15 VCs Funding Automotive and EV Startups in 2026

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

Last updated: April 2026

Automotive venture capital hit $54B globally in 2024 — the second-highest year on record behind only the 2021 SPAC boom (Oliver Wyman Mobility Investment Radar 2025). But seed-stage founders building connected-car platforms, battery materials, ADAS components, and automotive cybersecurity tools face a specific challenge: most of that capital flows to mega-rounds like Waymo's $5.6B raise, not to first checks.

TL;DR: Global automotive VC funding reached $54B in 2024 (+54% YoY in the Americas). Roughly 67% of automotive startups founded since 2020 are still early-stage (S&P Global AutoTechInsight, 2025). The average automotive seed round runs $4-6M — higher than the general $3.2M median because of hardware and deep-tech components. Below are 15 investors actively writing seed checks into automotive manufacturing tech, EV/battery, SDV platforms, and automotive cybersecurity in 2026.

Automotive investors are venture capital firms and corporate venture arms that specialize in funding companies across the automotive value chain — from powertrain and battery materials to software-defined vehicle platforms, ADAS sensor components, V2X infrastructure, automotive cybersecurity, and aftermarket technology. Unlike transportation and mobility investors who fund ride-sharing, freight movement, and multi-modal networks, or logistics investors who back warehousing, fulfillment, and cold-chain operations, automotive investors focus on the vehicle itself: what goes into it, what makes it drive, and what secures it.

I spent six years evaluating deep-tech and mobility deals at Backed VC and Target Global before co-founding Peony. The list below reflects where seed capital is actually flowing in 2026 — not where press releases say it might. When you are ready to share your pitch deck, patent filings, and technical documentation with these investors, Peony's data rooms provide page-level analytics, dynamic watermarks, and AI auto-indexing so you can track which investors engage with your materials and protect sensitive IP throughout the process.

Market Context: Automotive VC Funding in 2026

Before diving into individual investors, here is where the money is going.

Subsector funding breakdown (2024, Oliver Wyman):

- Sustainability (EV, battery, charging): $19.6B — the largest subsector globally, up 42% from 2022 baseline

- Connected and autonomous driving: $18.2B — doubled YoY, though Waymo's $5.6B round drove the bulk

- Mobility services: Up 89% YoY — driven by emerging market expansion

- Sales and after-sales: $4.8B — digital retail and aftermarket tech, up 9%

Subsectors attracting the most seed capital in 2025-2026:

- Software-defined vehicles (SDV): Projected $3.3T market by 2034 at 31.2% CAGR (InsightAce Analytic, 2025). OEMs are shifting from feature-based to ROI-driven software strategies, and zonal E/E architectures are gaining momentum.

- Automotive cybersecurity: Growing from $5.24B in 2025 to $18.88B by 2034 at 15.3% CAGR (Precedence Research, 2025). ISO 21434 is now baseline compliance.

- Battery technology: Silicon-anode, solid-state, and battery recycling attracting significant capital. Downstream manufacturing quality control is an emerging niche.

- Fleet electrification: Medium-duty EV (Harbinger Motors), fleet management software, and AI-driven fleet operations.

- V2X (vehicle-to-everything): $2.87B in 2025 to $18.67B by 2030 at 45.43% CAGR (Mordor Intelligence, 2025) — though growth is shifting from government-mandated V2I toward V2N network-based services.

Key seed-stage trend: The automotive seed landscape is bifurcated. Pure software plays (SDV platforms, cybersecurity, fleet management, AI diagnostics) attract standard $2-5M seeds. Hardware-heavy plays (battery materials, EV powertrain, sensors) need $5-10M or more because of lab validation, prototyping, and certification costs. About 67% of automotive startups founded between 2020 and 2024 are still early-stage (S&P Global AutoTechInsight, 2025), which means there is a deep pipeline of companies entering seed and Series A in 2026.

How Peony Helps Automotive Startups Raise Capital

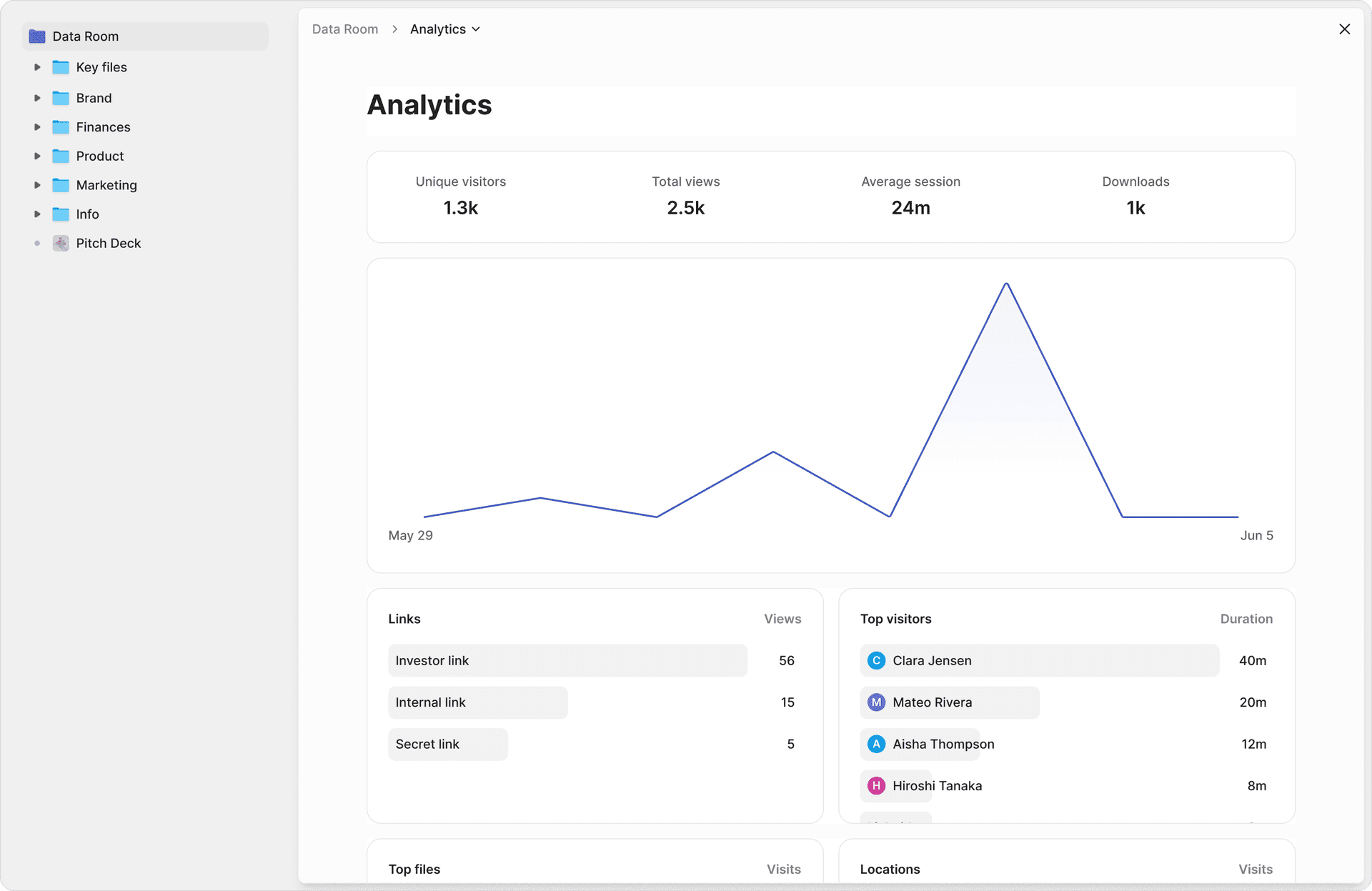

Peony provides venture capital data rooms purpose-built for startup fundraising. Automotive founders use Peony to organize patent filings, battery test data, certification roadmaps, and pitch decks in branded data rooms with page-level analytics that show which investors reviewed your technical documentation and for how long.

When you are sharing proprietary sensor designs or cell-test results with multiple VCs simultaneously, dynamic watermarks embed each viewer's identity into every page, screenshot protection blocks and logs capture attempts, and NDA gates require investors to sign before viewing sensitive IP. Set up your data room in under 5 minutes and let AI auto-indexing organize your documents in under 3 minutes.

Start your automotive fundraising data room — built for startups raising from seed to Series A.

15 VCs Funding Automotive and EV Startups

1. Autotech Ventures

Type: Automotive-specific VC | HQ: Menlo Park, CA | Founded: 2013

Fund size: $500M+ total AUM. Latest fund: $230M (Fund III, closed April 2023).

Seed check: $2-5M (average seed round: $5.86M across 12 seed investments)

Stage: Seed through Series C

Subsectors: Autonomous driving and ADAS, EV/electrification, connected vehicles, fleet management, aftermarket and auto retail

Notable portfolio: Lyft (IPO), SpotHero, HaydenAI, Gaussion ($12M Series A led by Autotech in magneto-electrochemistry), GenLogs, Agtonomy, BasicBlock. 4 IPOs and 10 acquisitions across the portfolio.

Why they matter at seed: Autotech is the most established dedicated automotive VC in the US. With 56 companies and 12 seed investments, they have the deal flow and LP relationships to lead automotive seed rounds that generalist VCs pass on because they do not understand automotive sales cycles.

2. Trucks VC

Type: Automotive/transportation-specific VC | HQ: San Francisco, CA | Founded: 2016

Fund size: $70M (Fund III, closed December 2024). Largest fund to date, with 7 strategic LPs including an automotive supplier, tire manufacturer, insurance company, and airline carrier.

Seed check: $500K-2M (targets 10% ownership)

Stage: Pre-seed and seed (primary), occasional Series A

Subsectors: Electric vehicles and charging infrastructure, autonomous systems, fleet electrification, zero-emissions aviation, AI for vehicle maintenance

Notable portfolio: Treehouse (charger installation-as-a-service), JetZero (zero-emissions jet aircraft), Bingo Technologies ($1.9M seed led by Trucks VC, April 2025 — "One Battery, Any Vehicle" urban fleet), Carvis (AI master tech for mechanics), Maritime Fusion, Auriga Space.

Why they matter at seed: Trucks VC is the most seed-focused automotive investor in the US with 25 seed-stage investments out of 60 total and plans for approximately 30 seed investments from Fund III. Their $500K-2M check size makes them accessible to very early founders, and their strategic LP base (automotive supplier, tire manufacturer, insurer) provides immediate industry introductions.

3. Maniv Mobility

Type: Automotive/mobility-specific VC | HQ: New York, NY (Israeli roots, global portfolio across 9 countries) | Founded: 2014

Fund size: $269.6M total raised. Latest fund: $140M (Fund III, closed April 2024).

Seed check: $2-5M (average seed round: $4.72M across 12 seed investments)

Stage: Seed (primary) and Series A. Founder Michael Granoff calls it "a seed-stage fund at heart that occasionally breaks its own rules."

Subsectors: Electric vehicles (medium-duty EVs, two-wheeler EVs), autonomous vehicle sensors and edge AI, automotive connectivity and data, EV charging networks, decarbonization

Notable portfolio: Harbinger Motors (medium-duty EV trucks, Series C follow-on November 2025), Hailo (AI edge silicon, Tel Aviv), Nexar (connected vehicle data), Revel (EV ridehail and charging, NYC), Turo (car sharing, IPO candidate), River (two-wheeler EV OEM, Bangalore).

Why they matter at seed: Maniv's cross-border portfolio across 9 countries means they understand automotive regulatory environments beyond just the US. Their edge AI and connected-vehicle data investments (Hailo, Nexar) make them especially relevant for SDV and ADAS software founders.

4. Toyota Ventures

Type: OEM corporate VC (Toyota) | HQ: Los Altos, CA | Founded: 2017 (originally Toyota AI Ventures)

Fund size: $800M+ total AUM. Two $150M funds announced April 2024: Frontier Fund II and Climate Fund II. Part of Toyota's broader $3B+ venture commitment.

Seed check: $2-5M (average seed round: $7.81M across 27 seed investments — higher due to deep-tech)

Stage: Seed (primary) and early-stage

Subsectors: AI and robotics, autonomous driving, hydrogen and clean energy, battery/EV technology, carbon capture, quantum computing applications for mobility

Notable portfolio: Joby Aviation (eVTOL, public), May Mobility (autonomous shuttles), Avalanche Energy (fusion microreactor), e-Zinc (energy storage), Ecolectro (green hydrogen), Sea Machines (autonomous marine).

Why they matter at seed: Toyota Ventures is the most active OEM corporate VC at seed stage, with 27 seed investments and an explicit seed mandate. Most other OEM CVCs (GM Ventures, Stellantis Ventures) skew Series A or later. The Frontier Fund targets breakthrough technology while the Climate Fund focuses on decarbonization — founders should pitch the right fund based on their technology category.

5. Fontinalis Partners

Type: Automotive/mobility-specific VC | HQ: Detroit, MI | Founded: 2009

Fund size: Approximately $270M across three funds. Latest fund: $104M (Fund III, closed August 2021).

Seed check: Not disclosed publicly. Invests from seed through Series B.

Stage: Seed through Series B

Subsectors: Transportation networks, freight intelligence, industrial robotics and autonomous manufacturing, hydrogen/clean energy, autonomous vehicle components, EV infrastructure

Notable portfolio: VulcanForms (unicorn, advanced manufacturing), Turo (unicorn, car sharing), Life360 (IPO), Ouster (IPO via SPAC, lidar), Damon Motors (listed NASDAQ November 2024, electric motorcycles), Hgen ($5M raise for hydrogen electrolyzers, September 2024), Swift Solar ($27M Series A, June 2024). Historical exits include Telogis (acquired by Verizon), Postmates (acquired by Uber), and nuTonomy (acquired by Aptiv).

Why they matter at seed: Co-founded by Bill Ford Jr., executive chairman of Ford Motor Company. This gives Fontinalis portfolio companies genuine OEM access that other VCs cannot replicate. Their Detroit base provides proximity to Big Three procurement and supplier networks.

6. Automotive Ventures

Type: Automotive-specific VC (dealership tech and aftermarket focus) | HQ: Atlanta, GA | Founded: 2020

Fund size: $35M total AUM across 3 funds. Inaugural fund: $7M+ (oversubscribed). Mobility Fund II active (Assurant Ventures invested March 2025).

Seed check: Approximately $250K (smaller than other automotive VCs)

Stage: Pre-seed and seed

Subsectors: Auto retail and dealership technology, aftermarket and auto services, fleet management, connected car data

Notable portfolio: 39 investments total across 3 funds. 11 seed-stage investments (average round: $4.09M). EvenFlow AI ($1.5M seed, December 2024), EECOMOBILITY (EV battery testing, seed 2024).

Why they matter at seed: Led by Steve Greenfield, who has 25+ years in automotive tech and has overseen $1B+ in automotive tech acquisitions. Automotive Ventures is the most accessible seed investor on this list — $250K checks mean they can participate in very early rounds where other automotive VCs require more traction. Ideal for aftermarket, dealership tech, and connected-car data startups.

7. BMW i Ventures

Type: OEM corporate VC (BMW Group) | HQ: Mountain View, CA | Founded: 2011

Fund size: BMW Group allocated up to EUR 500M over 10 years across 3 funds.

Seed check: $2-5M (average seed round: $4.98M across 12 seed investments)

Stage: Seed through Series B (primary at Series A/B, but does seed)

Subsectors: Car development technology, smart production and manufacturing, supply chain innovation, digital sales and services, sustainability, autonomous driving, data quality and enterprise AI

Notable portfolio: Kodiak Robotics/Kodiak AI (autonomous trucking, SPAC IPO 2025), Qualytics ($10M Series A led by BMW i Ventures, June 2025). 86 companies total with 11 unicorns in portfolio, 2 IPOs, 5 acquisitions, and 29 exits.

Why they matter at seed: BMW i Ventures combines OEM strategic access with a strong financial track record — 11 unicorns and 29 exits across 86 companies. Their seed investments benefit from BMW's testing infrastructure, supplier networks, and potential pilot programs. The Kodiak Robotics investment-to-IPO path demonstrates the full value chain.

8. Porsche Ventures

Type: OEM corporate VC (Porsche AG) | HQ: Stuttgart, with global offices | Founded: 2018

Fund size: Up to EUR 250M earmarked ("Porsche Ventures 2.0"). Annual investment framework: EUR 150M.

Seed check: $3-8M (average seed round: $7.78M across 10 seed investments)

Stage: Seed through growth

Subsectors: Auto tech and connected car, manufacturing acceleration, fintech (auto-adjacent — car repairs, financing), enterprise AI, cybersecurity

Notable portfolio: Via (ride-sharing unicorn), Cresta (unicorn), Nozomi Networks (unicorn), Bumper (fintech for car repairs), Atomic Industries (manufacturing acceleration). 52 companies total with 4 unicorns, 2 IPOs, and 5 acquisitions.

Why they matter at seed: Porsche Ventures writes larger seed checks ($3-8M) than most OEM CVCs, making them a potential seed lead rather than just a co-investor. Their cybersecurity thesis (Nozomi Networks) is particularly relevant as ISO 21434 compliance becomes mandatory across the supply chain.

9. Hyundai Motor Group (CRADLE and ZER01NE Fund)

Type: OEM corporate VC (Hyundai/Kia) | HQ: Silicon Valley, Tel Aviv, Berlin, Beijing, Singapore | Founded: 2016

Fund size: ZER01NE Fund III: $91.4M (launched 2025, backed by 10 Hyundai Group affiliates). Previous funds: Fund II ($58M), Fund I ($7M). Also anchor investor in Factorial Funds ($200M Menlo Park VC, January 2025).

Seed check: Not disclosed. Invests at early-stage (pre-seed/seed through Series A).

Stage: Pre-seed/seed through Series A

Subsectors: AI and robotics, cybersecurity, hydrogen and energy technologies, autonomous driving, connected car and IoT, advanced manufacturing

Notable portfolio: 105+ startups across Funds I and II through CRADLE. 61 investments via CRADLE alone. Key automotive holdings include Autotalks (V2X communication chipsets, acquired by Qualcomm in 2025), Netradyne (fleet safety AI, unicorn 2025), and Metawave (AI-powered radar for autonomous vehicles). 10 startup partnerships showcased at CES 2025.

Why they matter at seed: Hyundai's ZER01NE Fund III represents a significant escalation of early-stage commitment — $91.4M with 10 Hyundai Group affiliates as backers means portfolio companies get multi-division OEM access, not just a single business unit relationship. Their global office network (5 cities across 4 continents) makes them relevant for founders building for international automotive markets.

10. Stellantis Ventures

Type: OEM corporate VC (Stellantis — Chrysler, Jeep, Peugeot, Fiat) | HQ: Amsterdam (global, invests in US startups) | Founded: 2022

Fund size: EUR 300M (approximately $330M).

Seed check: Not disclosed. Invests in early and later-stage startups.

Stage: Early and later-stage

Subsectors: Sustainable mobility, connected vehicle technology, advanced manufacturing, EV/electrification, customer experience technology

Notable portfolio: 12 companies funded as of mid-2024. Viaduct (acquired by Sumitomo Rubber for $104M, October 2025 — demonstrating the OEM-to-acquisition exit pathway). Annual Venture Awards program recognizes 5-6 startups each year.

Why they matter at seed: Stellantis is the world's fourth-largest automaker by volume, encompassing 14 brands. Their Venture Awards program is a practical entry point for seed-stage founders — even if you do not receive investment immediately, the exposure to Stellantis procurement and engineering teams can lead to pilot programs. The Viaduct exit at $104M validates the OEM CVC-to-acquisition pathway.

11. Robert Bosch Venture Capital (RBVC)

Type: Tier 1 supplier corporate VC (Robert Bosch GmbH) | HQ: Stuttgart, Germany (invests globally including US) | Founded: 2007

Fund size: Sixth fund: approximately $270M / EUR 250M (announced 2024/2025). 60+ active investments in portfolio.

Seed check: Under EUR 500K for seed; EUR 500K-5M for early-stage; EUR 6-15M aggregate per portfolio company

Stage: Seed through late-stage

Subsectors: Automation and electrification, energy efficiency, enabling technologies (sensors, semiconductors), connected mobility, manufacturing tech

Notable portfolio: 158 total investments across 6 funds. Key automotive holdings include AImotive (ADAS software and autonomous driving AI), Cavan (FCEV and BEV commercial vehicle platforms), and ByNav (automotive-grade GNSS positioning units). Deep portfolio in sensor technology, electrification components, and industrial automation.

Why they matter at seed: Bosch is the world's largest automotive supplier. RBVC portfolio companies gain access to Bosch's testing labs, manufacturing expertise, and OEM supplier relationships that no pure-play VC can offer. Their smaller seed checks (under EUR 500K) mean they can co-invest alongside a lead automotive VC, adding strategic value without requiring a large allocation.

12. Volta Energy Technologies

Type: Battery/energy storage specialist VC | HQ: Chicago, IL | Founded: 2018 (spun out of Argonne National Laboratory)

Fund size: Fund I: $205.3M (closed). Fund II: $137.8M closed toward $500M target (as of October 2024).

Seed check: Not disclosed. Invests from seed through growth exclusively in battery and energy storage.

Stage: Seed through growth (battery/energy storage only)

Subsectors: Solid-state batteries, silicon-anode technology, battery recycling, EV battery materials, grid-scale energy storage, wireless/high-speed charging, battery manufacturing QC

Notable portfolio: NanoGraf ($65M round, 2024 — silicon-anode battery materials), Solid Power (solid-state batteries), Our Next Energy (battery tech scaling), Conamix (battery materials), OneD Battery Sciences (latest Fund I investment, July 2024). 34 total investments.

Why they matter at seed: Volta is the only VC on this list exclusively focused on battery and energy storage technology. Their Argonne National Laboratory roots give them access to lab-level technical diligence that generalist VCs and even OEM CVCs cannot replicate. If you are building battery materials, recycling processes, or charging technology, Volta's technical network is the strongest in the US.

13. Eclipse Ventures

Type: Generalist VC with heavy physical/industrial focus | HQ: Palo Alto, CA | Founded: 2015

Fund size: $2.5B+ total AUM. Latest raise: $1.3B across two funds in 2025 — $720M early-stage and $591M growth-stage.

Seed check: Not disclosed. Invests from pre-seed through early growth.

Stage: Pre-seed through early growth

Subsectors: Physical AI and robotics, manufacturing automation, battery technology and recycling, electric vehicles (boats, cars), autonomous systems, AI-native auto retail

Notable portfolio: Ever (AI-native auto retail, $31M Series A from stealth), Redwood Materials (battery recycling), Arc (electric boats), Wayve (autonomous vehicles, co-led $1.2B Series D), Mind Robotics ($115M seed), Bedrock Robotics (autonomous construction). 100+ portfolio companies.

Why they matter at seed: Eclipse brings factory math expertise — yield, throughput, COGS modeling, and production ramp planning — that pure-play automotive VCs typically lack. Their $1.3B 2025 raise signals continued appetite for physical industries. The Ever investment shows they also back pure software plays when the AI layer is differentiated enough.

14. Lux Capital

Type: Generalist VC with deep-tech/frontier focus | HQ: New York, NY | Founded: 2000

Fund size: $7B+ total AUM. Latest fund: $1.5B (Fund IX, closed January 2026 — largest ever).

Seed check: Not disclosed. Primarily early-stage for new investments.

Stage: Seed through growth

Subsectors: Autonomous vehicles and simulation, robotics and embodied intelligence, defense autonomy (military autonomous vehicles), AI/ML infrastructure, semiconductors and sensors, manufacturing innovation

Notable portfolio: Applied Intuition ($15B valuation, $600M Series F in 2025 — AV simulation software with Pentagon contracts), Forterra ($275M Series F — autonomous military vehicles). Focus on autonomy broadly, not just commercial automotive.

Why they matter at seed: Lux's $7B AUM and $1.5B latest fund provide massive follow-on capacity. They are selective at seed for automotive but have produced the largest outcomes in the autonomy space — Applied Intuition at $15B is the most valuable private automotive software company. If your technology has dual-use (commercial and defense) applications, Lux is especially relevant.

15. GM Ventures

Type: OEM corporate VC (General Motors) | HQ: Warren, MI | Founded: 2010

Fund size: Not publicly disclosed (CVC balance-sheet model). Estimated at several hundred million based on deal volume. Team of 19 (9 Partners, 5 Principals).

Seed check: Not disclosed. Primary focus is Series A and Series C.

Stage: Series A and Series C (primary) — less active at seed but relevant as follow-on capital

Subsectors: Electrification, autonomous driving, customer connectivity, digital enterprise and manufacturing AI, cybersecurity, space technology

Notable portfolio: Silverfort (cybersecurity unicorn, 2024), Turo (unicorn), SES Technologies (NYSE, solid-state batteries), AEye (NASDAQ, lidar), Nanoramic (latest investment, November 2025). 131 companies total with 4 unicorns and 20 portfolio exits.

Why they matter: While GM Ventures primarily invests at Series A and later, their 131-company portfolio and 20 exits make them essential follow-on capital for seed-stage automotive founders. Building a relationship now — through their accelerator programs or industry events — positions you for GM Ventures participation in your Series A.

How to Think About Choosing an Automotive Investor

The 15 investors above cover different subsectors, check sizes, and value-add profiles. Here is how to match your specific situation to the right shortlist.

If you are building battery materials, recycling, or charging technology and need lab validation support, Volta Energy Technologies and Toyota Ventures are your strongest leads. Volta's Argonne National Laboratory connection provides technical diligence depth that no other automotive VC can match, and Toyota Ventures has backed 27 seed-stage companies including hydrogen and battery startups. Robert Bosch Venture Capital adds manufacturing scale expertise as a co-investor.

If you are a pure software play — SDV platforms, automotive cybersecurity, fleet management AI — and need a fast-moving seed lead, Autotech Ventures and Trucks VC are the most active. Trucks VC writes $500K-2M checks with a 10% ownership target and plans 30 investments from their $70M fund. Autotech has the deepest connected-vehicle portfolio with $500M+ AUM. For cybersecurity specifically, Porsche Ventures has this as an explicit thesis and writes $3-8M seed checks.

If you need OEM access for pilot programs, testing infrastructure, or procurement introductions, start with Fontinalis Partners (Bill Ford Jr., Ford Motor Company access), BMW i Ventures (11 unicorns, proven Kodiak-to-IPO pathway), or Stellantis Ventures (14 OEM brands, Venture Awards entry point). These investors provide distribution leverage that pure-play VCs cannot replicate.

If you are building ADAS sensor components or autonomous driving technology and need both capital and follow-on capacity, pair a dedicated automotive VC lead (Autotech or Maniv) with a generalist deep-tech co-investor (Lux Capital or Eclipse Ventures). Lux backed Applied Intuition to a $15B valuation in AV simulation. Eclipse co-led Wayve's $1.2B Series D. Both provide massive Series A and B follow-on capacity that automotive-specific VCs lack.

If you are a very early founder — pre-revenue, pre-product, raising under $1M, Automotive Ventures ($250K checks, pre-seed focus) and Trucks VC ($500K minimum) are your most realistic options. Both invest before revenue and evaluate on team and technical differentiation rather than traction metrics. Toyota Ventures also has an explicit seed mandate.

If you are a cross-border founder building for international automotive markets, Maniv Mobility invests across 9 countries. BMW i Ventures operates from Mountain View with global deal flow. Porsche Ventures and Hyundai CRADLE/ZER01NE have offices across 4-5 continents. All four understand international regulatory environments and OEM certification requirements beyond the US market.

Notable Automotive Exits (2024-2025)

Understanding recent exits helps calibrate what investors are optimizing for.

| Company | Event | Value | Sector |

|---|---|---|---|

| Kodiak Robotics (now Kodiak AI) | SPAC merger, listed NASDAQ September 2025 | Approximately $2.5B | Autonomous trucking |

| Aurora Innovation | Began driverless commercial trucking operations April 2025 | Public (AUR) | Autonomous trucking |

| Damon Motors | Listed NASDAQ November 2024 | Public | Electric motorcycles |

| Viaduct | Acquired by Sumitomo Rubber Industries October 2025 | $104M | Connected vehicle data/AI |

| Applied Intuition | Series F at $15B valuation (2025) | $15B valuation | AV simulation software |

The pattern is clear: autonomous systems and connected-vehicle data companies are producing the largest outcomes. Battery and EV companies are scaling but exits are happening through strategic acquisition (OEMs buying their supply chain) rather than public markets.

5 Pitch Tips for Automotive Seed Rounds

Based on our work with deal teams raising from the investors above, here is what actually moves the needle.

-

Lead with the OEM or Tier 1 relationship. Automotive VCs know that enterprise sales cycles in this industry run 18-36 months. A signed LOI, pilot agreement, or even a confirmed meeting with an OEM procurement team dramatically changes your seed narrative. Organize these documents prominently in your data room.

-

Show the certification roadmap. Whether it is ISO 21434 for cybersecurity, ASIL for functional safety, or UL for battery components, investors want to see that you understand the regulatory path and have budgeted for it. Based on our work with deal teams, certification timelines are the most common reason automotive seed rounds take longer than founders expect.

-

Quantify the hardware-to-software ratio. Automotive VCs evaluate your capital efficiency differently depending on whether you are selling hardware, software, or both. If you are hardware-heavy, show your BOM cost glide path from prototype to production. If you are software-first, demonstrate your integration cost per OEM platform.

-

Name your competitive moat explicitly. The automotive supply chain has hundreds of startups at every layer. State clearly whether your advantage is IP (patents, trade secrets), data (proprietary training data, OEM telemetry access), relationships (exclusive pilot agreements), or speed (faster integration, shorter certification cycle).

-

Prepare for multi-party diligence. Automotive seed rounds often involve a lead VC plus an OEM CVC co-investor, each with different strategic interests. Use separate data room links with tailored document sets for each investor and track engagement across all conversations from one dashboard.

Frequently Asked Questions

I'm a 3-person team building solid-state battery materials raising a $4M seed — which automotive VCs understand deep-tech hardware timelines?

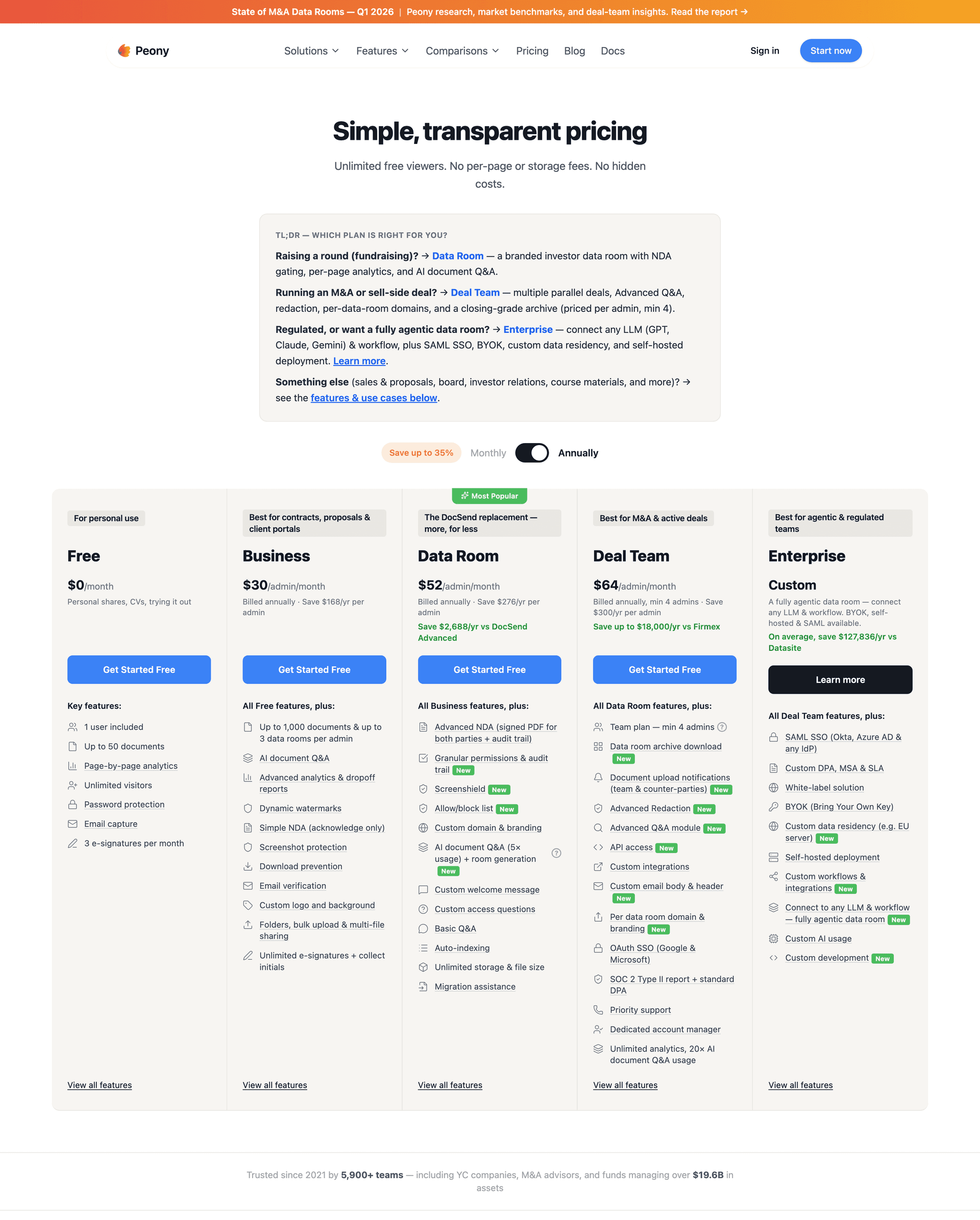

Volta Energy Technologies is your first call — they spun out of Argonne National Laboratory and run lab-level technical diligence that other VCs cannot match. Their Fund II is targeting $500M and they led NanoGraf's $65M round in 2024. Toyota Ventures writes $2-5M seed checks and has backed 27 seed-stage companies including battery and hydrogen startups. Both understand that battery startups need 3-5 years before production-scale revenue. When you share cell-test data and patent filings with these firms, use Peony's data room with dynamic watermarks that embed each viewer's identity into every page — so if your IP circulates, you know exactly who shared it. Business tier is $30 per admin per month for teams managing multiple investor relationships. Unlike Google Drive which has zero per-page engagement tracking, Peony shows you exactly which cell-test pages each VC reviewed and for how long.

We're a seed-stage automotive cybersecurity startup with $300K ARR from two Tier 1 suppliers — how do we position for a $3M round?

Automotive cybersecurity is growing at 15.3% CAGR to $18.88B by 2034 (Precedence Research, 2025), so your timing is strong. Lead with the Tier 1 supplier contracts as proof of OEM-adjacent traction and ISO 21434 compliance readiness. Autotech Ventures and BMW i Ventures both invest in connected-vehicle security. Porsche Ventures has cybersecurity as an explicit thesis area with $3-8M seed checks. Structure your data room with a compliance section showing your certification roadmap, penetration test results, and supplier agreements. Peony's screenshot protection blocks and logs capture attempts on sensitive security architecture documents — critical when sharing exploit-mitigation details with multiple investors simultaneously. This is something DocSend cannot detect on any plan, leaving your exploit-mitigation IP exposed to untracked screen captures.

I'm building a software-defined vehicle platform and need to raise $5M seed from investors who actually understand zonal E/E architectures — who should I pitch?

SDV is projected to reach $3.3T by 2034 at 31.2% CAGR (InsightAce Analytic, 2025), so this is the hottest automotive software category right now. Autotech Ventures and Trucks VC move fastest at seed for pure software plays — Trucks targets 10% ownership with $500K-2M checks and plans 30 investments from their new $70M fund. Maniv Mobility also writes $2-5M seed checks and has deep connected-vehicle expertise through portfolio companies like Nexar and Hailo. For your pitch, highlight integration partnerships with at least one OEM or Tier 1 supplier. Upload your technical architecture docs and pilot agreements to Peony, where AI auto-indexing organizes everything in under 3 minutes and page-level analytics show you which investors spent time on your architecture diagrams versus your go-to-market slides. Compared to Dropbox which offers no watermarking or leak tracing, Peony ensures your zonal architecture IP stays attributable to every viewer.

Our EV charging startup just closed a $1.5M pre-seed — when should we start building relationships with OEM corporate VCs like Toyota Ventures or Stellantis Ventures for our seed round?

Start now, 6-9 months before your seed raise. OEM CVCs move slower than dedicated automotive VCs because investment committees involve corporate strategy teams. Toyota Ventures is the most active OEM CVC at seed with $800M in AUM and an explicit seed mandate. Stellantis Ventures has EUR 300M and runs an annual Venture Awards program that surfaces seed-stage companies. Hyundai's ZER01NE Fund III just launched with $91.4M targeting early-stage startups. Build a lightweight data room in Peony today with your pitch deck, charging-site pipeline, and unit economics model. Share read-only links with NDA gates so corporate investors must sign before viewing — their legal teams expect this formality. You can set this up in under 5 minutes. Versus legacy platforms like Datasite that charge $15,000 or more per deal, Peony lets you run professional NDA-gated diligence from your first investor conversation at a fraction of the cost.

I'm raising a $2M seed for an AI-powered fleet electrification platform — should I target automotive-specific VCs or generalist deep-tech funds?

Target automotive-specific VCs first because they close faster and add more operational value at seed. Trucks VC backed Bingo Technologies at $1.9M seed for fleet electrification in April 2025 — this is exactly their thesis. Maniv Mobility invested in Harbinger Motors for medium-duty EVs and Revel for fleet charging. If your AI layer is genuinely differentiated, Eclipse Ventures writes larger checks from their $1.3B fund and backed Ever for AI-native EV retail. Generalists like Lux Capital are better as Series A co-leads after you have fleet deployment data. When pitching multiple firms in parallel, Peony lets you create separate data room links with different document sets for each investor — automotive VCs see your fleet contracts while deep-tech funds see your AI benchmarks. Track engagement across all from one dashboard. ShareFile offers no per-link document segmentation or investor-level analytics, so you would have no way to tailor access or measure engagement across parallel conversations.

We manufacture ADAS sensor components in Michigan and want to raise from a VC who can introduce us to OEM procurement teams — which investors have real OEM relationships?

Fontinalis Partners is co-founded by Bill Ford Jr., executive chairman of Ford Motor Company, and operates from Detroit with direct OEM access across the Big Three. BMW i Ventures backed Kodiak Robotics through to its SPAC IPO in 2025 and has 11 unicorns in portfolio — they provide genuine Tier 1 introductions. Robert Bosch Venture Capital invests from a $270M sixth fund and their parent company is the world's largest automotive supplier, so portfolio companies get pilot access across Bosch's OEM relationships. GM Ventures, while primarily Series A and later, is worth building a relationship with now for follow-on capital. Organize your supplier qualification docs, test data, and PPAP documentation in Peony's data room with Smart Q&A — investors submit technical questions, AI drafts responses, and your engineering team reviews before sending. Unlike Box which has no built-in Q&A workflow or AI-drafted response capability, Peony keeps technical diligence questions and answers in one auditable thread.

I'm a solo founder building V2X infrastructure tech raising $1M — is this subsector still attracting VC interest after government mandate delays?

V2X is projected to grow from $2.87B in 2025 to $18.67B by 2030 at 45.43% CAGR (Mordor Intelligence, 2025), but the growth is shifting from V2I government mandates toward V2N network-based services. Investors are cautious on infrastructure plays that depend on municipal rollout timelines. At $1M, target Automotive Ventures — they write smaller seed checks around $250K and focus on connected-car data plays that could include V2N. Trucks VC at $500K-2M is another option if you can frame V2X as fleet safety infrastructure rather than government-dependent connectivity. For a solo founder, Peony's data room takes under 5 minutes to set up, and the free tier lets you share your pitch deck while you are still in early conversations, with password protection on the Business plan ($30 per admin per month). When you move to deeper diligence, Business at $30 per admin per month adds page-level analytics to track which investors are engaging. Unlike OneDrive which offers no document-level watermarking or forwarding detection, Peony protects your V2X protocol specs with dynamic watermarks from day one on the Data Room plan ($52 per admin per month).

Our autonomous driving simulation startup raised $3M seed from Lux Capital — now we're adding automotive OEM CVCs to our cap table for Series A. How should we manage multi-party diligence?

OEM CVCs like Toyota Ventures, BMW i Ventures, and Stellantis Ventures each have different strategic interests and competitive sensitivities — never give them identical data room access. Create separate Peony data room links for each OEM CVC with tailored document sets: BMW sees your European deployment roadmap, Toyota sees your commercial trucking pipeline, Stellantis sees your multi-brand integration capability. Dynamic watermarks embed each viewer's identity so if simulation IP circulates internally at an OEM, you can trace it. Lux Capital backed Applied Intuition to a $15B valuation in this exact space, so leverage their introductions. The Data Room tier at $52 per admin per month supports unlimited data rooms with granular per-investor access controls — essential when managing competitive OEM investors in a single round. Versus legacy platforms like Intralinks that charge per-page fees and require multi-week onboarding, Peony gives you unlimited rooms with per-investor access controls in under 5 minutes.

We're a battery recycling startup with a working pilot and $500K in revenue — is Volta Energy Technologies or Eclipse Ventures a better fit for our $6M seed?

Both are strong but serve different needs. Volta Energy Technologies is laser-focused on battery and energy storage — they led NanoGraf's $65M round, backed Solid Power and Our Next Energy, and run diligence through Argonne National Laboratory's research network. If your recycling process has novel chemistry, Volta's technical depth is unmatched. Eclipse Ventures backed Redwood Materials and operates across a broader $2.5B portfolio focused on physical industries — they add manufacturing scale-up expertise and industrial buyer introductions. If your pilot is chemistry-proven and you need help with throughput and factory economics, Eclipse is stronger. Pitch both, but tailor your materials. Peony's AI auto-indexing organizes your pilot data, lab reports, and financial models in under 3 minutes, and you can share separate data room links with each firm tracking engagement independently. Compared to email attachments or WeTransfer where you lose all visibility the moment you hit send, Peony shows whether Volta spent time on your chemistry data while Eclipse focused on your factory economics — so you know exactly how to tailor each follow-up.

I'm a European founder building automotive aftermarket AI and want to raise seed from US automotive VCs — how realistic is cross-border fundraising in this space?

Very realistic in 2026. Maniv Mobility invests across 9 countries from their New York base and backed companies in Tel Aviv, Mexico City, and Bangalore. BMW i Ventures operates from Mountain View and invests globally. Porsche Ventures has offices worldwide with EUR 250M earmarked for investments. Automotive Ventures in Atlanta focuses on dealership and aftermarket tech specifically — Steve Greenfield has overseen $1B in automotive tech acquisitions and understands aftermarket unit economics. The key barrier is not geography but OEM validation: US automotive VCs want to see at least one North American pilot or LOI. When sharing diligence materials across time zones, Peony supports link expiry that ensures access closes automatically after your defined window, and NDA gates require each investor to sign before viewing sensitive supplier or pricing data. The Data Room tier at $52 per admin per month handles unlimited rooms across all your investor conversations. Compared to Firmex or Ansarada that charge thousands per deal with multi-week onboarding, Peony lets cross-border founders run professional diligence from day one without enterprise procurement cycles.

Related Resources

- Top Transportation and Mobility Investors — ride-sharing, freight movement, and multi-modal network investors

- Top Logistics and Supply Chain Investors — warehousing, fulfillment, and cold-chain VCs

- Top Climate Tech Investors — clean energy, carbon capture, and sustainability funds

- Top Hardware and IoT Investors — robotics, sensors, and deep-tech hardware VCs

- Top Deep Tech Investors — frontier technology and science-based startups

- Best Data Rooms for Startups — comparing data room options for fundraising

- Startup Data Room Checklist — what to include in your investor data room

- How to Send Your Pitch Deck to Investors — secure sharing best practices

- Fundraising Solutions — Peony's fundraising data room features

- Venture Capital Data Rooms — purpose-built for VC diligence

You might also like

Jun 29, 2026

How to Share an Interactive LP Report With Your Limited Partners (Securely)

Jun 26, 2026

Venture Debt Data Room: Why Lenders Underwrite the Floor, Not the Ceiling (2026)

Jun 25, 2026

SPV Data Room: The Syndicate Lead's Playbook for Co-Investment Deals (2026)