ownership actually close for a Nevada gaming licensee?

It closes in two acts, and the second one is the regulator — which is why I say every Las Vegas deal closes twice. Nevada runs a two-tier structure: the Nevada Gaming Control Board (NGCB) is the investigative and enforcement arm, and its Investigations Division vets every buyer, key employee, and change-of-ownership applicant for suitability; the five-member Nevada Gaming Commission (NGC), appointed by the Governor to four-year terms, is the decision-maker that finally grants, denies, rejects, or conditions the license. The Board investigates and recommends; the Commission decides. The practical sequence for selling a gaming-licensed business is: negotiate and sign the purchase agreement, then file — the buyer (and its principals and key employees) applies for licensure or a finding of suitability, the Board's Investigations Division runs a deep background and financial-source investigation, the Board holds a hearing and makes a recommendation, and the Commission votes at a later hearing. You cannot close before Commission approval — the license does not transfer with the stock or assets on the signing date the way it would in an ordinary business sale. That is the single load-bearing fact stale advisor lists miss: the deal is not done when the lawyers sign; it is done when the Commission votes yes. Structure the agreement accordingly, with an outside date that respects the licensing calendar. I run Peony, a data room company used by 5,900+ customers, and a clean, staged room with page-level analytics is the cheapest lever you control while the regulatory clock runs.

How long does Nevada Gaming Control Board approval take when selling a gaming business?

Plan for months, and know that a full suitability investigation can take up to one year, per licensing-practice guides including the ICLG Gambling 2026 Nevada chapter — this is the timeline stale listicles never warn you about. The Board's Investigations Division runs an intensive background and source-of-funds review of the buyer and its principals; the depth of that review, not the complexity of your business, sets the clock. For scale, the Fertitta Entertainment-Caesars approvals across all of Caesars' license states have been estimated at as long as 10 months, and that is a sophisticated buyer with experienced gaming counsel. So for your own sale, do not assume a signed deal closes in the ordinary 60-to-90-day window — the licensing overlay sits on top of the normal M&A timeline. The realistic shape is: a normal sell-side runs about 6-9 months from engagement to signing, and then the gaming-licensing period sits between signing and close on top of that. The two levers that shorten it: pick a buyer who is already licensed in Nevada or has a clean multi-jurisdiction gaming record (a known applicant clears faster than a first-timer), and get the buyer's application filed the moment the deal signs rather than weeks later. An advisor who has run gaming deals will build the licensing calendar into the process from day one instead of discovering it at the LOI stage. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects a long-timeline deal — staged, permissioned disclosure — is the same whether the clock is 90 days or 12 months.

Will licensing delays kill my slot-route sale — and how do I structure around that risk?

Licensing delays rarely kill a well-structured deal, but they routinely kill a badly structured one — the risk is real and it is manageable, which is exactly why you want a license-fluent advisor and gaming counsel before you sign. The core structural move is to acknowledge in the purchase agreement that closing is conditioned on the buyer obtaining Nevada Gaming Commission approval, and to set an outside date (a drop-dead date) that gives the licensing process realistic room — often a year or more for a buyer who is not already licensed — rather than a 90-day fantasy that forces a renegotiation when the calendar slips. Other protections a good advisor and gaming attorney build in: interim-operating and management provisions so the business runs cleanly while the application is pending; a well-defined allocation of who bears the risk (and cost) if the buyer is found unsuitable; and choosing a buyer whose suitability is a low-risk question in the first place. The Brightstar-PlayAGS deal is the honest cautionary tale — it was agreed May 9, 2024, cleared HSR in December 2024, but could not close until the Commission licensed Brightstar's principals and AGS's CEO, so it closed June 30, 2025, a roughly 14-month sign-to-close gap driven largely by licensing. It closed because it was structured for the wait. That is the goal: not to eliminate the regulatory clock (you cannot) but to build the deal so the clock cannot break it. I run Peony, a data room company used by 5,900+ customers, and a well-organized room keeps the buyer's licensing team and the Board's investigators moving instead of waiting on documents.

Should I hire a gaming-specialist investment bank or a local Las Vegas business broker?

For a gaming-licensed business of real size — a slot route, a tavern-gaming group, a casino, or a gaming supplier — hire a gaming-specialist investment bank, and understand that most of them are not physically in Las Vegas. This is the counterintuitive truth of this metro: the deepest gaming-M&A expertise sits at firms like CBRE Gaming (the former Union Gaming, the Vegas-native franchise, now inside CBRE), Macquarie Capital's Consumer, Gaming and Leisure team (led by David Berman, primarily in Los Angeles), Innovation Capital (a Los Angeles mid-market gaming and leisure boutique), and the gaming coverage groups at Houlihan Lokey and Jefferies — not at a general Las Vegas business brokerage. A specialist earns its fee two ways a generalist cannot: it already knows the buyer universe by name (the consolidators, the strategics, the gaming-focused sponsors), and it understands the licensing overlay that makes gaming deals close on a different clock. Reach for a local Las Vegas business broker only for a small, non-gaming Main Street business (a restaurant without gaming, a services company, a retail operation) where the buyer pool is individuals and small operators, not institutions — and remember that in Nevada, brokering the sale of most businesses requires a Business Broker Permit under NRS 645.863, not just any real-estate license. If your business holds a gaming license, the sector fluency and buyer relationships of a gaming specialist beat local convenience every time. I run Peony, a data room company used by 5,900+ customers, and whichever you pick, a clean data room is the lever you control before you even sign an engagement letter.

Two consolidators already approached me — can I sell directly without an advisor?

You can, but for a licensed gaming business it is usually the most expensive shortcut you can take — the two consolidators who called are professional buyers who transact constantly, and you are a first-time seller negotiating without leverage or a market check. Selling directly to one of them means no competing bid, so you have no way to know whether the multiple on the table is generous or a lowball dressed up as a compliment ("we love your locations and want to move fast, just you and us"). An advisor's core job is to convert those inbound calls into a competitive process — quietly running the two who approached against each other and against other credible consolidators and sponsors, under NDA, so price is set by the market rather than by whoever called first. In distributed gaming specifically, the natural buyers are namable — J&J Ventures Gaming, Century Gaming, and the tavern consolidators — and a route-fluent advisor knows which of them is actually acquiring, at what multiples, and how to make them compete. The competitive tension typically moves the outcome by far more than the advisor's fee. An advisor also manages the licensing overlay — structuring the deal so the buyer's suitability review does not blow up the timeline — which a first-time seller negotiating solo will not see coming. If the offers are genuinely extraordinary and you have independently pressure-tested them, a full auction is not always mandatory, but at minimum get a license-fluent advisor or a strong gaming attorney to read the terms before you sign exclusivity. I run Peony, a data room company used by 5,900+ customers, and the discipline that protects you is the same whether one buyer called or five did.

How is a slot-route business valued — location contracts, participation splits, and all?

A slot-route (distributed-gaming) business is valued on the durability and transferability of its cash flow, which in turn rests on the things unique to the model: the location contracts (how many, how long the remaining terms, renewal and exclusivity provisions), the participation and revenue-split economics with each location, the machine count and mix, the space-lease-versus-participation structure, and — critically — whether the licenses and the location relationships survive a change of ownership. I want to be honest and precise here: there is no verified public multiple benchmark for route businesses, so the right answer is not a made-up "5-7x EBITDA" rule of thumb but a comparable-transaction analysis run by a license-fluent advisor who has actually seen where recent route and tavern-gaming deals cleared. Anyone who quotes you a crisp universal multiple for a route business without looking at your contracts is guessing. The real valuation work is: normalize EBITDA (adjust for owner comp, one-time items, and the true economics of each location), assess contract-renewal risk and location concentration, model the participation splits, and then triangulate against genuinely comparable recent transactions the advisor can point to. Buyer diligence will focus on exactly those points — contract assignability, license transferability, location concentration, and the machine base — so the valuation and the diligence file are two sides of the same coin. I run Peony, a data room company used by 5,900+ customers, and organizing location contracts, license records, and participation schedules into a clean, permissioned room is what lets an advisor build a defensible value story and a buyer confirm it.

What EBITDA multiple do Nevada route and tavern-gaming businesses sell for?