12 Consumer Capital Partners for Independent Sponsors in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

We run Peony, a data room platform. Consumer and CPG independent sponsor deals sit at a specific inflection point in 2026: broader consumer M&A multiples hit a 10-year low in 2025, but sub-sectors (pet, beauty, outdoor, better-for-you food) are trading at premium multiples with real dry powder chasing founder-led brands. Consumer industry deals fell 18.9% year-over-year in 2025 while tactical products rebounded +54.3%, outdoor recreation +47.7%, and vitamins and supplements +30% (Capstone Partners Annual Consumer M&A Report, 2025). This is the market where independent sponsors can source founder-led brands at reasonable multiples without competing with mega-cap PE.

The challenge is that most consumer capital partners look nothing like a healthcare PE firm or a tech-software sponsor. You are not pitching a vertical SaaS with 112% NRR. You are pitching a $9M-revenue artisanal hot-sauce company with a single co-manufacturer, two distributor relationships, a trademark that was never filed in Canada, an Amazon ACOS that spiked after the last seasonal reset, and a founder who signs the checks for every slotting fee. The capital partner has to underwrite brand defensibility, co-manufacturer capacity, retailer concentration, trademark portfolio, and founder succession simultaneously. Generic "industry-agnostic" PE firms that back manufacturing or services rollups are not the right partner here.

This guide maps 12 verified capital partners actively funding consumer IS deals in 2026 -- consumer-focused PE co-investors, flexible structured-capital shops, and SBICs that write checks for branded CPG, food and beverage, pet, beauty, outdoor, and specialty consumer services platforms in the lower middle market. Every firm listed is real, verified, and actively deploying capital. For the foundational IS mechanics (deal economics, capital assembly, exclusivity windows), see our complete independent sponsor guide. I spent years evaluating consumer deals at Target Global before starting Peony, and the consumer IS diligence stack below is the one I would run on my own capital.

TL;DR: Consumer M&A is in selective recovery in 2026 -- broader multiples at a 10-year low, but premium sub-sectors trading at real dry powder. Consumer industry EV/EBITDA multiples hit 9.2x median in 2025, the lowest in 10 years of Capstone tracking, with PE paying 10.4x versus strategics at 8.6x (Capstone Partners Annual Consumer M&A Report, 2025). Beauty and personal care commands 14.9x EV/EBITDA average through YTD 2025 -- five turns above the broader consumer industry average of 9.8x (Capstone Partners Beauty M&A Update, December 2025). Pet sector EBITDA multiples averaged 14.5x from 2022 through YTD 2025, though H1 2025 PE median compressed to 12.2x from 16.8x in 2024 (Capstone Partners Pet Sector M&A Update, March 2026). Food and beverage M&A is pacing toward $120 billion in annual deal value in 2025 despite PE deal count falling about 20% year-over-year (PitchBook Q3 2025 Food & Beverage CPG Report). Four major consumer-focused funds closed in 12 months -- VMG Fund VI at $1B (May 2025), Monogram Fund III at $350M (November 2025), CAVU Fund V at $325M (February 2026), Topspin Fund III at $328M (April 2026) (VMG, PRNewswire / Monogram / CAVU, GlobeNewswire / Topspin). 777 Consumer Goods Independent Sponsors are active on Axial, and independent sponsors closed 26.8% of all Axial deals YTD 2025 -- outpacing PE funds at 21.1% (Axial 2025 Independent Sponsor Report). 54% of IS transactions still close at 4x-6x EBITDA (Citrin Cooperman 2025 IS Report) -- a multiple floor below the consumer median that is the core IS opportunity in consumer. Below: 12 capital partners funding these deals, sub-sector multiples, the Highlander NiTEO and Consortium brand-roll-up templates, and what consumer capital partners actually need in your data room.

Why Consumer Is a Selective But Durable Vertical for Independent Sponsors in 2026

Four structural forces converge in 2026 to make consumer a compelling but selective IS target sector in the lower middle market:

Consumer Multiples Hit a 10-Year Low, Opening IS Entry Points

The 2025 broader consumer market is the cheapest it has been in a decade. Capstone Partners reports consumer industry EV/EBITDA multiples at 9.2x median in 2025, the lowest since they began tracking the data 10 years ago. PE buyers paid a premium at 10.4x median versus strategic buyers at 8.6x, with the spread expanding year-over-year (Capstone Partners, 2025). Consumer industry deal count fell 18.9% year-over-year in 2025, a third consecutive year of declines (2022: -9.6%, 2023: -29.6%, 2024: +8.6%). For IS sponsors, this multiple compression plus the 4x-6x EBITDA IS multiple floor creates an entry window that was not available during 2021-2022 consumer frothiness. The 54% of IS transactions still closing at 4x-6x per Citrin Cooperman 2025 sit more than three turns below the PE-buyer consumer median.

Sub-Sector Rebounds in Pet, Beauty, Outdoor, and Better-For-You

While the broader consumer market is down, specific sub-sectors are posting strong growth. Tactical products rebounded +54.3% YoY in 2025, outdoor recreation and enthusiasts +47.7% YoY, vitamins and supplements +30% YoY (Capstone Partners, 2025). Beauty and personal care M&A multiples averaged 14.9x EV/EBITDA YTD 2025 -- five turns above the broader consumer average of 9.8x (Capstone Partners Beauty M&A Update, December 2025). Pet sector EBITDA multiples averaged 14.5x from 2022 through YTD 2025 (Capstone Partners Pet Sector M&A Update, March 2026). The sub-sector spread is the core value-creation mechanism: IS sponsors sourcing a 4x-6x founder-led branded food platform can build toward a 10x-14x exit multiple as the platform scales into premium sub-categories.

Record Consumer-Focused PE Fund Closes Signal Real Dry Powder

Four major consumer-focused funds closed in a 12-month window, explicitly targeting lower-middle-market branded consumer: VMG Partners Fund VI at $1 billion in May 2025 (VMG, PRNewswire), Monogram Capital Fund III at $350 million oversubscribed in November 2025 (Monogram, PRNewswire), CAVU Consumer Partners Fund V at $325 million in February 2026 (CAVU, GlobeNewswire), and Topspin Consumer Partners Fund III at $328 million oversubscribed in April 2026 (Topspin). Aggregate consumer-focused dry powder available for lower-middle-market deployment is at multi-year highs. Financial buyer dry powder for outdoor recreation alone reached $1.9 trillion in 2025 (Capstone Outdoor Recreation Market Update). For IS bringing a proprietary $3M-$10M EBITDA consumer brand deal, the capital partner side of the stack is not the constraint in 2026 -- deal sourcing and brand defensibility are.

Independent Sponsors Now Dominate Consumer Deal Flow

Independent sponsors account for 26.8% of all closed deals on Axial year-to-date in 2025, outpacing Private Equity Funds at 21.1% and every other buyer type (Axial 2025 Independent Sponsor Report). Axial has 777 Consumer Goods Independent Sponsors with recent deal activity (Axial Consumer Goods Directory). The IS structure -- deal-by-deal capital raises, carry on each deal, no fund management fees -- is particularly well-suited to consumer where sub-sector expertise (a sponsor who knows pet, beauty, or specialty food deeply) matters more than generalist portfolio diversification. The Citrin Cooperman 2025 IS Report also shows 54% of IS transactions still closing at 4x-6x EBITDA, down from 64% the prior year -- meaning IS sponsors are stretching into higher-quality assets but the multiple floor remains structurally below the consumer PE median.

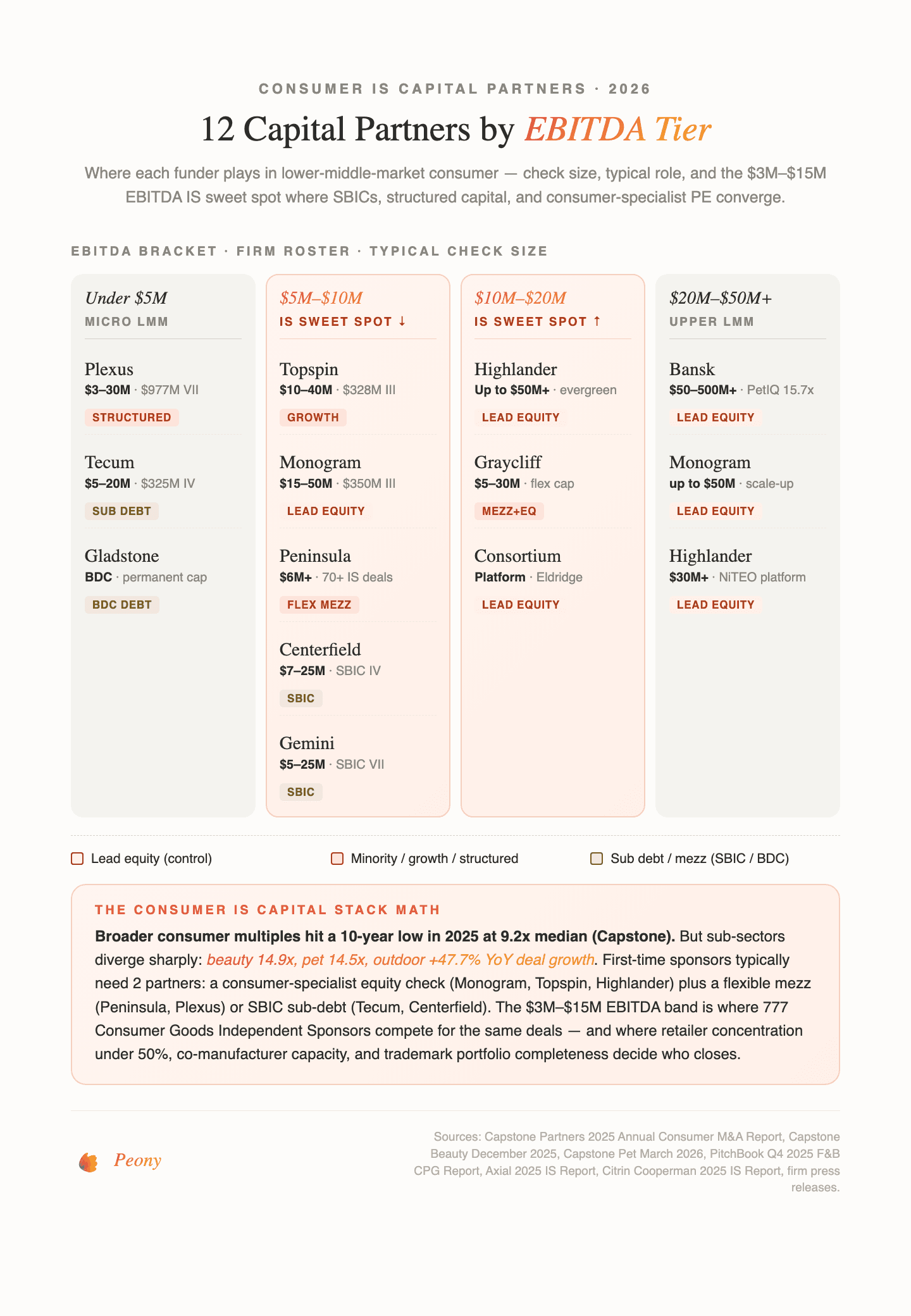

The 12 Capital Partners Funding Consumer Independent Sponsor Deals in 2026

Below is a quick-reference map of the 12 capital partners actively funding consumer IS deals in 2026, organized by role (consumer-focused PE, flexible structured capital, and SBIC sub-debt providers). Every firm has been verified against 2024-2026 deal activity and check-size guidance. For data room setup ahead of capital partner outreach, Peony Data Room at $52/admin/month handles the consumer-specific document mix out of the box.

| Firm | Website | Check Size | EBITDA Sweet Spot | Consumer Sub-Sector Focus |

|---|---|---|---|---|

| Monogram Capital Partners | monogramcapital.com | $15M-$50M equity | $5M-$25M | Food and beverage, beauty, pet, consumer services |

| Topspin Consumer Partners | topspincp.com | $10M-$40M | $3M-$15M | Health and wellness, beauty, F and B, pet, household |

| Highlander Partners | highlander-partners.com | Mezz/equity to $50M+ | $5M-$30M | Branded CPG, food, household, specialty retail |

| Consortium Brand Partners | cbpinvests.com | Platform-level | $5M-$40M | Specialty retail, apparel, home, restaurant |

| Bansk Group | banskgroup.com | $50M-$500M+ | $10M-$75M | Beauty, consumer health, F and B, household |

| Peninsula Capital Partners | peninsulafunds.com | $6M+ flexible | $3M+ | Branded CPG, specialty food, packaging, retail-adjacent |

| Plexus Capital | plexuscap.com | $3M-$30M | $2M-$20M | Food service, branded food, consumer distribution |

| Graycliff Partners | graycliffpartners.com | $5M-$30M | LMM | Niche manufacturing and value-added consumer distribution |

| Tecum Capital | tecum.com | $5M-$20M | $3M+ | Branded consumer, specialty food, fragrance CM (SBIC) |

| Centerfield Capital | centerfieldcapital.com | $7M-$25M | $3M-$15M | Branded CPG food, specialty retail, consumer (SBIC) |

| Gemini Investors | gemini-investors.com | $5M-$25M | $3M-$15M | Consumer products and services, specialty (SBIC) |

| Gladstone Investment (GAIN) | gladstoneinvestment.com | Flexible BDC | $4M-$15M | Consumer products, branded consumer goods (BDC) |

Tier 1 -- Consumer-Focused PE That Co-Invests with Independent Sponsors

These firms actively co-invest in consumer IS deals or operate as consumer-focused platforms. Each has a verified 2024-2026 track record deploying capital into branded CPG, food and beverage, pet, beauty, and specialty consumer services acquisitions in the lower middle market.

Monogram Capital Partners

Website: monogramcapital.com | Fund III: $350M (November 2025, oversubscribed) | HQ: Los Angeles

Monogram Capital Partners closed Fund III at $350 million hard cap (oversubscribed) in November 2025, bringing total AUM to approximately $1.75 billion (Monogram, PRNewswire). The firm invests $15M-$50M of equity in four consumer verticals: food and beverage, beauty and personal care, pet, and consumer and business services. Recent 2025-2026 deals include the Western Smokehouse Partners reacquisition (2025, 39th investment -- premium meat-snack contract manufacturer), the Luckyscent acquisition (January 2025 -- niche fragrance e-commerce), and portfolio company OLIPOP valued at $1.85B. Monogram's portfolio has achieved approximately 3x revenue growth and 600+ bps EBITDA margin expansion across investments 5+ years old.

Why it matters for IS: Monogram's four-vertical consumer focus with an IS-friendly $15M-$50M check and $5M-$25M EBITDA sweet spot makes them one of the most IS-accessible consumer-specialist PE firms in the market. They will back founder-led supply-chain consumer infrastructure -- like contract manufacturers and specialty ingredient platforms -- which is exactly the profile IS sponsors source proprietarily without having to compete with DTC growth equity. Fund III fresh dry powder means active deployment through 2027.

Topspin Consumer Partners

Website: topspincp.com | Fund III: $328M (April 15, 2026, oversubscribed) | HQ: Great Neck, NY

Topspin Consumer Partners closed Fund III at $328 million hard cap (oversubscribed, $250M target) on April 15, 2026 (Topspin) -- the freshest consumer-specialist capital in the market. Total AUM is approximately $830 million. Topspin writes $10M-$40M checks into companies with $3M-$15M EBITDA across health and wellness, personal care, beauty, food and beverage, household goods, pet, and consumer value-chain services. Recent portfolio activity includes Grid (premium lockers/flooring for fitness and health) and broader high-loyalty consumer brands. Topspin takes minority or growth-oriented positions and can lead in LMM deals.

Why it matters for IS: The $328M Fund III close one week before this post means Topspin has deeper dry powder than nearly any other consumer-focused shop in the LMM. Their minority-friendly profile works perfectly for IS sponsors who want to keep operating control while bringing in growth capital. The "high-loyalty" thesis (care/wellness/pet/outdoor) aligns with defensive consumer IS roll-ups -- exactly the sub-sectors where 2025-2026 deal flow is concentrated. For a first-time IS on a $4M-$8M EBITDA founder-led consumer brand, Topspin is a first-call equity co-invest partner.

Highlander Partners

Website: highlander-partners.com | Capital: Evergreen family-office-style (no LP structure) | HQ: Dallas

Highlander Partners operates as evergreen family-office-style capital with $3B+ reported AUM (Tracxn) -- no LPs, no fund-cycle pressure, faster decision cycles. The firm writes mezz and equity checks up to $50M+ for $5M-$30M EBITDA branded consumer platforms. Recent 2025-2026 deals include Tapatio Hot Sauce acquired from the Saavedra family (January 2026 -- #5 US hot sauce brand), portfolio company NiTEO Products acquiring Faultless Brands (December 2025 -- Faultless, Niagara, Magic, Bon Ami), Ergo Baby from Compass Diversified (December 2024), and SFERRA Fine Linens acquiring Antica Farmacista (2024-2025). Highlander takes control-preferred positions with flexibility on structure.

Why it matters for IS: Highlander is one of the few PE firms actively doing direct consumer branded platform acquisitions in the lower middle market without the LP-reporting overhead. Their roll-up playbook is institutional: NiTEO is a household and automotive brand platform that keeps adding bolt-ons (Faultless is the 4th major acquisition). For an IS with an $8M-$20M EBITDA founder-led branded CPG platform and a bolt-on thesis, Highlander is a realistic lead-equity or mezz partner who can write checks at IS speed.

Consortium Brand Partners

Website: cbpinvests.com | Capital: Evergreen consumer brand platform (Eldridge-backed) | HQ: New York

Consortium Brand Partners operates as an evergreen consumer brand investment platform backed by Eldridge Industries, taking control buyer positions while partnering with operator partners (Aurify, Convive Brands) on specific platforms. The firm has completed 4 consumer brand platform investments over roughly 5 years. Recent deals include California Pizza Kitchen (December 2025, alongside Eldridge, Aurify Brands, Convive Brands -- CBP's 4th acquisition) (BusinessWire), Outdoor Voices, Jonathan Adler, and Draper James. CBP targets $5M-$40M EBITDA platforms.

Why it matters for IS: Consortium is a rare post-2020 consumer brand platform actively consolidating distressed and orphan consumer brands (apparel, home goods, restaurant). For IS sponsors with a mature founder-led brand at $5M-$15M EBITDA needing operating muscle and capital, CBP is an end-game partner. Their cross-category exposure (apparel to home to restaurant) signals comfort with branded consumer that doesn't fit neatly in any single PE sector box.

Bansk Group

Website: banskgroup.com | Capital: $1.5B+ deployed (founded 2019) | HQ: New York

Bansk Group is a consumer-focused PE firm that has deployed $1.5B+ in single-check consumer deals since its 2019 founding. The firm writes $50M-$500M+ checks in companies with $10M-$75M EBITDA across beauty, consumer health, food and beverage, and household products. The flagship recent deal was the PetIQ take-private at $1.5B in October 2024 -- 15.73x EV/EBITDA and 1.25x EV/revenue (GlobeNewswire), signaling their appetite for pet health platforms at premium multiples. Bansk takes control positions.

Why it matters for IS: Bansk is more often an exit buyer than an IS co-invest partner at the earliest stages -- their $10M+ EBITDA floor puts them out of reach for first-time IS deals. But for IS running a $20M+ EBITDA consumer health or household care platform ready for second-bite or scaled exit, Bansk is a realistic path to a premium multiple. The PetIQ 15.73x exit multiple is the kind of outcome that IS sponsors should model as the high end of a multi-year roll-up thesis.

Tier 2 -- Flexible Structured Capital (The IS Specialists)

These firms provide structured capital -- mezz, minority equity, preferred stock -- explicitly designed for independent sponsor deal-by-deal flexibility. For consumer IS sponsors, the mezz layer is often where the capital stack gets assembled or falls apart.

Peninsula Capital Partners

Website: peninsulafunds.com | Capital: $2.4B raised across 8 partnerships, 150+ platforms, 70+ IS deals | HQ: Detroit

Peninsula Capital Partners is arguably the single most IS-friendly lower-middle-market credit and equity shop in the country, with 70+ independent sponsor platform deals across its history (Peninsula Funds overview PDF). The firm provides mezz plus minority or majority equity with $6M+ flexible check sizes in companies with $3M+ EBITDA. Recent consumer deals include Wisconsin's Best (branded cheese and meat snacks CPG with e-commerce), Specialized Packaging Group (consumer product packaging for P&G, Unilever, Colgate-Palmolive), Foodhandler (food-service branded disposables), and Dart Casting. Peninsula can be minority or majority, deal participant or sponsor.

Why it matters for IS: With 70+ IS platforms over their history, Peninsula is self-described pioneer in IS-structured capital. Will write mezz + equity in the same transaction for consumer IS sponsors needing flexible capital stack. For an IS on a $10M-$25M EV branded consumer deal where the mezz layer is the sticking point between senior debt and sponsor equity, Peninsula is the first call -- and often the only one needed.

Plexus Capital

Website: plexuscap.com | Fund VII: $977M Structured Capital Fund | HQ: Raleigh, NC

Plexus Capital Fund VII closed at $977 million in structured capital explicitly designed to support independent sponsors, search funds, and equity funds (Plexus Capital strategy). The firm provides debt and equity co-invest of $3M-$30M in companies with $2M-$20M EBITDA on non-control terms. Recent consumer deals include the Food Evolution LLC acquisition with Akoya Capital and Balance Point Capital -- gourmet fresh-prepared sandwiches, wraps, salads for retail, food-service, airports, and universities (Akoya Capital press release). Plexus is explicitly non-control.

Why it matters for IS: Plexus is one of the most explicit "we-back-IS" structured capital shops in the country. Fund VII is nearly $1B in dry powder earmarked for IS, search funds, and minority deals. Food Evolution shows active consumer sub-sector deployment in 2024-2025. For an IS running a $3M-$8M EBITDA specialty food or consumer distribution deal where the capital stack needs structured mezz plus minority equity rather than control equity, Plexus has the mandate and the fund size to deploy.

Graycliff Partners

Website: graycliffpartners.com | Capital: Active in LMM since 1991 | HQ: New York (with Latin America capability)

Graycliff Partners writes $5M-$30M checks of equity or mezzanine across LMM niche manufacturing, business services, and value-added distribution including consumer-adjacent subsectors. Active since 1991, Graycliff is listed in IS-friendly capital partner directories and maintains flexible capital structures.

Why it matters for IS: Flexible capital shop that will write equity or mezz behind IS deals. For consumer IS deals that sit at the branded-consumer-plus-industrial-distribution boundary (private-label manufacturers, specialty ingredient distributors, co-packers), Graycliff's distribution fluency and willingness to go either minority-equity or mezz makes them one of a handful of LMM shops that fits cleanly into a $15M-$30M EV consumer IS capital stack.

Tier 3 -- SBIC / Mezz / Sub-Debt with Consumer Allocation

SBICs and sub-debt providers fill the debt side of consumer IS capital stacks. With SBA-leveraged capital, SBICs offer more flexible terms than traditional bank lenders -- particularly valuable for branded consumer where senior lenders cap advance rates on inventory-heavy borrowing bases. Four of the most consumer-active SBIC and sub-debt capital partners:

Tecum Capital

Website: tecum.com | Fund IV: $325M SBIC (February 2025) | HQ: Pittsburgh

Tecum Capital Partners IV launched in February 2025 at $325 million -- the firm's fourth SBIC-licensed fund (Tecum Capital, PRNewswire). Tecum provides mezzanine debt and minority equity of $5M-$20M in businesses with EBITDA greater than $3M. Consumer-sector anchors include Shake Smart Holdings (healthy fast-casual), Marcy Laboratories (contract manufacturing for fragrance brands -- pick-and-shovel CPG), and CM Industries (branded welding consumables). The 74-company portfolio includes meaningful consumer exposure.

Why it matters for IS: Tecum is a workhorse SBIC for IS sponsors on sub-$15M EBITDA consumer deals. Fresh $325M Fund IV plus a consumer-active portfolio (Shake Smart, Marcy Laboratories) means real deployment appetite. The Marcy Laboratories deal especially signals willingness to back consumer supply-chain infrastructure -- an IS-friendly niche because the deals are less brand-dependent and more operationally defensible.

Centerfield Capital Partners

Website: centerfieldcapital.com | Fund IV: Active SBIC | HQ: Indianapolis

Centerfield Capital Partners provides SBIC sub-debt plus equity co-invest of $7M-$25M in companies with $3M-$15M EBITDA -- a precise match for the IS sweet spot. Recent consumer deals include Honey Smoked Fish (2025, Denver -- branded ready-to-eat fish products), Indigo Wild (2018, Kansas City -- bath, skin, and home products), Indo~European Foods (ethnic specialty foods, Glendale), and Hunter's Specialties (hunting accessories).

Why it matters for IS: Centerfield's $3M-$15M EBITDA range precisely matches the IS sweet spot for founder-led branded consumer. The Honey Smoked Fish 2025 deal signals active branded-CPG deployment. Like Tecum, Centerfield writes sub-debt behind IS equity for founder-led consumer acquisitions where the IS sponsor retains operating authority while picking up SBA-leveraged debt at flexible terms.

Gemini Investors

Website: gemini-investors.com | Fund VII: Active SBIC | HQ: Wellesley, MA

Gemini Investors operates as an SBIC writing sub-debt and equity co-invest of $5M-$25M in lower-middle-market consumer products and services targets. Fund VII is currently investing (PitchBook). Recent consumer deals include Tablescapes (event rental services, August 2024) and Winterberry Gardens (landscaping and irrigation services, October 2024). Gemini was named SBIC of the Year at the inaugural 2009 award.

Why it matters for IS: Long-standing consumer-services portfolio including event rental and landscaping -- exactly the kind of "consumer-adjacent services" that IS sponsors like to roll up when a pure branded CPG deal is not sourceable. Non-control minority structure preserves IS operating authority.

Gladstone Investment Corporation (GAIN)

Website: gladstoneinvestment.com | Capital: Publicly traded BDC (permanent capital) | HQ: McLean, VA

Gladstone Investment (NASDAQ: GAIN) is a publicly traded Business Development Company providing senior secured debt, subordinated debt, and equity with BDC flexibility in companies with $4M-$15M EBITDA (GAIN portfolio). Consumer portfolio anchors include Brunswick Bowling Products (full-line bowling center equipment and consumer bowling products) plus a diversified consumer products portfolio. Permanent capital means no fund-cycle pressure.

Why it matters for IS: Permanent-capital BDC means Gladstone can hold consumer platforms indefinitely -- no forced exit pressure at year 5 or year 7. $4M-$15M EBITDA range is squarely the IS zone. Active in consumer products at the smaller end where most IS sponsors source deals. For an IS who wants a capital partner who will let a branded consumer platform compound beyond the typical PE hold period, Gladstone is uniquely positioned.

Sub-Sector Multiples: How Consumer IS Deals Are Priced in 2026

Consumer and CPG multiples vary more than any other IS sector except tech/software because the category spans branded food, beauty, pet, outdoor, household, and specialty services -- each with distinct economic profiles. The 2025-2026 ranges we see on Peony data rooms and in published market data:

| Sub-sector | Revenue multiple | EBITDA multiple | Source |

|---|---|---|---|

| Consumer industry median (all sub-sectors) | -- | 9.2x (2025, 10-year low) | Capstone Partners |

| Branded CPG food and beverage ($1-3M EBITDA) | -- | 6.8x | Windsor Drake LMM 2025 |

| Branded CPG food and beverage ($3-5M EBITDA) | -- | 8.1x | Windsor Drake LMM 2025 |

| Branded CPG food and beverage ($5-10M EBITDA) | -- | 9.0x+ | Auxo Capital Advisors, 2025 |

| Pet products and services | -- | 14.5x (2022-YTD 2025 avg); 12.2x (H1 2025 PE) | Capstone Pet Update March 2026 |

| Beauty and personal care (mass + prestige) | -- | 14.9x avg YTD 2025 | Capstone Beauty December 2025 |

| Outdoor and lifestyle brands | -- | 9.2x industry median; premium platforms 12.5x | Capstone Annual Consumer M&A 2025 |

| Specialty retail (general) | -- | 4-8x LMM; mid-teens for scaled platforms | IB Interview Questions 2025-2026 |

| Consumer services (franchises, home services) | -- | 3-8x founder-led; mid-teens PE platforms | KPMG Home Services Fall 2025 |

Roll-up math for branded consumer platforms: Acquire founder-led brands at 4x-6x EBITDA (the IS multiple floor), integrate into a multi-brand platform with shared co-manufacturing and retail relationships, exit at 9x-14x EBITDA depending on sub-sector premium. Beauty and pet are the highest-premium sub-sectors (14.9x and 14.5x averages respectively), while generic household and specialty retail compress to 4x-8x for founder-scale platforms.

Retailer concentration is the single biggest price-chip source in CPG diligence. Any single retailer representing more than 30% of revenue triggers material working-capital and risk-premium adjustments. Target portfolios with the top-3 retailers under 50% of revenue and the top 10 under 70%. Co-manufacturer concentration compounds the risk: brands with a single co-manufacturer and no qualified backup face 10-15% multiple compression during diligence.

The NiTEO / Consortium / Monogram Roll-Up Templates (Consumer IS Playbooks)

Unlike tech/software where Evergreen Services Group provides a single dominant roll-up template, consumer IS has three distinct playbooks worth studying:

Template 1: The Highlander / NiTEO Household-Brand Roll-Up

NiTEO Products (Highlander Partners portfolio) is a formulator, packager, and marketer of household and automotive chemical brands. In December 2025, NiTEO acquired Faultless Brands, adding Faultless, Niagara, Magic, and Bon Ami to a platform already containing multiple household brands (PRNewswire, December 2025).

Why it's a template: Specialty household-chemical sub-sector is fragmented, founder-owned, modest EBITDA per brand, with a heavy retail-distribution moat. Highlander provides capital and operational scale; NiTEO executes bolt-on acquisitions of 3-5 brands over 3-5 years. For an IS with household or automotive-chemical sub-sector expertise, this is the closest thing to an "Evergreen Services Group of consumer" -- a multi-brand branded platform with disciplined bolt-on cadence.

Template 2: The Consortium Brand Platform

Consortium Brand Partners has completed 4 consumer brand platform investments over roughly 5 years -- Outdoor Voices, Jonathan Adler, Draper James, and California Pizza Kitchen (December 2025 with Eldridge, Aurify, and Convive Brands) (BusinessWire, December 2025).

Why it's a template: CBP rolls up distressed or orphan consumer brands across apparel, home, and restaurant. For IS sponsors, this is the "consolidate founder brands needing operating muscle" template with cross-category exposure. Partners with operating brand builders (Aurify, Convive) on specific platforms rather than trying to operate every brand internally -- a model an IS sponsor could replicate at smaller scale by partnering with a single operator per sub-category.

Template 3: The Monogram Supply-Chain Pick-and-Shovel

Monogram Capital has made 39 investments to date with a "scale supply chain partners for the fastest-growing food and beverage brands" thesis. Western Smokehouse Partners is a premium meat-snack contract manufacturer that Monogram reacquired in 2025 (PRNewswire, 2025).

Why it's a template: Pick-and-shovel consumer roll-up -- buy co-manufacturers and contract packers serving hot consumer brands rather than taking brand risk directly. For IS sponsors who want consumer-sector exposure without the consumer-brand operational complexity, this is the template: acquire a specialty co-manufacturer, add capacity and customer diversification, compound through adding 2-3 bolt-ons.

IS sponsors cannot replicate these at the scale Highlander, CBP, or Monogram operate. But the mechanics -- vertical focus, platform economics before add-on velocity, disciplined retailer relationships -- travel down-market. Our LOI playbook covers the capital-assembly mechanics that make branded consumer roll-ups possible at IS scale.

Consumer-Specific Due Diligence Requirements Capital Partners Expect in 2026

Consumer diligence is structurally different from tech/software or manufacturing diligence because the assets are brand equity, retailer relationships, and co-manufacturer capacity, and the risks are mostly commercial (retailer concentration, category dynamics, distribution loss) rather than technical. Based on hosting hundreds of consumer IS data rooms on Peony, here is what 2026 capital partners expect -- organized for the staged diligence approach in our complete IS guide and IS data room checklist. Set up your data room on day one of the exclusivity window.

Retailer Concentration and Scorecards

Retailer concentration is the single biggest driver of consumer deal multiples. Capital partners expect a complete retailer-by-retailer breakdown with dollar revenue, unit velocity, on-shelf availability, reset history, and any Nielsen or SPINS third-party data. Top-3 retailer concentration above 50% triggers material working-capital and risk adjustments. Top-10 concentration above 70% is a yellow flag. Provide 3-year retailer scorecards showing shelf space expansion or contraction trends, slotting fee amortization, trade spend reconciliation, and promotional effectiveness.

Co-Manufacturer Agreements and Capacity

Co-manufacturer concentration is the second-biggest operational risk. Capital partners expect every co-manufacturer agreement with capacity commitments, change-of-control language, exclusivity clauses, quality audit history, and pricing escalators. Brands with a single co-manufacturer and no qualified backup face material multiple compression during diligence because post-close capacity loss can take 12-18 months to rebuild. Provide co-manufacturer capacity utilization reports and any qualified-backup manufacturer relationships already in place.

Trademark Portfolio and IP Assignments

Trademark registrations in all primary markets are non-negotiable -- USPTO for US, CIPO for Canada, EUIPO for EU, INPI for Brazil, and registration in any DTC-served geography. Capital partners expect a complete trademark portfolio audit with any opposition proceedings or oppositions-in-progress flagged. Domain names, social handles, and licensing agreements with clean chain of title should be documented. Missing secondary-market trademark registrations (particularly Canada and UK for US brands with DTC traffic from those markets) are the most frequent consumer M&A red flag because they trigger launch delays or infringement risk in expansion theses.

Amazon and DTC Velocity

For consumer brands with meaningful Amazon or DTC revenue, capital partners expect detailed velocity data: ACOS (advertising cost of sales), ROAS (return on ad spend), category rank trends, Amazon Seller Central or Vendor Central performance metrics, and a 3-year trend of organic versus paid revenue share. DTC brands should provide LTV/CAC cohort analysis, retention rates, and subscription versus one-time purchase mix. Sudden ACOS spikes or category rank declines are material red flags.

FDA, FD&C, and Sustainability Compliance

Branded food, dietary supplement, and beauty/personal-care targets require compliance documentation: FDA food registrations, 510(k) clearances if applicable, FD&C compliance files for cosmetics, state TTB licenses for alcohol, any outstanding consumer complaints or class-action exposure, and sustainability certifications (Fair Trade, USDA Organic, Non-GMO, Leaping Bunny, etc.) where the brand's positioning depends on them. Any compliance gaps or pending FDA warning letters materially impact multiples.

Founder Succession and Key Employee Retention

Founder-led consumer brands have a specific succession risk: the founder often is the brand's key relationship with retailers, distributors, and co-manufacturers. Capital partners expect a founder transition plan, key employee retention analysis with proposed stay bonus pool, and any outstanding equity grants or earn-outs. A founder exiting immediately at close without a 12-24 month transition agreement is a material red flag for any branded consumer deal.

For the complete 174-document due diligence data room checklist applicable across all deal types, see our cluster guide.

Peony Data Room at $52/admin/month includes AI auto-indexing that organizes all of these consumer-specific documents into a professional folder structure in under 3 minutes. The AI-powered Smart Q&A workflow lets capital partners ask questions like "What is the top-10 retailer concentration?" or "What is the Amazon category rank trend?" and get cited answers with exact page numbers -- the sponsor reviews and approves before any response is sent. Advanced Redaction on Peony Deal Team identifies PII, supplier pricing, and confidential formulations across uploaded documents before you share with capital partners, a workflow that Datasite charges $25K+ per deal to configure manually.

Where to Meet Consumer IS Capital Partners in 2026

Consumer and CPG IS outreach has a different rhythm than manufacturing or tech/software. The best sourcing happens at a mix of IS-specific conferences and consumer-category trade shows where targets (not just capital partners) congregate. Events happening AFTER April 22, 2026:

| Event | Date | Location | Organizer |

|---|---|---|---|

| ACG DealMAX (InterGrowth rebrand) | April 27-29, 2026 | Las Vegas | ACG Global |

| SBIA Independent Sponsor Forum | May 6, 2026 | Sheraton Philadelphia Downtown | SBIA |

| iGlobal Independent Sponsor Summit Dallas | June 11, 2026 | Dallas | iGlobal Forum |

| Cosmoprof North America (beauty) | July 2026 | Las Vegas | Cosmoprof |

| SuperZoo (pet) | August 2026 | Las Vegas | WPA |

| Natural Products Expo East | September 2026 | Philadelphia | New Hope |

| iGlobal Independent Sponsor Summit NYC | September 28-29, 2026 | New York | iGlobal Forum |

| Outdoor Retailer | Summer/Winter 2026 | Salt Lake City | Outdoor Retailer |

| McGuireWoods Independent Sponsor Conference | October 27-28, 2026 | Fairmont Dallas (1,600+ attendees) | McGuireWoods |

| iGlobal IS Summit West Coast | October 29-30, 2026 | Los Angeles | iGlobal Forum |

For consumer IS sponsors specifically, the three highest-leverage events are ACG DealMAX (April 27-29) -- the largest LMM dealmaking conference anchoring Q2 capital partner meetings -- the McGuireWoods IS Conference (October 27-28) with 1,600+ attendees, and whichever category trade show matches the sponsor's sub-sector (SuperZoo for pet, Cosmoprof for beauty, Natural Products Expo East for specialty food, Outdoor Retailer for outdoor).

Axial-platform IS deal flow: Independent sponsors closed 26.8% of all deals on Axial YTD 2025, outpacing Private Equity Funds at 21.1%, and 777 Consumer Goods Independent Sponsors have active deal flow on the platform (Axial). Repeat capital partner relationships account for 59% of IS deals according to Citrin Cooperman 2025. For an IS building a 5-to-10 firm capital partner rolodex focused on consumer, the fastest path is one consumer-specialist equity co-investor (Monogram or Topspin) + one flexible structured-capital shop (Peninsula or Plexus) + one SBIC (Tecum or Centerfield) + one sub-sector specialist (Highlander for household, Bansk for beauty/health at scale).

Use Peony's page-level analytics to track which capital partners are reading the retailer scorecards and co-manufacturer agreements versus skimming the CIM. The ones who spend 20+ minutes on the top-10 retailer breakdown and the trade spend reconciliation are the ones worth second meetings. Use personalized sharing links so every capital partner gets a distinct tracking URL, and NDA gates so nobody sees confidential retailer scorecards or co-manufacturer pricing until they sign -- something DocSend cannot detect on any plan.

Consumer Independent Sponsor Deals By the Numbers

- Consumer industry EV/EBITDA multiple: 9.2x median in 2025 -- the lowest in 10 years of Capstone tracking (Capstone Partners)

- Consumer industry deal count: -18.9% YoY in 2025 (third consecutive year of declines) (Capstone)

- PE buyer consumer multiple premium: 10.4x median versus strategics at 8.6x (spread expanding YoY) (Capstone)

- Beauty and personal care: 14.9x EV/EBITDA average YTD 2025 -- five turns above consumer average (Capstone Beauty Update December 2025)

- Pet sector: 14.5x EBITDA average 2022-YTD 2025; H1 2025 PE median 12.2x (down from 16.8x in 2024) (Capstone Pet Update March 2026)

- Outdoor recreation: +47.7% YoY deal growth in 2025; financial-buyer dry powder at $1.9T (Capstone Outdoor Recreation Update)

- Tactical products: +54.3% YoY deal growth in 2025 (Capstone)

- Vitamins and supplements: +30% YoY deal growth in 2025 (Capstone)

- Food and beverage M&A: pacing toward $120B annual deal value in 2025 (PE deal count -20% YoY, Q4 at 9-year low) (PitchBook Q4 2025 F&B CPG Report)

- Shelf-stable foods: deal value +19% despite double-digit drop in deal count (flight to defensive pantry brands) (PitchBook Q4 2025 F&B CPG)

- VMG Partners Fund VI: $1B closed May 2025 (VMG, PRNewswire)

- Monogram Capital Fund III: $350M oversubscribed November 2025 (Monogram, PRNewswire)

- CAVU Consumer Partners Fund V: $325M closed February 2026 (CAVU, GlobeNewswire)

- Topspin Consumer Partners Fund III: $328M oversubscribed April 15, 2026 (Topspin)

- Tecum Capital Fund IV: $325M SBIC launched February 2025 (Tecum, PRNewswire)

- Plexus Capital Fund VII: $977M Structured Capital Fund explicitly for IS, search funds, equity funds (Plexus Capital)

- Independent sponsors: 26.8% of all Axial deals YTD 2025 (outpacing PE funds at 21.1%) (Axial 2025 IS Report)

- Consumer Goods Independent Sponsors active on Axial: 777 (Axial Consumer Goods Directory)

- 54% of IS transactions closed at 4x-6x EBITDA in 2024-2025 (down from 64% prior year) (Citrin Cooperman 2025 IS Report)

- 59% of IS capital partner deals come from repeat relationships (Citrin Cooperman 2025)

How Peony Fits the Consumer IS Workflow

Peony is a data room platform purpose-built for the exact workflow consumer and CPG IS sponsors run: multiple simultaneous deals during roll-up phases, heavy document diligence (retailer scorecards, co-manufacturer agreements, trademark portfolios, Amazon velocity data, FDA compliance, sustainability certifications), and capital partner engagement tracking. Peony Data Room at $52/admin/month is the plan consumer IS sponsors use.

AI auto-indexing organizes retailer scorecards, co-manufacturer agreements, trademark registrations, P and L by SKU, Amazon velocity reports, and FDA or FD&C compliance files into a professional folder structure in under 3 minutes. Junior analysts spend 2-3 hours on this same workflow in Datasite.

Page-level analytics tell you which capital partner spent 30 minutes on the retailer concentration analysis versus skimmed the CIM, and which one lingered on the co-manufacturer capacity report versus flipped through it. DocSend gives you deck-level views; Peony gives you page-by-page engagement so you know who is genuinely diligencing versus pattern-matching.

Smart Q&A lets counterparties submit diligence questions where AI drafts answers by surfacing the exact document sections and page citations. Your team approves every response before it ships, and every Q&A exchange is audit-trailed. For CPG diligence where questions like "What is the top-3 retailer concentration?" or "Are there any pending FDA warning letters?" come in from every capital partner, this workflow compounds across 3-to-5 simultaneous deals.

AI redaction identifies PII, supplier pricing, and confidential formulations across uploaded documents before capital partners see them -- a feature Datasite charges $25K+ per deal to configure manually.

Screenshot protection blocks and logs screen-capture attempts on sensitive files. Dynamic watermarks embed viewer identity on every frame of every document, which branded consumer capital partners require before reviewing retailer scorecards, co-manufacturer pricing, or confidential product formulations.

NDA gates require signature before any materials are visible -- DocSend cannot detect this on any plan. AI document extraction lets capital partners ask "What is Amazon category rank trend?" and get a cited answer. E-signatures close the loop after conference introductions -- capital partners sign the NDA and access materials in a single workflow.

Unlimited data rooms on Peony Data Room mean an IS running 3-to-5 simultaneous deals during a roll-up phase does not pay per-deal licensing. An IS running three consumer deals per year pays roughly $624 annually on Peony Data Room versus $45,000-$150,000 on Datasite. The free tier is the entry point; Peony Data Room at $52/admin/month is where serious IS workflows run.

For deeper context on private equity co-investment structures, M&A deal process, due diligence expectations, and fundraising best practices, see our dedicated solutions guides.

Quick Guide: Match Your Situation to the Right Capital Partner

| Situation | Best CP Fit | Why |

|---|---|---|

| First-time IS, $10M EV branded CPG food, $2M EBITDA, regional | Plexus Capital + Centerfield Capital (SBIC mezz) | Plexus $2M-$20M EBITDA + explicit IS mandate; Centerfield $3M-$15M precise fit |

| Experienced IS, $25M EV premium pet brand, $4M EBITDA | Topspin Consumer Partners + Tecum Capital (mezz) | Topspin fresh Fund III $328M targeting pet; Tecum consumer SBIC |

| Operating-partner IS, $40M EV beauty platform, $5M EBITDA | Monogram Capital + Peninsula Capital (flex mezz) | Monogram explicit beauty vertical; Peninsula 70+ IS platforms |

| First-time IS, $12M EV specialty food DTC, $2M EBITDA | Topspin Consumer Partners + Centerfield Capital | Topspin minority-friendly structure; Centerfield $3M+ EBITDA SBIC |

| Experienced IS, $35M EV household-chemical roll-up, $6M EBITDA | Highlander Partners + Graycliff Partners (mezz) | Highlander direct NiTEO template fit; Graycliff flexible mezz |

| First-time IS, $18M EV outdoor brand, $3M EBITDA | Monogram Capital + Plexus Capital | Monogram consumer services vertical; Plexus structured capital for IS |

| Operating-partner IS, $50M EV better-for-you F&B platform, $7M EBITDA | Monogram + Peninsula Capital + Tecum Capital (mezz) | Monogram food and bev vertical; Peninsula IS specialist; Tecum SBIC |

| Experienced IS, $60M+ EV consumer health platform, $10M+ EBITDA (scale exit) | Bansk Group or Topspin + Consortium Brand Partners | Bansk $10M+ EBITDA floor + PetIQ 15.73x track record; Consortium platform scaling |

Bottom Line

Consumer and CPG is a selective but durable IS sector in 2026 because the structural forces work in opposite directions across sub-sectors: broader consumer multiples at a 10-year low (9.2x median per Capstone) create IS entry windows at the 4x-6x EBITDA multiple floor, while premium sub-sectors (beauty at 14.9x, pet at 14.5x, outdoor +47.7% YoY) offer exit-multiple expansion paths for disciplined roll-ups. Four major consumer-focused funds closed in 12 months (VMG $1B, Monogram $350M, CAVU $325M, Topspin $328M) signaling real dry powder chasing founder-led brands. Independent sponsors now dominate the platform deal mix at 26.8% of Axial closed deals in 2025 -- outpacing PE funds at 21.1%, and 777 Consumer Goods Independent Sponsors are active.

If you are targeting branded food and beverage, beauty, or pet with defensible niche positioning: Monogram Capital Partners, Topspin Consumer Partners, and Highlander Partners are the most active consumer-specialist equity co-investors. Platform acquisitions at 8x-10x EBITDA with retailer concentration under 50% and clean co-manufacturer relationships remain the premium profile. Retailer concentration, co-manufacturer capacity, and trademark portfolio completeness are the three diligence kill-switches.

If you are targeting specialty retail, household, outdoor, or cross-category brand roll-ups: Highlander Partners (NiTEO template), Consortium Brand Partners (distressed brand consolidation), and Monogram Capital (supply-chain pick-and-shovel) have verified sub-sector deal flow. Branded CPG add-ons at 6x-8x EBITDA exiting as platforms at 9x-14x is the proven arbitrage depending on sub-sector premium. Expect trademark portfolio, co-manufacturer agreements, and founder transition diligence to be mandatory.

If you need mezzanine, structured capital, or sub-debt: Peninsula Capital Partners (70+ IS platforms, $2.4B raised), Plexus Capital ($977M Fund VII explicitly for IS), Tecum Capital ($325M Fund IV SBIC, consumer-active), Centerfield Capital ($3M-$15M EBITDA SBIC), Gemini Investors (SBIC of the Year), and Gladstone Investment (BDC permanent capital) all provide flexible capital structures tailored to consumer IS capital stacks. Pair one SBIC with one senior lender -- the debt side of the stack is not the bottleneck in 2026.

For every consumer IS deal: Set up your data room on day one of the exclusivity window. Consumer diligence is document-heavy at the commercial-dynamics level (retailer scorecards, Amazon velocity, co-manufacturer agreements, trademark portfolios, FDA or FD&C compliance) -- and capital partners expect the data room to be organized and complete at Week 1. You cannot afford to lose days to VDR setup. Peony lets you build a complete consumer IS data room in under 5 minutes, with page-level analytics that show which capital partners are reading the retailer concentration analysis versus skimming the CIM, AI-powered Smart Q&A that surfaces hard answers with page citations so capital partners complete diligence faster, and NDA gates that prevent any capital partner from seeing retailer scorecards or co-manufacturer pricing before signing.

Peony Data Room at $52/admin/month includes AI auto-indexing, AI-powered Smart Q&A, dynamic watermarks, screenshot protection, NDA gates, page-level analytics, AI document extraction, and e-signatures. An IS running three consumer deals per year pays roughly $624 annually versus $45,000-$150,000 on Datasite. When your exclusivity clock is ticking and five capital partners need to get comfortable with the branded CPG deal simultaneously, every hour matters.

Set up your first consumer or CPG IS data room -- see plans and pricing.

Frequently Asked Questions

I am a first-time IS with an LOI on an $8M EBITDA branded food deal -- which capital partners fund consumer independent sponsor deals?

Consumer independent sponsor deals are funded by three capital partner types: consumer-focused PE firms that co-invest on a deal-by-deal basis such as Monogram Capital Partners, Topspin Consumer Partners, Highlander Partners, and Consortium Brand Partners; flexible mezz and structured capital providers like Peninsula Capital Partners, Plexus Capital, and Graycliff Partners that fill the debt side of the stack; and SBIC sub-debt lenders such as Tecum Capital, Centerfield Capital, Gemini Investors, and Gladstone Investment that provide sub-debt behind IS equity. For a first-time IS on an $8M EBITDA branded food deal, a $4M-$6M mezz check from Peninsula or Plexus plus a minority equity co-invest from Monogram or Topspin is the typical stack. Peony Data Room at $52 per admin per month includes AI auto-indexing that organizes the P and L by SKU, customer concentration analysis, co-manufacturer agreements, trademark registrations, and retailer scorecards in under 3 minutes -- so the data room is ready before the first capital partner call.

I run corp dev at a mid-market PE firm -- what EBITDA multiples do consumer IS deals trade at in 2026?

Consumer IS deals in 2026 trade across a wide range by sub-sector: the broader consumer industry median hit 9.2x EV/EBITDA in 2025 -- a 10-year low according to Capstone Partners -- with PE paying 10.4x median versus strategics at 8.6x, beauty and personal care commands the richest multiples at 14.9x EV/EBITDA average through YTD 2025, pet products and services averaged 14.5x sector EBITDA from 2022 through YTD 2025 with H1 2025 PE median compressing to 12.2x from 16.8x in 2024, branded CPG food and beverage ranges from 6.8x for $1M-$3M EBITDA platforms up to 9.0x plus for $5M-$10M EBITDA, outdoor recreation and lifestyle brands trade in line with the 9.2x consumer median (with exceptional platforms like Kontoor-Helly Hansen hitting 12.5x in February 2025), and specialty consumer services like franchises and home services range from 3x to 8x for founder-led platforms up to mid-teens for scaled PE platforms. For a corp dev lead evaluating a $15M-$30M branded consumer platform, the spread between the 9.2x consumer median and the 14.9x beauty premium is the core sub-sector arbitrage. Peony Data Room includes AI document extraction that lets capital partners ask What is the Amazon velocity by SKU or What is the retailer concentration by chain across uploaded retailer scorecards and get cited answers with exact page numbers, a workflow that takes junior analysts 2-3 hours per room on legacy platforms like Datasite.

Our family office is evaluating our first CPG IS deal -- what is the state of consumer M&A in 2026?

Consumer M&A is in a selective recovery in 2026 after three consecutive years of declines: total consumer industry deals fell 18.9% year-over-year in 2025 according to Capstone Partners, with multiples at a 10-year low of 9.2x EV/EBITDA median, but discretionary and defensive sub-sectors are rebounding sharply with tactical products up 54.3% YoY, outdoor recreation and enthusiasts up 47.7%, and vitamins and supplements up 30%. Food and beverage M&A is pacing toward $120 billion in annual deal value in 2025 despite PE deal count falling about 20% year-over-year per PitchBook. Beauty and personal care multiples at 14.9x EV/EBITDA remain five turns above the broader consumer average. Three major consumer-focused PE funds closed in a 12-month window signaling real dry powder: VMG Partners Fund VI at $1B in May 2025, Monogram Capital Fund III at $350M in November 2025, CAVU Consumer Partners Fund V at $325M in February 2026, and Topspin Consumer Partners Fund III at $328M in April 2026. For a family office allocating $5M-$15M equity to its first CPG IS deal, focus on founder-led brands with defensive positioning in pet, better-for-you food, outdoor, or clean beauty -- the four sub-sectors where 2025-2026 deal flow is concentrated. Peony Business at $30 per admin per month includes page-level analytics that show which capital partners spent 30 minutes on the retailer scorecards versus skimmed the CIM, so you can prioritize follow-ups with genuinely engaged partners.

I am a corp dev analyst building my first CPG data room -- what documents do consumer capital partners need?

Consumer and CPG capital partners require standard M&A diligence plus consumer-specific materials: P and L by SKU with gross margin analysis, customer concentration by retailer with top 10 chains and wholesale versus DTC split, Amazon and DTC velocity data with ACOS, ROAS, and category rank trends, co-manufacturer agreements with capacity commitments and change-of-control language, distributor and broker agreements with minimum purchase obligations, retailer scorecards including on-shelf availability, reset history, and Nielsen or SPINS data, trademark registrations in primary markets (USPTO, EUIPO, CIPO, INPI), FDA registrations for food and dietary supplements or FD&C cosmetic compliance for beauty, slotting fee and trade spend reconciliation, promotional calendar with planned activations, and sustainability and supply chain certifications (Fair Trade, USDA Organic, Non-GMO, Leaping Bunny) where applicable. For a corp dev analyst running point on a $20M-$40M branded consumer deal, these are the documents that kill or close the transaction. Peony Data Room auto-indexing organizes all of these in under 3 minutes into a professional folder structure, and Smart Q and A routes capital partner questions through AI-drafted answers with page citations before your team approves each response.

Our IS targets pet sub-sector roll-ups -- which capital partners fit pet and specialty consumer?

Pet sub-sector independent sponsor roll-ups benefit from some of the richest consumer multiples in the market -- Capstone reports pet sector EBITDA multiples averaged 14.5x from 2022 through YTD 2025, though H1 2025 PE median compressed to 12.2x from 16.8x in 2024, and Q3 2025 pet sector deal volume was 96 transactions. For IS sponsors imitating the pet roll-up template, the right capital partner mix is specific. Monogram Capital Partners explicitly names pet as one of its four consumer verticals alongside food and beverage, beauty, and consumer services, with Fund III at $350M closed November 2025. Topspin Consumer Partners Fund III at $328M (April 2026) names pet brands in its target sectors. Bansk Group backed the $1.5B PetIQ take-private in October 2024 at 15.73x EV/EBITDA -- an exit buyer for scaled IS platforms above $10M EBITDA. Peninsula Capital Partners provides mezz and equity across consumer segments including pet, and has backed 70+ IS platforms historically. For a specialized IS targeting a $15M-$30M pet platform with $3M-$5M EBITDA, the stack typically pairs a consumer-specialist equity lead with SBIC mezzanine. Peony's Data Room plan at $52 per admin per month includes dynamic watermarks with viewer identity embedded in every frame, with NDA gates starting on the Business plan at $30 per admin per month so capital partners sign before any vet clinic network or e-commerce velocity data is visible.

Our IS is running three to five CPG deals per year -- how much does a data room cost for consumer IS deals?

Legacy data rooms like Datasite charge 15,000 to 50,000 dollars per deal, which is disproportionate for independent sponsors targeting 3 to 25 million dollar EBITDA branded consumer and CPG businesses. Consumer deals require extensive document uploads including trademark filings across multiple jurisdictions, co-manufacturer agreements, retailer scorecards, Amazon velocity reports, FDA or FD&C compliance files, promotional calendars, and customer contract assignability audits, meaning sponsors often need three to five active data rooms simultaneously during a roll-up phase. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing, AI document extraction, Smart Q and A, NDA gates, dynamic watermarks, page-level analytics, and screenshot protection. An IS running three consumer deals per year pays roughly 624 dollars annually on Peony Data Room versus 45,000 to 150,000 dollars on legacy platforms, a workflow that Datasite charges $25K+ per deal to configure.

I am a capital-partner PE principal diligencing a branded CPG deal -- what sub-sectors have the most IS activity in 2026?

The most active consumer sub-sectors for independent sponsor deals in 2025-2026 are better-for-you food and beverage (the CAVU Fund V $325M close February 2026 is explicitly targeting this category), pet products and services (14.5x sector average EBITDA multiple per Capstone), beauty and personal care (14.9x EV/EBITDA average with deal count falling from 108 in 2024 to 67 in 2025 signaling lower-mid-market consolidation), outdoor recreation and enthusiasts (+47.7% YoY deal growth in 2025 per Capstone), tactical products (+54.3% YoY), consumer health and vitamins (+30% YoY growth), and specialty consumer services including home services and franchises where PE platforms trade at mid-teens EBITDA while founder-led single-digit EBITDA deals trade at 3x-8x. For a capital-partner PE principal diligencing a $20M-$40M branded consumer platform, expect retailer concentration, co-manufacturer capacity, and trademark portfolio assignability to be the three biggest diligence issues. Peony Data Room at 52 dollars per admin per month includes AI-powered Smart Q and A that lets capital partners submit diligence questions where AI surfaces relevant document sections with exact page citations, something DocSend cannot detect on any plan.

I am an M&A attorney advising a first-time IS -- how do consumer capital partners expect deal books to be structured?

Consumer and CPG capital partners expect deal books organized in a standard 3-stage diligence flow: Stage 1 initial risk scan including the CIM, P and L by SKU, customer concentration by retailer, trademark registration summary, and co-manufacturer overview; Stage 2 deep dive with Q of E, full trademark portfolio audit with any opposition proceedings flagged, co-manufacturer capacity certifications and change-of-control clauses, retailer scorecards with Nielsen or SPINS third-party data, Amazon and DTC velocity with ACOS and category rank trends, promotional calendar reconciliation to trade spend accruals, and slotting fee amortization schedules; Stage 3 comprehensive validation covering FDA registrations or FD&C compliance files, sustainability certifications, distributor agreements with minimum purchase obligations, promotional effectiveness analysis, and 100-day integration plan with sales and operations continuity. For an M&A attorney advising a first-time IS running a $20M enterprise value branded CPG deal, missing or unassignable co-manufacturer agreements are the most frequent M&A red flag in consumer deals because they can trigger capacity loss or renegotiation on close. Peony Data Room at 52 dollars per admin per month includes AI auto-indexing that organizes documents into a professional folder structure in under 3 minutes, and personalized sharing links that track each capital partner separately so you know who is engaged before you draft the capital call.

Our IS is running a $35M specialty food roll-up -- how do we handle co-manufacturer and trademark diligence?

Specialty food and branded CPG targets require a disciplined co-manufacturer and IP package in the data room: co-manufacturer agreements with capacity commitments, exclusivity clauses, change-of-control language, and quality audit history; trademark registrations across all primary markets (USPTO, EUIPO, CIPO, INPI, and any DTC-served geographies) with any opposition proceedings flagged; domain name and social handle portfolios with clean chain of title; licensing agreements with third-party brand usage; FDA food registrations, 510(k) clearances if applicable, or FD&C compliance files for supplements; state TTB licenses for alcohol; and any outstanding consumer complaints or class-action exposure. For an IS running a $35M specialty food roll-up, co-manufacturer capacity bottlenecks are the single biggest post-close operational risk because rebuilding manufacturing partnerships can take 12-18 months. Trademark gaps in secondary markets (Canada, UK, EU) trigger launch delays for expansion theses. Peony Data Room at 52 dollars per admin per month includes screenshot protection that blocks and logs screen capture attempts on sensitive files, and Advanced Redaction on Peony Deal Team identifies PII, supplier pricing, and confidential formulations across uploaded documents before capital partners see them, a workflow that Datasite charges $25K+ per deal to configure.

I am a first-time IS building a capital partner network -- where do consumer independent sponsors meet capital partners in 2026?

Consumer and CPG independent sponsors meet capital partners at ACG DealMAX on April 27-29 2026 in Las Vegas (the InterGrowth rebrand anchoring the spring LMM calendar), the SBIA Independent Sponsor Forum on May 6 2026 at the Sheraton Philadelphia Downtown, Natural Products Expo West typically held in early March for organic and better-for-you brand sourcing, SIAL America on March 25-27 2026 in Las Vegas for food and beverage, the iGlobal Independent Sponsor Summit Dallas on June 11 2026, Expo East typically held in September for specialty foods, the iGlobal IS Summit NYC on September 28-29 2026, Cosmoprof North America in Las Vegas typically July for beauty, SuperZoo in Las Vegas typically August for pet, the McGuireWoods Independent Sponsor Conference on October 27-28 2026 at the Fairmont Dallas with 1,600+ attendees, the iGlobal IS Summit West Coast on October 29-30 2026 in Los Angeles, and through platforms like Axial where 777 consumer goods independent sponsors are active and IS sponsors closed 27% of all deals on the platform in 2025. Repeat relationships account for 59% of capital partner deals according to Citrin Cooperman. For an IS building a 5-to-10 firm capital partner rolodex focused on consumer, starting with a consumer-specialist like Monogram or Topspin plus one SBIC like Tecum or Centerfield is the fastest path. Peony Data Room at 52 dollars per admin per month includes NDA-gated data rooms with built-in e-signatures so capital partners can sign and access materials in a single workflow after conference introductions.

Related Resources

- Independent Sponsor Guide -- complete IS mechanics, economics, and capital partner dynamics

- Independent Sponsor Capital Raising Playbook -- pre-LOI cultivation, term sheet economics, SBIC leverage, and capital stack design

- Independent Sponsor Tech/Software Capital Partners -- 13 firms funding tech and software IS deals

- Independent Sponsor Manufacturing Capital Partners -- 12 firms funding manufacturing IS deals

- Independent Sponsor Distribution & Logistics Capital Partners -- 12 firms funding wholesale, 3PL, cold chain, and specialty distribution IS deals

- Independent Sponsor Cleantech & Energy Capital Partners -- 12 firms funding HVAC, energy services, environmental services, and data center grid resilience IS deals

- Independent Sponsor Healthcare Capital Partners -- 17 firms funding healthcare IS deals

- Independent Sponsor Business Services Capital Partners -- 15 firms funding business services IS deals

- Independent Sponsor Data Room Checklist -- the document set capital partners expect

- Independent Sponsor LOI Playbook -- exclusivity windows, capital-partner outreach timing, and closing mechanics

- Independent Sponsor Conferences and Forums -- 18 IS events mapped for 2026

- Best Data Rooms for Independent Sponsors -- 8 VDRs scored for IS deal workflows

- Due Diligence Data Room Checklist -- 174 documents across all deal types

- Consumer Investors -- VC firms active in consumer (earlier-stage than IS capital partners)