IPO Readiness Checklist 2026: 10 Steps to Going Public

Co-founder at Peony. Former M&A at Nomura, early-stage VC at Backed VC, and growth-equity / secondaries investor at Target Global. I write about investors, fundraising, and deal advisors from the deal-side perspective I spent years in.

IPO Readiness Checklist 2026: 10 Steps to Going Public

Last updated: May 2026

Quick answer: IPO readiness is the 18-to-24-month preparation arc that turns "we think we're ready" into "we have S-1 audit trail proof." The 10 steps span go/no-go decision (months -24 to -18), working-group assembly and audit firm upgrade (months -18 to -12), SOX 404 gap remediation and pre-IPO diligence file build (months -12 to -6), S-1 drafting and confidential JOBS Act submission (months -6 to -3), SEC review with 2-3 comment cycles and roadshow (months -3 to 0), pricing and Day-1 trading, lockup management at day 180, and Year 1 SEC reporting cadence (8-K within 4 business days, 10-Q within 40 days for accelerated filers, 10-K within 60 days for large accelerated filers). All-in transaction cost runs 4-7 percent of gross proceeds plus $3-5 million in legal, audit, and IR setup; 60 percent of newly public companies spend $1 million-plus annually on ongoing compliance per PwC's IPO cost study.

This checklist is written for four specific people: the CFO 12 months from confidential S-1 filing mapping SOX 404 scope and audit-firm-upgrade timing against a late-2026 or early-2027 listing window; the general counsel managing S-1 disclosure obligations preempting SEC staff comments on customer concentration, generative-AI risk factors, and ASC 280 segment reporting; the underwriter coverage banker running readiness assessments and beauty-contest gross-spread math for a Series D-and-later issuer; and the late-stage-startup founder evaluating the IPO-versus-sell-versus-stay-private decision at $200M-plus ARR with a $1.5B-plus private valuation.

The single hardest question in this entire process is not "are we ready?" — it is "can we prove it in the data room six months before the bell rings?" The companies that price clean in 2024-2025 had documentation visible to the underwriter syndicate, outside counsel, and the audit partner on a same-day basis; the ones that pulled deals or repriced down all had 60-to-90-day documentation gaps in SOX evidence, customer-concentration disclosure, or generative-AI risk-factor language. This is the 10-step framework that turns the answer from "we think we're ready" into "we have S-1 audit trail proof."

I run Peony, a data room platform used by 6,800+ deal teams. I see inside hundreds of pre-IPO and post-IPO documents every quarter — the auditor confirmations, the SOX evidence libraries, the redlined S-1 drafts that bank syndicates pass between Morgan Stanley, Goldman Sachs, JPMorgan, and BofA, and the board-meeting minutes that committees review at 11pm the night before a filing. The companies that price clean and trade well are the ones whose readiness was visible in the data room six to twelve months before the bell. The ones that delay or pull deals usually had the same gap: documentation that lagged 60 to 90 days behind the schedule the bankers built.

This post is the company-side IPO readiness checklist — what your team needs to assemble, file, and survive before and after the bell. If you are an investor evaluating an IPO target's S-1 risk factors, head to the investor due diligence guide. If you are researching pre-IPO M&A trends and how the public-market window shapes private-deal multiples, see M&A trends and facts. For the underlying VDR mechanics that the IPO working group runs on, the virtual data room guide covers the platform-level concepts. For biotech-specific pre-IPO documentation, the biotech data room guide maps the FDA correspondence and clinical-data layers.

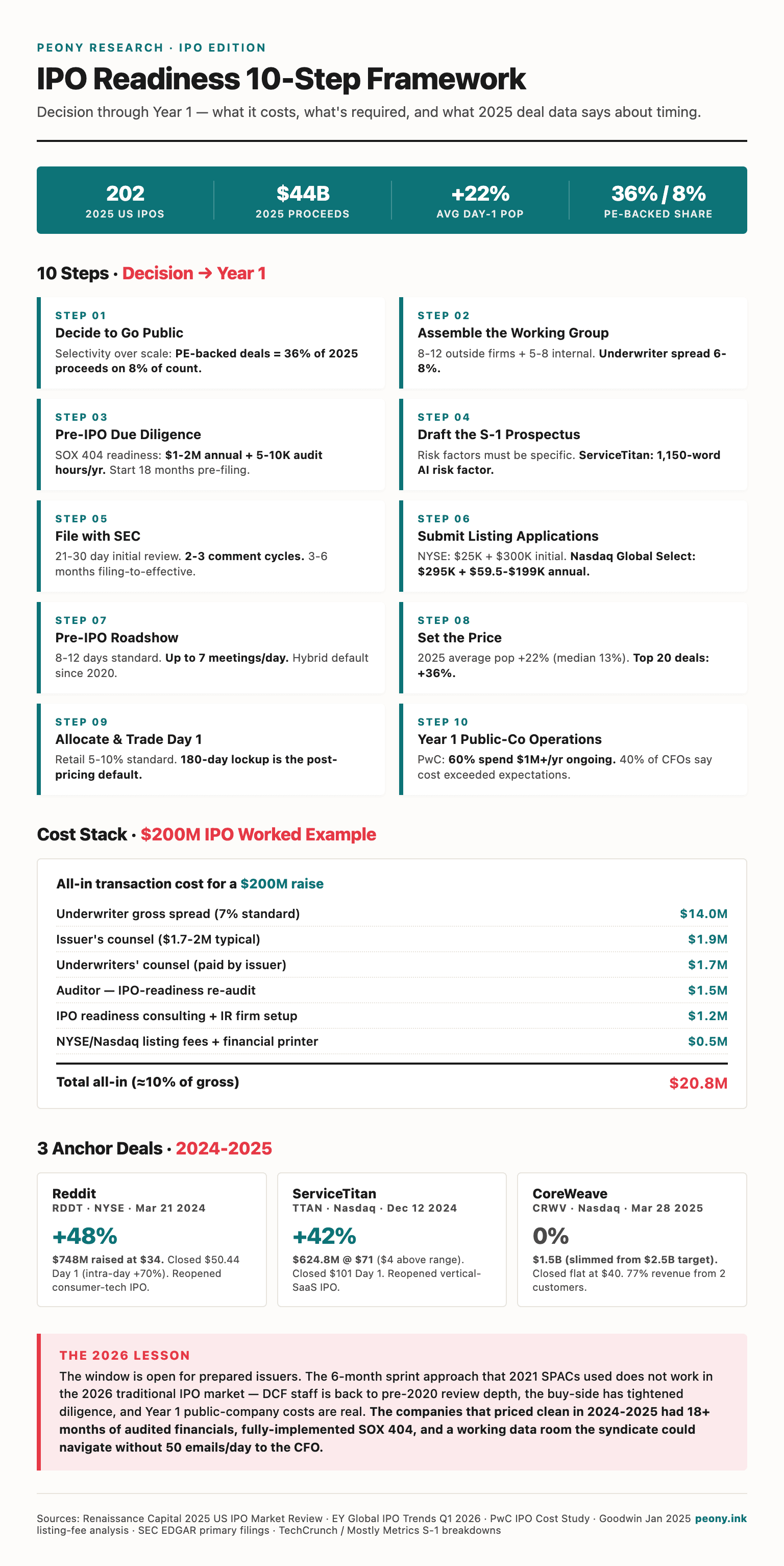

TL;DR: 2025 saw 202 US IPOs raise $44 billion per Renaissance Capital's 2025 US IPO Market Review (January 2 2026), with average Day-1 pop of 22 percent (median 13 percent) and the top 20 deals averaging +36 percent. PE-backed deals delivered 36 percent of global proceeds on just 8 percent of deal count per EY Global IPO Trends 2025 (using Dealogic, S&P Capital IQ, PitchBook, Mergermarket data). Q1 2026 globally: 230 IPOs raised $40.6 billion (count down 23 percent year-over-year, proceeds up 36 percent) per EY Global IPO Trends Q1 2026, with defense the largest Q1 sector. Pipeline names include Cerebras (S-1 filed April 17 2026), Databricks ($130 billion private valuation), and Stripe ($100 billion-plus). Below is the 10-step framework with the deal-data and 2025 case anchors that actually shape modern IPOs — plus the data room math that determines whether your prospectus stays on time. Total all-in going-public cost runs 4 to 7 percent of gross proceeds plus $3 million to $5 million in legal, audit, and IR setup, with 60 percent of newly public companies spending $1 million-plus annually on ongoing compliance per PwC's IPO cost study.

Why Are Companies Going Public Again in 2026?

Companies are going public again in 2026 because the institutional demand window reopened in 2024 and held through 2025, with 202 US IPOs raising $44 billion per Renaissance Capital's 2025 US IPO Market Review and a 22 percent average Day-1 pop signaling genuine buy-side appetite — but the market is selective in a way it was not during the 2021 free-money cycle.

The 2024-2025 reopening

The IPO market collapse of 2022-2023 (where US deal count fell to roughly 70-90 issuances per year, the lowest in a decade) ended in March 2024 with three signal deals. Reddit priced March 21 2024 on the NYSE under ticker RDDT, raising $748 million at $34 per share with Morgan Stanley, Goldman Sachs, JPMorgan, and Bank of America leading. The stock closed at $50.44 on Day 1 (+48 percent), with intra-day high of $57.80 (+70 percent) — the strongest social-media debut since Twitter and the deal that re-opened the consumer-tech IPO window. Astera Labs followed days later with a similar Day-1 pop, validating the AI-infrastructure IPO thesis. Then ServiceTitan priced December 12 2024 on Nasdaq under ticker TTAN, raising $624.8 million at $71 per share (8.8 million shares, $4 above the marketed range) with Morgan Stanley and Goldman Sachs leading. The stock closed at $101 on Day 1 (+42 percent) — the deal that re-opened the vertical-SaaS IPO window for late 2024 and early 2025 issuers.

By full-year 2025, Renaissance Capital tracked 202 US IPOs raising $44 billion. EY Global IPO Trends Q1 2026 reported 230 global IPOs raising $40.6 billion in the first quarter alone — count down 23 percent year-over-year as the market consolidated around larger deals, but proceeds up 36 percent. Defense was the largest Q1 2026 sector, reflecting the geopolitical capex cycle.

Who is going public

The structural shift in the 2024-2025 reopening is the dominance of PE-backed issuers. Per EY Global IPO Trends 2025 (using Dealogic, S&P Capital IQ, PitchBook, Mergermarket data), PE-backed deals delivered 36 percent of global proceeds on just 8 percent of deal count in 2025 — meaning sponsors were using the IPO window selectively for their largest, most-prepared portfolio companies rather than the broad-based platform-exit strategy of 2021. The 2021 SPAC peak was 613 SPAC IPOs at $145 billion of proceeds; 2025 saw 138 SPAC IPOs raising $25.8 billion, a meaningful rebound from 2022-2023 but still well below peak.

The 2026 pipeline reflects the same selectivity. Cerebras filed its S-1 on April 17 2026 in the AI-chip space. Databricks sits at a $130 billion private valuation, regularly cited as the largest pre-IPO software company. Stripe at $100 billion-plus has stayed private through multiple secondary cycles. Shein delayed its IPO multiple times due to regulatory and geopolitical complications. Klarna priced September 10 2025 on the NYSE under ticker KLAR, raising $1.37 billion — the largest IPO of 2025. CoreWeave priced March 28 2025 on Nasdaq under ticker CRWV, raising $1.5 billion (37.5 million shares at $40, slimmed from the original $2.5 billion target at $47-55) with Morgan Stanley, JPMorgan, and Goldman Sachs leading. The stock closed flat at $40 on Day 1 — softer demand than the Reddit and ServiceTitan cycle, but still the biggest tech IPO since 2021.

The lesson from CoreWeave, Reddit, and ServiceTitan together: in 2025, institutional buyers will fund a $1 billion-plus deal at a fair price, but they will not pay 2021 multiples for unproven concentration risk. CoreWeave's S-1 disclosed 77 percent of revenue from two customers (Microsoft 62 percent) per the Mostly Metrics S-1 breakdown, and the soft pricing reflects that disclosure.

What this means for your readiness assessment

For a CFO targeting a late-2026 or early-2027 IPO, the implication is that the demand window is open, but the bar on quality of process is high. The companies that priced clean in 2024-2025 had three things in common: 18-plus months of audited financials by a recognized firm, fully-implemented SOX 404 control environment, and a working data room that the underwriter syndicate could navigate without 50 emails per day to the CFO. The companies that pulled deals or repriced down all had visible documentation gaps in at least one of those three areas.

The 2026 question for any IPO candidate is not whether the market is open — it clearly is for prepared issuers. The question is whether your readiness work was done 18 months ago. The 6-month sprint approach that some 2021-vintage SPAC mergers used does not work in the 2026 traditional IPO market. The Division of Corporation Finance staff is back to pre-2020 review depth, the institutional buy-side has tightened diligence standards, and the public-company-cost trap is real for issuers who underestimate Year 1 ongoing compliance.

The retrospective from the 2024-2025 cycle is also instructive on timing. Reddit went public 5 years after its last private financing round, ServiceTitan 7 years after its first major round, CoreWeave 8 years after founding, and Klarna nearly 20 years after founding. The 2026 IPO candidates are not 3-year-old fast-scale companies — they are mature businesses with audited operating history and management teams who have lived through revenue cycles. The companies that priced poorly or pulled deals in 2024-2025 generally had less than 3 years of compliant audited financials or material weaknesses in their pre-IPO ICFR environment.

Who Belongs on the IPO Team — and What Will They Cost?

The IPO working group typically includes 8 to 12 outside parties plus a 5 to 8 person internal core, and the all-in cost lands at $11 million to $19 million for a $200 million IPO before listing fees and ongoing compliance — driven by the underwriter gross spread (7 percent standard, $14 million on a $200 million raise), legal ($1.7 million to $2 million typical, with outliers like Circle's $7.3 million), audit ($1 million to $2 million-plus for IPO-readiness re-audits), and 18 to 24 months of IPO-readiness consulting before filing.

The team

Internal core (5 to 8 people). CEO, CFO, controller, head of legal/general counsel, head of investor relations (often hired specifically for the IPO), head of internal audit (often hired specifically), and 1 to 2 finance managers running the SEC reporting workstream. Most pre-IPO companies under-staff the IR and internal audit roles by 12 months — the readiness cycle assumes they are in place, and gaps show up in the first 10-Q.

Underwriters (typically 4 to 8 banks). Lead bookrunners (typically 2 to 3 of Morgan Stanley, Goldman Sachs, JPMorgan, Bank of America for $500 million-plus deals — these four led the bulk of 2024-2025 mega-IPOs from Reddit through CoreWeave through Circle through Klarna). Mid-size or sector-specialist co-managers (Jefferies, Citi, Barclays, Wells Fargo, RBC, Cowen, Stifel, Raymond James, Piper Sandler depending on size and sector). Gross spread is 7 percent standard for $20 million to $100 million deals (94 percent of US deals at this size band per Goodwin January 2025 IPO economics analysis), with a typical range of 6 to 8 percent. Mega-deals at $1 billion-plus negotiate down to 1 to 2 percent — Circle's June 2025 $1.05 billion IPO at $31 (NYSE CRCL, +168 percent Day-1 close to $83.23) reportedly paid roughly 4 percent gross spread per Fortune coverage.

Issuer's counsel (typically 1 firm). Cooley, Wilson Sonsini, Latham, Skadden, Davis Polk, Weil, Goodwin, Kirkland are the most active 2024-2025 issuer-side IPO firms. Typical fee: $1.7 million to $2 million on a $200 million IPO. Underwriters' counsel runs separately and is typically Cravath, Simpson Thacher, Sullivan and Cromwell, Skadden, or Latham — typical fee $1.5 million to $2 million paid by the issuer.

Auditor. Big 4 (PwC, Deloitte, EY, KPMG) for 95 percent of 2024-2025 IPOs above $200 million; mid-tier (BDO, Grant Thornton, RSM) for some smaller and biotech-specific deals. Typical IPO-readiness re-audit fee: $1 million to $2 million-plus for the first compliant fiscal year, with ongoing audit fees $750,000 to $1.5 million per year post-IPO.

Service providers. IPO readiness consulting (Big 4 advisory, Withum, Aprio, RSM consulting; typical scope $200,000 to $500,000 fixed fee for an 18-month gap-assessment-to-go-live engagement). IR firm (ICR, Edelman Smithfield, Sard Verbinnen, Joele Frank; typical retainer $30,000 to $60,000 per month from 12 months pre-IPO through 12 months post-IPO). Financial printer / EDGAR filer (DFIN, Donnelley Financial Solutions, Workiva; typical $100,000 to $300,000 per filing cycle). Transfer agent (Equiniti, Computershare, Continental Stock Transfer; typical $50,000 to $100,000 setup plus ongoing fees). Virtual data room for the IPO working group's document repository, where underwriter syndicate, auditor, outside counsel, and SEC comment-response evidence all flows — this is where Peony fits.

Board and governance build. Pre-IPO companies typically need to hire 3 to 5 independent directors before filing (NYSE and Nasdaq both require a majority-independent board within 12 months of listing), structure audit committee, compensation committee, nominating/governance committee, and adopt code of ethics, whistleblower policy, insider trading policy, and clawback policy. Total board fees: $300,000 to $750,000 per year ongoing.

Cost breakdown for a $200 million IPO

| Cost line | Typical 2026 cost | Source / benchmark |

|---|---|---|

| Underwriter gross spread (7%) | $14.0M | 7% standard for $20-100M raises (94% of deals); range 6-8% per Goodwin Jan 2025 |

| Issuer's counsel | $1.7-2.0M | Typical Big Law IPO ranges; Circle disclosed $7.3M legal cost outlier |

| Underwriters' counsel | $1.5-2.0M | Paid by issuer per standard engagement |

| Auditor (IPO readiness re-audit) | $1.0-2.0M+ | Big 4 typical first-cycle fees |

| IPO readiness consulting | $0.2-0.5M | Big 4 advisory fixed-fee scopes |

| IR firm setup (12 months pre + 12 months post) | $0.5-1.0M | $30-60K per month retainer |

| Financial printer / EDGAR filer | $0.1-0.3M | DFIN / Workiva published rates |

| Transfer agent setup | $0.05-0.1M | Equiniti / Computershare published rates |

| SEC registration + FINRA filing fees | ~$0.06M combined | SEC FY2026 rate $138.10 per $1M (eff. Oct 1, 2025, down from $153.10); FINRA corporate financing cap raised to $1.125M on July 1, 2025 |

| Virtual data room (typical 18-24 month engagement) | $0.025-0.1M+ Datasite range; $0.000624 Peony per admin/yr | industry analyses pricing 2026; Peony published rate |

| Listing fees (NYSE) | $0.025M application + $0.3M initial flat | NYSE 2026 listed company manual |

| Listing fees (Nasdaq Global Select) | $0.295M initial all-inclusive | Nasdaq 2026 listing fee schedule per Goodwin |

| All-in total (including listing) | $19-23M | 4-7% of gross proceeds plus $3-5M legal/audit/compliance |

The single biggest variance line is virtual data room cost. Datasite's per-page model (roughly $0.60 per page, $7,000 for 10,000 pages per third-party VDR pricing surveys (2026)) and enterprise quote pricing ($50,000 to $100,000-plus per year per third-party VDR pricing surveys (2026)) means that a $200 million IPO data room with 30,000 to 50,000 pages of historical materials commonly runs $30,000 to $60,000 in per-page overage on Datasite alone. Intralinks runs in the same range ($7,500 for 10,000 pages per third-party VDR pricing surveys). DFIN's Venue platform was rebuilt and relaunched in September 2025 with quote-based pricing typically bundled with their ActiveDisclosure SEC filing product.

Peony's flat $52 per admin per month on the Data Room plan (see pricing) removes the per-page exposure entirely. Enterprise VDR realized cost typically lands at 2 to 10 times the initial quote due to per-page, per-user, and concurrent-room overages — and an IPO working group with 4 to 6 underwriter banks, 2 to 3 law firms, the auditor team, and the SEC comment response cycle typically maintains 3 to 5 concurrent rooms (the main S-1 drafting room, a board-only room, an underwriter beauty-contest room, an SEC comment-response room).

Underwriter spread tier table

| Deal size | Standard gross spread | Notes |

|---|---|---|

| Sub-$20M | 8-10% | Smaller specialty banks; less competitive bookrunner pool |

| $20M-$100M | 7% standard (94% of deals) | Middle of the standard band; range 6-8% per Goodwin Jan 2025 |

| $100M-$500M | 6.5-7% | Negotiable; lead-bank position matters more than spread |

| $500M-$1B | 5-6.5% | More leverage; mid-cap CFOs negotiate retail allocation aggressively |

| $1B-$5B | 3-5% | Mega-deal pricing; Klarna $1.37B Sep 2025 precedent |

| Over $5B | 1-3% | Mega-deal floor; Circle paid roughly 4% per Fortune coverage |

The spread compression at scale reflects three structural factors: more bank-syndicate competition (10 to 15 banks pitching the bookrunner mandate); larger absolute fee dollars on the lead bank (5 percent of $5 billion is $250 million, easily justifying a fee compression to win the mandate); and more sophisticated CFO negotiation leverage (mega-deal CFOs typically have prior IPO experience or M and A advisory relationships that produce specific spread benchmarks).

When the team starts forming

The IPO working group typically forms 18 to 24 months before the targeted filing date. Months 24 to 18 pre-filing: hire IR firm, hire head of internal audit, engage IPO readiness consulting (Big 4 advisory). Months 18 to 12 pre-filing: identify and onboard 3 to 5 independent directors, structure committees, draft governance policies. Months 12 to 6 pre-filing: run underwriter beauty contests, select issuer's counsel, finalize auditor (typically incumbent if Big 4, otherwise transition to Big 4). Months 6 to 0 pre-filing: kick off S-1 drafting, finalize SOX 404 control environment, complete IPO-readiness re-audit. Filing date through effectiveness: SEC review cycles, roadshow prep, pricing call. The companies that compress this timeline typically run into avoidable friction during S-1 drafting, where the working group is still onboarding while the staff comments are arriving — and the comment cycle compounds quickly when the team is not in place.

What Goes in the Pre-IPO Due Diligence File?

The pre-IPO due diligence file is the structured documentation set the underwriter syndicate, outside counsel, and auditor build to support every claim in the S-1 — distinct from the investor-side investment due diligence the buy-side runs on a portfolio company, this is process-side due diligence that creates the evidence trail behind the registration statement. The file typically spans 30,000 to 50,000 pages across 8 to 10 categories and lives in the IPO working group's data room from kick-off through SEC effectiveness.

The 9 categories of the pre-IPO DD file

1. Corporate organization and governance. Articles of incorporation, bylaws, board minutes for the prior 36 to 48 months, committee minutes, written consents, equity plans, stockholder agreements, voting agreements, registration rights agreements, and the cap table (typically Carta export with full equity history). Underwriter counsel reads every board minute looking for material events, related-party transactions, and gaps in governance — pre-IPO companies whose board minutes are sparse get extensive comments.

2. Audited and reviewed financial statements. Three years of audited statements per Regulation S-X for issuers above the EGC threshold ($1.235 billion in revenue per JOBS Act 2024 indexing), two years for emerging growth companies. Plus interim reviewed quarterly statements for the most recent 4 quarters, quality of earnings (QofE) workpapers if available, and the underlying audit binder. The IPO readiness re-audit typically spans 6 to 12 months and is the single largest source of schedule slip.

3. Tax filings and tax-position memos. Three years of federal, state, and foreign tax returns. Tax opinions on positions taken (R and D credits, foreign-derived intangible income, transfer pricing, state-tax nexus). Sales tax and use tax compliance posture. The IRS's Schedule UTP discloses uncertain tax positions, and the SEC staff often probes alignment between Schedule UTP and S-1 risk-factor language.

4. Material contracts. Customer contracts representing more than 10 percent of revenue (plus aggregations across customer concentration thresholds); supplier contracts where the issuer is materially dependent; lease agreements for material real estate; license agreements for material IP; partnership and joint venture agreements; debt agreements with covenants summarized. The CoreWeave S-1 disclosure of 77 percent of revenue from two customers (Microsoft 62 percent) is the canonical 2025 case study — the SEC staff probed disclosure quality, and the issuer ended up with a heavy concentration risk factor.

5. Intellectual property. Patent family list, trademark registrations, copyright registrations, IP assignment agreements with all current and former employees, IP indemnification language in customer contracts, and any pending or threatened IP litigation. For tech and biotech issuers, this category alone often runs 5,000 to 10,000 pages.

6. Litigation and regulatory. Litigation log (open and closed for the prior 5 years, with materiality assessment), regulatory inquiry log (SEC, FTC, DOJ, state AGs, EU regulators), industry-specific regulatory correspondence (FDA for biotech, OFAC for fintech, state insurance regulators for insurance, FERC for energy). The S-1 risk factor section pulls heavily from this category.

7. Employment and benefits. Senior executive employment agreements, severance and change-of-control provisions, equity plan documents, 401(k) plan documents and audits, ERISA fiduciary minutes, and any pending or threatened employment litigation. Compensation counsel coordinates Item 402 disclosure (pay-versus-performance, CEO pay ratio, clawback) with this category.

8. SOX 404 evidence repository. Control narratives, walkthroughs, test results, IT general controls, application controls, end-user computing controls, third-party SOC 1 reports, entity-level controls, and management remediation memos. Crowe and Moss Adams 2024 benchmarking finds 5,000 to 10,000 internal audit hours per year of SOX work for typical mid-cap public companies. Pre-IPO companies who scope SOX narrowly during readiness assessment often discover during the first compliant fiscal year that the actual scope is double.

9. ESG, cybersecurity, data privacy. ESG disclosures (increasingly mandatory for EU-exposed issuers under CSRD), cybersecurity incident response history (the SEC's 2023 cybersecurity disclosure rules require Item 1.05 8-K filing within 4 business days of a material cybersecurity incident), and data privacy compliance documentation (GDPR, CCPA, sector-specific frameworks like HIPAA and PCI DSS).

How the file actually lives

The pre-IPO DD file lives in the IPO working group's data room from kick-off through SEC effectiveness, with continued retention requirements post-IPO under SEC Rule 17a-4 (typically 7 years for broker-dealer related communications, 6 years for adviser communications, with public-company audit work-paper retention under PCAOB AS 1215 typically 7 years). The auditor needs same-day access to control narratives during the SOX cycle. The underwriter counsel needs same-day access to material contracts during S-1 drafting. The SEC comment response team needs same-day access to specific cited documents during comment cycles. Friction in document retrieval is consistently the #1 cause of schedule slip in IPO cycles.

Peony Data Room at $52 per admin per month supports the IPO DD file with AI auto-indexing sorting documents into the standard 9-category taxonomy in under 5 minutes; page-level analytics showing exactly which underwriter MD, outside counsel partner, or auditor manager reviewed which document and for how long; NDA gates requiring signed acceptance for every viewer; and audit trail logs that satisfy SEC Rule 17a-4 retention requirements.

How Do You Draft an S-1 That Survives SEC Review?

Drafting an S-1 that survives SEC review means producing a registration statement detailed enough to satisfy the Division of Corporation Finance staff on first review, defensible enough to survive 2 to 3 comment cycles, and disclosed enough to pre-empt the six recurring SEC comment letter themes that surface in 80 percent of 2026 S-1 reviews — and the 2024-2025 cycle reset the bar on what "detailed enough" means, with ServiceTitan's 1,150-word generative-AI risk factor and CoreWeave's 77-percent-revenue-concentration disclosure as the new reference points.

The S-1 architecture

A modern S-1 typically runs 250 to 400 pages and includes:

- Prospectus summary (5 to 15 pages) — business overview, summary financial data, summary risk factors, terms of the offering. Bankers and prospective investors read this section in detail; the rest gets skimmed.

- Risk factors (40 to 80 pages, 30 to 80 individual factors) — the most-read section by SEC staff and plaintiffs' lawyers. Modern S-1 risk factor architecture trends toward longer, more specific factors. ServiceTitan's November 2024 S-1 included a 1,150-word generative-AI risk factor that became an industry first per TechCrunch coverage — covering training-data IP exposure, model hallucination liability, competitive moat erosion, and regulatory uncertainty. The SEC staff now expects this level of specificity from materially exposed issuers.

- Use of proceeds (1 to 3 pages) — how the IPO proceeds will be deployed. Vague language ("general corporate purposes") draws comments; specific allocations (R and D, sales and marketing, working capital, debt repayment with named lender) survive.

- Capitalization and dilution (3 to 5 pages) — pre and post-offering cap table, dilution analysis for existing holders.

- Selected financial data and MD and A (40 to 80 pages) — three years of summary data plus management's discussion. The single longest-running source of SEC comments. Segment reporting under ASC 280 (post the FASB 2024 update) is a particular focus.

- Business (40 to 100 pages) — narrative description of products, markets, competition, growth strategy, regulatory environment, intellectual property. This section drives investor narrative; bankers spend the most time here.

- Management (10 to 25 pages) — executive bios, board bios, executive compensation under Item 402 (pay-versus-performance, CEO pay ratio, clawback policy disclosure under SEC's 2023 final rules).

- Principal stockholders (3 to 8 pages) — ownership table for 5-percent holders, directors, executive officers.

- Certain relationships and related-party transactions (3 to 10 pages) — Schedule of related-party transactions for the prior 3 years.

- Description of capital stock (5 to 15 pages) — terms of common stock, preferred stock, anti-takeover provisions.

- Underwriting (5 to 15 pages) — terms of the underwriting agreement, gross spread, lockup terms, stabilization mechanics.

- Legal matters and experts (1 to 2 pages) — counsel and auditor identifications.

- Financial statements (40 to 80 pages) — three years audited (or two for EGCs), interim reviewed.

The six recurring SEC comment letter themes

Per Division of Corporation Finance comment letter analysis 2024-2025:

- Customer concentration disclosure. Post-CoreWeave (77 percent of revenue from two customers, Microsoft 62 percent, per the March 2025 S-1), the SEC staff now expects quantified concentration disclosure with named-customer risk language wherever a single customer represents more than 10 percent of revenue. Narrative-only disclosure is no longer adequate.

- Generative AI risk factors. ServiceTitan's November 2024 S-1 1,150-word generative-AI risk factor became the industry reference point. The SEC staff probes training-data IP exposure, model hallucination liability, competitive moat erosion, and regulatory uncertainty for any materially AI-exposed issuer.

- Revenue recognition policy detail under ASC 606. Performance obligation identification, transaction price allocation, over-time-versus-point-in-time recognition. Multi-element arrangements draw heavy staff comments.

- Segment reporting under ASC 280. The FASB's 2024 segment disclosure update raised the bar on quantitative segment expense disclosure. The SEC staff is testing implementation in early 2026 filings.

- Going-concern and liquidity disclosure. Burn-rate language, cash runway projections, capital-need disclosure for any pre-profitability issuer.

- Material weakness disclosure in ICFR. Issuers who restated financials in the prior 36 months or remediated material weaknesses in the prior 12 months should expect detailed staff comments.

Confidential filing under JOBS Act EGC status

Most 2024-2025 issuers filed confidentially under JOBS Act emerging-growth-company status, which permits non-public S-1 review until 15 days before the launch of the roadshow. ServiceTitan, Reddit, CoreWeave, and Circle all used confidential filing. The mechanic is: file the confidential S-1 with the SEC, receive comment letters and respond confidentially through 1 to 2 cycles, then file the public S-1 (which incorporates the confidential cycle's responses) and proceed to the marketing window. The benefit is competitive — your pre-roadshow disclosures stay private until you are ready to market — and many CFOs now treat confidential filing as default for any deal under the EGC threshold.

Three S-1 drafting practices that compress timelines

Pre-circulate the risk factor draft 90 days before filing. Risk factors are the most-iterated section of a modern S-1, and the comment cycle compounds when the working group is still rewriting Section 1A on day 30 of the SEC review. Strong working groups distribute a complete risk-factor draft to the underwriter syndicate, outside counsel, and the auditor 90 days before the targeted filing date — meaning each party has reviewed and commented before the official drafting cycle begins. ServiceTitan's 1,150-word generative-AI risk factor was reportedly through 8 to 10 internal redrafts before the November 2024 filing.

Anchor the MD and A on segment-level KPI consistency. The MD and A is the second-most-commented section of a modern S-1, and the most common comment is inconsistency between non-GAAP measures discussed narratively and the GAAP segment data in the financial statements. Strong working groups build an MD and A KPI dashboard 60 days before filing showing every metric mentioned in the narrative, the source GAAP measure, the reconciliation to non-GAAP if applicable, and the segment-level breakdown. This eliminates the most common comment cycle round 2 finding.

Run a mock SEC review with retired staff. Several IPO advisory firms (notably Withum, Aprio, and former-staff partners at Big 4 firms) offer mock SEC review services where retired Division of Corporation Finance staff review the draft S-1 and produce a comment letter modeled on actual recent staff comments. Typical scope: $100,000 to $200,000 fixed fee for a 4-to-6-week review cycle starting 90 days before filing. The comments compress real SEC review by 1 to 2 cycles for issuers who incorporate them.

Peony Data Room at $52 per admin per month supports the S-1 drafting workflow with page-level analytics showing which sections each working-group lawyer reviewed; AI extraction pulling specific risk-factor language from precedent S-1 filings into your draft (Reddit, ServiceTitan, CoreWeave, Circle, Klarna are all useful precedents); and Smart Q and A with cited answers from your own audit and contract documents — saving 20 to 40 hours of associate time per comment-response cycle.

What Happens After You File With the SEC?

After you file the S-1, the Division of Corporation Finance staff issues a first comment letter within 21 to 30 days, you respond, the staff issues a second-round comment letter (typically narrower), you respond, and 2 to 3 comment cycles later the staff declares the registration statement effective — the full filing-to-effectiveness window typically runs 3 to 6 months on a clean process and 6 to 12 months when the staff probes accounting policies, revenue recognition, or risk-factor disclosure quality. In parallel, the company completes Blue Sky filings, FINRA notification, exchange application, and lockup-and-allocation paperwork.

The SEC review timeline

Day 1: File S-1. Confidentially under JOBS Act EGC status (most 2024-2025 issuers) or publicly. The filing date triggers the 21-to-30-day SEC initial review window.

Day 21 to 30: First comment letter. The Division of Corporation Finance staff issues a comment letter, typically 10 to 30 individual comments spanning the six recurring themes plus issuer-specific items. Staff comment letters are public 20 business days after issuer response (per SEC's 2005 confidential review policy update).

Day 31 to 60: First response. Issuer's counsel and the auditor draft responses to each comment, the issuer files an amended S-1, and the response cycle restarts.

Day 61 to 90: Second comment letter. Typically narrower, focusing on items that did not resolve in the first cycle.

Day 91 to 120: Second response and (if needed) third comment cycle. By this stage, comments are typically narrow technical items (specific accounting language, specific risk-factor wording).

Day 90 to 180: Effectiveness. The staff declares the registration statement effective, the issuer files the Rule 424(b) prospectus, and the IPO can price.

Parallel workstreams

Blue Sky filings. State-level securities registration is largely preempted by federal law for NYSE and Nasdaq listings (per NSMIA), but 1933 Act Rule 251 Blue Sky filings still apply for some Regulation A and Regulation Crowdfunding offerings. For traditional S-1 IPOs, Blue Sky paperwork is administrative.

FINRA notification. The underwriter syndicate files a FINRA Rule 5110 corporate financing review submission, which FINRA reviews for fairness of underwriting compensation. Typical review timeline: 30 to 45 days, often parallel to SEC review.

Exchange application. NYSE charges $25,000 application fee plus $300,000 initial flat listing fee per the NYSE 2026 listed company manual, with annual fees ranging $80,000 to $500,000 depending on shares listed. Nasdaq Global Select tier charges $295,000 initial all-inclusive plus $59,500 to $199,000 annual all-inclusive per Goodwin's January 2025 IPO economics analysis. Nasdaq Global tier and Nasdaq Capital Market tier have lower fees but more limited investor following. Most 2024-2025 mid-to-large IPOs chose NYSE (Reddit RDDT, Circle CRCL, Klarna KLAR, eToro ETOR, Newsmax NMAX) or Nasdaq Global Select (ServiceTitan TTAN, CoreWeave CRWV, Chime CHYM); the choice often comes down to peer-group fit and analyst coverage rather than fee differential.

EDGAR Next. The SEC's modernized EDGAR filing system (EDGAR Next, rolled out 2024-2025 in phases) requires registered agents and individual filer authentication for all filings — a workflow change that pre-IPO companies should test in dry-run before the first live filing. Most IPO companies engage their financial printer (DFIN, Workiva, Donnelley Financial Solutions) to manage EDGAR Next filing logistics.

SOX 404 final readiness. The first 10-K after IPO requires SOX 404(a) management certification (always) and SOX 404(b) auditor attestation (after the JOBS Act EGC ramp). Crowe and Moss Adams 2024 benchmarking finds 5,000 to 10,000 internal audit hours per year of SOX work — and the auditor attestation cycle typically runs 6 to 9 months from start of fiscal year through 10-K filing.

How the data room actually flows during review

The IPO working group typically maintains 3 to 5 concurrent data rooms during SEC review: the main S-1 drafting room (where outside counsel and the auditor work in version control); a board-only room (where directors review draft S-1 and committee materials); an underwriter beauty-contest room (where the lead and co-lead banks see shared materials but with bank-specific watermarks); and an SEC comment-response room (where each comment letter, draft response, supporting evidence, and final filed amendment is tracked). Each room has different access permissions, NDA gates, and watermark settings.

Five common SEC comment cycle traps that delay effectiveness

Trap 1: Late delivery of audit confirmations. The auditor needs original-source confirmations on customer balances, vendor balances, debt covenants, and bank reconciliations to support the audited financials. Late delivery (typically because the customer's accounting team is slow to confirm a balance) consistently delays effectiveness. Strong working groups confirm balances 6 months pre-filing with paper backup, then re-confirm 60 days before filing.

Trap 2: Inconsistent segment-level disclosure. The 2024 FASB segment update raised quantitative disclosure requirements, and the SEC staff is testing implementation in early 2026 filings. Issuers who under-disclose segment-level expense data in the first draft typically get round 1 staff comments that require an amended filing — adding 30 to 45 days to the cycle.

Trap 3: Material contract redaction overreach. Issuers can request confidential treatment for trade secrets and competitively sensitive information in material contracts. Overreach (redacting routine provisions that are not actually competitive) draws staff comments and typically requires re-filing the contract with narrower redactions. The SEC's 2019 confidential treatment rule changes simplified this process but increased the staff scrutiny of redaction breadth.

Trap 4: Going-concern language inconsistency. For pre-profitability issuers, the auditor's going-concern assessment must be consistent with the management's MD and A discussion, the risk factors, and the use-of-proceeds discussion. Inconsistencies (typically because the auditor's going-concern memo lags the S-1 drafting cycle) draw round 2 comments and require synchronized rewrites.

Trap 5: Insider trading policy and clawback policy gaps. The SEC's 2023 final rules on clawback policies (Rule 10D-1) and the broader insider trading policy disclosure under Item 408(a) of Regulation S-K require specific policy language adopted before the IPO. Issuers who treat policy adoption as a closing-day item typically discover during round 1 staff review that the policy disclosure is incomplete — adding 14 to 21 days to the cycle.

Peony Data Room at $52 per admin per month supports unlimited concurrent rooms with per-folder permissions, dynamic watermarks embedding each viewer's identity into every page, NDA gates requiring signed acceptance, and page-level analytics tracking exactly which document each viewer accessed and for how long. Compare to Datasite enterprise pricing that typically charges per-room overage fees beyond an initial 1 or 2 rooms, or Intralinks per-page pricing that compounds across concurrent rooms — both materially more expensive workflows for the multi-room IPO use case.

How Does the Pre-IPO Roadshow Actually Work in 2026?

The pre-IPO roadshow in 2026 is a hybrid 8-to-12-day marketing tour combining in-person investor meetings (typically NYC, Boston, and the West Coast for US-only deals; London, Frankfurt, Paris, Hong Kong, Singapore for global deals) with virtual sessions, with mega-deals running 50-plus investor meetings across 1 to 2 months — and the format defaulted to hybrid post-COVID, with most 2024-2025 deals running 60 to 70 percent in-person and 30 to 40 percent virtual.

The roadshow timeline

T-minus 21 days: Roadshow prep. Management presentation deck (60 to 90 slides), banker pitch deck (separate, typically 30 to 50 slides), management Q and A prep, and investor target list (typically 100 to 200 institutional accounts for a $200 million-plus deal, 200 to 400 for a $1 billion-plus deal).

T-minus 14 days: Confidential analyst day. Sell-side research analysts from the underwriter syndicate get an in-person session with management. Post-quiet-period research initiations follow within 30 to 40 days of pricing per FINRA Rule 472 and the SEC's 2003 Global Settlement framework.

T-minus 7 days: Public S-1 amendment with marketed price range. For confidentially-filed deals, the issuer files the public amendment 15 days before the roadshow start (per JOBS Act EGC mechanics). Marketed price range is typically 20 percent wide (e.g., $24-26 for Chime CHYM, which priced at $27 above range June 2025) and is the public marker the bankers use during the roadshow.

Day 1 to 8: Standard roadshow. Typically 6 to 7 management meetings per day, 1-on-1s and small-group lunches and dinners. Standard 8-day roadshow covers NYC (days 1 to 3), Boston (day 4), Chicago (day 5), West Coast (days 6 to 7), and a closing day in NYC (day 8). Hybrid format means some meetings are virtual with West Coast investors who do not travel.

Day 9 to 12: Pricing window and Asia/Europe (mega-deals only). Mega-deals like Klarna ($1.37 billion September 2025) and CoreWeave ($1.5 billion March 2025) extended roadshows into Europe and Asia, often running 50-plus investor meetings across 1 to 2 months total.

Pricing day: Pricing call. The underwriter syndicate, issuer management, and counsel hold a pricing call (typically the evening before the IPO trade date), set the IPO price based on order book, allocate shares to institutional accounts, and the stock prices for trade the next morning.

What investors actually ask in 2026 meetings

Three question themes dominate 2024-2025 investor meetings:

Customer concentration and quality of revenue. Post-CoreWeave's 77-percent-from-two-customers disclosure, institutional investors probe revenue concentration aggressively. A clean answer with three or four diversification proof points (named net new logos, gross retention rate, expansion within existing accounts) typically resolves the line.

Path to profitability and unit economics. For SaaS issuers, CAC payback period, net retention, gross margin trajectory, and free cash flow conversion. For consumer issuers, contribution margin and customer LTV.

AI strategy and competitive moat. Particularly for software issuers post-ServiceTitan's 1,150-word AI risk factor — investors want to see how the company is using AI to reinforce moat versus how AI commoditization risk could erode it.

The pricing dynamics

Roadshow demand drives pricing. The 2024-2025 cycle showed three patterns:

Strong demand → pricing above range. ServiceTitan priced at $71 against a marketed $65-67 range ($4 above), reflecting heavy oversubscription. Chime priced at $27 against $24-26 ($1 above range, +37 percent Day-1 close). eToro priced at $52 upsized from a lower indicated range (May 2025, +29 percent Day-1 close).

In-range pricing with strong Day-1 pop. Reddit priced at $34 in-range ($31-34), closed at $50.44 on Day 1 (+48 percent). Circle priced at $31 (June 2025, NYSE CRCL), closed at $83.23 (+168 percent) — Fortune (citing University of Florida IPO researcher Jay Ritter) framed the Day-1 outcome as having left $1.72 billion on the table, the seventh largest underpricing on record since 1980.

Slimmed pricing reflecting softer demand. CoreWeave priced at $40 against an originally-marketed $47-55 range, slimmed from a $2.5 billion target to a $1.5 billion raise (37.5 million shares at $40), and closed flat on Day 1 — soft demand, but the deal still went out as the biggest tech IPO since 2021.

Outlier retail-driven volatility. Newsmax priced March 31 2025 at $10 (NYSE NMAX), raising $75 million, and the stock closed at $82.25 on Day 1 (+722 percent) with multiple volatility halts — an outlier driven primarily by retail demand rather than institutional roadshow allocation, reflecting the post-2021 retail-investor structural presence in IPO aftermarket trading.

Roadshow logistics that actually matter

Three logistics items consistently separate well-run roadshows from messy ones. First, management presentation rehearsals: strong working groups run 5 to 8 dry-run sessions with the bookrunner equity capital markets team in the 14 days before launch, where ECM bankers play hostile institutional accounts and stress-test the management Q and A. The dry runs surface knowledge gaps (typically around segment-level unit economics, AI strategy specifics, and customer-concentration mitigation) that management can address before live meetings. Second, the materials handoff: the management presentation deck (60 to 90 slides), summary investor materials (10 to 15 slides for attendee leave-behinds), and the financial model summary need to be in the data room before the first meeting. Late delivery delays follow-up Q and A and signals process disorganization. Third, the post-meeting follow-up cadence: every institutional account that takes a meeting expects a follow-up email within 24 hours with answers to specific questions raised. Strong CFOs delegate this to a dedicated finance manager who tracks every commitment and clears the queue daily.

The hybrid format adopted post-COVID changed the roadshow economics meaningfully. Pre-2020, an 8-day roadshow required physical travel through 4 to 5 cities with associated CFO time investment. Post-2020, the same 8-day roadshow can include 2 days of virtual sessions reaching West Coast and London accounts that previously required dedicated travel days — roughly 20 to 30 percent more meetings per day with no incremental CFO time. The 2024-2025 cycle saw most issuers running 60 to 70 percent in-person and 30 to 40 percent virtual, with the largest deals (Klarna, CoreWeave) extending into Asia and Europe via virtual sessions during a single physical roadshow week.

Peony Data Room at $52 per admin per month supports the roadshow workflow with NDA-gated sub-rooms for selected institutional investors who request post-meeting follow-up materials, page-level analytics showing which institutional accounts engaged with the management presentation versus which did not, and personalized sharing links tracking each meeting attendee's review activity — controls that legacy IR portals charge enterprise rates for.

How Are IPO Prices Set — and Why Are Day-1 Pops So Wide?

IPO prices are set the evening before the trade date by the underwriter syndicate based on order book demand, anchor allocations, and a deliberate underpricing convention that targets a 10-to-30-percent Day-1 pop to reward early institutional buyers — and the 22 percent average 2025 Day-1 pop (median 13 percent, top 20 deals averaging +36 percent per Renaissance Capital) reflects that convention working as designed in most cases, but the wide outliers from CoreWeave's 0 percent flat to Circle's +168 percent to Newsmax's +722 percent show that order-book mechanics break down at the tails.

Three 2024-2025 IPOs That Reshape the Modern Playbook

| Deal | Date | Ticker | Raise | Day-1 Pop | What Made It Notable |

|---|---|---|---|---|---|

| Mar 21 2024 | RDDT (NYSE) | $748M | +48% | First major social-media IPO post-Twitter; Morgan Stanley/Goldman/JPM/BofA lead; intra-day +70% peak to $57.80; reopened the consumer-tech IPO window | |

| ServiceTitan | Dec 12 2024 | TTAN (Nasdaq) | $625M | +42% | $4 above range pricing ($71 vs $65-67); 1,150-word generative-AI risk factor (industry first per TechCrunch); reopened the vertical-SaaS IPO window |

| CoreWeave | Mar 28 2025 | CRWV (Nasdaq) | $1.5B | 0% (flat) | Slimmed from $2.5B / $47-55 → $40 to print; biggest tech IPO since 2021 but soft demand; 77% revenue from 2 customers (Microsoft 62%) per Mostly Metrics S-1 breakdown |

Plus three 2025 outliers worth noting:

- Circle priced June 5 2025 on the NYSE under ticker CRCL, raising $1.05 billion at $31 with a +168 percent Day-1 close to $83.23. Per Fortune coverage citing University of Florida IPO researcher Jay Ritter, the deal left $1.72 billion on the table — the seventh largest underpricing on record since 1980 and the cleanest example of underpricing-pop dynamics breaking down in 2025.

- Klarna priced September 10 2025 on the NYSE under ticker KLAR, raising $1.37 billion — the largest IPO of 2025.

- Newsmax priced March 31 2025 on the NYSE under ticker NMAX at $10, raising $75 million, with a +722 percent Day-1 close to $82.25 and multiple volatility halts — a retail-driven outlier rather than a roadshow-allocation case study.

Why pricing works the way it does

Three structural reasons drive the 10-to-30-percent Day-1 underpricing convention:

Anchor investor preference. The underwriter syndicate wants to keep the largest institutional accounts (Fidelity, T. Rowe Price, BlackRock, Capital Group, Wellington) happy because those accounts allocate to dozens of IPOs per year. Underpricing 10 to 20 percent rewards anchors with a built-in Day-1 gain that reinforces the long-term banking relationship.

Aftermarket stability. A modest pop signals strong institutional demand and supports aftermarket trading liquidity, which feeds analyst coverage and retail demand. A flat or down Day-1 (CoreWeave's 0 percent) signals weak demand and creates a 30-to-90-day reflexive selling cycle.

Risk transfer mechanics. The underwriter takes commitment risk on the offering. A 7 percent gross spread plus underpricing-to-anchors compensates for the risk that the deal does not clear at the marketed range. The bank's fee math is calibrated to expect a small Day-1 pop on average.

The convention breaks down when retail demand swamps institutional allocation (Newsmax +722 percent), when bookrunners materially under-call demand (Circle +168 percent), or when bookrunners materially over-call demand and slim the deal to print at all (CoreWeave 0 percent flat after slimming from $2.5 billion to $1.5 billion).

The 180-day lockup

Every modern IPO includes a 180-day lockup on pre-IPO holders (founders, employees, VC investors, institutional pre-IPO buyers) restricting their ability to sell shares in the public market. The lockup typically expires 180 days after the IPO trade date, with some 2024-2025 deals adopting structured tiered-release lockups (e.g., 25 percent at day 90, 25 percent at day 135, 50 percent at day 180) to smooth supply.

SpaceX's anticipated lockup structure reportedly includes a 30 percent retail-friendly carve-out allowing pre-expiry secondary sales to retail allocators — an emerging 2025-2026 pattern in deals where retail demand is structurally important to long-term aftermarket. Most 2024 and 2025 deals (Reddit, ServiceTitan, CoreWeave, Circle, Klarna) used standard 180-day single-cliff lockups.

What CFOs negotiate at pricing

Beyond the IPO price itself, three pricing-call items matter:

Green shoe overallotment. Standard 15 percent (the underwriters can buy up to 15 percent more shares from the issuer for 30 days post-IPO at the IPO price). This is risk-free profit for the bank if Day-1 trading is strong, and a meaningful additional capital raise for the issuer. ServiceTitan's December 2024 IPO included a standard 15 percent green shoe; CoreWeave's March 2025 deal included a 15 percent green shoe that was partially exercised given the soft demand profile.

Allocation. The underwriters split the order book among institutional accounts. CFOs sometimes negotiate specific allocations to strategic accounts (anchor LPs, customer institutional accounts, sovereign wealth funds with strategic value). Reddit's March 2024 IPO reportedly allocated specific tranches to Reddit power users via a directed-share program — an unusual structure that reinforced the brand-investor narrative. Most 2024-2025 deals use standard institutional-only allocation with 5 to 10 percent retail tranches via the syndicate.

Quiet period and research initiation timing. Sell-side analysts from the underwriter syndicate must wait at least 25 days post-pricing per FINRA Rule 472 before initiating coverage. Some banks negotiate longer quiet periods to manage research-coverage rollout. The post-quiet-period research initiation cycle typically launches at day 26 to 35 with 6 to 10 sell-side initiations, and the cumulative analyst price target relative to the IPO price is the strongest single predictor of the 60-day post-IPO price action.

Three under-discussed pricing-cycle dynamics

The "free" anchor allocation as relationship currency. Anchor allocations to top-tier institutional accounts (Fidelity, T. Rowe Price, BlackRock, Capital Group, Wellington) carry value beyond the immediate Day-1 gain. Strong CFOs treat anchor allocations as multi-year relationship currency — the same accounts allocate to follow-on offerings, support buyback programs, and provide aftermarket stability. The 2024 Reddit IPO's institutional allocation reportedly skewed toward long-only growth funds that became multi-year holders. The 2025 Circle IPO's allocation skewed toward digital-asset-focused institutional accounts that priced the +168 percent Day-1 pop on conviction rather than flipping pressure.

The retail tranche size and aftermarket trading. Retail investor participation in IPOs has structurally increased since 2021 — the +722 percent Day-1 close on Newsmax (March 31 2025, NYSE NMAX) is the extreme tail of this dynamic, but retail demand also supported the +48 percent Day-1 on Reddit, +42 percent on ServiceTitan, +37 percent on Chime (June 2025, Nasdaq CHYM, $700 million at $27, above the $24-26 range), and +29 percent on eToro (May 2025, Nasdaq ETOR, $620 million at $52 upsized). Strong CFOs work with their underwriters to size the retail tranche deliberately — too small (under 5 percent) means missing structural retail demand support; too large (over 20 percent) means heavy Day-1 volatility that can trigger unfavorable analyst commentary.

The syndicate concentration trade-off. A tight syndicate of 4 to 6 banks delivers cleaner roadshow execution but limits research coverage. A broad syndicate of 10 to 15 banks delivers wider research coverage and broader retail distribution but adds friction during the pricing call when bookrunner positions need consolidation. The 2024-2025 cycle showed Reddit and ServiceTitan running tight 4-bank syndicates, while CoreWeave ran a broader 12-bank syndicate that arguably contributed to the round-trip-priced soft Day-1 outcome — too many cooks at the order book consolidation phase.

Peony Data Room at $52 per admin per month supports the post-pricing-call workflow with audit trail logs of every viewer interaction during the roadshow, page-level analytics tracking which anchor investors engaged with which materials, and NDA-gated sub-rooms for sovereign wealth or strategic-account discussions that warrant separate access controls.

What Does the First Year as a Public Company Actually Cost?

The first year as a public company costs $3 million to $5 million all-in beyond the IPO itself, with PwC's IPO cost study finding 60 percent of newly public companies spend $1 million-plus annually on ongoing compliance and 40 percent of CFOs reporting that post-IPO costs exceeded their pre-IPO expectations — and the largest variance line is consistently SOX 404, where the typical 5,000-to-10-000-internal-audit-hour annual scope is roughly double what pre-IPO companies estimate during readiness assessment.

The Year 1 SEC reporting calendar

8-K filings within 4 business days of any material event (acquisitions, leadership changes, material agreements, going-concern triggers, cybersecurity incidents under SEC's 2023 Item 1.05 rules). 4 business days is shorter than most CFOs internalize — material agreements signed late on a Friday often miss the Wednesday filing deadline. Implement same-day 8-K trigger workflows with dedicated counsel coverage.

10-Q quarterly filings within 40 days for accelerated filers and 45 days for non-accelerated filers. Detailed MD and A, segment data under ASC 280 (post the 2024 FASB update), and risk-factor updates. The first 10-Q is consistently the most-commented filing — staff reviewers cross-reference against the S-1 and probe deltas.

10-K annual filing within 60 days for large accelerated filers, 75 days for accelerated filers, and 90 days for non-accelerated filers. Includes SOX 404(a) management certification (always) and SOX 404(b) auditor attestation (after the JOBS Act EGC ramp — typically the first fiscal year after the company's fifth post-IPO anniversary, or sooner if revenue exceeds $1.235 billion or float exceeds $700 million per JOBS Act 2024 indexing).

Proxy statement (DEF 14A) filed at least 40 days before the annual meeting. Includes Item 402 executive compensation disclosure (pay-versus-performance, CEO pay ratio, clawback policy under SEC's 2023 final rules), board nominations, auditor ratification, and stockholder proposals.

Form 144 for affiliate sales. Insider transactions trigger Forms 3, 4, and 5 filings under Section 16. Lockup expiry programmatic sales typically generate 1 to 2 Form 4 filings per insider per quarter for 12 to 18 months post-lockup-expiry.

The Year 1 cost stack

| Cost line | Typical 2026 Year-1 cost | Notes |

|---|---|---|

| External legal (SEC reporting + governance + transactions) | $1.0-1.5M | Cooley, WSGR, Latham, Skadden ongoing engagement |

| External audit (10-K + 4 quarterly reviews + SOX 404(b)) | $0.75-1.5M | Big 4 ongoing fees post-IPO |

| Internal audit / SOX 404 program | $0.75-1.5M | 5,000-10,000 internal hours per year (Crowe / Moss Adams 2024) |

| Board fees and D&O insurance | $0.5-0.75M | Independent directors $200-400K each per year; D&O insurance $300-500K per year |

| IR firm and disclosure technology | $0.3-0.5M | ICR / Edelman Smithfield $30-60K per month retainers; Workiva or DFIN ActiveDisclosure platform fees |

| Listing fees (NYSE annual) | $0.08-0.5M | Per NYSE 2026 listed company manual |

| Listing fees (Nasdaq Global Select annual) | $0.0595-0.199M | Per Nasdaq 2026 listing fee schedule per Goodwin |

| Virtual data room (ongoing 10-Q evidence retention + board portal + transaction work) | $0.025-0.1M+ Datasite range; $0.000624 Peony per admin/yr | industry analyses pricing 2026; Peony published rate |

| Total Year 1 ongoing compliance | $3-5M | 60% of newly public companies spend $1M+ on compliance per PwC; 40% of CFOs say cost exceeded expectations |

The SOX 404 line is consistently the largest variance line. The reason: pre-IPO companies typically scope SOX 404 narrowly during readiness assessment (assuming a 12-month run-rate at 3,000 to 5,000 hours of internal audit) but discover during the first compliant fiscal year that the actual scope spans IT general controls, application controls, end-user computing controls, third-party SOC 1 reports, and entity-level controls — each adding documentation hours that compound.

Three avoidance practices for the cost-overrun trap

SOX 404 gap assessment 18 to 24 months pre-IPO. Big 4 advisory teams (PwC Risk Assurance, Deloitte Risk and Financial Advisory, EY Consulting, KPMG Advisory) charge $200,000 to $500,000 fixed-fee for an 18-month gap-assessment-to-go-live engagement that benchmarks your control inventory against peer public companies and identifies the scope items most pre-IPO companies miss.

Hire the head of internal audit 12 months pre-IPO. A dedicated leader for the first SOX cycle eliminates the most common failure mode: a stretched-thin controller running SOX as a side workstream while also closing the books, managing the audit, and supporting the IPO drafting cycle.

Build an evidence repository with same-day auditor access. Most cost overruns trace to evidence-retrieval friction during PCAOB inspection cycles. A purpose-built data room with version-controlled control narratives, walkthroughs, test results, and management remediation memos accessible to the auditor on a same-day basis cuts SOX cycle hours materially.

The post-IPO data room workflow

Year 1 of public-company compliance generates ongoing data room workload distinct from the pre-IPO IPO-prep room. Three workstreams matter:

SOX evidence retention. SEC Rule 17a-4 retention requirements (typically 7 years for broker-dealer related communications, 6 years for adviser communications, with PCAOB AS 1215 audit work-paper retention typically 7 years). The post-IPO data room must support audit trail logs that satisfy these requirements.

Board portal and committee minutes. Independent directors typically review board materials 5 to 10 days before each meeting. Committee meeting materials (audit, compensation, nominating/governance) require version control, NDA gating for outside director access, and access logs that document fiduciary review.

Transaction work. Public companies do M and A. The 10-K segment reporting and risk-factor updates often hinge on acquired-business integration. Each M and A transaction generates its own data room workstream that integrates with the public-company evidence repository.

Peony Data Room at $52 per admin per month supports all three workstreams with audit trail logs satisfying SEC Rule 17a-4 and PCAOB AS 1215 retention requirements; AI auto-indexing sorting board materials, audit workpapers, and M and A diligence files into review-ready folders; and page-level analytics showing exactly which audit-committee members and outside counsel reviewed which evidence — at a flat $52 per admin per month rather than the $50,000 to $100,000-plus that DFIN Venue and Datasite charge enterprise public-company clients per third-party VDR pricing surveys (2026).

How Peony Helps the IPO Working Group

Peony was built for the kind of multi-party, multi-room, multi-month workflow that an IPO requires — and the price point makes it usable across the full 18-to-24-month readiness cycle plus Year 1 of public-company compliance without enterprise VDR overage exposure.

The IPO working group documents flow through a single platform. The S-1 drafting room (where outside counsel and the auditor work in version control), the board-only room (where directors review draft S-1 and committee materials), the underwriter beauty-contest room (where 4 to 6 banks see shared materials but with bank-specific dynamic watermarks), and the SEC comment-response room (where each comment letter, draft response, supporting evidence, and final filed amendment is tracked) all run on the same Peony Data Room plan with unlimited rooms, per-folder permissions, and page-level analytics tracking exactly which document each viewer accessed.

SOX 404 evidence repository. The post-IPO SOX cycle requires PCAOB AS 1215 audit work-paper retention (typically 7 years), control narratives, walkthroughs, test results, IT general controls, application controls, and management remediation memos. Peony's AI auto-indexing sorts the typical 200-plus control documents into the standard COSO framework taxonomy in under 5 minutes, and the audit trail logs satisfy SEC Rule 17a-4 retention requirements.

Underwriter syndicate Q and A. The roadshow and SEC comment cycle generates dozens of underwriter and staff questions per week. Peony's Smart Q and A drafts cited-answer responses from your own audit and contract documents in under 60 seconds, with human-in-the-loop review before sending — saving 20 to 40 hours of associate time per cycle.

Pricing. Peony Data Room plan at $52 per admin per month billed annually — see pricing — with no per-page overages, no per-user fees, no concurrent-room limits, and no enterprise quote opacity. Compare to Datasite per-page pricing roughly $0.60 per page ($7,000 for 10,000 pages per third-party VDR pricing surveys (2026); enterprise IPO clients typically $50,000 to $100,000-plus per year per third-party VDR pricing surveys (2026)); Intralinks similar range ($7,500 for 10,000 pages per third-party VDR pricing surveys); DFIN Venue rebuilt and relaunched September 2025 with quote-based pricing typically bundled with their ActiveDisclosure SEC filing product. Enterprise VDR realized cost typically lands at 2 to 10 times the initial quote due to per-page, per-user, and concurrent-room overages — Peony's flat rate removes that exposure entirely.

For the IPO working group, the practical math: a typical 18-month readiness cycle plus 12 months of post-IPO compliance is 30 months of data room usage. At Peony's $52 per admin per month, that is $1,560 per admin all-in. At Datasite's typical enterprise IPO range, that is $62,500 to $250,000-plus all-in. The savings funds 1 to 4 months of CFO time on the project.

Frequently Asked Questions

I am the CFO of a $200M ARR SaaS company targeting an IPO in late 2026 — what does the realistic 18-month readiness timeline actually look like?

For a $200M ARR SaaS company targeting a late-2026 IPO, the realistic readiness timeline starts now (May 2026) with an 18-month runway: months 1-6 for IPO readiness assessment, audit firm upgrade if needed, and SOX 404 gap remediation; months 7-12 for underwriter beauty contests, S-1 drafting kickoff, and corporate governance build (independent directors, audit committee charter, whistleblower hotline); months 13-18 for confidential S-1 submission via JOBS Act emerging-growth-company status, SEC comment cycles, roadshow prep, and pricing. The single largest schedule risk for late-stage SaaS is the SOX 404 implementation cycle — Crowe and Moss Adams 2024 data show 5,000 to 10,000 internal audit hours per year of SOX work, and most pre-IPO issuers underestimate that by half. The 2025 IPO market saw 202 US listings raise $44 billion per Renaissance Capital's 2025 US IPO Market Review, with Day-1 pop averaging 22 percent (median 13 percent). PE-backed names delivered 36 percent of global proceeds on just 8 percent of deal count per EY Global IPO Trends 2025 (using Dealogic, S&P Capital IQ, PitchBook, Mergermarket data) — meaning the bar is raised on quality of process. Peony Data Room at $52 per admin per month gives your IPO working group a data room with AI auto-indexing that organizes the SOX evidence library, audit confirmations, S-1 drafting backup, and underwriter beauty-contest materials in under 5 minutes — at a fraction of the $50,000 to $100,000 per year that Datasite, Intralinks, and DFIN's Venue VDR charge enterprise IPO clients per third-party VDR pricing surveys (2026). See our pricing page for the flat per-admin Data Room pricing with no per-page or per-user overage exposure.

I am general counsel at a pre-IPO biotech and we are 12 months out — what does the SEC review process actually look like in 2026 and how many comment cycles should we expect?

For a pre-IPO biotech 12 months out, expect SEC review on your S-1 to span 21 to 30 days for the initial staff comment letter, with 2 to 3 comment cycles standard before effectiveness — the full filing-to-effectiveness window typically runs 3 to 6 months on a clean process and 6 to 12 months when the staff probes accounting policies, revenue recognition, or risk-factor disclosure quality. The 2024-2025 cycle reset the bar on risk-factor architecture: ServiceTitan's S-1 (filed November 2024) included a 1,150-word generative-AI risk factor that became an industry first per TechCrunch coverage at the filing date, and CoreWeave's S-1 (filed March 2025) disclosed 77 percent of revenue from two customers (Microsoft 62 percent) per the Mostly Metrics S-1 breakdown — concentration disclosure the SEC staff now expects to see quantified rather than narrative. For biotech specifically, expect comment cycles on FDA correspondence summaries, Phase 2 and Phase 3 readout disclosure, manufacturing partner concentration, and IP family scope. Peony Data Room at $52 per admin per month supports page-level analytics showing exactly which sections of the S-1 draft your outside counsel, auditor, and underwriter syndicate are reviewing — so the IPO working group spots gaps in coverage before the SEC flags them. Compare to legacy VDRs (Datasite, Intralinks, DFIN Venue) charging $50,000 to $100,000 or more per year per third-party VDR pricing surveys (2026) for the same workflow.

I am the CEO and founder of a Series D fintech preparing to file confidentially via the JOBS Act — what does the underwriter beauty contest actually look like and how do we negotiate the gross spread?

For a Series D fintech filing confidentially under JOBS Act emerging-growth-company status, the underwriter beauty contest typically spans 6 to 10 weeks with 4 to 6 banks pitched — usually 2 bulge-bracket leads (Morgan Stanley, Goldman Sachs, JPMorgan, Bank of America are the four most active 2024-2025 IPO bookrunners across Reddit, ServiceTitan, CoreWeave, Circle, and Klarna) plus 2 to 4 mid-size or sector-specialist banks for the syndicate. On gross spread, the standard for $20 million to $100 million IPOs is 7 percent (94 percent of US deals at this size band), with a typical range of 6 to 8 percent. Mega-deals at $1 billion-plus typically negotiate down to 1 to 2 percent — Circle's June 2025 IPO ($1.05 billion at $31, +168 percent Day-1 close to $83.23) reportedly paid roughly 4 percent gross spread per Fortune coverage, which Fortune (citing University of Florida IPO researcher Jay Ritter) later framed as having left $1.72 billion on the table given the Day-1 pop — the seventh largest underpricing on record since 1980. The negotiation levers are: lead bank versus co-lead positioning, retail allocation percentage (some banks fight for higher retail to support aftermarket trading), green shoe overallotment size (typically 15 percent), research coverage commitment (post-quiet-period analyst initiations), and lockup carve-outs for early-investor secondary share sales. Peony Data Room at $52 per admin per month gives the IPO working group NDA-gated sub-rooms for each beauty-contest bank, dynamic watermarks with each MD's identity baked into every page, and page-level analytics showing which bank's team actually read the management presentation versus which sent associates to skim — exactly the controls counsel expects when 4 to 6 banks see your numbers concurrently.

I run corporate development at a $1B revenue industrial company and we are evaluating going public via traditional IPO versus SPAC versus direct listing — what does the 2025-2026 data say about which path actually delivers?

For a $1 billion revenue industrial company evaluating the three paths in 2025-2026, the data favors traditional IPO for industrial issuers at this scale, but the choice depends on use of proceeds and capital structure. Traditional IPO 2025 data: 202 US IPOs raised $44 billion per Renaissance Capital's 2025 US IPO Market Review (January 2 2026), with Day-1 pop averaging 22 percent (median 13 percent) and the top 20 deals averaging +36 percent — strong signal that institutional demand returned. PE-backed deals delivered 36 percent of global proceeds on just 8 percent of deal count per EY Global IPO Trends 2025 (using Dealogic, S&P Capital IQ, PitchBook, Mergermarket data), which favors industrial sponsors. SPAC 2025 data: 138 SPAC IPOs raised $25.8 billion, a meaningful rebound from the 2022-2023 trough but still well below the 2021 peak of 613 SPAC IPOs at $145 billion — and the redemption-economics math typically penalizes industrial issuers with longer revenue ramps. Direct listing remains rare for industrial issuers because the path foregoes primary capital, which industrial businesses typically need for capex. Q1 2026 globally: 230 IPOs raised $40.6 billion (count down 23 percent year-over-year, proceeds up 36 percent) per EY Global IPO Trends Q1 2026, with defense the largest Q1 sector — supportive backdrop for industrial issuers. Pipeline indicators include Cerebras (S-1 filed April 17 2026), Databricks ($130 billion private valuation), and Stripe ($100 billion-plus private valuation), with Shein delayed. Peony Data Room at $52 per admin per month supports the strategic-options diligence process with unlimited rooms so your strategic-finance team can run parallel diligence files for IPO bankers, SPAC sponsors, and direct-listing advisors without paying per-room fees. Compare to Datasite per-page pricing roughly $0.60 per page — a $1 billion industrial typically uploads 5,000 to 10,000 pages of historical financials, board minutes, and contracts, which would cost $3,000 to $6,000 in per-page overage on Datasite alone per third-party VDR pricing surveys (2026).

I am the audit committee chair at a pre-IPO company — what is the realistic SOX 404 budget and timeline, and how do we avoid the 40 percent-of-CFOs-say-cost-exceeded-expectations trap PwC documented?

For a pre-IPO company building SOX 404 capability, the realistic annual budget is $1 million to $2 million-plus once fully ramped, with 5,000 to 10,000 internal audit hours per year of work (Crowe and Moss Adams 2024 benchmarking). The PwC IPO cost study found 40 percent of CFOs report post-IPO cost exceeded expectations, and SOX is consistently the largest variance line. The reason: pre-IPO companies typically scope SOX 404 narrowly during readiness assessment (assuming a 12-month run-rate at 3,000 to 5,000 hours of internal audit) but discover during the first compliant fiscal year that the actual scope spans IT general controls, application controls, end-user computing controls, third-party service organization controls (SOC 1 reports), and entity-level controls — each adding documentation hours that compound. Three avoidance practices that work: first, run a SOX 404 gap assessment 18 to 24 months pre-IPO with a Big 4 advisory team (typical $200,000 to $500,000 fixed-fee scope) that benchmarks your control inventory against peer public companies; second, hire the head of internal audit 12 months pre-IPO so the first SOX cycle has a dedicated leader rather than a stretched-thin controller; third, build an evidence repository with version-controlled control narratives, walkthroughs, test results, and management remediation memos accessible to the auditor on a same-day basis — most cost overruns trace to evidence-retrieval friction during PCAOB inspection cycles. Peony Data Room at $52 per admin per month supports the SOX evidence repository with page-level analytics showing which auditor team members reviewed which control narrative and for how long, AI auto-indexing sorting 200-plus control documents into the standard COSO framework taxonomy in under 5 minutes, and audit trail logs that satisfy PCAOB AS 2201 documentation requirements — at a flat $52 per admin per month rather than the $50,000 to $100,000-plus that Datasite charges enterprise SOX clients per third-party VDR pricing surveys 2026.

I am the head of investor relations at a newly public company that priced six weeks ago — how do I prepare for the lockup expiry without tanking the stock?

For a newly public company six weeks post-IPO, lockup expiry preparation should start in week 6 of the standard 180-day lockup window — meaning you have roughly 18 to 20 weeks to prepare. Three practices separate strong post-IPO IR from weak. First, pre-announce the lockup expiry in your second 10-Q earnings call so the sell-side analyst community models the share supply increase 90 days ahead of the expiry date — surprises drive the 5 to 15 percent typical lockup-expiry drawdown, not the share supply itself. Second, negotiate a structured lockup release with your underwriters: a tiered release (e.g., 25 percent at day 90, 25 percent at day 135, 50 percent at day 180) smooths the supply curve and is increasingly common for 2024-2025 issuers; some 2025 IPOs (notably SpaceX's anticipated structure) reportedly include a 30 percent retail-friendly carve-out that allows pre-expiry secondary sales to retail allocators. Third, brief major holders on their post-lockup intent — if your top 5 pre-IPO holders represent 60 percent of restricted shares (typical for a Series D-funded issuer), their stated 6-month and 12-month sale intent is the single largest predictor of post-lockup price action. The 2024 Reddit IPO (March 21 2024, NYSE RDDT, $748 million raise at $34, +48 percent Day-1 close to $50.44) executed a textbook lockup management process with 90-day quiet-period programmatic sales by early VC holders. Peony Data Room at $52 per admin per month supports the post-IPO investor relations workflow with NDA-gated sub-rooms for selected institutional holders, page-level analytics showing which holders engaged with your latest 10-Q materials, and personalized sharing links tracking each holder's review activity — controls that legacy IR portals like Q4 and IRIS charge enterprise rates for.

I am a securities partner at a mid-market firm — what are the most common SEC comment letter themes I should preempt in S-1 drafting for 2026 issuers?